Abstract

As the financial condition of most individuals has taken the toll during the COVID-19 pandemic, this study aims to analyze varied risk perceptions owing to dynamic behavioral aspects ingrained in individuals. The study primarily incorporates the impact of COVID-19 induced risk perceptions on psychological bias and its aftermath on perceived investment performance, with gender differences being moderators in the aforesaid relationship. A mix of probability and non-probability sampling has been used to collect data from 1,133 respondents through a structured questionnaire. The partial least square structured equation modeling (PLS-SEM) has been employed as an estimation technique. The findings highlight that risk perception has been significant in affecting the heuristics and prospects. However, it is insignificant in directly impacting the perceived investment performance. However, psychological biases, proxied by heuristics and prospects, were found to mediate the relationship between risk perception and perceived investment performance. Practical implications suggest a judicious combination of risk, return, and behavioral portfolio to stimulate, and upscale investments thereby enhancing the investment momentum to reach pre-covid levels. At the same time, the relevance for society lies in the fact that they need to re-consider their investment portfolio to adjust for uncertainties like COVID-19. Future studies can embark on cross country research to investigate varied risk perception-investment performance relationships prevalent in respective economic settings. Also, studies can explore the variation in findings with respect to different classes of investors that is, experiences, first timers, institutional, influencers and others.

Plain language summary

The purpose of the study is to assess the influence of individuals risk perceptions due to psychological bias on their investment performance. The structured questionnaire was shared with prospective respondents and total of 1,133 responses were received. SEM was used to assess the influence of psychological bias on the relationship of risk perception and investment performance of an individual. The findings highlight that with clear understanding of risk perception, people tend to use few mental shortcuts and focus more on rational decision making and better investment performance. Practitioners/portfolio managers/financial planners can design combinations of risk, return and behavioral portfolio to bring investors back in the market in post covid19 investment scenarios. The researchers can build on the findings of the present study by assessing the longitudinal effect of the heuristics and prospects that influence the investment decision of household investors. In terms of assessment of risk, the studies can be conducted by incorporating various personality traits, cultural influences, family influence, exposure to better investment advice and others such additional variables for having a deeper understanding of differences in the risk perceived by different people.

Keywords

Background of the Study

The unprecedent COVID-19 outbreak has led to phenomenal repercussions in the global stocks and financial markets with significant changes evident in investor sentiments toward the same (Naseem et al., 2021). Research corroborates such socio-economic-political-environmental uncertainties as exogenous shocks, (Eckel et al., 2009; Espinosa-Méndez & Arias, 2021; Fisman et al., 2015) whose aftermath sow seeds of fear and pessimism in investor sentiments. This also paves way for limited appetite for risky assets accompanied by heavy retail selling (A. Y. Wang & Young, 2020). Secondly, a proliferation of optimistic and pessimistic expectations on potential market recoveries from innumerable news sources inundate retail investors with inconclusive evidence on optimal investment strategies (Ortmann et al., 2020). As a result, investors are presumed to behave irrationally due to information asymmetry and inefficient markets, both emphasizing behavioral finance as a prudent rationale for diverse investment decisions (F. Wang et al., 2022). This is because behavioral finance validates and factors in social, emotional, judgmental and cognitive investor capabilities as drivers of investment decisions with variations in risk perceptions specifically harming prudent decision making (Ahmed et al., 2022). (Mahmood et al., 2016; M. Wang et al., 2011)

Extant research also posits that behavioral finance is the apt theory that underpins the systematic psychological process embedding human feelings and cognitive errors on investment behavior (Barberis & Thaler, 2005; Waweru et al., 2008), which in this paper is perceived investment performance. Adding on, Bailey et al. (2011), exert that psychological bias is one of the most vital factors affecting investment decisions. These unavoidable biases prevent the individuals from making rational decisions, thus curtailing efficient investment decision-making. To validate, Chhapra et al. (2018) conclude that psychological bias act as a prominent reason for irrational decisions and poor investment performance. Taking its roots from the prospect theory (Kahneman & Tversky, 1979), perceived investment performance, an obvious outcome of investment behavior, is based on the rationale that individuals prefer wealth maximizing options when they are given an opportunity to choose. However, these behavioral theories contradict the conventional classic Capital Asset Pricing Models (Markowitz, 1952) which posit that markets are efficient and ensure information symmetry. Adding on, Malik et al. (2022) assign several behavioral factors such as heuristics (overconfidence, anchoring, ability bias and herding amongst others), prospects (loss aversion, mental accounting, regret aversion) and market factors explaining investor decision making and subsequently investor performance, the unconscious ignorance of which lead to sub-optimal investment performance (Mahmood et al., 2016).

That said, celebrating its 76th independence in 2022, Indian investors mentality has phenomenally changed from investing in fixed income instruments to stocks and mutual funds. They are also known to be risk averse, collective decision makers and significantly influenced by previous stock performance (Adil et al., 2022). However, as interest rates tanked from early 2010, orientation toward market linked securities are evident. Nonetheless, COVID-19 upended investment behavior especially when SENSEX plunged 31% in 2020 (Mudgill, 2020) due to massive selling spree from foreign and retail investors. As highlighted earlier, behavioral finance theory propounds that individual’s investment decision making is driven by cognitive and emotional elements. These elements are captured by the heuristics and prospects theory, which often influence the individuals to trade irrationally and end up having lower returns (Seetharaman et al., 2017). Nevertheless, the acute paucity of behavioral finance studies in the Indian economic setting and limited evidence of the impact of changing investor risk perceptions on psychological bias, emerge as valid research gaps warranting further research. Prior research has also been emphatic on financial risk tolerance rather than clients risk perception about investments that may jeopardize investment assessments and consequently investment performance (M. Wang et al., 2011). Apart from varying degrees of risk perceptions, every investor has unique motivations, investment purpose, varying levels of cash inflows and outflows as well as inherent personal limitations which lead to dissimilar investment decisions and consequently investment performances (Mahmood et al., 2016).

