Abstract

This study endeavors to explore whether financial permeation stimulates economic growth in Asian region. To answer this, we collect data of 24 Asian economies for the duration of 2004 to 2016 and apply panel unit root, Granger causality, and regression techniques. The regression results controlled for country and time effects reveal that various indicators of financial permeation have substantial positive impact on the economic growth of Asian economies. Based on the findings of Granger causality, we find that financial permeation as well as economic openness has mutual causalities with economic growth. Therefore, it seems rational to conclude that financial permeation has positive impact on the economic growth in Asian economies. We also find a negative impact of financial crisis (2007-2008) on economic growth of Asian countries.

Introduction

One of the main objectives of every economy is to accelerate and sustain high economic growth and financial permeation can play a significant role to achieve this objective. Recently, the idea of financial permeation has gained an increased consideration and as such has been accepted as a policy primacy by central banks, supervisory body, and Governments’ officials. During the G20 summit 2010 held in Seoul (Korea), financial permeation has been accepted as one of the major pillars of world development agenda (Zins & Weill, 2016). The reasons for this recent emphasis are twofold: First, financial permeation aims to ensure access by providing financial services to the people and get them under the canopy of formal financial system so that these people may play their role in economic activity (Sethi & Acharya, 2018). Second, it targets poor and disadvantaged people in specific, and therefore it may reduce poverty and increase economic growth (Cull, Beck, & Holle, 2014). In short, the overriding goal of financial permeation is to build an atmosphere in which all the individuals may have an easy and equal access to financial services and to warrant contribution of all the individuals in the economic activity.

Recent literature regarding financial permeation focusing on different regions of the globe enhances our understanding of its impact on economic growth. For example, Kim, Yu, and Hassan (2018) studied the impact of financial permeation in Organisation of Islamic Cooperation (OIC) countries and find a positive influence of financial permeation on economic growth. Pradhan, Arvin, Norman, Nair, and Hall (2016) studied the same for ASEAN (Association of Southeast Asian Nations) states, whereas Inoue and Hamori (2016) inspected the effects of financial permeation for sub-Saharan African countries. A recent study investigated the effects of financial permeation in 31 advanced and emerging economies and found a significant affirmative association of financial permeation with economic growth (Sethi & Acharya, 2018). However, findings of these studies are mixed; some found positive impacts, whereas some observed negative effects and thus inconclusive. In addition, none of the previous significant studies comprehensively examined the role of financial permeation in economic growth of Asian region as a whole. Asian economies have experienced a higher economic growth in recent years, especially when compared with the economies outside of the Asian region. It is the reason that Asia has become a vital part of the global economy and as a consequence the center of global economic gravity has moved to Asia. Many countries in Asia have paid attention to promote and ensure inclusive growth and accordingly formulated financial inclusion strategies to achieve the same by increasing the level of financial inclusion 1 (Beck & Ayyagari, 2015). However, the extent to which financial permeation affected the economic growth of the Asian region is yet to be explored. Consequently, the objective of this study is to address these significant research gaps by investigating the impact of financial permeation on economic growth of Asian economies and thus provide a conclusive direction of the impacts.

To achieve the objective of the study, we collect data for 24 Asian economies for the period from 2004 to 2016 and panel unit root, Granger causality, and regression techniques controlled for country and time effects. The contribution of this study is manifold: First, the study investigates the impact of financial permeation on economic growth of 24 Asian countries; second, the study also investigates the impact of economic openness on economic growth of Asian countries; third, the study considers two dimensions of financial permeation (supply-led, demand-driven) and use two proxies for each of the dimensions. Moreover, the study also controls for global financial crisis (2007-2008) and investigates the impact of financial permeation on economic growth.

The rest of the article is structured as follows; Section “Literature Review” summarizes significant literature regarding the study, Section “Methodology” explains data and methodology; Section “Empirical Findings and Discussion” explains the results; and Section “Conclusion” concludes the results. References are provided at the end.

Literature Review

Notion of “inclusive finance” has been considered as a precedence program by organizations including the World Bank, Asian Development Bank, G20, governments, and policymakers of developing countries. Hannig and Jansen (2010) discussed that financial inclusion programs are purported to provide easier access to appropriate financial services to individuals, including marginalized section of the society that leads to contribute to a country’s economic development. Sarma (2015) delineated financial inclusion as a route to ensure easy entrance, availability, and use of financial services for all individuals of an economy. This elucidation firmly focuses on access and usage dimension of proper financial services for whole segments of a country. Similar to Sarma (2015), we focus on access to as well as usage facet of financial inclusion and describe financial permeation as a procedure which targets to enlarge the financial system among individuals. Just as water permeates through the sand, a proliferation in the financial sector action widens added economic prospects among individuals including poor, women, and marginalized, which tend to stimulate economic growth. In developing countries, the banking sector is considered as the crucial pillar and the greatest role-playing sector in the process of economic development. Therefore, we measure two dimensions of financial permeation, that is, supply led and demand driven. Furthermore, we measure each dimension using two proxies. Financial access is measured by commercial bank branches per 100,000 adults, and commercial bank branches per 1,000 km2. To measure financial depth, we take the proportion of outstanding deposits with commercial banks to gross domestic product (GDP) and the share of outstanding credits from commercial banks to GDP.

