Abstract

This study investigates how government ownership (state-owned IPOs) and the political regime affect the flipping of IPO shares, as well as the moderating impact of investor demand on the association between the political regime and flipping activity. Ordinary least square was employed to investigate the impact of government ownership and political regime on the flipping of IPO shares. The data set consists of 95 IPO firms listed on the Pakistan Stock Exchange (PSX) during the period of January 2000 to December 2019. The findings of this study reveal that government ownership and a political regime have a positive influence on the flipping of IPO shares, demonstrating the quality that creates liquidity in Pakistan’s IPO market. Furthermore, in Pakistan, investor demand has been reported to moderate the association between the political regime and IPO flipping activity. This research offers valuable insights that may result in abnormal trading behavior or flipping immediately after listing. Likewise, state-owned IPOs and the political regime appear to be more appealing to investors, signaling the firms’ high quality, causing in increased demand and higher levels of flipping. As a result, the government and regulators may devise policies to control unusual trading, ensuring that government investments in the capital market are successful and also that the government’s economic and political objectives are met. Moreover, this research is critical for investors and issuers making investment decisions.

Keywords

Introduction

One of the trending topics among researchers is to examine events around initial public offerings (IPOs), which refers to an unusual trading volume pattern on the first few trading days after listing. This activity is referred to as IPO flipping (Aggarwal, 2003; Leow & Lau, 2020). Flipping is the practise of immediately selling allotted shares within the first few days of a company’s listing by rational investors, often known as flippers. Flipping gives investors with immediate market gains and increases the liquidity of the new market by reserving additional shares for later trading activities (Aggarwal, 2003). Notwithstanding its advantage, excessive flipping can destroy a company’s value and shareholders’ wealth. An excessive flipping generates unexpected and significant movements of new shares that could pull IPO prices down below their reasonable value (Gounopoulos, 2006).

Researchers have widely documented in terms of the evidence of flipping activity, for example, the United States (Aggarwal, 2003; Gounopoulos, 2006) and Australia (Bayley et al., 2006), and in emerging markets, for instance, China (Kooli & Zhou, 2020) and Malaysia (Albada et al., 2022). Yet, there is dearth of empirical evidence on flipping from the Pakistani IPO market. Nonetheless, Yar and Javid (2014) provide evidence of unusual trading behavior in the Pakistani IPO market, which may indicate flipping; however, no detailed empirical evidence of flipping and its determinants is provided. Thus, the purpose of this article is to look at the impact of state-owned IPOs on flipping in the Pakistani capital market and to provide additional empirical evidence about whether or not flipping activity occurs on the day of listing.