Interestingly, it is this vacuum that serves as the prime motivator to empirically conduct a first-hand study to explore the mediating effects of heuristics and prospects elements in the risk perception–perceived investment performance relationship. Another novelty of this study is that it considers the subjective dimension of investment performance namely perceived investment performance which pertains to the self-evaluation of one’s investment returns in terms of quality and standards achieved without referring to the objective facts of one’s circumstances, a concept explored in very few research papers (Akhtar et al., 2018; Nareswari et al., 2021).

Therefore, this paper focusses on achieving threefold objectives. Firstly, to assess the relationship between risk perception and perceived investor performance. Secondly to evaluate the mediating effects of heuristics and prospects on relationship of risk perception and perceived investor performance and thirdly, to examine the differences in perceived investment performance between males and females. To achieve the above objectives and to infer the risk perception- investment performance nexus, this paper studies 1,133 respondents, and employs SmartPLS 4 to perform structural equation modeling along with predictive modeling assessment to estimate five testable hypotheses. Results indicate no significant relationship between risk perception and investment performance while the mediation effects of heuristics and prospects constructs stay relevant in the risk perception–investment performance relationship.

The remaining sections of the study are structured as follows. The next section outline the theoretical framework underpinning the adoptability of various psychological bias. The empirical framework is elaborated in the following section, along with highlighting the results in next section. After that discussion has been presented with respect to results, followed by implications and conclusion of research.

Theoretical Framework and Hypotheses Formulation

Ajzen (1991) developed the theory of planned behavior, which gave the framework for understanding the complexities of human social behavior. The theory postulates that attitude, subjective norm, and perceived control predict the behavioral intention to a greater extent. Based on the former, prior research has explored the dynamic role of behavioral biases in investment decisions (Kartini & Nahda, 2021; Mittal, 2022; Zahera & Bansal, 2019). Nonetheless, the risk perception of managers also has a close relationship with investment behavior and such behavioral biases keep many potential investment options un-explored, thus further impacting investment decisions and thereby investment performance. Roberts (2009) stress the pertinence of exploring long term cognitive and psychological traits which have a concrete bearing on investors response behavior. More recently, Kathpal et al. (2021) caution the paucity of research evident in exploring the influence of the aforesaid factors in influencing perceived investment performance. Since many participants exhibit emotions and behavioral patterns, this investment selection becomes quite complex (Riaz et al., 2020; Zahera & Bansal, 2019).

Linking the biases together and establishing that they influence individual behavior, is the master work of Tversky and Kahneman, the pioneers of behavioral finance. In their research about heuristics (Tversky & Kahneman, 1973, 1974) and prospects (Kahneman & Tversky, 1979) they have concluded that multiple aspects influence one’s investment decision, making it rigorous for an investor to have an appropriate risk-return assessment. Concurrently, gender also acts as a vital determinant of perceived investment performance with research evidence on the same being indecisive. To warrant the former claim, Rajasekar et al. (2023) note that risk perception specifically has a close link with gender orientation as males have high resistance toward risk perception as compared to female managers. Additionally, while a certain strand of literature highlights the confidence, rationale, and risk adverse nature of female investors (Gonzalez-Igual et al., 2021), Plieger et al. (2021) assert the heightened self-directedness and risky behavior prevalent in men leading to positive stock market evaluations.

Although several studies (Dangol & Manandhar, 2020; Ishfaq et al., 2020; Kumari et al., 2022; Mahmood et al., 2016) have percolated through the risk perception—investor performance domain, the results have been equivocal either with respect to the relationship of variables used or remained incongruous with the passage of time. Adding to the woes, uncertainties associated with COVID-19 in the form of income instability have persuaded individuals to decipher the prospects of sustaining their earnings, investments, and spending, once again urging an in-depth analysis of differing investor psychology leading to investment decisions.

Risk Perception and Investment Performance

Risk perception is one unique domain of individual decision making entangled in the affective process quagmire, as it assigns the “dependence on feelings, experiences, and intuitions” (Ahmad & Shah, 2022) in cost-benefit judgments, as one of its vital valuation processes (Skagerlund et al., 2020). It is defined as “the citizen’s subjective expectation of suffering a loss in pursuit of a desire outcome” (Warkentin et al., 2002). In the financial arena, it is measured in terms of attitude toward risk which can be either risk absorption or risk aversion (Kahneman & Tversky, 1979). Raut and Kumar (2018) has concluded that risk perception stems from seven behavioral traits evident between two types of investors that is, early-career investors and experienced investors. Their study resulted in heterogeneous (both positive and negative) perceptions regarding the seven behavioral biases. On another note, Parveen et al. (2023) have examined the interlinkages among behavioral biases, investor sentiments, and investment decisions in the stock market during Covid spread era. Their analysis asserted that covid spread has changed investors’ perception, investment decisions, and even the trade volume of the Pakistani stock market. Moreover, Slovic and Peters (2006) assign a cognitive and psychological dimension to risk perception where the former is termed as risk as analysis and the latter is termed as risk as feelings. Risk as analysis relates to the degree of risk comprehension and understanding while the risk as feelings refer to how individuals feel about the risks.