Previous studies inspected the effects of financial permeation in different ways. For example, applying financial access survey data on Uganda and Kenya, Johnson and Nino-Zarazua (2011) examined whether the countries’ socioeconomic and demographic elements have influences on access to finance. Demirgüç-Kunt and Klapper (2012) employed Global Findex and Enterprise Surveys data and explored the picture of access of individuals and small and medium-sized enterprises (SMEs) to financial services in African economies. They observed that in Africa most of the individuals use informal sources of finance and that most of the SMEs are also unwilling to go to banks. In the context of microfinance, Inoue and Hamori (2013) studied the influence of financial permeation on poverty percentage. Employing 90 developing countries’ panel data, from 1990 to 2008, they observed significant impacts of financial permeation on poverty reduction. Using the data of 37 sub-Saharan African countries for the period from 2004 to 2012, Inoue and Hamori (2016) tested the association between financial access and economic development of countries. They found that access to financial resources contributes to the process of economic growth of sample economies. Yang (2019) conducted a study on the issue of financial development and economic growth of middle-income countries. He found that the level of financial development significantly contributes to economic growth of the sample countries.

Mandel and Seydl (2016) conducted a research on U.S. banks’ data. They found a significant contribution of financial inclusion to financial stability which in order promotes economic stability of the country. Using insurance market penetration data of ASEAN countries for the period of 1988 to 2012, Pradhan et al. (2016) inspected the rapport of financial inclusion with economic growth. They observed positive impacts of insurance market penetration on economic growth of the sample countries. Employing data for the period of 2004 to 2016, Bigirimana and Hongyi (2018) found that financial inclusion through commercial banks has major long-run effects on Rwanda’s economic growth. Kim et al. (2018) employed the data of 55 OIC countries from 1990 to 2013 and found significant contributory effects of financial inclusion on economic growth.

Reviewing prior studies, we observe mixed evidences on the link between financial permeation and economic growth. We also observe that none of the previous studies investigated the impact of financial permeation on economic growth of the Asian region as a whole. Accordingly, to fill these gaps, we put forward a framework starting from the methodology, examine the issue regarding the impacts of financial permeation on economic growth of Asian economies, and contribute to the existing literature.

Method

Sample and Data Sources

To address the objective of our study, we collect data from 24 Asian economies. We have chosen these Asian economies as we confronted with scarcity of data, and therefore we had to reduce our sample to 24 countries. World Development Indicators (WDI) of World Bank is considered as the leading cross-country databank in this field. It comprises cross-country time series data on many variables related to financial permeation and development. 2 However, this databank encompasses comparatively data for a shorter period of time on main variables alongside many economy-wise missing data. Based on data handiness, we have accumulated and sorted data on economic growth (LogGDPC i,t ) from 2004 to 2016 and control variables of Asian economies from the World Bank database. The International Monetary Fund’s (IMF) Financial Access Survey (FAS) database has been used to collect data on financial permeation variables. FAS is an accessible cross-country database, 3 which encompasses commercial banks and non-bank financial institutions’ time series data.

Variables

Dependent and explanatory variables

In this research, our main aim is to examine the link between financial permeation and economic growth. Therefore, following previous significant studies (Beck & Levine, 2004; Beck, Levine, & Loayza, 2000; Ehigiamusoe & Lean, 2018), economic growth is considered as a dependent variable, which we measure by real GDP per capita. As the target of this study is to inspect whether financial permeation contributes to countries’ economic growth, financial permeation is the central independent variable of the study. We consider four proxies to measure financial permeation based on maximum availability of data: number of commercial bank branches per 100,000 adults (LogFP1 i,t ), number of commercial bank branches per 1,000 km2 (LogFP2 i,t ), proportion of outstanding deposits with commercial banks to GDP (LogFP3 i,t ), and ratio of outstanding loans from commercial banks to GDP (LogFP4 i,t ). The first two capture individual’s accessibility to financial services and are known as supply-led financial permeation. Access to finance is vital to a country’s economic growth, especially for developing nations, because access to finance from formal organizations generates economic prospects and consequently leads to the economic development of the country. Previous empirical studies applied these proxies and observed a positive connection between these two proxies and economic growth in India (Anand & Chhikara, 2013; Joseph & Varghese, 2014) and in Ghana, Nigeria, and South Africa (Ehigiamusoe & Lean, 2018). The demand-driven parts of financial permeation comprise two proxies which focus on the usage dimension of financial services by the individuals. Progress in accessibility to and usage of formal financial services expand opportunities for the households to pursue economic doings that ultimately leads to acceleration of economic growth. Employing these proxies, previous empirical studies examined significant positive effects on economic growth in Nigeria (Babajide, Adegboye, & Omankhanlen, 2015) Ghana, Nigeria, and South Africa (Ehigiamusoe & Lean, 2018) and India (Sharma, 2016). In line with these studies, we also expect an affirmative rapport between financial permeation proxies and economic growth.

Control variables

We have considered some control variables in our study to segregate the relationship between level of financial permeation and economic growth. First, consistent with previous studies (Ehigiamusoe & Lean, 2018; Inoue & Hamori, 2013), we control for the portion of net foreign direct investment (FDI) inflows to GDP (FDI i,t ), because the results of previous studies have revealed that FDI has substantial effects on countries’ economic growth (Ali & Mingque, 2018; Comes, Bunduchi, Vasile, & Stefan, 2018; Ehigiamusoe & Lean, 2018; Makki & Somwaru, 2004; Solarin & Dahalan, 2014; Zhuang, 2017). Arguing the same, we assume that FDI is important and thus controlled for in this study.

