Abstract

In recent years, investing in cryptocurrencies has become a fad worldwide. However, fewer studies have explored the intention of using cryptocurrencies. Different from traditional financial commodities, cryptocurrencies have a unique appeal. Therefore, this study uses technology mindfulness, technology readiness, and financial literacy, and through perceived trust and perceived risk, to understand users’ intentions to use cryptocurrencies. The respondents to this study were cryptocurrency owners or those having financial investment experience. A total of 337 valid samples were obtained and analyzed by the partial least square-structural equation model (PLS-SEM) method. The results showed that technology mindfulness and negative technology readiness significantly impacted perceived trust and perceived risk. On the other hand, perceived trust and perceived risk significantly impacted the intention to use. Finally, this study proposes theoretical and practical implications which can help cryptocurrency trading platforms understand the motivations of potential and existing users. Finally, this study can also serve as a reference for cryptocurrency trading service providers to develop marketing strategies.

Plain Language Summary

In recent years, investing in cryptocurrencies has become a fad worldwide. However, fewer studies have explored the intention of using cryptocurrencies. Different from traditional financial commodities, cryptocurrencies have a unique appeal. Therefore, this study uses technology mindfulness, technology readiness, and financial literacy, and through perceived trust and perceived risk, to understand users’ intentions to use cryptocurrencies. The respondents to this study were cryptocurrency owners or those having financial investment experience. A total of 337 valid samples were obtained and analyzed by the partial least square-structural equation model (PLS-SEM) method. The results showed that technology mindfulness and negative technology readiness significantly impacted perceived trust and perceived risk. On the other hand, perceived trust and perceived risk significantly impacted the intention to use. Finally, this study proposes theoretical and practical implications which can help cryptocurrency trading platforms understand the motivations of potential and existing users. Finally, this study can also serve as a reference for cryptocurrency trading service providers to develop marketing strategies.

Keywords

Introduction

With the rapid development of information technology, many emerging technologies have been developed. Among them, blockchain has been a prevalent technology in recent years. Since its appearance, many applications have begun to develop. Blockchain can provide fast and cheap transactions, increase transparency, prevent fraud and increase user trust (Alshamsi & Andras, 2019). Today, cryptocurrency using the blockchain is the most flourishing. Cryptocurrency is a digital currency that uses blockchain decentralized technology. Blockchain is the basis of cryptocurrency, which is a distributed ledger technology (DLT), and transaction information is shared and verified by participants in a peer-to-peer (P2P) network (Nakamoto & Bitcoin, 2008). Cryptocurrency relies on the decentralized P2P of the blockchain, allowing users worldwide to trade freely and anonymously without relying on the government or third-party institutions (Alshamsi & Andras, 2019).

The advent of cryptocurrencies has led to a global boom in mining. “Mining” means that many cryptocurrency enthusiasts are optimistic about the cryptocurrencies whose market value is constantly rising, so they invest a lot of electronic equipment to deal with the computing needs generated during the transaction process, store transaction information in public blocks, and create block nodes through this process. These participants are rewarded with cryptocurrencies after completing the calculation assistance. These mining activities have triggered a surge in the price of electronic-related equipment and increased global electricity demand. While earning cryptocurrencies, related applications have gradually become popular, such as purchasing Non-Fungible Tokens (NFT). As a result, the prices of various cryptocurrencies have also risen strongly; various cryptocurrencies are also constantly being introduced. The emergence of cryptocurrency represents that the blockchain is gradually moving from the theoretical stage to the application stage. In recent years, the encryption technology of the blockchain has also begun to be applied in life (e.g., NFT, digital identity authentication, Web 3.0). In addition, cryptocurrency is also considered to be the circulation currency for various application services toward virtualization in the future. Cryptocurrency inherits many properties of blockchain technology, and it also has decentralization and DLT (Nofer et al., 2017). Due to the absence of government supervision, cryptocurrencies generally lack relevant laws and financial regulations to regulate, thus creating a lot of chaos.

In addition to the demand for investment, cryptocurrencies also have a demand for cross-border trade. At present, the transfer of gold flow in international trade mostly relies on the Society for Worldwide Interbank Financial Telecommunications (SWIFT). Therefore, it is easy to have problems when trading across borders or to be hindered when withdrawing currency in high-risk countries. However, the decentralization of cryptocurrencies means that they are less likely to be restricted. Many small and medium-sized enterprises (SMEs) rely on cryptocurrencies when they trade across borders but cannot conduct normal transactions. On the other hand, cryptocurrency transactions mainly use third-party cryptocurrency trading platforms for currency transfer and storage, which is similar to banks in the traditional financial system. This kind of platform acts as an intermediary for transactions. They have a large number of cryptocurrencies and are vulnerable to hackers. Therefore, users must choose cryptocurrency trading platforms carefully. In addition, not many countries currently list cryptocurrencies as fiat currency, and most of these platforms are privately owned, so cryptocurrency trading platforms are at risk of fraud and bankruptcy. When users use cryptocurrencies, the trading platform’s security is also an important factor affecting behavioral intentions. Based on its economic value, Bitcoin is considered to be as one of the most sensitive currencies due to its high volatility. In addition, price volatility was discovered as a negative factor in Bitcoin investment (P. Palos-Sanchez et al., 2021). Furthermore, any institution or organization does not guarantee the value of cryptocurrencies. Their prices fluctuate dramatically depending on investor and user confidence in them. This phenomenon is also prone to speculation and highly variable transaction costs (Mendoza-Tello et al., 2019). In summary, the characteristics of cryptocurrencies, such as being unsupervised by government agencies, not easily tampered with, and highly speculative, have led to an upsurge in investing in and using them in recent years.