The current study contemplates on adopting “risk-as-feelings” as the apt dimension to consider as it relates to investment decisions which are the outcome of momentary and intuitive reactions to avert impending dangers which in our case is COVID-19 related fears. However, risk perceptions influence individual behavior and can have diverse impacts on perceived investment performance based on the degree and variations in the interpretation (positive or negative) of available information (Shehata et al., 2021). Alluding to the former, T. A. N. Nguyen and Rozsa (2019) contemplate that financially literate and experienced investors exhibit more accuracy in risk perceptions in comparison to inexperienced investors. Here, we argue that individual who employs diligence, rationale, and analytical skills to interpret the risks inherent in the available investment information refrain from risky investment decisions, resulting in enhanced perceived investment performance (Kumar, Pillai et al., 2023; Trang & Tho, 2017). On the contrary, if risk perception evolves from irrational and illogical behaviors, the perceived investment performance will be dissatisfactory due to erroneous and substandard investment decisions. This is where the study of Robinson and Marino (2015) emerge relevant in justifying the role of biased risk perceptions in venture creation decisions. Risk perception has also been studied as a significant mediator between behavioral bias and investment performance (Ishfaq et al., 2020; Wangzhou et al., 2021).The risk perception—perceived investment performance nexus, especially during COVID is underpinned by the prospect theory (Kahneman & Tversky, 1979) which purport that individuals experiencing uncertainties display cognitive bias and risk avoidance behavior and concentrate more on assured gains albeit adopting risk taking behavior during an impending loss.

Furthermore, the paper unveils the moderating effects of gender on perceived investment performance. Prior research has been inconclusive on the former claims as a certain school of thought (Gonzalez-Igual et al., 2021; Hira & Loibl, 2008) argue that males are confident about their investment and risk-taking capabilities and switch to profitable investments from lessons learnt, thus having high levels of perceived investment performance. Another school of thought (Barber & Odean, 2001) reason that women perform better in investment related decisions due to their meticulous scrutiny of individual stocks, therefore foreseeing enhanced perceived investment performance. However insignificant relationships between gender and investment performance were notified by Willows and West (2015), justifying further research on the same. That said, prior research has extensively investigated risk perception as a mediating variable (Wangzhou et al., 2021) or a moderating variable (Ishfaq et al., 2020; Shehata et al., 2021) with Trang and Tho (2017) being the limited few who look subtly into the direct impact of risk perception on investment performance, although being inconclusive about the same. Investment decisions are influenced by the perception of risk, as evidenced by various studies (Hoffmann et al., 2015; L. T. M. Nguyen et al., 2016; Weber et al., 2005). According to Hariharan et al. (2000), individuals tend to allocate their funds to low risk assets when they perceive a higher level of risk, while avoiding high risk assets. According to previous researches of Aren and Zengin (2016) and Keller and Siegrist (2006), individuals who exhibit a lower risk perception are more likely to opt for high-risk stocks as opposed to low-risk deposits when making investment decisions. Surprisingly, explicit information related to gender differences on perceived investment performance remains unexplored. To address this void, the following hypotheses are formulated:

H1: Perceived investment performance differ across genders.

H2: Risk perception has a significant positive affect on perceived investment performance.

Risk Perception and Heuristics

Risk perceptions are pertinent behavior predecessors to prevent or encounter risks, leading to behavioral bias or affective states, better termed as affect heuristic (Slovic et al., 2002). Furthermore, Ahmad and Shah (2022) opinion that heuristic methods enable information search and change the course of problematic situations to facilitate feasible solutions.

The risk perception–heuristic relationship concurs to the affective event theory (Weiss & Cropanzano, 1996) which explain an individual’s subsequent behavior (heuristics bias) as an outcome of the emotions he is going through (risk perceptions). Here we argue that risk perceptions encompass one’s beliefs, values and norms and these perceptions can result in misrepresentations in the form of heuristics (Ritter, 1988). This argument holds strong during the pandemic when investors became paranoid about the undulations in stock movements, thereby resorting to heuristics biases (Shah et al., 2019) to both save time and harness benefits. To reiterate, heuristic bias is a mental shortcut amassed from experience to solve complex issues amidst inadequate information and uncertainties (Ritter, 1988). Thus, the current paper discusses three dimensions of heuristics namely anchoring (Tversky & Kahneman, 1974), herding and overconfidence (Waweru et al., 2008).

Anchoring is a psychological behavior where one heavily bases his/her judgment on prior information or first available information. In the investment domain, this can relate to future investment decisions based on prior knowledge and initial price paid for the aforesaid stocks (Robin & Angelina, 2020). Prior research of Lavin et al. (2019) and Piotrowski and Bünnings (2024) attests the influential effect of anchoring as the most prominent bias in determining investment behavior. Herding is a situation where individuals blindly follow other people’s actions without engaging in any form of analysis or diligence about the actions taken (Kahan et al., 1996). Over confidence on the other hand is a heuristic bias where the investor overestimates his analytical abilities, skills, and financial knowledge whilst self-assuring high returns (Hvide, 2002). Surprisingly, prior literature implies the heightened prevalence of herding and overconfidence during market turbulences especially covid (Azam et al., 2022; Bouri et al., 2021).

Referring to Kahneman and Tversky (1979) who measure risk perception in terms of risk absorption or risk aversion, we propose dual dimensions that risk absorbers with a cognitive risk perception have higher risk tolerance levels and better investment returns (Nur Aini & Lutfi, 2019) and exude heuristic traits such as over-confidence and anchoring and do not succumb to herding behavior. This is because these individuals, with their extensive investment experience and inherent risk-taking behavior, are confident in their decisions which they usually based on their prior experience without following the irrational crowd. However, investors embedding psychological risk perceptions, especially during market shocks like COVID display less confidence whilst displaying both anchoring and herding behavior. Their mental faculties are disturbed and are paranoid about the uncertainties associated with future returns, thereby following the existing crowd, or basing their decisions on the available past investment portfolio. However there has been dearth of studies on the risk perception—heuristics nexus (Ahmad & Shah, 2022; Robin & Angelina, 2020; Skagerlund et al., 2020).

