Abstract

Business transformation has become an important way of sustainable development of enterprises. However, the transformation performance is not ideal. Using data from Chinese listed companies from 2001 to 2016, this article employs the Heckman selection model to explore the impact of managerial cognitive bias on transformation strategy and firm performance. The results demonstrate that managerial cognitive bias plays an important role in inducing business transformation. The higher the degree of managerial overconfidence and overoptimism, the more the enterprise will tend to implement business transformation. An important contribution of the article is that it reveals the significant difference between overconfidence and overoptimism: The more overconfident the managers are, the more likely they are to adopt both internal cultivation and mergers and acquisitions (M&A) to realize firm business transformation, whereas the more overoptimistic the managers are, the more likely they are to adopt M&A rather than internal cultivation to realize firm business transformation. Furthermore, business transformation conducted by overconfident managers helps improve firm financial performance and market value, while transformation conducted by overoptimistic managers helps reduce both.

Introduction

Enterprises are increasingly conducting business transformation actively or passively amid the acceleration of economic globalization, the discontinuous progress of technology, the relaxation of government regulations, and ever-changing consumer preferences (Keiningham et al., 2020). In North America, nearly 20% of the continuously growing companies had experienced at least one fundamental change to their core business. In some Asian countries, the economic transition and market-oriented reforms have brought tremendous investment opportunities, encouraging many failing (and even some well-performing) firms to choose business transformation as their principal growth strategy (D. Wang et al., 2016). However, business transformation is not a common type of organizational change; rather, it strengthens a reform after business restructuring and process reengineering have occurred and represents a fundamental adjustment of a firm’s core business. Business transformation may lead to changes in many firm characteristics, such as organizational structure, resource structure, management mode, and enterprise culture, and is thus more systematic and less reversible than are business restructuring or process reengineering and more narrowly targeted, procedural, and revolutionary than is mere diversification (Ilic et al., 2017). The development history of corporations worldwide shows that firms, even industry leaders, can fade due to a failed business transformation.

Against the backdrop of increasing enterprise business transformation despite poor transformation performance, why and how to engage in business transformation have been cutting-edge issues in change management research. Studies on the determinants of business transformation and firm performance tend to overemphasize the corporation and industry characteristics while ignoring the senior manager. These literature note that the recession of industry and declining firm performance are the main driving factors in firms’ business transformation and that corporate business transformation is an adjustment reaction to industrial recessions or product decline based on long-term considerations (Kohnová et al., 2019). Pereira et al. (2019) pointed out that the timely transformation of a core business is a wise choice when an industry can no longer provide enough space for the enterprise to grow. However, in reality, not all enterprises are in declining industries or failing drastically before the transformation, and many blue-chip companies with room to grow are also keen on business transformation. In addition, the choices of transformation strategies and transformation performance seen in many companies with similar operating conditions and industry characteristics differ significantly. Existing theories and findings provide no rational explanation for these phenomena.

The upper echelon theory (UET) developed by Hambrick and Mason (1984) provides new insights for the analysis of corporate business transformation. According to the UET, senior managers are the core factor affecting enterprise development, and their bounded rationality and cognitive bias have a strong effect on strategic choice (Díaz-Fernández et al., 2020). Cognitive bias is a pattern of thinking frequently exhibited in times of uncertainty (Sajid & Li, 2019) and is seen more often among administrators than among non-administrators (D. Wang et al., 2018). We examine the relationships between managerial cognitive bias and business transformation for two reasons. First, managers are firms’ strategic decision-makers, and their cognitive bias will significantly influence the strategic behavior of the company (Dölarslan et al., 2017). Kor (2006) illustrated that the managers often play an important role in directing the major strategy change of a company, and the more drastic the change, the more significant is the effect of managerial cognition. As business transformation is one of the firm’s most important strategic decisions, it may also be impacted by managerial cognitive bias. Second, overconfidence and overoptimism are thought to be the most robust findings in various forms of cognitive bias, and some studies indicate that managers in Eastern countries are more likely to be overconfident and overoptimistic than those in Western countries. For example, cross-cultural studies of overconfidence by Acker and Duck (2008) and Fang et al. (2019) show that the Chinese generally have much higher levels of overconfidence than Americans. Moreover, many specifically Chinese factors, such as the rapidly developing national economy, the promotion of firms’ international status, and the belief in the absolute authority of Chinese traditional culture, will increase managerial overconfidence and overoptimism (D. Wang et al., 2018).

Measures for overconfidence and overoptimism are often conflated in empirical studies (Hribar & Yang, 2016). However, these two types of cognitive bias have substantial differences. Specifically, overconfidence is a cognitive bias generated by an individual’s self-evaluation emphasizing the self-assessment of their abilities, and the objects of the assessment are themselves (He et al., 2019). Overoptimism mainly refers to the individual’s cognitive bias regarding the external environment and events, stressing the individual’s expectation of positive results or conditions, and the objects of the assessment are external events and environments (Kambourova & Stam, 2017). Overconfidence and overoptimism reflect the psychological root of individual bounded rationality from, respectively, the internal and external aspects. Some of the literature has shown theoretically and experimentally that these two forms of cognitive bias may have opposite effects on enterprise behavior. For instance, Astebro et al. (2007) studied the role of overoptimism and overconfidence in the perseverance of investors after receiving advice to stop their business activity; they found that investors were more overoptimistic and overconfidence than the general population and overoptimism is related to continuing to invest after receiving stopping advice, but overconfidence is not related to continuing investment. In addition, overconfident managers are not necessarily overly optimistic. For example, as the founder and CEO of Huawei Technologies Co., Ltd, which became the world’s largest telecom equipment maker in 2013, the media deem Mr. Ren to be an overconfident entrepreneur and insist that Huawei will become a prominent IT enterprise. However, at the same time, he remains pessimistic about the economic situation. Therefore, we attempt to show whether it is possible to empirically differentiate between overconfidence and overoptimism and investigate the impact of each independently on firms’ business transformation strategy and performance. Moreover, in this article, the business transformation strategy refers to the means by which the enterprise enters a new industry: internal cultivation, or mergers and acquisitions (M&A). Although both internal cultivation and M&A are two basic ways for companies to realize diversified expansion, there are essential differences between diversification and business transformation. Business transformation is an enterprise’s realization of fundamental change in its core business by reallocating resources. Diversification strategy is an enterprise’s expansion of its business scope by entering a new industry, but the core business usually does not change. Internal cultivation is an enterprise’s fostering of new business from its seed stage to the incubation and growth stages, depending completely on its own resources and capabilities. In M&A, corporations win ownership of or controlling power over target enterprises through a merger, acquisition, or other methods. In addition, in this article, the M&A here means the mergers and acquisitions between enterprises with different businesses.

