Abstract

In response to the deterioration of the global environment, more and more firms are adopting eco-friendly strategies such as an environmental entrepreneurial orientation. We use the resource-based view of the firm and stakeholder theory to examine how environmental entrepreneurial orientation improves firm performance. We construct and test a moderated mediation model using survey data from 416 Chinese firms and find that environmental innovation mediates the positive effect of environmental entrepreneurial orientation on firm performance, stakeholder pressure positively moderates the influence of environmental entrepreneurial orientation on environmental innovation, and environmental entrepreneurial orientation influences firm performance through environmental innovation. This study makes theoretical contributions to the literature and provides management insights.

Keywords

Introduction

Global warming, water and soil loss, water and soil pollution, food safety, and other environmental problems are becoming increasingly urgent threats to the survival of human beings. Thus, governments, consumers, non-governmental organizations, and other stakeholders are paying more attention to firms’ environmental behaviors (Doran & Ryan, 2016). In response, an increasing number of firms are acknowledging their social responsibility (Chen et al., 2006) and gradually integrating environmental management into their internal strategic decisions and business activities (Chang, 2011; Chen, 2008). In the entrepreneurial process, firms must strike a balance between their economic objectives and environmental management. Therefore, environmental entrepreneurship based on sustainable development that protects the environment has become an important issue in entrepreneurial studies (Koe & Majid, 2014).

For firms, an environmental entrepreneurial orientation (EEO) is a tendency to be proactive, risk-taking and innovative in the search for opportunities that provide both economic and ecological benefits. A number of studies examine environmental entrepreneurship’s driving factors (Gast et al., 2017; Schaltegger & Wagner, 2011) and its important roles in firms’ economic and non-economic outcomes (Shepherd & Patzelt, 2011). However, only a few focus on how EEO affects corporate financial performance; in particular, there is very little research in emerging economies such as China (Jiang et al., 2018). Therefore, the first aim of our study is to examine the relationship between EEO and firms’ financial performance.

Traditional entrepreneurial orientation improves firm performance by encouraging different types of entrepreneurial behavior (Kollmann & Stöckmann, 2014; Wiklund & Shepherd, 2005). However, it is unclear which entrepreneurial behaviors promote environmental sustainability or how EEO can promote firm performance (Jiang et al., 2018). Environmental innovation (EIN), which consists of innovations such as new or improved systems, practices, processes, or products that reduce a firm’s environmental burden (Chen et al., 2006; Kemp & Pearson, 2008), may mediate the effect of EEO on firm performance. According to some studies, EIN may be the most effective method for firms to achieve success in environmental management (Maxfield, 2008). Several studies find that EIN improves a corporation’s green image, creates product diversity and increases market share in the future, and consequently leads to increased profits (Cai & Li, 2018; Clemens, 2006; Ping, 2009). According to the Porter hypothesis (Porter & Van der Linde, 1995), EIN strengthens firm competitiveness.

However, EIN is more complicated and uncertain than traditional innovation (Spence et al., 2011); its success requires strategic reform and new value integration (Slevin & Terjesen, 2011), which require internal strategic resources (Xavier et al., 2017; Zhou et al., 2018). Despite this, studies of EIN generally focus on the external factors that drive EIN, and the relationship between internal corporate factors and EIN is unclear (Guo et al., 2020b). A few recent studies examine how internal strategies or entrepreneurship-related factors affect firms’ implementation of EIN (Arnold & Hockerts, 2011; Horbach, 2008). EEO, as an eco-friendly business strategy, may foster EIN. Recent studies indicate that EEO helps firms to mitigate the adverse effects of their activities on the environment (e.g., Jiang et al., 2018; Leonidou et al., 2017). Therefore, this study proposes that EIN mediates the effect of EEO on firm performance. The second aim of this study is to investigate whether EEO fosters EIN, which improves firm performance.

Most corporate activities are embedded in stakeholders’ relational networks. Stakeholder theory suggests that firms need to consider the expectations of a wide group of constituents, including suppliers, employees, customers, competitors, media, government, and community, to achieve corporate goals (Freeman, 2010). Thus, pressure from stakeholders is an important driver of firms’ adoption of environmental strategies (Buysse & Verbeke, 2003; Eesley & Lenox, 2006; Jakhar et al., 2019). EIN is affected by micro-, meso-, and macro-level factors, and the interactions between these factors change their effects on EIN (Shafique & Mehwish, 2020). For example, when EEO interacts with micro-/meso-/macro-level factors such as stakeholder pressure, its effects on EIN may be moderated. However, the boundary conditions under which stakeholder pressure is more or less effective in prompting EIN have received little attention, especially in the context of the relationship between EEO and EIN. Moreover, most studies use data from developed economies (Vaitoonkiat & Charoensukmongkol, 2020a); the influence of stakeholder pressure on the practice of EIN in China’s emerging economy needs to be further explored. Thus, the third aim of our study is to examine how stakeholder pressure moderates the effect of EEO on EIN.