We also argue that the direct relationship noted between risk perception and perceived investment performance does not offer a compelling claim in the absence of a mediator which is heuristic. Piotrowski and Bünnings (2024) implore academicians to intensify their research on heuristics and biases in the context of financial decision-making as existing studies are confined to conditions. Prior research attest that heuristic bias varies from nation to nation (Pompian, 2012) implying that regional and cultural factors have a vital impact on human psychology which is invariably the principal tenet in the prospect theory. In this regard, Wangzhou et al. (2021) have explored the impact of heuristic bias of investors on investment decisions in Pakistan and found a significant positive impact of representative’s biases on investment decisions. Similarly, another empirical analysis conducted by Ahmad and Shah (2022) and Kumar, Islam et al. (2023) argue that risk perception about future investment can mediate the link between heuristic overconfidence and investment performance.

The studies by Salman et al. (2021) reveals the co-movement among risk tolerance, external locus of control, and their impact on heuristic biases and investment decisions. According to Robinson and Marino’s (2015) study, there exists a partial mediation of the relationship between venture formation decision and the overconfidence heuristic by risk perceptions. According to Lim et al. (2018), there exists a mediation effect of risk perception on the association between financial knowledge and investment intention. That said, it is evident that early research ventures in behavioral finance have not delved into the mediating effects of heuristics in the risk perception-perceived investment performance relationship. The present study claims that covid 19 fears and aggravated risk perceptions of averting impending risks and gaining immediate competitive advantage led to cognitive overload and misinterpretations in the form of herding, anchoring and over confidence heuristics (Azam et al., 2022), which in turn significantly impact investment decisions detrimentally due to irrational and cognitive bias embedded decisions (Du & Budescu, 2018) arising from mental short cuts. The hypotheses formulated are therefore as follows:

H3: Risk perception positively influence heuristics.

H4: Heuristics mediates the relationship between risk perception and perceived investment performance.

Risk Perception and Prospects

To reiterate, risk perception is an individuals’ subjective judgment of risky situations and is primarily dependent on the social, cultural, regional, and psychological conditions surrounding the individual. It is here where Kahneman and Tversky (1979) established the prospect theory as an alternative to enlighten individual’s decision-making under turbulent and risky circumstances. For instance, they claimed that people give more weight to confirmed outcomes than probable ones (Hoffmann et al., 2015). Within the field of behavioral finance, risk perception has been viewed from multiple angles of which the general tendency of humans to be risk averse in situations where gains and losses are likely is widely known. Prospect behavior represents the uncertainties attached to investment decisions and rationalizes the inherent factors in financial decisions to avoid impending loss (Frederiks et al., 2015). The current paper discusses three dimensions of prospect behavior namely loss aversion, mental accounting, and regret aversion to explain their emergence from varied risk perceptions which in turn pose as mediators in perceived investment decision making. These act as mental shortcuts applied or used by investors to make fast and easy decisions in complex and challenging situations.

Loss aversion implies that losses are principal decision drivers rather than profits of the same magnitude (Kahneman & Tversky, 1979). It refers to a deviant behavioral condition where individuals exhibit a high degree of risk aversion due to intentions to dissuade from impending losses (Isidore & Christie, 2019), all of which have clearly emerged from some form of negative risk perception (Ahmed et al., 2022). Moving on, regret aversion is a situation when individuals realize, they made a poor option in the past although they could have made one with a better outcome. Kahneman and Riepe (1998) note dual dimensions to regret aversion where the first refers to regret of commission where the investors regret on taking an irrational decision leading to loss with regret of omission being the second dimension which relates to regret surfacing from lack of capitalizing on opportunities. This in turn leads to avoidance in future decision making to prevent the regret of doing so if unfavorable outcomes arise. Due to this tendency, people tend to make very conservative financial decisions out of regret about past hazardous adverse investment decisions (R. H. Thaler & Johnson, 1990) thereby urging them to invest in assured positive contribution plans.

Lastly, mental accounting bias urges investors to evaluate every stock in terms of its value set in ones’ mental accounts they currently belong to. The winning stocks have presumably been stored in a specific mental account with the losing ones being stored in another mental account (Naseem et al., 2021). This suggest that investors influenced by mental accounting do not have a robust portfolio and irrationally discriminate between income and capital returns on investment. This is because they segregate investments into different subjective accounts based on their personal goals which dissuade them from viewing positions that correlate across accounts (Renu & Christie, 2018) thus leading to sub optimal investment decision.

Thus, it can be deduced that risk adverse investors tend to develop varying degrees of loss aversion, mental accounting and regret aversion, the cumulative effect of which can lead to substandard investment decisions (Rehan et al., 2021). The present study also contend that prospects are one of the vital reasons inducing and enforcing the risk perception–perceived investment performance relationship. This is due to varying degrees of loss aversion, mental accounting, and regret aversion arising out of dynamic risk perceptions leading to significant differences in perceived investment decisions. Forlani and Mullins (2000) posit that risk perception pertains to the cognitive processes through which individuals interpret the level of uncertainty and potential for negative outcomes associated with specific actions. Consequently, decision makers who overestimate their abilities are less inclined to avoid risk (Gervais et al., 2011), leading to unsuitable investment choices. According to Rahman et al. (2019), there exists a positive correlation between an individual’s propensity for trust and their financial risk tolerance, indicating that those with higher levels of trust propensity tend to exhibit greater tolerance for financial risk. Till date, prior research has either focused on factors affecting risk perception (Saivasan & Lokhande, 2022; Singh & Bhattacharjee, 2019) with no papers investigating the prospect effects as an after effect of risk perception or the mediating effects of prospects in the risk perception investment decision making relationship. This paper will address the aforesaid gap and the hypotheses formulated are as follows:

H5: Risk perception positively affects the prospects.

H6: Prospects mediates the relationship between risk perception and perceived investment performance.