A country’s unemployment situation, the share of the labor force without having work but looking for employment, also influences its economic growth. Higher unemployment rate has a negative influence on countries’ economic growth (Imran, Mughal, Salman, & Makarevic, 2015; Kukaj, 2018). Recognizing its consequences, we control for the unemployment effect by adding this in the analysis, where it is being measured as the ratio of total labor force without work (UMP i,t ). Another control variable, education level, is a vital element of development and plays a crucial role in the process of human resource development that finally promotes economic growth (Ehigiamusoe & Lean, 2018; Gundlach, 2001; Seetanah, 2009). Thus, we measure it by the percentage of primary school enrollment to population (EDU i,t ) and expect encouraging effects of education levels on a countries’ economic growth. Furthermore, population is also an imperative factor of economic growth as previous studies (Akbar, Imdadullah, Ullah, & Aslam, 2011; Solarin & Dahalan, 2014) noticed negative influences of population growth on countries’ economic growth. Thus, we also believe that population (LPOPG i,t ) may influence the economic growth and it is important to control for population growth.

Furthermore, we control for inflation rate (LINF i,t ), which is measured by consumer price index (CPI), because many studies found that inflation has influences on countries’ economic growth (Adebola & Dahalan, 2011; Behera & Mishra, 2017; Divya & Devi, 2014; Mallik & Chowdhury, 2001). Another control variable we added is the ratio of domestic credit delivered by the financial sector to GDP. Abida, Sghaier, and Zghidi (2015) stated the significance and used this variable in their analysis. They observed significant effects of domestic credit on economic growth. Hence, we applied the ratio of domestic credit provided by the financial sector to GDP and thus control it in our research.

Moreover, our study period is from 2004 to 2016, and therefore it is important to control for the impact of global financial crisis of 2007-2008. Prochniak and Wasiak (2017) observed negative consequences of financial crisis on economic growth, whereas based on data of 26 European countries for the period of 1990 to 2016, Asteriou and Spanos (2019) found that financial crisis slows down the economic growth. Following Kodongo and Ojah (2016), we incorporate time dummies in this study. The global financial crisis dummy variable, GFC, takes the value of 1 for years 2007 and 2008, whereas it is 0 for the other years. Table 1 presents the variables, definitions, and measurement along with the sources of data.

Variables, Their Proxies, Model Name, and Source.

Note. GDP = gross domestic product; WDI = World Development Indicators; FAS = Financial Access Survey; FDI = foreign direct investment; CPI = consumer price index.

The Model

To empirically explore the impact of financial permeation on economic growth, and based on our discussion in Section “Variables,” we develop the following regression equation 4 :

where LogGDPC i,t is the dependent variable which mirrors the economic growth of countries i at time t; Xi,t – 1 is a 1-year lag of financial permeation measured by four proxies, that is, LogFP1i,t – 1, LogFP2i,t – 1, LogFP3i,t – 1, LogFP4i,t – 1; β1 is the coefficient, which computes the effects of financial permeation on economic growth; Yi,t – 1 is a 1-year lag of control variables, that is, FDIi,t – 1 (fraction of net FDI inflows to GDP); UMPi,t – 1 (unemployment rate); EDUi,t – 1 (ratio of primary school enrollment rate); LPOPGi,t – 1 (population growth rate); LINFi,t – 1 (inflation rate); DCPFSi,t – 1 (domestic credit provided by the financial sector); β2 is the coefficient for control variables; CNT i is the country fixed effect, YR t is the time fixed effect, and ε i,t is the error term.

To incorporate the impact of global financial crisis, we include a dummy variable in the regression equation (Equation 1) and develop the following:

where GFC t is a time dummy that takes 1 for years 2007 and 2008, and 0 otherwise; β3 is the coefficient explaining the impacts of global financial crisis on countries’ economic growth. Furthermore, we employ country and time fixed effects regression in Equation 1 and country fixed effects regression in Equation 2 considering the findings of Hausman test, our dataset type (Baltagi, 2008), and a recent significant study (Sethi & Acharya, 2018).

