Abstract

Business survival has been a widely studied phenomenon in management literature given its impact on economic and social reality. There is some consensus that crises have a catalytic effect by driving the least efficient, productive, and profitable firms out of the market, while those best prepared with better technology, products, or business structure survive; this process is known as creative destruction. This study analyzed a sample of 5,000 firms using statistical survival models in order to identify the main factors affecting the life and disappearance of firms in periods of crisis (2008–2012) versus periods of recovery (2016–2020) to detect differentiated patterns of behavior. It was found that those firms that were driven out of the market during the crisis, unlike in the subsequent recovery period, were neither the less profitable nor the less efficient. Instead, more indebted firms or those that did not get the support of credit institutions were withdrawn from market. This result casts doubt on the effectiveness of the theorized process of creative destruction in times of economic crisis.

Introduction

The analysis of business dynamics is a subject that has aroused great interest among academics, both for its direct impact on the economic reality of territories and on the quality of life of their inhabitants (Roser et al., 2023). The positive correlation between economic growth and the evolution of the business fabric has led to an extensive study of the factors that affect business activity and, in particular, the survival of firms (Ahmad et al., 2019; Liñán et al., 2011; Shrivastav, 2019). Schumpeter (1939, 1942), a pioneer in the analysis of business dynamics and economic growth, stressed that survival of firms is complex, marked by constant innovation and by a phenomenon he called creative destruction. Creative destruction means that new firms with better solutions for the market replace old firms as they have updated and innovative offerings (Pyka et al., 2019; Schumpeter, 1939, 1942).

However, in business survival, not only innovation must be considered (Shakina & Barajas, 2020). There are also factors of an economic-financial nature that directly affect the operation of firms and that, if not properly managed, can result in their disappearance (Carmona & Dios, 2020; Park & Yoon, 2022). This reality was observed in different contexts and with different parameters, such as the interest rates faced by firms in Canada (Chirinko & Schaller, 1995), the problems of information asymmetry in access to financial resources in the United Kingdom (Binks & Ennew, 1996), or the non-payment of debts in Italy (Bottazzi et al., 2007). All these financial parameters undermine the possibility of survival, complementing the idea of creative destruction suggested by Schumpeter.

The process of business destruction was particularly intense in Spain during the period of economic crisis experienced between 2008 and 2012. In fact, different analyses of business demographics have been carried out to understand the impact on the business fabric (Crecente et al., 2015; Fariñas & Huergo, 2015; García Perea, 2020; Lampón, 2020). However, the general analysis in Spain could reduce the focus on specific situations, like that experienced in Galicia, which is particularly relevant because of its specificities as a peripheral region. In this regard, literature does exist that studies the effects on business dynamics in peripheral areas (Böckerman & Maliranta, 2007; Bosma et al., 2011; Psycharis et al., 2014) as well as the importance of these areas in economic development (Baumgartinger-Seiringer et al., 2022; Downs et al., 2023; Sánchez-Carreira et al., 2019). The center-periphery model of industrial structure is related to regional inequalities (Krugman, 1992), thus the importance of understanding which factors affect business dynamics in a peripheral region (Mazzola et al., 2022) such as Galicia. The regional factor, which has a major effect on business survival (Fritsch et al., 2006), must be considered in the light of two points. First, that the productive fabric of Galicia is based on micro, small and medium-sized enterprises that are highly dependent on funding from banks. Second, that the economic restrictions stemming from the crisis of 2008 were increased by the existence of a process of financial concentration among the local and regional savings banks (cajas de ahorro) and banks, which further hindered loan concessions to companies located in Galicia.

However, through the prism of complexity theory in which research regarding business survival is framed (Jiao et al., 2020), a small number of studies have made it possible to compare the behavior of influential variables on business survival in time periods with different circumstances (Jiao et al., 2020). The aim of this article is, on the one hand, to explain which economic and financial variables have an impact on business survival in an EU peripheral region, that is, Galicia, and analyse it in two contrasting periods of the economic cycle. One period, from 2008 to 2012, is of economic crisis aggravated by the banking concentration process occurring in the region that widened the gap between the supply and demand of credit. The other, from 2016 to 202, is of economic stability, when credit for companies was more fluid. This analysis enables observation of whether Schumpeter’s creative destruction process, based on the substitution of less profitable and productive companies by more modern and innovative ones, will occur (Malthus, 1990).

Particularly, this paper contributes to the business survival literature in two ways. Firstly, in times of crisis it was observed that profitability and productivity do not influence survival, while indebtedness does, unlike periods when the crisis has subsided. This research also identifies that company size is a variable that is statistically related to business survival both in period of crisis and recovery. Secondly, this research feeds the Schumpeterian literature related to those sources of creative destruction (Dodgson, 2011). The results obtained show that in periods of crisis, the bankruptcy of businesses does not only depend on their productivity and profitability, but rather on their capacity to access credit. With this aim, the paper is organized as follows. Section “Literature Review: Firm Survival in Times of Crisis” includes the literature review on firm survival with a special focus on times of crisis, highlighting the main variables considered from the economic-financial perspective. Next, section “Methodology” shows the research methodology. The results and analysis are presented in section “Analysis and Results,” and finally, sections “Discussion” and “Conclusions” contain the discussion and main conclusions, respectively.

Literature Review: Firm Survival in Times of Crisis

The phenomenon of firm entry, growth and exit has been extensively theorized in academic studies (Park & Yoon, 2022). From the Gibrat or proportional growth law (Gibrat, 1931)—which postulates the independence between firm growth and firm size, which has subsequently been demonstrated in different studies (Leitão et al., 2010; Nassar et al., 2014; Park & Yoon, 2022). And from the so-called passive learning model, which detected the importance of learning in firm growth, according to which firms will know their efficiency when they have entered the market and have a learning process when producing their products (Jovanovic, 1982). Thus, the less efficient firms will exit the market, so managers who want to keep firms in the market must assume an active learning process, increasing their efficiency with respect to their competitors through investments in R&D (Ericson & Pakes, 1995; Jiao et al., 2020).