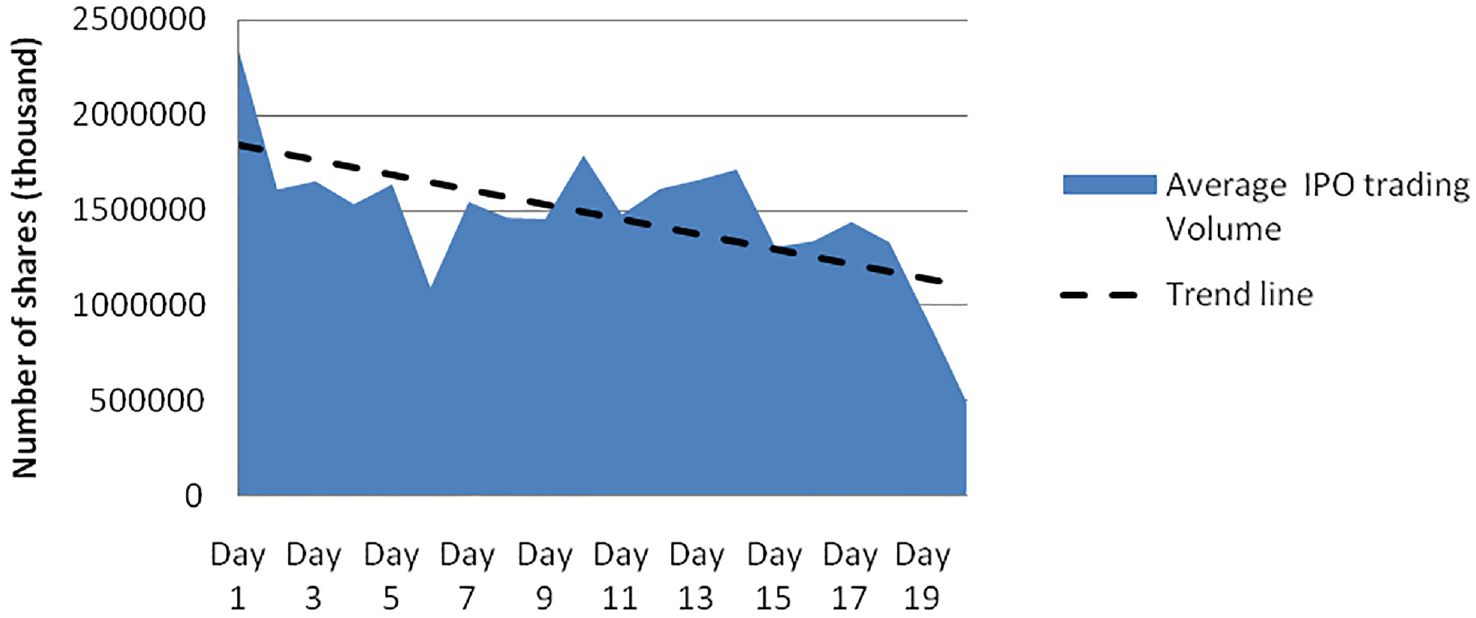

For several reasons, the Pakistani IPO market is worth investigating. First, there is evidence of a high trading volume on the first five trading days, indicating that flipping occurs in the Pakistani IPO market (refer Figure 1). Second, privatization policies differ across countries based on economic and political factors. For example, the government owns the majority of industries in Pakistan, and the majority of them are underperforming. As a result, the government uses IPOs to privatize inefficient industrial units while also developing the capital market. On other hand, countries such as the United States, use privatization to balance the government budget and raise revenues by transferring shares to the private sector, thereby reducing government ownership (Goodman & Lovemen, 1991). Furthermore, Borisova et al. (2015) show that sick industrial units perform well after privatization because privatization limits political discretion. As a result, the current study seeks to investigate the performance of state-owned IPOs in terms of abnormal trading volume (flipping activity) during democratic regimes.

Trend of IPO trading volume for the first 20 days after listing (2000–2019).

Third, Pakistan has a unique governance system and experienced two different regimes: a democratic regime (post-2007 period) and a military regime (ruled between 1998 and 2007). Each regime has a specific aim for privatization. On the one hand, the democratic regime aims to privatize unhealthy industrial units and transfer shares to the private sector to tighten the monitoring mechanisms, increase capital, and improve technology. The military regime, on the other hand, used privatization mainly to broaden the capital market. Thus, high levels of flipping are expected to occur in Pakistan’s stock market during the democratic regime. Thus, IPOs by state-owned firms issued during a political regime are recognized as crucial factors affecting the flipping activity. According to the signaling theory (Grinblatt & Hwang, 1989), government ownership (secured investment) can provide a credible signal of IPO quality to investors and influence flipping. Furthermore, State-owned IPOs can be vulnerable to political interference, which can impact their performance and perception. This interference can include changes in government priorities, shifts in privatization policies, or government intervention in decision-making. Such risks can undermine investor confidence and increase the likelihood of flipping. Additionally, state-owned companies may face governance challenges and corruption risks, leading to concerns about transparency, accountability, and the fair treatment of minority shareholders. These risks can further impact investor confidence. Governments have privatized state-owned enterprises (SOEs) for decades to improve their performance and lower fiscal risk. However, the success of this strategy is closely linked to government credibility in the market. If the partially privatized asset is vulnerable to government interference, this creates uncertainty for investors with adverse effects on the value of shares. It also means that the full benefits of privatization in terms of improved efficiency may not be realized. Hence, this paper investigates the impact of government ownership and political regime on flipping activity. To test our proposition, we consider 95 IPOs listed on the PSX from 2000 to 2019. The results report that IPOs issued by state-owned firms have a positive and significant relationship with IPO flipping. Also, investors’ demand positively influences the relationship between a political regime and the flipping activity.

This study extends the existing literature, as to the best of the author’s knowledge, this issue has never been addressed in Pakistan’s context. Two previous studies examined on the short- and long-run performance of IPOs by state-owned and non-state-owned firms based on the information asymmetry concept. Nonetheless, these studies provide no direct evidence of the association between government ownership, political regime, and the flipping of IPO shares. Hence, this paper extends previous study Malik et al. (2017) on short- and long-run underpricing by examining the impact of government ownership and political regime on flipping. The government, in the role of the issuer, has superior information. Thus, they lower IPO prices to attract investors. Chen et al. (2017) documented that governments of emerging countries underpriced their IPOs unnecessarily and did not care about the IPO proceeds as long as they could achieve their political objectives. However, Pakistan has been under the ruling of two government regimes—a political and a non-political regime—and these two regimes may have different privatization objectives.

This paper extends the work of Malik et al. (2017) by testing the unusual trading behavior of flipping during the first 5 days after listing. This paper proposes that the IPOs by state-owned firms during the political regime may convey firms’ good quality, which may increase the confidence of rational investors and encourage the flipping of IPO shares. Rational investors tend to anticipate high returns from state-owned IPOs due to government ownership. In addition to it, this paper contends that investor demand for state-owned IPOs in Pakistan could influence the signaling role of government ownership and political regime. According to the signaling theory, government ownership in initial public offerings can serve as a credible signal to investors regarding the quality of the IPO. In the case of state-owned initial public offerings (IPOs) in Pakistan, government ownership indicates that the government has a stake in the company and may have superior information about its prospects, financial health, or growth potential. This ownership can make investors believe that the IPO is of a higher quality, which boosts confidence in the company and the demand for its shares. As this issue has not been addressed in previous studies, this paper fills the gap by examining the effect of government ownership and political regime on the flipping of IPO shares using the signaling theory.

The findings of this study are expected to have practical implications for the government, policymakers, and investors. Government and regulatory authorities, such as the Securities and Exchange Commission of Pakistan (SECP) and the Privatization Commission of Pakistan (PCP), may use the findings of this study to set guidelines on the monitoring of state-owned IPOs during the listing process. Also, they need to keep an eye on the trend of investor demand, which may lead to excessive trading activities during the first few days after listing, as excessive flipping can put downward pressure on IPO prices. Thus, the government and regulators may devise policies to control unusual trading ensuring successful government investments in the capital market and the government’s economic and political objectives could be met. Besides, this paper offers insights to investors regarding making rational decisions on whether to invest in state-owned IPOs during the rule of a political regime or a non-political regime.

The remainder of this paper is organized as follows. Section “Literature Review and Hypothesis Development” discusses the existing literature on IPO shares’ flipping, state-owned IPOs, and political regime. Section “Data and Methodology” presents the data and research methods. Section “Results” reports the results, and Section “Conclusion” provides the conclusion and implications of this study.