Based on the analysis above, using data from non-financial listed companies covering 2001–2016, the authors employed the Heckman selection model to empirically investigate the direct impact of managerial cognitive bias on business transformation behavior and the moderating effects of managerial cognitive bias on the relationships between business transformation and firm performance. This study contributes to the literature in two ways. First, extant studies note that corporate business transformation is an adjustment reaction to industrial recessions or product decline based on long-term considerations, whereas this article highlights the impact of managerial cognitive bias on business transformation strategy and transformation performance. The results obtained in this study show that managerial overconfidence and overoptimism are critical factors that lead firms to conduct business transformations, thus enriching the literature on enterprise business transformation motivation. Second, most studies consider overconfidence and overoptimism as having consistent impacts on firm behavior and fail to distinguish between the two forms of managerial cognitive bias. However, this article finds significant differences between not only the business transformation strategies adopted by overconfident managers and those adopted by overoptimistic managers but also the moderating effects of the two kinds of cognitive bias on the relationships between business transformation and firm performance. This finding both expands the literature on the impact of managerial cognitive bias on enterprise behavior and provides new insights into the decision mechanism of China’s growing enterprises.

Research Hypotheses

Managerial Cognitive Bias and Business Transformation Selection

Setting aside the “rational man” assumption, overconfidence is the main psychological factor influencing administrator behavior. Overconfident managers often overestimate their own capacity and the revenue potential of their decisions while underestimating the risk of their decisions or the probability of failure (Heaton, 2002; Kraft et al., 2017). This psychological bias may have an important influence on a firm’s business transformation decisions. The substance of business transformation is that the firm must establish a new main business that can maintain the firm’s sustainable growth, and its core aim is for the firm to become stronger rather than larger, which means that successful firms improve their quality by improving the efficiency of resource allocation. Meanwhile, the properties and characteristics of the corporation’s core business largely determine the organizational structure, operational patterns, resource investment, and cultural characteristics. Thus, the business transformation will give rise to the reforming and transformation of all these levels (Warner & Wäger, 2019). Failed transformation not only influences firm growth but may also threaten the firm’s existence. Overconfident managers always have some illusions about their knowledge, leading them to overestimate the accuracy of information or their judgment of uncertainty. Driven by this psychology, they firmly believe that they will succeed when faced with high-profitability investment opportunities and thus ignore potential risks and the limitations of the objective conditions during firm transformation, finally leading a firm to pursue business transformation. Thus, we propose the following:

Overoptimism is a cognitive bias frequently discussed by economists (Herz et al., 2014). Overoptimistic managers often overestimate the trend of the macroeconomy, the prospects of securities markets, and the future benefits of investment. As a result, this psychological bias may have an important influence on a firm’s business transformation decisions. Moreover, building a privately owned empire is an important part of the entrepreneurial spirit, and the desire for expansion is a significant aspect of entrepreneurs’ endogenous behavior; it may be even more so for overoptimistic managers. Regardless of whether the economic system is a complete market or involves strong government intervention, all investment decisions and behaviors are carried out based on the development prospects of the firm and the industry. Therefore, the industry’s future and its degree of prosperity are the major factors impacting firm expansion. Modern industry organization theory indicates that an industry’s high Tobin’s Q suggests a high yield advantage and that firms in such an industry can acquire large market power and profits, which is why firms are likely to transfer from an industry with low Tobin’s Q to one with higher Tobin’s Q. Overoptimistic managers believe that their firm’s earning performance is much better than it is (Hackbarth, 2008; Heaton, 2002). Thus, they may overestimate the prospective earnings of the entry industry when there are many investment opportunities, and they may adjust their firms’ major businesses. China’s transition and emerging economy, the investment-driven growth pattern, the huge market requirement potential, and the reform in the competitive field of state-owned enterprises all provide industrial investment opportunities for firms, making overoptimistic managers more inclined to pursue business transformation. Thus, we propose the following:

Managerial Cognitive Bias and Business Transformation Strategy

Transforming a firm’s business through M&A can lower the entry cost for new industries and thus rapidly increase the value of disposable capital (Biggadike, 1979). Firms entering a new industry are faced with many obstacles, including the learning cost of entering a new field as well as rejection by and competition from existing enterprises in the industry. Enterprises need to invest abundant funds to solve a series of problems, such as the development of new products and the establishment of new market channels. Moreover, existing firms make it more difficult for the enterprise to enter the industry because they instinctively resist new competitors. Enterprises that enter a new industry through investment alone bring new capacity, which may influence the balance between supply and demand, thus leading to external excess production capacity and finally triggering a price war. However, enterprises that enter a new industry through M&A can not only rapidly obtain resources that belonged to competitors but also maintain the current competitive structure in the short term, thus lowering the probability of a price war or retaliation in the early stages of the newcomer’s arrival. Thus, M&A is favored by managers during business transformation, particularly by overconfident and overoptimistic managers. According to the existing empirical studies, the reasons can be summarized as follows: First, overconfident CEOs usually think that they have superior decision-making abilities and are more capable than others. This cognitive bias encourages CEOs to engage in highly complex transactions such as diversifying acquisitions (Doukas & Petmezas, 2007); second, the investment of overconfident CEOs is more sensitive to the costs of external finance (Malmendier & Tate, 2015), such as the frequencies of non-diversifying and diversifying acquisitions, and the use of cash to finance a merger deal (Pan et al., 2019). For example, Ferries argued that overconfident CEOs can maximize the use of cash to finance a merger deal (Ferris et al., 2013); third, overconfident CEOs are generally more resilient to risk and optimistic about M&A performance (Pereiro, 2016; Yu et al., 2013). Thus, when manager overconfidence is higher, more possible of the M&A decision is made (Z. Wang, 2017). Together, many theoretical and empirical studies have shown that managerial overconfidence and overoptimism were positively correlated with M&A.

Unlike with M&A, cultivating a new main business through research and development (R&D) investment cannot bring immediate results, but the enterprise can cultivate its core competitiveness, particularly technical skills, after business transformation this way. We hold that, to promote the constant development and expansion of new business during business transformation, overconfident managers are keen not only on M&A but also on technological innovations for several reasons. First, overconfident managers are loyal to shareholders and are active in the firm’s technological innovations. The managerial hubris hypothesis posits that managers are loyal to shareholders (Heaton, 2002) and make strategic decisions based on their confidence rather than self-interest (Michael & Hussein, 2018). Hackbarth (2008) determined that overconfident managers can reduce the principal–agent cost and that their decisions benefit shareholders. Thus, overconfident managers can overcome their short-term psychology and pursue the high returns of R&D investment (S. Wang et al., 2013). Second, the overconfident manager is more adventurous and more willing to take the initiative. It also typically takes a long time to demonstrate an innovation’s effectiveness, and technological innovation comes with considerable risk. Forbes (2005) has shown that overconfident managers are more entrepreneurial than rational ones. Moreover, when making R&D investment decisions, overconfident managers are likely to overestimate the profits and underestimate the risk of failure, thus tending to invest more funds in high-risk technological innovation projects. Third, overconfident managers have illusions of control and use technological innovation to show off their management experience and talent. The extent of managers’ control illusion largely depends on whether they have decision-making power and control ability. Galasso and Simcoe (2011) built a professional attention model of innovation to show that senior managers always exhibit their control over the market via creative actions. Similarly, Salehi et al. (2018) demonstrated that overconfident CEOs are more likely to show their management capabilities and experience through technological innovation. Therefore, overconfident CEOs are more inclined to invest in R&D projects for the sake of more patents and patent citations. Based on the analysis above, we propose the following:

