Abstract

The study is an attempt to find the reasons for biased behavior of overconfident managers while making financial decisions on behalf of shareholders. The study further seeks the ways to resolve the problems faced by firms due to such biased decision-making. For this purpose, quantitative research method is used to uncover the new information for better understanding of study. The comparative analysis has been done through survey-based data collected from executives/managers of firms listed on Pakistan Stock Exchange and New York Stock Exchange. The results indicate that overconfidence bias plays a significant role in managerial decisions for Pakistan compared with U.S. managers. This study applied mediation and moderation tests and found the significant mediating role of risk perception for overconfidence bias and manager decisions. The study further checked moderating role of cultural value, that is, the role of uncertainty avoidance between overconfidence bias of managers and risk perception. Hence, the role of cognitive biases and bounded rationality is undeniable for managerial decision-making and ultimate behavioral cost that firms have to pay due to undesired outcomes of situations. Consequently, this study has reached to extract the hidden facts and solutions to the observed issues for developed and emerging economy’s firms through cultural differences.

Introduction

International financial system and global markets are more resilient than we presume them. Many past and current upsets, for example, dot-com bubble, world wars, depressions, financial crises, and unexpected Trump government establishment, have placed substantial impact on global markets (Mager & Meyer, 2017). Managers in such situations still work hard because of motivation to get some profit on behalf of shareholders. The cognitive and emotional biases of these managers initially lead them to make decisions accordingly (Borchardt, 2010). The limited cognitive ability of managers influences their risk perception (RISKP) in processing of the information related to some problem of firm’s decision. RISKP is more likely creates the positive perceived situation puts the managers to seek for opportunities in a risk seeking manner based on past experiences.

People from diverse cultures might be different in their expectations, choices, and perceptions about risk, cognition, and emotions (Shah et al., 2018), which can be better understood with the help of behavioral finance (BF; Statman, 2008). Braun (2017) put forward the belief that organizational culture significantly affects the RISKP of people. The dimensions of organizational culture predominantly avoid the uncertainty and are an influential factor on manager’s RISKP in a social dynamics (Braun, 2017). Cultural theory has found cultural values to be a predictor of RISKP and risk-taking behavior (Johnson & Swedlow, 2019). Moreover, the firms in a highly globalized environment have a greater need to understand the preferences and priorities of people in other countries. This is the reason that the study has explored and compared the cognitive biases of U.S. managers with firms’ managers in Pakistan keeping in view of their RISKP for firm decisions. The comparative study of developed economy (U.S.) manager’s decisions with underdeveloped country (Pakistan) firm’s managers helps to find the grounds and ways to overcome the issues faced by firm managers in Pakistan.

To make cross-cultural study more elucidating toward behavioral finance, Hofstede’s cultural dimension (uncertainty avoidance [UA]) has been targeted for both the United States and Pakistan. UA dimension of culture was defined by Greet Hofstede as “The degree to which people feel threatened by ambiguous situations, and have created beliefs and intuitions that try to avoid (Hofstede, 1980, p. 4).” Principle argument about culture is that “it is a set of norms, beliefs, shared values, and expected behaviours that serves as guiding principles in people’s lives” (Hofstede, 1980, p. 2). Therefore, it is crucial to create the awareness about cultural differences in perception and preference. In U.S. culture, it is expected to greet one another while arriving at work, whereas in Mexico and Latin America, people discuss little bit family matters along with greeting co-workers. The significance of cultural variation for cognitive judgments and idea of differences in cultural UA might have an impact on RISKP of people.

The decision maker’s verdict revolves around the efficient market hypothesis, whereas in behavioral finance, the decisions are influenced by the heuristics and biases of the decision makers. Based upon the notion of BF and bounded rationality, the psychological information of decision maker is explained by descriptive theories under behavioral decision theory. Biases are systematic deviation from a balance pathway or inclination toward one’s judgment. These behavioral biases of managers are the result of cognitive limitations (Harvey & KoehlerD, 2008). This concept of cognitive limitations and behavioral biases comes under the bounded rationality theory (Aigbovo & Ilaboya, 2019; Slovic, 2002). This study targets the managers’ overconfidence bias (OVERCB) for one’s own self, positive illusions, and illusion of control (Skala, 2008). Managers overestimate their own actual ability, performance, phase of control, and chance of success (Handoyo et al., 2020; Moore & Healy, 2007).

Managers go for optimal financing decisions where they consider the tax benefits and bankruptcy cost. Behaviorists have emphasized on the role of bounded rationality of managers while making these financial decisions on behalf of shareholders. They believe that while making financial decisions, managers may follow pecking order or trade-off theories (Chaffai & Medhioub, 2018; Tomak, 2013). The CEOs of companies make optimal decisions to maintain the balance between financial constraints of firm and excessive liquidity. The inability of manager can affect the financial health of firm and can create organizational financial distress (Bellouma, 2011).

The objective of this research work was to explore the mediating role of RISKP between behavioral bias and firm’s financing decisions in the United States and Pakistan, respectively. Furthermore, it suggests how to cover these shortcomings that increase the performance challenges of firms. Organizations are culturally bounded, and numerous studies emphasized on the importance of culture for corporate (Kwok & Tadesse, 2006; Tang & Koveos, 2008). Most of them employed UA to see the financial performance of organizations. Cultural elements are the rational micro-foundation models of corporate governance and agency theory (Griffin et al., 2015). Keeping in view this situation, it is imperative to further explore the dimensions of culture pertaining to manager’s RISKP for firm’s decisions.