Previous research have mainly explored the impact of cryptocurrencies on the financial system or their role in financial activities. Baek and Elbeck (2015) mention that most cryptocurrency research has focused on market information. On the other hand, as mentioned earlier, cryptocurrency is an emerging technology. Many studies use technology mindfulness (Flavián et al., 2020; Swanson & Ramiller, 2004) and technology readiness (Geng et al., 2019; Kaushik & Agrawal, 2021; Walczuch et al., 2007; Wiese & Humbani, 2020) to explore users’ attitudes and perceptions of various emerging technologies. However, few studies have discussed users’ intentions to use cryptocurrencies in terms of technology readiness and technology mindfulness. In addition, as mentioned earlier, cryptocurrencies are high-risk and user confidence can affect their market value. Also, the financial literacy of the users affects the intention to use them. Therefore, the research purpose is to explore the impact of users’ technology mindfulness, technology readiness and financial literacy on the intention to use cryptocurrency through perceived trust and risk.

This research study’s theoretical foundation is based on technology mindfulness, perceived risk, perceived trust, and financial literacy. This study aims to cover the following research gaps. First, the research explores the impact of perceived risk and perceived trust on the intention to use. Second, it explores the associations of perceived trust and perceived risk on technology mindfulness. Third, it examines the impacts of positive and negative technology readiness on perceived trust and perceived risk. Lastly, it analyzes the impact of financial literacy on perceived trust and perceived risk. The research results show that users’ trust in the use of cryptocurrencies comes from the cryptographic guarantees in the characteristics of the blockchain. Since DLT makes it less tamper-proof, users trust the security mechanisms for cryptocurrencies. This study is structured into the following sections. The first section is related to reviewing the literature related to the cryptocurrencies, followed by developing the proposed hypotheses. The next section deals with the research methodology, specifying information about the data collection and data analysis techniques used in this study. The third section is related to the data analysis showing the reliability and validity of the constructs used in this study, followed by the empirical analysis of the hypotheses. The last section is related to the discussion of the results and conclusion of the study.

Literature Review and Hypothesis Development

Perceived Trust

Trust is the belief that other people’s future actions will conform to one’s expectations based on past interactions, and it is widely used in various scientific fields, such as social psychology, e-commerce, and e-banking (Carlos Roca et al., 2009). Mayer et al. (1995) define trust as an act, a belief that a person is satisfied with the attributes of a person or thing. From the perspective of social psychology, trust is the expectation and willingness of buyers and sellers when conducting transactions. Gundlach and Murphy (1993) believed that trust is the consumer’s certainty that the firm is sincere and keeps its promises. Coulter and Coulter (2002) also proposed that trust is the belief consumers hold about specific characteristics of suppliers and their possible future behavior. Obviously, trust is an important factor in social interaction, which enables buyers and sellers to conduct various transactions under the premise of trusting each other.

Since the uncertainty of transactions is higher in the virtual environment than in the traditional environment, trust becomes an important influencing factor. Roca et al. (2006) argued that trust comprises multiple dimensions. Honesty and kindness are the most commonly associated with consumer trust. Carlos Roca et al. (2009) further pointed out that trust is based on the emotion of caring and benevolence, and is based on rational evaluation of personal ability and integrity. Mayer et al. (1995) argue that trust is the settlor’s belief that the trustee will abide by a set of exchange principles or rules acceptable to the settlor during and after the transaction.

One of the critical changes revolutionizing industries is technology. With the help of technology adaptation, many industries experience various opportunities in production, marketing, and efficient management tools. The advent and adaptation of the internet is deemed as a revolutionary change that has diversified and drastically improved the operations of all industries (Raza et al., 2017). Furthermore, another study indicates the use and adaptation of blockchain technologies by practitioners and managers to improve information transparency and ensure financial well-being for the clients (Farah et al., 2023). Many industries have been impacted by the adaptation of information and communication technologies (ICT). The internet has played a key role in the industries’ adaptation of these innovative technologies (P. Palos-Sanchez et al., 2021b). A recent study defines trust in the context of information technology adoption as the level of customers’ confidence on the security related to data provided by the internet-providing company (P. R. Palos-Sanchez et al., 2019).

Perceived Risk

Harridge-March (2006) believes that certain behaviors or events may cause bodily injury or other damage, and these situations are full of uncertainty, which is a risk. Perceptions of risk may vary across people, goods, or services (Stone & Grønhaug, 1993). For example, uncertain factors in the trading environment, unsatisfactory product effects, or information asymmetry between buyers and sellers are all accompanied by risks. As mentioned earlier, since cryptocurrency transactions have not yet been fully regulated by law, related transactions are full of risks. At present, cryptocurrency transactions are mostly conducted through cryptocurrency trading platforms. Compared with transactions in brick-and-mortar stores, consumers are less likely to trust transactions through the Internet (Fung & Lee, 1999). Therefore, users lack substantial interaction in transactions on the Internet, and cannot know the seller’s identity or effectively evaluate the product (Flavián & Guinalíu, 2006). These situations will make users perceive higher risks.

Previous research divided perceived risk into several dimensions (Kamalul Ariffin et al., 2018; Bearden & Mason, 1978; Featherman & Pavlou, 2003). This study adopts the subdimensions of perceived risk proposed by Featherman and Pavlou (2003) and Kamalul Ariffin et al. (2018), including financial, security, time, and psychology. Next, these risks are introduced in detail. First, financial risk is the tolerance of financial risk, which refers to the maximum price someone is willing to accept when making financial decisions or the financial management behavior when taking risks (Bapat, 2020; Featherman & Pavlou, 2003; Grable, 2000; Grewal et al., 1994; Second, security risk refers to possible losses caused by external or unexpected events, and often poses a large number of threats to customers (Cheung & Lee, 2006); third, time risk is caused by time uncertainty, time demand and the process required to use the service (Giovanis et al., 2019); fourth, psychological risk refers to customers’ dissatisfaction or frustration due to unfulfilled expectations of a product or service, which affects purchase decisions (Kamalul Ariffin et al., 2018; Jacoby & Kaplan, 1972; Namahoot & Laohavichien, 2018; Stone & Grønhaug, 1993; Ueltschy et al., 2004).