Literature Review and Hypothesis Development

Flipping Activity and Its Determinants

A unique paradox of initial public offerings known as flipping activity has been investigated in both developed and emerging economies’ perspectives. For example, flipping activity studies in the US market show that underwriters are responsible for IPO price stability, most likely because underwriters are a key factor (Ellis et al., 2000). Whereas, Krigman et al. (1999) found that institutional financial investors appear informed by flipping underperforming IPOs, demonstrating their ability to trade profitably. Underwriters also support US institutional investors, who are considered a “solid hand” due to their long-term investments (Aggarwal, 2003). Additionally, the findings demonstrate that institutional investors limit flipping, therefore they get more IPO shares. Conversely, Gounopoulos (2006) found that institutional investors flipped more hot IPOs than prior studies. From Australian Stock Market, Bayley et al. (2006) found a negative relationship between flipping and issue size in the first 3 days of Australian trading. Like Aggarwal (2003), they found higher flipping rates for underpriced IPOs than overpriced ones. Whereas, Trana et al. (2007) found that institutional investors flipped more hot IPO issues in Finland’s IPO market, similar to the findings of earlier studies by Aggarwal (2003), Bayley et al. (2006), and Gounopoulos (2006). Moreover, the study found that flipping levels varied across industries, disproving the idea that some industries were privileged at a certain time.

From emerging market, Islam and Munira (2004) were the first to study the flipping behavior and factors in Bangladesh’s IPO market. Institutional participation positively affects flipping in the Bangladeshi IPO market, but initial return does not. Later, Neupane et al. (2017) found new drivers of investors’ flipping behavior across two primary IPO allocation systems in India (i.e., book building and auction). Underwriters’ flexibility in allocating shares prevented flippers and allowed them create long-term ties with IPO investors. Afterwards, Kooli and Zhou (2020) examined the drivers of flipping in China and the disposition effect and long-term success of IPOs. They found that investors sold more of their allocated shares in hot issues than cold issues. Recently, Leow and Lau (2020) and Albada et al. (2022) investigated how pre IPO information affects flipping in the Malaysian IPO market.

Based on the above discussion on developed and emerging IPO markets, it can be surmised that little attention has been given to the influence of state-owned IPOs and political regime on flipping. Nonetheless, state-owned IPOs and the political regime are considered as important determinant in improving the economy. Despite the occurrence of unusual trading behavior in Pakistan’s IPO market (Anwar et al., 2023; Kayani & Amjad, 2011; Malik et al., 2017), which may indicate flipping, very few studies have examined the determinants of flipping in Pakistan. Therefore, this study aims to assess the level of IPO flipping activity and identify its determinants in Pakistan, especially for state-owned IPOs and political regimes.

State-Owned IPOs

State-owned IPOs refer to the IPOs issued by firms owned by the government. This paper uses the signaling theory to explain the influence of government ownership on flipping. This theory argues that the government’s decision to retain a large proportion of a firm’s shares in an IPO generated by a state-owned firm produces signals of the firm’s sound quality to investors (Grinblatt & Hwang, 1989), resulting in increased investor confidence in the IPO as they believe that better prospects would maximize their wealth from the IPO investment. Consequently, the demand for the IPO would rise and there would be more significant flipping of the IPO shares compared to the IPOs issued by non-state-owned firms.

Some previous studies have examined firm ownership and underpricing (see Aussenegg, 2000; Choi & Nam, 1998; Dewenter & Malatesta, 1997; Peter, 2007; Setiobudi et al., 2011; Vieira & Serra, 2006). Most of these studies (see Aussenegg, 2000; Peter, 2007: Setiobudi et al., 2011) reported high levels of underpricing of state-owned firms compared to non-state-owned firms. However, other studies (e.g., Choi & Nam, 1998; Vieira & Serra, 2006) reported contradicting results. Only two studies have looked into the relationship between state-owned IPOs and liquidity (see Bortolotti et al., 2007; Ding & Suardi, 2019). According to Bortolotti et al. (2007), IPOs initiated by state-owned firms increase the overall market liquidity and have spillover effects on the liquidity of non-state-owned firms. In addition, these IPOs offer improved risk diversification opportunities and risk-sharing brought about by privatization. Meanwhile, Ding and Suardi (2019) found increased investors’ demand for IPOs initiated by state-owned firms due to the better prospects of the firms.

In the context of Pakistan, only two studies have investigated the short-term and long-term performance of IPOs with the performance of state-owned firms in Pakistan (see Malik et al., 2017; Rizwan & Khan, 2007). Both studies concluded that state-owned companies underpriced their first public offerings. Bash (2001) observed a negative association between underpricing and flipping, while Kooli and Zhou (2020) discovered the positive relationship. Despite the abundance of research showing that company ownership affects an IPO’s short- and long-term returns and liquidity, the relationship between state ownership and flipping has received relatively little attention. Hence, given the unexplained trading volumes or flipping after the first few days of listing, an investigation of IPOs of state-owned firms is required.

H1: State-owned IPOs are significantly related to the flipping activity.