Associated with this line of active learning is the idea of creative destruction (Schumpeter, 1939, 1942), an approach proposed for times of crisis, in which resources are transferred from less productive companies to those with higher productivity, preparing the economy for subsequent growth and generating higher levels of profitability. Productivity and economic profitability are therefore two key parameters for understanding the creative destruction suggested by Schumpeter. This effect was subsequently analyzed and verified in different contexts and in different countries. Thus, in Israel, firms begin to reduce their productivity before exiting the market (Griliches & Regev, 1995), as well as their profitability, as in the United States (Foster et al., 2001; Haltiwanger, 1997) or France (Bellone et al., 2008), the effect being particularly pressing for the most recent firms.

However, the underlying motivation for this exit from the market depends on multiple reasons, and the validity of these models and postulates is questioned. Thus, Fotopoulos and Giotopoulos (2010), Piergiovanni (2010), Teruel-Carrizosa (2010), and Villari et al., (2021) concluded that the Gibrat law was not fulfilled when the object of study are SMEs or service sector industries respectively. Moreover, the “cleansing” effect produced in the economic system in periods of crisis (Caballero & Hammour, 1994), a consequence of Schumpeter’s (1939, 1942) theorized creative destruction, seemed to have a limited effect (Barlevy, 2003). This paradox occurs because the most efficient firms are the ones that need more means to develop their activity due to higher initial costs, producing, in many cases, a redirection of resources with repercussions on the future economic development of the economy (Barlevy, 2003; Ouyang, 2009).

In the particular case of the economic crisis suffered by the United States between 2008 and 2012, the creative destruction that occurred in industry was lower than had been assumed a priori (Foster et al., 2015). On the other hand, the author found that productivity improved less than in previous crises, because the strategic reorientation of firms may have been highly conditioned by the financial shock of the crisis rather than by other variables. Kelly et al. (2015) in an analysis of SMEs in Ireland, concluded that, among other issues, the decline in bank borrowing at any time reduces the firm's chances of survival. While Carreira and Teixeira (2016a, 2016b) found that the financial crisis in the Portuguese economy led to a decrease in the redirection of resources, with less of a cleansing effect, both in start-ups and large firms.

All in all, the analysis of business dynamics does not follow a single behavioral model (Scarpetta et al., 2002). However, there is a set of control variables that affect the risk of their demise. With the aim of identifying variables and accomplishing the current research objectives, accounting information has been used here, which is one of the main approaches used by the literature on the failure of firms (Altman, 1968; Megaravalli, 2017). Among the variables under analysis, size is the most recurrent parameter (Jovanovic, 1982; Villari et al., 2021) and, depending on the models described above, it can become the most determinant. Age is another variable considered as an important business survival indicator (Zhou & Gumbo, 2021), because it suggests a certain consolidation and stability in the sector (Simbaña et al., 2017); moreover, it is a classic control variable in the literature (Audretsch et al., 2014; Villari et al., 2021). Another variable used is economic profitability, which indicates the firm’s ability to generate profits in relation to the assets invested in it, which is why a higher return on assets increases the probability of survival (Baumöhl et al., 2020). Solvency, associated with financial stability and probability of survival, is another variable that has been widely analyzed as it indicates the firm’s ability to meet its financial obligations to its suppliers and other creditors (Guariglia et al., 2016; Li et al., 2020). Productivity is a different benchmark indicator in this type of study insofar as more productive firms have better survival prospects (Dias et al., 2016; Osotimehin & Pappadà, 2017). Finally, indebtedness, understood as the sum of the financial obligations that a firm has at a given point in its life, has also been identified as a factor that influences business survival (Belda & Cabrer-Borrás, 2021; Lee, 2014; Nunes et al., 2013; Simbaña et al., 2017). In fact, it has been found that in cases of insolvency there is greater creditor protection when existing indebtedness is moderate (Barbosa, 2016).

Therefore, analysis of these variables will allow an understanding of the extent to which survival is directly conditioned by the economic-financial management of the firm. Also, indirectly, it will be possible to assess the extent to which the variables most associated with the phenomenon of creative destruction influence survival and to understand their scope in times of crisis.

Methodology

The analysis carried out for this research focuses on the region of Galicia, located in the northwest of Spain. At the national level, it is a region with great socio-economic potential. GDP per capita in 2022 stood at 92.4% of the Spanish average. Its level of development and the competitiveness index is close to the median in Spain. Business activity in 2020, even after being affected by COVID-19, generated a volume of operating income of 93,556 million euros and wealth of 23,698 million euros (Ardán, 2022). However, from the European perspective, Galicia has, according to Eurostat (2023) data, a GDP per capita of almost 77% of the EU-27 average, which places it among the transitioning peripheral regions. Furthermore, two issues are particular to this region. First, its business fabric is mainly made up of micro-sized (78.73%), small-sized (16.71%), and medium-sized enterprises (3.67%), with only 0.9% being large enterprises. Second, although most SMEs require banks for funding (Kelly et al., 2015), the uniqueness of the study of this region revolves around the circumstance, mentioned previously, that credit to SMEs, already reduced, was aggravated by a complex merger of savings banks during the crisis period.

For this analysis, two time periods are differentiated, one in the midst of the crisis (2008–2012) and the other in recovery (2016–2020), so that the results can be compared to understand the different factors that influence business survival. Now, the term non-surviving firm requires definition for the study. These are organizations that exit the market due to economic problems or disappear for reasons such as retirement and/or health problems of the owner, or acquisition by other firms (Headd, 2001).

In line with the purpose of the study, 5,000 firms were randomly selected from the Ardán database. This is a database with economic-financial information on firms from all sectors in Spain, extracted, among other documents, from the balance sheets and profit and loss accounts that have been deposited in the Mercantile Register. The firms selected come from all sectors of activity located in Galicia in each of the periods analyzed. Table 1 includes information on the selected firms.

Sample using the Spanish National Classification of Economic Activities (CNAE).

As can be seen, the most relevant percentage of firms corresponds to the commerce sector, followed by construction and the manufacturing industry. Supply firms, financial activities and extractive industries are those with the smallest presence. Therefore, the sample is a good representation of Galicia’s productive reality.