The cryptocurrency platforms are deemed to be in their initial stages of development and hence are considered to be highly prone to various risk factors (Yousaf et al., 2021). More specifically, in the case of cryptocurrencies, investors can reduce their perceived risk by diversifying their cryptocurrency portfolios. According to the findings of a study related to the performance of Islamic and conventional cryptocurrencies, investors were encouraged to diversify their cryptocurrency portfolio and add Islamic currencies due to their promising performance and unique features (Ali et al., 2023).

Intention to Use

Intention to use refers to the actual reflection of people’s motivation after being stimulated by various factors. In other words, people’s behavioral intention is the result of being influenced by various factors. In the Technology Acceptance Model (TAM) (Davis, 1989), intention to use plays a mediation role between the actual use behavior and other potential antecedents. Thus, intention to use is considered a technology acceptance behavior related to perceived ease of use and usefulness (Joo, Park, & Lim, 2018). Additionally, Joo, So, and Kim (2018) defines the intention to use technology as the degree to which users hope to use technology in the future.

Research by Schierz et al. (2010) confirmed that usefulness, ease of use and trust significantly positively impact customers’ behavioral intentions. Liébana-Cabanillas et al. (2018) also emphasized that the trust and security of systems and emerging technologies can drive users’ intentions to use them. Research on cryptocurrencies has shown that cryptocurrency trading platforms can reduce users’ doubts by providing users with the promise and guarantee of safe accounts (Sas & Khairuddin, 2015). Therefore, this study infers that high trust can enhance users’ intention to use cryptocurrencies.

On the other hand, research by Forsythe et al. (2006) showed that users expect poor service quality and transaction losses from websites than traditional transactions, so they feel a certain level of risk about trading tools and delivery time. Users’ attitudes toward online transactions significantly impact online transaction behavior (Kamalul Ariffin et al., 2018). Moreover, in general, if an emerging technology is not supported by the government or recognized institutions, user confidence in the technology is greatly weakened (Alshamsi & Andras, 2019). Cryptocurrencies have proven to be vulnerable to fraud and theft by hackers. Featherman and Pavlou (2003) pointed out that perceived risk is considered to be the main barrier for consumers to accept electronic services. Based on the above research findings, this study proposes the following hypothesis.

H1. Perceived trust has a positive and significant effect on the intention to use.

H2. Perceived risk has a negative and significant effect on the intention to use.

Technology Mindfulness

Mindfulness refers to consciously involving and paying attention to the momentary experience of interaction with oneself and the environment with personal thoughts and is also regarded as a way of psychotherapy (Bishop et al., 2004; Brown et al., 2007; Shapiro et al., 2006). Sternberg (2000) identified three perspectives on mindfulness. First, mindfulness should be understood as a cognitive ability. People differ in their ability to think mindfully, just as people differ in their memory or intelligence. Second, mindfulness is considered a personality trait. It is a trait and personality, like extroversion or neuroticism. Third, mindfulness is considered a cognitive style, representing a preferred mode of thinking.

Thatcher et al. (2018) apply mindfulness to information technology. They define it as a general mindset motivated by an individual’s perception of the environment and openness to information technology. Flavián et al. (2020) pointed out that mindfulness can help users better assess the characteristics of technology, facilitate their views on emerging technologies, and be able to explain the influence of other factors. Sternberg (2000) and Butler and Gray (2006) divided mindfulness into five dimensions: openness to novelty, alertness to distinction, sensitivity to different environments, awareness of multiple perspectives, and orientation in the present. Since cryptocurrencies can all be used on the same trading platform or online environment, this research adopts all dimensions except the sensitivity to different environments. This study further explains these four dimensions. (1) Awareness of multiple perspectives refers to a person’s ability to look at things from different perspectives and understand the unique value of each potential use; (2) openness to novelty refers to the individual’s willingness to explore and try new technologies; (3) orientation in the present refers to the degree to which individuals understand, participate in and use information technology, and they will vary according to different environments; (4) alertness to distinction refers to users’ understanding of the differences between technologies (Flavián et al., 2020; Sternberg, 2000; Thatcher et al., 2018).

Based on previous research, this study uses technology mindfulness to understand users’ perceptions of emerging technologies and the impact on trust and risk of cryptocurrencies. Drawing on previous research describing the four subdimensions of technology mindfulness (Flavián et al., 2020; Sternberg, 2000; Thatcher et al., 2018), this study infers that technology mindfulness has an impact on perceived trust or risk, and put forward the following hypothesis.

H3. Technology mindfulness has a positive and significant effect on perceived trust.

H4. Technology mindfulness has a negative and significant effect on perceived risk.

Technology Readiness

People’s use of information technology will be affected by different factors such as usage habits, personality, and use background, leading to different opinions among people on the attitude and behavior of using information technology. Rogers (1995) showed that there are differences in people’s attitudes toward the use of technology. He divided their personalities into five categories and described individual differences separately. Because people have different personality traits, they have different beliefs about various aspects of technology, that is, technology readiness. The relative strength of each personality trait indicates a person’s openness to technology (Walczuch et al., 2007). Technological readiness reflects a person’s beliefs and attitudes toward technology, but it is not an indicator of their ability to use technology. Alternatively, technology readiness can be viewed as an overall state of mind produced by both positive and negative psychological factors. These factors together determine the attitude of users to try new technologies (Lin et al., 2007). Parasuraman (2000) believes that technology readiness refers to people’s attitude toward accepting and using new technologies to achieve their family life and work goals. Moreover, these factors will directly or indirectly affect customers’ beliefs and behaviors about technology (Agarwal & Karahanna, 2000).