Political Regime

The primary goal of privatizing state-owned firms through IPOs is to increase government revenues (López-de-Silanes, 1997). The most common reason for privatization is fiscal pressure on the government (Yarrow, 1999). However, Fan et al. (2007) argue that privatization is fundamentally a political process and might have political goals. To achieve political desires, governments underprice the IPOs of state-owned firms, resulting in high underpricing of state-owned IPOs in emerging markets. However, Beatty and Ritter (1986) found a strong and significant negative relationship between retained government ownership and underpricing. Moreover, Albada et al. (2022) found a significantly positive relationship between underpricing and flipping, but Bash (2001) found a significantly negative relationship between the two variables. Pakistan has experienced ruling by two different regimes, namely, a democratic and a military regime. Each of the regimes has a different aim for privatization. For example, the democratic regime aims to privatize unhealthy industrial units and to transfer shares to the private sector in order to tighten the monitoring mechanisms and inject more capital and technology. In contrast, the military regime’s aim of privatization is mainly to broaden the capital market (Anwar et al., 2022). Therefore, high levels of flipping in the stock market of Pakistan are expected during the democratic regime’s ruling.

H2: Pakistan’s political regime significantly influences the flipping activity for IPOs generated by state-owned firms.

Investors’ Demand and Political Regime

This study was designed to examine the moderating effect of investor demand on the link between Pakistan’s political regime and flipping activity following listing. As government ownership has been found to improve liquidity (Borisova et al., 2015; Ding & Suardi, 2019). The government has several political motives for privatization, such as low unemployment rate, high economic growth, ensuring the survival of crucial but sick industrial units that offer primary services to the economy, and safeguarding the reputation of the government by showing that government investments do not fail (Borisova et al., 2015). Therefore, investors tend to have a high demand for state-owned IPOs because they find that government ownership enhances firms’ value. Highly demanded IPOs signal firms’ good quality, thereby motivating rational investors to flip more during the first few days post-listing (Anwar & Mohd-Rashid, 2021; Mohd-Rashid et al., 2016). Following the above discussion, this paper proposes that the effect of a political government regime on flipping activity is higher for highly demanded IPOs (Leow & Lau, 2020).

H3: Investor demand moderates the association between a political regime and the flipping activity.

Data and Methodology

Data

The developed hypotheses were tested for a sample of 95 IPO exercises held between 2000 and 2019. The year 2000 was chosen as the beginning year for the sample because, firstly, Pakistan Stock Exchange transitioned from a manual to a computerized system in the year 2000. Secondly, IPO exercises in Pakistan before the year 2000 were on a declining trend because of political, economic, and social crises. As a result, there was no listing of IPO firms in Pakistan in 1999.

The initial total population of this study consisted of 108 IPO firms. Subsequently, three firms were omitted due to the non-availability of data, two firms were omitted due to inconsistent data, and eight modaraba firms were omitted due to their specific asset-liability reporting structure that does not allow for accounting comparisons. Hence, this study’s final sample consisted of 95 IPO firms. The omission of these IPO firms is consistent with previous IPO studies, such as Aslam and Ullah (2017), as these IPO firms are non-operating firms and have different regulatory criteria.

This research employed both pre-listing and post-listing secondary data. Pre-listing information includes state-owned initial public offerings (IPOs), offer price, issue size, firm sector, and the Karachi Stock Exchange (KSE) 100 price index. The sources of pre-listing data were firm prospectuses, DataStream, the Pakistan Stock Exchange’s website, and the SECP’s Data Centre. Post-listing data comprises of opening and closing prices of the IPO shares on the first trading day, as well as the trading volumes and subscription ratios for the first trading week after listing. These data were also collected from DataStream, the Pakistan Stock Exchange, and the SECP websites. In addition, the variables, descriptions, definitions, and data sources for this study are listed in Table 1.

Variables Description Definition and Data Sources.

Model Specification

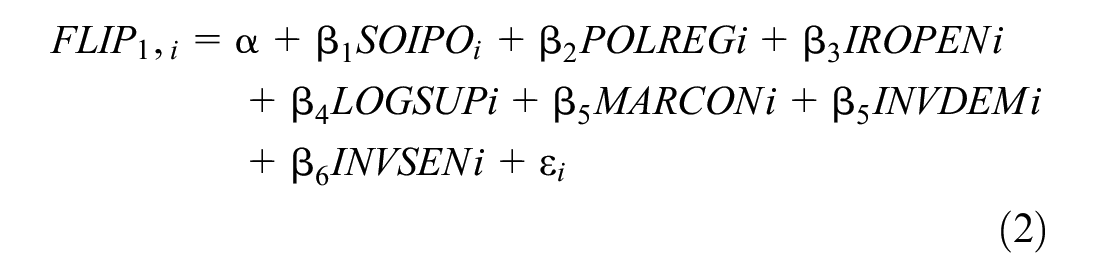

We employed an ordinary least square (OLS) method to analyze the effect of state-owned IPOs and political regime on the IPO flipping. We also investigate the moderating effect of investors’ demand on the relationship between state-owned IPOs and the flipping. To test our proposition, we develop the following model:

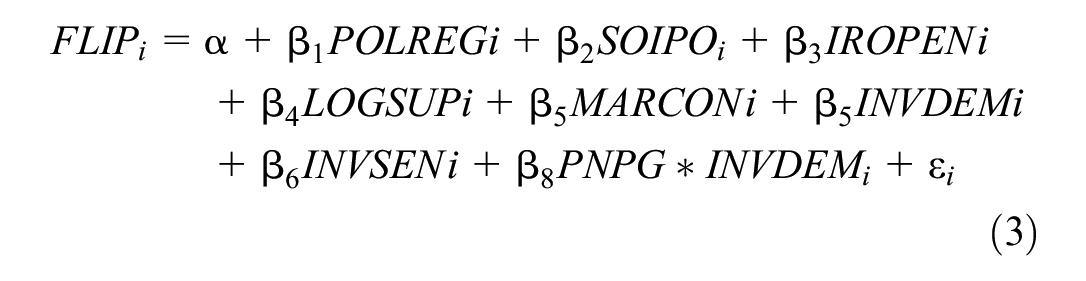

We also include the political regime in the model which can be expressed as:

