Abstract

In an evolving stock market landscape characterized by diversified participants, the personal financial behavior of corporate insiders has garnered much attention, especially concerning its impact on stock liquidity. A key financial behavior under scrutiny is share pledging, where corporate insiders use their shareholdings as collateral for personal loans. Using a sample of Chinese listed firms from 2007 to 2021, this study examines the relationship between insiders’ share pledging and the stock liquidity of listed firms, as well as possible underlying mechanisms. Our analysis reveals a positive association between share pledging and stock liquidity. The findings withstand a series of robustness tests. Further analysis shows that stock repurchases and increased shareholdings may be the underlying mechanisms driving the positive effect of share pledging on stock liquidity. Our results have significant implications for regulators managing liquidity risk and offer valuable insights for other stakeholders. As insiders’ personal financial behavior significantly impacts the sustainable quality of securities markets, investors, managers, and analysts can benefit from understanding the influence of share pledging on stock liquidity.

Plain language summary

Our study aims to explore the impact of corporate insiders’ share pledging on stock liquidity in Chinese firms. Using data from 2007 to 2021 on Chinese listed firms, we employ a range of rigorous statistical tests, such as Difference-in-Differences (DID), Propensity Score Matching with Difference-in-Differences (PSM-DID), two-stage least squares (2SLS), and Lewbel instrumental variables, to mitigate potential biases and establish causal relationships. We find a positive correlation between share pledging by insiders and stock liquidity. We further identify stock repurchases and increased shareholdings as the likely mechanisms that drive this positive impact. These findings provide valuable insights for regulators in liquidity risk management and furnish corporate insiders, investors, and market analysts with actionable knowledge. However, our focus on Chinese firms limits the broader applicability of the results. Also, the study leaves unexplored the intersection of insiders’ financial behaviors with wider sustainability objectives like ESG performance, leaving room for future research.

Introduction

Share pledging is a financial practice where corporate insiders—defined in this study as shareholders who own at least 5% of a firm’s outstanding shares (Hirschey & Zaima, 1989; Kim et al., 2007)—use their shares as collateral to secure personal loans. This practice allows corporate insiders to unlock the liquidity of their shareholdings without directly selling them. However, it also exposes them to the pressure of margin calls. When the value of the pledged shares decreases, insiders may need to furnish additional collateral or margin. Over the past decade, share pledging has witnessed significant growth, attracting heightened attention from the public, academics, and regulatory bodies. Prior literature has documented several economic consequences resulting from insiders’ engagement in various price-supporting activities to avoid margin call pressure, and that affect the firm’s value, innovation, and risk-taking (Anderson & Puleo, 2020; Chang et al., 2022; Pang & Wang, 2020; Q. Wang et al., 2020). However, little is known about how corporate insiders’ financial activities affect a stock’s liquidity. Behavioral finance holds that the psychological effect of corporate internal shareholder behavior on the decisions of external investors must be considered when understanding the performance of financial markets (Baker & Wurgler, 2007; DellaVigna, 2009; Valaskova et al., 2019). In this paper, we investigate how the unique behavior of insiders, namely, share pledging, affects stock liquidity.

The impact of insiders’ share pledging on stock liquidity is an issue worth exploring. A large literature documents that the personal behaviors of insiders have a significant impact on investors’ trading decisions, particularly in countries with a highly concentrated corporate ownership structure, thereby affecting stock liquidity (De Cesari et al., 2011; Hillert et al., 2016). For instance, research conducted in Italy, Canada, Switzerland, Sweden, and the United States indicates that stock repurchases can significantly enhance firms’ stock liquidity (D. Y. Chung et al., 2007; De Cesari et al., 2011; Hillert et al., 2016; McNally & Smith, 2011; Råsbrant & De Ridder, 2013). K. H. Chung et al. (2010) document that firms with better corporate governance have higher stock liquidity, because good governance can improve financial and operational transparency. Roy et al. (2022) show that firms spending more on education and healthcare projects have higher stock market liquidity. Therefore, we argue that insiders’ share pledging affects invertors’ expectations and thereby leading to changes in stock liquidity.

There are two competing views on how share pledging affects firm value or risk-taking. The negative view holds that the agency problems and margin call pressures resulting from share pledging can induce insiders’ opportunistic behaviors, which may harm firms’ value (Chauhan et al., 2021; Pang & Wang, 2020; Q. Wang et al., 2020) and reduce firms’ risk-taking (Anderson & Puleo, 2020; Cai, 2019; Dou et al., 2019). The positive view, on the other hand, argues that the threat of losing control can strongly encourage insiders to engage in value-enhancing activities, which can improve firms’ value (M. Li et al., 2019; Chang et al., 2022; Puleo et al., 2021; Zhu et al., 2021). Such differing findings are based on the economic consequences of insiders’ varying value management strategies after pledging their shares. How market participants, such as investors and market makers, evaluate, and react to insiders’ share pledging remains unclear.

Focusing on stock liquidity is helpful to further understand the longstanding concerns on whether share pledging enhances or impedes a firm’s risk-taking and market stability. Using a sample of Chinese listed firms from 2007 to 2021, we investigate the effects of insiders’ share pledging on a firm’s stock market liquidity, and find that firms with insiders’ share pledging exhibit higher stock liquidity than those without share pledging. The results are robust when using alternative measures of share pledging, alternative sample selections, and alternative measures of control variables.

Although our results show that firms with insiders’ share pledging outperform firms without insiders’ share pledging in improving stock liquidity, our findings may be the result of reverse causality, which means differences in stock liquidity trigger insiders’ share pledging. Unobserved firm characteristics correlated with both share pledging and stock liquidity could introduce bias (i.e., the omitted variables). To address these concerns, we employ the Difference-in-Differences (DID) approach, Propensity Score Matching with Difference-in-Differences (PSM-DID) approach, two-stage least squares (2SLS), and Lewbel (2012) instrumental variable approaches to test the effect of share pledging on stock liquidity.

After demonstrating the relationship between share pledging and stock liquidity, we further explore possible mechanisms for the improvement effects of share pledging on stock liquidity. As expected, share pledging affects a firm’s stock liquidity through two channels. First, we show that firms with insiders’ share pledging are more likely to initiate buyback programs than those without share pledging. Second, we demonstrate that an increase in shareholdings is also a mechanism through which insiders’ share pledging improves stock liquidity.

In sum, our paper contributes to the literature in the following ways. First, this paper examines the impact of insiders’ financial behavior on corporate risk-taking from the perspective of stock liquidity. In contrast to the ample empirical evidence that insiders’ share pledging may cause negative economic consequences (Chauhan et al., 2021; Chou et al., 2021; W. Li et al., 2020; Y. C. Wang & Chou, 2018; Xia et al., 2022), we document one bright side of share pledging for firms in improving market quality and a role for share pledging in aligning the interests of inside shareholders with those of outside investors. This supports the study by Haron et al. (2021), who use Indonesian firm data to show a positive effect of debt financing on mitigating possible agency conflicts between the large controlling and minority shareholders. We show that insiders have strong incentives to maintain the safety of pledged stocks after their share pledging, such as initiating buyback programs and increasing their holdings to boost stock prices, which in turn has a positive impact on stock liquidity. This finding is of great importance for policymakers, as it demonstrates that share pledging offers some significant benefits. Thus, our paper reveals a previously unrecognized beneficial consequence of regulators’ efforts to deregulate the share pledgees.

