Abstract

This study provides additional evidence on information technology (IT) governance and its relationship to firm performance in emerging markets. It aims primarily to determine the level of IT governance in Saudi Arabian companies; it also aims at examining the impact of IT governance on the firm performance. The study target sample is 131 companies taken from 20 sectors of the Saudi financial market; during the year 2017. The researchers have used the IT-related backgrounds of the members of the board of directors as an indicator of IT governance. The researchers have also used another group of corporate governance indicators in addition to a set of control variables. The performance of the companies has been referred to as the operational performance which is represented as Return on Assets (ROA) and the financial performance as the Return on Equity (ROE). The descriptive results have been shocking. The study has shown a sharp decline in IT governance in Saudi companies; only 15% of companies have members of the board of directors with IT-related backgrounds, and the IT governance is not adopted or used in many important sectors. However, the regression analysis shows that there is a positive impact on IT governance only on the operational performance of Saudi companies. The results of this study provide a significant indicator of IT governance in Saudi companies. These results can be also used to develop the corporate governance code to focus more on IT governance.

Keywords

Introduction

Traditional boards of directors are characterized by the fact that they focus on the structure and composition of the board, its size, and the number of independent members. However, these boards lack risk management and efficient control of information technology (IT). Sarbanes–Oxley’s requirements have changed these concepts and have had a significant impact on the boards’ attention to the IT governance (Li, Lim, & Wang, 2007). Despite the growing importance of IT controls, their position in the business world remains a challenge for corporate management and stakeholders. The Kingdom of Saudi Arabia is considered as one of the developing economies that have a relatively closed economic environment; it has recently embarked on economic openness. In parallel, it has moved to develop and modernize its own legislative system, corporate laws, and corporate governance code (Hamdan, 2018). The Saudi Capital Market Authority (CMA) adopted the new corporate governance regulations in 2017 which aimed to establish effective governance arrangements in the listed companies in the Saudi financial market to ensure clarity of the relationship between the shareholders and the board of directors, on one hand, and between the board of directors and the executive directors, on the other hand. It has also considered shareholders’ rights in these companies. These regulations contribute to the interaction between these companies and the national legislation system within which these companies operate; they also contribute to integrate with these companies to achieve their objectives effectively and honestly. The benefits gained by corporate governance are not limited to the companies only; they extend to the national economy, in general, in view of the role of corporate continuity and growth in accordance with the rules of governance in driving the economy and increasing gross domestic product (GDP), which is consistent with the vision of the Kingdom of Saudi Arabia in 2030 (CMA, 2018).

This study argues that the economic openness witnessed by Saudi Arabia is attracting a large number of international companies, together with the technology and advanced technical and managerial expertise they have, which makes it necessary for the Kingdom of Saudi Arabia to go beyond looking at the traditional characteristics of corporate governance; it is also vital to ensure the IT governance in these companies. The structure of the board of directors, that includes specialists in IT or at least experienced in IT, contributes to the effectiveness of the performance of companies in various aspects whether they are operational and/or financial; it also contributes to the prevention of manipulation and fraud, which by its turn contributes to the improvement of the performance of the company. Therefore, the main purpose of this article is to explore the level of IT governance in Saudi Arabian companies, and its impact on the companies’ financial and operational performance.

This study has many contributions on the level of literature; it also has practical values. First of all, this study adds, to the previous literature, evidence on the role of IT governance in the performance of companies in developing countries that are economically improving and are constantly showing economic openness to foreign investment with which the risks, related to IT under the system of legislative laws and corporate governance, are in the process of growing and development. Second, this study contributes greatly as it adds a new dimension to corporate governance in Saudi Arabia by focusing on the board of directors’ characteristics related to the governance of IT, which is expected to have a significant effect on the improvement of the company’s operational performance with respect to effective monitoring of processing systems as well as electronic monitoring systems and financial performance related to the prevention of fraud, manipulation, and wasting the funds of the company. Third, previous literature, in the field of accounting, has focused on identifying and monitoring points of weakness in internal control systems. The findings of these studies yielded mixed results concerning the factors affecting the control of operating systems and electrical monitoring. Our study adds a new dimension to these studies as it intends to discuss the structure of the board of directors and the extent to which it is characterized by IT governance that can affect operational performance, including the control of operating systems and monitoring.

The rest of the article is organized as the following: the second part is concerned with the literature review and hypothesis development. The third part is concerned with the study sample and methodology, in addition to the study model, variables, and the method used in measuring such variables. The fourth part presents a descriptive study. The fifth part discusses the empirical results. The final part is concerned with conclusions, implications, and future studies.