The dependent variable is the flipping activity (FLIP) referring to the trading volume on the first day of listing divided by the total number of shares issued. Previous studies widely used this proxy because excessive trading volumes during the initial couple of trading days are likely to be attributed to flippers (Aggarwal, 2003; Kooli & Zhou, 2020), Moreover, the flipping activities based on third and fifth days of trading volumes. Independent variables include state-owned IPOs (SO IPO). In line with Setiobudi et al. (2011), and Malik et al. (2017), state-owned IPOs is used as a dummy variable if a firm is state-owned that takes the value of 1 and 0 otherwise. The purpose of using a dummy variable instead of the percentage of state-owned IPOs is due to the low number of state-owned IPOs offered during the sample period. State-owned IPOs indicate government ownership, reflect a large percentage of government shareholding, and signal firms’ good quality, resulting in increased investor demand and higher levels of flipping in comparison to non-state-owned IPOs. A dummy variable represents the political or non-political regime (POLREG); an IPO issued during a political government’s tenure is given a value of “1” and “0” otherwise. Pakistan has experienced two types of government regimes, namely, a military government in 2000–2007 and a democratic government from 2008 to the present. Government ownership improves liquidity, and a political government has certain economic and political motives behind privatization to show that government investments do not fail (Borisova et al., 2015; Ding & Suardi, 2019). Consequently, the government signals firms’ good quality, thereby generating investor demand and motivating flipping.

Other variables that may impact the flipping of IPO shares are controlled in the statistical model. This study controls other pre-IPO characteristics, such as the initial return (IROPEN), market conditions, supply, investor demand, and investor sentiments. Using the initial return as a control variable is in line with previous works (see Aggarwal, 2003; Che-Yahya et al., 2018; Kooli & Zhou, 2020). In these previous studies, the initial return was measured as the percentage change in price between the opening price on the first day and the offer price, and it is argued that the initial return on the day of listing provides a signal of a firm’s quality and accordingly influences flipping.

To capture the IPO market’s condition, a dummy variable (MARCON) was created to distinguish a hot issue from a cold issue market. MARCON takes a value of 1 if a company made an IPO during a hot issue market, whereby the total issue size exceeds the mean issue size of the sample (Che-Yahya et al., 2014). A positive relationship should be anticipated between a hot issue market and the flipping activity. A high volume of IPOs (a hot issue market) is usually linked with high initial returns (Ritter, 1998). The supply of IPOs (LOGSUP) stands for the issue size, which is calculated using the total IPO proceeds (Che-Yahya et al., 2018). A bigger offer size shows a bigger supply of the IPO shares such that, ceteris paribus, more subscription applications will be satisfied and fewer numbers of the shares will be demanded during the first few days post-listing. This study argues that IPO supply is negatively linked to the flipping activity.

Investor demand (INVDEM) particularly focuses on the pre-listing demand by investors for the IPO (Che-Yahya & Abdul-Rahim, 2015) and is generally measured by the over-subscription ratio (OSR). Pre-offering information in the prospectus provides a signal to investors, which is then reflected in their demand for the IPOs (Aggarwal et al., 2008). Therefore, this study proposes that an excess demand for an IPO would typically put extra weight on the aftermarket IPO price and consequently, induce more flipping of the IPO shares.

Investor sentiment (INVSEN) is measured by heuristic representation that is estimated as the mean returns of the three most recent IPOs before the issuance of a given IPO (Bayley et al., 2006; Che-Yahya et al., 2018). Investors are less inclined to flip their shares when they are idealistic about the future or the long-term gains of the IPO (Chong et al., 2011). This study proposes that a positive (negative) mean initial return of the three most recently issued IPOs tends to draw an optimistic (pessimistic) sentiment among investors, thus causing increased (decreased) flipping of IPO shares.

The moderating model was used to examine the subsample for the signaling hypothesis. Since state-owned IPOs that are listed during the ruling of a political government regime tend to be in high demand, it is proposed that investors’ demand has a significant moderating effect on the relationship between a political regime and the flipping of IPO shares. The moderating regression model developed in this study is as follows.

Results

Figure 1 exhibits the average trading volume of IPOs on the first 5 days after listing. Average trading volume on the first 5 days is high followed by a decreasing trend on days 6 and 7. Subsequently, the average trading volumes fluctuate from day 9 to 15 and adopt a declining trend afterwards. This trend of high fluctuations after listing may indicate the occurrence of flipping in Pakistan’s IPO market.

Descriptive Statistics

Table 2 presents a summary statistic of the variables used in this study. We report that the range of flipping activity on the first trading fluctuates between 0 and 73.98%. The average flipping activity is 10.68% with a median of 3.60%. These results show the occurrence of flipping activity in Pakistani IPO market following listing. However, the level of flipping in the Pakistani market is lower than those experienced in developed markets, such as the US at 15% (Aggarwal, 2003), and Australia 22% (Bayley et al., 2006).

Descriptive Statistics.

Note. FLIP i = flipping activity on the first, third, and fifth trading days; State-owned IPO is a dummy variable that takes the value of one if IPO is issued by state-owned firm; Political regime = Political Government is equal to 1 and 0 for Military government. Initial returns at the start of IPO trading; Shares issued = natural logarithm of shares issued which is used as a proxy of supply of shares; MARCON = market conditions; INVDEM = investor demand; INVSEN = investor sentiments.