Empirical Findings and Discussion

Descriptive Statistics

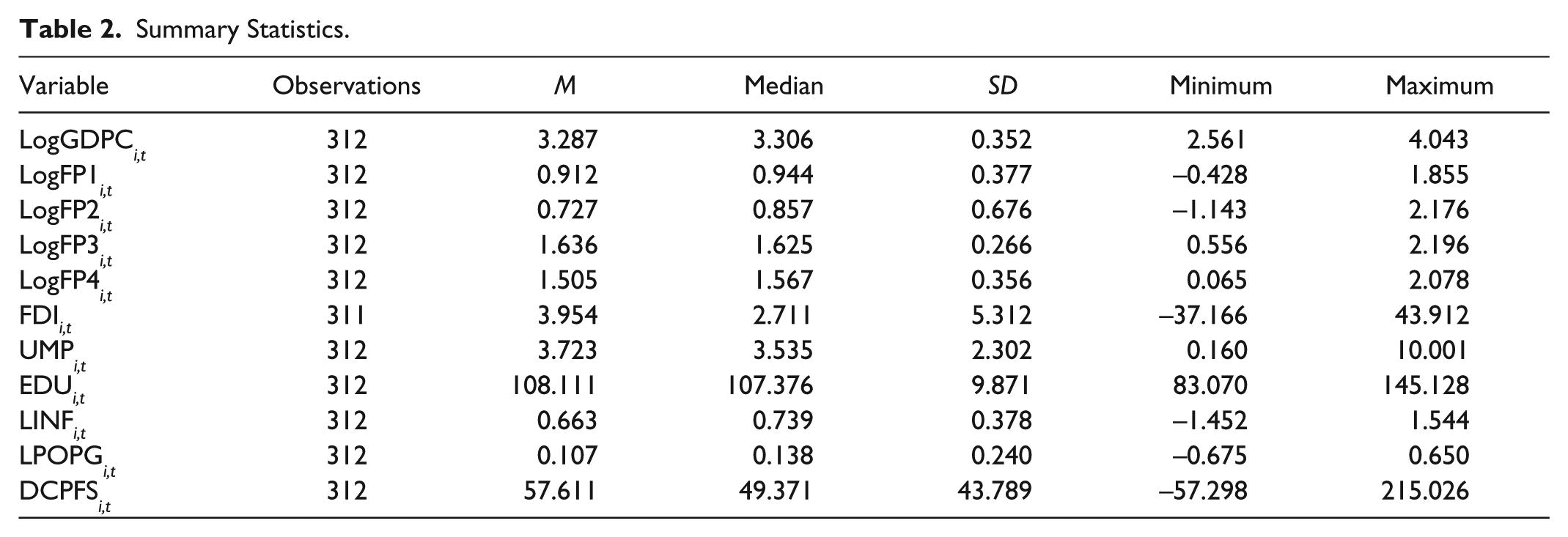

Table 2 reveals the descriptive statistics for the complete dataset and Table 3 provides mean values for all the variables, separately for all the countries included in our sample. The mean value of 3.287 with a standard deviation of 0.352 for LogGDPC i,t explains that these Asian countries have enjoyed a stable economic growth during 2004 to 2016. Afghanistan has the lowest economic growth of 2.711 and Malaysia has the highest economic growth of 3.966. Afghanistan also has the lowest number of commercial bank branches per 100,000 adults with a mean value of 0.186 for LogFP1 i,t and Mongolia has the highest with a mean value of 1.761. On the contrary, Maldives has the highest number of commercial bank branches per 1,000 km2 with a mean value of 2.015. Furthermore, the mean value of 1.636 with a median of 1.625 for LogFP3 i,t explains that the ratio of outstanding deposits with commercial banks to GDP of half of the countries is close to the mean value of overall dataset and China has the highest with a mean value of 2.121. The mean value of 1.505 with a median of 1.567 for LogFP4 i,t explains that the ratio of outstanding loans from commercial banks to GDP of half of the countries is higher than the mean value of overall dataset and Malaysia has the highest with a mean value of 2.007.

Summary Statistics.

Country-Wise Mean Value for All the Variables.

Furthermore, the mean value of 3.954 with a standard deviation of 5.312 for FDI i,t explains that there is a huge difference between these Asian countries in their proportion of net FDI inflows to the GDP ratio. Mongolia has the highest proportion of net inflows to GDP with a mean value of 10.898 and Bangladesh has the lowest with a mean value of 1.116. The mean value of 3.723 for UMP i,t explains that the unemployment rate is quite high in these Asian countries. Furthermore, primary school enrollment rate is highest in Nepal with a mean value of 132.629 and lowest in Pakistan with a mean value of 91.011 for EDU i,t . The mean value of 0.663 with a maximum value of 1.544 for LINF i,t explains that these countries have experienced a quite high inflation rate during 2004 to 2016. Furthermore, most of these Asian countries have positive population growth except China (–0.284), Fiji (–0.161), Myanmar (–0.098), Samoa (–0.144), Sri Lanka (–0.129), Thailand (–0.315), and Tonga (–0.274). Moreover, the mean value of 57.611 with a standard deviation of 43.789 for DCPFS i,t explains that there is a huge difference between these Asian countries in their ratio of domestic credit provided by their financial sector. The financial sector of China provides the highest amount of domestic credit with a mean value of 150.172 and this value is the lowest for Afghanistan (0.133).

Correlation Statistics and Robustness Tests

Table 4 presents the pairwise correlation matrix for dependent and all the explanatory variables. We find a significant correlation greater than 0.50 between financial permeation variables (LogFP1 i,t , LogFP2 i,t , LogFP3 i,t , and LogFP4 i,t ). However, this high correlation is not a problem because we use four different regression models and include only one proxy of financial permeation in one model (see Tables 8 and 9). Furthermore, we find a high correlation between DCPFS i,t and LogFP3 i,t as well as LogFP4 i,t . Therefore, we find out variance inflation factor (VIF) to check for multicollinearity issue. However, we do not find VIF greater than 10 (see Table 4), and therefore multicollinearity is not a problem for our regression models (Ott & Longnecker, 2015). Furthermore, we check for heteroscedasticity by applying modified Wald test and check for autocorrelation by applying Wooldridge test. We use clustered robust standard errors to control for heteroscedasticity and serial correlation in the fixed effects regression model. Moreover, we use 1-year lag of independent variables to control for possible endogeneity that may arise from simultaneity between economic growth and financial permeation, following previous studies (Lin, 2014; Rugman, Li, & Hoon Oh, 2009; Xie & Li, 2013). Moreover, we also run country and time fixed effects regression model to validate the results of our study.

Correlation Matrix.

Note. VIF = variance inflation factor.

Significance level at 5%.

Cross-Sectional Dependence (CD) Test

When employing panel data into analysis, it is essential to inspect the existence of CD in the series. Overlooking CD determination may yield influenced and inconsistent outcomes. Pesaran (2004) stated that the CD test is a common test relatable to a great array of panel data models, containing stationary and non-stationary dynamic heterogeneous panel. We perform the CD test of the Lagrange multiplier (LM) test by Breusch and Pagan (1980) and the CD test recommended by Pesaran (2004) to examine whether CD exists in our model. Breusch and Pagan (1980) recommended LM statistic, which is usable for fixed N as T goes to infinity. Under the null hypothesis of no cross-sectional dependence, ei,t is anticipated to be independent and distributed identically over time and across cross-sectional units. Under the alternative, ei,t might be correlated across cross-sections but the assumption of no serial correlation remains. LM statistic is calculated as follows:

where

Pesaran (2004) suggested the CD statistic as follows:

where T reflects the time period, N is the number of the cross-sections, and

where

Results for CD Test.