The study has found a major gap regarding its focus on the bounded rationality of managers and the ultimate behavioral cost that managers have to pay in the form of suboptimal decisions. This study has contributed toward the research by comparing the work environments of the United States and Pakistani firms to extract and suggest possible solutions for the role of culture in behavioral decision-making under RISKP. The concept of behavioral cost was given by Shefrin in 2001 where he added that behavioral cost prevents to create firm’s value creation. Furthermore, this cost arises due to imperfections in the emotional and cognitive aspects of managers that endeavor toward the Simon’s concept of bounded rationality. Therefore, it is imperative to locate the concealed dynamics that causes the RISKP to affect the behavioral decision-making of managers. The adaptive nature of financial decision makers is depicted by the decision environment as it may shape the course of action utilized in the financial decision-making (Olsen, 2001). In this regard, the cultural dimension of the decision maker is an important factor that has not been studied deeply in finance previously with respect to behavioral decision-making under RISKP. The subsequent part is conferred with literature review, methodology, and results of data analysis. The final part of the article comprised discussion of results, managerial implications, and conclusion that explains in detail the findings and also provides suggestions for managers facing problems in firm’s decisions.

Literature Review

Managers are often sloganed as corporate agents of decision-making on behalf of corporate owners. Sometimes, their unfolded behaviors, that is, manager’s biases, may affect the underlying decisions taken by them. These biases are further categorized into emotional and cognitive biases. According to Statman (2005), managers were normal in 1945 and they are also normal today rather than being rational as defined by the standard finance, which is enormously confirmed by Bazerman (2005) and Ricciardi (2006). This study has integrated these areas and outlined a framework consisting of behavioral decision theory and RISKP theory for financial decision-making under cultural distress. Risk is inherently subjective and it is independent of minds and cultures (Sato et al., 2020).

Behavioral decision theory under extensive academic history stated that managers may deviate from the systematic pathways of economic rationality by miscalculating (under- or overestimating) probabilities of decision choices due to some noneconomic factors (Rasheed et al., 2018). It has elucidated those aspects of humans that caused professional managers and executives to depart from rational choice during systematic measurement while making decisions for firms. Moreover, such managerial choices are influenced by the perception in a given scenario or situation. This introduced the prominent role of bounded rationality for behavioral finance decision theory (BFDT). Bounded rationality explained by Simon in 1947 and 1956 states that decision-making process of mangers is limited by their unconscious reflex (biases), values (cultural), skills, and habits. These limitations are especially concerned during decisions pertaining to risk and uncertainty.

OVERCB

OVERCB is seen when somebody relies too much on his own judgment, foresight, and abilities. Managers’/executives’ overconfidence may lead them toward wrong decisions. Such biased decisions may result in negative performance of firms. Ben-David et al. (2007) work on OVERCB of executives and found that overconfident executives utilize more long-term debts than short-term debts. Manager’s OVERCB significantly affects their decisions (Mushinada, 2020).

Manager’s Capital Structure Decisions (CSDs)

Previously capital structure theories were based on rational managerial choices. But after the introduction of human psychology, it is evident that managers are subject to some heuristics biases in CSDs (Azouzi & Jarboui, 2012). After the influential work of Modigliani and Miller (1958), the BF approach has revealed useful results in the process of solving decision makers’ behaviors and thoughts. Grezo (2020) in this regard found the strong indirect effect of OVERCB than the direct effect.

Manager’s Asset Management Decision (AMD)

Asset management symbolizes the firm’s liquidity position that demonstrates the difference between current assets and current liabilities of a particular firm. AMDs cover cash, inventory, and receivable management under its umbrella. Maintaining a balanced sum of working capital is a serious challenge for managers in the maximization of shareholders wealth. The excess accumulation leads potential assets to stay idle and their unavailability makes liquidity constraints for firms in needed time. It is evident from previous literature that improper AMDs lead firms toward bankruptcy and real crises (Dunn & Cheatham, 1993). Asset management has been studied by scholars in detail pertaining to its basic characteristics, whereas behavioral aspects of AMDs have been greatly ignored (Belt & Smith, 1991; Zaiane & Moussa, 2018).

Literature is endowed with evidences that financing decisions of managers are affected by OVERCB. Shefrin (2007) and Wang et al. (2018) gave insight into the theory of bounded rationality by arguing that OVERCB may conserve managers from making optimal capital structure. Overconfident managers prefer high debt and they are more prone to increase debt in future. Leverage is considered as debt burden of firm and it raises the future bankruptcy risk, which ultimately increases the investor’s required rate of return. Barros and Silveira (2008) investigated the rationale behind high leverage preference under managerial decisions, and the behavioral experts found that managers with OVERCB are more prone to support leverage by increase of debt financing. Hackbarth (2004) and Oliver (2005) supported the thought by confirming positive significant relation between capital structure of firm and manger’s overconfidence. Shefrin (2001) and Heaton (2002) coined the findings of Uckar (2012) in which he added that OVERCB results into manager’s suboptimal CSDs and less payment of dividends. In the light of above, it is important to further extend the area of BF toward RISKP so that manager’s perception about risk and its impact on firm decisions can be explored.

The future positive cash flows can contribute to mitigate external financing problems and increase the dividend payments. Sloan (1998) said that earning management can be used as a tool to mystify investors and to attract them to invest in overvalued stocks that can assist to augment share price (Moez & Amina, 2018). Nofsinger (2002) put forward the findings that OVERCB causes managers to underestimate the risk factor attached with cash, inventory, and account receivable. He further added that overconfidence can cause managers to exaggerate their abilities and skills to better analyze the situation. Literature further incorporated the details that overconfident managers are daring toward asset management and reserve approach as they prefer to utilize firms inside funds more candidly by overestimating the future performance of firm. Nofsinger (2002) adjoined that managers are provoked by the belief that their firm’s worth is undervalued in the market. He further said that overconfident managers tend to maintain low inventory levels, high receivables, and low cash holdings. Following this, Ullah (2017) maintained the assumption that overconfident managers have negative impact on AMDs of firm. Managers prefer to use inside funds of the firm and ultimately reduce the asset management balance (Heaton, 2002). Malmendier and Tate (2005) and Manandhar (2020) supported the results and established the thought that overconfident managers see external financing more expensive because of the perception about firm’s low market value. As the effect of OVERCB on asset management is imminent, the current study extends the research by testing the mediating role of RISKP to solve the questions raised for OVERCB due to RISKP.