Therefore, this study adopts a framework of positive and negative technology readiness comprising four sub-dimensions. Next, this study further describes the four dimensions. (1) The optimism of the positive technology readiness refers to the positive attitude toward technology as it solves users’ problems and brings value to make life easier (Parasuraman, 2000; Walczuch et al., 2007; Wiese & Humbani, 2020; (2) The innovativeness of the positive technological readiness refers to the individual’s willingness to try any emerging information technology without showing fear or rejection (Parasuraman, 2000; Swanson & Ramiller, 2004; Walczuch et al., 2007; Wiese & Humbani, 2020; (3) The discomfort of negative technology readiness refers to the shock caused by the new technology that increases users’ discomfort and their preference to use easy-to-use alternatives (Parasuraman, 2000; Upadhyay & Chattopadhyay, 2015; Walczuch et al., 2007; Wiese & Humbani, 2020; (4) The insecurity of negative technology readiness refers to users’ perceptions that the results of using emerging technologies are not as expected or cause losses (Parasuraman, 2000; Walczuch et al., 2007; Wiese & Humbani, 2020).

Technological readiness refers to an individual’s belief in the ability to use information technology and is used to measure an individual’s attitude toward using new technology, including the optimism and innovation of positive factors and the discomfort and insecurity of negative factors (Blut & Wang, 2020). In recent years, many investors have been making a beeline for cryptocurrencies. Decentralization makes cryptocurrencies immune to financial regulations. Users and investors believe this is the trend of the information age, and they are optimistic that cryptocurrencies will continue to grow. However, the volatility of cryptocurrency prices also deters many investors. Because they believe that cryptocurrencies are too different from traditional financial products and are not guaranteed by the government or recognized institutions, which strengthens their sense of insecurity toward cryptocurrencies, this study infers that technology readiness has an impact on perceived trust or risk. Hence, the following hypotheses are proposed.

H5. Positive technology readiness has a positive and significant effect on perceived trust.

H6. Positive technology readiness has a negative and significant effect on perceived risk.

H7. Negative technology readiness has a negative and significant effect on perceived trust.

H8. Negative technology readiness has a positive and significant effect on perceived risk.

Financial Literacy

Financial literacy refers to people’s knowledge and cognition of economic activities, financial systems, investment, and other business behaviors. Mandell and Klein (2007) define financial literacy as assessing new and complex financial instruments and making informed judgments about the choice of instruments and the extent of their use in one’s own best long-term interest. Hastings et al. (2013) argue that financial literacy is important to effective financial decision-making. Hilgert et al. (2003) pointed out that there is a positive correlation between financial literacy and behavior in specific fields. In general, highly financially literate individuals are also knowledgeable about debt (Lusardi & Tufano, 2009, 2015), understand the concept of compound interest (Lusardi & Mitchelli, 2007), and the time value of money (Agarwalla et al., 2013; Atkinson & Messy, 2012). In short, financial literacy may influence users’ financial behaviors, such as borrowing, saving, and investing.

Hilgert et al. (2003) state that financial literacy in a specific field is positively related to practicing financial behavior in that field. Hence, having relevant financial literacy helps people’s financial behavior in business activities. At present, cryptocurrencies are mostly used for investment, because their trading patterns are different from traditional financial investments. Decentralization makes them unsecured by government agencies. There are higher risks for those with less investment experience and lack financial literacy. Hastings et al. (2013) believe that financial literacy is one of the keys to effective decision-making. Thus, this study infers that having richer financial literacy can improve users’ perceived trust and reduce perceived risk and puts forward the following hypotheses.

H9. Financial literacy has a positive and significant effect on perceived trust.

H10. Financial literacy has a negative and significant effect on perceived risk.

The research purpose to explore the effects of users’ technology mindfulness, technology readiness, and financial literacy on perceived trust and risk and their perceived trust and risk on their intention to use cryptocurrencies. After the literature review, put forward research hypotheses and then establish the research model (see Figure 1).

Research model.

Research Method

Research Subjects and Data Collection

The research purpose is to understand the intention to use cryptocurrency. This study designed an online questionnaire. The data was collected with the help of a professional questionnaire collection company. The Likert seven-point scale was used to measure the questionnaire in this study. The questionnaire collection period is from 2022/01/28 to 2022/03/14. Before the respondents answered the questionnaire, the researchers would explain the purpose of the study and the experiment’s background to ensure that they fully understand the operation and related knowledge of cryptocurrencies. Respondents were also asked about their financial literacy at the end of the questionnaire.

A pre-test pilot questionnaire was distributed to a sample of 100 respondents to test the reliability of the questionnaire items. The reliability tests of the pilot test were found to be reliable, making the questionnaire suitable for collecting the data for this research. Finally, a total of 374 questionnaires were collected with the help of a convenience sampling method. Out of the 374 samples, with an effective response rate of 90.1%, 337 were found valid.

Research Methodology

This study used the Partial Least Squares Structural Equation Modeling (PLS-SEM) proposed by Wold (1975) to analyze the research model. It is an analytical technique for detecting or constructing predictive models, especially for causal model analysis among potential variables. PLS is a SEM technique based on an iterative method, which can optimally explain the variation of endogenous variables (Fornell & Bookstein, 1982). PLS-SEM can effectively handle wide sample sizes, increased model complexity, and less restrictive hypotheses on the data (Ficapal-Cusí et al., 2023; Hair et al., 2016). Additionally, the SmartPLS (version 3.3.6) developed by Ringle et al. (2015) was used to examine the data, and the reliability and validity were analyzed according to Hulland’s (1999) suggestion. The model analysis in this study has two stages. First, the reliability and validity were examined; second, the significance of the path coefficients and the explained variation (R2) were examined. Finally, this study used bootstrapping, conducted 5,000 repeated sampling, and calculated p-values to determine whether the path coefficients were significant.

