Abstract

This paper examines the impact of firms’ characteristics and corporate governance on the auditor change decisions using a logistic regression. The sample includes all U.K. companies listed on the London Stock Exchange that have changed their auditors between March 2013 and February 2018. The objectives are two-fold: (a) investigating the antecedents of audit change decision in general and (b) exploring the drivers of the decision to change auditors to a big 4. Results show that board independence, executive board members diversity and board members compensation are negatively related to auditor change decision, whereas return on assets and size are positively related to such decision. Moving to the second objective, results support the positive role of the company’s size in the choice of a big 4 auditor. The findings help stakeholders better understand the auditor change context prior to any strategic decision. Fruitful implications are highlighted too.

Introduction

The audit market has been a topic of considerable interest to both researchers and regulators. Following the demise of Arthur Andersen, a new trend of changing auditors appeared. Subsequent to Enron’s scandal, and until 2006, 7,629 cases of auditor changes among U.S. firms were reported, representing approximately half of the registered U.S. companies at that time (Grothe & Weirich, 2007). More than half of these change cases were initiated by the company and not by the auditor. Companies change their auditors in search for a better service, more specialization in a certain industry or lower audit fees. Sometimes the change is triggered by a disagreement with the incumbent auditor, change in their management perceptive or even as result of a certain policy that dictates a consistent change to bring in a new blood. While some companies disclose the true driver behind the change, many others choose to keep it secret. During 2005 and 2006, more than 2,000 companies that changed their auditors refrained from disclosing the reason behind this change (Grothe & Weirich, 2007).

The audit industry was dominated by the Big Eight (Arthur Andersen, Arthur Young, Coopers & Lybrand, Deloitte Haskin & Sells, Ernst & Whinney [EY], Peat Marwick Mitchell, Price Waterhouse [PwC], and Touche Ross), which has become the Big Four today (Deloitte, PwC, EY, and KPMG). Although the big auditors have failed many times in spotting financial wrongdoings in big corporations which resulted in a decline in the public confidence (Sankar & Narayan, 2017), they are still dominating the industry. Ninety-seven percent of the publicly owned corporations in U.S. and 70% of the European public entities are audited by one of these firms. Similarly, the UK market raised concerns about the concentration of the big N accounting firms and the absence of competition (McMeeking, 2009). In 2006, the big N firms were auditing 99 companies of the FTSE100 and 242 companies of the FTSE250 (Oxera Consulting Ltd, 2006). The problem of concentration continued in 2010. The big four firms earned 99% of audit fees paid by the FTSE350 firms (Competition Commission, 2012). The absence of competition resulted in lower audit quality and less efficiency. The auditors lost their significant role in reflecting a trustworthy image of the company’s position to shareholders, investors and creditors (Competition Commission, 2012).

Many researchers discussed the possibility of the big 4 to become big 3 at any time; however, both the regulators and the clients expressed their desire to preserve the four industry pillars operational (Harris, 2017)

After more than 15 years of big accounting scandals in the audit industry, a study is warranted to uncover the factors that are behind the company’s decision to change its auditor. Companies incur direct and indirect costs when changing their auditors, and scholars always aim to shed light on the reasons behind such a decision. Thus, the objective of this study is two-fold, and aims to answer the following questions: (a) What are the factors that affect the companies’ decisions to change their auditors? and (b) What are the factors that affect the companies’ decision to change their auditors to big 4? More specifically, this study attempts to find out the factors determining an auditor change decision in general and the choice of a big four, in particular among companies included in FTSE 250 index. These factors are divided into two categories, firm specific factors, and corporate governance factors. To address the research questions, a logistic regression is used. Indeed, this research is of a great importance, as it aims to assist stakeholders in better understanding the auditor change context, enabling them to formulate and implement effective and efficient strategies.

The remainder of this paper is organized as follows. Section “Review of Literature and Development of Hypotheses”reviews the literature and the formulated hypotheses, while section “Research Methodology” presents the sample as well as the research methodology. Section “Presentation of Findings” presents the results, while section “Presentation of Findings” analyzes and discusses the findings. Finally, section “Analysis of Findings” includes the conclusion, limitations, and research implications.

Review of Literature and Development of Hypotheses

Theoretical Background

Schwartz and Menon (1985) argued that an auditor change is a multi-factor issue that cannot be limited to one theory. In fact, auditor change decisions can be explained by four different theories: the agency theory, the signaling theory, the opinion shopping theory, and the assurance theory. First, according to the agency theory (Jensen & Meckling, 1976), also known as the contracting theory, there is an information asymmetry between shareholders (owners) and managers(agents) (Watts & Zimmerman, 1983) and between shareholders and debtholders which can create moral hazard problem. Therefore, auditing is considered as a monitoring tool needed to increase the objectivity and reliability of financial statements, reducing the misreporting of information, and thus, diminishing the agency costs (Jensen & Meckling, 1976). Farooq and Tabine (2015) found that the presence of high agency problems is positively related to the choice of a big N auditor. Moreover, company’s characteristics such as low dividend payout ratio, a high ownership concentration and a high complexity intensify the principle-agent conflict and thus alarm the need for a high-quality auditor to mitigate the problem. Given that this theory restricts the factors that could explain the auditor choice (Corten et al., 2018), complementary theories are needed. Second, the signaling theory explains how companies choose their auditors to convey the quality of their financial statements(Chaney et al., 2004). The signaling theory expects that companies decide to switch to a brand name auditor to send a signal about an optimistic future vision to its shareholders. Choosing high quality auditors, mainly big audit firms, shows that the managers are working for the shareholders’ best interest, and that they are mitigating all signs of the agency problem (Houghton & Jubb, 2003). Third, the opinion shopping theory provides the most common explanation of an auditor change, especially when initiated by the client. When the company is struggling financially, it searches for a new auditor to avoid receiving unfavorable audit reports from its current auditor. By hiring a new auditor, the company tries to stop the bad information from reaching the public and tries to cover its bad financial situation (Chow & Rice, 1982). Companies are more likely to seek a lower quality auditor to reduce the quality of published financial statements and increase the information asymmetries between managers and shareholders. Thus, they have mainly big N firms as predecessors and non-big N as successors, which can be explained by the fact that big N are reluctant to take risky clients (Turner et al., 2005) and unwilling to manipulate the financial reports (Guedhami et al., 2014). Fourth, the assurance theory assumes that companies, that have previously issued unreliable financial reports, change their auditors in order to strengthen back their position. They choose to switch to a new high-quality auditor that is able to issue more professional financial reports and offers good understanding of the available information, which ultimately improves their performance (Teh et al., 2016). Indeed, these theories are used to develop this study’s research framework.

Empirical Studies

Empirically, several studies have tacked the internal and external determinants of auditor change and auditor choice decisions, but mixed results were obtained. While some studies investigated the role of auditor related factors such as qualified audit opinion, audit delay and audit fee (Qomari & Suryandari, 2020), other studies focused on the client related factors (Hsu et al., 2015). Lennox (1999) found a relationship between financial distress and auditor switch. Struggling companies are more likely to replace their audit firms as compared to their counterparts, and they tend to hire a higher quality auditor over local ones (Fan & Wong, 2005). Grothe and Weirich (2007) found that large firms with overseas presence tend to choose big auditors firms which are known for their international exposure and their affiliation with foreign audit firms. Ismail et al. (2008) suggest that leverage, growth turnover, and financing activities determine the decision to change auditor in Malaysian companies, in addition to longevity of audit engagement and audit fee. Within the same context, Mustapha Nazri et al. (2012) investigated the factors influencing auditor change decisions of Malaysian companies and found that such decisions are significantly affected by the client’s characteristics rather than by some audit characteristics, notably changes in management, size, complexity, and growth. Moreover, Hsu et al. (2015) and Gerakos and Syverson (2015) explained the importance of company’s characteristics and industries in influencing auditor choice. More specifically, company’s financial situation, size, investment risk, growth, assets, and foreign sales are reported to affect the company’s auditor choice. In Indonesia, Augustyvena and Wilopo (2017) investigated the impact of management changes, audit opinion and financial distress on the decision to change auditor for manufacturing companies; and none of these variables is found to have a significant impact. In Indonesia too, Alisa et al. (2019) found that the size of the firm and the management size have a positive impact, whereas financial distress has no significant impact on auditor change decisions.

Moreover, client risk and asset growth are found to be associated with the choice of the auditor (DeFond et al., 1999; Firth & Liau-Tan, 1998; Johnson & Lys, 1990), while the impact of sales growth and leverage had been inconsistent (Chaney et al., 2004; DeFond et al., 1999; Francis & Wilson, 1988; Johnson & Lys, 1990). More recently, Darmayanti et al. (2021) revealed that financial difficulties are found to have a negative impact on the auditor change decision, while management changes ended up with a positive impact.