Risk management has been recommended by researchers as an important factor of managerial decisions pertaining to cash management, capital structure, and discount rate decisions (Graham & Harvey, 2001; Zia et al., 2017). Risk plays a comprehensive role in financial decisions and AMDs (Moosa, 2007; Zheng & Shen, 2008). Broihanne et al. (2015) focused on the relationship between risk, agent’s behavioral biases and RISKP, and found that risk is positively related to OVERCB and negatively related to RISKP. Therefore, it can be said that OVERCB is negatively related to RISKP of managers, and high RISKP is further positively related to optimal CSDs. This finding clarifies the mediating role of RISKP between cognitive behavior and decisions, and depicts agency cost of firm. Corporate asset management is another aspect where agents may be the victim of behavioral biases and RISKP. AMDs may pertain to cash, inventory, account receivable, and account receivable management decisions (Belt & Smith, 1991; Kumari & Sar, 2016). Authors have quoted that liquidity position of firm shows the risk associated with financial crises (Vanden, 2010). Keeping in mind the above arguments regarding mediating role of agent’s RISKP in firm’s decision-making under OVERCB, it is worthwhile to mention that improper firm decisions could lead them toward indifferent outcomes.

The role of RISKP and behavioral biases is obvious in managerial decision-making but the role of culture in firm’s decision-making under BF has been ignored by previous literature. The previous literature supported the risk-related cultural values that in turn moderated the relationship between behavioral biases and RISKP of managers. Scholars believe that risk-taking orientation acts as the distinguishing factor among organizational cultures (Deal & Kennedy, 1982). Consequently, firms with moderate risk values take slow but accurate decisions than firms with risky cultural values. Cultural theory of manager’s RISKP covers the individuals, groups, and organizations (Slovic, 1997):

Keeping in view the empirical evidence and theoretical justification, the study developed the following conceptual model. Figure 1 represent the conceptual framework regarding behavioral cost model under bounded rationality.

Behavioral cost model under bounded rationality.

Research Methodology

This article targets CEO/CFO, director finance, chief accountant, managing director, general managers, finance manager, controller, financial project analyst, and treasure in the firms. These firms were from nonfinancial sector and cover the energy and oil, sugar, cement, chemical, textile, and other firms listed at Pakistan Stock Exchange and New York Stock Exchange. As survey-based research work for BF has been supported enormously by researchers both from outside world and from Pakistan (Hassan et al., 2013; Pepper et al., 2010), survey-based data have been collected through questionnaire adapted. The sampling technique used was convenient sampling. Total questionnaires distributed to Pakistani firms were 400, of which 309 questionnaires were received back with a response rate of 77% in total, whereas total questionnaire distributed to U.S. managers were 150, of which only 100 were having information in complete form with a response rate of 67%.

Measures Validity

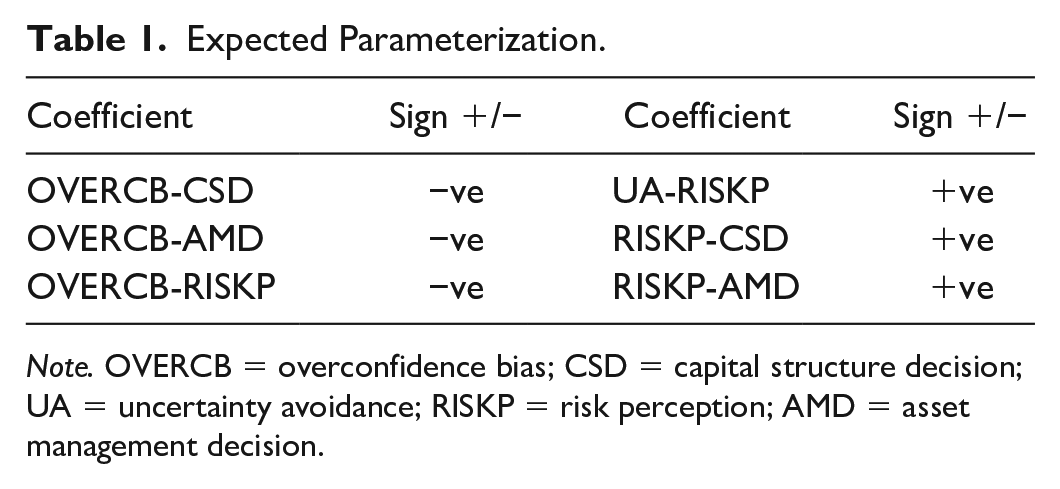

Measures for Overconfidence Bias are used from Svenson (1981), which are further confirmed by (Shiller, 2000; Dorn, and Huberman, 2005). All measures used were on 7 point likert scale where 1 indicates strongly disagree and 7 indicates strongly disagree. In addition to above, Capital Structure Decisions (CSD) and Asset Management Decisions’ (AMD) have been adopted from (Pruitt & Gitman, 1991). All measures used were on 7 point liker scale where 1 indicates Not Important at all while 7 indicates Very Important. Measures used for Risk Perception have been adopted from Mac Crimmon & Wehrung (1990) which is further confirmed by (Simon & Hougton, 1999). All measures used were on 7 point liker scale where 1 indicates very low and 7 indicate very high. Measures for Uncertainty Avoidance in the study have been adopted from Hofstede’s (1980) which are further confirmed by (Wu, 2006). All measures used were on a 7-point Likert-type scale where 1 indicates strongly disagree and 7 indicates strongly disagree. A four-item scale of UA is used to collect managers’ responses. Sample measure adapted in the study is, “I often feel nervous at work.” Cronbach’s alpha for the scale was .75. Table 1 represent the expected relationship between the variables.