Unlike overconfident managers, overoptimistic managers tend to underestimate market pressure, which lowers the firm’s motivation to build core capability during business transformation. Overoptimistic managers favor market prospects and overestimate the firm’s profitability while underestimating market competition, which can lead to insufficient crisis awareness. As market pressure and crisis awareness are important factors influencing a firm’s core capability construction, the less pressure managers feel, the less motivation they must build capability, and the less R&D investment they make. Based on the pro-cyclical characteristics of capital and an analysis of the opportunity cost effect, Hud and Carreep (2017) found that the firm’s R&D investment is counter-cyclical, suggesting that the enterprise is likely to decrease R&D investment during economic prosperity and increase R&D investment in an economic recession. The research of Dugal and Morbey (1995) also supports this viewpoint. Jean-Sebastien (2010) studied the influence of managerial overoptimism on firm investment using a sample of 777 venture-funded initial public offerings (IPO) firms, showing that overoptimistic managers tend to invest less in R&D and that their R&D investment figure is sensitive to cash flow. Based on the analysis above, we propose the following:

Managerial Cognitive Bias and Business Transformation Performance

Most of the research on managerial overconfidence has followed the “negative–negative” paradigm positing that managers with negative mentalities can negatively impact enterprise value. However, some research has shown that managerial overconfidence is not always negative for the enterprise and can allow managers to dare to do what they were unwilling or afraid to do, thus producing positive income for the enterprise. We hold that managerial overconfidence may contribute to the success of business transformation for three reasons. First, overconfident managers have the courage to overcome the resistance of business transformation. Implementing business transformation redistributes the interests among the subjects of an enterprise, causing much strife and internal struggle and leading to resistance against the business transformation. Overconfident managers usually have a vigorous and resolute style and dare to overcome difficulties (Asamoah, 2017). They firmly believe that their decisions are correct. These personal traits are beneficial for overcoming resistance during business transformation and promoting organizational change. Second, as an important strategic investment behavior during the business development process, business transformation often needs the support of huge capital. Studies have shown that overconfident managers believe that the new business will let the enterprise withdraw cash flow quickly and thus prefer low-cost financing styles such as internal financing and current liability to external financing or long-term liability, which would face the enterprise with high funding costs (Heaton, 2002). Hence, financing decisions made by overconfident managers can lower the cost of business transformation. Third, managerial overconfidence can help enterprises allocate resources rationally during the process of transformation. As the analysis above showed, overconfident managers have the impulse to pursue M&A and technological innovation. The comprehensive application of those two transformation modes can not only accelerate a firm’s business transformation to improve short-term operating states but also contribute to obtaining and maintaining its core competence to promote firm development. Thus, we propose the following:

Unlike with overconfident managers, business transformation implemented by overoptimistic managers will reduce firm performance for three reasons. First, overoptimistic managers will overestimate the macroeconomic and industrial investment opportunities, which may lead them to bring their enterprises into industries weakly related to their main business. Many empirical studies and the practices of enterprises have indicated that the relevance between the original main business and the new main business is positively correlated with transformation performance (Grubljesic et al., 2017). In other words, the lower the relevance between the original main business and the new main business is, the poorer the performance of the business transformation will be, as the enterprise will use the knowledge and capabilities accumulated in the original industry during the process of business transformation. A high degree of business relatedness can help the enterprise promote the utilization ratio of the original resources (e.g., knowledge, technologies, experience, and knack). Second, managerial overoptimism can easily lead to unreasonable resource allocation among the links of the value chain. Due to their weak subjective feelings about the pressure of market competition, overoptimistic managers pay more attention to the speed of business transformation and the scale of the expansion of new business, which will cause enterprises to not only reduce the funds invested in core capacity-building (impeding the healthy development of new business) but also underestimate the risk of business transformation or neglect the control of transformation risk, thus reducing the efficiency of the business transformation. Finally, overoptimistic managers often overestimate the future cash flow of their companies and believe that they will not face a financial crisis (Hackbarth, 2008), leading them to not only choose high-risk debt financing but also issue new debt more frequently, thus increasing the corporation’s financial risk (Bellouma & Belaid, 2016). Thus, we propose the following:

Materials and Methods

Sample and Data

Referencing the research of D. Wang and Song (2010), we first provide a specific definition of “enterprise transformation” according to the industry classification guidance of listed companies formulated by the China Securities Regulatory Commission (CSRC). If the four-digit industry code of the enterprise’s main business has changed, we define the enterprise as a transformation enterprise; if the new main business revenue accounts for more than 30% of the total, we conclude that the company has completed the transformation. Moreover, according to the industry classification guidelines for China’s listed companies released by the CSRC, we selected the enterprises whose new main business revenue accounts for more than 30% of the total as a criterion. Following this guideline, if a business revenue accounts for more than or equal to 50% of the total, we classified this business into the corresponding industry; if no one business has revenue accounting for more than 50% of the total but the revenue accounts of a business are the highest and represent more than 30% of the total, we classified this business into the corresponding industry.

To empirically test the hypotheses proposed in this article, we selected Chinese listed companies from 2001 to 2016 as our initial sample. It is important to note that the revision of the industry classification guidance of Chinese listed companies may reclassify corporate core business, by which the enterprise may be mistaken for a transformation enterprise. To avoid this mistake, we compared each enterprise’s core business before and after transformation during the sample collection. To guarantee the standardization of the sample, we excluded some companies from it: (a) Taking into account the special nature of the balance sheet of financial companies, we excluded financial companies and companies that included financial operating units, and (b) we excluded comprehensive listed companies. According to the industry classification guidelines for China’s listed companies released by CSRC, a comprehensive listed company is one for which the revenue accounts of any business are not significantly higher than those of others, and the revenue accounts of each business are less than 10% of the total. Thus, this kind of company does not have an obvious main business. Because the business-transforming enterprise (a company whose main business has been transformed to another) is the research object of this article, we excluded comprehensive listed companies from the initial sample. As a result, these criteria produced 5,238 observed values. Based on the above samples, we collected the data and information relevant to the main businesses of the samples covering 2001–2016. During this period, 318 companies implemented and completed business transformation.

The transformation mode and the start and end time of the transformation were collected by the authors from the information disclosure website Huge Tide Network (www.cninfo.com.cn). The data on managers’ overconfidence and overoptimism and the data on enterprise performance variables and other control variables were all collected from the China Center for Economic Research database.

Variable Definition and Measurement

Overconfidence

Other than a few documents that use a direct measurement method (Li & Tang, 2010), most of the literature uses proxies to measure the degree of manager overconfidence indirectly, such as CEO stock options (J. H. Lai et al., 2017), CEO’s relative salary (Hayward & Hambrick, 1997), mainstream media coverage of the CEO (Y. H. Lai & Tai, 2019), frequency of M&A (Doukas & Petmezas, 2007), and prior performance of the enterprise (Hayward & Hambrick, 1997). In Western countries, these indicators have good applicability; in China, however, they all have limitations. For example, equity incentives are not a common practice in China’s listed companies; the imperfections of the M&A market make multiple acquisitions uncommon. China’s mainstream media usually focus on the CEOs of large listed companies or famous entrepreneurs and seldom report on the CEOs of middle and small-sized enterprises, including transforming enterprises. In addition, China’s listed companies’ accounting reports disclose the salaries of only the three highest paid executives, not of all executives, preventing us from adopting the method proposed by Hayward and Hambrick (1997). Considering the availability of data and the special circumstances of China’s securities market, we draw from Jiang et al. (2009) and use the ratio of the total salary of the three highest paid executives’ accounts for all executives’ salaries to measure managerial overconfidence; the larger the ratio, the more overconfident the managers are.