Lin and Liu (2010) examined the role of corporate governance in China and their results indicate that firms with weaker internal governance tends to switch to smaller auditors. However, few are the studies that focused on the role of corporate governance characteristics on auditor change decisions.

Concerning audit quality DeAngelo (1981), posit that larger audit firms are known for their professionalism and for the quality of services they offer. Indeed, they have much to lose if they tend to lower the quality of the auditing services offered (Houghton & Jubb, 2003). They are distinguished by their ability to deal with the agency problem with high professionalism. Beisland et al. (2015) posit that hiring a big N auditor is highly associated with audit quality signs, and Alfraih (2017) argued that the auditor’s type is a measure of audit quality. Grothe and Weirich (2007) found that small audit firms do accounting restatements at a rate of 13% while the big audit firms do it at a rate of 6% only.

This study, thus, focuses on the two factors, which influence auditor change decisions, namely clients’ characteristics and corporate governance characteristics, for U.K. listed companies.

Development of Hypotheses

Based on previous empirical evidence and related theories, the sign of the relationship between each variable and the auditor change decision is formulated and summarized below.

Firm’s Characteristics

Size

The most important factor affecting the auditor change decision, is the client’s size(Abidin et al., 2016; Hudaib & Cooke, 2005). Knechel et al.(2008) stated that the choice of one of the big N auditors is highly related to the size of the company, its need for equity issuance and loan acquisitions as well as the size of its labor force. Being largely scrutinized by the media channels and the financial regulators, big companies are discouraged to change their auditors as they fear the public criticism (Carcello et al., 2002). Many findings have revealed that large companies do not change their auditors as frequently as small ones(Francis & Wilson, 1988; Krishnan, 1994). On the other side, as companies grow in size, they will have more complex structures and the number of agency relationships will increase. Given the resulting increase in agency costs, the company might need to search for a better audit quality provider (Mustapha Nazri et al., 2012). Empirically, many scholars have reported a positive association between the company’s size and the auditor change decision (Johnson & Lys, 1990; Mustapha Nazri et al., 2012). Sankaraguruswamy and Whisenant (2004) and Woo and Koh (2001) found that the bigger the size of the company is, the more severe the agency problem becomes and, the higher is the need for a more independent auditor. Furthermore, Watts and Zimmerman (1983) reported that bigger companies experience a higher risk of manager-shareholder misalignment, and therefore they need a highly independent auditor to attenuate the agency problem.

Furthermore, size is found to play a role in the choice of an auditor. The bigger the company is, the more it tends to choose a big N auditor (Davidson et al., 2006; Hogan & Martin, 2009). Knechel et al. (2008) reported that companies switching from big N to another big N auditor tend to be bigger than those engaging in other auditor change types, and Lin and Liu (2010) found that the bigger the companies are, the lower is the probability to switch to a small auditor. On the other hand, Chang et al. (2010) found that small companies tend to switch to a small audit firm.

H1.1: There is a positive relationship between firm’s size and the auditor change decision.

H1.2: There is a positive relationship between firm’s size and the choice of a big 4 auditor.

Growth

Researchers have associated the auditor change to the companies’ growth process(Abidin et al., 2016). Growing companies suffer from difficult control mechanism and thus require the expertise of a highly qualified auditor (DeAngelo, 1981; Johnson & Lys, 1990). Several studies argued that as companies grow, they tend to change from non-big N to big N audit firms (DeAngelo, 1981; Johnson & Lys, 1990). Similarly, Chang et al. (2010), Lin and Liu (2010), and Woo and Koh (2001) found that growing companies are more likely to switch to a brand name auditor to benefit from the positive quality and the good reputation echoes resulting from hiring brand names. On the other hand, Chang et al. (2010) reported that low-growth companies tend to switch to small auditors. Contrary to all the previous findings, Williams (1988) did not find any significant relation between the auditor change and the company’s growth.

H2.1: There is a positive relationship between the firm’s growth and the auditor change decision.

H2.2: There is a positive relationship between the firm’s growth and the choice of a big 4 auditor.

Leverage

The auditor choice is highly dependent on the financing needs and the leverage level (Knechel et al., 2008; Lin & Liu, 2010). Companies planning to get external financing know that lenders grant high priority to the auditor’s competence, as clean, transparent and credible financial reports are needed. Therefore, to meet the creditor’s requirements, moving up in the auditors’ quality scale is needed (Knechel et al., 2008).

Studies have highlighted the association between companies’ leverage and auditor change, however inconsistent results were reported. Chang et al. (2010) found that the lower the companies’ need for financing is, the higher is their tendency to choose a small auditor. Furthermore, Knechel et al. (2008) found that the higher the debt ratio is, the more is the tendency to hire a high-quality auditor. However, Wang and Xin (2011) results have contradicted the previous findings as they revealed that big companies with low leverage ratio tend to choose big N auditors. In this study, a positive relationship is expected.

H3.1: There is a positive relationship between the firm leverage and the auditor change decision.

H3.2: There is a positive relationship between the firm leverage and the choice of a big 4 auditor.

Profitability and Loss

Based on the opinion shopping theory and the assurance one, companies’ profitability is found to be a driver for auditor change decisions. Knechel et al. (2008) suggested that firms have incentive to hire a low-quality auditor to hide their true profitability. DeFond et al. (1999) stated that companies that were unprofitable in the past have incentive to choose a small auditor, while highly profitable firms change to a big auditor to expose their good financial position to the public. Furthermore, profitable companies might tend to choose large auditors just because they can afford the high audit fees. C.-S. Chen (2016) found that unprofitable companies tend to manipulate their earnings, by choosing non-big N auditors to hide their losses. Within the same context, Chang et al. (2010) found that low profitable firms are more likely to switch to a small auditor. Furthermore, Berger and Hann (2007) reported that unprofitable companies usually avoid declaring their true financial figures, especially to shareholders and creditors, and therefore search for a low-quality auditor to help them in the concealing process. Thus, financial distress plays an important role in the decision of auditor switching. Firms with lower profitability or ones with losses incurred are more likely to change their auditor, but less likely to choose a big 4 one.

H4.1: There is a negative/positive relationship between the firm’s positive/negative earnings and the auditor change decision.

H4.2: There is a positive/negative relationship between the firm’s positive/negative earnings and the choice of a big 4 auditor.

Performance

Studies tackling the association between companies’ performance and the auditor change decisions have supported both the assurance theory and the opinion shopping one. Companies with financial problems tend to choose an independent, high-quality auditor to help them re-establish their position (assurance theory; Francis & Wilson, 1988). However, some scholars argued that struggling companies tend to change their auditors to cover their actual bad situation (opinion shopping theory) (Chow & Rice, 1982; Fried & Schiff, 1981). Wang and Xin (2011) have used the operating cash flow (OCF) as a measure of the firm’s performance and stated that companies having low OCF are more likely to change their auditors. Furthermore, (Hogan & Martin, 2009) found that companies that have financial problems are more likely to switch from big N to non-big N auditors.

H5.1: There is a negative relationship between the firm performance and the auditor change decision.

H5.2: There is a positive relationship between the firm performance and the choice of a big 4 auditor.

Corporate Governance Variables

Board Diligence

Board diligence refers to the frequency of the board meetings and the board members’ behavior. Board members who meet frequently tend to be more responsible and committed. They show an effective control process and a high need for transparency and compliance with the best reporting standards (Kuang, 2011). Many research findings have supported this argument and found that the higher the board meetings frequency, the more the auditor change will occur (Kuang, 2011; Vafeas, 1999). Abbott and Parker (2000) found that boards with more than one annual meeting tend to choose a high-quality specialist auditor. Furthermore, Quick et al. (2018) found that the higher the number of board meetings, the lower is the company’s tendency to choose a big N auditor.

H6.1: There is a positive relationship between the number of board meetings and the auditor change decision.

Board Size

The board size is found to be an important corporate governance factor for auditor change decisions. Boards that include many members contain varied leadership styles that enrich the company’s vision and encourage diversified participation in the decision-making process. Board size is highly associated with the auditors’ selection. Many studies revealed that the larger the board is, the higher is the tendency to choose a high-quality auditor (Alfraih, 2017; Ianniello et al., 2015; Quick et al., 2018). K. Y. Chen and Zhou (2007) found that the number of members on board, irrespective if they are outsiders or insiders, is by itself a determinant of auditor change decisions. However, Beisland et al. (2015) and Lin and Liu (2010) failed to find any relation between the board size and the auditor choice in the profit and non-profit micro finance institution.

H7.1: There is a positive relationship between the board size and the auditor change decision.