Brief Literature Review and Hypotheses

Modern institutions rely heavily on IT and increasingly use it in managing business acts and procedures. This reliance on IT, coupled with the increasing complexity and interconnected nature of IT and infrastructure, as well as the threats to these systems and their growing risks are all key factors that increase companies’ need to implement internal IT controls to reduce those risks (Stoel & Muhanna, 2011). The elements of corporate governance of IT controls refer to the administrative, operational, and technical procedures that aim at ensuring protection of the confidentiality, integrity, availability, and information of the system (International Organization for Standardization/International Electrotechnical Commission, 2005; IT Governance Institute [IGTI], 2005; The National Institute of Standards and Technology, 2006). Information governance is a component of corporate governance (Lunardi, Becker, Macada, & Dolci, 2014; Webb, Pollard, & Ridley, 2006). IT governance is among the functions or tasks of the board of directors and executive officers (ITGI, 2003). IT governance helps organizations and companies to manage the risks that may result from using IT (Mohamed & Singh, 2012) and the assessment of the efficiency of IT investment (Weill & Ross, 2004), which in turn reflects positively on the performance of the company (Scheeren, Filho, & Tavares, 2013). There is a lot of discrepancy and debate among the previous studies that were concerned with the importance of IT in influencing the performance of the company. Carr (2003) argued that IT has not had strategic significance on projects since it has become a widely available commodity; it has not been considered strategically important by the directors of these companies. Other researchers such as Stiroh (2008) have found an inverse relationship between investment using IT and the performance of the company. On the contrary, other researchers (Sandulli, Fernández-Menéndez, Rodríguez-Duarte, & López-Sánchez, 2012; Tambe & Hitt, 2012) have argued that there is a positive relationship between investment in IT and the performance of the company.

However, with the great development of using IT in businesses, the Chief Executive Officer (CEO) should have an IT-related experience that qualifies him/her to express his/her opinion/s on many issues related to the operations of the organization. Li et al. (2007) stated that the expertise and knowledge that the CEO has in IT will affect the degree of involvement in IT management and will be more able to channel funds toward optimal investment in IT. Therefore, the main argument of this study is to assume that the CEO has adequate expertise, and the relevant IT-related background, can follow the details of all technical tasks and missions in a company; and establish appropriate control measures that will positively reflect on the company’s operational and financial performance. The Chief Information Officer (CIO) is assigned to suggest, develop, and implement a unique vision for the role of IT in promoting business strategies (Li et al., 2007). One of the key motivations behind the creation of the CIO position is to establish effective control over IT that is internally acceptable to the company’s management (Ross & Feeny, 2000). The CIO is considered as a chief executive of the company’s IT and is hence able to design and manage the IT department effectively. Li et al. (2007) have found that when a company has CIO positions with a larger proportion of independent members in the board of directors, the company would have a low probability of having IT material weaknesses, vulnerabilities, or pitfalls. Thus, we are able to build the study hypotheses as follows:

The scientific and professional background of the CIO contributes significantly to the success of the company’s strategy in adopting IT; it also contributes to the improvement of the company’s performance (Blaskovich & Mintchik, 2011; Karanja & Zaveri, 2012). In general, the company needs to have IT experts on the board of directors to help it make decisions about IT efficiently and effectively (Heroux & Fortin, 2017).

Empirical Method

Sample and Data

For purpose of generating data for hypotheses, we start the sample collection process with all the listed companies on the Saudi financial market in 2017 from publicly available financial statements, board composition, and ownership structure accessible through the Saudi financial market database. Financial, board, IT governance data were collected from 131 companies covering 20 sectors as presented in Table 1.

Sample Selection.

Model Design and Definition of Variables

We employed the regression analysis to test the impact of IT governance and board characteristics on firm performance. The basic model is presented as follows:

where Perf i = the firm performance including operational performance and financial performance for the firm (i); α = the constant; β1-7 = the slope for independence and control variables; BoardITback i = The Board IT-related background for the firm (i); BoardSize i = the number of board members in the firm (i); BoardIndep i = the percentage of independent directors on the board of firm (i); Companiesize i = the total assets of the firm (i); FirmAge i = the total number of firm (i) age; FinLev i = the financial leverage of the firm (i); Sector i = the sector to which the firm (i) listed; ε i = Random errors.