Overoptimism

For managers’ overoptimism, most research has used questionnaires to gather data (Tasoff & Letzler, 2014), although some scholars have used a business climate index (Yu et al., 2006) or entrepreneur optimism index (Su & Zeng, 2011) as proxies. Considering the availability of data and the consistency between proxy variables and the connotation of managerial overconfidence, we follow Su and Zeng (2011) and use the entrepreneur optimism index from The People’s Bank of China Quarterly Statistical Bulletin to measure the degree of managerial overoptimism.

Transformation strategy

According to the definition of “enterprise transformation” shown above, a dummy variable (Trans_DUM) is used as a measurement of whether the main business changes (1 for yes and 0 otherwise). Enterprise business transformation methods include internal cultivation and M&A as the two basic types. We used two variables—M&A amount (MA) and presence of M&A (MA_DUM)—as substitution variables for the M&A method and used internal investment (INInvest) as a substitution variable for internal cultivation. Referring to the method proposed by Richardson (2006), we represented the internal investment as payment of cash for building fixed assets and intangible assets – net cash of selling fixed assets and intangible assets. Accordingly, the total enterprise investment (Invest) is equal to the amount of internal investment and the M&A amount, and the index reflects the strength of the enterprise’s transformation motive and the speed of enterprise business transformation to a certain extent. In addition, to study the relationship between the two kinds of transformation methods—M&A and internal cultivation—we set the dummy variable (MA–INInvest) to measure whether the M&A amount is greater than the internal investment.

Transformation performance

Firm performance can be measured using financial performance indicators (such as return on assets and return on net assets) and market value indicators (such as Tobin’s Q value and stock return). The accounting index is comprehensive and reflects the company’s short-term annual operating conditions; the market value index reflects the expected situations of enterprises and measures the company’s long-term performance. Finally, we use two indicators—return on assets (ROA) and Tobin’s Q value—to examine firm performance. Index calculation is as follows: ROA = Net income/Average of initial and final total assets; Tobin’s Q = [Shares outstanding × Current share price + (Total number of shares – Shares outstanding) × Current share price × (1%–82%) + The book value of the debt]/Book value of the assets. In the measurement of enterprise transformation performance, we use the difference value of the year after completion of the transformation and the value of the year before transformation of these two indicators.

Control variable

Enterprise business transformation and transformation performance are affected by other factors. Following the literature (Trad & Kalpic, 2016; D. Wang et al., 2016), we select the following four categories of control variables. For corporate governance variables, we use actual controller, largest shareholder’s shareholding ratio, board size, and senior executives’ shareholding ratio; for financial characteristic variables, we use company size, cash flow, operational risk before transformation, and average performance of companies in the new industry; we use enterprise age and educational background; finally, for virtual variables, we use the year of the enterprise’s transformation and the enterprise’s industry before transformation.

Table 1 provides definitions and measurement methods for the relevant variables.

Definitions and Measurement Methods for Variables.

Note. ROA = return on assets; M&A = mergers and acquisitions.

Models

Empirical studies in strategy research rely on samples of observations that represent fractions of underlying populations. Bias may arise when the samples rather than populations were used to test hypotheses (Certo et al., 2016). The intuition of sample selection bias was routinely described as requiring a two-stage approach (Wooldridge, 2010): in the first stage, determining whether or not an observation in an overall population appears in its final representative sample; and in the second stage, modeling the relationship between the hypothesized dependent and independent variables in the final sample. When an omitted variable produces correlations between the error terms in the two stages, traditional approaches such as the ordinary least squares (OLS) regression may report biased coefficient estimations. To resolve this potential bias, Heckman (1979) introduced the Heckman model, which is a two-step process for data analysis. Because its operation is simple and does not rely on the assumption of normality, the Heckman selection model has gradually become the most popular method to resolve the sample selectivity bias.

In this study, to solve the problem of sample selection bias, an empirical analysis was conducted using the Heckman selection model. In the first stage, a probit model was employed to analyze whether the enterprise implemented business transformation and construct the error correction term, the inverse Mills ratio (IMR). In the second stage, we placed IMR as a control variable into an OLS regression model and analyzed the direct impact of managerial cognitive bias on business transformation behavior and the moderating effects of managerial cognitive bias on the relationships between business transformation and firm performance.

In the first stage, the probit regression model is shown as follows:

This model was used to test H1a and H1b.

In the second stage, observation data of the selection sample

This model was used to test H2a and H2b. When the dependent variables were Trans–DUM, MA_DUM, and MA–INInvest, we adopted the probit model; when the dependent variables were INInvest and Invest, we adopted OLS regression models:

This model was used to test H3a and H3b.