Methodology

Data Collection

The present study focusses on assessing the mediating impact of psychological biases, proxied as heuristics and prospects, on the relationship of risk perception and perceived investment performance. To assess the hypothesized relationships, a survey methodology was adopted. Sample selection was conducted using a mix of random and snowball sampling technique. The structured questionnaire was personally administered as well as sent through social media platforms, WhatsApp, and emails between the period of March’22 to June’22 as most of the COVID protocols have been used by then which led to opening of colleges, government offices, corporate offices, and others. The questionnaires were also distributed to prospective respondents by visiting banks and shopping malls. Once the respondent completes our questionnaire, we used to request them to kindly share the questionnaire with their colleagues, friends, and relatives for better reach. In this way researchers were able to have wider reach for the present study.

The scope of the survey was limited to the individuals who have invested their income in any investment alternatives be it equity or debt, thus excluding individuals who were not earning or not involved in any kind of investment options. The questionnaire first asked the willingness of the individual to take part in the survey, stressing both anonymity and confidentiality apart from stating that participation is voluntary and does not entail any right or wrong answers. This would reduce the occurrence of social desirability bias and common method variance (Podsakoff et al., 2003). The structured questionnaire was divided into different sections, that is, Section A for items measuring independent variable (i.e., risk perception); Section B focusing on items measuring heuristics and prospects (i.e., mediating variables); followed by Section C for items measuring perceived investment performance (dependent variable). The last section gathered the demographic profile of a respondent, age, gender, investment horizon, and the percentage of income invested.

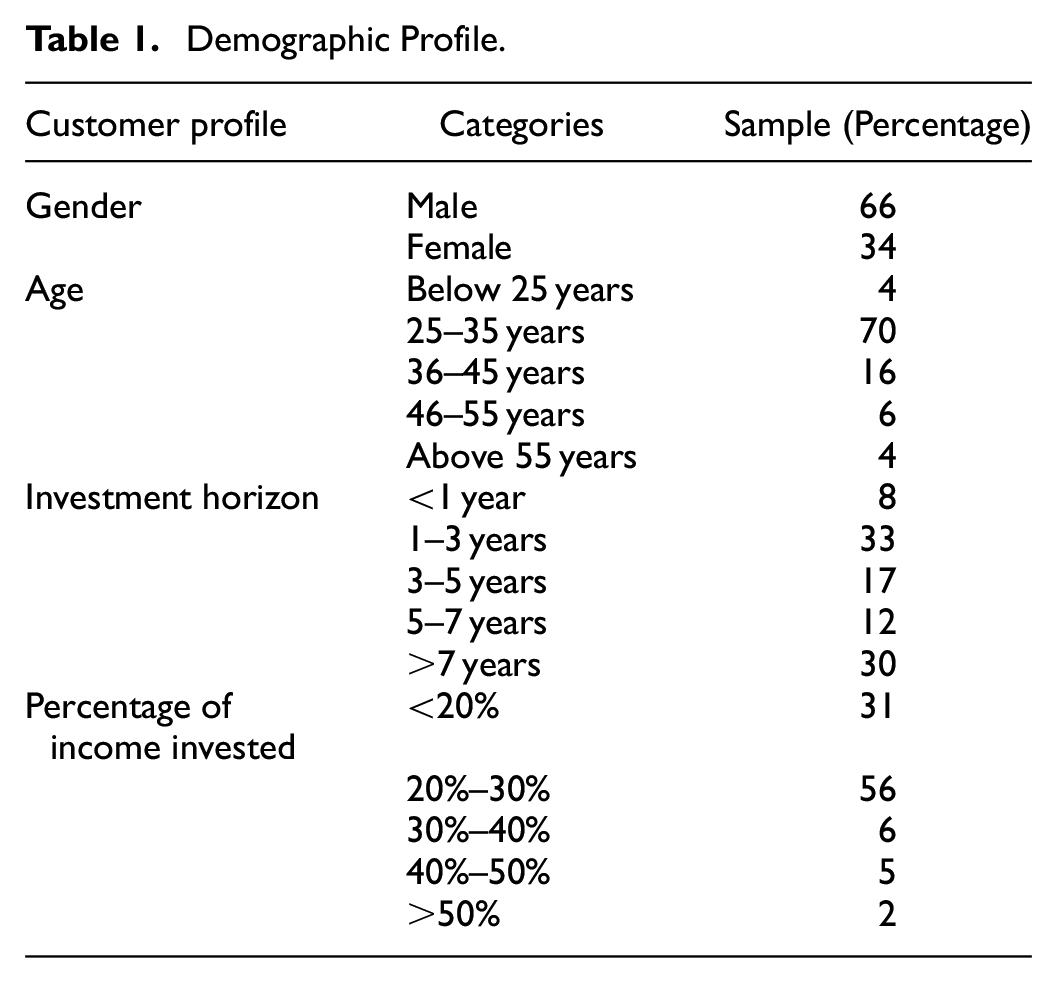

The final sample comprised of 1,133 valid responses. To calculate the minimum sample size requirement for hypothesis testing using PLS-SEM, G*Power software was used. The sample size calculation was based on statistical power of 0.80 with effect size of 0.15 and an alpha value of .05. G*Power estimated the minimum sample size of 103, thus concluding that the present study has the acceptable sample size (Hair et al., 2019; Rasoolimanesh et al., 2017). Table 1 classifies the profile of the respondents as 66% males and 34% females. Most of the respondents were in the age group of 25 to 35 years (70%), followed by 36 to 45 years (16%). Thus, most of the sample comprised of young and middle-aged individuals who regularly invest in various investment avenues. Around 52% of the respondents had child’s education as their major financial objective for making the investments, followed by emergency health needs (20%), child marriage (12%), fund accumulation (9%), and retirement planning (7%). About 50% of the investors had an investment horizon of 1 to 5 years, while 30% had more than 7 years.