Note. CD = cross-sectional dependence.

Panel Unit Root Test

From the results of the CD test shown in Table 5, we found that there exists CD among the series. Hence, we conducted second-generation unit root tests in preference to first generation because second-generation panel unit root tests illustrates the CD among the cross-sectional units of the panel, whereas the first-generation one considers the independency of all the cross-sections. To tackle the cross-section dependence issue, Pesaran (2007) recommended cross-sectional augmented Dickey Fuller (CADF) test statistic by adding cross-section average of lagged levels and first differences of the specific series to traditional or augmented Dickey Fuller test. In other words, the CADF test is an extension of the Cross-Sectional Augmented IPS (CIPS) test of Im, Pesaran, and Shin (2003):

where

Taking into account of the CD, Table 6 shows the results of Pesaran (2007) panel unit root test. As shown in Table 6, we reject the null hypothesis of unit root for all the variables in both intercept and intercept-trend models at the 1% significance level and indicate that all variables are stationary. Thus, it is suitable to employ regression on stationary dataset.

Results of Pesaran Unit Root Test (CIPS statistics).

Note. CVs are obtained from Pesaran (2006). CIPS = Cross-Sectional Augmented IPS; CV = critical value.

Granger Non-causality Test

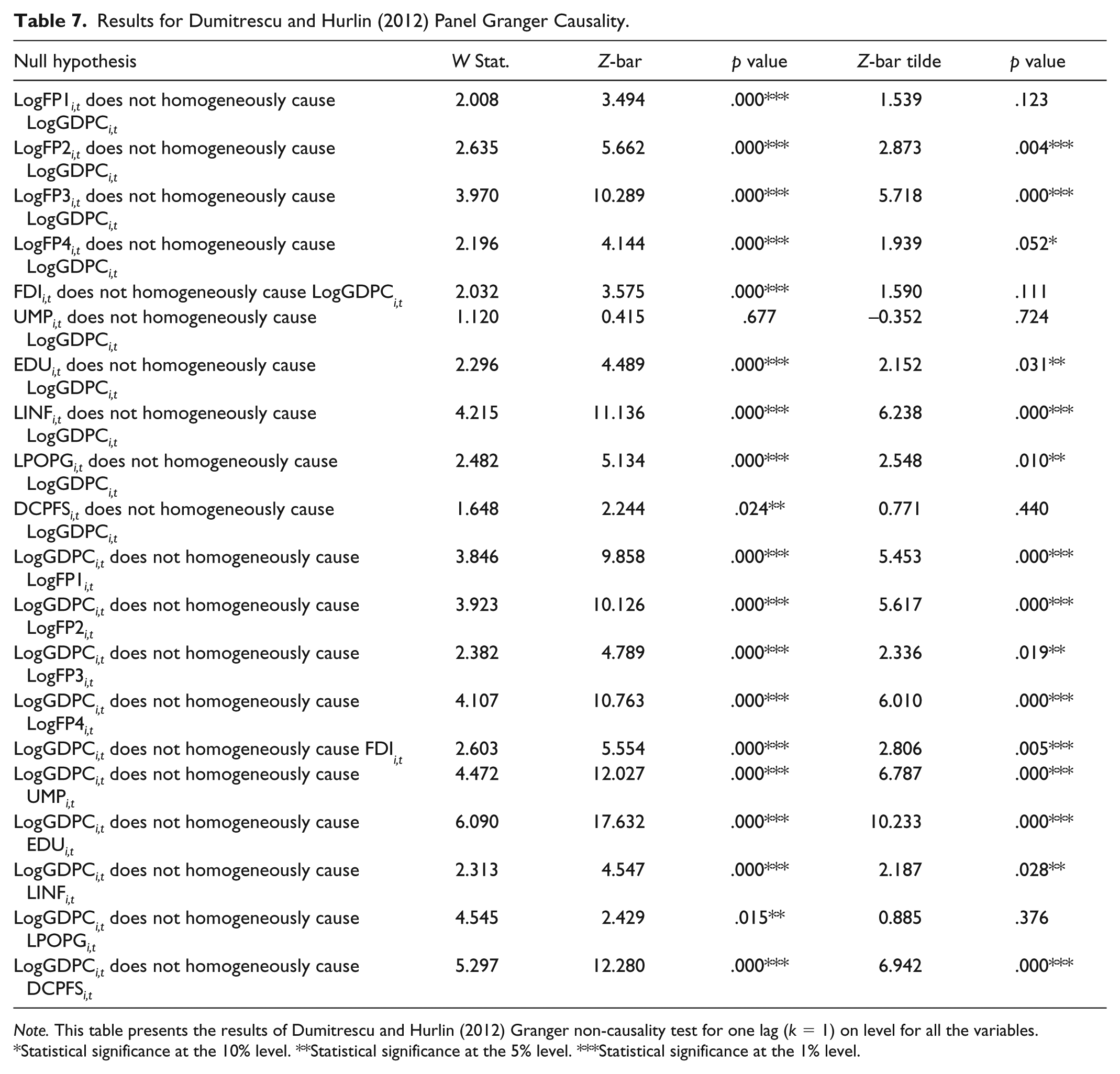

We report the results of Granger non-causality test for each of the variables in Table 7 to find out causality between dependent and independent variables. We choose Dumitrescu and Hurlin (2012) Granger non-causality test because it assumes that all the coefficients are different across all cross-sections and we have 24 different countries. The optimal lag was determined to be 1 by Akaike’s information criterion (AIC). Focusing on the causalities between LogGDPC i,t and different financial permeation proxies, we find that LogFP2 i,t and LogFP3 i,t cause LogGDPC i,t at 1%. Whereas LogFP1 i,t causes LogGDPC i,t at 1% according to W-statistic and Z-bar statistic but does not cause according to Z-bar tilde statistic, LogFP4 i,t causes LogGDPC i,t at 1% according to W-statistic and Z-bar statistic at 10% according to Z-bar tilde statistic. The results also explain that LogGDPC i,t causes LogFP1 i,t , LogFP2 i,t , LogFP3 i,t , and LogFP4 i,t at 1%. Thus, we find that there exists reverse causality between financial permeation and economic growth consistent with the findings of Evans and Lawanson (2017), Gourène and Mendy (2017), and Sharma (2016). Focusing on the causalities between LogGDPC i,t and control variables, we find that EDU i,t and LINF i,t cause LogGDPC i,t at 1% and 5%. DCPFS i,t and FDI i,t cause LogGDPC i,t according to W-statistic and Z-bar statistic but does not cause according to Z-bar tilde statistic. Findings indicate that LogGDPC i,t also causes EDU i,t , LINF i,t , DCPFS i,t , and FDI i,t . Thus, there is bidirectional causality between per capita GDP and education, per capita GDP and inflation, per capita GDP and domestic credit provided by the financial sector, and per capita GDP and FDI. Findings shown in Table 7 indicate that, consistent with Kim et al. (2018), there is unidirectional causality from population growth to per capita GDP. We find that UMP i,t does not cause LogGDPC i,t , whereas LogGDPC i,t causes unemployment. That is, there is unidirectional causality from per capita GDP to unemployment rate which is consistent with Bist (2018). Therefore, according to these results, we find evidence for the overall causality between financial permeation, economic openness factors, and economic growth in 24 Asian countries.

Results for Dumitrescu and Hurlin (2012) Panel Granger Causality.

Note. This table presents the results of Dumitrescu and Hurlin (2012) Granger non-causality test for one lag (k = 1) on level for all the variables.

Statistical significance at the 10% level. **Statistical significance at the 5% level. ***Statistical significance at the 1% level.