Using a sample of Chinese firms, this paper constructs a theoretical model of the relationships between EEO, stakeholder pressure, EIN and firm performance (seen in Figure 1) and determines whether EEO promotes EIN and improves firm performance, whether stakeholder pressure moderates the influence of EEO on EIN, and the indirect effect of EEO on firm performance through EIN. Figure 1 illustrates our theoretical model.

The theoretical model.

Theoretical Background

An EEO Research Perspective

EEO organically combines corporate environmental entrepreneurship and entrepreneurial orientation, but it is a relatively new concept and lacks a clear definition. Following Guo et al. (2020a), we define EEO as a firm’s tendency to be proactive, risk-taking, and innovative in the search for opportunities that provide both economic and ecological benefits. Similar to traditional entrepreneurial orientation, EEO is composed of innovative orientation, proactive orientation, and risk orientation (Rauch et al., 2009). However, EEO also involves environmental orientation, which gives EEO a prominent role in sustainable development activities (Provasnek et al., 2017; Shepherd & Patzelt, 2011) and makes it a critical strategic tool for improving firm performance (Kirkwood & Walton, 2014; Thompson et al., 2011).

Compared with traditional innovation, EIN is a relatively new concept; its definition is still emerging and varies with the scholars’ intentions. Chen et al. (2006) define EIN as a series of innovative technological and management methods related to energy conservation, emission reduction, pollution reduction, and waste recycling. Kemp and Pearson (2008) hold that enterprises adopt EIN to create products, techniques, and services that are beneficial to the environment. Following Rennings (2000), we define EIN as innovations such as new or improved systems, practices, processes, or products that reduce a firm’s environmental burden. EIN can help firms gain a sustainable competitive advantage through the use of more environmentally friendly and highly recognized modes (Chen et al., 2006). According to the Porter hypothesis (Porter & Van der Linde, 1995) and ecological modernization theory (Zhu et al., 2012), EIN or ecological innovation is an opportunity for firms to improve their competitiveness. Nevertheless, as EIN is more complex and uncertain than traditional technological innovation (Spence et al., 2011), its successful implementation requires strategic reform and new value integration (Slevin & Terjesen, 2011). Thus, without the support of firms’ internal strategic resources, EIN cannot develop smoothly.

The resource-based view (RBV) of the firm emphasizes that valuable, rare and inimitable resources deliver competitive advantages to firms (Barney, 1991). Traditional/“normal” entrepreneurial orientation is generally considered an important strategic resource (Vaitoonkiat & Charoensukmongkol, 2020b), and RBV has been applied to explain the positive contribution of traditional entrepreneurial orientation (Wiklund & Shepherd, 2005). Extending this logic, EEO can also be regarded as an important internal strategic resource (Jiang et al., 2018). Drawing on RBV theory and previous research (Dean & McMullen, 2007), this study proposes that EEO, as a strategic resource, helps enterprises extend the traditional development mode by adopting environmental proactive orientation, environmental risky orientation, and environmental innovative orientation, which promote the adoption of proactive environmental behaviors, including EIN.

Stakeholder Theory

Stakeholders are the individuals and groups that influence the fulfilment of corporate objectives and that are influenced by corporate behavior (Freeman, 2010); almost all corporate activities are related to some form of stakeholder pressure. The basic logic of stakeholder theory is that firms’ behavior can affect stakeholders, so firms need to respond to the demands of stakeholders, especially important stakeholders (Buysse & Verbeke, 2003; Miles, 2015). Stakeholders may be either external or internal groups: external stakeholders are groups or individuals that do not belong to enterprises but interact with them, such as governments, customers, NGOs, communities and competitors, and internal stakeholders are part of enterprises’ institutional framework, including owners, managers, and employees (Seroka-Stolka, 2020).