Results and Discussion

Descriptive Statistics, Correlation Coefficient, and Subgroup Test

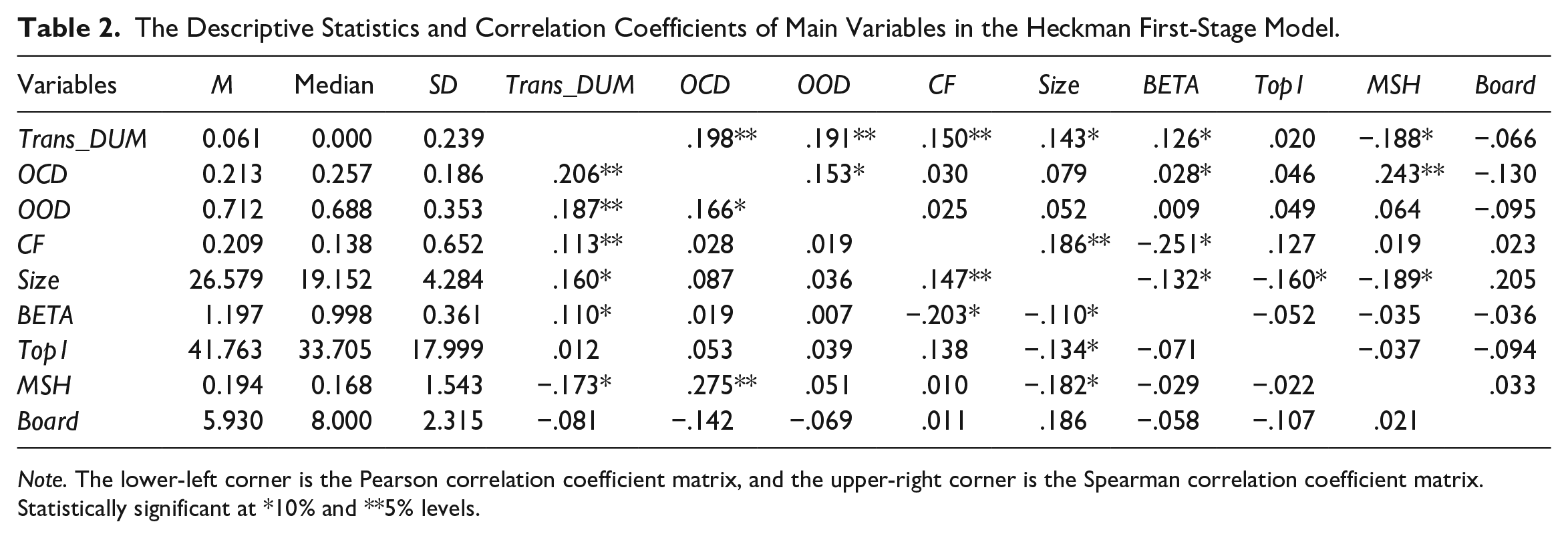

Table 2 reports the descriptive statistics and correlation coefficients of the major variables in the Heckman first-stage model. The data show that the mean values of OCD and OOD are 0.213 and 0.712, respectively, and that the degree of managerial overconfidence and overoptimism is significantly positively correlated with whether the companies implement business transformation or not, which is consistent with the discussion above. Table 3 reports the descriptive statistics and correlation coefficients of the major variables in the Heckman second-stage model. The data show that the mean value of the ΔROA is 1.115, with a standard deviation of 11.271, indicating that the transforming enterprises’ financial performance is relatively good, but there are significant differences among the enterprises. The average of ΔTobin’s Q is –2.689, and the standard deviation of ΔTobin’s Q is 10.580, indicating that the overall market value of the sample enterprises is poor. The differences among the enterprises are also significant in this regard: The mean values of OCD and OOD are 0.368 and 0.825, respectively, both of which are higher than those in the Heckman first-stage model, indicating that the overconfidence and overoptimism of the managers of transforming enterprises are generally higher. In terms of business transformation method, 62.3% of the enterprises used M&A, and 66.5% of their investment amounts are higher than those in internal investment transformations. According to the correlation coefficient, OCD is significantly positively correlated with ΔROA, ΔTobin’s Q, MA, INInvest, and Invest; OOD is significantly positively correlated with MA but negatively correlated with ΔROA and ΔTobin’s Q. These results are consistent with the analysis above. In addition, the absolute value of the explanatory variables’ correlation coefficient is less than 0.3. Therefore, the collinearity problem does not exist.

The Descriptive Statistics and Correlation Coefficients of Main Variables in the Heckman First-Stage Model.

Note. The lower-left corner is the Pearson correlation coefficient matrix, and the upper-right corner is the Spearman correlation coefficient matrix.

Statistically significant at *10% and **5% levels.

The Descriptive Statistics and Correlation Coefficients of Main Variables in the Heckman Second-Stage Model.

Note. The lower-left corner is the Pearson correlation coefficient matrix, and the upper-right corner is the Spearman correlation coefficient matrix.

Statistically significant at *10%, **5%, and ***1% levels.

Table 4 reports the subgroup test results for the characteristics of enterprise business transformation based on cognitive biases.

Packet Inspection of Characteristics of Enterprise Business Transformation.

Statistically significant at *10%, **5%, and ***1% levels.

For managerial overconfidence, the Part A packet inspects whether significant differences exist between the high-overconfident managers sample and the low-overconfident managers sample in terms of M&A, internal investment, total investment, and transformation performance. The inspection methods included a t test and a Wilcoxon test. The data show that, for M&A, internal investment, total investment, and transformation performance, the mean and median of the overconfident managers sample are higher than those of the non-overconfident sample, and the two kinds of inspection are significant. The preliminary result shows that overconfident managers tend to engage in enterprise M&A and internal investment at the same time for business transformation, that their investment scale for business transformation is significantly higher than that of other enterprises, and that the transformation performance of enterprises with overconfident managers is better than that of other companies.

The Part B subgroup tests whether significant differences exist for M&A, internal investment, total investment, and transformation performance between the overoptimistic managers sample and the non-overoptimistic managers sample; the inspection methods are the same as those used for Part A. The data show that, for M&A and total investment, the mean and the median of the overoptimistic managers sample are higher than those of the non-overoptimistic managers sample and that the two kinds of inspection are significant. For internal investment, the mean and median of the overoptimism sample are lower than those of the non-overoptimism samples, but the two kinds of inspection are not significant; for business transformation performance; the ROA and Tobin’s Q of the overoptimism samples are significantly lower than those of the non-overoptimism sample. These preliminary results show that overoptimistic managers tend to engage in enterprise M&A for business transformation and that the investment scale of their business transformation is significantly higher than that of other enterprises but that the transformation performance of enterprises with overoptimistic managers is significantly lower than that of other companies.

Regression Results

Regression results of business transformation selection

Table 5 reported the regression results of the Heckman sample selection model in the first stage; the dependent variable is the dummy variable Trans_DUM—for whether the enterprise implemented business transformation. In the regression of the probit model, we attempted to obtain IMR through four models and apply it to the regression analysis of the second stage. Model 1 was a foundation model comprising variables such as CF, FCR, Size, BETA, Top1, MSH, Board, and Age. Based on Model 1, we introduced OCD and OOD into Models 2 and 3, respectively, and both OCD and OOD were introduced into Model 4 simultaneously.

Regression Results of Business Transformation Selection on Overconfidence and Overoptimism.

Note. The t-statistics are in parentheses.

Statistically significant at *10%, **5%, and ***1% levels.

According to the regression results of Models 2 and 3, the coefficients of OCD and OOD are significantly positive at 5% and 1% levels, respectively, and the adjusted goodness of fit of Models 2 and 3 are 0.41 and 0.40, respectively, both of which are higher than that of Model 1, indicating that the models have higher explanatory power when OCD and OOD are introduced. The regression results of Model 4 show that the coefficients of OCD and OOD are significantly positive at the 1% level, and the adjusted goodness of fit is 0.052, higher than those of Models 2 and 3, indicating that the explanatory power of Model 4 is higher than Models 2 and 3 when both OCD and OOD are introduced simultaneously into it. The above results indicate that the higher the degree of managerial overconfidence and overoptimism, the more likely the enterprise is to implement business transformation; thus, H1a and H1b are supported. As Model 4 has higher explanatory power than Models 1, 2, or 3, we use the normal distribution function estimated by Model 4 to calculate IMR.

Regression results of business transformation strategy

Table 6 shows the regression results of the Heckman second-stage model, whose dependent variable is business transformation strategy. We obtain five regression models by using MA_DUM, MA, INInvest, MA–INInvest, and Invest as dependent variables, respectively; OCD and OOD as key independent variables; and IMR and other correlated variables as control variables. The data in Table 6 show that the IMR of all models are statistically significant, indicating a sample selection bias. It is thus appropriate to employ the Heckman selection model for analysis.

Regression Results of Business Transformation Strategy on Overconfidence and Overoptimism.

Note. The t-statistics are in parentheses.

Statistically significant at *10%, **5%, and ***1% levels.