Regression Analysis

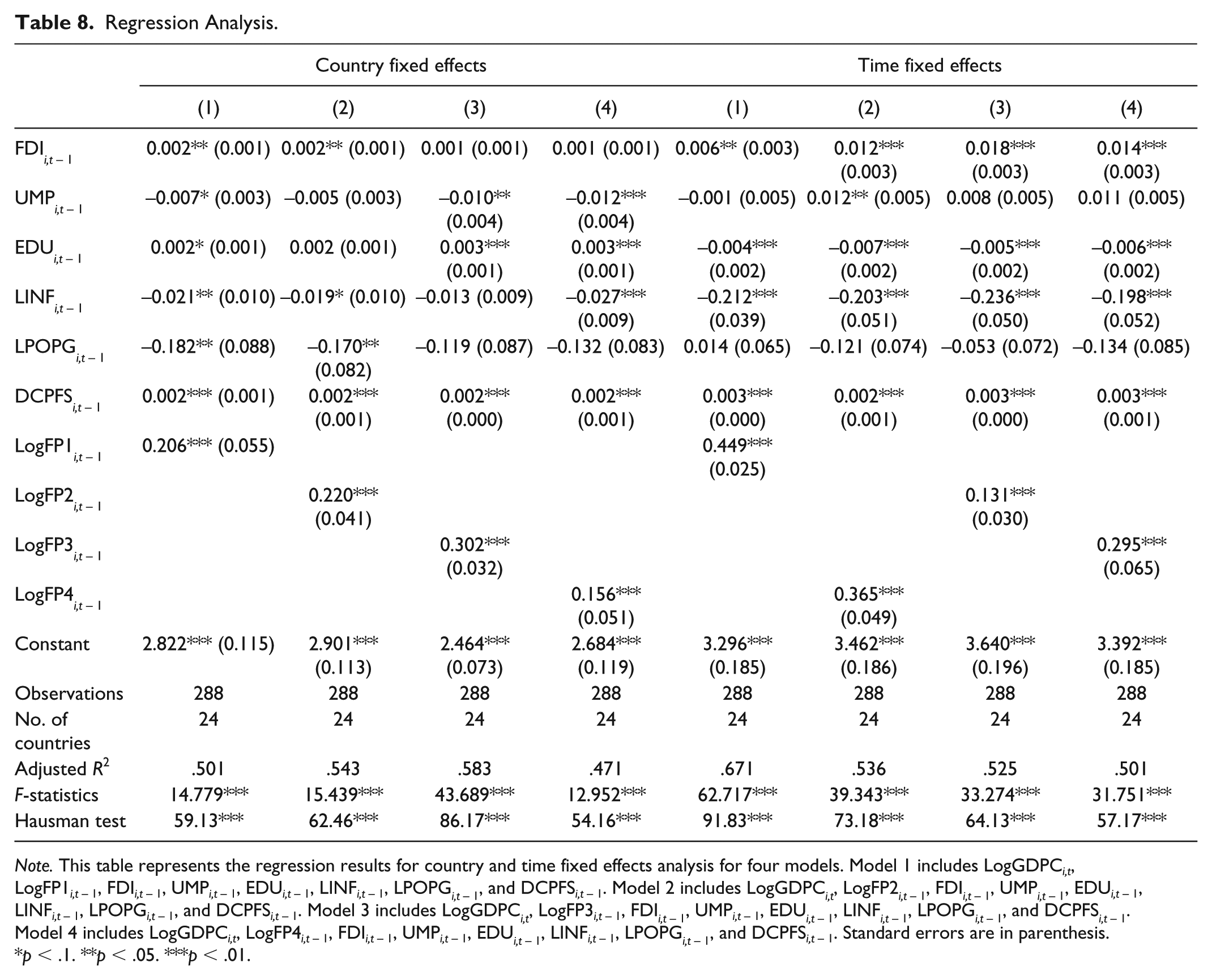

The results of Dumitrescu and Hurlin (2012) Granger non-causality test (see Table 7) explain that our model contains reverse causality or simultaneity. To counter this reverse causality or simultaneity that may cause endogeneity, we use 1-year lag of independent variables in our regression model following the studies of Lin (2014), Rugman et al. (2009), and Xie and Li (2013). The optimal number of lags was 1 (k = 1) selected using AIC. Table 8 presents the results of country and time fixed effects regression techniques for four regression models, separately. Based on the findings of Hausman (1978), we conducted the fixed effects regression analysis. The fixed effects regression explains 47% to 58% of the variations in economic growth of Asian countries, whereas time fixed effects regression explains 50% to 67% of the variations.

Regression Analysis.

Note. This table represents the regression results for country and time fixed effects analysis for four models. Model 1 includes LogGDPC i,t , LogFP1i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, and DCPFSi,t – 1. Model 2 includes LogGDPC i,t , LogFP2i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, and DCPFSi,t – 1. Model 3 includes LogGDPC i,t , LogFP3i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, and DCPFSi,t – 1. Model 4 includes LogGDPC i,t , LogFP4i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, and DCPFSi,t – 1. Standard errors are in parenthesis.

p < .1. **p < .05. ***p < .01.

Furthermore, we find a significant positive relationship between economic growth and all four proxies of financial permeation at 1% after controlling for country as well as time fixed effects. These results explain that an increase in the number of commercial bank branches per 100,000 adults, number of commercial bank branches per 1,000 km2, outstanding deposits with commercial banks to GDP, and outstanding loans from commercial banks to GDP stimulates economic growth, irrespective of country as well as time. Our estimated findings are consistent with the findings of Inoue and Hamori (2016) and Kim et al. (2018). We also find a positive relationship between share of net FDI to GDP and economic growth for Models 1 and 2 of country fixed effects regression and all four models of time fixed effects regression. This positive relationship, which is similar to the findings of Solarin and Dahalan (2014), explains that an increase in FDI increases economic growth in Asian countries. Furthermore, we find a negative relationship between unemployment rate and economic growth for Models 1, 3, and 4 of country fixed effects as well as Models 1 and 2 of time fixed effects regression. This negative relationship explains that an increase in unemployment rate decreases economic growth of Asian countries. Furthermore, we find a negative relationship between inflation rate and economic growth for Models 1, 2, and 4 of country fixed effects regression and all four models of time fixed effects regression. We also find a negative relationship between population growth and economic growth but only for Models 1 and 2 of country fixed effects regression at 5% significance. These negative relationships explain that an increase in inflation rate and population growth decreases economic growth in Asian countries. Moreover, we also find a significant positive relationship between domestic credits provided by the financial sector and economic growth for all four models of country fixed effects as well as time fixed effects regression. This positive relationship explains that the developed financial institutions also stimulate economic growth.