Multiple studies use stakeholder theory to explain firms’ adoption of practices that promote environmental protection (Rodrigue et al., 2013), corporate sustainability (Hörisch et al., 2014; Rondinelli & Berry, 2000; Steurer et al., 2005), corporate social responsibility (Friedman & Miles, 2002), and environmental management activities (Eesley & Lenox, 2006; Jakhar et al., 2019; Sarkis et al., 2010). These studies demonstrate that an increase in stakeholder pressure may effectively reduce enterprises’ irresponsible behaviors and increase enterprises’ environmentally friendly behaviors. For example, pressures from external stakeholders such as governments, communities, green consumers, competitors, and the public can prompt firms to formulate and execute environmental strategies (Pinzone et al., 2015; Zhou et al., 2018), and internal pressures such as employee environmental commitment and employee participation can promote the implementation of forward-looking environmental strategies (Alt et al., 2015).

Together, the pressure from different stakeholders for sustainability exert a “binding force” on firms’ environmental behavior. EIN, which is a corporate environmental strategic behavior, may thus be positively influenced by stakeholder pressure. To respond to stakeholders’ environmental concerns, managers must recognize environmental issues and advance EINs to address them. Thus, stakeholder pressure can lead firms to innovatively eliminate polluting emissions, save energy, improve resource utilization and produce green products (Liu et al., 2015). Based on the above analysis, stakeholder theory can be used to explain the impact of stakeholders on corporate EIN behavior. However, stakeholder pressure—a stakeholder-oriented force—has not been examined as a boundary condition for the adoption of an environmental strategy, especially in the context of the EEO–EIN relationship.

Research Hypothesis

EEO and Firm Performance

EEO improves firm performance through its effects on environmental proactive orientation, environmental risk orientation, and environmental innovative orientation. First, the environmental proactive orientation of EEO encourages firms’ pursuit of leadership, enthusiasm for the future market, and ability to anticipate market competition for environmentally friendly goods and services (Lumpkin & Dess, 1996). An environmental proactive orientation may help firms quickly seize new opportunities in competitive markets (Woldesenbet et al., 2012), as such firms can use their resources to develop and use potential market spaces. Thus, EEO, through the mechanism of environmental proactive organization, may drive firms to rapidly input resources, seize opportunities in the market for environmentally friendly goods, promote new environmentally friendly products or services ahead of competitors and realize product differentiation. EEO may thus help firms improve their performance and competitive advantage in the context of sustainable development.

Second, environmental risk orientation, which is firms’ tendency to participate in risky environmentally friendly projects, encourages firms to take bold actions even if all of the potential consequences are unknown (Wiklund & Shepherd, 2003). An environmental risk orientation leads firms to regard market risk as an opportunity (Dutton & Jackson, 1987) and to undertake commercial risks when opportunities and challenges coexist. In other words, EEO ensures the commitment of sufficient resources to new environmentally friendly market spaces and “high-risk and high-profit” environmentally friendly projects that will allow the firms to meet future market demands. By enabling firms to recognize and quickly occupy environmentally friendly markets, EEO meets clients’ increasing demands for environmentally friendly consumption and further improves firm performance.

The third mechanism, environmental innovative orientation, reflects firms’ willingness, and ability to adopt new environmentally friendly ideas, new experiments, and the creative process (Lumpkin & Dess, 1996). According to RBV theory, successful firms should have the ability to recognize and integrate existing resources (Barney, 1991), and an environmental innovative orientation boosts firms’ ability to integrate firm resources in a creative way and to optimize resource distribution. Furthermore, EEO alleviates environmental influence (Provasnek et al., 2017; Shepherd & Patzelt, 2011), so firms’ resources and abilities may continue to tilt toward products and services that are favorable to the environment, enabling firms to promote energy conservation, and reduce environmental pollution in their management and production processes. Some studies note that firms’ environmental entrepreneurial initiatives help reduce production costs and further improve firm performance (Dean & McMullen, 2007; Orazalin & Baydauletov, 2020).

Based on the above discussion, we propose the following hypothesis.

The Mediating Role of Environmental Innovation

EIN may have a positive impact on firm performance (Guo et al., 2019; Wijethilake et al., 2018). First, it improves income by leading firms to improve production techniques and thus create new value. Studies suggest that EIN improves firms’ internal efficiency (Cai & Li, 2018), enhances overall productivity (Chang, 2011) and increases firm profit. The essence of EIN is to reduce the adverse impact of firms’ production activities on the environment (OECD, 2009), help firms establish and maintain a green image (Chen, 2008), cultivate a good reputation, and even explore new markets (Chen et al., 2006). EIN helps firms to achieve product differentiation, which allows them to set higher prices (Chen, 2008) and improve product profitability. For all of these reasons, EIN may increase firms’ profits. In terms of cost, as EIN may effectively reduce waste in production processes (e.g., by recycling materials), it can improve resource efficiency and productivity (Chen, 2008; Porter & Van der Linde, 1995). EIN also helps firms improve the efficiency of product manufacturing, reduce resource consumption and, to a certain extent, reduce production costs. Furthermore, EIN helps firms reduce environmental burdens (such as emissions of toxic and harmful substances) and decrease the high punitive cost of complying with environmental laws (Chang, 2011; Tang et al., 2018). Thus, EIN may reduce firms’ costs.