Board Gender Diversity

Gender Diversity has been lately under the spotlight. Indeed, female managers in controlling positions are found to be more independent than their male counterparts, while showing a lower absenteeism rate during meetings. Their participation on board adds objectivity and reliability in the decision-making process (Adams & Ferreira, 2009). Many scholars have reported that the gender diverse board encourages the selection of a big N auditor (Adams & Ferreira, 2009; Alfraih, 2017; Lai et al., 2017), since women are more demanding, ethical and professional than men. However, Quick et al. (2018) failed to report any significant relationship between the female presence on board and the auditor’s choice decision.

H8.1: There is a positive relationship between the board gender diversity and the auditor change decision.

Board Independence

The board can be composed of either independent outside directors or insider managers. It is generally believed that outsiders can serve this position more efficiently as they protect the shareholders’ rights and detect any managerial misconduct. The more independent members are serving on board, the more efficient is the monitoring process over the management team (Fama & Jensen, 1983). Abidin et al. (2016) found that the more the board includes independent members, the more the company is likely to change its auditor. Carcello et al. (2002) stated that independent directors search for a high-quality auditor to avoid litigation problems and protect shareholders’ wealth. They can effectively monitor the managers’ performance and reduce the agency problem. One way to do it is to choose a high-quality auditor (Beasley & Petroni, 2001). Leung and Cheng (2014) found that the number of independent members on board is positively associated with the choice of an auditor. Independent board members exert more efforts in the governance mechanism and the monitoring process and consequently tend to choose big N auditors. Beasley and Petroni (2001) found that the higher the board independence is, the higher is the tendency to search for brand names in the audit industry. However, Aljabr (2010) and Bradbury et al. (2006) failed to report any significant relation between the board independence and the selection of the auditor.

H9.1: There is a positive relationship between the board independence and the auditor change decision.

CEO-Chairman Separation

The association between the CEO-chairman duality is dependent on the type of the potential agency problem within the firm. If the potential problem exists between the management and the controlling shareholders, then the duality will attenuate the problem. If the potential disagreement lies between the controlling shareholders and the minority shareholders, the duality will make the problem more severe, and the CEO/chairman will take the role of the advocate of the controlling shareholders. In that case, the controlling shareholders might tend to choose a low-quality auditor who supports their personal interests (Waresul Karim et al., 2013). As the CEO-chairman duality hinders the independence of the board, the separation of the two roles is expected to be positively associated with the auditor change (Tonello, 2011). Many researchers have found that the presence of CEO-chairman duality is positively associated with the switch to a small auditor (Alfraih, 2017; Beisland et al., 2015; Ianniello et al., 2015; Lin & Liu, 2010). However, Abidin et al. (2016) did not find any significant relationship between the CEO-chairman duality and the auditor change.

H10.1: There is a positive relationship between the CEO-Chairman separation and the auditor change decision.

Audit Committee Independence

The audit committee is the body responsible for appointing external auditors and deciding on their compensations (Lamm et al., 2018). It is also responsible for the financial reporting control, the ethical compliance checks and the communication with outside stakeholders (Lamm et al., 2018). Therefore, this body is closely engaged in the auditor change decision. Brandt and Li (2003) argued that when all audit committee members are independent, the possibility of engaging in earnings management decreases. Independent members are very cautious about their image and the financial burden associated with litigations and regulatory sanctions, which pushes them to search for high quality auditors (Abbott & Parker, 2000).

H11.1: There is a positive relationship between the audit committee independence and the auditor change decision.

Board Member Compensation

Two viewpoints can be offered to find a possible relation between the compensation and the auditor change. First, board members who receive high compensation believe that they must repay to shareholders with more efforts, greater transparency, and better control. Therefore, high compensations can be positively linked to more effective internal monitoring system (Dah & Frye, 2017). In the light of this argument, companies with highly compensated members might choose a high-quality auditor to keep shareholders assured and protected and hence, keep receiving their benefits in return. Second, it is found that high compensations make the agency problem more severe (Dah & Frye, 2017). Core et al. (1999) found that companies with principle-agent problems report high compensation levels. Based on this finding, companies might tend to search for brand name auditors when their directors are highly compensated to solve the principle-agent problem. Furthermore, a negative relation is reported between the compensation levels and the company’s future performance (Brick et al., 2006; Core et al., 1999). Nevertheless, Cheng and Warfield (2005) found that high board members compensation is associated with earnings manipulations. Earnings are overstated especially in companies where compensations are performance-based, in order to push compensation high. While not all auditors accept such practices, and most of the board members desire high compensations, a disagreement between the two parties can occur in case of low compensation. According to the opinion shopping theory, the auditor change occurs when there is a disagreement between the two parties (Fried & Schiff, 1981).

H12.1: There is a positive relationship between the board members’ compensation and the auditor change decision.

Board Members’ Industry Specific Skills and Financial Background

The most important competence that every board member should have is the industry knowledge. Knowing the industry rules, being aware of the regulatory system, and having a clear understanding of all the market’s risks and opportunities, help in anticipating many problems and consequently many possible solutions. Board members’ industry expertise is positively associated with the firm’s value, its innovation levels, R&D investments and acquired patents. Moving upward in the innovation scales requires an upward shift in the audit services provided (Small, 2012). Because innovation needs a more effective monitoring system due to the high-risk levels that are involved, the presence of these board skills can be associated with auditor change, and more specifically with a switch to high audit quality providers. Thus, a positive relation between the board members’ skills (industry and financial) and the auditor change decision is expected.

H13.1: There is a positive relationship between the board members’ skills and the auditor change decision.

Board Structure Type

The board structure can be a single-tier (unitary) or a two-tier (dual). The two-tier board structure is where there are two boards: the management board that copes with daily operations and the supervisory board that controls all the activities and is in charge of the managers’ appointments (Belot et al., 2014). Thus, the two-tier structure is a fertile soil for agency problems and therefore, a positive relation might exist between the two-tier board structure and the auditor change decision. The single-tier board structure allows an easier flow of information which helps mitigate the information asymmetry and the delay caused by bureaucratic processes (Jungmann, 2006). No previous literature has reported a clear relation between the board structure type and the auditor change decision. However, some findings have led to a potential association between the two variables. In the dual structure, the two boards meet rarely which enlarges the information asymmetry and creates distance between the members. Nevertheless, unifying the two boards’ role in one single unit might annul the supervisory role of the board, which risks its independence (Jungmann, 2006).

H14.1: There is a positive relationship between a two-tier structure and the auditor change decision.

Research Methodology

Sample

In this study, secondary data is used to answer our two research questions. The sample consists of all the 250 UK companies that are part of the FTSE 250 index (representing approximately 15% of UK market capitalization). From these companies, 155 companies had changed their auditor based on the Financial Times News website, while 95 companies had no auditor change from March 2013 till February 2018. Out of these 155 companies, 11 were reappointment cases. Moreover, 14 companies had missing data, resulting in a final sample of 225 companies which included 130 auditor-changed companies and 95 non-auditor changed companies (See Table 1).

All variables are collected from DataStream.

Sample Selection.

The full sample of 225 companies is used to answer the first research question (factors explaining the decision to change auditors), whereas only the auditor changed companies (N = 130) are included for the second research question (factors explaining the switch to a big 4 auditor). In the latter, these 130 UK companies that have engaged in an auditor change are divided into two categories, according to the type of their successor auditor (to a big 4 auditor versus to a non-big 4 auditor).

Variables Definition

Dependent Variables

To answer the first research question, the dependent variable is auditor change (CHNG), a dichotomous variable that is equal to 1 when there is an auditor change, or 0 otherwise. In order to answer the second research question, the dependent variable is changing to a big four (CHNGBIG), which is a dichotomous variable that is equal to 1 when the successor auditor is a big N and 0 otherwise.