As the data in Table 6 show, when the model uses MA_DUM, MA, and INInvest as the dependent variables, the regression coefficient of OCD is significantly positive at the 1% or 5% level, but, when the model uses MA–INInvest as the dependent variable, the regression coefficient of OCD is not significant. Thus, the more overconfident the managers are, the more likely they are to use both internal cultivation and M&A to realize firm business transformation. There is no priority between M&A and internal cultivation. When the model uses Invest as the dependent variable, the regression coefficient of OCD is significantly positive at the 1% level, indicating that the more overconfident the managers are, the larger the investment scale of the enterprise tends to be during business transformation. The result above is consistent with the results of the previous subgroup test, which supports H2a.

As the data in Table 6 show, when the model uses MA_DUM, MA, and MA–INInvest as the dependent variables, the regression coefficient of OOD is significantly positive at the 1% level; when the model uses INInvest as the dependent variable, the regression coefficient of OOD is significantly negative at the 1% level. Thus, the more overoptimistic the managers are, the more they tend to use M&A rather than internal cultivation to realize business transformation and the lower the enterprise’s internal investment level tends to be. Moreover, when the model uses Invest as the dependent variable, the regression coefficient of OOD is significantly positive at the 1% level, indicating that the more overoptimistic the managers are, the larger the investment scale of the enterprise tends to be during business transformation. The result above is consistent with the results of the previous subgroup test, which supports H2b.

In the literature, most explanations of the influencing factors in enterprise transformation strategies rely on company and environmental characteristics; performance and industrial decline are viewed as the fundamental factors that lead to enterprise transformation. The deficiency of these studies is that they neglect the influence of managers, especially top managers, on enterprise behavior. For some real-world problems, such as why many companies with good performance and growth favor business transformation or why many enterprises with the same operating conditions and industry backgrounds have significantly different transformation strategies, the existing literature is unable to provide a convincing explanation. This article’s research results show that managers’ overconfidence and overoptimism are important factors in enterprise business transformation but that managers with different psychological characteristics make significantly different choices of business transformation strategy, which not only provides a reasonable explanation for the above problems but also establishes a bridge between corporate executives and business transformation strategy, laying the microeconomic foundation for a growth strategy for Chinese enterprises. From 2001 to 2007, for example, the golden stage of China’s rapid economic growth, gross domestic product (GDP) grew at an average annual rate of 10%, but the average R&D intensity of enterprises conducting business transformation dropped from 1.47% in 2001 to 0.35% in 2007. Since the global financial crisis in 2008, growth in China’s economy has sharply slowed from 9.5% in 2008 to 7.7% in 2012, but the average R&D intensity of transforming enterprises has increased from 0.38% to 2.55%. This article indicates that the negative correlation between enterprises’ R&D intensity and the macroeconomic situation may be occurring for the following reasons. Managers can easily become overoptimistic during a macroeconomic upturn. As their subjective feeling about market competition pressure is weak, they pay more attention to the expansion of enterprise scale and ignore the reengineering of core ability. In a macroeconomic downturn, the market space of enterprises is severely compressed, giving managers a pessimistic attitude toward economic development and enhancing the sense of the urgency of enterprise technology innovation.

Regression results of transformation performance

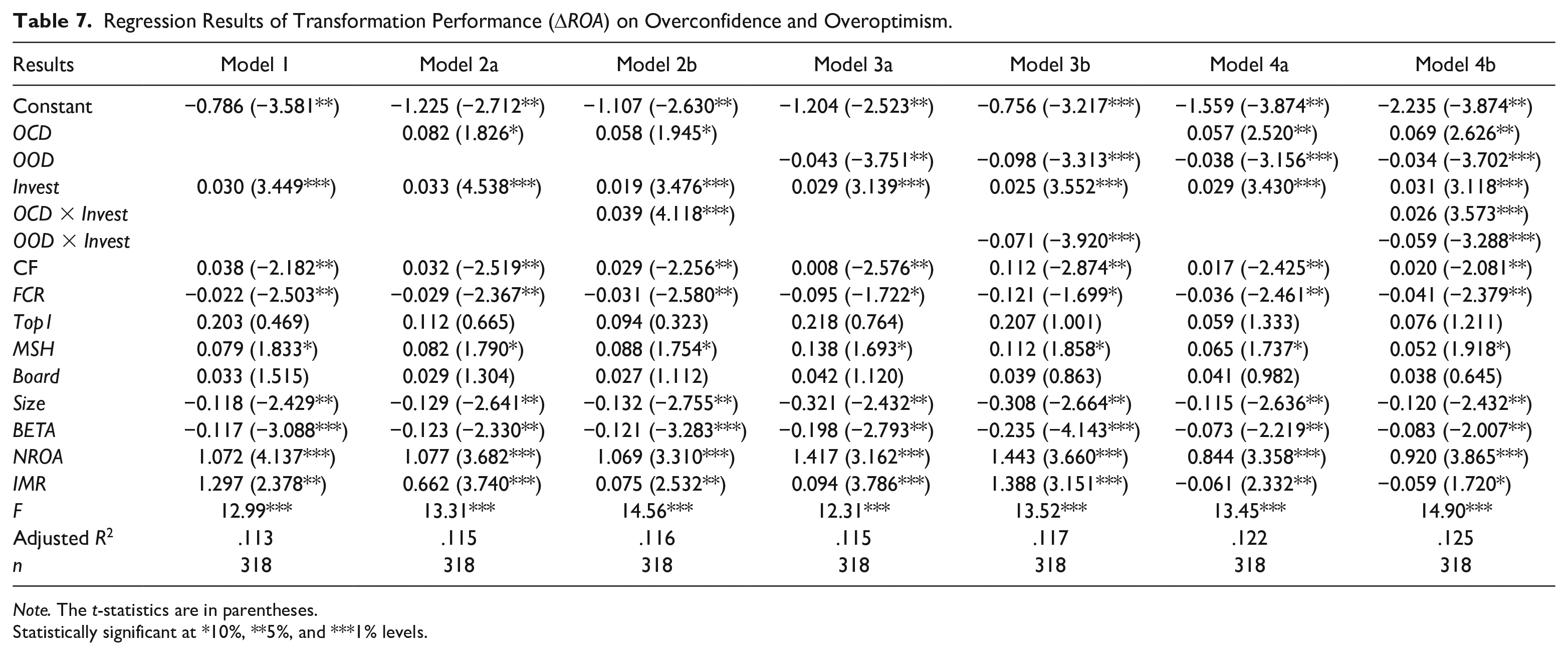

The empirical results above show that managers’ cognitive bias is an important factor inducing enterprise business transformation and that significant differences exist between the business transformation strategies adopted by overconfident and overoptimistic managers. This raises another question: Does enterprise business transformation resulting from managers’ overconfidence and overoptimism affect transformation performance? To address this issue, this article proceeds with a corresponding regression analysis. Tables 7 and 8 report the regression results of a Heckman selection model whose dependent variables are financial performance and market performance. Model 1, a foundation model, reports the effect of control variables (e.g., Invest, CF, FCR, Top1, MSH, Board, Size, BETA, and NROA) on business transformation performance. Based on Model 1, Models 2a and 2b introduce the independent variable (OCD) and the interaction terms of managerial overconfidence with the total investment of the enterprise (Invest × OCD); Models 3a and 3b introduce the independent variable (OOD) and the interaction terms of managerial overoptimism with the total investment of the enterprise (Invest × OOD); Model 4a introduces both OCD and OOD simultaneously. As a full model, Model 4b simultaneously includes OCD, Invest × OCD, OOD, and Invest × OOD.