EEO may have a positive influence on EIN activity through the following mechanisms. First, EEO’s essential attribute is innovation (Schumpeter, 1934), and some studies even consider technological innovation to be an indicator of entrepreneurial orientation. Like entrepreneurial orientation, EEO is an indicator of firms’ ability to recognize and master opportunities in the market for environmentally friendly goods and services (Wiklund & Shepherd, 2003). Given market demand for sustainable development, firms with high levels of EEO focus on innovations that will save resources and improve the environment. As a result, firms with high levels of EEO are more likely to improve their competitive advantage by implementing EIN activities and developing products, technologies, R&D and services that do not harm the environment.

Second, the environmental proactive orientation of EEO helps firms quickly recognize and adapt to sudden changes in society and the competitive environment (Groza et al., 2011). To achieve this, firms must monitor governments, markets and clients in real time (Courrent et al., 2016) and respond rapidly to changes, but they must also take environmental issues into account when making operation decisions (Sharma, 2000). In the process of establishing sustainable development (Courrent et al., 2016), EEO may guide firms to use entrepreneurial innovation to collect and integrate the necessary resources (Zhou et al., 2005). In other words, EEO integrates environmental management into the deployment and configuration of controllable resources. Therefore, as a strategic posture, EEO may motivate firms to voluntarily adopt environmentally friendly actions such as EIN.

Third, as EIN is associated with high risks and uncertainty (Spence et al., 2011), especially in the context of an emerging economy, EIN places high demands in terms of costs and technology. Firms with high EEO tend to regard environmental management as an opportunity rather than a threat (Dean & McMullen, 2007; Shepherd & Patzelt, 2011) and are thus willing to commit sufficient resources despite the high risks and uncertainty (Barney, 1991). Furthermore, firms with high EEO levels are more willing to bear risk and uncertainty, which translates into acceptance and application of innovative products, services and processes (Russo & Fouts, 1997). Therefore, EEO promotes EIN.

To summarize, EEO may encourage firms to adopt EIN, which can improve firm performance. Firms with high levels of environmental proactive orientation, environmental risk orientation, and environmental innovative orientation are more likely to improve firm performance by implementing EIN. Therefore, we propose the following hypothesis.

The Moderating Role of Stakeholder Pressure

Stakeholder pressure may strengthen the effect of EEO on EIN. To establish long-term positive relations with stakeholders, firms must adjust their strategies and behaviors to respond to stakeholders’ demands for better environmental protection. Studies show that stakeholder pressure can push firms to address environmental issues (Jennings & Zandbergen, 1995), adopt active environmental management measures (Lee et al., 2018), innovatively eliminate pollution emissions, save energy, improve resource utilization and produce green products (Liu et al., 2015). Therefore, stakeholder pressure may help promote EEO strategies and EIN measures. More concretely, stakeholder pressure may increase the positive effect of EEO on EIN. Hence, we propose the following hypothesis.

As H2 and H3a together suggest a moderated mediating effect, we propose the following hypothesis.

Method

Questionnaire Design

We constructed a questionnaire with the following five sections: firms’ descriptive data (such as industrial department, year of establishment, and number of staff), EEO, EIN, stakeholder pressure, and firm performance. To ensure both reliability and validity, we used mature scales adapted to the research setting. All of the questionnaire items used a 7-point Likert scale, where 1 = “strongly disagree” and 7 = “strongly agree.” We measured EEO using five items developed by Zhao et al. (2011), Jiang et al. (2018), and Li et al. (2010). To measure EIN, we used the five items developed by Cai and Li (2018), whose scale has been validated in the context of China. To measure stakeholder pressure, we adopted the 4-item scale in Lee et al. (2018). Drawing on Li et al. (2018), we measured firm performance with three items. Interviewees were required to compare the firm performance of their own companies and that of their competitors in the previous 3 years from three perspectives. We also used three control variables, company age, size and industry, to eliminate the influence of firm performance. This research measures company age with the company’s establishment term and divides it into four layers (Liao, 2016). We measure company size with the number of staff and divides it into five layers (Dibrell et al., 2011). By referring to previous studies (Horbach, 2008; Huang et al., 2016), this paper divides the industry into two types, namely the manufacturing industry and the service industry.