Expected Parameterization

Expected Parameterization.

Note. OVERCB = overconfidence bias; CSD = capital structure decision; UA = uncertainty avoidance; RISKP = risk perception; AMD = asset management decision.

Results

Descriptive Statistics

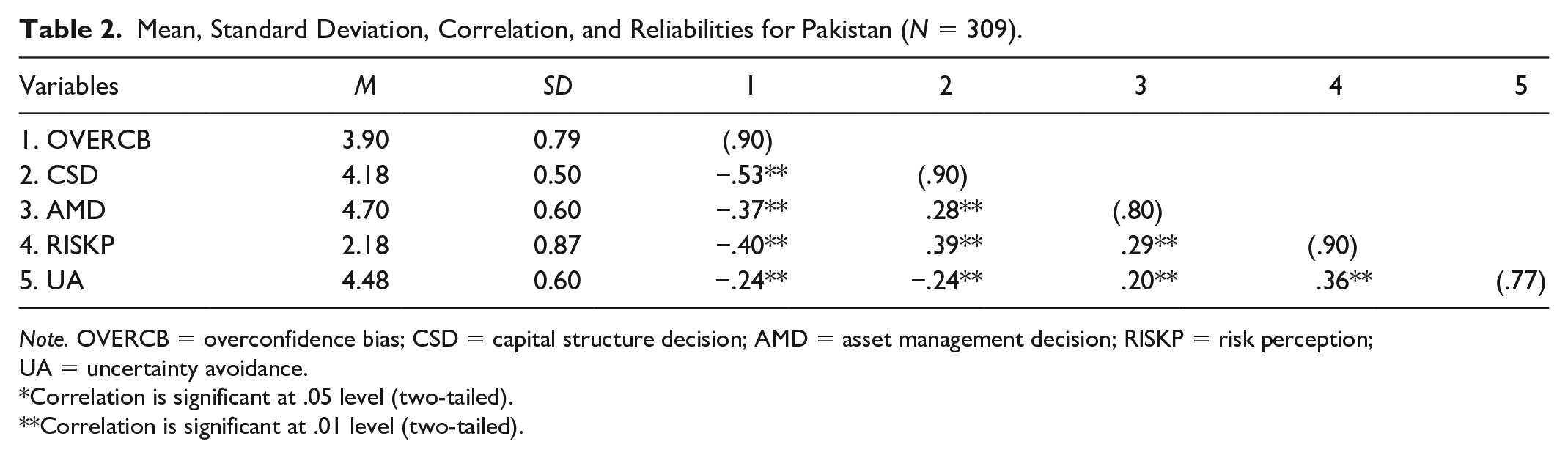

The survey-based study has been conducted to find the relationship between behavioral biases with managerial decisions. Data collected through survey were checked for the presence of any abnormality. Descriptive statistics, including mean, standard deviation, correlation, and reliability, were done for all variables. Table 2 shows the mean value for Pakistan where OVERCB mean value was 3.90 (SD = 0.79).

Mean, Standard Deviation, Correlation, and Reliabilities for Pakistan (N = 309).

Note. OVERCB = overconfidence bias; CSD = capital structure decision; AMD = asset management decision; RISKP = risk perception; UA = uncertainty avoidance.

Correlation is significant at .05 level (two-tailed).

Correlation is significant at .01 level (two-tailed).

In addition, mean values for the rest of variables in Table 2 were as follows: CSD: M = 4.18 (SD = 0.50), RISKP: M = 2.18 (SD = 0.87), and UA: M = 4.48 (SD = 0.60). Correlation results shown in Table 2 explain the bivariate relationship between the variables under study. The results indicated that overconfident managers have negative impact on AMDs (Malmendier & Tate, 2005; Ullah, 2017).

Table 3 shows the mean, standard deviation, correlation, and reliabilities for the United States. The mean value for OVERCB was 4.90 (SD = 0.63) and for AMD was 3.98 (SD = 0.77). Mean and standard deviation for the rest of variables were as follows: CSD: M = 4.10, SD = 0.50; AMD: M = 3.98, SD = 0.77; RISKP: M = 2.21, SD = 0.80; and UA: M = 4.87, SD = 0.55. Correlation results shown in Table 3 explain the bivariate relationship between the variables under study for the United States. OVERCB is negatively related to managers’ CSDs (Uckar, 2012).

Mean, Standard Deviation, Correlation, and Reliabilities for the United States (N = 309).

Note. OVERCB = overconfidence bias; CSD = capital structure decision; AMD = asset management decision; RISKP = risk perception; UA = uncertainty avoidance.

Correlation is significant at .05 level (two-tailed).

Correlation is significant at .01 level (two-tailed).