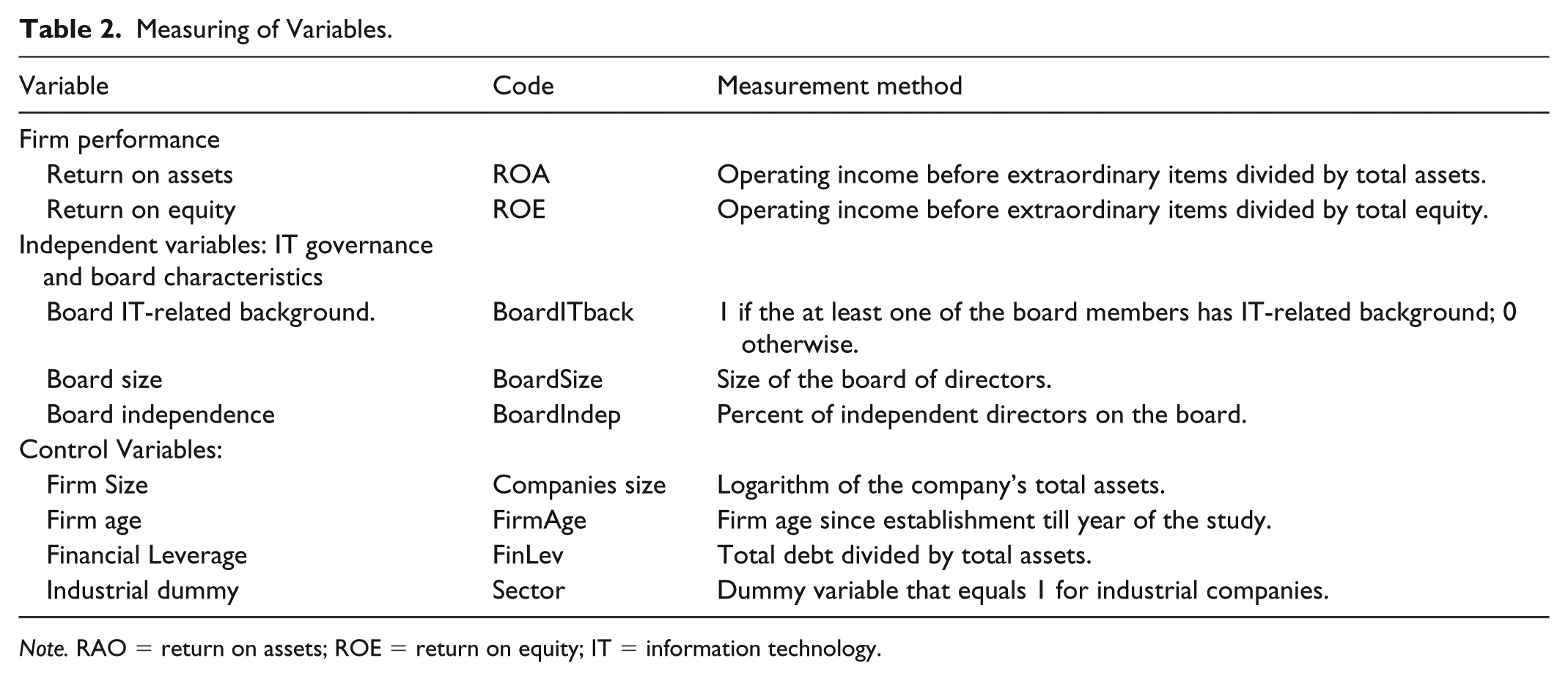

The selection of variables is based on an examination of previous empirical studies (Heroux & Fortin, 2017; Li et al., 2007; Stoel & Muhanna, 2011; Tonelli, Bermejo, Santos, Zuppo, & Zambalde, 2017), Table 2 shows the dependent variable, the independent variables, and the control variables employed in the study models.

Measuring of Variables.

Note. RAO = return on assets; ROE = return on equity; IT = information technology.

Descriptive Statistics

Table 3 shows the initial descriptive statistic of the study variables; it shows that return on assets (ROA) in Saudi companies is 6.379% with a high standard deviation. The same is true about the return on equity (ROE), which represents the financial return of Saudi companies. The most interesting result relates to the number of board members who have an IT background. Table 3 shows that the mean of members on the board of directors with IT background is 0.157; they make no more than 2% of the board members which is very low. The researchers have found that the presence of directors with an IT background is random and unorganized in Saudi companies and is not based on rules governing the presence of members with a background in IT on the boards of directors. This, in turn, indicates the low level of IT governance in Saudi companies. Table 4 depict that IT governance has been enacted in some sectors within the Saudi financial market. The distribution of board members with a background in IT by sector shows that only one board of directors has two members with an IT background, while 16 companies have one IT qualified member only. The majority of the remaining 98 companies do not have any qualified member in IT. Table 4 also shows that there are eight banks in which none of the board members have an IT background, while only three banks have one board member with IT background and only one bank has two members with an IT background. Members with IT background have been missing in many vital sectors in the Saudi financial market; these sectors are in dire need of such expertise at least for the members of the board to help streamline their decisions regarding the operation and control of IT. With respect to the features of the board of directors in Saudi companies, Table 3, the average number of board members is eight; the maximum number can sometimes be 11. The percentage of independent members is 25.9% which indicates an acceptable level of corporate governance in Saudi companies.

Descriptive Statistics.

Note. IT = information technology.

Board IT-Related Experience.

Note. IT = information technology.