Data Collection

We interviewed middle-senior managers of firms to ensure that we obtained accurate and reliable information. The data collections consisted of three steps. First, we designed the primary questionnaire. Using mature scales available in the literature, we selected the most appropriate items for our questionnaire and then interviewed firm managers face to face. Based on the results of these interviews, we revised the questionnaire to make the questions more accurate, thus obtaining the primary questionnaire. Second, we conducted a preliminary investigation of 33 interviewees, including firm managers, professors of entrepreneurship management, and postgraduates. We revised or deleted some of the questions based on the analysis of the questionnaire’s reliability and validity. Third, we distributed the questionnaires to firms in a range of Chinese provinces and municipalities, including Shaanxi, Guangzhou, Shenzhen, and Shanghai. These areas represent China’s geographical, economic, and demographic diversity (Zhao et al., 2011). According to the scale and industry conditions, we extracted a sample of 784 enterprises from the list provided by official governmental organizations. To guarantee the survey response rate, we distributed questionnaires to these 784 enterprises through university resources and individual relationships. We conducted semi-structured interviews with firm managers enrolled in EMBA and MBA courses in five universities in Xi’an and invited them to complete the questionnaire. We also asked colleagues and friends to distribute questionnaires to firm managers through multiple channels, such as face-to-face interviews, emails, and the Internet. We distributed 784 questionnaires and recovered 480, giving a response rate of 61.2%. After deleting 25 improperly completed questionnaires and 39 incomplete ones, we obtained a sample of 416 valid questionnaires. The firms include state-owned enterprises and private enterprises from a range of industries, including the chemical and pharmaceutical and medical industries. All of the participants were assured that we would protect their firms’ commercial privacy, and the data were anonymized. The summary statistics of the firms and participants are shown in Table 1.

Summary Statistics of the Sampled Firms and Respondents.

To identify possible differences between the questionnaire respondents and those who did not return the questionnaire, we compare the answers of the first 216 respondents with the answers from the 200 questionnaires collected in the middle and later periods (Lambert & Harrington, 1990). The t-test result indicates that there are no obvious differences in the demographic characteristics of these two groups (p ≤ .05). Therefore, this sample does not have severe non-response bias.

We use two methods to reduce the potential threat of common method variance (CMV). First, we target middle-senior managers who are knowledgeable about firms’ environmental management, as the information that they provide is deemed to be accurate and reliable (Narayanan et al., 2011). Second, following Harman’s method, we conduct a single-factor analysis of all of the variables (Podsakoff & Organ, 1986) to test for CMV. The un-rotated factor analysis indicates that the first factor explains 38.1% of the variance and that no single factor can explain a large percentage of variance. In addition, the dependent variable and the independent variable load on different factors, indicating that CMV is not severe in this research.

Reliability and Validity

First, we conduct an exploratory factor analysis (EFA) of the 17 items in the questionnaire to determine the basic factor structure using principal component analysis and the oblique rotation method. As expected, we obtain four factors that account for 78.5% of the total variance, indicating that all of the items load onto the expected constructs. This ensures that the constructs are one-dimensional.

This study tests the reliability of the scales using Cronbach’s alpha coefficients. The results in Table 2 indicate that all of the variables have coefficients greater than .7, showing that the data are reliable (Carmines & Zeller, 1979). To ensure content validity, our questionnaire uses mature scales reviewed by experts in related fields and is revised according to feedback from interviews and preliminary research. These procedures give our questionnaire high content validity. We test convergent validity using average variance extracted values (AVE) and composite reliability (CR) values. As shown in Table 2, the minimum AVE value is .672 and the minimum of CR is .871, indicating that the variables have high convergent validity.

Convergent Validity and Reliability.

We further evaluate convergent validity using CFA. The results presented in Table 3 suggest that our model fits the data well (χ2 = 302.327, df = 113, χ2/df = 2.675, SRMR = .034, GFI = .918, IFI = .965, NFI = .945, CFI = .965, TLI = .958, RMSEA = .0642). Therefore, all of the variables in the model are distinct and the model construct is good. The means, standard deviations, and correlations of the variables are given in Table 4.

Results of CFA.

Note. Four-factor model: EEO, stakeholder pressure, EIN, and firm performance. Three factor model: like the four-factor model, but EEO and EIN are combined. Two-factor model: like the four-factor model, but EEO, EIN, and firm performance are combined. One-factor model: all four factors, EEO, EIN, firm performance, and stakeholder pressure, are combined.