Regression Results of Transformation Performance (ΔROA) on Overconfidence and Overoptimism.

Note. The t-statistics are in parentheses.

Statistically significant at *10%, **5%, and ***1% levels.

Regression Results of Transformation Performance (ΔTobin’s Q) on Overconfidence and Overoptimism.

Note. The t-statistics are in parentheses.

Statistically significant at *10%, **5%, and ***1% levels.

The data in Tables 7 and 8 show that the regression coefficients of the Invest variable are all significantly positive at the 1% level, which means that, to some extent, investment from managers without cognitive bias can improve firms’ transformation performance when controlling for a number of other determinants. Whether the dependent variable is ΔROA or ΔTobin’s Q, the regression coefficient of Invest × OCD is significantly positive at the 10% or 5% level, and its sum with that of Invest is also positive. Furthermore, the results of the F test are significant, indicating that, during a firm’s business transformation, investment from overconfident managers contributes to the growth of the firm’s financial and market performance and that the more overconfident the managers are, the more helpful the business transformation they implement is in the improvement of the firm’s performance. The results above fully support H3a. Whether the dependent variable is ΔROA or ΔTobin’s Q, the regression coefficient of Invest × OOD is significantly negative, and its sum with that of Invest is also negative. Furthermore, the results of the F test are significant, indicating that investment from overoptimistic managers will reduce the firm’s financial and market performance and that the more overoptimistic the managers are, the more likely the business transformation they implement is to damage the firm’s performance. The results above fully support H3b. These results demonstrate the necessity of distinguishing between the two similar types of cognitive bias (i.e., overconfidence and overoptimism) while also providing empirical evidence for the view in Hirshleifer et al. (2012) that managerial overconfidence does not always have a negative effect on firm performance but can have a positive effect because it also encourages managers to do what they would otherwise be unwilling to do or dare not do. Finally, according to the regression result of Model 4b, the regression coefficient of Invest × OCD is still significantly positive, and the regression coefficient of Invest × OOD is still significantly negative. In addition, whether the dependent variable of Model 4b is ΔROA or ΔTobin’s Q, the adjusted goodness of fit are 0.125 and 0.127, respectively, higher than those of the other six regression models, indicating that the model that takes managerial overconfidence, managerial overoptimism, and the moderating effects into consideration has higher explanatory power.

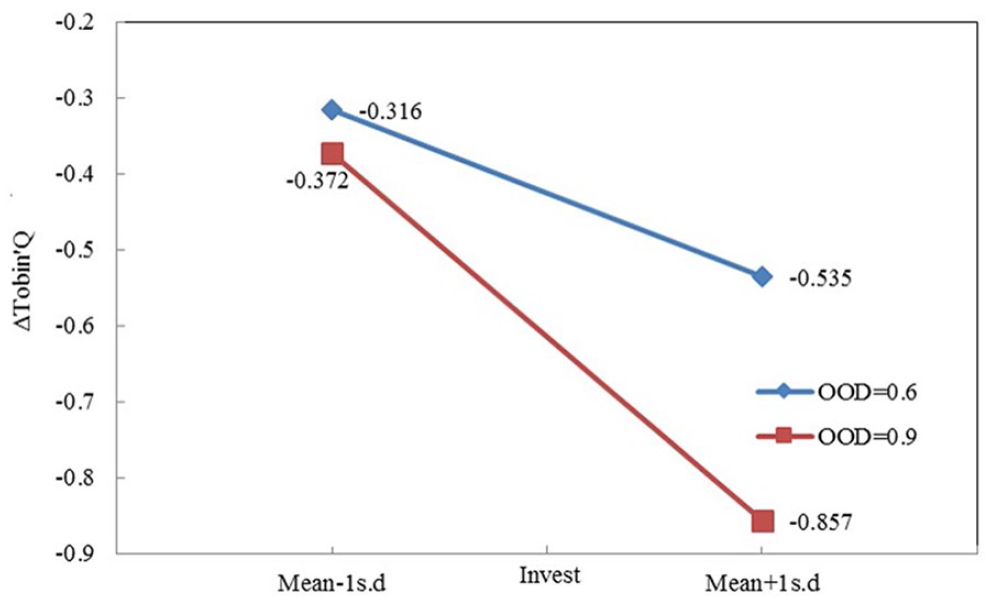

To describe the moderating effect of managerial cognitive bias, which would support H3a and H3b, we follow the method proposed by Aiken and West (1991) and plus and minus a unit of standard deviation on the mean of the independent variable (Invest) and draw Figures 1 to 4 using the data of Model 4b seen in Tables 7 and 8, respectively. Figures 1 and 2 show the moderating effect of managerial overconfidence on the relationships between business transformation and firm performance; Figures 3 and 4 show the moderating effect of managerial overoptimism on the relationships between business transformation and firm performance. In Figures 1 and 2, we can see that, whether the dependent variable of Model 4b is ΔROA or ΔTobin’s Q, the higher the degree of managerial overconfidence, the greater the positive slope of the line segment. This means that the more overconfident the managers are, the more remarkable the positive influence of investment scale on transformation performance tends to be. From Figures 3 and 4, we see that, whether the dependent variable of Model 4b is ΔROA or ΔTobin’s Q, the higher the degree of managerial overoptimism, the greater the negative slope of the line segment. This means that the more overoptimistic the managers are, the more remarkable the negative influence of investment scale on transformation performance tends to be. For managerial overoptimism, if the investment scale of the enterprise is large, the transformation performance of the enterprise whose managers are more overoptimistic will be far below that of the enterprise whose managers are less overoptimistic. These results are consistent with the regression analysis results.

The moderating effect of OCD on the relationship between Invest and ΔROA.

The moderating effect of OCD on the relationship between Invest and ΔTobin’s Q.

The moderating effect of OOD on the relationship between Invest and ΔROA.

The moderating effect of OOD on the relationship between Invest and ΔTobin’s Q.

Robustness Test

In consideration of the lag time of the influence of managerial cognitive bias and transformation strategy on transformation performance, business transformation conducted by overconfident and overoptimistic managers is likely to impact firm performance several years later. Thus, we made some adjustments to the performance equation. First, we define the ΔROA+1 (or ΔTobin’s Q+1) in the second year after business transformation minus that of the year before transformation as the firm’s transformation performance of period t + 1, and the ΔROA+2 (or ΔTobin’s Q+2) of the third year after business transformation minus that of the year before transformation as the firm’s transformation performance of period t + 2. Second, we used the transformation performance of the t + 1 period (ΔROA+1 and ΔTobin’s Q+1) as explained variables, introduced the cross-term of the total investment and the managerial cognitive bias to the model, and conducted another linear regression. Third, we selected the transformation performance of the t + 2 period (ΔROA+2 and ΔTobin’s Q+2) as explained variables and conducted the regression again. The results are basically in line with the former results, indicating that business transformation conducted by overconfident and overoptimistic managers has significant impacts on firm performance in subsequent years. In addition, we chose ROA and Tobin’s Q as substitute variables for performance of the first year after transformation and conducted an analysis of regression. The results show no changes to the basic conclusions. Finally, we revised the measures of overconfidence and overoptimism. We adopted the prior performance of the company as a proxy variable for managerial overconfidence (Hayward & Hambrick, 1997) and, following the method proposed by Y. Wang (2011), measured the degree of managerial overoptimism by matching relations between the investment behavior of the enterprise and macroeconomic fluctuations. The results remain unchanged. Owing to the limitation of the scope, this article does not report those regression results here.