Correlation Analysis

The correlation result for firms in Pakistan shows that OVERCB is highly significantly positively correlated with CSD (r = −.53). However, OVERCB has a significant negative correlation with AMD (r = −.37), RISKP (r = −.40), and UA (r = −.24). The correlation between OVERCB and RISKP was high compared with other variables. Previous studies also confirm the results depicting that manager’s OVERCB and its relation to variables in the light of risk (Broihanne et al., 2015). Results show the significant positive correlation between CSD and AMD (r = .28), and negative between CSD and RISKP (r = −.39), UA (r = −.24). AMD shows the significant positive correlation with RISKP (r = .29) and UA (r = .20). RISKP was significantly and positively correlated with UA (r = .36). The correlation results for USA firms show that OVERCB has a significant negative correlation with CSD (r = −.29). Moreover, OVERCB is negatively correlated with AMD (r = −.37), RISKP (r = −.23), and UA (r = −.27) and the results were significant. But the correlation between OVERCB and AMD is comparative as compared with the other variables in this correlation analysis (Fabricius & Büttgen, 2015). Result shows that CSD has a significant negative correlation with AMD (r = −.10), RISKP (r = −.24), and UA (r = −.08). AMD was positively correlated with RISKP (r = .59) and UA (r = .48). The results in this correlation analysis show that RISKP is significantly and positively correlated with UA (r = .22). Keeping in view the correlation analysis of both countries, it is clear that overconfidence has a significant correlation with firm’s decisions in Pakistan and in the United States. But this OVERCB is more prevailed among managers in U.S. firms compared with Pakistan.

Regression Analysis

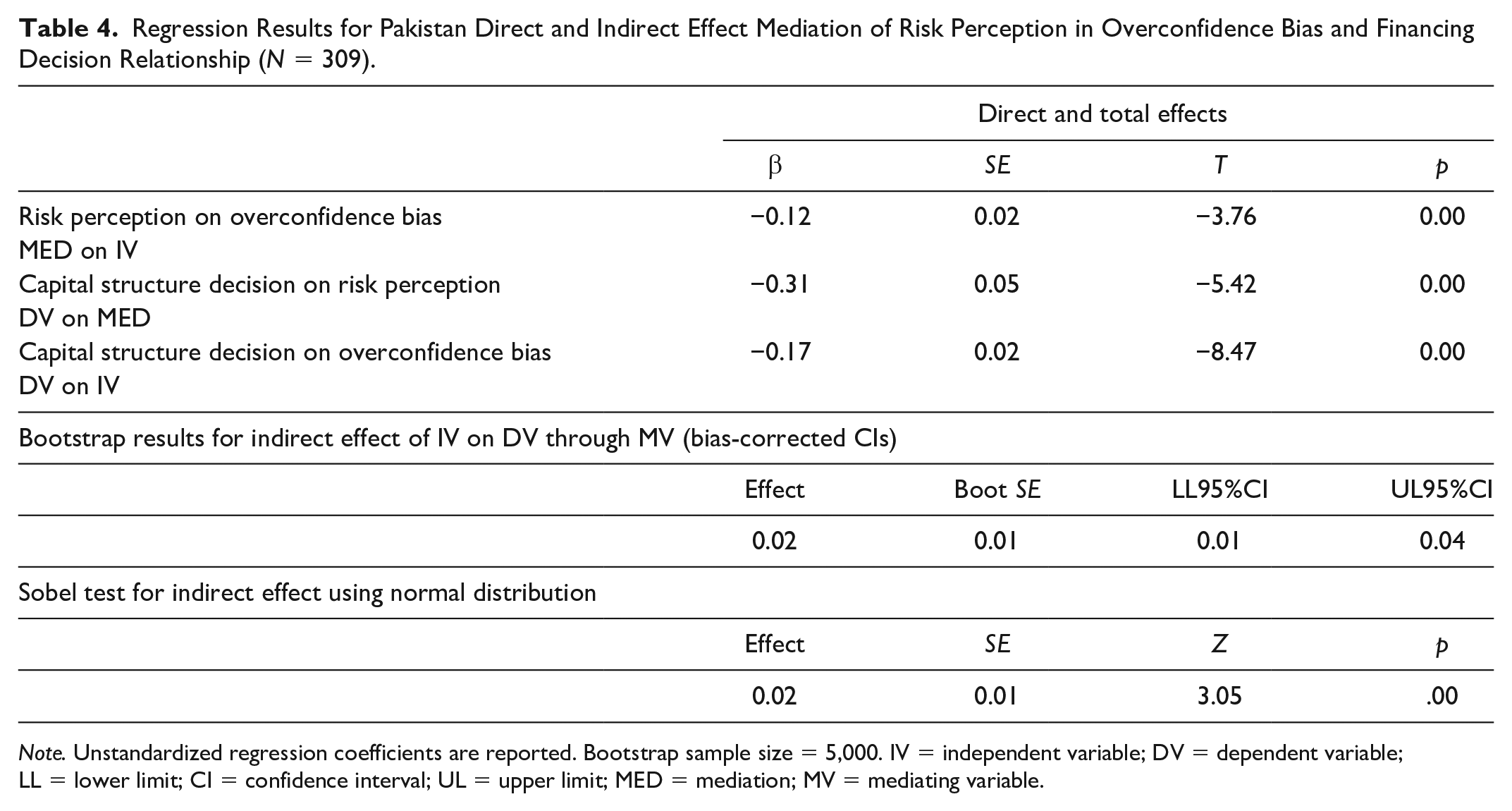

The direct effect has been checked through linear regression analysis prior to mediation and moderation tests for the proposed hypothesis. This direct effect was confirmed through process by Preacher and Hayes (2008). Preacher and Hayes (2008) introduced more convenient method for testing indirect effect through Sobel test. Indirect relationship for mediation has been checked (Preacher & Hayes, 2008). The mediation hypotheses were also tested by bootstrap technique suggested by Preacher and Hayes (2008). Saleem et al. (2018) worked on the theory of bounded rationality in Pakistan and added that managers have tendency to take uncertain decisions based upon certain psychological biases which are the result of manager’s bounded rationality. Under this assumption of bounded rationality, the current study has checked the direct and indirect effect of behavioral biases on managerial decision-making. The results for Pakistan show that OVERCB is negatively related to CSD, which is confirmed by the values in Table 4 (β = −0.17, p < .001). Hence, hypothesis H1 is accepted for Pakistan. The results in Table 5 confirmed the relationship between OVERCB and AMD (β = −0.03, p = .00 < .001); hence, hypothesis H2 is also accepted. OVERCB was negatively related to RISKP in Table 4 (β = −0.12, p < .001). Furthermore, the study confirmed the relationship between RISKP and CSD in Table 4 (β = −0.31, p < .001). But RISKP tends to have a positive relationship with AMD in Table 5 (β = 0.22, p < .001) for Pakistani firms.