Second, our paper enhances our understanding of the relationship between insiders’ behavior and stock liquidity. Stock liquidity is an important factor in determining stock market accessibility and sustainability. Thus, prior studies have explored how insiders’ behavior affects stock liquidity from various dimensions, including institutional investors (Z. Chen et al., 2013; Ferreira & Matos, 2008; Gompers & Metrick, 2001; Hillert et al., 2016; Roy et al., 2022). We extend these studies to investigate the effect of a specific financial behavior—share pledging—by insiders on stock liquidity.

Third, we also focus on the potential impact of share pledging on insiders’ incentives and their managerial decisions, which in turn affect stock liquidity. Thus, our paper provides more evidence that stock repurchases and increased shareholdings help share-pledging firms mitigate potential margin calls and forced sales. This is consistent with Chan et al. (2018), who find that firms with insiders’ share pledging are more likely to initiate buyback programs.

The rest of the paper is organized as follows. The next section (Section 2) outlines the institutional background and literature review, and proposes hypotheses. Section 3 describes our data and descriptive statistics. Section 4 analyzes the impact of share pledging on stock liquidity and explores the mechanisms through which it operates. Section 5 presents our conclusions and recommendations.

Institutional Background, Literature Review and Hypotheses Development

Institutional Background in China

In this section, we provide a brief overview of the institutional background of share pledging in China, which is the reason we chose to conduct this research in China and the basis for the hypotheses proposed in the subsequent sections.

Collateral, such as real estate, plays an important role in improving borrowers’ (or pledgers’) ability to access external financing (Hart & Moore, 1994; Rampini & Viswanathan, 2013; Stiglitz & Weiss, 1981) and securing lenders’ (or pledgees’) loans. Specifically, the right to confiscate and sell collateral can help lenders in reducing expected losses in cases where borrowers default on their promised payments (Benmelech & Bergman, 2009).

Using stock as collateral to obtain loans from financial institutions, share pledging, is a popular financing method for corporate insiders (or major shareholders), particularly in emerging markets like China. According to the “Guaranty Law of the People’s Republic of China” in 1997, insiders of listed firms can pledge their shares as collateral for personal loans offered by banks or trust firms. On May 24, 2013, the Shanghai Stock Exchange, Shenzhen Stock Exchange, and China Securities Depository and Clearing Corporation jointly issued the “Business Measures (Trial) on Trading, Registration and Settlement of Collateralized Repo of Shares” (the Measures). This policy, allowing brokerage firms to provide loans secured by stocks, has significantly fostered the growth of share pledging in China (Zhu et al., 2021), thereby offering a natural experiment for causal inference about the impact of share pledging on stock liquidity.

Share pledging provides insiders and financial institutions with obvious benefits. On the one hand, the loan with insiders’ share pledging is low-cost, fast, and easy to obtain, which can quickly alleviate pledgers’ financing constraints without losing their control rights on pledged shares. Thus, share pledging is a good way to raise funds for insiders who lack liquidity. On the other hand, the market value of listed firms is readily observable, and their stocks are generally more liquid compared to traditional forms of collateral like real estate and land. Share pledging, therefore, can alleviate information asymmetry and adverse selection problems between pledgers and pledgees. Through the use of credit management measures like mark-to-market, maintenance requirements, and liquidation, pledgees can mitigate their risk exposure should the value of pledged shares decline significantly before loan maturity or if pledgers default at maturity.

China has strict disclosure requirements for insiders’ share pledging in listed firms. Since 2004, the “Rules Governing the Listing of Stocks on Shanghai (Shenzhen) Stock Exchange” has required firm’s insiders with share pledging (owning more than 5% of the firm’s outstanding shares), to provide timely and accurate information about the status of the pledge. Specifically, insiders are obligated to notify the firm within two business days if they initiate, modify, or repay a margin loan backed by the firm’s stock. The firm is then required to publicly disclose the details of the pledge, including the number of pledges, the aggregate volume of pledges, and the ratio of pledged shares to total outstanding shares. This strict disclosure requirement on share pledging makes it possible for us to obtain the specific information of each share pledged loan, such as the precise time, size, and insider’s identity, as well as the adjustments in these loans.

Compared with developed markets, the Chinese stock market is still immature concerning distinct investors’ trading behavior and institutional features. The market is dominated by unsophisticated individual investors who tend to overreact to news and exhibit herding behavior (Zhou et al., 2017). In addition, there is a lack of sound corporate governance and shareholder protection in most Chinese listed firms (Allen et al., 2005), and tunneling practices by major shareholders are prevalent (Ding et al., 2007; Liu & Lu, 2007). As a result, investors in the Chinese market may be particularly sensitive to insiders’ share pledging activities.

In conclusion, China provides a good research opportunity to investigate the effects of insiders’ share pledging on the firm’s stock market liquidity.

Literature Review and Hypotheses Development

The rapid growth of share pledging in recent years has garnered widespread academic attention. One line of research explores the motivations behind insiders’ share pledging, including alleviating financial constraints, extending control rights (Y. Chen & Hu, 2007), tunneling firm resources (Kao et al., 2004), and undermining minority shareholders’ interests (Y. C. Wang & Chou, 2018).

Insiders involved in share pledging face increased stock price pressure due to margin calls and forced sales. As a result, they have a strong incentive to engage in various price-supporting activities, such as earnings management (DeJong et al., 2020; Huang & Xue, 2018), reducing cash dividend payments (W. Li et al., 2020; Xu & Huang, 2021), curtailing investment in innovation projects (Pang & Wang, 2020), engaging in mergers and acquisitions (Zhu et al., 2021), and initiating buyback programs (Chan et al., 2018; Chou et al., 2022). Therefore, another line of research focuses on the impact of insiders’ share pledging on listed firms.

Studies using Taiwanese data, such as Kao et al. (2004), Y. Chen and Hu (2007), Y. C. Wang and Chou (2018), and Dou et al. (2019), consistently find a negative impact of insider share pledging on firm value. Meanwhile, P. P. Singh (2018), using Indian data, indicates that share pledging for personal loans can reduce firm value, whereas share pledging for business loans can enhance it. A. Chen and Kao (2011) demonstrate that an increase in risk exposure to share pledging reduces bank profits. Pang and Wang (2020) find that both controlling shareholders’ share pledging and share pledging ratios are significantly negatively related to firm innovation. Furthermore, Cai (2019), Dou et al. (2019), Anderson and Puleo (2020), and Chauhan et al. (2021) find that insiders’ share pledging reduces firms’ risk-taking.

However, several other studies argue that insiders’ share pledging has certain positive effects. M. Li et al. (2019) use Chinese data to show that share pledging is associated with higher firm value. Zhu et al. (2021) find that firms with insiders’ share pledging are more likely to initiate diversified, unaffiliated, and cash-financed acquisitions, which can significantly improve firm value. Chang et al. (2022) find that share pledging helps deter excessive innovation inputs and increases the number of invention patents, hence improving firms’ innovation efficiency and market value. Also, A. Singh (2023) uses Indian data to show a positive effect of share pledging on firms’ market value by improving stock price informativeness.