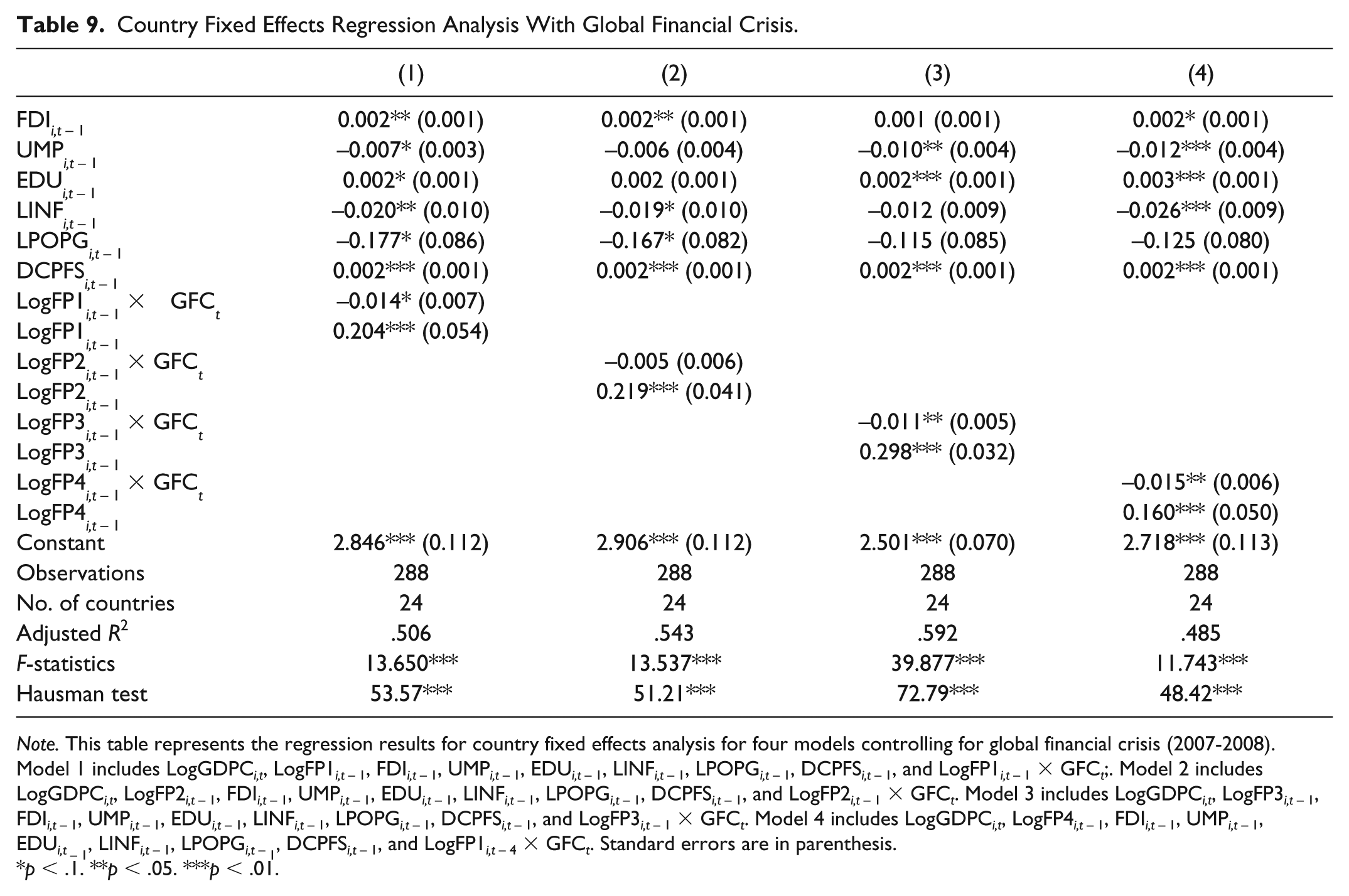

Table 9 presents the results of country fixed effects regression techniques for Equation 2. We include a time dummy (GFC t ) interaction variable for 2007 and 2008 to control for the impact of global financial crisis.

Country Fixed Effects Regression Analysis With Global Financial Crisis.

Note. This table represents the regression results for country fixed effects analysis for four models controlling for global financial crisis (2007-2008). Model 1 includes LogGDPC i,t , LogFP1i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, DCPFSi,t – 1, and LogFP1i,t – 1 × GFC t ;. Model 2 includes LogGDPC i,t , LogFP2i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, DCPFSi,t – 1, and LogFP2i,t – 1 × GFC t . Model 3 includes LogGDPC i,t , LogFP3i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, DCPFSi,t – 1, and LogFP3i,t – 1 × GFC t . Model 4 includes LogGDPC i,t , LogFP4i,t – 1, FDIi,t – 1, UMPi,t – 1, EDUi,t – 1, LINFi,t – 1, LPOPGi,t – 1, DCPFSi,t – 1, and LogFP1i,t – 4 × GFC t . Standard errors are in parenthesis.

p < .1. **p < .05. ***p < .01.

We find significant results of this dummy interaction variable for Models 1, 3, and 4, explaining the negative impact of financial crisis on economic growth of Asian countries which is similar to the results of Asteriou and Spanos (2019). However, the impact of financial permeation on economic growth remains positive and significant. These positive/negative relationships explain that although global financial crisis reduces the positive impact of financial permeation on economic growth of Asian countries, its impact was not very much significant. The plausible reason for this less significant negative impact may be that the origin of global financial crisis was the United States and its foremost impact was in the United States and Europe. Asian countries also faced its consequences but the impact was very low as compared with the United States and European countries.

Conclusion

Asian countries are the fast-growing developing economies as compared with the other economies in the world. Although the level of financial permeation in Asian countries is low, governments of these countries have articulated and adopted financial inclusion policies to attain inclusive economic growth and as such the level of financial permeation is also growing in these economies. Using the panel data of 24 Asian countries for the period from 2004 to 2016, this research empirically explored whether financial permeation contributes to economic growth of the Asian