Research Results

Descriptive Statistical Analysis

This study surveyed the demographics of the respondents, including gender, age, education level, and occupational category, and asked the respondents whether they had held cryptocurrencies, used cryptocurrency trading platforms, and had investment experience. The results are shown in Table 1.

Demographic Statistics (N = 337).

Furthermore, the descriptive statistics of the questions of each dimension are shown in Table 2. In the questionnaire designed in this study, except for the questions about financial knowledge, which use multiple-choice questions, the others use the Likert seven-point scale. Table 2 shows that the mean of all dimensions is >4 and the skewness is negative, indicating that most respondents tend to agree. In addition, the standard deviation can be used to understand the difference between the respondents’ perception of the item and the parent population. Variance and kurtosis represent the difference between the population and the sample. The results are shown in Table 2.

Descriptive Statistics (N = 337).

Note. ITM = technology mindfulness; PTR = positive technology readiness; NTR = negative technology readiness; FL = financial literacy; PT = perceived trust; PR = perceived risk; ITU = intention to use.

Reliability and Validity

In this study, the factor loadings of the items were analyzed to measure the construct’s reliability, and according to Hair et al. (2010), a factor loading >0.7 indicates that the item has good reliability, whereas the factor loading values below 0.7 indicates low reliability and hence, is supposed to be deleted from the construct. In this study, all the items measuring different constructs were discovered to have values higher than 0.7; hence, no item was deleted from the model. Moreover, convergent validity aims to measure the similarity of the results of different indicators in examining the same dimension. This study used PLS for composite reliability (CR) and average variance extracted (AVE) analysis. Fornell and Larcker (1981) suggested that AVE should be >0.5, indicating convergent validity. Then, according to Hulland (1999), the CR must be >0.7, which means that each question conforms to the same dimension and has internal consistency. Finally, the variance inflation factor (VIF) values are <5, indicating no multicollinearity among the dimensions. Table 3 shows that factor loading, CR, AVE, and VIF all meet the criteria, indicating that the questionnaire meets reliability and validity.

Reliability and Validity Analysis.

Note. VIF = variance inflation factor; CR = composite reliability; AVE = average variance extracted.

Next, the Fornell-Larker criterion was used to examine this study’s discriminant validity. In Table 4, the value of the diagonal angle is the square root of AVE; others are correlation coefficients between dimensions. The former is larger than the latter, indicating good discriminant validity between the dimensions.

Fornell-Larker Criterion of Discriminant Validity.

Note. The value of the diagonal is the square root of AVE. ITM = technology mindfulness; PTR = positive technology readiness; NTR = negative technology readiness; FL = financial literacy; PT = perceived trust; PR = perceived risk; ITU = intention to use.

Moreover, the discriminant validity was also validated with the help of another technique named heterotrait-monotrait (HTMT). HTMT was introduced by Henseler et al. (2015) to address the limitations of the discriminant validity computation with the help of Fornell and Larcker (1981). HTMT follows the criteria of the average mean of the indicators across constructs in association with the mean of the constructs measuring the construct (Henseler et al., 2015). According to the findings shown in Table 5, it can be observed that all the HTMT values are below the threshold value of 0.90, and hence, discriminant validity is assured for this research (Gold et al., 2001).

Heterotrait-Monotrait Ratio (HTMT).

Note. ITM = technology mindfulness; PTR = positive technology readiness; NTR = negative technology readiness; FL = financial literacy; PT = perceived trust; PR = perceived risk; ITU = intention to use.

Structural Equation Modeling Analysis

This study used SmartPLS as a tool to analyze the path and test hypotheses and conducted a two-stage testing process according to the suggestion of Anderson and Gerbing (1988). This study examined the explained variation (R2) between potential variables in the model, the path coefficient, and the p-value to determine whether the hypotheses were supported. This study uses the path coefficient to measure the explanatory strength between the various dimensions. If the results are in the same direction as the hypotheses and are significant, it means the hypotheses are established.