Demographic Profile.

Measurement Scales

The data collection instrument for the present study was a structured questionnaire. It was divided into four sections. The first section dealt with items measuring risk perception of an investor independent variable (i.e., risk perception; six items). The second section focused on items measuring heuristics and prospects (i.e., mediating variables) including overconfidence (four items), loss aversion (three items), herding (three items), mental accounting (four items), representativeness (four items), anchoring (four items) and regret aversion (three items). The third part captured the responses of respondents on the items measuring perceived investment performance (dependent variable; three items) (refer annexure 1 for items). The dependent variable is the attitudinal scale for measuring the investor’s investment performance (Le Phuoc & Doan Thi Thu, 2011). The last section gathered the demographic profile of a respondent, age, gender, investment horizon, and the percentage of income invested. The independent, dependent, and mediating variables in the study were measured using the multi-item validated Likert scale of 1 to 5, adapted from the existing literature, presented in Table 2 and annexure 1 (construct wise scale items).

Constructs.

Statistical Procedures

The initial step in the data analysis is to assess the model for the absence of common method bias (CMB). In the present study the same has been assessed using the bivariate correlations between the constructs and the variance inflationary factor (VIF). The bivariate correlations were not found to be excessively high (<0.85) (Lowry & Gaskin, 2014) and all the VIF values were less than 3.3 (Hew & Syed Abdul Kadir, 2016) as shown in Annexure 2. Thus, implying absence of common method bias in the model.

The partial least squares structural equation modeling (PLS-SEM) technique is used to test the theoretical model. According to Hair et al. (2019), PLS-SEM estimates partial model structures by combining the analysis of main components with ordinary least squares regressions. This technique is applied because the model was based on composites; it had second order formative constructs (heuristics and prospect) and is suitable for performing multi group analysis (Rasoolimanesh et al., 2017). The SmartPLS 3.3 was used to assess the conceptual model. As suggested by the PLS-SEM literature, the first step is to assess the validity and reliability of the measurement model. Later, a structural model was developed, and hypotheses were tested using bootstrapping technique. Since the present study involved second order constructs that is, heuristics and prospects, thus measurement model first assessed the reliability and validity of lower order constructs only. After that the latent variable composite scores were saved and the second order model was formed using those scores. Hence, only lower order construct scores will be used as the items to measure the second order construct in this phase and rest all the other constructs would be measured using their standard multi-item measures as in stage one. This process is known as a Disjoint approach for assessing the higher order models (HOC). For conducting the multi-group analysis (MGA), measurement invariance was assessed using the MICOM procedure (Henseler et al., 2016). This was followed by the application of Henseler’s MGA and the permutation test to estimate the multi group analysis results.

Results

Measurement Model

Measurement model was assessed for evaluating the reliability and validity of constructs, for both the groups that is, male and female. The item loadings were studied for assessing the individual reliability and all the loadings except for RP2, RP4, and RP7, were found to be greater than 0.708, that is, threshold suggested by Hair et al. (2019). To assess the construct reliability, Composite Reliability (CR) and Dijkstra-Henseler’s rho (ρA) are reported and presented in Table 3 and Figure 1. Both the CR and (ρA) exceeded the threshold value of 0.70 in the case of all the constructs in both the groups, thus confirming construct reliability. Average Variance Extracted (AVE) was estimated to assess the convergent validity of a construct. In both the groups, AVE values were greater than 0.50 (Fornell & Larcker, 1981). Thus, only RP2 and RP4 were removed due to lower loadings of 0.61 and 0.56 respectively.

Measurement Model results.

Measurement model.

The discriminant validity of the measurement model was assessed using the HTMT ratio. As suggested by Hair et al. (2019) the value of the heterotrait–monotrait correlations should less than .85 or .90. In case of both males and females, PIP and RP have HTMT values less than 0.90 (see Table 4). As the other constructs have presence of high correlation among them and the HTMT ratio also surpasses the conservative threshold of .85, thus confirming the presence of higher order construct.

Discriminant Validity.

The validity of the second order constructs heuristics (anchoring, herding, and overconfidence) and prospects (loss aversion, mental accounting, and regret aversion) were also assessed, to conclude the assessment of measurement model. Both heuristics and prospects were reflective-formative second order constructs. To assess the reliability and validity of the formative order construct, the outer weights must be significant and variance inflation factor (VIF) should be <5 (Hair et al., 2019). Table 5 shows that weights of the lower order constructs were significant and so as their loadings. The VIF values were <5, thus indicating no collinearity issues, hence no indicator was eliminated.

Validity Assessment of HOC.

“*” indicates significant at 5% level of significance.

Multi Group Analysis (MGA)

MGA was conducted to estimate the moderating potential of gender on the perceived investment performance. It is necessary to conduct the MICOM procedure before proceeding with the MGA (Henseler et al., 2016). This MICOM analysis was conducted to confirm that the differences between the male and female are, in fact, due to differences between the latent variables and not to other issues. It is three step process: Step 1—assessment of configuration invariance, in this it is confirmed that models for both male and female has same configuration; Step 2—assessment of compositional invariance, that is, the original correlation is either equal or greater than 5% quantile correlations, thus compositional invariance is established; and Step 3a and 3b—the equality of composite mean values and variances assessment (Henseler et al., 2016). In the present study, the full measurement invariance was established as the equality of the composite mean values and variances was confirmed. The results of measurement invariance is presented in Table 6.

Results of MICOM (Step 2 & Step 3).