, **, *** denote significance level at the 10%, 5%, and 1%, respectively.

Average flipping activity in Pakistan is also low as compared to other developing countries. For example, Islam and Munira (2004), Che-Yahya et al. (2014), Neupane et al. (2017), and Kooli and Zhou (2020), documented the average flipping activity of 29.67%, 38.30%, 44%, and 64% in Bangladesh, Malaysia, India, and China, respectively. However, the average flipping activity is higher than that reported by Chong et al. (2009) of 7.66% in the Malaysian market.

State-owned IPOs account for 12.60% of the total IPOs issued. Initial returns at the start of IPO trading ranges between −32% and 344% with an average initial return of 20.745% (offer price to opening price). The average market condition averages 0.432 and has a maximum of 1.000, indicating that 43% of IPOs were issued during a hot IPO market activity. The demand by investors on average is 2.7 times. While 46% of IPOs were issued during the military regime and the rest were issued during the democratic regime.

Correlation Analysis

Table 3 reports the correlation matrix for all the variables used in the analysis. The correlation results indicate a significant correlation between state-owned firms and the flipping activity. Moreover, the table shows that most of the correlation coefficients have small values below the 0.70 cut-off point. These results imply that multicollinearity is not a problem in the regression analysis.

Correlation Matrix.

Note. FLIP i = flipping activity on the first, third, and fifth trading days; State-owned IPO is a dummy variable that takes the value of one if IPO is issued by state-owned firm; Political regime = Political Government is equal to 1 and 0 for Military government. Initial returns at the start of IPO trading; Shares issued = natural logarithm of shares issued which is used as a proxy of supply of shares; MARCON = market conditions; INVDEM = investor demand; INVSEN = investor sentiments.

Effect of State-Owned IPOs and Political Regime on Flipping Activity

Table 4 illustrates the results of the state-owned IPO with other control variable in OLS regression of flipping activity models. Additionally, the political/ non-political regime included in OLS regression models for flipping on day 1 (Model 1), flipping on day 3 (Model 2), and flipping on day 5 (Model 3) are reported in Table 5, with flipping activity standing as the dependent variable. The R2 values for three models of the dependent variable, namely, flip1, flip 3, and flip 5, show that all the explanatory variables explain 28% to 38% of the variation in the flipping activity on the first, third, and fifth day. Additionally, the coefficient of the baseline OLS regression is 25.66%, and it improves to 28% by including the political/non-political regime factor. The 28% reported for flip1 is higher than the 15.78%, 7.30%, 17.60%, and 15.56% reported in Aggarwal (2003), Chong et al. (2011), Gounopoulos (2006), and Islam and Munira (2004), respectively. The significance of F-statistics (.003) at the level of 0.01%.

Effect of State-Owned IPOs on the Flipping Activity.

Note. FLIP i = flipping activity; SO IPO = state-owned IPO; POLREG = Political Government (democratic government and Non-Political Government [Military government]); IROPEN = initial return open; LGSUP = log of supply; MARCON = market conditions; INVDEM = investor demand; INVSEN = investor sentiments.

, **, *** denote significance level at the 10%, 5%, and 1%, respectively

OLS Regression Results of Political Regime with Flipping Activity Models.

Note. FLIP i = flipping activity; SO IPO = state-owned IPO; POLREG = Political Regime (democratic government and Non-Political Government [Military government]). IROPEN = initial return open; LGSUP = log of supply; MARCON = market conditions; INVDEM = investor demand; INVSEN = investor sentiments.

, **, *** denote significance level at the 10%, 5%, and 1%, respectively.

The OLS findings demonstrate that state-owned IPOs are positively significant on the flipping activity of IPO shares for Model 1, Model 2, and Model 3 in Table 4. The results mean that state-owned IPOs experience increased levels of flipping following listing in Pakistan’s IPO market, which generates liquidity. The results of this study are similar to Bortolotti et al. (2007), which documented that IPOs issued by state-owned firms increased the overall market liquidity and had spillover effects on the liquidity of IPOs issued by non-state-owned firms. IPOs issued by state owned-firms signal good quality as the government offers only a certain portion of the shares during listing while retaining a substantial percentage. As a result, investors’ confidence is boosted and there will be increased flipping in comparison to the IPOs issued by non-state-owned firms. The results support the signaling theory of Grinblatt and Hwang (1989), whereby the government’s retained ownership could influence flipping by sending credible signals of the quality of the firm to investors. Investors will be more confident to invest in the IPO, as they believe that the firm’s good prospects would maximize their wealth from the investment. Consequently, there will be a significant influence on flipping on the first day of listing of the IPO shares.

Table 5 demonstrates political/non-political regime is also positive and significant to the flipping activity on the first day of listing. This result is in line with Ding and Suardi (2019) and Borisova et al. (2015), which find that a political government improves liquidity as there are certain economic and political motives behind state-owned IPOs. The political regime can have an impact on investor perceptions and confidence in the IPO market. Under a democratic regime, state-owned IPOs may be perceived as having better prospects and governance due to the government’s focus on improving industrial performance. This positive perception can encourage investors to engage in flipping, anticipating higher returns. However, political interference can also impact the performance and perception of state-owned IPOs, leading to concerns about transparency, accountability, and the fair treatment of minority shareholders. Therefore, it is important to ensure good governance practices and transparency in the IPO market to avoid political interference and create certainty for investors. Furthermore, this result indicates that there is greater political influence in emerging markets than developed market, specifically in Pakistan’s IPO market. Because most of the firms are family owned and these families have political background.