In sum, these differing findings on the economic consequences of share pledging are based on insiders’ various value management strategies in response to margin call pressure. How market participants like investors and market makers evaluate and respond to this behavior, especially in terms of the firm’s stock market liquidity, remains unclear. Extensive literature shows that firms with greater stock liquidity are associated with higher institutional and foreign ownership (Ferreira & Matos, 2008; Gompers & Metrick, 2001), greater credit ratings (Lee et al., 2016), better internal governance (Jain et al., 2016; Pham, 2020) and higher corporate investment (Kang et al., 2018), as well as stock splits (Muscarella & Vetsuypens, 1996) and stock repurchases (Hillert et al., 2016). As a result, a firm’s stock liquidity is highly related to its financial decisions and development.

From a signaling perspective, insiders’ share pledging may send a positive signal about a firm’s development and growth prospects. There is a potential risk of transferring control rights if insiders fail to withstand the pressure of margin calls and forced sales. Given the risk aversion of insiders, insiders’ share pledging may be a signal of their confidence in firms’ stock prices (A. Singh, 2023). In addition, in order to avoid potential margin calls and forced sales, insiders have a strong incentive and ability to boost stock prices after pledging their shares. Therefore, insiders’ share pledging could significantly impact market expectations and contribute to enhanced stock liquidity. We propose the following hypothesis:

The underlying mechanisms for share pledging’s effect on stock liquidity may include stock repurchases and increased shareholdings, which can boost investor confidence and consequently drive up liquidity. Although insiders can take various opportunistic measures to prevent potential margin calls and forced sales, such as manipulating reported earnings, paying less in cash dividends, and cutting innovation investment, the securing effects are reversible and temporary. Once market participants realize those measures will erode stock price and harm firm value in the long run, stock liquidity might decline.

Firms that initiate buyback programs can signal to the market that the prevailing stock prices are undervalued and the stock is a “good investment” (Ikenberry et al., 1995; Vermaelen, 1981). Almeida et al. (2016) find that firms that repurchase stocks generate positive abnormal announcement returns in both the short and long term. Using Taiwanese data, Chao and Huang (2022) also find that superior operational performance is associated with stock repurchases. Moreover, stock repurchases reduce the number of external shares outstanding, improve the firm’s earnings per share with a certain amount of current surplus, and are therefore an effective method to boost stock prices when growth chances decrease (Brav et al., 2005; Renneboog & Trojanowski, 2011). Given the predominance of stock repurchases in improving investor confidence and stock prices, insiders (especially controlling shareholders) who have pledged their stocks have a strong incentive and ability to initiate buyback programs to fend off potential margin calls and forced sales, thereby increasing stock market liquidity.

Similar to stock repurchases, increased shareholdings are also an effective stock price-supporting strategy. Increased shareholdings refer to the practice of insiders using their own money to purchase shares on the secondary market and increase their holdings in the firm. In the presence of information asymmetry, when insiders believe that the firm’s stock price is undervalued, they could show their confidence in the firm’s stock price by increasing their shareholdings. From investors’ perspective, insiders’ shareholding increases represent their willingness to share the benefits and risks with outside investors. Given the positive market reaction to insiders’ increased shareholdings, insiders with share pledging have an incentive to increase their holdings to release positive signals to outside investors, consequently, leading to an increase in stock liquidity.

Consistent with our discussion above, Chou et al. (2021) find that stock repurchases are a more effective strategy than cash dividends for pledging firms to support stock prices and fend off crash risk. Chan et al. (2018) also find that firms with controlling shareholders’ share pledging are more likely to initiate buyback programs. Hillert et al. (2016) investigate the effect of realized repurchases on the liquidity of a firm’s market for its stock and find that this effect is significantly positive. Therefore, we argue that firms with insiders’ share pledging can improve the market liquidity of their stocks through engaging in price-supporting activities, that is, stock repurchases and increased shareholdings that improve investor confidence. Based on this discussion, we propose the following hypotheses:

Data and Methodology

This section describes our data collection and sample construction (Subsection 3.1), how we measured the main variables (Subsection 3.2), and finally provides descriptive statistics for these main variables (Subsection 3.3).

Data Source

We obtain daily stock trading data of listed firms from the China Stock Market & Accounting Research Database (CSMAR), which provides information on all firms listed on two major stock exchanges of China, the Shanghai and Shenzhen Exchanges (A-share market). Following standards suggested in the literature (Amihud, 2002; Hillert et al., 2016; Karolyi et al., 2012), we construct stock liquidity measures at quarterly intervals using daily trading data, including individual stock daily returns, individual stock daily trading volume, and the number of effective trading days each quarter. We then combine the quarterly liquidity measures with quarterly firm-level characteristics (described in detail in Table 1), also collected from the CSMAR, for the 15-year study period from 2007 to 2021. To ensure the robustness and reliability of our results, we conduct rigorous data-cleaning procedures:

(a) Firms traded on the STAR market (Science and Technology Innovation Board) and those in the financial sector are excluded to mitigate any idiosyncratic operational and financial characteristics, thereby enhancing the generalizability of the results.

(b) Inaccurate records, such as daily stock returns exceeding 110%, are removed to ensure data reliability.

(c) Trading records from the initial year of a firm’s listing or when the firm is under special treatment (e.g., ST and *ST) in a given quarter are also excluded for a more consistent dataset.

(d) Observations with fewer than 30 non-zero return days per quarter are excluded to ensure sufficient data points for each firm.

(e) All continuous variables are winsorized at the 1st and 99th percentiles to minimize the influence of outliers.

Variable Definitions.

After these cleaning procedures, our final sample consists of 3,587 stocks with a total of 131,282 firm-quarter observations.

Variable Measures

Liquidity Measures

We use the illiquidity measure proposed by Amihud (2002) to measure a stock’s daily liquidity, which is defined as the ratio of the absolute value of daily return to daily trading volume (Amihud’s measure). While several liquidity measures have been presented in the market microstructure literature, Amihud’s measure is generally regarded as the most effective liquidity measure in emerging markets (Karolyi et al., 2012). And Amihud’s measure is ideal for our study as it can be calculated using daily frequency data for a much longer period (Koch et al., 2016). The quarterly illiquidity is defined as the arithmetic mean of the daily illiquidity during a quarter:

where Ri,d is stock i’s daily return on day d, DVoli,d is the daily trading volume (measured in billion Chinese yuan), and N denotes the number of observations available in quarter t.

Measuring Share Pledging

We define the main explanatory variable of interest, TPledge, as a dummy variable that equals one if a firm has shares pledged by insiders at the end of a given quarter, and zero otherwise. In China, at least one-third of the listed firms have pledging controlling shareholders, who dominate the firm’s decision-making. Therefore, we adopt an alternative dummy variable, CPledge, to measure share pledging, which equals one if a firm’s stocks are pledged by the controlling shareholder at the end of a given quarter, and zero, otherwise.