region. Findings show that access to finance indicators and usage indicators have significant positive effects on economic growth of Asian countries. Therefore, we argue that financial permeation promotes economic growth of Asian economies. Accordingly, in terms of policy implications, we recommend that Asian countries’ governments should develop and implement supportive policies to magnify financial permeation through commercial banks as a way of achieving sustainable economic growth. For instance, they can assist banks to increase the level of penetration and eradicate access blockades while maintaining banks’ profitability. These include a reduction in cost of financial transactions and ensuring conducive environment to the financial system. Policymakers can make policies to connect with financial technology providers, FinTechs, to provide digital financial services which will allow banks to offer low-cost products and services to all including individuals in remote areas, which in turn will raise the level of financial permeation. We also detected that schooling has significant positive impacts, whereas unemployment has negative effects on economic growth. Thus, we contend that, to accomplish sustainable growth, governments and policymakers of Asian nations should focus on the proliferation of education as well as employment level of the countries.

The key implication of this research is that it will generate notable attention of governments and policymakers of the Asian region to carry out such plans and policies to form more facilitating atmosphere for financial inclusion, which eventually will stimulate inclusive and sustainable economic growth of countries. Although this research made a wide-ranging exertion on inspecting whether financial permeation promotes economic growth, the main limitation of this study is that we have used 12- to 13-year dataset which is not enough to make a decision in the long run. Also, data scarceness on other indicators of financial permeation such as ATMs per 1,000 km2, data relating to Microfinance Institutions (MFIs), was a gigantic issue. Therefore, upon availability of data, future research might include these measures of financial permeation which will make the findings more inclusive and robust. Our study focused only on the association of financial permeation on economic growth which calls for further investigation on regulatory frameworks and financial technologies that could foster financial permeation and make the economic growth more sustainable.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.