Independent Variables

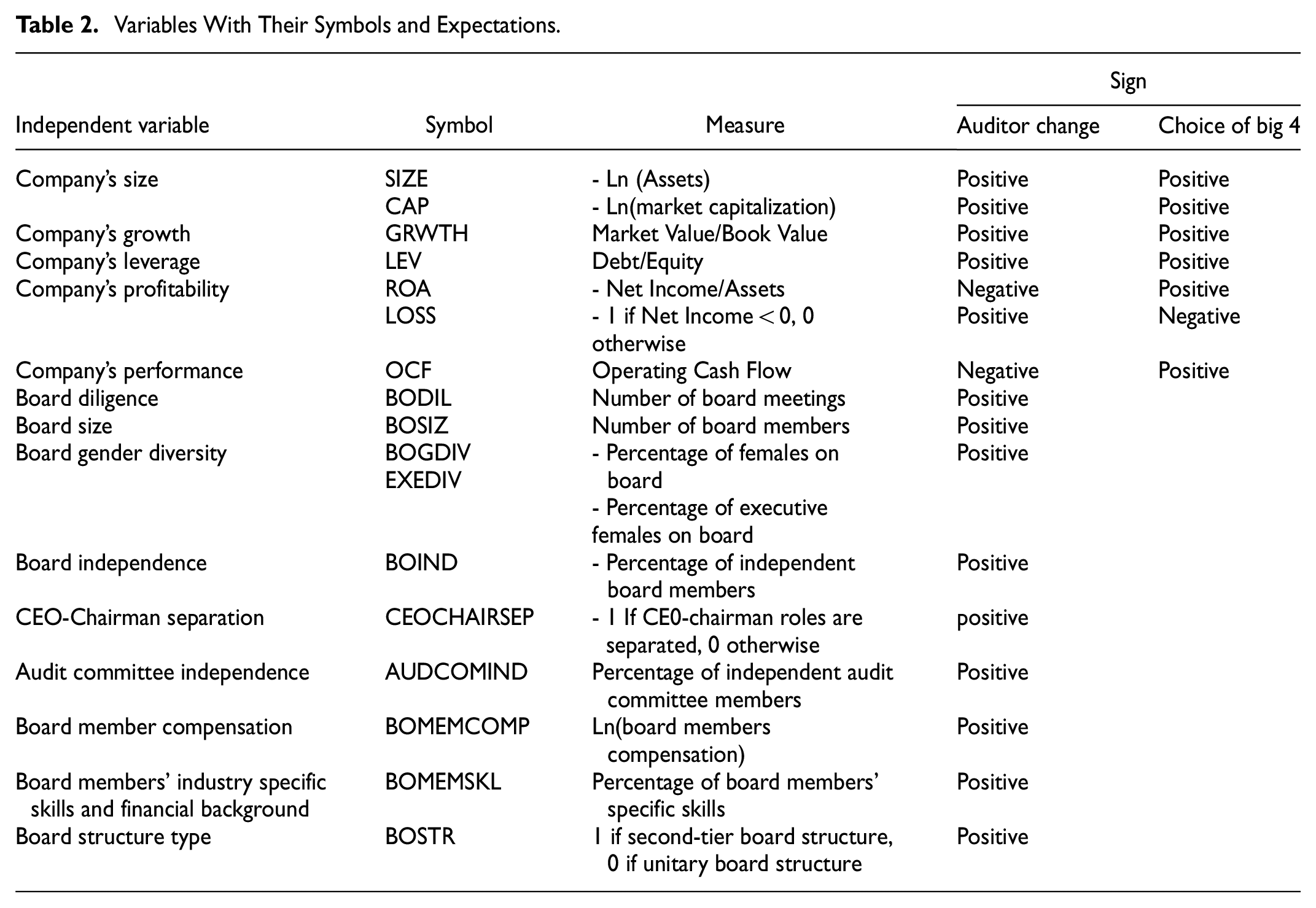

Independent variables are divided into two categories, namely the firm’s characteristics and the corporate governance ones, as follows. All variables, with their symbols and expected signs, are presented in Table 2. All variables are collected one year prior to the change.

Variables With Their Symbols and Expectations.

Firm’s Characteristics

The five firm’s characteristics variables included in this paper are as follows:

- Size (SIZE): It is measured by log total assets and log market capitalization (Chang et al., 2010). The larger the size, the more likely an auditor change will occur, and the more likely the choice goes to a big N auditor.

- Growth (GRWTH): It is measured by the market to book value (Chung & Kallapur, 2003; Lin & Liu, 2010; Wang & Xin, 2011). The higher the growth of the company is, the more likely an auditor change will occur, and the more likely a firm will choose a big N auditor.

- Leverage (LEV): The company’s leverage is measured by the debt-to-equity ratio (Darmayanti, 2017). The higher the financial leverage is, the more likely an auditor change will occur and the more likely a firm chooses a big N auditor.

- Return on Assets (ROA): It is defined as net income divided by total assets (Chang et al., 2010; Knechel et al., 2008) and it is used to capture profitability.

- Loss (LOSS): LOSS is a dummy variable equals to 1 if net income is less than zero, 0 otherwise (Chang et al., 2010; Lin & Liu, 2010; Wang & Xin, 2011).

- Performance (OCF): It is measured by operating cash flow. The lower the performance is, the more likely the auditor change will occur, and the less likely a firm chooses a big 4 auditor.

Corporate Governance Variables

This paper investigates the impact of nine corporate governance variables on the decision to change auditor.

- Board diligence (BODIL): it is measured by the number of board meeting(Kuang, 2011).

- Board size (BOSIZ): it is measured by the number of board’s members (K. Y. Chen & Zhou, 2007).

- Board gender diversity: it is measured by the percentage of females on board (BOGDIV) and more precisely among executive board members (EXEDIV).

- Board independence (BOIND): it is measured by the percentage of the independent members on board

- CEO-chairman separation (CEOCHAIRSEP): it is dichotomous that is equal to 1 when there is a separation, and 0 otherwise.

- Audit committee independence (AUDCOMIND): it is measured by the percentage of the independent audit committee members.

- Board member compensation (BOMEMCOMP): it is measured by the log total compensation of the board members (in US dollars).

- Board members’ industry specific skills and financial background (BOMEMSKL): it is measured by the percentage of the board members having industry-related skills or financial ones.

- Board structure type (BOSTR): it is measured as a binary variable that is equal to 1 in case of a two-tier structured board, and 0 otherwise.

Choice of Models

After testing Multicollinearity using Variance Inflation Factor (VIF), a “model fitting process” is adopted to come up with the best model by adding and dropping variables from one preliminary model. First, the model specification is tested by regressing the dependent variable on the prediction (hat) and the prediction squared (hatsq; Williams, 2018). The model that fails the specification test (significant “hatsq”) is automatically dropped out. The model that passes the specification test (insignificant “hatsq”) is subject to further post-estimation tests, mainly a goodness-of-fit, a classification test, and Receiver Operating Characteristic (ROC) area before using the results to make any statistical inference. First, goodness-of-fitness is measured using the Hosmer and Lemeshow’s chi-square, the AIC and the BIC (Williams, 2018). Second, the classification test shows the percentage of the predicted data that was correctly classified by looking to its specificity and sensitivity percentages. Sensitivity is the proportion of the observations that has been classified as ‘an event’ (auditor change in this case) and which has been in reality “an event.” Specificity is the proportion of observations that has been classified as “non-event” (no auditor change) and which is actually “non-event” (Reichenheim, 2002). Third, the ROC area is used. For a model to sufficiently fit well, it should have high p-value for Hosmer and Lemeshow’s chi-square test, low BIC and AIC and a high classification percentage and a high ROC (Williams, 2018).

Model Equation

To answer research question 1, Model 1 includes only firms’ characteristics variables and Model 2 includes firms’ characteristics and as well as corporate governance ones. After running several attempts, the final fitted models are:

Where: CHNG is the dichotomous independent variable equals 1 when there is an auditor change, 0 otherwise. Independent variables are previously defined in Table 2. The industry dummies included are 10 categories based on the SIC classification code.

In order to answer research question 2, due to data unavailability, only the firm’s characteristics’ effect are tested, and the best fit model is as follows:

The dependent variable ‘CHNGBIG’ is a dichotomous variable equals 1 when the successor auditor is a big N and 0 otherwise.

Presentation of Findings

Changing Auditor Versus Non-changing Auditor

Descriptive Statistics

Table 3 displays the mean of each variable, grouped by companies’ cases: those changing their auditor versus those that did not change their auditor. The final column reports the t-test which is conducted to check whether the average difference is statistically significant.

Univariate Analysis: Changing Auditor Versus Non-changing Auditor Companies.

, **, *Denote significance at 1%, 5%, and 10% respectively.

Two variables under the firms’ characteristics are found to be significant. Companies that changed their auditors are found to be smaller in size (lower log assets), which might suggest that big companies are less likely to change their auditors as compared to small ones. Carcello et al. (2002) stated that big companies are under the media spotlight, are always scrutinized by the financial analysts and face public judgments after any strategic decisions. This public exposure discourages them from changing their auditors. Moreover, the difference in the debt equity ratio is found significant at 10%, revealing that low leveraged firms are more likely to change their auditors compared to high leveraged ones. This relationship is supported by Abid et al. (2018) who revealed that the company’s leverage is negatively associated with the issuance of an unqualified audit opinion.

Two corporate governance variables are also found to be statistically significant. Companies with more independent audit committee members tend to change their auditors more than their counterparts (statistically significant difference at 5%). Second, the board member compensation is found to be significant at 10%, showing that companies granting low compensations to their board members tend to change their auditors more frequently than companies granting high compensations. This finding might suggest that in case the management is not satisfied with the low compensations received, a conflict occurs resulting in a change of auditor, in an attempt to higher their pay (Fried & Schiff, 1981).