Control Variables

Following the stock liquidity literature (De Cesari et al., 2011; Hillert et al., 2016; Roy et al., 2022), we control for a vector of firm- and stock-specific characteristics that may affect a stock’s liquidity. In the baseline regressions, the control variables include market risk (Mbeta) and volatility (RR), estimated by the market model using quarterly windows of daily returns; stock turnover, Tov, measured by the average daily data in a quarter; stock price, Prc, measured by the average of closing prices in a quarter; market size, Mvos, measured by the natural logs of firm’s market value. Market size and stock price are included to control for differences in liquidity among firms (stocks) of different sizes.

Omitting firm-specific characteristics may lead to biased estimates. Therefore, we also include the following firm-level control variables, which are constructed from quarterly financial data: firm size (SIZE), firm profitability (ROA), leverage ratio (LEV), book-to-market ratio (BM), institutional ownership (IO), and cash ratio (CASH). Detailed variable definitions are presented in Table 1.

Descriptive Statistics

In Panel A of Table 2, we present descriptive statistics of the main variables for our sample firms. We note that Illiq has a mean (median) of 0.054 (0.033). The mean of TPledge (CPledge) is 0.530 (0.459), suggesting that on average, approximately one-half of all sample firms engage in share pledging. Panel A also reports the summary statistics of the control variables. In our sample, an average firm has a stock turnover (Tov) of 0.264, return on assets (ROA) of 0.025, total debt-to-total assets (LEV) of 0.435, and book-to-market ratio (BM) of 0.542.

Descriptive Statistics.

Note. This table reports descriptive statistics of all variables. Panel A reports the descriptive statistics for the entire sample, while Panel B presents the mean and median of firm characteristics for the sub-samples of firms with and without share pledging. Variable definitions are presented in Table 1.

denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Panel B of Table 2 reports descriptive statistics for firms with insiders’ share pledging and those without shareholders’ pledging (pledging group and non-pledging group), and provides the results of univariate comparisons between the two groups. The mean and median values of Illiq of the pledging group are 0.050 and 0.031, respectively, significantly lower than the corresponding numbers of the non-share pledging group, 0.058 and 0.035. This is consistent with our Hypothesis H1. In addition, the results of univariate analysis for control variables also imply that the pledging group differs from the non-pledging group along several dimensions. For example, firms with insiders’ share pledging are significantly smaller, older, as well as having higher leverage and stock turnover than firms without share pledging.

Empirical Models and Results

Baseline Regression

To assess how share pledging affects stock liquidity, we estimate the following model using the ordinary least squares (OLS) based on stock-quarter panel data:

where i indexes firm, t indexes time (quarter), and εi,t is the error term. The dependent variable is Illiq, which measures stock liquidity. Controls contains a set of firm and stock-quarter characteristics that potentially affect stock liquidity as discussed in Section 3.2.3. All control variables are computed for firm i over its fiscal quarter t. We also include quarter-fixed effects (ηi) to capture intertemporal variations that may affect the relationship between share pledging and stock liquidity, as well as firm fixed effects (µi) to control for the effects of omitted firm characteristics that are constant over time. Since stock liquidity (Illiq) is likely to be autocorrelated over time, hence, we cluster standard errors by firm to avoid inflated t-statistics (Petersen, 2009). Our main interest lies in the parameter β1, which captures the effects of insiders’ share pledging on stock liquidity.

We start with a parsimonious model that regresses stock liquidity on the key variable of interest TPledge. Columns (1) and (3) of Table 3 show that the estimated coefficient TPledge and CPledge on Illiq are negative and significant, suggesting a negative association between insiders’ share pledging and stock liquidity. We then add a set of control variables as described above and report the results in Columns (2) and (4) of Table 3, the estimated coefficients of TPledge and CPledge remain negative and significant at the 1% level.

Baseline Results.

Note. This table reports OLS estimation results of regressions that investigate the effects of shareholders’ share pledging on stock liquidity. The dependent variable is Illiq. Coefficient estimates are reported and their t-statistics are shown in parentheses below. Standard errors are clustered by firm. Definitions of variables are provided in Table 1.

and ** denote statistical significance at the 1%, 5%, and 10% levels, respectively.

As to the control variables, we find that stock liquidity tends to be lower if a firm has a higher book-to-market ratio (BM), stock price (Prc), and institutional shareholding ratio (IO). These results are similar to those reported in previous studies (Brockman & Chung, 2001; Ginglinger & Hamon, 2007; Hillert et al., 2016; Stoll, 2000).

To provide more insights, we conduct a number of additional tests to examine the robustness of the OLS results. In summary, the results in Table 3 are robust to replacing the proxy for firm size (book value of total assets) with the market capitalization of equity, the use of alternative measures of share pledging, the use of all financial control variables at the prior quarter-end, controlling for the potential effects of time-variant industry and province characteristics, and the use of the firm-month sample. These robustness checks are discussed in Section 4.4, and the results are tabulated in Appendices A1 to A3. Overall, our baseline model results support Hypothesis H1.

Identification

Whereas the basic findings reported above suggest that there is a negative relationship between share pledging and stock illiquidity, our baseline results could also run the other way around. Firms with lower stock liquidity may induce insiders to pledge their shares. Another reasonable concern regarding the findings is that omitted variables associated with share pledging may be the true underlying cause of stock liquidity reduction. To address these concerns, as well as potential endogeneity and omitted variable biases, we employ a comprehensive set of empirical methods, including Difference-in-Differences (DID), Propensity Score Matching with Difference-in-Differences (PSM-DID), Two-Stage Least Squares (2SLS), and Lewbel (2012) instrumental variable approaches, to robustly assess the effect of share pledging on stock liquidity.

Difference-in-Difference Regression

The deregulation of share pledgees in May 2013 allowed securities institutions to provide loans secured by stocks, which led to a significant increase in shareholders financing by share pledging. Such a regulatory change offers an exogenous shift in stock liquidity; while it directly influences insiders’ propensity to pledge shares, it is less probable to have a direct bearing on a firm’s stock liquidity (Zhu et al., 2021). Therefore, this quasi-natural experiment allows us to explore the stock liquidity changes stemming from shifts in share pledging induced by the deregulation.

We start designate firms, where insiders pledged shares post-May 2013 for the first time, as the treatment group, maintaining this event window up to the end of the initial pledge. This accounts for 1,653 firms. In contrast, firms where insiders did not pledge any shares up to December 2021 are categorized as the non-pledging (control group), encompassing 951 firms. We then construct a regression model as follows, to compare the liquidity of firms with insiders’ share pledging and those without share pledging, using the difference-in-differences approach.

where the dependent variable Illiq is the stock market liquidity, as defined in Section 3.2.1, of firm i in quarter t. Treat is a dummy variable that equals one for treated firms and equals zero for control firms. Post is a dummy variable that equals one for observations after share pledging. Controls is a vector of control variables that could affect a firm’s stock liquidity, as defined in Section 3.2.3. µi and ηi represent firm and quarter fixed effects, respectively, and standard errors are clustered at the firm level in all regressions.