Furthermore, the robust regression results to evaluate the association of state-owned IPOs and political regime with flipping activity. Firstly, the outliers were omitted from the data set in order to obtain error-free results, and then robust regression analysis was performed. Robust regression has fewer preventive assumptions, and also delivers improved regression coefficients in comparison to OLS regression. The presence of outliers in the data set affects the assumption of normally distributed data. In addition, the existence of high values of outliers in the data set could lead to misrepresentation of the coefficients. Consequently, the use of robust regression minimizes the impact of outliers, as it is recognized as an iterative technique that assists in classifying outliers and reduces its effect on the coefficient estimates. Based on this analysis, government ownership of IPO shares emerged as a key variable.

As for the control variables, initial return (IR OPEN) has a negative association with the flipping activity, but it is not significant for Model 1. However, for Model 2 and Model 3 of Table 5, the initial return has a significant negative association with the flipping activity. This negative relationship is consistent with the previous study by Krigman et al. (1999), which found that low under-pricing is due to mispricing by underwriters and has nothing to do with flipping. Next, market condition (MARCON) is negatively significant on the flipping activity for day 1, day 3, and day 5. This negative result is consistent with Mohd-Rashid et al. (2016), which found that rational investors will hold their new allotted shares during a hot (good) market condition as they expect that the price will increase in the long run.

The next control variable is the supply (LOGSUP) of IPOs. The findings show that in the Pakistani IPO market, there is a significant negative association between IPO supply and the flipping activity on the first day after listing. This result supports the expectation that when the IPO supply is high, additional subscriptions will occur. Subsequently, further demand will be made which will encourage more flipping immediately after the first couple of days of listing. Prior studies that support the influence of IPO supply include Islam and Munira (2004), Bayley et al. (2006), and Che-Yahya et al. (2014). Besides, these studies find that smaller offerings have documented higher levels of flipping. The coefficient of investor demand (INVDEM) is positively significant. The results suggest that state-owned firms signal good quality and investors are confident that the firms’ good prospect would maximize their wealth from the IPO investments. Consequently, there will be a rise in demand that will significantly influence the flipping of the IPO shares on the first, third, and fifth-day post-listing. The result is consistent with Rahim et al. (2013). Investors’ sentiments (INVSEN) have a positive but insignificant effect on flipping. This result implies that a high average return on the three most recently issued IPOs causes diverse opinions on the new IPO’s valuation. Alternatively, investors’ decision to flip a new offer is associated with the performance of past recent IPOs. The result also indicates that the IPOs of state-owned firms during a political government era have high demand, which causes flipping.

Moderating Effect of Investor Demand on the Political Regime and Flipping Activity