With respect to the binomial variables, they are generally described by looking at the frequency tables rather than the means (Table 4). LOSS is found to be significantly different (at a 1% significance level) between the two categories of companies. More specifically, 10.53% of the companies that are not changing their auditors are found to be non-profitable (LOSS = 1), while 29.69% of the companies that are changing their auditors are found to be non-profitable companies (LOSS = 1), which might indicate that non-profitable firms are more likely to change their auditors. This reasoning is attributed to the opinion shopping theory which states that unprofitable firms tend to change their auditors in order to hide their true financial situation (Fried & Schiff, 1981).

Frequency Distribution of Binomial Variables.

Denotes significance at 1%.

Regression

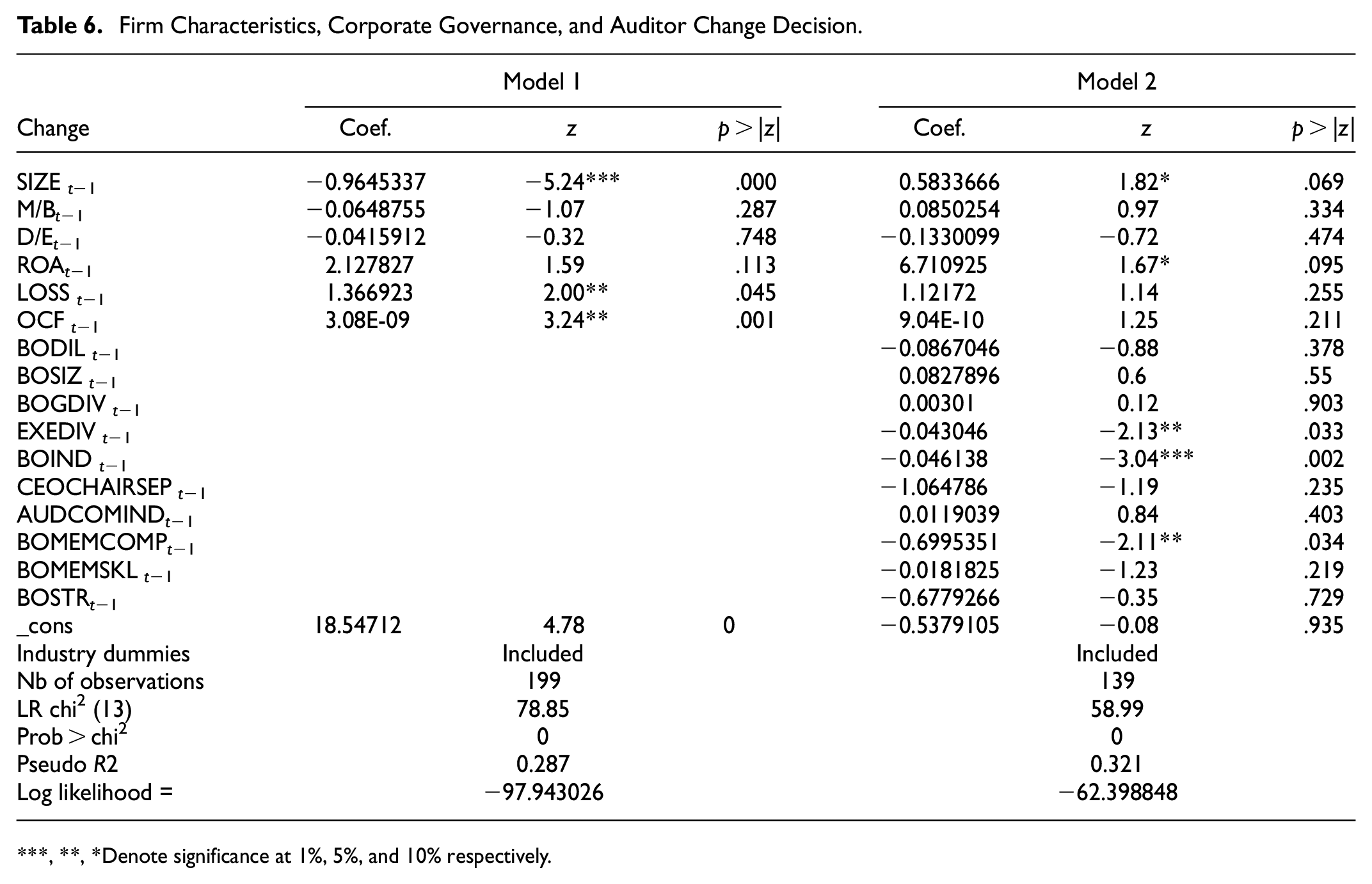

First, multicollinearity was tested using Variance Inflation Factor. The mean and the maximum VIF of all the variables are found to be 1.90 and 4.80 respectively (<10) suggesting the absence of a collinearity problem (Berry & Feldman, 1985). After seven attempts of adding and dropping variables and proxies, two models are found to be the best model. Model 1 addresses the relationship between the firm’s internal characteristics and the auditor change decision, while Model 2 addresses the impact of the firm’s internal characteristics and the corporate governance variables on the auditor change decision.

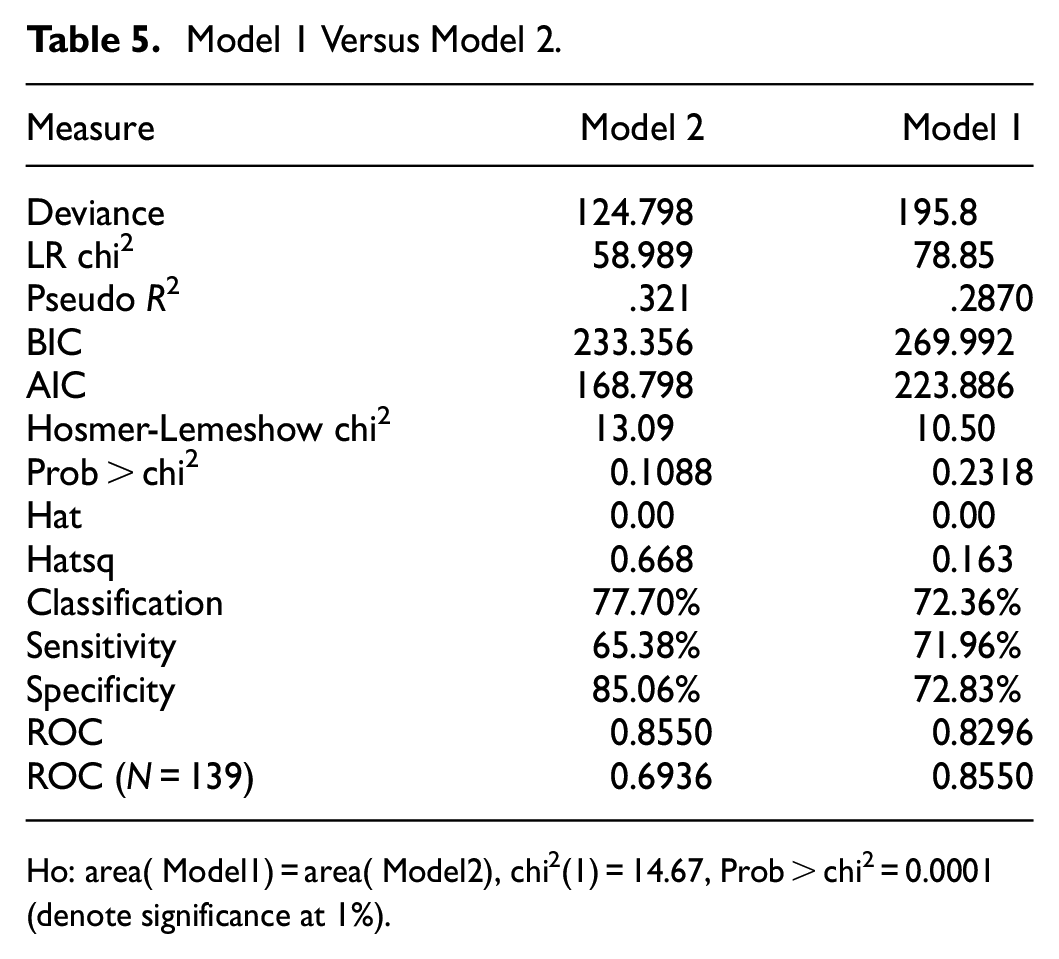

To determine whether adding the corporate governance factors can improve the model fit, model 1 and model 2 are compared as displayed in Table 5.

Model 1 Versus Model 2.

Ho: area( Model1) = area( Model2), chi2(1) = 14.67, Prob > chi2 = 0.0001 (denote significance at 1%).