With reference to the variables used, accounting data provides the theoretical framework for studies on business survival (Altman, 1968; Megaravalli, 2017). It is suggested that age, and therefore the company’s capacity to survive, depends on the variables of size, economic profitability, solvency, and indebtedness. Age is considered the control variable and is defined as the time elapsing between the creation of the company and its disappearance, or the time of the study if they were still active in the market. In order to define the

These parameters have been subjected to different statistical analyses applied using the R statistical program. The Kaplan–Meier estimator is used to compare the two groups of individuals analyzed: surviving or non-surviving companies (Kaplan & Meier, 1958). This estimator indicates the estimated probability of surviving a specific period conditioned by current age. One peculiarity of survival analysis is that the event, the disappearance of companies, can happen at a point during the analyzed period or after it has finished, that is, the survival time is censored (Bland & Altman, 1998; Clark et al., 2003). The advantage of the Kaplan and Meier method is that it takes censoring into account, that is, it allows analysis of both companies that disappeared in the specific period (not censored) and those that have survived the observation period (censored). Thus the registers for both groups can be processed and included in the analysis jointly. The probability estimate was calculated as the product of successive conditional probabilities estimated separately (with censored observations). They are represented graphically by means of the survivial curve (Etikan et al., 2017; Jager et al., 2008; Stel et al., 2011).

Additonally, to analyse company survival, other parameters were estimated. The non-parametric Kruskal–Wallis test was used to test the null hypothesis of equality of the medians of the accounting variables, indicating the relationship, or lack thereof, existing between the independent variables and company survival (Kruskal & Wallis, 1952). The Harrington-Fleming (1982) test was used to evaluate the effect of each one of the considered parameters on survival. The null hypothesis to be compared is that there is no difference between the survival curves and the categories established for the variables. Finally, to evaluate the influence and impact of the variables on survival, the hazard ratio (HR) has been estimated and the Cox regression model used. When HR >1, there is an increase in the risk of shortening survival time; when HR <1 the risk decreases. The values close to one are interpreted as no risk (Cox, 1972).

Analysis and Results

Crisis Period (2008–2012)

Size

The size was measured as the volume of income, applying the recommendation of the European Union (2003). As mentioned above, the business fabric in Galicia is mainly made up of micro and small firms. This is a weakness of the Galician productive fabric, especially in situations of deep economic crisis. Firms with an annual turnover of over ten million euros, medium and large firms, which have most capacity to develop more commercial, financial, innovation, or productivity increase strategies, among others, have very little weight in the Galician economy (3.67% and 0.90%, respectively). Moreover, the percentage of these firms is a small part of the total in the sample (4.57%). For this reason, only two levels in the size of firms were considered: those whose turnover level does not exceed 10 million euros, 95.44% of the sample, and those that exceed it, 4.57% of the total sample.

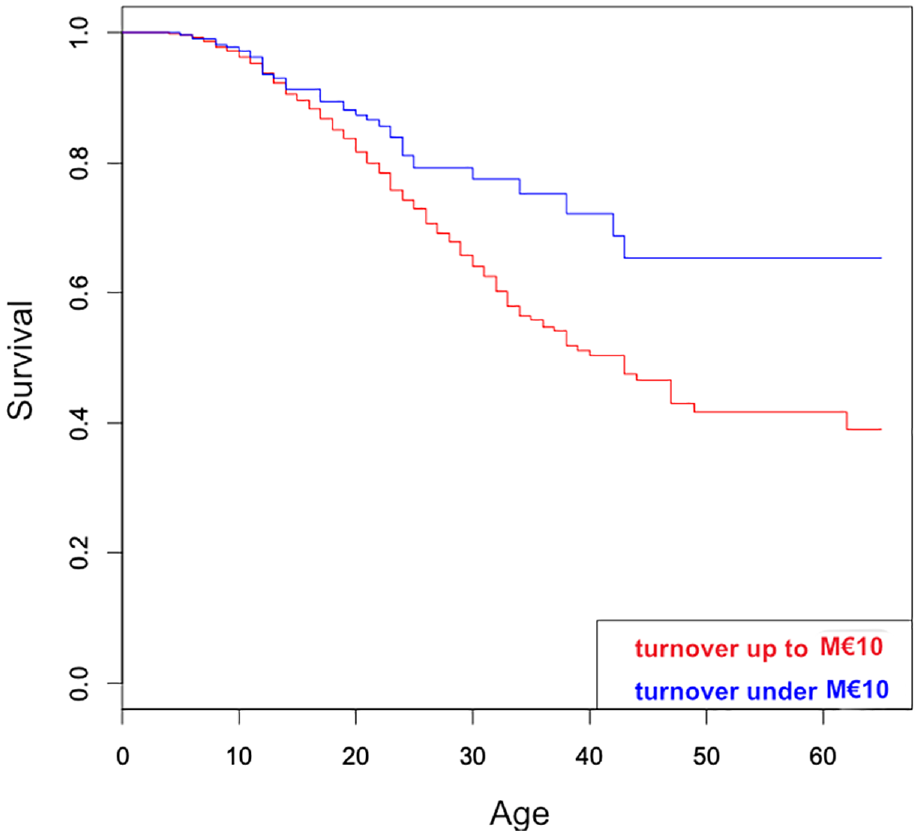

First, through the nonparametric Kruskal–Wallis test, it is verified that the age of firms is related to size during the crisis period (2008–2012). The result, statistically significant (p-value of contrast <.0001), shows that older firms are larger than new ones. The Kaplan–Meier method was applied to draw up the survival table and the survival curve. The survival table shows the number of existing firms by age group (Time) and the estimation of their survival (Survival). As shown in Table 3, among firms whose turnover does not exceed 10 million euros, the probability of survival is 96.3%; that probability is 97.2 % for those whose turnover exceeds 10 million euros. When these firms are 50 years old, the difference is more noticeable: for those whose turnover is under or equal to 10 million euros, the probability of survival is 41.6%, while for those that exceed 10 million euros, the probability of survival is 65.4%.