Regression Results for Pakistan Direct and Indirect Effect Mediation of Risk Perception in Overconfidence Bias and Financing Decision Relationship (N = 309).

Note. Unstandardized regression coefficients are reported. Bootstrap sample size = 5,000. IV = independent variable; DV = dependent variable; LL = lower limit; CI = confidence interval; UL = upper limit; MED = mediation; MV = mediating variable.

Regression Results for Pakistan Direct and Indirect Effect Mediation of Risk Perception in Overconfidence Bias and Asset Management Decision Relationship (N = 309).

Note. Unstandardized regression coefficients are reported. Bootstrap sample size = 5,000. IV = independent variable; DV = dependent variable; LL = lower limit; CI = confidence interval; UL = upper limit; MED = mediation; MV = mediating variable.

Managers tend to be more risk prone when talking about losses (Marsh & Kacelnik, 2002). Under this assumption, this study extended the research toward the difference between U.S. managers and Pakistani managers to find the indirect effect of behavioral biases on managerial decision-making. In addition to this, the study analyzed the direct relationship of behavioral biases with manger’s financial decision-making. The findings of this study suggested that OVERCB is negatively related to CSD and the results are presented in Table 7 (β = −0.06, p < .001) and resultantly accepted H1. But OVERCB indicates an insignificant relationship with AMD and the results are reported in Table 8 (β = 0.-0.01, p = .20 > .001). Hence, hypothesis H2 is rejected for the United States. The study also examined the direct relationship between independent variables and the mediator. OVERCB was expected to be negatively related to RISKP, which was confirmed by the results in Table 9 (β = −0.17, p < .001). Furthermore, the study found the significant negative relationship of RISKP with CSD and the results are given in Table 7 (β = −0.08, p = .00 < .001). Relationship between RISKP and AMD was significantly positive as indicated in Table 8 (β = 0.11, p < .001) for U.S. firms.

Mediation Analysis

Bootstrap for indirect effects of OVERCB on financing decision through agent RISKP (Pakistan)

Hypothesis H3 proposed the mediating role of RISKP for OVERCB and CSD. Results in Table 4 show that there exists a negative relationship between OVERCB and RISKP (β = −0.12, p < .001) and RISKP and financing decisions (FIND) (β = −0.31, p < .001). However, the direct effect of OVERCB on CSD was also negative (β = −0.17, p < .001). Results also show significant indirect effect as the bootstrap confidence interval (CI) did not take into consideration zero between upper and lower limits (0.02, CI = [0.01, 0.04]). Sobel test for indirect effect using normal distribution was significant for financing decisions (Sobel z = 3.05, p < .00). Consequently, hypothesis H3 is established significantly. The results are supported by work of Hackbarth (2008) that RISKP is inversely related to risk-taking behavior of the overconfident managers and therefore results into suboptimal CSDs.

Bootstrap for indirect effects of OVERCB on AMDs through RISKP (Pakistan)

Hypothesis H4 proposed the mediating role of RISKP for OVERCB and AMD. Results in Table 5 show that there exists a negative relationship between OVERCB and RISKP (β = −0.12, p < .001), whereas RISKP and AMD have positive significant relationship (β = 0.22, p < .001). Results also added to knowledge that direct effect of OVERCB on AMD was significantly negative (β = −0.03, p = .00 < .001). The bootstrap CI considers zero between upper and lower limits (−0.01, CI = [0.14, −0.02]), which explains that indirect effect is significant. Sobel test for indirect effect with the help of normal distribution has also confirmed the significant results of AMDs (Sobel z = −2.23, p < .21). Hence, hypothesis H1 is accepted. These results are supported by findings of previous researchers that RISKP plays a mediating role in the relationship between manager behavioral biases and firm’s decisions in Pakistan (Riaz et al., 2012).

Bootstrap for indirect effects of OVERCB on financing decision through RISKP (United States)

Hypothesis H3 proposed the mediating role of RISKP for OVERCB and CSD. Results in Table 6 show that there exists a negative relationship between OVERCB and RISKP (β = −0.17, p < .001) and significant relationship between RISKP and financing decisions (FIND) (β = −0.16, p < .001). The direct effect of OVERCB on CSD was significant (β = 0.20, p < .001). The significant indirect effect as the bootstrap confidence interval does not take into consideration zero value between upper and lower limits (0.05, CI = [0.03, 0.09]). Sobel test for indirect effect using normal distribution was significant for financing decision (Sobel z = 2.39, p < .001). Consequently, hypothesis H1 is accepted for U.S. managers.

Regression Results for U.S. Direct and Indirect Effect Mediation of Risk Perception in Overconfidence Bias and Financing Decision Relationship (N = 309).

Note. Unstandardized regression coefficients are reported. Bootstrap sample size = 5,000. IV = independent variable; DV = dependent variable; LL = lower limit; CI = confidence interval; UL = upper limit; MED = mediation; MV = mediating variable.

Bootstrap for indirect effects of OVERCB on AMDs through RISKP (United States)

Hypothesis H4 proposed the mediating role of RISKP for OVERCB and AMD. Results in Table 7 show that there exists a negative relationship between OVERCB and RISKP (β = −0.17, p < .001), whereas RISKP and AMD have a positive significant relationship (β = 0.11, p <0 .00). The results also added to knowledge that direct effect of OVERCB on AMD was negative and insignificant (β = −0.01, p = .20). The bootstrap CIs do not consider zero value between upper and lower limits (−0.05, CI = [−0.03, −0.01]), which explains that indirect effect is significant. Sobel test for indirect effect has also confirmed the significant results of AMDs (Sobel z = −2.73, p < .001). Hence, hypothesis H1 is accepted.