The significance of the p-value in both models (Table 5) indicates a good model fit. Model 2 is better than Model 1 since it has a lower deviance, higher pseudo R2, higher Hosmer and Lemeshow’s chi-square, and lower BIC and AIC. The absolute value of the difference between the BIC’s of the two model is 36.634 which gives strong evidence to prefer model 2 over model 1(Williams, 2018). Additionally, the overall classification of Model 2 is 77.70%, higher than the overall classification percentage of Model 1 (72.36%). More specifically, 71.96% and 65.38% of companies that changed their auditors are correctly classified (sensitivity) in Models 1 and 2 respectively, while 72.83% and 85.06% of companies that did not change their auditors are correctly classified (specificity) in Models 1 and 2 respectively. Finally, the area under the ROC for Model 2 is 0.8550 as compared to 0.8296 for model 1. Since the ROC area measure cannot be used to compare two samples with different number of observations, the last column shows the ROC area after equalizing the number of observations in the two samples (139 observations). The ROC area of model 2 is 0.8550, higher than the ROC area of model 1, which is 0.6936. The chi-square test shows a significance probability of 0.0001, which indicates that Model 2 has a higher ROC than Model 1, a difference statistically significant at 1%. Consequently, all measures indicate that model 2 is better than model 1, only Model 2 will be analyzed.

With respect to the firm’s specific variables (Table 6), size and ROA are significant with a positive impact. Furthermore, executive board member diversity, board independence, and the log of the board members’ compensation are significant with a negative coefficient.

Firm Characteristics, Corporate Governance, and Auditor Change Decision.

, **, *Denote significance at 1%, 5%, and 10% respectively.

Choice of the Successor Auditor’s Type

Descriptive Statistics

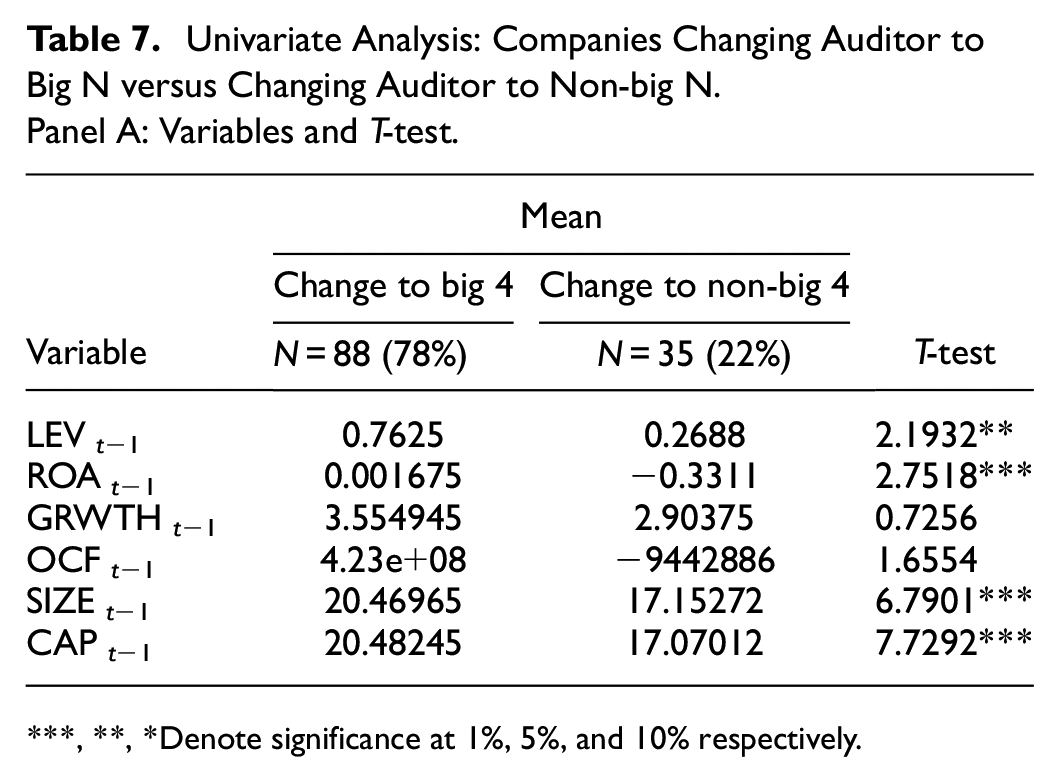

This part will uncover how the same firm’s characteristics affect the auditor’s choice (big 4 versus non-big 4). The sample, for this objective, comprises 130 UK companies that changed their auditors from March 2013 till February 2018. First, the sample is divided in two broad categories based on the successor auditor’s type (changing to a big 4 auditor [coded as 1] vs. changing to a non-big 4 auditor [coded as 0]). Second, the sample is divided into 4 categories based on both the predecessor auditor’s type and the successor auditor’s type (big to big (Type 1), non-big to non-big (Type 2), big to non-big (Type 3), and non-big to big (Type 4). While the difference in the mean is tested using the T-test in the first part (comparing two groups) (Table 7), it is tested using the F-test in the second part (comparing four groups) (Table 8).

Univariate Analysis: Companies Changing Auditor to Big N versus Changing Auditor to Non-big N.

Panel A: Variables and T-test.

, **, *Denote significance at 1%, 5%, and 10% respectively.

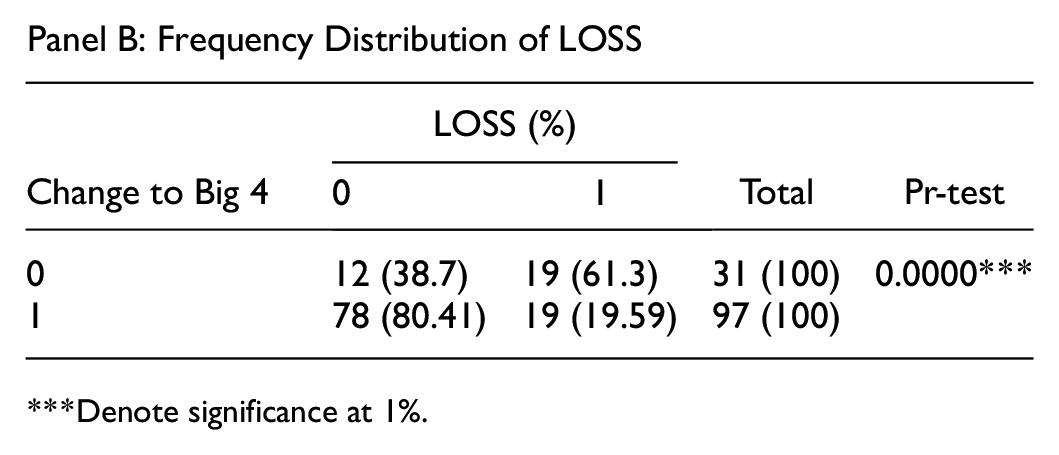

Panel B: Frequency Distribution of LOSS

Denote significance at 1%.

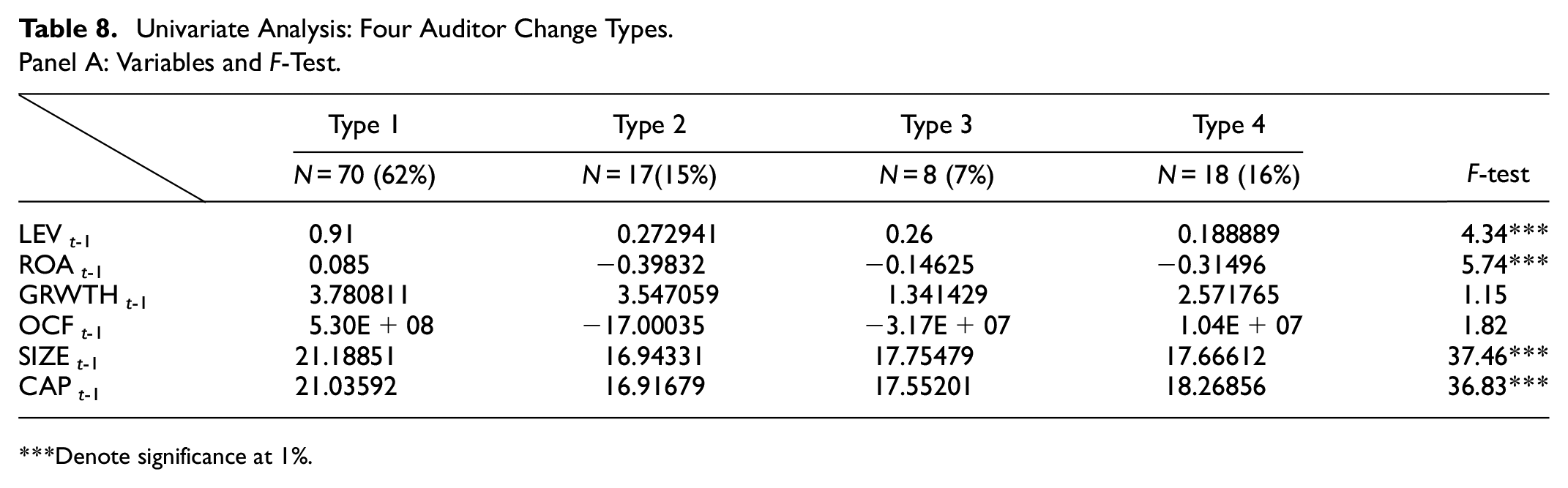

Univariate Analysis: Four Auditor Change Types.