Correlations Between Variables.

p < .05. **p < .01. ***p < .001.

Results

To test our moderated mediation model, we implement hierarchical multiple regressions with bootstrapping.

Main and Mediating Effects

The results of the multiple regression analysis are shown in Table 5. Model 5 shows that EEO has a positive impact on firm performance (b = 0.389, p < .001), which supports H1.

Regression Results (N = 416).

p < .05. **p < .01. ***p < .001.

According to Preacher and Hayes (2008), two methods can be used to evaluate the mediating effect of a variable. The first is a four-step procedure developed by Baron and Kenny and the second is a non-parametric test of the indirect effect. As shown in Table 5, Models 4 and 5 find that EEO and firm performance are positively correlated (b = 0.389, p < .001), verifying the first step in the mediation effect test. Models 1 and 2 (Table 5) show that EEO and EIN are positively correlated (b = 0.448, p < .001), verifying the second step in the mediating effect test. For the last two steps, we conduct a regression that takes firm performance as the dependent variable and EEO, EIN and the control variable as independent variables. Model 6 (Table 5) shows that EIN and firm performance are positively correlated (b = 0.346, p < .001). In addition, the connection between EEO and firm performance is still positive (b = 0.234, p < .01), but the significance level is lower than in Model 5, which generally supports H2.

To further confirm H2, we implement bias-corrected bootstrapping on Model 4 using the PROCESS macro in SPSS (Preacher & Hayes, 2008), and the result is shown in Table 6. Preacher and Hayes’s bootstrapping algorithm assesses the indirect effect of the hypothesized mediator for a 95% bias-corrected confidence interval (BC CI) by running 5,000 bootstrap resamples (MacKinnon et al., 2004). Our bootstrapping results show that EEO’s indirect impact on firm performance through EIN is 0.181 and the 95% confidence interval is [0.035, 0.105], which does not contain zero. Therefore, EIN significantly mediates the impact of EEO on firm performance. These results support H2.

Bootstrapping Results (N = 416).

Note. Bootstrapping sample = 5,000.