Survival by Turnover.

The curve in Figure 1 shows that firms with a turnover of over 10 million euros have a higher probability of surviving. This difference increases gradually with age.

Survival curves by size (two levels).

Table 4 shows the median survival age calculated for each group using the above data. As this table shows, for those firms whose turnover is under 10 million euros, the median age, that is, that age at which half of the firms have disappeared, is 43 years, while for firms whose turnover exceeds 10 million, the median survival is 70 years, clearly higher.

Median survival by size at two levels.

The relationship between a firm’s size and its survival was also studied. To this end, the Harrington-Fleming contrast was applied. The p-value of the test = .003, below the significance level of .05, makes it possible to affirm that a firm’s size is significantly related to its survival, considering the division into two groups, large and medium firms versus small and microenterprises. The Cox regression method was selected to check the relationship between the risk of a firm’s disappearance and its size. Smaller firms were used as a reference level, that is, those whose turnover is equal to or under 10 million euros. The result is shown in Table 5.

Effect of Size on Survival. Cox Regression.

Significant at 5%.

It can be observed that the effect of size on the survival of firms is significant, given that the p-value of the contrast is .00336. The negative coefficient (−0.4936) indicates that firms whose turnover exceeds 10 million euros are less likely to disappear; the hazard ratio (HR) indicates that the risk of disappearance of firms whose turnover exceeds 10 million euros is multiplied by 0.61 or, in other words, that the risk of disappearing for those firms whose turnover exceeds 10 million euros is 39% lower.

Indebtedness

According to their debt ratio, three groups of firms where established: low, medium, and high levels of indebtedness, using the 33rd and 67th percentiles as cut-off points. The nonparametric Kruskal–Wallis test, with a p-value <2.2e-16, practically zero, indicates that the age of firms is significantly related to indebtedness in the crisis period, 2008 to 2016.

The Kaplan–Meier method was used to draw up the survival tables for these three levels of indebtedness. As seen in Table 6, those firms at ten years old with high indebtedness have a probability of survival of 96%, those with an average indebtedness, 97.2%, and those with low indebtedness, 98.1%. However, at 50 years old, there is almost no difference in the probability of survival of firms depending on their degree of indebtedness. In fact, for low, medium and high debt ratios, the probability of survival is 52%, 49.2%, and 51.8%, respectively.

Life Table of Firms According to Three Levels of Indebtedness.

The representation of the survival of firms in relation to indebtedness is shown in Figure 2.

Survival curves for all three levels of indebtedness.

It can be observed that, in the 10-to-30-year-old section, a group in which there are more firms, the curves are systematically separated. However, the higher the level of indebtedness, the lower the curve, indicating a greater probability of disappearing. Finally, from age 30, the curves intersect, showing a certain random variability, without a defined pattern. The median estimated survival was calculated from the tables above. Thus, Table 7 shows the age at which the probability of disappearing is equal to that of surviving, and for those firms with low indebtedness, this age is 84 years.

Median Survival According to Indebtedness.

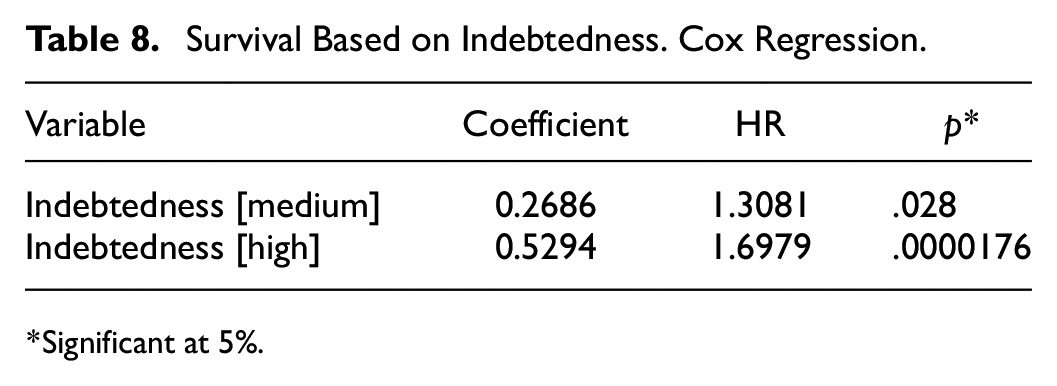

Applying the Harrington-Fleming contrast, results suggest that the debt factor influences survival in a clearly significant way (p-value = .00008). Analysis was made of the effect of indebtedness on survival using the Cox regression model, using the low level of indebtedness as a reference. As reflected in Table 8, the results obtained are statistically significant, given that the p-value of the contrast is lower than the usual significance level, .05.

Survival Based on Indebtedness. Cox Regression.

Significant at 5%.

Both medium and high levels are statistically different from the low reference level. The positive values of the coefficient (0.2686 and 0.5294, respectively) indicate that mortality is higher for both levels than for the reference level. The hazard ratio worth 1.3081 and 1.6979, respectively, indicates that the risk of disappearance of a firm with average indebtedness is 30.81% higher than that of a firm with low indebtedness, and for a firm with high indebtedness, it is 69.79% higher.

Solvency

The solvency ratio was also grouped into low, medium and high, corresponding to the terciles of the frequency distribution. In order to determine whether the age of the firm is statistically related to its solvency, in the period of crisis, 2008 to 2012, the Kruskal–Wallis test was applied. The result of the p-value <2.2e-16 indicates that this relationship is statistically significant: the age is higher for the most solvent firms.

To analyse survival, the Kaplan–Meier method, drawn up on Table 9, was used. As can be seen, firms with higher solvency are more likely to survive than those with lower solvency. For example, at 30 years old, the probability of survival for firms with a high level of solvency is 75.2%, for those with average solvency it is 68.5 %, and this probability of survival is 66.2% for those with low solvency. At the age of 50, firms with a medium and high solvency level have a survival rate slightly higher than 50%, while the probability is 42.5% for those with low solvency.

Life Table of Firms According to Three Levels of Solvency.