Regression Results for U.S. Direct and Indirect Effect Mediation of Risk Perception in Overconfidence Bias and Asset Management Decision Relationship (N = 309).

Note. Unstandardized regression coefficients are reported. Bootstrap sample size = 5,000. IV = independent variable; DV = dependent variable; LL = lower limit; CI = confidence interval; UL = upper limit; MED = mediation; MV = mediating variable.

Moderation Analysis

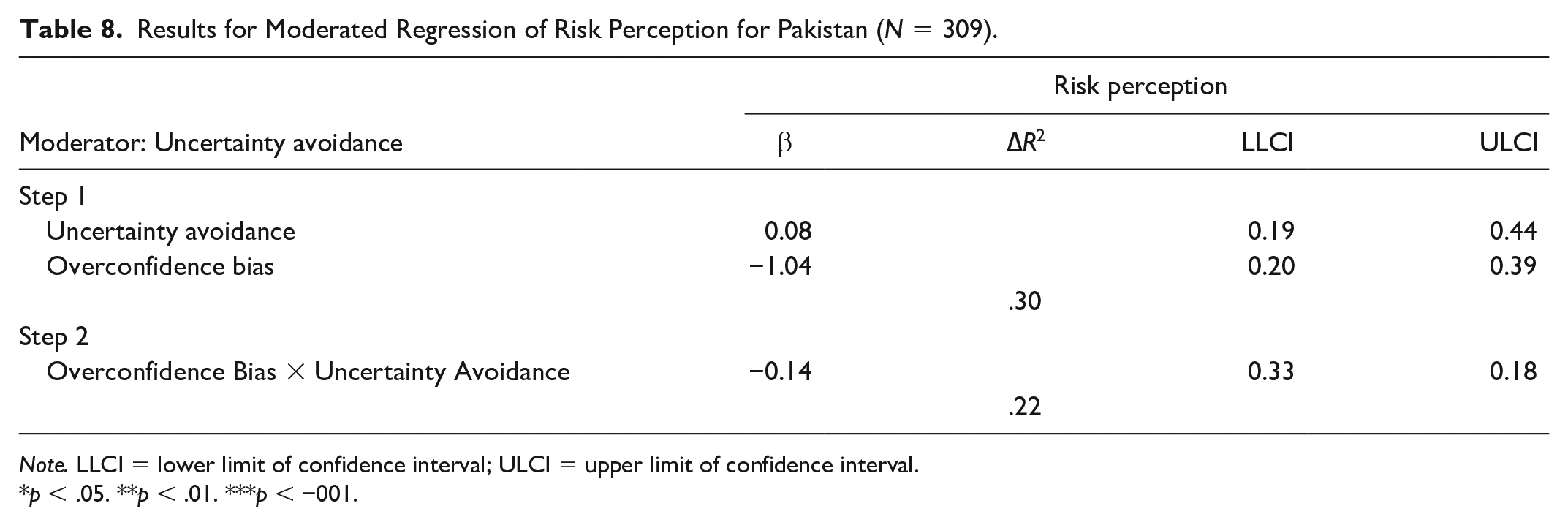

Interactive effect of OVERCB and UA on RISKP (Pakistan)

Hypothesis H5 proposed the moderating role of RISKP between OVERCB and UA. The moderation analysis is done by taking OVERCB and UA in Step 1, whereas interaction term was entered in the second step. RISKP was taken as the dependent variable in this moderation. The control variables were not found to be significant in the results. The results related to the moderation analysis are given in Table 8, which depicts that the interaction term of OVERCB and UA was significant (β = −0.14, p < .005, ∆R2 = .22, p < .005). The slope test also depicted that slope was significant at high (β = 0.32, p < .005) and low level (β = 0.11, p < .005) of UA. Therefore, hypothesis H5 is accepted.

Results for Moderated Regression of Risk Perception for Pakistan (N = 309).

Note. LLCI = lower limit of confidence interval; ULCI = upper limit of confidence interval.

p < .05. **p < .01. ***p < −001.

Interactive effect of OVERCB and UA on RISKP (United States)

Hypothesis H5 proposed the moderating role of RISKP between OVERCB and UA for U.S. firm managers. The moderation analysis is done by taking OVERCB and UA in Step 1, whereas interaction term was entered in the second step. RISKP was taken as dependent variable in this moderation. Results related to moderation analysis are given in Table 9 that depicts the interaction term of OVERCB with UA is significant (β = −0.12, p < .05 = .03, ∆R2 = .09, p = .03). Therefore, hypothesis H5 was accepted. Literature in this regard supports the findings related to moderating role of culture in both countries. People raised in Asian cultures exhibit more behavioral biases than people from the United States (Yates et al., 1998).

Results for Moderated Regression of Risk Perception for the United States (N = 100).

Note. LLCI = lower limit of confidence interval; ULCI = upper limit of confidence interval.

p < .05. **p < .01. ***p < −.001.

Results and Discussions

This study proposed five hypotheses both for the United States and Pakistan, of which five are accepted for Pakistan and four are accepted for the United States. For U.S. firms, overconfidence has a significant direct impact on CSDs but it is insignificantly related to asset management. Moreover, the RISKP was found to be significantly related to all financial decisions. Behaviorists identified that bounded rationality of managerial decisions-making cause managers to deviate from normal pathways (Chira et al., 2008). The evidence from previous research work supports the pecking order theory for Pakistani and U.S. firms. Firms prefer to use internal funds and profits and then use the financing techniques to raise funds at the time of need of money for investment purpose. But the strength of direct effect of overconfidence on financing was stronger in the case of Pakistan than the United States. The study also found that overconfidence is negatively related to RISKP in both countries, which is consistent with Simon and Houghton (2003). OVERCB of managers tends to dwindle the perception of mangers about risk, which in turn mediates the risk-related behavior of managerial decision-making. The study tested the indirect effect of OVERCB on financial decisions of firm managers.