The Moderating Effect

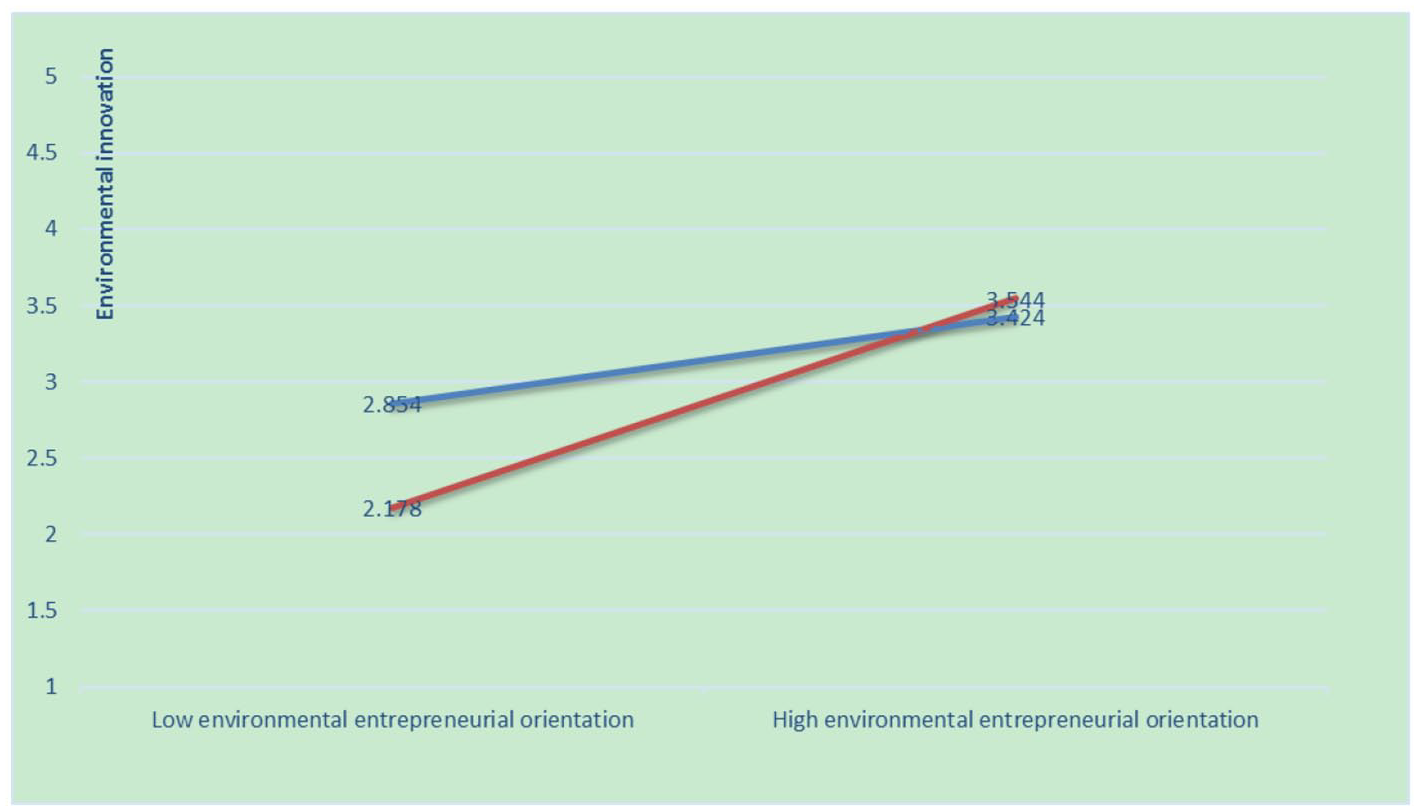

To examine whether stakeholder pressure moderates the influence of EEO on EIN, we implement a multiple regression analysis and use PROCESS to check the confidence interval. To avoid multicollinearity (Aiken et al., 1991), the independent variable and the moderating variable are centralized before the product item is constructed. Model 3 in Table 5 indicates that the interaction item of EEO and stakeholder pressure positively affects EIN (b = 0.196, p < .001). To show the moderating role of stakeholder pressure more directly, we follow Aiken et al. (1991) and create a diagram of the moderating effect of stakeholder pressure. Specifically, we regress the relationship between EEO and EIN at high, medium, and low levels of stakeholder pressure (defined as one standard deviation higher or lower than the mean). As shown in Figure 2, when stakeholder pressure is high, the positive correlation between EEO and EIN is stronger than when it is low. These results support H3a.

Moderating effect of stakeholder pressure.

Test of the Moderated Mediating Effect

Finally, we investigate the moderated mediating effect, which is the conditional indirect effect, with stakeholder pressure as the moderating variable. As shown in Table 6, EEO’s indirect influence on firm performance through EIN is stronger when stakeholder pressure is high (b = 0.239, 95% BC CI = [0.166, 0. 326]) than that when it is low (b = 0.084, 95% BC CI = [0.025, 0.162]). The moderated mediating effect index is 0.066 (higher than 0) and the 95% confidence interval is [0.035, 0.105], which does not contain zero, so the moderated mediating effect is significant and positive. These results indicate that increased stakeholder pressure strengthens the influence of EEO on firm performance through EIN. Therefore, H3b is supported.

Discussion and Conclusion

This paper uses a sample of Chinese firms to develop and test a theoretical model of the relationship between EEO and firm performance in emerging economies. Using RBV and stakeholder theory, we show that EEO improves firm performance by boosting green innovation and verify that stakeholder pressure moderates the effect of EEO on EIN.

Theoretical Contributions

This study makes at least three important contributions to the literature. First, it advances EEO research by applying RBV. Traditional entrepreneurial orientation is generally considered an important resource that can improve firm performance (Donbesuur et al., 2020; Lumpkin & Dess, 1996; Wiklund & Shepherd, 2005). However, the study of EEO (an entrepreneurial attitude that emphasizes environmental protection responsibility) is still in its infancy, and there are few studies of the relationship between EEO and firm performance. The lack of theoretical models linking EEO and firm performance limits our understanding of EEO. RBV is arguably one of the most important theories for the study of strategic management, and it is particularly pertinent to EEO, which is an internal important strategic resource that combines environmental entrepreneurship and entrepreneurial orientation. This study uses RBV to theoretically specify and empirically validate an EEO–environmental innovation–firm performance model that explains how EEO influences firm environmental innovation behaviors and its onward effect on firm performance. This organizing framework is consistent with the RBV tenet that the proper implementation of a firm’s business strategy will result in competitive advantages (Wernerfelt, 1984). Thus, this study fills a theoretical gap by investigating EEO from the RBV perspective.