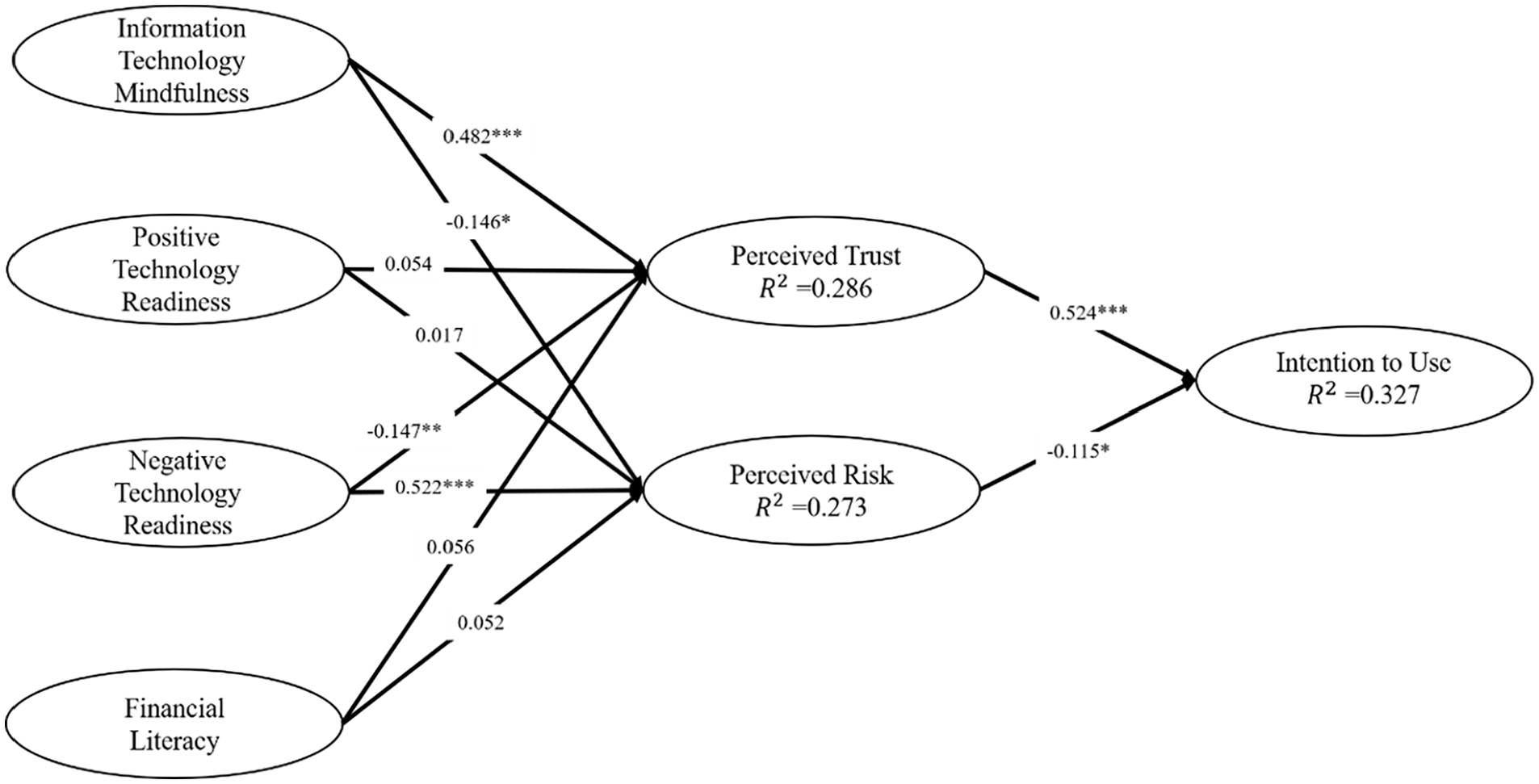

Table 6 shows the results of the hypothesis tests. Perceived trust has a positive and significant effect on the intention to use (β = .526, p < .001). Perceived risk has a negative and significant effect on the intention to use (β = −.118, p < .05). Technology mindfulness has a positive and significant effect on perceived trust (β = .479, p < .001), and Technology mindfulness has a negative and significant effect on perceived risk (β = −.149, p < .05). Positive technology readiness has a positive but non-significant effect on perceived trust and perceived risk (β = .054, p > .05; β = .017, p > .05). Negative technology readiness negatively and significantly affects perceived trust (β = −.147, p < .05). Negative technology readiness positively and significantly affects perceived risk (β = .507, p < .001). Financial literacy has a positive but non-significant effect on perceived trust and perceived risk (β = .056, p > .05; β = .052, p > .05). In summary, the results of H1, H2, H3, H4, H7, and H8 are consistent with the prediction direction and are significant, so they are supported. However, the results for H5, H6, H9, and H10 are insignificant, so they are not supported.

Path Analysis.

Note. NTR = negative technology readiness; FL = financial literacy; PT = perceived trust; PR = perceived risk; ITU = intention to use.

R2 refers to the percentage of variation that can be explained by exogenous variables to endogenous variables. R2 ranges from 0 to 1, and the closer it is to 1, the greater the predictive power of the research model. The results found (see Figure 2) the explanatory power of perceived trust is 28.8% (R2 = .288), the explanatory power of perceived risk is 25.7% (R2 = .257); the explanatory power of intention to use is 32.8% (R2 = .328).

Research results.

This study used a blindfolding methodology to skip some part of the construct’s data during the framework’s estimation. Furthermore, the projected parameters were employed to estimate the previously skipped data (Chin, 1998). The model’s predictive accuracy was examined following the methodology of calculating Q2, proposed by Stone (1974). The Q2 of the model was found to be 0.352, which was above zero, and hence the predictive model of this study was found to be reliable.

Furthermore, the standard root mean square (SRMR) value was analyzed to determine the adjusted approximation of the model (Henseler, 2017). SRMR examines the difference between the employed and observed correlation matrix. Hence, SRMR measures the strength of the mean differences (Saura et al., 2020). In this study, the value of SRMR was found to be 0.08, which is in accordance with the recommendation by Hu and Bentler (1998), which states that the SRMR should be lower or equal to 0.08.

Discussions

Conclusions

As mentioned above, it is understood that perceived trust, perceived risk, technology mindfulness, and negative technology readiness are important factors in this study. Through the analysis, this study has the following conclusions.

First, perceived trust positively and significantly affects intention to use. The results of this study can be compared to an earlier study by Singh and Sinha (2020). According to Singh and Sinha (2020), the demand for mobile wallets has increased drastically; hence, there is a need to examine the stances of various stakeholders concerned in the development. However, traders are often found to be neglected to use these applications. Singh and Sinha’s (2020) study aims to explore the traders’ intention to employ these mobile wallets. Singh and Sinha’s (2020) study also explored the mediating role of trust on the relationship between perceived usefulness and intention to use mobile wallets. The data for Singh and Sinha’s (2020) study were collected from 315 traders, and according to the results, customer value and perceived usefulness were found to significantly impact the intention to use. Furthermore, trust significantly mediated the relationship between perceived usefulness and intention to use.