Discussion

The present study shows that, using data from Chinese listed companies from 2001 to 2016, the higher the degree of managerial overconfidence and overoptimism, the more likely the enterprise is to implement business transformation. Specifically, the more overconfident the managers are, the more likely they are to use both internal cultivation and M&A to realize firm business transformation. This finding fits with the results of Yang et al. (2012), whose study showed that manager overconfidence does induce M&A by employing the sample of A-share listed companies with M&A behavior from 2006 to 2011. Our regression results also demonstrate that the more overoptimistic the managers are, the lower the enterprise’s internal investment level, and the more they tend to use M&A rather than internal cultivation to realize business transformation. One possible explanation for this finding may be that, just as the viewpoint of Heaton (2002), overoptimistic managers believe that capital markets undervalue their firm’s risky securities and may decline positive net present value projects that must be financed externally. Moreover, our study distinguishes the impact of overconfidence from that of overoptimism on a firm’s performance. Specifically, during business transformation, overconfidence is positive with the firm’s financial and market performance, and overoptimism is negative with the improvement of the firm’s performance. This result differs from the prior studies, for example, Hilary et al. (2016) thought that the overoptimism can improve firm performance in terms of firm accounting performance and quarterly market return because of that managers appear to exert greater effort to meet their own overoptimistic forecasts; Kim (2019) confirmed that overconfident CEOs proceed with M&A against the enhancement of corporate value.

Together, we examine the relationships among managerial bias, business transformation, and firm performances by both theoretical and empirical analysis. Our results suggest that managerial cognitive bias plays an important role in inducing business transformation. Chinese companies are still continuously being developed and consummated, and some managers may inevitably make some unreasonable decisions by self-cognition bias, which could enable companies into the predicament. How to clearly measure and assess the impact of managerial overconfidence and overoptimism is an enduring management proposition. Compared with several recent studies, our research contributes to the literature by distinguishing the impact of overconfidence from overoptimism on business transformation by analyzing validated measures for both simultaneously. The findings extend the horizon of research in the field of managers and business transformation among Chinese listed companies.

Conclusions, Managerial Implications, and Outlook

Conclusions

This article investigated how managers’ cognitive bias impacts transformation strategy choice and transformation performance, providing both theoretical insights and empirical evidence in support of the broad hypothesis that managerial cognitive bias is an important determinant of a firm’s business transformation performance. Our theory and results clearly point to the importance of both overconfidence and overoptimism in business transformation. We also find significant differences between the business transformation strategies adopted by overconfident managers and those adopted by overoptimistic managers and between their economic consequences. In particular, managerial overconfidence helps promote enterprise transformation performance, while managerial overoptimism does the opposite.

Managerial Implications

First, as for managers, overconfidence and overoptimism are very common in them, so it is very important to carry out an objective assessment and scientific guidance on managers’ cognitive biases. The present results show that managerial cognitive biases do not always have negative effects on companies and that managerial overconfidence contributes to transformation success. Thus, for enterprises planning to conduct business transformation, taking senior managers’ overconfidence and overoptimism into full account when selecting and employing their strategy is crucial for improving the efficiency of the transformation decision. Factors such as the managers’ gender, age, educational background, work experience, character traits, and self-cultivation have significant impacts on their psychological cognition, making it necessary to establish an assessment indicator system for managers’ personal characteristics. Such a system will not only evaluate managers’ personal characteristics comprehensively, clearly, and scientifically but also provide references for the appointment and removal of senior managers and important assistance in external recruitment and internal talent cultivation. Moreover, when overconfident managers try to achieve business transformation through M&A or internal cultivation, it is necessary to fully consider the actual business operation situation and market expectation, take into account the long- and short-term interests of the company, and avoid aggravating the risk of enterprise transformation due to managers’ personal cognition and leadership style.

Second, as for business transformation, not all business transformations are driven by the psychology of managerial self-interest or stress from internal and external surroundings. For example, booms in biotechnology, media, and network technology have induced many listed firms to turn to these hot industries. If a company announces it will invest in networks, biological chips, or bio-pharmacy, its stock prices will soar, and its refinancing will be approved. Because of this, herd behavior occurs in the capital market, and many companies have abandoned their major projects one after another to turn to the so-called “high-tech industry.” Any forced or blind business transformation is a manifestation of a company’s lack of strategic foresight. The company should recognize the high risk of business transformation and strive to improve its strategic management capabilities. Specifically, corporations should establish management systems for the periods before, during, and after the business transformation decision process. Moreover, it is necessary to perfect and improve the independent director system, which should make independent judgments about decisions made by the management and timely avoid the irrational ones.

Finally, as for firm performance, not all business transformations conducted by overconfident managers succeed, despite the research results showing that business transformations conducted by overconfident managers help improve firm performance. In theory, business transformation is a kind of self-adaption behavior conducted when firms face huge environmental changes and aim to realize sustainable growth. Forced, blind, or even frequent business transformations can reflect a lack of long-term strategic perspective. As mentioned, business transformation is a complex system project involving the management system, enterprise culture, enterprise competence, and many other factors that all need to change. Moreover, this project has a relatively high risk. From this perspective, business transformation is not a panacea for sustainable firm growth. Thus, the enterprise should recognize the high risk and complexity of business transformation and avoid or reduce the risk by improving its strategic management consciousness, strategic management capability, and, especially, strategic executive capacity. Only in this way can the firm realize sustainable growth and leapfrog through development stages by successfully implementing business transformation.

Outlook

As with any empirical research, this study has limitations. First, our sample comprises Chinese listed companies, and no comparative cross-cultural studies have been conducted. The research suggests that Chinese psychological features differ from those of other countries, especially in the West. For example, the Chinese have a higher degree of overconfidence than do Americans (Meisel et al., 2016; Moore et al., 2018). Thus, in future research, we will emphasize the influence of managerial cognitive bias on firm business transformation and performance in different cultural and institutional contexts. Second, we used secondhand data instead of firsthand data for mutual authentication, which may lead to some subjectivity in the variable values. For example, even though we conducted a robustness test, caution should be applied when assessing the explanatory power of this article’s conclusions. Moreover, the case of business transformation through collaboration is not considered in our research scope because the data availability, which should be addressed in future studies. Finally, a further direction for future research may be to consider the possibility of using mixed methodological designs that allow the combination of qualitative and quantitative data.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the National Natural Science Foundation of China (No. 72074210), and the Think Tank of Energy Mining Economy (2018 Project for Cultural Evolution and Creation of CUMT 2018WHCC01).

Ethical Consideration

Ethics and privacy are not involved in this paper.