Second, our study enriches the field of EIN, improving our understanding of the causes of environmental innovation practices. Although there are studies of EIN from different perspectives, they are relatively few. Studies of the antecedents of EIN focus on external factors, such as laws and regulations (Chen et al., 2012), social and community expectations (Lee et al., 2018), and competitive pressure (Li, 2014). There is a lack of empirical studies of firms’ intrinsic motivation to adopt EIN (Guo et al., 2020b; Zhou et al., 2018). This study investigates the effect of EEO (an internal factor) on EIN and contributes to the literature on environmental innovation.

Third, this study introduces stakeholder pressure as a moderating variable in the relationship between EEO and corporate environmental innovation, and thus enriches stakeholder theory. Previous studies indicate that stakeholder pressure has a positive influence on firms’ environmental protection initiatives (Bossle et al., 2016; Lee et al., 2018; Li, 2014). However, these studies investigate the direct effect of stakeholder pressure, and it remains unclear whether stakeholder pressure moderates the effectiveness of environmental strategies, specifically the relationship between EEO and EIN. Our study regards stakeholder pressure as a boundary condition in the EEO–EIN relationship and indicates that stakeholder pressure strengthens the positive influence of EEO on EIN. Furthermore, although many studies explore the influence of stakeholder pressure in developed economies (Vaitoonkiat & Charoensukmongkol, 2020a), commercial activities and marketing environments are different in emerging economies than in advanced economies (Sharma, 2019; Zhuang et al., 2019). Thus, studies conducted in advanced economies may not reflect the reality of emerging economies. This study explores these issues in the context of China’s emerging economy.

Management Insights

This study provides three main practical implications for managers. First, EEO, as a strategic orientation, can promote EIN. Similar to sustainable entrepreneurship (Bos-Brouwers, 2010), the aim of environmental entrepreneurship is not only to improve technologies and reduce costs, but also to develop EIN in products, services, and processes. Firms with higher levels of EEO can better realize EIN and improve firm performance than firms that focus exclusively on economic benefits. To maintain competitive advantages in the context of sustainable development, managers should fully exploit the positive effect of EEO. Specifically, firms should implement activities that boost EEO to positively guide and allocate resources and that extend beyond the traditional entrepreneurship mode. Senior managers should encourage the development and introduction of new environmentally friendly products or services and create a positive atmosphere for EIN within their organizations. Firms should also seek to become leaders in the use of environmentally friendly technologies and services and meet market demands ahead of competitors. In addition, firms should seize opportunities in the environmental protection market through the strategic use of important resources and some risk capital.

Second, implementing and promoting EIN may help firms to fully benefit from EEO. Managers need to encourage EIN practices and transform EEO into concrete actions. Managers should also be aware of the economic benefits of EIN, which helps build a green image, improves corporate reputation and enhances firm performance. Given these potential advantages, senior managers should develop EIN throughout their organizations and regard EIN as a key component of their corporate strategy. More concretely, managers should provide resources and opportunities for EIN, build and cultivate an EIN culture, and encourage staff to participate in EIN. Managers can implement and organize relevant training activities to improve the EIN of technicians. Firms should focus on the interaction and exchange with the external environment so that they can absorb advanced technologies from other organizations and promote the exchange and application of related EIN knowledge.

Third, our research emphasizes the role of stakeholder pressure in stimulating EIN, which encourages us to think about the influence of external factors on firms’ environmental management and proactive environmental strategies. As stakeholder pressure on management increases, enterprises’ operating decisions become more focused on the coordination of economic, social, and ecological outcomes. Firms seeking growth and market opportunities should respond positively to environmental issues and fulfill their social responsibilities. Stakeholder pressure from governments, consumers, and competitors tends to encourage firms to adopt EIN practices. For example, environmental laws and government supervision compel firms to implement EIN, so governments and regulators should monitor firms’ environmental management more strictly. In addition, managers should purposefully consider the environmental concerns of other stakeholders, such as consumers and suppliers. Strong stakeholder pressure can increase firms’ EIN and thus improve firm performance.

Limitations and Suggestions for Future Research

Our study expands the literature but has some limitations. First, the sample consists of firms in China, and future studies must examine whether EEO implementation varies across countries. Second, as we use cross-sectional data, our analysis cannot consider the dynamic interactions between firms’ EEO, environmental innovation and firm performance over time. Future research could examine long-term trends in firms’ conditions and conduct using longitudinal data. Third, most of our data are based on self-evaluation. Although the interviewees’ views on EEO, environmental innovation and stakeholder pressure may be reasonable and reliable, the evaluation of firm performance should be improved.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by “Yanta Scholars” Program of Xi’an University of Finance and Economics.