The Kaplan–Meier survival curve for the three solvency levels is shown in Figure 3. This figure shows that the survival rate of firms is different depending on their level of solvency. The survival curve of firms with a low and medium level of solvency is systematically below those with a high level until the firms are 30 years old (the vast majority of firms in the sample are in this age group). This reflects that firms with high solvency have a higher probability of survival.

Survival curves for all three-solvency levels.

The median survival estimated from the Kaplan–Meier survival curves is clearly different depending on solvency, as shown in Table 10. It was observed that the estimated median survival of firms with high solvency is much higher than those with low solvency: more than double (84 years versus 40). Firms with high solvency are longer-lasting.

Median Survival According to Solvency.

To verify that solvency is a factor that significantly influences firms’ survival, the Harrington-Fleming contrast was applied. With a p-value = .000007, clearly lower than the level of significance, the survival of firms is significantly different between firms with different degrees of solvency. The Cox regression model was applied to check if the level of solvency is an influential factor in survival. The group of firms with medium and high solvencies was compared with those with low solvency, the latter being the reference level. The regression model results are shown in Table 11, which shows clearly significant differences.

Effect of Solvency on Survival. Cox regression.

Significant at 5%.

The coefficients are negative (Coefficient = −0.2341 and −0.5503), which indicates that the mortality of firms is lower with medium and high solvency levels compared to those with low levels. As shown by the value of the hazard ratio in the table, the probability of disappearance of a firm with an average level of solvency is multiplied by 0.791, that is, it is reduced by 20.9%, in relation to the low level, and for a firm with a high level of solvency, it is multiplied by 0.5768 (it is reduced by 42.32%), in relation to the group with low solvency. The p-value of the contrast obtained for both groups of firms with medium solvency and high solvency (.03 and .00000152, respectively) is small, indicating that the difference between the solvency levels is significant.