Path Analysis

In Table 5, the sample of the study is divided into two parts. The first part includes companies that have at least one member on the board with an IT background, and the second part includes the companies that do not have any members with IT background. In both parts, the mean performance of the companies is calculated and the difference between the two groups is tested using t statistic and z statistic. Table 5 depicts that companies that has at least one member on the board with IT background have achieved 6.258% of ROA and 12.505% of ROE; while the companies that do not have members with IT background have had lower ROA (6.181%) and (10.865%) ROE. These results have positive implications over the impact of IT governance on corporate performance.

Path Analysis and Correlation Matrix.

Note. t/z/R statistic (top), p value (bottom). t Critical: at df 130, and confidence level of 99% is 2.358 and level of 95% is 1.658 and level of 90% is 1.289. IT = information technology.

, **, and *** denote significance at the 10%, 5%, and 1% levels.

However, the difference between companies is not statistically significant. It can be deduced from this that the difference between companies in terms of performance according to the level of IT governance is random and unsystematic as it does not follow an authentic and real approach in recruiting experienced members, in the board of directors of Saudi companies, who have adequate qualifications in the field of IT. This is clearly stated in the correlation matrix in Table 5 which highlights a positive relationship between IT governance and firm performance; however, this relationship is not statistically significant.

Multivariate Regression Results

Models Validation Techniques

General Linear Model (GLM) was used to test the relationship between IT governance and corporate performance. We, hence, rendered several tests to assess check whether data of this study met the conditions of the linearity assumptions. As presented in Table 6, it can be noticed that the variance inflation factor (VIF) values for all independent variables are less than 5 which means that we do not have any collinearity problems in the study model. To test the autocorrelation problem in the study models, we used Durbin Watson (D–W) test. Table 6 depicts that the Durbin Watson values of the models are within 1.5 to 2.5 range. This indicates there is no autocorrelation in this model.

Regression Results.

Note. VIF = variance inflation factor; RAO = return on assets; IT = information technology.

Testing of Hypotheses

We used the multiple regression analysis to test its basic hypothesis pertaining to the impact of IT governance on corporate performance. Two models were employed: the first relates to the company’s performance of ROA and the second relates to the company’s performance on the ROE. The results are shown in Table 6.

The R2 and Adjusted R-squared values of the study models did not meet the acceptable threshold values; indicating a weak representation of IT governance in the performance of Saudi companies. However, the regression analysis revealed a statistically significant impact of IT governance on operational performance ROA, whereas IT governance has no impact on the firm’s financial performance ROE. Therefore, the researchers accept the study’s first hypothesis which states that there is an impact of IT governance on ROA. However, the researchers reject the second hypothesis pertaining to the impact of IT governance on the firm’s financial performance ROE. These results indicate that companies seeking greater representation of experienced qualified IT professionals in their board will positively impact their operational performance through controlling operational processes related to IT and implementing better regulatory policies that will contribute to the improvement of the firm’s operating procedures. The results of this study are consistent with ample previous literature, such as Henderson et al.

Concerning the impact of corporate governance variables on the study models, the study has found that there is no impact of the size of the board of directors on the performance of the Saudi companies, while the independence of the board of the directors has showed a positive impact on the performance whether it is financial or operational. Table 6 depicts results related to the impact of control variables. The firm size has been shown to have a negative impact on operational performance. Small companies are more capable of managing their assets efficiently. The firm age has a positive impact on both the financial and operational performance. By virtue of early market entry and acquisition of large market shares, companies can achieve better returns. Finally, the study discovered that leverage has had a negative impact on the performance, but it was not statistically significant.

Conclusion

IT governance is a modern concept in corporate governance that has found its way into the rules and regulations of the developed countries, but emerging markets are still making first strides in this direction. This study aims at providing an additional evidence towards the relationship between of IT governance and firm performance in an emerging market that is currently undergoing a change in its economic structure, namely Saudi Arabia.

This study seeks to provide insights for the development of corporate governance in Saudi Arabia. The researchers have decided to take the scientific IT background of the members of the board of directors as an indicator of IT governance in 131 Saudi companies listed in 20 different sectors in the Saudi financial market in the year 2017. The study also has set of corporate governance variables and other control variables into consideration.

The study findings highlight a widespread weakness in the IT governance index in Saudi companies. Most of the boards of directors are almost inexperienced in terms of IT in different sectors. Although the regression analysis results express a positive impact of IT governance on operational performance, these results cannot be generalized. Consequently, further extensive studies are needed to be conducted to determine and identify the real status of IT governance in Saudi companies and their various impacts. However, these results give an initial warning regarding the urgent needs to take the necessary measures to activate the governance of IT in the Saudi corporate governance regulations and the search for practical mechanisms for implementing and supervising them to ensure greater effectiveness in the performance of Saudi companies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.