Other possible reasons related to the current study’s aforementioned result might include the characteristics of cryptocurrencies (e.g., decentralized management, blockchain immutability, and algorithmic encryption) that can give users peace of mind. Users believe that their cryptocurrency wallets can be kept safely. Especially decentralized, cryptocurrency cannot be affected by external factors (e.g., foreign exchange control, war, income tax) and can be used as long as you go to an ATM where you can withdraw cryptocurrency. In addition, some cryptocurrencies (e.g., BTC, DOGE) are favored and held by celebrities, such as Elon Musk, the CEO of Twitter, which invisibly strengthens other users’ trust in them and their intentions to use them. As Lou and Yuan (2019) pointed out, when there are business people who are optimistic about the prospects of cryptocurrencies or celebrity endorsements, more people will be willing to use them.

Secondly, according to the current study’s results, perceived risk negatively affected intention to use. This result implies that perceived risk is a factor that discourages new users from adopting cryptocurrencies. The result can be compared to a previous study conducted by Marafon et al. (2018). Marafon et al.’s (2018) research aimed to explore the moderation impacts of risk acceptance and confidence in the relationship between risk and intention to use. The data for Marafon et al.’s (2018) study was collected from 180 bank customers in Brazil with the help of a questionnaire. According to the findings of Marafon et al.’s (2018) study, confidence significantly moderated the relationship between perceived risk and intention to use. This implies that for people with high confidence, the impact of perceived risk on the intention to use will be comparatively lower than that of people having low confidence. Furthermore, risk acceptance was also found to be positively moderating the relationship between perceived risk and intention to use. This indicates that individuals prone to accept risk will have lower impact of perceived risk on intention to use; on the other hand, people with lower acceptance of risk will have a higher impact of perceived risk on intention to use. As mentioned earlier, governments or financial institutions do not supervise and guarantee cryptocurrencies, so they are vulnerable to hacking and theft. Their high risk will hinder users’ online transaction activities, which is similar to Masoud’s (2013) research. It follows that, compared to fiat currencies, cryptocurrencies are riskier, which reduces the user’s intention to use them.

Moreover, according to the results of the present study, technology mindfulness has significant effects on perceived trust and perceived risk. The result shows that users are quite optimistic about cryptocurrencies’ prospects and current status. They believe that cryptocurrencies can make up for the shortcomings of traditional currencies in business activities and are willing to understand the role and positioning of cryptocurrencies in today’s trading activities. Apparently, when users are open, receptive, and alert to the rise of cryptocurrencies, their perceived risk decreases. Grable (2000) and Featherman and Pavlou (2003) pointed out that when people are willing to accept the greatest uncertainty in making decisions, they perceive less risk. In other words, people who are open to emerging technologies perceive less risk in using cryptocurrencies.

The result of the current study can be compared to an earlier study by Oredo (2020). According to Oredo’s (2020) study, there is a lack of research on using cloud computing for personal purposes. Oredo’s (2020) research employed variables like perceived risk, perceived trust, technology mindfulness, and intention to use. Oredo’s (2020) study collected data from 122 university students, and according to the results, technology mindfulness was found to be in significant relationships with the intention to use and perceived risk. Furthermore, perceived trust and perceived risks significantly impacted the intention to use.

Next, according to the present study, technology readiness negatively and significantly affects perceived trust. This result shows that the higher the user’s mastery and adaptability to new technology, the more willing they are to trust and use it. Walczuch et al. (2007) pointed out that if users feel that they cannot master a technology, they will look for easy-to-use alternatives. Because the transaction mechanism of cryptocurrencies is very different from that of traditional currencies, some people think that their transaction mechanism is more complicated. At present, cryptocurrency trading platforms are almost operated by private enterprises, and they are not protected by regulations and are supervised by financial institutions. Alshamsi and Andras (2019) state that when a technology is not supported by government or recognized institutions, user confidence in it is greatly weakened. As a result, users find it difficult to trust cryptocurrencies because they perceive them to be difficult to understand and not well protected. Wiese and Humbani (2020) mentioned that the impact of new technologies replacing old behaviors will increase users’ discomfort. Therefore, this study infers that users who are discomforted with new technologies have lower trust in cryptocurrencies and trading platforms.

The result can also be compared to an earlier study conducted by Caldeira et al. (2021). The purpose of Caldeira et al.’s (2021) study is to examine the impact of technology readiness on technology acceptance in the context of mobile payment methods in Brazil. Hence, Caldeira et al.’s (2021) study employed variables like technology readiness, perceived usefulness, trust, quality, and perceived ease of use in their research model. Caldeira et al. (2021) collected the data from 402 participants and according to the results, quality, trust, and usefulness were found to significantly impact the technology acceptance in the context of mobile payment.

On the other hand, negative technology readiness has a positive and significant effect on perceived risk. Obviously, negative technology readiness also affects perceived risk. As mentioned above, the security of a cryptocurrency trading platform is one of the important reasons for users to consider whether to use it or not. With frequent incidents of hackers attacking cryptocurrency wallets or trading platforms, people have doubts about the security of cryptocurrencies. Furthermore, when cryptocurrencies are traded, the blockchain will disclose the relevant records. Many people think there is a problem of personal information and privacy leakage. As a result, security issues also lead to a higher perceived risk of users for cryptocurrencies. Furthermore, countries have different attitudes toward cryptocurrencies. Coutu (2015) points out that these decentralized digital currencies (e.g., BTC) have legitimacy issues, and users may not be effectively protected. Alshamsi and Andras (2019) argued that security is considered to be valued by online transaction users and has a significant impact on the use of online transactions. Hence, the research findings are consistent with previous research.