We are interested in the key coefficient of the interaction term Treat × Post, which is the DID estimator that shows the causal impact of insiders’ share pledging on stock liquidity. The key coefficient we are interested in is the interaction term Treat × Post, which is the DID estimator that shows the causal impact of insiders’ share pledging on stock liquidity. The key coefficient of interest is the interaction term Treat × Post, which is the DID estimator that measures the differences in stock liquidity between the treatment and the control groups. We report the DID regression results of Model (3) in Columns (1) and (2) of Table 4, it can be observed that both the estimates of coefficient on Treat × Post on Illiq are negative and significant at 1% level.

DID and PSM-DID Regression Results and Balance Test.

Note. This table presents the results of DID and PSM followed by PSM-DID regression analyses, alongside a balance test, to assess the effect of insiders’ share pledging on stock liquidity. Panel A presents the regression results for assessing the impact of insiders’ share pledging on stock liquidity, using a difference-in-differences (DID) and Propensity Score Matching (PSM-DID) approach. Columns (1) to (6) depict various model specifications and sub-samples. Panel B displays the post-matching balance test, confirming the effectiveness of the matching approach with post-match standardized biases for all controlled variables remaining below an absolute 10%. The matching variables include firm size (SIZE), age (AGE), leverage ratio (LEV), book-to-market value ratio (BM), current ratio (CURI, defined as the firm’s current assets divided by current liabilities), cash ratio (CARI, defined as the firm’s cash and cash equivalents divided by its current liabilities), growth rate in revenue (SP, calculated as the year-over-year change in revenue, normalized by revenue from the prior year), and Tobin’s Q ratio (Tobin Q). Standard errors are clustered at the firm level across all regressions. Definitions for other control variables are provided in Table 1. Firm and quarter fixed effects are controlled for in all regressions, and standard errors are clustered at the firm level. t-Statistics are reported in parentheses. All variable definitions are reported in Table 1.

and ** denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Considering that some firms went public after 2013, we, therefore, exclude these firms, based on the treat and control groups selected above, to further examine the changes in stock liquidity after the changes in share pledging caused by the deregulation. And then we re-estimate Model (3) based on this sub-sample. The results are shown in Column (3) of Table 4. In addition, we redefine firms whose shareholders pledged shares for the first time after May 2013, and continue to have not ended their release until December 2021 as the treatment group, with a total of 845 firms. The results are shown in Column (4) of Table 4. Overall, the results are in line with our baseline results, providing further support to our hypothesis.

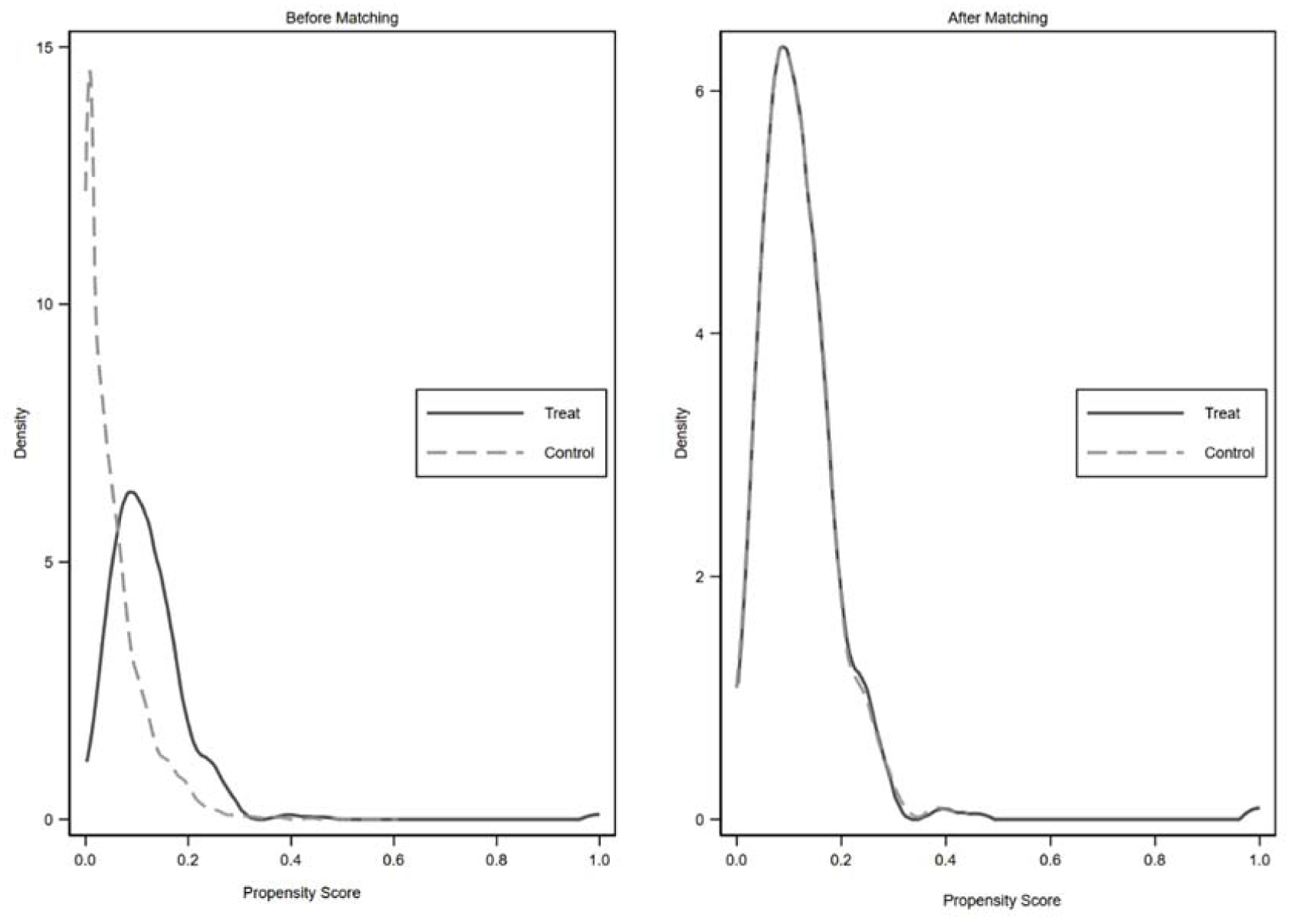

To reinforce the causal interpretation of our findings, we extend our analysis by employing the Propensity Score Matching approach. Specifically, for each firm in the treatment group that initiated and concluded share pledging within a particular timeframe, we use data from the year prior to the start of pledging to identify a match from the control group. The matching firm is one that had not engaged in share pledging by the time the treated firm concluded its pledging. This matching approach enhances the credibility of our findings by ensuring a more apples-to-apples comparison between the treated and control groups.

Post-matching balance checks confirm the efficacy of our matching approach. Figure 1 demonstrates that the distributions of propensity scores for both the treatment and control groups show no significant differences across all controlled variables, and the post-match standardized biases for these variables remain below an absolute 10%, as detailed in Panel B of Table 4. This attests to the effectiveness of our matching in ensuring a balanced comparison between the two groups. We then re-estimate Model (3) using this PSM-DID combined approach and present these results in Columns (5) and (6) of Table 4. The PSM-DID results are consistent with our baseline DID estimates, thereby reinforcing the robustness of our primary findings.