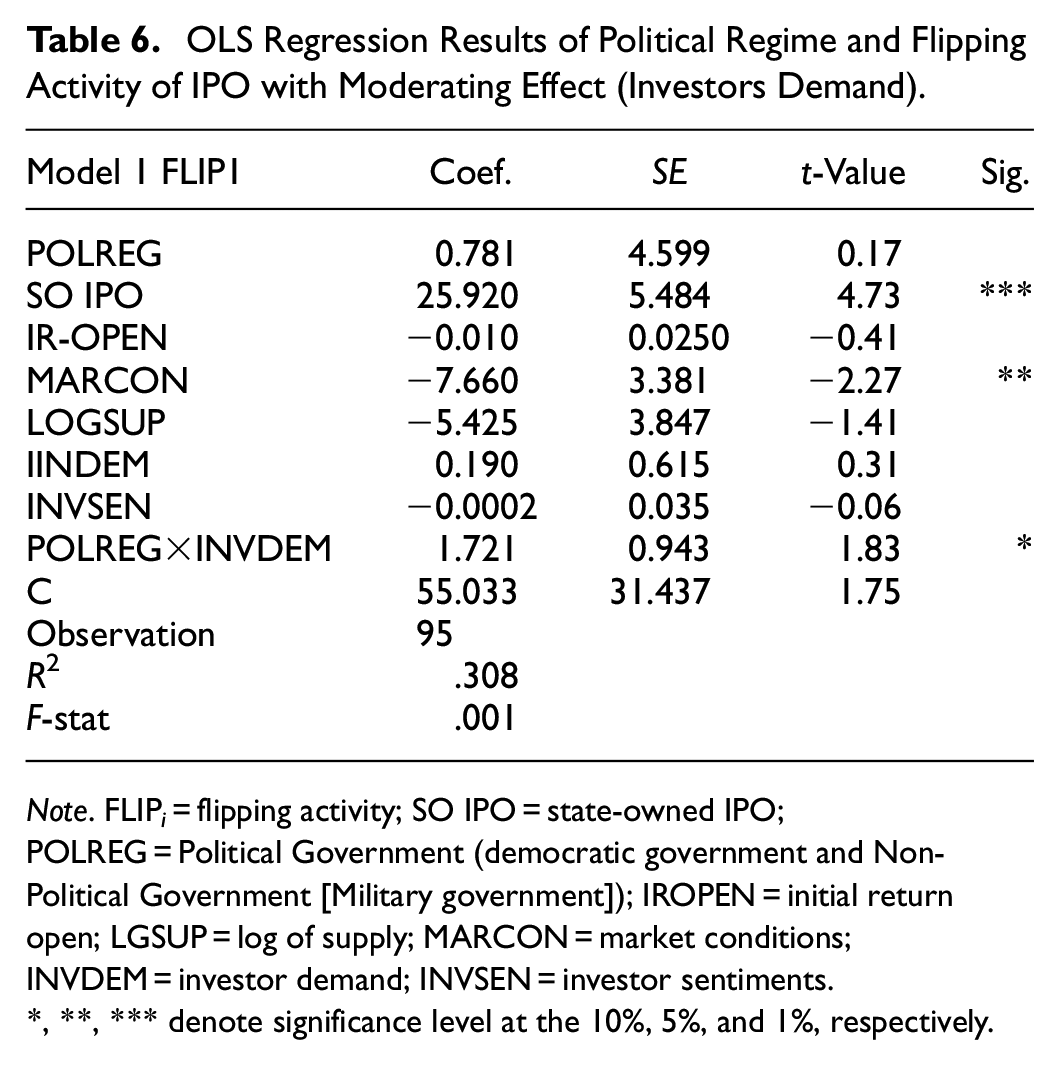

Furthermore, this study tested the moderating impact of investor demand on the association between political regime and the flipping of IPO shares. Model 1 of Table 6, shows that there is a positive moderating impact, indicating that investors’ demand strengthens the relationship between political regime and flipping.

OLS Regression Results of Political Regime and Flipping Activity of IPO with Moderating Effect (Investors Demand).

Note. FLIP i = flipping activity; SO IPO = state-owned IPO; POLREG = Political Government (democratic government and Non-Political Government [Military government]); IROPEN = initial return open; LGSUP = log of supply; MARCON = market conditions; INVDEM = investor demand; INVSEN = investor sentiments.

, **, *** denote significance level at the 10%, 5%, and 1%, respectively.

The results of this study confirm the findings of Che-Yahya et al. (2014) and Leow and Lau (2020) that rational investors are profit-driven and quickly flip their new stocks when they learn that the shareholdings are in high demand on the IPO market. The findings indicate that the IPOs of state-owned firms listed during a political regime signal the firms’ high quality, which increases investor demand and motivates flipping. This perception is associated with the explanation of signaling theory (Grinblatt & Hwang, 1989). Investors view political government ownership as value-enhancing, which increases their demand for state-owned initial public offerings (Ding & Suardi, 2019).

Conclusion

This paper investigates whether government ownership and political regime influence the flipping of IPO shares in Pakistan’s IPO market using the sample of 95 IPOs from 2000 to 2019. We find that state-owned IPOs and political regimes positively influenced the flipping activity. This evidence corroborates the signaling theory Leow and Lau (2020), which shows that state-owned IPOs play an important role in flipping of tradable shares since government ownership signals to the public about the firm’s good quality, which boosts investor confidence and the share price. Flippers (rational investors) tend to sell their allotted new shares immediately after listing to obtain abnormal returns in the long run. We further argued that flippers are profit-driven and positively flip their new shares in the light of high demand.

The importance of political goals is supported by the positive influence of political regime. It means that the Pakistani IPO market receives a significant political impact. A comparison of the coefficients of the baseline and political/non-political government models indicates that after including the political regime, the coefficient improves and the political government sends a credible signal of quality which enhances investor’ demand, resulting in a high level of flipping in Pakistan’s IPO market. The findings are consistent with Ding and Suardi’s (2019) findings on the Chinese IPO market, in which investors perceive government ownership as adding value and, as a result, demand for state-owned IPOs increases.

Furthermore, it has been discovered that investor demand plays a moderating role in the relationship between a political regime and flipping activity. Specifically, the political regime is significantly and positively associated with flipping during the first day of IPO listing. Therefore, these results support the signaling theory after incorporating investor demand in the IPO model’s flipping activity. The findings reveal the state-owned firms and political regime signal good quality, thereby increasing the flipping activity in emerging markets and show that investors recognize state-owned IPOs to be of high quality.

This study’s findings have practical implications for the government, policymakers, and investors. To attract investors in the Pakistani market, which is subject to significant uncertainties due to economic and political instability, the government offers IPOs of state-owned firms to signal good quality through large issue sizes. Additionally, investors believe that the government safeguards state-owned IPOs from investment failure. Thus, these firms provide healthy long-run returns and increase in value in the future. Additionally, this study is valuable for policymakers and regulatory agencies such as the Securities and Exchange Commission of Pakistan (SECP) and the Privatization Commission of Pakistan. As the results of the study suggest that under a democratic regime, state-owned IPOs may be more likely to do flipping due to the perception of good quality firms and higher investor demand. Thus, policymakers can use the findings to design privatization strategies that align with the goals of each political regime and account for potential flipping activity. It is important to maintain investor confidence in the IPO market, particularly during political regime transitions. Policymakers can work to create a stable and predictable environment for investors by implementing measures to reduce political uncertainty, ensuring transparent governance practices, and promoting fair treatment of minority shareholders. This can help mitigate risks associated with investor behavior, including flipping activity. Additionally, policymakers should strive to ensure policy continuity during regime transitions. Sudden shifts in privatization policies or inconsistent approaches can create uncertainty and negatively affect investor confidence.

The study’s scope is limited to examining abnormal trading volume specifically in relation to IPOs during the initial days following their listing. This limitation arises due to the occurrence of flipping, a phenomenon commonly observed during the early days of listing. To ascertain the long-term performance of IPOs in relation to trading volume, it is imperative for IPO companies to conduct a comprehensive liquidity analysis. Future research may consider additional factors that influence flipping activity prior to an IPO. Lock-up regulations are a prevailing feature in the global IPO markets, with each market having its own distinct set of regulations. The potential impact of diverse lock-up regulations on IPO flipping activity is a subject of interest.

Footnotes

Acknowledgements

We thank all authors for their contributions. We also appreciate Dr. Badru Bazeet Olayemi for his valuable suggestions and comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest concerning the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

It’s not applicable.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.