The result is also somewhat comparable to an earlier study by Choi and Yoo (2021). The purpose of Choi and Yoo’s (2021) study is to examine the roles of various self-construals on perceived risk and technology readiness. Choi and Yoo’s (2021) study collected data from 284 tourists, and according to the results it was found that tourists experienced a high level of perceived risk in the technology readiness of tourism mobile app, having no concern with the type of self-construal type. In addition, in case of an independent self-construal, individuals are found to perceive less risk. Moreover, technology readiness was found in a mediating role for the relationship between self-construal and intention to use. Hence, according to Choi and Yoo (2021), companies need to reduce the risks associated with tourism apps and design customized messages for tourists based on their self-construal.

Theoretical Implications

In the past, many researches exploring cryptocurrencies have focused on the impact on financial markets, changing business activities, the financial characteristics of cryptocurrencies, and the acceptance of e-commerce (Fry & Cheah, 2016; Pelster et al., 2019; White et al., 2020). Fewer researchers have focused on the intent to use cryptocurrencies. On the other hand, technology mindfulness and technology readiness are often used to discuss the use of emerging technologies but rarely used to discuss cryptocurrencies. Therefore, this study attempts to explore the influence of users’ technology mindfulness, technology readiness, financial knowledge, perceived trust, and perceived risk on the intention to use cryptocurrencies. This study finds that users’ insecurity and discomfort with cryptocurrencies are the main reason for the increased perceived risk. Even though blockchains are claimed to be secure and immutable, users still have doubts about cryptocurrency trading platforms. Potential risks such as hacking and fraud also deter users. Fujiki (2020) found that people with investment experience are more likely to use cryptocurrencies, which is consistent with the findings of this study. Moreover, Fujiki (2020) and Zhao and Zhang (2021) also indicated that financial literacy is not significantly related to the motivation to use cryptocurrency, which is similar to the findings of this study. In short, the research results supplement the gaps in past research and can be used as a reference for future research on cryptocurrencies.

Practical Implications

The research results show that users’ trust in the use of cryptocurrencies comes from the cryptographic guarantees in the characteristics of the blockchain. Since DLT makes it less tamper-proof, users trust the security mechanisms for cryptocurrencies. According to the research of Hoffman et al. (1999), an insecure environment will hinder users from using electronic transaction services. Users have a strong sense of discomfort and insecurity about the damaging technology readiness. However, these users are potential users for cryptocurrency trading platforms that provide intermediary services. Cryptocurrency trading platforms can provide services such as guarantee mechanisms, user contracts, and network security to reduce the users’ negative technology readiness. Thus, when choosing a cryptocurrency trading platform, users will depend on whether the platform can provide a sufficiently secure storage environment. For example, the well-known cryptocurrency trading platform “Binance” has a Secure Asset Fund for Users (SAFU). When there is an accident of funds, SAFU funds can be used to compensate users to ensure that users’ funds will not be lost. Binance activated this security mechanism when hackers stole a large amount of BTC in 2019, so the incident did not affect users. To sum up, the better security mechanism provided by cryptocurrency trading platforms is one of the factors for users to use cryptocurrency. In addition, the issuance of cryptocurrency Exchange Traded Funds (ETFs) and Stablecoins provides investors with more options to diversify their risk and increase their intention to use them.

Additionally, the research results showed that positive technology readiness has no significant effect on perceived trust and risk, which is different from the findings of Walczuch et al. (2007). However, technology mindfulness about the prospect and development of cryptocurrencies significantly affects perceived trust and risk. Hence, this study argues that the incentives and stimuli for users of cryptocurrencies come from speculative motives. If a cryptocurrency trading platform can provide more favorable handling fees or better services, it can attract the intention of existing and potential users.

Research Limitations and Future Research Suggestions

This study examines the effects of technology mindfulness, technology readiness, and financial literacy on perceived trust and risk, which affect intention to use cryptocurrencies. The research results are hoped to provide a reference for cryptocurrency investors, users, and trading platforms to make decisions. Although this study has done its best to complete the research, there are some limitations. This study did not conduct an individual analysis of cryptocurrency enthusiasts with different experience, so the results cannot be used as a reference for the detailed target market classification strategy, which limits its generalizability. In addition, some factors have not been considered in this study, for example, the development of Metaverse and NFT and changes in the international political and economic situation; the development and characteristics of various cryptocurrencies and their conversion to fiat currencies are different. Therefore, a sub-dimension of technology mindfulness called “sensitivity to different environments” was not used in this study. It is suggested that future research can conduct more oriented investigations to take sensitivity into consideration.

Second, in recent years, countries have paid more and more attention to cryptocurrencies, but their secrecy has made it difficult for governments to manage them, leading some countries to start promoting digital fiat currencies. China banned the trading of cryptocurrencies in 2013 but announced the digital currency electronic payment “E-CNY” in 2021. Unlike general cryptocurrencies, government-issued digital fiat currencies can bring more economic activities under management. Therefore, before the positioning of cryptocurrencies is widely recognized by various countries, there are major challenges in practical application. The future development of both cryptocurrencies and digital fiat currencies deserves further discussion.

Finally, different ethnic groups, ages, incomes, lifestyles, and experiences have different financial investment and risk preferences. Future research can further explore these issues with the help of measurement invariance and multigroup analysis (P. Palos-Sanchez et al., 2021). Moreover, the services, interactive interfaces, and fees offered by each cryptocurrency trading platform differ, affecting users’ intention to use them. All in all, cryptocurrencies and financial technology are still developing rapidly, coupled with the different political and economic environments in different countries; it is suggested that future research can further discuss the above issues.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the World Class Professor (WCP) Indonesia grant based on Decree Number 3252/E4/DT.04.03/2022.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.