Balance test.

This figure displays the PSM balance test results. The results show no significant differences between the control and treatment groups across all control variables after matching.

Instrumental Variable Approaches: 2SLS and Lewbel

We also employ both the Two-Stage Least Squares (2SLS) approach and the instrumental variable technique developed by Lewbel (2012) to address the potential endogeneity in assessing the effects of insiders’ share pledging on stock liquidity.

The 2SLS approach requires that the instrument be correlated with the propensity of controlling share pledging, but uncorrelated with stock liquidity, except indirectly via share pledging. According to this identification requirement, we construct the instrumental variables AvgProRio and AvgIndRio, as “the average percentage of shares pledged by controlling shareholders of firms in the same province” and “the average percentage of shares pledged by controlling shareholders of firms in the CSRC 2-digit industry.” Firms in the same province and industry may have comparable financing strategies and desires for external financing, which may influence the willingness of insiders’ share pledging (Chang et al., 2022; Pang & Wang, 2020; Xia et al., 2022). Therefore, AvgProRio and AvgIndRio separate the more exogenous component of insiders’ share pledging. The first-stage F statistics in Columns (1) and (2) are larger than 10 (776.03 and 1297.00), with the p-value being .001, and the partial R2 is considerably large (.161 and .130) indicating that the instruments are valid.

Table 5 shows our estimation results of the 2SLS analysis. Columns (1) and (2) show the first-stage regression results with TPledge and CPledge as the independent variables, respectively. The main variables of interest are AvgProRio and AvgIndRio. All other control variables are the same as those in the baseline regression Equation 2. The coefficients of AvgProRio and AvgIndRio are positive and significant at the 1% level, indicating that the instrument is significantly correlated with share pledging. Columns (3) and (4) of Table 5 report the results from the second-stage regression, which are Equation 2 with the main variable of interest replaced by the fitted values of TPledge and CPledge from the first-stage regression. Columns (3) and (4) present the results with Illiq as the dependent variable. Consistent with the findings from the OLS analysis, the coefficient estimate of TPledge (CPledge) is negative and significant at the 1% level.

Endogeneity Test Results: Two-Stage Least Squares (2SLS) and Lewbel Instrumental Variable.

Note. This table presents the endogeneity test results, assessing the impact of insiders’ share pledging on stock liquidity using Two-stage least squares (2SLS) and Lewbel (2012) instrumental variable approaches. Panel A focuses on the 2SLS method. Columns (1) and (2) display the first-stage regression results, where TPledge and CPledge serve as the independent variables. Columns (3) and (4) report the second-stage regression results, which indicate the fitted values of TPledge and CPledge. Panel B presents the results from the Lewbel (2012) method. Columns (5) and (6) report the corresponding results for TPledge and CPledge. Firm and quarter fixed effects are controlled for in all regressions. Standard errors are clustered at the firm level. t-Statistics are reported in parentheses. Definitions for other control variables are provided in Table 1.

, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

We also employ the Lewbel (2012) technique, which has been widely used in recent corporate finance literature (Y. Chen et al., 2021; Hasan et al., 2021; Mavis et al., 2020). This approach becomes crucial when traditional external instruments are either unavailable or their validity is questionable, as Lewbel’s method generates endogenous instruments from the existing data to establish causality. The results of this method, as reported in Columns (5) and (6) of Table 5, also indicate that both TPledge and CPledge are significantly and negatively correlated with stock illiquidity, thus corroborating our primary findings.

Overall, the results suggest that insiders’ share pledging can significantly improve stock liquidity.

Mechanism of Improvement Effects of Share Pledging on Stock Liquidity

Although we find that share pledging by insiders has a positive causal effect on stock liquidity, the mechanism through which share pledging improves liquidity remains unclear. In this section, we explore the possible underlying economic mechanisms behind this. Stock repurchase and increased shareholdings could be the underlying mechanisms. Because insiders with share-loan pledges have incentives to boost stock prices once the share pledging process begins, knowing that they are at risk of margin calls and forced liquidations (Chan et al., 2018; Guo et al., 2021). Initiating buybacks and increasing shareholdings can signal to the market that the stock is undervalued, hence enhancing stock trading activity and improving stock liquidity (Hillert et al., 2016). Subsections 4.3.1 and 4.3.2 examine these mechanisms, respectively.

Stock Repurchases

In this subsection, we delve into whether stock repurchases act as a channel for improving stock liquidity following insiders’ share pledging activities. Stock repurchases have long been studied as a form of insider trading that sends potent value signals to investors (Barclay & Smith, 1988; Brockman & Chung, 2001; De Cesari et al., 2011; Hillert et al., 2016). The practice of corporate repurchasing activities is not just about signaling firm strength, it is a multi-faceted strategy that holds unique implications for firms with insider share pledging. The signaling power of stock repurchases is especially amplified when insiders have share pledges on the line. Studies by Chan et al. (2018) and Guo et al. (2021) robustly demonstrate a significant positive correlation between insiders’ share pledging activities and the initiation of stock repurchases.

In such contexts, insiders are more driven to stabilize stock prices to mitigate the margin calls associated with pledged shares (Chan et al., 2018), serving as an effective counterweight to potential market skepticism. This aligns well with traditional signaling theories and the empirical evidence from previous works such as Hillert et al. (2016), which reveals the liquidity-boosting effects of corporate repurchases.

Moreover, the proportion of insider ownership in a pledged-share environment becomes a critical focal point. Stock repurchasing offers a dual advantage: it not only elevates the value of each share by reducing the volume of shares in circulation but also solidifies insiders’ control over the firm. This often catalyzes positive market sentiments about the firm’s prospects, a crucial asset when insiders are navigating the complexities of share pledges. Rooted in traditional signaling theory, an announcement of stock repurchase often acts as a reliable indicator of a firm’s robust fundamentals and optimistic future outlook. This is especially salient in an emerging market context like China, where retail investors are significantly influenced by such actions. To test this conjecture, we estimate the following model:

where i indexes firm, t indexes time (quarter), and εi,t is the error term. The dependent variable, Illiq, captures stock liquidity. We add the new variable, Repurchase, which equals one for firm-quarters with buyback programs (zero otherwise), and the interaction term between TPledge and Repurchase. The coefficient estimate of the interaction term reflects the different effects of share pledging on stock liquidity for firms that initiate repurchase programs. All other variables are defined in Table 1.

The interaction term in Equation 4 is the key variable of interest in this analysis. If our conjecture is correct, that is, if more share pledging firms take advantage of stock repurchases to support stock prices, then we expect β1 to be negative and significant. We report the regression results in Table 6. Both the coefficients of TPledge × Repurchase and CPledge×Repurchase are negative and significant, suggesting that stock repurchase is a possible mechanism through which share pledging improves stock liquidity.

Share Pledging and Stock Repurchases.

Note. The table reports the results of how stock repurchases affect stock liquidity for firms with insiders’ share pledging. Firm and quarter fixed effects are included in the regressions. Definitions of variables are presented in Table 1.

and ** indicate significance at the 1%, 5%, and 10% levels, respectively.