The p-values in the last column of Table 6 indicate significance levels of the differences between path coefficients of males and females. Taking the MGA into consideration, the difference in p-values indicated insignificant difference for all the structural paths. It implies that there was no significant difference between male and female perceived investment performance. Hence, the H1 was not supported by the results. The direct effect of heuristics on perceived investment performance is more in case of females as compared to males (β = .218ns → .338*) (refer to Table 7). However, it is insignificant in the case of males. This scenario is different for direct effect of prospect (β = .455* → .396*) which is strong, and significant in case of males. The direct effect of risk perception to heuristics as well as prospects is significant for both males and females, which with strong positive in case of males. Although effect of risk perception on perceived investment performance becomes insignificant in case of both males and females (β = .081ns, β = .024ns). Across both the genders, perception has significant positive mediating impact on the relationship of risk perception and perceived investment performance (β = .374* → .311*). Since the multi group analysis highlighted no significant difference between males and females perceived investment performance, thus the full sample results have been considered for the structural model analysis.

Results of MGA Based on 10,000 Permutations.

“*” indicates significant at 5% level of significance; “ns” indicates not significant.

Structural Model

The proposed structural model was examined using the bootstrapping resampling procedure with 10,000 sub samples. The explanatory power of the combined model was assessed by R2 (Hair et al., 2019) that is, variance explained of the perceived investment performance. The R2 value for perceived investment performance was 46%, which indicates relatively high explanation power (Figure 2). Table 8 also shows the beta coefficients and bias corrected confidence intervals for assessing the combined structural relationships.

Structural model.

Structural Model Analysis of Pooled Sample.

“*” indicates significant at 5% level of significance; “ns” indicates not significant.

In the pooled sample, risk perception has been significant in affecting the heuristics and prospects. However, it is insignificant in directly impacting the perceived investment performance (β = .016ns). The results also highlight that heuristics and prospects positively mediate the relationship between risk perception and perceived investment performance. Since the direct effect between these is insignificant, there is evidence of full mediation. Thus, the findings support H3, H4, H5 & H6, and reject H2. The model predictive relevance was also tested using the Stone–Geisser’s Q 2 calculated using blindfolding technique (Hair et al., 2019). All the Q 2 values are greater than 35%, thus indicating high predictive relevance. The model is also tested for the out sample predictive power using the PLS predict (Table 9). The PLS predict has been conducted with 10-folds and 10 repetitions and concluded that difference of errors, between RMSE of PLS and LM model (naïve benchmark), for all the indicators of perceived investment performance has been negative. Thus, indicating high out sample predictive power in the model.

PLS Predict_Pooled Sample.

Discussion

The current study focused on analyzing the relationship of heuristics and prospects with the risk perception of investors. Also, an attempt has been made to assess the interplay effect of heuristics, prospects, and risk perception on the subjective perceived investment performance of an investor. Moreover, the study contributes to the behavioral science domain for three reasons. For research scholars interested in various dimensions of cognitive influences, this paper introduces the influence of unconventional mechanisms such as heuristics and prospects as unexplored mediators in the risk perception-investment performance relationship. For innovators in behavioral science domain, the finding of this paper will attempt to challenge conventional schools of thought endorsing classical investment theories by defending that the prospect theory better justifies the behavioral biases and risk perceptions that precede investment decision making. The study makes a social contribution by exploring the behavioral biases inherent in the Asian (Indian) investment decision makers that waver them from being rational investors.

The first hypothesis focused on assessing the behavioral demarcations across males and female’s perceived investment performance. The results contradicted the hypothesis formulated, thereby indicating parity in perceived investment performance across both the genders. The results contradict with the study of Gonzalez-Igual et al. (2021) and Plieger et al. (2021), which concluded that risk perceptions vary across the gender and thus the investment performance. However, studies conducted by Dangol and Manandhar (2020) and Ishfaq et al. (2020) purport that males and females think and behave alike in terms of investment performance. This can be associated with increasing number of self-independent females who are being empowered with resources to develop better risk perception, thus narrowing down the investment performance gap among genders.

Risk perception entails a prospective investors outlook toward particular investment instruments, and the basic knowledge one has about risk. Moving on, the risk perception scale focused on assessing the basic outlook of an investor on various aspects such as diversified portfolios, difference between investment and gambling; wealth-investment relationships and age-risk perceptions. This connotes that, if an investor is clear about the risk perception dynamics, then it can directly affect his/her perceived investment performance. As suggested by T. A. N. Nguyen and Rozsa (2019), financially literate investors have a rationale-based risk perception which leads to enhanced investment performance. On the contrary, if risk perception evolves from irrational and illogical behaviors, the perceived investment performance will be dissatisfactory due to erroneous and substandard investment decisions. However, we contend that risk perception in independence does not play a significant role in influencing the perceived investment performance. The same has been contemplated by our study that there is absence of direct significant influence of risk perception on perceived investment performance (H2 rejected), thereby contradicting the findings of Kumar, Pillai et al. (2023) and Trang and Tho (2017). The whole premise of risk perception and perceived investment performance nexus is explored by the prospect theory, which highlight that in the light of risk avoidance and cognitive bias behavior, individuals will take hasty decisions and focus short gains only (Kahneman & Tversky, 1979). Thus, we presume that factors like financial literacy, level of bias, role of heuristics, financial skills, amongst others also play a dominant role in present context on the level of perceived investment performance. Hence, in our study the indirect effect between risk perception and perceived investment performance has been strong and significant.

Additionally, H3 and H5 explored the influence of risk perception on heuristics and prospects. As per results, clarity in risk perceptions implies a sound and judicious application of heuristics and prospects. Hence, both the hypotheses failed to be rejected. Therefore, it is recommended that the investors understand the basic nature and mechanism of risk, base it on scientific and logical backgrounds, which in turn will help in reducing the biases leading to wrong choices. The heuristics theory also claims that because of the risk averse nature of individuals, they inevitably find losses relatively more dissatisfying than an equivalent gain. The risk perception–heuristic relationship concurs to the affective event theory (Weiss & Cropanzano, 1996) which explain an individual’s subsequent behavior (heuristics bias) as an outcome of the emotions he is going through (risk perceptions). Here we argue that risk perceptions encompass one’s beliefs, values and norms and these perceptions can result in misrepresentations in the form of heuristics (Ritter, 1988). This argument holds strong during the pandemic when investors became paranoid about the undulations in stock movements, thereby resorting to heuristics biases (Shah et al., 2019) to both save time and harness benefits. In other words, unexpected fears/events (COVID-19) and aggravated risk perceptions leading to cognitive overload and misinterpretations in the form of herding, anchoring and over confidence heuristics (Azam et al., 2022).