Panel A: Variables and F-Test.

Denote significance at 1%.

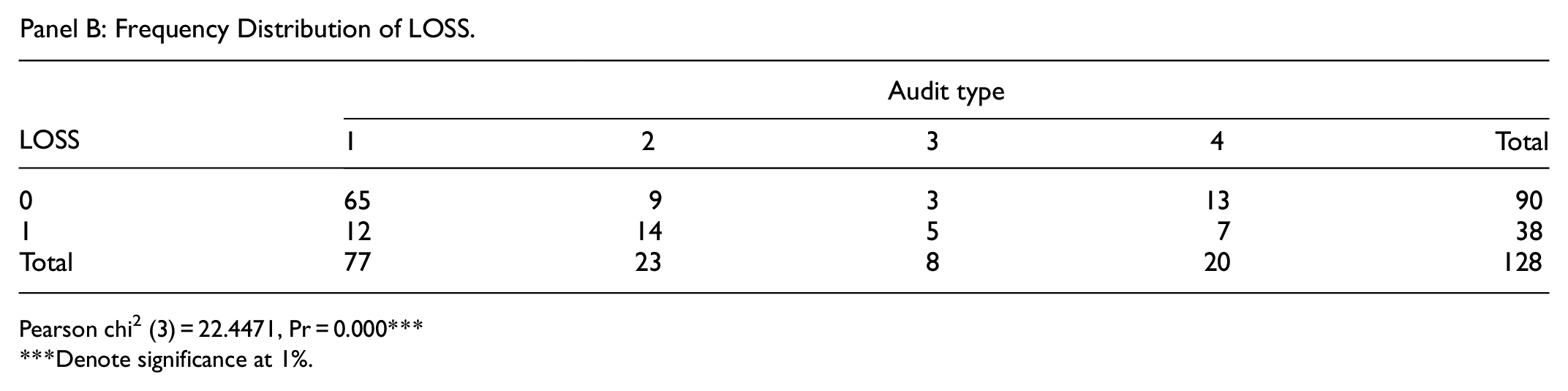

Panel B: Frequency Distribution of LOSS.

Pearson chi2 (3) = 22.4471, Pr = 0.000******Denote significance at 1%.

Table 7 shows that 78% of the companies under investigation are changing to big 4 showing the big 4 dominance in the U.K. market. Moreover, those companies have a higher financial leverage, are more profitable, have higher growth and more operating cash flow, and are bigger than those changing to non-big 4. Results of the t-test (last column; Panel A) show that four variables are significant (the ROA, SIZE, CAP, and Leverage), confirming previous studies. First, large companies are characterized by a complex structure where more empowerment and delegation of authority are required. Consequently, they search for big N auditors to re-establish their control system (Mustapha Nazri et al., 2012). Second, high leverage companies tend to choose a big N auditor (Knechel et al., 2008). Getting external financing is subject to strict financial requirements, which are easier to meet by hiring a big N auditing firm. Finally poorly performing firms hire a non-big N, considered a low-quality auditor, to hide their financial failure, an argument grounded in the opinion shopping theory (Chow & Rice, 1982). Panel B reports 80.41% of companies that are changing to big 4 have a positive net income (LOSS = 0). The significance of Pr-test indicates that loosing companies are more likely to choose a non-big N. The results confirm (DeFond et al., 1999) that profitable firms choose a big N auditor to better expose their profitability to the public; and back up the opinion shopping theory(Chow & Rice, 1982).

When the sample is divided based on both the predecessor auditor’s type and the successor auditor’s type, the results show that 62% of the auditor’s change are of type 1 (big 4 to big 4). The lowest percentage (7%) is for the type 3 while the percentages for type 2 and type 4 are 15% and 16% respectively.

Furthermore, the means of each variable for all the four types are tabulated in Table 8, Panel A. Results reveal that all the variables’ means are the highest for Type 1 auditor change. The F-test in the last column shows that the differences are significant for all the variables except for Growth and OCF. Companies switching from big 4 to big 4 seem to be the biggest, the most leveraged and the most profitable ones among all types of auditor changes.

Results in Table 8, Panel B show that the majority of type 1 and type 4 auditor changes (84.41% and 65% respectively) are companies with positive net income, while the majority of type 2 and type 3 auditor changes (60.86 % and 62.5% respectively) are losing companies. These differences in the frequencies are significant with a Pearson chi 2 p-value of 0.000. (DeFond et al., 1999) found that highly profitable firms tend to choose brand name auditors because they can easily meet the high expenses. The same argument is presented by Chan et al. (2011) who stated that low profitable firms choose non-big 4 auditors just to benefit from low audit costs.

Regression

The same sequence of tests presented before will be repeated with CHNGBIG as the dependent variable. After several attempts, the fitted model is as follows:

To control for the predecessor auditor’s type, a dummy variable (PREAUD) is added to the model (Model 4). This variable takes the value of 1 if the predecessor auditor was a non-big 4 and 0 otherwise.

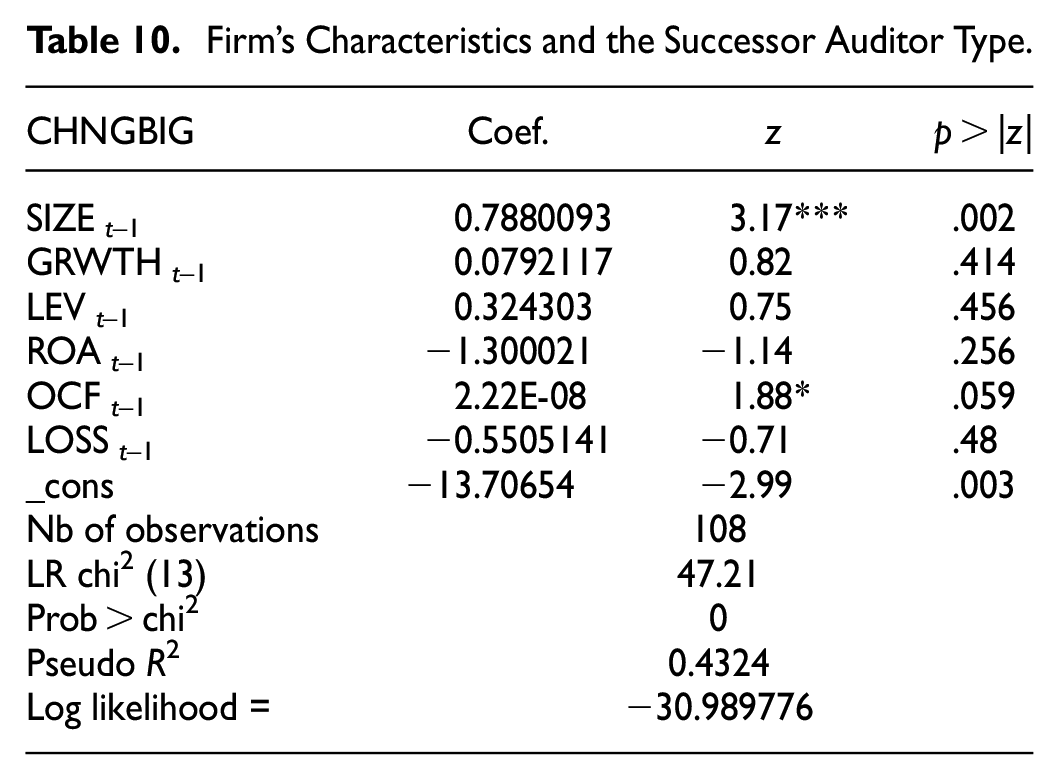

Table 9 compares model 3 and model 4. Results show that the majority of the reported statistical measures are very similar under both models. Since PREAUD is found to be insignificant, Model 3 is chosen to the best model which will be analyzed. The insignificance of the p-value and the low value of both the AIC and the BIC of Model 3 indicate a good model fit. Furthermore, it is able to correctly classify 84.26% of the overall observations, with a sensitivity of 93.02%, and a specificity of 50%. The area under the ROC curve is 0.9186. Results in Table 10 show that only two variables are significant with a positive sign, mainly SIZE (significant at 1%) and OCF (significant at 10%).

Model 3 Versus Model 4.

Firm’s Characteristics and the Successor Auditor Type.