Productivity

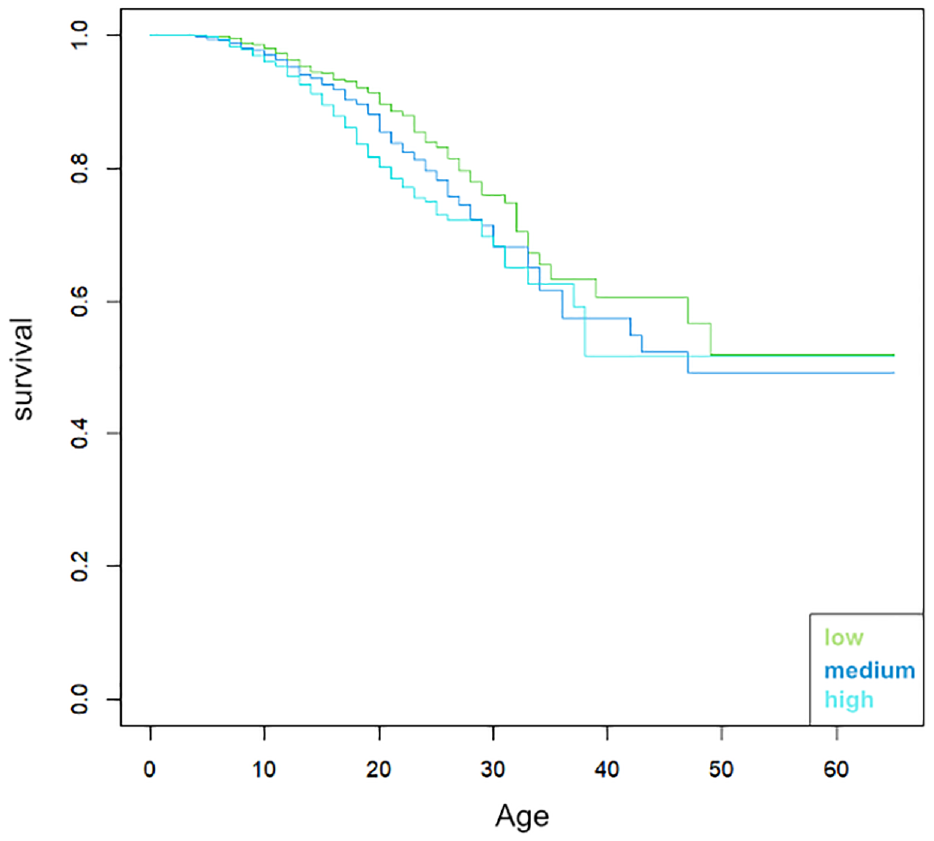

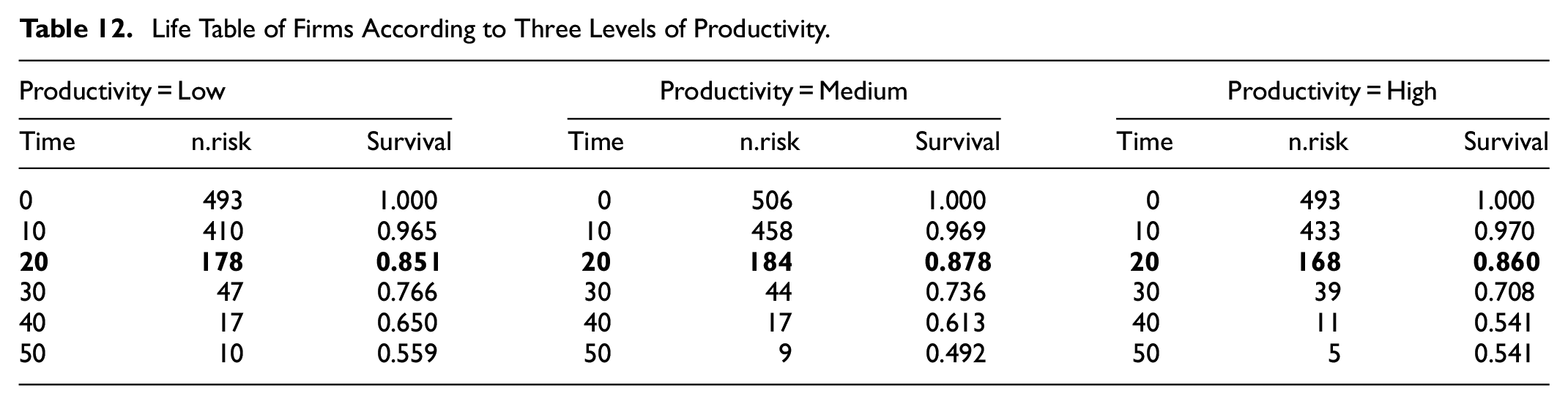

The survival of firms in Galicia was studied considering three groups according to productivity, with low, medium and high levels of productivity, and with the terciles of the frequency distribution as cut-off points. In the crisis period, 2008 to 2012, performing the Kruskal–Wallis test obtained a p-value = .589, which indicated that the age of the firms is not related to productivity in a statistically significant way. To corroborate this result, analyzed was performed of the survival of firms in relation to productivity through the Kaplan–Meier method. As seen in Table 12, the probability of survival at 20 years of age is 85.1% for firms with low productivity, 87.8% for those with medium productivity and 86.0% for those with high productivity. Furthermore, it can be observed that the chances of survival for different ages are similar in the three productivity groups.

Life Table of Firms According to Three Levels of Productivity.

The survival curve for each productivity level is shown in Figure 4. Again, it can be observed that survival curves overlapped and intersected, with no significant differences between them.

Survival curves according to the productivity level.

The median value for the three groups of firms established by productivity level is 17 years. The Harrington-Fleming contrast indicates that productivity is not related to survival since, the p-value = .9 is higher than the usual significance level (0.05). The effect of productivity on survival was assessed with the Cox regression model. Using the “low” level of productivity as a reference, this model was applied to obtain the data in Table 13.

Effect of Productivity on Survival. Cox Regression.

Significant at 5%.

The p-value of the two levels of productivity (.774 and .801) are higher than the usual significance level (.05), indicating that the level of productivity is not significantly related to survival. This relationship was not observed in Galician firms in the period of crisis analyzed, which is consistent with some results in the literature and also indicates that, in times of acute crisis, the productivity variable is much less important than other variables such as liquidity or solvency. Firms with high productivity can fail, while others with low productivity manage to survive since they have cash and solvency.

Return on Investment (ROI)

Three levels of ROI were also considered, low, medium and high level, using terciles 1 and 2 of the ROI ratio as cut-off points throughout the sample. In this particular compilation, the three groups are about the same size. First, the nonparametric Kruskal–Wallis test was performed to check whether return on investment is related to the age of firms. The p-value obtained equal to .1572, higher than the usual significance level (.05), indicates that, in the crisis period, 2008 to 2012, the age of firms is not significantly related to ROI.

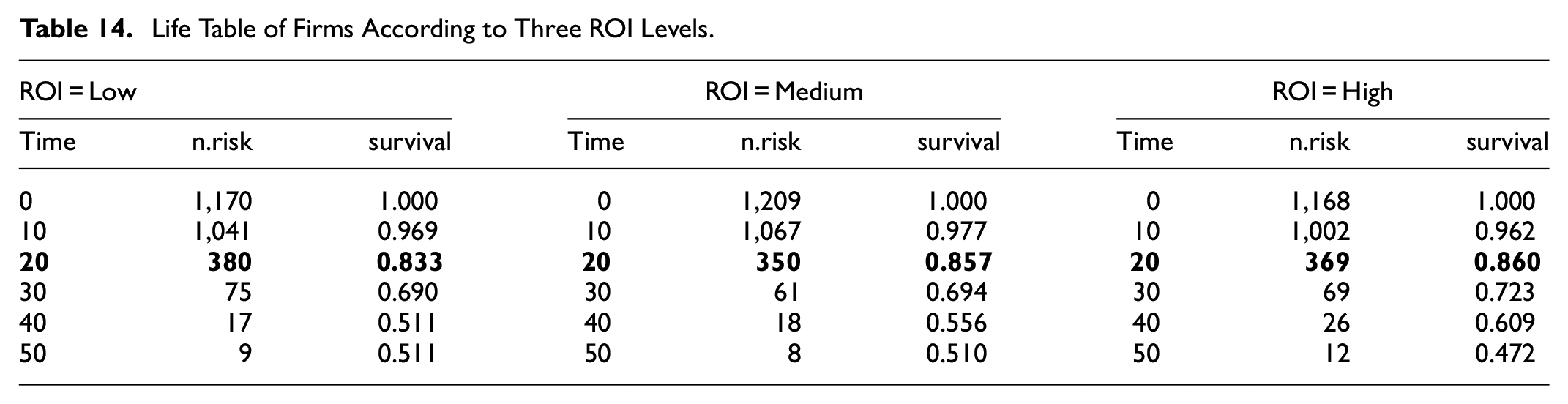

The Kaplan–Meyer method was applied to estimate the probabilities of the disappearance of firms with different economic performances, and the Life Table was drawn up. As seen in Table 14, the probability of survival at 20 years is 83.3% for firms with low ROI, 85.7% for firms with medium ROI and 86.0% for those with high ROI. It can be observed that these probabilities are similar for the three groups and the other age groups.

Life Table of Firms According to Three ROI Levels.

The Kaplan–Meier survival curve for the ROI levels is shown in Figure 5. In the graph, it is possible to appreciate that the curves are confused and intersect. This is because firms with low, medium and high levels of profitability behave similarly throughout their life.

Survival curves for the three ROI levels.