Increased Shareholdings

We next explore another intriguing channel by which insiders can inject liquidity into the stock—increased shareholdings. Like stock repurchases, insider shareholdings serve as a strong signal of firm strength and insider confidence, attracting new investment and bolstering existing shareholder trust.

In the aftermath of share pledging, insiders often increase their shareholdings in the firm, presenting an intriguing mechanism that has the potential to positively affect stock liquidity. From a signaling perspective, increased shareholdings can act as a strong signal to the market about the insiders’ confidence in the firm’s future prospects. This not only attracts new investors but also reinvigorates the trust of current shareholders, thus injecting liquidity into the stock.

Further adding nuance to this mechanism, increased shareholdings stabilize control rights, avoiding off potential shareholder conflicts that could otherwise roil the market and cause volatility. This stabilization is particularly crucial in the context of share pledging, where the risk of losing control rights looms large. Moreover, the action of increasing shareholdings can be seen as a buffer against the crash risks often associated with share pledging. It mitigates the impact of potential margin calls and in doing so, alleviates one of the key concerns that might deter would-be investors from entering the market.

To test this hypothesis, we define a dummy variable, Increase, which equals one if the firm makes an increased shareholdings announcement after insiders’ share pledging, and zero otherwise. In order to ensure that increased shareholdings by insiders is indeed related to their share pledging, we exclude those listed firms whose announcement of the increase in shareholdings does not fall between the start and end quarters of share pledging, and only the firm-quarter observations for firms with share pledging before the end of the first pledge remain. Then we estimate the following model:

We are interested in examining whether the estimated coefficient β1 in Equation 5 is significantly negative. If it does, suggest that increased shareholding is a mechanism by which share pledging enhances stock liquidity. Table 7 presents the results. In Columns (2) and (4), the coefficients of TPledge × Increase and CPledge × Increase are significantly negative after controlling for a set of important control variables related to stock liquidity, as well as firm and time fixed effects, indicating that an increase in insider ownership after share pledging leads to increased stock liquidity.

Share Pledging and Increased Shareholdings.

Note. The table reports the results of how increased holdings stock liquidity for firms with insiders’ share pledging. Firm and quarter fixed effects are included in the regressions. Definitions of variables are presented in Table 1.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Overall, the evidence presented in this section suggests that stock repurchases and increased holdings due to share pledging positively affect stock liquidity, that is, stock repurchases and increased holdings are potential mechanisms by which share pledging enhances stock liquidity.

Robustness Checks

We conduct a variety of additional tests to check the robustness of our baseline results. For brevity, we report the results of the following four sets of robustness checks in Tables A1 to A3 in the Appendix.

First, although we use two dummy variables to measure the presence of share pledging in this study, we admit that the magnitude of share pledging also matters. The higher number of shares pledged by insiders may reflect their confidence in the firm’s stock price. Therefore, we use the aggregate number of shares pledged by all shareholders as a percentage of the firm’s total shares outstanding at the end of each quarter (TPleRio) as an alternative measure of share pledging, and the aggregate number of shares pledged by controlling shareholders as a percentage of their shareholdings (CPleRio). The results in Columns (1) and (2) of Appendix A1 show that the coefficients of TPleRio and CPleRio are always negative and significant, which is consistent with what we observed for the relationship between share pledging and stock liquidity.

Second, to control for the potential effects of time-variant industry and province characteristics, we further add industry × quarter- and province × quarter-fixed effects in our baseline model, and the results in Columns (3) and (4) of Appendix A1 show that the relationship between share pledging and stock liquidity is not affected.

Third, In Columns (1) and (2) of Appendix A2, we perform baseline tests by replacing the firm size SIZE (measured by the natural logarithm of the firm’s market value in quarter t) with the natural logarithm of firm i’s total assets at the end of quarter t. In addition, we use one-quarter lag control variables, including BM, LEV, ROA, IO, and CASH, all as defined in Section 3.2.3. The results are reported in Columns (3) and (4) of Appendix A2. Our results remain robust to an alternative definition of the firm size and the lagged control variables.

Fourth, to further capture the changes in stock liquidity, we also use alternative sample selection, that is, replacing the quarterly sample with a monthly sample to check our baseline findings. The test results reported in Appendix A3 indicate that our baseline results remain unchanged.