The last set of hypotheses that is, H4 & H6, tested the mediating role of heuristics and prospects into the relationship of RP and PIP. The present study focused on overconfidence, anchoring, herding, representativeness, loss aversion, mental accounting, and regret aversion to explain their emergence from varied risk perceptions which in turn pose as mediators in perceived investment decision making. In our study we fail to reject both hypotheses, that risk perception and perceived investment performance relationship is fully mediated by heuristics and prospects. This confirms with the studies of Rehan et al. (2021), Singh and Bhattacharjee (2019), and Saivasan and Lokhande (2022). The same conclusion was reported by Ahmad and Shah (2022) and Salman et al. (2021) that heuristics can mediate the link between risk perception about future investment and investment performance. Thus, aggravated risk perceptions leading to application of mental shortcuts for having short gains, result in more losses or in other words irrational investment decision making.

Implications, Limitations, and Recommendations for Future Research

There are various implications for the investors, policy makers, and academicians. The investors should focus on assessing and understanding their risk perceptions as it plays a key role in limiting the use of biases in investment decision making. Once the investor is self-aware about ones’ risk perception, instead of using mental shortcuts for short terms goals, they will prefer rational decision making which in turn will increase their investment performance. Also, with enhanced initiatives from policy makers toward investor’s awareness with respect to risk-return nexus and awareness programs for increasing the financial literacy, the investment decision making can further be improved. Policy makers should consider the behavioral aspect of financial decision making and devise strategies to acclimatize investors about the nuances of better financial planning, rational decision making, refraining from short term gains, and focusing on long term investment plans curated as per ones needs. Practitioners/portfolio managers/financial planners can design combinations of risk, return and behavioral portfolio to bring investors back in the market in post COVID-19 investment scenarios. The relevance for society lies in the fact that they need to re-consider their investment portfolio post COVID-19, as the aftermath is likely to remain, and these kinds of uncertainties can come into one’s life anytime.

That said, although the study emerges to be the initiators to study the risk perception—perceived investment performance nexus with heuristics and prospects as mediators, it is not free from limitations. The study extends its focus to the economic setting which encompasses risk mindsets based on cultural, political, and structural frameworks. Future studies can embark on cross country research to investigate varied risk perception-investment performance relationships prevalent in respective economic settings. Secondly, the limited application of demographic moderators, such as gender leads to interpretation of the results from a general perspective. To further this research, academicians can explore the interplay of financial skills and financial literacy nexus on reducing the heuristics and prospects shortcuts while making investment decisions. Also, pre and post study can be conducted to test the effectiveness of investor awareness initiative and financial literacy programs on the younger population to make further inferences.

Conclusion

The present study is envisaged with an objective to understand the nexus between risk perception and investment performance through the lens of heuristics and prospects mental shortcuts. With the help of 1,133 respondents, and the usage of SmartPLS 4 to perform the structural equation modeling along with predictive modeling assessment, the study evaluated five testable hypotheses. It has been concluded that risk perception does not impact the perceived investment performance directly. Rather risk perception and perceived investment performance relationship is mediated via heuristics and prospects. Heuristics was formed with the inclusion of herding, overconfidence, anchoring, while prospects were the combination mental accounting, loss aversion and regret aversion. Both the heuristics and prospects were strongly influenced by the risk perception of an investor. Also, risk perception has been significant in affecting the heuristics and prospects. However, it is insignificant in directly impacting the perceived investment performance. With clear understanding of risk perception, people tend to use few mental shortcuts and focus more on rational decision making and better investment performance. To further extend the findings of the study, future studies should explore initiation of literacy and educational programs, which could enhance the objective and practical risk taking, and reduce the cognitive bias or usage of mental shortcuts. The researchers should focus on assessing the longitudinal effect of the heuristics and prospects that influence the investment decision of household investors. In terms of assessment of risk, the studies can be conducted by incorporating various personality traits, cultural influences, family influence, exposure to better investment advice and others such additional variables for having a deeper understanding of differences in the risk perceived by different people. The present studies have been more inclined toward the individual factors/determinants. However, the external factors like political scenario, market conditions, regulatory frameworks and others should be researched further to estimate the influence of investor decision making capacity. As the present study focus on overall household investors, future studies can explore the variation in findings with respect to different class of investors that is, experiences, first timers, institutional, influencers, and others.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440241256444 – Supplemental material for Risk Perception-Perceived Investor Performance Nexus: Evaluating the Mediating Effects of Heuristics and Prospects With Gender as a Moderator

Supplemental material, sj-docx-1-sgo-10.1177_21582440241256444 for Risk Perception-Perceived Investor Performance Nexus: Evaluating the Mediating Effects of Heuristics and Prospects With Gender as a Moderator by Parul Kumar, Md. Aminul Islam, Rekha Pillai and Mosab I. Tabash in SAGE Open

Footnotes

Acknowledgements

The authors are grateful to all the participants who spared their valuable time in answering the questionnaire.

Author Contributions

Dr. Parul Kumar: Conceptualization, Methodology, Formal Analysis; Prof Aminul Islam: Reviewing and editing; Dr. Rekha Pillai: Conceptualization, Writing – original draft; Dr Mosab Tabash: Reviewing and editing.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.