Indirect Effect

The indirect effect shows that RISKP has a significant mediating role on manger’s financial decision-making, which may lead firms to face behavioral cost and ultimately decrease the firm value. Perception of risk goes beyond the individual and it is a social and cultural construct reflecting values, symbols, history, and ideology (Weinstein, 1989). Fabricius and Büttgen (2015) extended the knowledge in this regard by arguing that manager’s RISKP serves as a mediator between OVERCB and risk assessment linked with the decision-making process. The study focused on the mediating role of RISKP between behavioral biases and firm decisions in the United States and Pakistan. Results have been supported by Ricciardi (2008) where he suggests the foundations of RISKP for “psychological aspects” in the areas of behavioral finance, accounting, and economics (Ricciardi, 2008).

CSDs

CSDs are of due importance for the firms to raise capital for future running of business and its growth in times when it could not find sufficient funds from own sources. The study explored the mediating role of RISKP between OVERCB and financing decision of the United States and Pakistani firms. The results showed the significant mediating role of RISKP of managers in the relationship between OVERCB of mangers and CSDs. Shah et al. (2018) worked on the OVERCB of Pakistani managers and found that OVERCB leads mangers to maintain high cash flow and high debt level. Similarly for U.S. managers, Hackbarth (2008) found that managerial overconfidence drives the decisions toward high debt financing in U.S. firms. Results showed that the relationship between OVERCB and financing decision was significantly mediated by RISKP in both countries. But this relation was stronger for U.S. managers in relation to debt financing compared with the Pakistani firms. On the contrary, the mediating role was significant for ambiguity aversion bias but the mediation was strong for Pakistani firm’s managers. This shows that U.S. mangers prefer high debt by perceiving low risk overestimating their abilities. Pakistani managers, on the contrary, prefer to go for debt financing by perceiving more risk related to issuance of equity. Managers who prefer financing underestimate the risk associated with their financing decisions. High uncertainty over the known probability outcomes (RISKP) leads to less leverage, whereas high uncertainty over the unknown probability outcomes (high ambiguity aversion) may cause the managers to take high leverage (Izhakian et al., 2017), which is directly related to bounded rationality theory.

AMDs

Asset management of firm, including cash and reserves, has depicted that it acts as a security for the liquidity shocks that a firm may face at the time of investment or repayment of loans. Cash holding has the due importance that depicts that managerial investment decisions come up with deficit investments (Breuer et al., 2017). The current study targets the indirect effect of agent’s RISKP on the relationship between OVERCB and ambiguity aversion bias with AMDs of managers in Pakistan and the United States. The role of RISKP was found significant for the variables under study. Furthermore, the role of RISKP was stronger for ambiguity aversion bias for both countries. The RISKP of overconfidence managers lead them to perceive the cost of external financing to be low in future because of which they are less concerned about raising cash reserves. Managers with OVERCB perceive low risk to avoid raising cash reserves to finance via debt rather than using its cash holdings because they feel it will be less costly for them (Hackbarth, 2008).

Moderation

The role of UA as moderator was found significant for OVERCB in both countries but the effect was stronger in the case of Pakistan than the United States. Graham and Sathye (2017) worked on the uncertainty cultural dimension of Hofstede for Indonesian and Australian listed firm’s financial decisions. The study argued that uncertainty has influence on economic, social, and legal aspects of financial decisions. Furthermore, the UA is high in Indonesia compared with Australian culture.

Conclusion

The study aims to find the behavioral cost of managerial decisions under RISKP and culture of firms in Pakistan and the United States. The study found significant mediating role of RISKP for behavioral biases and financial decisions. Moreover, RISKP is the determining factor for behavioral cost that firms pay in the form of suboptimal decisions taken by managers. The study established ground-breaking facts concerning the behavioral cost that firms pay due to high RISKP about the decisions in the case of Pakistan while low RISKP in the case of the United States under the moderating effect of managerial cultural aspects. RISKP was a strong mediator between OVERCB and firm decisions in Pakistan rather than in the United States. The moderating effect of UA cultural dimension was found to be present but not robustly. The high leverage ratios are due to risk of bankruptcy and result into a decrease of internal cash flows as observable in Pakistani firm. Conversely for U.S. managers, the strong negative relationship between OVERCB and RISKP signals toward low cash reserves. The managers perceive debt financing to be less costly but among them with OVERCB do high debt financing. The more the firms are capable of understanding the nature of their executives, the better such firms would be able to reduce the behavioral cost and ultimately enhance their performance and growth. The study guides about what interactive steps toward RISKP and cultural variations can secure the firm decisions. Firms can revise their policies to deal with their managers’ OVERCB. Managers can enhance their governance mechanism and ultimately reduce problems faced by them. The study would also help the organizations/principals of manufacturing industries to better understand the behavioral aspects of their managers and their forthcoming decisions pathways. Managers can overcome the psychological challenges in the light of RISKP, which further increase the conflict between the shareholders and management. Future research can be extended through the use of secondary data along with survey-based data to explore new dimensions of research. The research can also be extended toward other biases, especially conservatism bias, so that manager behavior can be compared with OVERCB. Furthermore, the study can be expanded to other countries. The findings would help the multinational firms to expand their business by better understanding the managers in other countries.

Footnotes

Questionnaire

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.