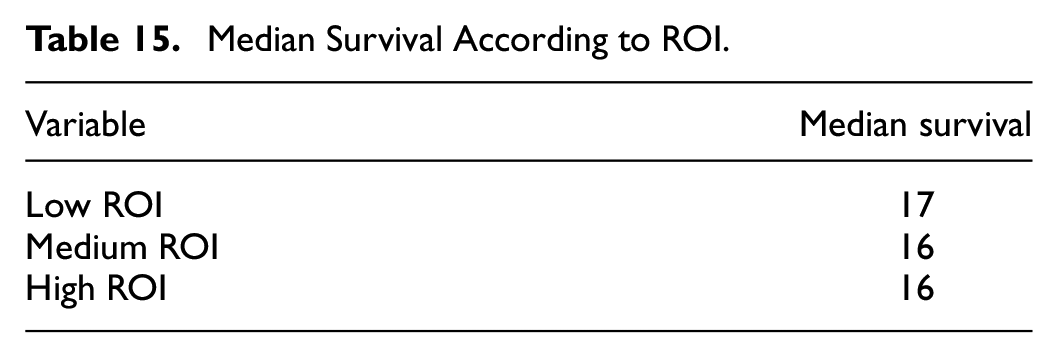

The median survival age, calculated for each ROI level, is shown in Table 15. The table shows there is almost no difference in the years in which the probability of disappearing and surviving is the same. The median for these three levels is 16 and 17 years.

Median Survival According to ROI.

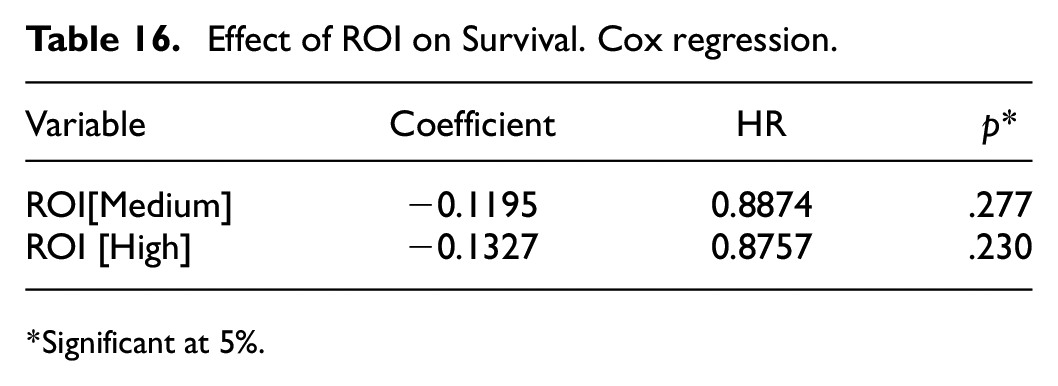

The results of the Harrington-Fleming test with a p-value = .4, higher than the usual significance level (.05), indicates, once again, that survival does not seem to depend on the ROI in Galician firms in this period. A check was made on whether ROI is an influential factor in their survival by applying the Cox regression model. The group of firms with low ROI were used as a reference level. The result of this model is shown in Table 16.

Effect of ROI on Survival. Cox regression.

Significant at 5%.

The relationship between the survival of firms and medium and high ROI is not significant. Although the negative value of the coefficient (−0.1195 and −0.1327) indicates a lower risk of disappearance for the firms with the highest ROI (medium or high level respectively compared to the low), none of the contrast p-values is below .05. Considering the above-mentioned statistical tests, results confirm that ROI does not affect survival significantly.

Not Crisis Period (2008–2012)

Size

Applying the same methodology described above to another sample of the same size from 2016 to 2020, the recovery period after the crisis, it was found that the size has, in the same way, a statistically significant effect on the survival of firms (with p-values with the Cox regression method = 0.01415).

Indebtedness

During this period (2016–2020) it was also found that indebtedness is not an influential variable in the disappearance of Galician firms (p-value = .5081 with the Cox regression method). Furthermore, firms with higher and lower indebtedness do not have significantly different mortality.

Solvency

From 2016 to 2020, the recovery period after the crisis, it was found that solvency (with p-values with the Cox regression method = 0.0001386) has shown a statistically significant effect on the survival of firms.

Productivity

In the period away from the crisis, 2016 to 2020, it was found that productivity is also not related to survival since the p-value with Cox regression method = 0.1187 is higher than the usual significance level (.05).

Return on Investment (ROI)

In the period away from the crisis, 2016 to 2020, survival depended statistically on profitability. There is a greater probability of survival of firms by increasing their returns. This dependence would show that, in periods of economic normality, the theorized effect of creative destruction occurs since less profitable firms are driven out of the market, but this does not happen in times of crisis.

In fact, the p-value obtained = 6e-10, lower than the usual level of significance, indicates that the survival of Galician firms depended statistically on profitability in a regular period, away from the crisis. Similar results were obtained when applying the Cox Regression method and are shown in Table 17. This confirms the relationship between the risk of disappearance of a firm and the ROI in this period. Again, resort was made to the firms with the lowest ROI as a reference level.

Effect of ROI on Survival. Cox Regression (period 2016–2020).

Significant at 5%.

It can be observed that effect of ROI on the survival of Galician firms in years in which there was no economic crisis does have a significant effect; the p-value of the contrast .000000155 and .00567 being below the significance level. The negative coefficients, −2.2600 and −.7020, indicate that the mortality of firms was lower with medium and high ROI levels. The probability of disappearance of a firm with an average level of ROI is multiplied by .1043, that is, it is reduced by 89.57% in relation to the group with a low level, and for one with high ROI, it is multiplied by 0.4956 (it is reduced by 50.44%) in relation to the group of firms with low level.

Discussion

The analysis carried out has compared the behavior of certain economic and financial variables of firms that survive versus those that disappear in two different periods of time: in times of crisis and in times of recovery. This analysis has made it possible to identify factors that may be associated with the survival of firms, including the parameters of size, indebtedness, solvency, economic profitability, and productivity. As discussed in the literature, the last two variables would be associated with creative destruction suggested by Schumpeter (1939, 1942).

Contrary to the Gibrat law, the results significantly relate size and growth to a firm’s survival, a relationship that holds true both in periods of crisis and recovery. This result is in line with studies conducted by Fotopoulos and Giotopoulos (2010); Piergiovanni, (2010), Teruel-Carrizosa (2010), and Villari et al., (2021). In addition to these works, an interesting aspect of size has been identified, which is that it is a variable that directly affects the improvement of productivity: the larger the size, the higher the productivity.