Analysis of Findings

Firm’s Characteristics

Size explains the company’s decision to change its auditor in general (Hypothesis 1.1), and to a big 4 auditor (Hypothesis 1.2), supporting previous studies (Abidin et al., 2016; Hudaib & Cooke, 2005). As companies get bigger, the agency problems might get more severe, pushing firms to change their auditors to mitigate these problems. Similarly, Mustapha Nazri et al. (2012) stated that big firms try to search for a high-quality auditor to remedy this problem. This finding is confirmed in our results in the third model that controls for the successor auditor’s type. As for ROA, highly profitable firms tend to change their auditors, contradicting our expectations. When it comes to LOSS, our findings supported (Wang & Xin, 2011) who failed to report any relation between the two variables. LOSS has been associated with auditor changes in almost all the studies reviewed, some have extended their research and found that the successor auditor is a non-big 4 (Chang et al., 2010) and others found it to be a big 4 (Francis & Wilson, 1988). However, this reasoning is not applicable here, as LOSS has not been found significant in model 3, rejecting Hypothesis 4.1. Finally, the operating cash flow is found to be positively significant in Model 3, accepting Hypothesis 5.1, but the coefficient is very small which reflects a very minimal effect.

Corporate Governance

When the corporate governance variables are tested in Model 2, only three variables are found significant, with signs against our expectations. First, board diversity was measured by two proxies: the board members diversity and the executive board members diversity. While the BOGDIV was found to be insignificant, the EXEDIV showed a significant result but with a negative sign (Hypothesis 8.1). (Quick et al., 2018) failed to report a significant relationship between the board diversity and the audit change decision, which could have been compliant to our results if the BOGDIV alone was used as a proxy of board diversity. However, the executive board members play a crucial role in mirroring the situation to the uninformed non-executives before they take any strategic action, as the formers are always aware of the company’s day-to-day operation. In addition, almost all the literature reviewed reported that women are more efficient in their decision making, and tend to be cautious about the professionalism of the auditors, their accuracy in the financial reporting, and their ethical compliance (Adams & Ferreira, 2009). For this reason, gender diverse boards were found to be more likely to choose a big N auditor (Adams & Ferreira, 2009; Alfraih, 2017; Lai et al., 2017). In this research, a negative relation has resulted, indicating that boards that lack the female presence tend to change more frequently their auditors. When such decision is taken by non-diverse boards, it can be justified by the opinion shopping theory. Therefore, we can assume that non-diverse boards switch their auditors to cover their weaknesses and bad performance. This finding could have been more affirmed if we were able to detect a negative relation between this variable and the decision to choose a big 4 auditor. However, the corporate governance factors effect on the choice of the successor auditor was not tested due to data unavailability.

The significance of the board independence (Hypothesis 9.1) in this study contradicts Aljabr, (2010) and Bradbury et al. (2006) who found no significant relation between the auditor choice and board independence. Furthermore, in contrast to (Abidin et al., 2016) who reported a positive relationship between auditor change and board independence, our findings revealed that the auditor change decision and the board independence are negatively related. As it was previously mentioned, the management team is responsible for prevailing company’s financial situations whether it is a failure or a success. The non-independent board members are influenced by the management desires; therefore, their decision to change the auditor has to attract the managers. This evidence might recall the opinion shopping theory that illustrates the auditor change as a mean to cover the management inappropriate actions by searching for an auditor who can help them with the concealing process.

Although no previous studies have tackled the relation between the board members compensation and the auditor change, our findings revealed a negative relationship (Hypothesis 12.1). According to Cheng and Warfield (2005), high compensations are associated with earnings manipulation practices. While all board members desire to be highly paid, not all auditors accept to engage in such wrongdoing. Thus, a conflict occurs between the board members and the auditors when low compensations are granted. The resulting disagreement might push the firm to change its auditor, as supported by the opinion shopping theory (Fried & Schiff, 1981). Furthermore, setting the level of board compensations is in the hand of the audit committee who works in collaboration with the external auditor (Lamm et al., 2018), consequently an undesirable pay leads to an auditor change.

The results so far suggest that the sign of the three significant corporate governance variables are explained by the opinion shopping theory, supporting Chow and Rice (1982) statement that opinion shopping is the mostly used theory to explain auditor changes.

Conclusion and Recommendations

This research investigated the factors affecting the auditor change decisions. The firms’ characteristics and the corporate governance factors have been observed. The relation between the firms’ characteristics and the choice of a big 4 successor auditor, in particular, has been also tested. The results revealed that three board characteristics (the executive board members diversity, the board independence and the board members compensation) are found to be negatively related to an auditor change decision and two firm’s characteristics (company’s size and profitability) are found to be positively related to such decision. Furthermore, a positive relation between the company’s size and the choice of a big 4 auditor has been revealed. While the effect of board structure characteristics is justified by the opinion shopping theory, the size effect is interpreted by the agency theory.

Since most of the findings can be justified by the audit shopping theory, one can conclude that the regulatory efforts to eliminate the opinion shopping intentions behind auditor changes might have failed. The auditing profession should be more under the government sight and the regulatory bodies should be stricter when it comes to reporting the reasons of auditor changes and investigating any possible hidden intention. Furthermore, this research shows that more than 75% of the auditor change cases are switches to a big 4 auditor. Therefore, the problem of the big 4 dominance that UK, among others, has been suffering from, between 2002 and 2011, seems to persist until today. More serious measures should be implemented to give smaller firms the opportunity to enter the audit market. When more competition exists, the audit quality will be automatically enhanced, and the audit fees will go down. If the concentration problem is not remedied, the big 4 firms will end up dominating the market, imposing their own rules and the government will lose control. Government agencies might start hiring non-big 4 auditors to encourage the public to trust these firms. They have to eliminate the barriers to entry in this industry to allow new companies to enter and help them compete with the dominating firms. The government can stop big 4 firms from getting too big, by setting ceilings to limit the number of clients and the audit fees charged.

This study suffers from some limitations. First, including ownership structure in the analysis could have enriched the research and generated more significant results. However due to some data constraints, the history of annual corporate governance measures was not available. The data kept changing on a monthly basis with no accessibility to older records, and therefore, it was impossible for the researchers to check the impact of the ownership structure on the auditor change decision for the selected sample. Second, the number of observations that were initially 157 companies has shrunken due to some missing data. Third, the firm’s characteristics relation with the switch to a big 4 has been examined, however the same test was not possible for the corporate governance factors due to the small number of observation. Furthermore, the factors that impact the choice of a non-big 4 could not be tested. Less than 25 % of the cases in the sample were switch cases to non-big 4 auditors, and consequently, not being a substantial sample to test.

Theoretical Implications

This study enriched the literature to a great extent. First, three board characteristics were tested for the first time in this study: board compensation, board structure type, and board members skills; out of which one (board compensation) is found to be significantly affecting the auditor change decision. Furthermore, most of the reviewed literature on the auditor change topic highlighted the cases of Malaysia and China. Other studies focused on countries like Kuwait, Nigeria, Taiwan, Saudi Arabia or regions like East Asia or the MENA region. Consequently, the U.K. market has been a new context for such research. This work will pave the way for further studies to expand the research especially that very few scholars have tackled these questions in this market. In this study, the UK companies listed on the London Stock Exchange were the subjects of analysis, over a 5-year period. As the observations obtained were not so numerous, new research can reexamine the same topic over a longer period of time, and/or by adopting a cross sectional analysis in two different stock exchange markets, two different countries or two different industries. Furthermore, complimentary research can investigate the impact of an auditor change decision on the company’s earnings quality, as measured by discretionary accruals. Such study can uncover the company’s intentions behind the change by detecting earning manipulations practices following the new auditor’s appointment.

Practical Implications

When it comes to the practical implications, this study helps different stakeholders to better understand the auditor change context before taking any strategic decision. Moreover, the audit industry problems that have always existed are found to still persist. This conclusion urges the government to take serious actions regarding the big 4 powerful perceived quality, their dominance in the market, the opinion shopping attempts, the agency theory and the marginal position of non-big 4 firms. For instance, regulators and supervisory authorities may also better enhance the standing of UK as a reputable financial jurisdiction. Furthermore, creditors will scrutinize the financial reports of the companies engaging in auditor changes, before extending any credit lines, as the hidden intentions behind the auditor changes were shed light on. The tax authorities too, will be surged to examine attentively the tax declaration reports issued by companies hiring a new auditor. Moreover, practitioners will become more aware of any deficiency in their relationship with their clients, which might help them securing the retention of their existing clientele and preventing any potential loss. Form a managerial perspective, the findings of this study assist managers in the wise selection process of their auditors, given that the determinants of auditor choice are highlighted. More specifically, managers can foresee which factors will change in the future so that they can hire the right auditors accordingly. Finally, by discussing the agency problem and the opinion shopping theory, the stakeholders are now better informed about the auditor’s hiring decisions, taken solely to ensure clean audit opinions.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets analyzed during the current study are available from the corresponding author on reasonable request.