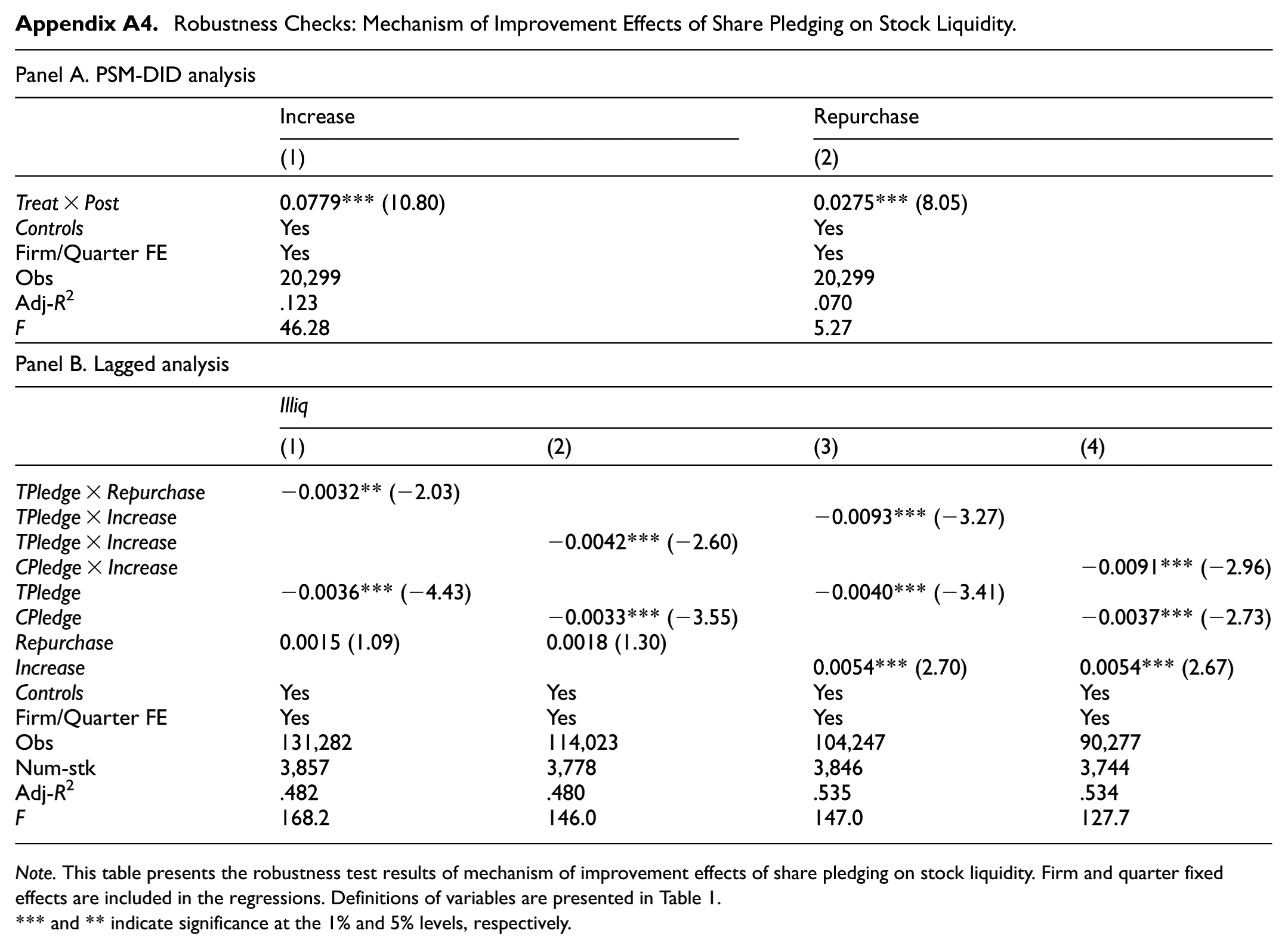

Finally, to more rigorously establish the mechanisms through which share pledging impacts stock liquidity, we conduct additional tests to clarify the causal relationships involved. Firstly, we employ a sample from our PSM-DID approach as described in Section 4.2.1. Using this approach allows us to control for observable variables, minimize selection bias, and isolate the impact of share pledging on consequential corporate behaviors such as stock repurchasing and increase holdings. The regression results, reported in Panel A of the Appendix 4, indicate that insiders’ share pledging does lead to changes in share repurchasing and increasing holding behaviors. Secondly, we enhance our models by incorporating lagged variables specifically for stock repurchasing and increased holdings into Models 4 and 5, respectively. The results of these robustness checks, presented in Appendix A4, lend further support to our hypothesis that stock repurchases and increased holdings serve as channels through which share pledging influences stock liquidity.

Overall, the evidence presented above suggests that insiders’ share pledging is positively related to stock liquidity.

Discussion and Conclusion

Share pledging by corporate insiders has long been a topic of interest, particularly in environments like China where controlling shareholders wield significant influence over corporate governance. Existing research has primarily painted a negative picture of share pledging, emphasizing its potential adverse impacts. This study brings new insights by exploring its impact on stock liquidity, an essential financial metric crucial for a firm’s sustainability and growth prospects.

Our empirical analysis reveals a surprising but significant finding: insiders’ share pledging is positively associated with enhanced stock liquidity. This positive relation is further strengthened by the fact that firms with insider share pledging are more likely to engage in share buybacks and expand their shareholdings, corroborating earlier studies (Chan et al., 2018; Chou et al., 2021). Such corporate behaviors amplify investor expectations, thereby driving market liquidity upwards for such firms.

As a broader implication, this research addresses an important economic question: How do corporate financial behaviors intersect with market mechanics, and what does that mean for economic sustainability? Our findings indicate that insider share pledging can enhance stock liquidity, potentially making the firm more attractive to investors and impacting the overall economic environment positively. While our study is based on the Chinese market, similar economic principles could apply in other emerging markets with significant insider ownership. As such, policymakers and economic strategists can consider our findings when crafting regulations or economic models that aim to balance corporate governance with market liquidity.

The insights gained from this study have multiple practical applications. Regulators, corporate insiders, investment professionals, and market analysts all stand to benefit from these findings. For instance, corporate insiders could better strategize their share pledging activities, knowing that it could positively affect their firm’s stock liquidity and consequently the market perception of their firm. For investment professionals, the findings could serve as a risk assessment tool. If share pledging is related positively to stock liquidity, this could be considered less of a red flag than traditionally assumed, enabling more nuanced investment decisions. Market analysts could similarly benefit from our research by incorporating these insights into more accurate evaluations of market dynamics and firm valuations.

Limitations and Future Research

It is important to acknowledge the limitations of our study. Our sample predominantly comprises Chinese firms, which could narrow the applicability of our findings to other cultural or regulatory settings. Additionally, the study focuses on a specific time period, and changing market conditions could potentially alter the relationships we have observed.

In an era where the sustainability of business operations is under scrutiny, our research also raises questions for further study. The relationship between share pledging and key sustainability indicators like ESG (Environmental, Social, and Governance) performance and innovation remains an open area for future investigation. As insiders’ financial behaviors influence stock liquidity, a critical measure of a company’s market stability, it would be worthwhile to examine how these behaviors intersect with broader sustainability objectives.

Footnotes

Appendices

Robustness Checks: Mechanism of Improvement Effects of Share Pledging on Stock Liquidity.

| Panel A. PSM-DID analysis | ||||

|---|---|---|---|---|

| Increase | Repurchase | |||

| (1) | (2) | |||

| Treat × Post | 0.0779*** (10.80) | 0.0275*** (8.05) | ||

| Controls | Yes | Yes | ||

| Firm/Quarter FE | Yes | Yes | ||

| Obs | 20,299 | 20,299 | ||

| Adj-R2 | .123 | .070 | ||

| F | 46.28 | 5.27 | ||

| Panel B. Lagged analysis | ||||

| Illiq | ||||

| (1) | (2) | (3) | (4) | |

| TPledge × Repurchase | −0.0032** (−2.03) | |||

| TPledge × Increase | −0.0093*** (−3.27) | |||

| TPledge × Increase | −0.0042*** (−2.60) | |||

| CPledge × Increase | −0.0091*** (−2.96) | |||

| TPledge | −0.0036*** (−4.43) | −0.0040*** (−3.41) | ||

| CPledge | −0.0033*** (−3.55) | −0.0037*** (−2.73) | ||

| Repurchase | 0.0015 (1.09) | 0.0018 (1.30) | ||

| Increase | 0.0054*** (2.70) | 0.0054*** (2.67) | ||

| Controls | Yes | Yes | Yes | Yes |

| Firm/Quarter FE | Yes | Yes | Yes | Yes |

| Obs | 131,282 | 114,023 | 104,247 | 90,277 |

| Num-stk | 3,857 | 3,778 | 3,846 | 3,744 |

| Adj-R2 | .482 | .480 | .535 | .534 |

| F | 168.2 | 146.0 | 147.0 | 127.7 |

Note. This table presents the robustness test results of mechanism of improvement effects of share pledging on stock liquidity. Firm and quarter fixed effects are included in the regressions. Definitions of variables are presented in Table 1.

and ** indicate significance at the 1% and 5% levels, respectively.

Acknowledgements

We thank the reviewers for their constructive comments.

Ethical Considerations

Not applicable.

Authors’ Contributions

Junping Zhang: Conceptualization, Methodology, Investigation, Data Curation, Writing-Original draft preparation, Project administration. Ping Li: Investigation, editing, proofreading, and language editing. Yong Li: Methodology, revising, proofreading, funding.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China [71873022] and the National Social Science Foundation of China Major Project, “Research on the Statistical Measurement Theory and Application of Industrial Big Data” [21&ZD153].

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets used or analyzed during the current study are available from the corresponding author upon reasonable request.