The results also show that in economic cycles of recovery, profitability and productivity are influential in business survival, while they are not relevant in periods of crisis. In periods of crisis, indebtedness and solvency are elevated as relevant factors. In other words, the availability of finance for the firm is prioritized over the maximum utilization of invested assets in the form of profitability or productivity. On the one hand, dependence on external financing weakens a firm’s situation in times of crisis, especially when it is limited and increases the risk of non-payment. On the other hand, high levels of solvency improve the capacity to face economic and financial difficulties, allowing them not to be an obstacle to future investments. These results confirm the role of financial constraints as a key aspect in the probability of SME bankruptcy (e.g., Fougère et al., 2013).

Another finding is derived from the above, the null statistical relationship between profitability and productivity with the survival of organizations in periods of crisis. This result contradicts Schumpeter’s postulate, casting doubt on his theorized process of creative destruction in periods of crisis. As in previous findings, these results show that the cleansing effect is limited in times of crisis (Carreira & Teixeira, 2016a, 2016b, Foster et al., 2015; Kelly et al., 2015), while it does apply in periods of recovery. Therefore, in periods of crisis the probability of bankruptcy of firms depends not only on their productivity or profitability but also on their ability to access credit. The paradox may arise whereby credit is allocated to less productive projects, taking it away from the more efficient ones, since the latter require more resources because of their higher initial costs in many cases. This redirection of resources may have positive consequences in the short term for the survival of certain firms but may have serious repercussions on the future economic development of the economy, because they may not be directed toward the most productive or profitable firms (Barlevy, 2003; Ouyang, 2009).

Conclusions

This article has studied the survival of firms, the factors that determine it, and its intensity and statistical significance during a period in which there was a severe economic crisis—between 2008 and 2012—and in another period in which economic activity was far from the crisis—from 2016 to 2020. The Kaplan–Meier method has been used to show that size, indebtedness and solvency are factors that influence the firm’s survival in periods of economic crisis. The significant relationship of these variables with age and survival has been demonstrated with the Kruskal–Wallis and Harrington-Fleming tests. In addition, there has been verification of the predictive capacity of these factors with the Cox regression model. Specifically, it has been shown that the risk of disappearance of large firms is 39% lower than that of small ones; firms with high indebtedness have an increase in the risk of disappearance by 69.79%; and the risk of disappearance for firms that have high solvency is reduced by 42.3%.

On the other hand, the empirical analysis has shown that ROI and productivity are not significant factors in the business survival of firms in periods of crisis. The least profitable ones do not have significantly different survival rates from the most profitable in the crisis period studied here. Similarly, firms with higher productivity ratios do not have a significantly higher probability of surviving than those with lower productivity ratios. The crisis has not eliminated the least profitable or least productive firms. In short, the effect of creative destruction is, at least, doubtful in the context of crisis. Meanwhile, in a period far from the crisis, the least profitable firms have significantly lower survival rates than the most profitable ones: the effect of market cleansing or creative destruction appears in periods of stability but not during the economic crises.

In terms of theoretical implications, it has been found that the theory of creative destruction does not always hold true, at least not in periods of crisis. In other words, contingencies directly affect business survival criteria. It is therefore necessary to refine this theoretical proposal by adding contingency factors and variables of an economic-financial nature to complement the proposal and make this theoretical approach more robust. In addition stimulating sustained growth, efficient allocation of resources (Acs et al., 2014; Fan et al., ;) could prevent that, in periods of crisis, business projects with high productivity levels but also highly dependent on credit have to abandon their activity, preventing the transfer of resources from companies with less potential toward those that are more prepared for the near future. In this regard, it is important to innovate as a means of survival and to obtain a higher return on business activity, but this approach must be adjusted to the context in which the firm is operating.

In the case studied here, it should be considered that the Galician business fabric is mainly comprised of small- and/or micro-sized companies, which are the type of company most affected when faced with reduced credit supply from banks that are suffering the effects of a crisis (Cortés et al., 2020). Thus, from the point of view of business management, it is very important to work on the scale of the company, because size provides an advantage to companies as it has a direct impact on negotiations with credit institutions, as well as on productivity. Self-financing or capitalization of profits can also be prioritized so as to achieve growth in the company with levels of indebtedness that allow a balanced equity equation. In times of crisis, it is important for managers to focus their efforts on financial availability rather than on productivity or profitability as a measure of survival. However, they must keep the medium and long term in mind because they must prepare the foundations for a renewal of the firm and its market offer, given that the process of creative destruction will return once the crisis period is over.

Finally, as implications for public administrations, there are several main ideas. The first is that public policies should favor the scaling up of firms. However, public authorities should focus on those companies with a strategic itinerary, since large companies die because of errors in strategical decisions (Manjón-Antolín & Arauzo-Carod, 2008). It is also that indiscriminate support for companies could lead to an ossified economy, that is, with little growth in productivity and less flexibility in the face of continencies (Naudé, 2022); additionally, there could be an increase in zombie companies, with persistent problems meeting their payments but able to stay in the market thanks to state or credit aid. (McGowan et al., 2017; Naudé, 2022). Strengthening the size of the business fabric could be promoted through mergers or acquisitions, R&D policies, or tax measures such as deductions for reinvestment and business consortia. In addition, in times of crisis, support should be reinforced for those firms with high profitability and productivity indices, but which have occasional difficulties in accessing credit. This aspect is of great importance for future economic regional development because if the firms that disappear are those that would best resist creative destruction, this could lead to the maintenance of firms with little future potential.

As far as limitations are concerned, it is worth highlighting the work’s geographic scope, which, despite having a certain academic interest due to its specific circumstances, should be increased to evaluate other regions from a comparative point of view. This would make it possible to find similar patterns of behavior in business survival. Furthermore, the study analyses only five variables, which could be complemented with others of an economic-financial nature, or also of an innovation nature, a composition of the workforce, or the internationalization of the firm, together with other contextual factors. Finally, as a result of the findings obtained, it is considered interesting to analyse the survival of companies distinguishing between rural and urban areas, as well as determining the role that foreign investments could play in their survival.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.