Abstract

In the aftermath of the 2007–08 financial crisis, the worsening financial conditions of households increased concerns about their financial vulnerability (FV). In this context, policymakers embraced the notion of financial knowledge to foster sound financial behaviors among individuals and households, aiming to mitigate the detrimental effects of FV on households’ financial wellbeing and the overall economy. However, the relationship between FV and financial literacy remains inconclusive. This lack of definitive findings may stem from limitations in measuring FV and narrow focus on specific dimensions of financial literacy. This paper analyzes the relationship between financial literacy and FV by creating a comprehensive measure of (the level of) FV and considering different dimensions of financial literacy. Using a sample of 8,554 individuals in Spain obtained from the 2016–17 Survey of Financial Competences, we construct a continuous measure of FV by using Nonlinear Principal Components Analysis (NLPCA). Then, we employ OLS and ordered probit regressions to examine the potential association between different dimensions of financial literacy and FV. The findings indicate that the level of FV is negatively related to self-perceived financial knowledge, while no statistically significant relationship is found regarding objective financial knowledge. Evidence also reveals that “highly financially included” individuals are more likely to exhibit financial resilience. These findings highlight the need for the development of financial education initiatives that are action-oriented.

Keywords

Introduction

Over the last decade, research on household financial vulnerability (FV) has gained momentum (Azzopardi et al., 2019) due to increasing concerns about worsening in households’ financial conditions (Anderloni et al., 2012), particularly after the 2007–08 financial crisis. FV not only poses detrimental effects at the household level but also has far-reaching implications for the economy (Ali et al., 2020; Ampudia et al., 2016) and the stability of the financial system (Azzopardi et al., 2019; Noerhidajati et al., 2021).

In an attempt to alleviate the FV, policymakers have focused on enhancing financial literacy. It is widely acknowledged that a significant portion of the population lacks the necessary financial knowledge to make informed decisions (Anderloni et al., 2012; Sherraden, 2013). However, the effectiveness of these policies is still being evaluated, and some scholars point to a weak connection between financial knowledge and positive financial behaviors (Disney & Gathergood, 2011; Fernandes et al., 2014; Loke, 2017; Nicolini & Haupt, 2019).

One possible explanation for this inconclusive evidence is the lack of a common definition of FV (Fernández-López, Álvarez-Espiño, Rey-Ares, & Castro-González, 2023; Seldal & Nyhus, 2022; Singh & Malik, 2022). Consequently, researchers have resorted to measuring FV using a single financial behavior or perspective, either objective or subjective. As a result, households are typically classified as either financially vulnerable or financially non-vulnerable, rather than considering that households can suffer from different levels of FV (O’Connor et al., 2019). In line with these methods of measuring FV, it is not surprising to read that in 2018, approximately 30% of EU households were considered financially fragile as they were unable to cope with an unexpected expense (Demertzis et al., 2020). To the best of our knowledge, only Anderloni et al. (2012), Daud et al. (2019), Fei et al. (2020), and Singh and Malik (2022) have developed a FV index, with the aim of providing a more comprehensive assessment of household FV.

Another possible explanation lies in how financial literacy has been measured. Whereas objective financial knowledge has been measured more consistently than FV, other dimensions of financial literacy have received limited attention. Particularly, few studies have investigated the role of self-reported financial knowledge (Allgood & Walstad, 2016; Daud et al., 2019; Lee et al., 2018; Loke, 2017), even though it can impact financial behavior through different mechanisms than objective financial knowledge, such as confidence (Allgood & Walstad, 2016; Wiersma et al., 2020). Consequently, recent research has emphasized the importance of jointly considering objective and self-reported financial knowledge to enhance the understanding of decision-making processes (Hauff et al., 2020). Additionally, while the objective financial knowledge increases an individual’s “ability to act,” the “opportunity to act” (i.e., financial and/or banking inclusion) is also required for sound financial decisions (Johnson & Sherraden, 2007). The combination of both aspects has been referred to as “financial capability” in recent literature (Fernández-López, Álvarez-Espiño, Castro-González, & Rey-Ares, 2023; Friedline & West, 2016; Sherraden, 2013). Despite numerous studies exploring the relationship between FV and financial knowledge, only Friedline and West (2016) have considered financial capability as a potential determinant of FV.

This paper aims to fill the gaps identified in previous literature. It analyzes the relationship between financial literacy and FV by creating a comprehensive measure of (the level of) FV and considering different dimensions of financial literacy, going beyond objective financial knowledge. By gaining a deeper understanding of FV, this research aims to inform the design of more effective interventions to promote financial resilience, reduce financial exclusion (Daud et al., 2019), and alleviate poverty (Ali et al., 2020).

This paper makes the following contributions. Firstly, it extends the empirical research on FV by constructing an index based on a more comprehensive definition of FV, which has been lacking in existing literature (O’Connor et al., 2019). While Anderloni et al. (2012), Daud et al. (2019), Fei et al. (2020), and Singh and Malik (2022) have previously attempted this approach, their FV indexes primarily focuses on consumption-related issues, overlooking individuals’ self-perception of their financial situation. Secondly, this paper explores diverse dimensions of financial literacy, beyond objective financial knowledge. In so doing, it offers insights into the different relationships between financial literacy constructs and FV. Thirdly, it expands the empirical evidence by presenting new findings from Spain, a South-European country of interest for the analysis due to its relatively low financial literacy levels (Arrondel et al., 2021) and moderately high levels of FV (Arellano & Cámara, 2021).

The remainder of the paper proceeds as follows. Section 2 provides the theoretical framework and hypothesis development. Section 3 describes the data used in the analyses and the construction of the FV index. Section 4 presents the results of the multivariate analyses and Section 5 outlines the discussion remarks.

Literature Review and Hypothesis Development

Measuring Household Financial Vulnerability

In recent years, household FV has gained the attention of scholars and policymakers. Some studies have defined FV as a consequence of high levels of household debt (Allgood & Walstad, 2016; Disney & Gathergood, 2011; Ray et al., 2019), while broader definitions encompass households’ inability to meet basic living expenses (Loke, 2016; Singh & Malik, 2022) or unforeseen expenses (Lusardi et al., 2011; Philippas & Avdoulas, 2020), as well as to raise a given amount of funds to tackle a rush (Friedline & West, 2016; Lusardi et al., 2011; Philippas & Avdoulas, 2020; West & Mottola, 2016). Additionally, adverse economic shocks (e.g., interest or unemployment rates, adjustments in housing or retirement accounts…) can also render households financially vulnerable (Ali et al., 2020).

The lack of a common definition of FV has led to a considerable number of measures. Fernández-López, Álvarez-Espiño, Rey-Ares, & Castro-González (2023) propose classifying these measures according to four criteria (Table 1). The first criterion differentiates measures that focus on household debt-related issues (4 out of 23 studies) from those focus on consumption or saving, such as covering basic living expenses (Loke, 2016) or quickly raising emergency funds (14 out 23 studies). Few studies have used measures based on indebtedness and on consumption and saving capacity simultaneously (5 out of 23 studies).

Summary of the Studies Relating Financial Knowledge and FV.

Note.*The study does not provide additional information on the financial literacy variable. **The questions used in the study are similar to those proposed by Lusardi and Mitchell (2011), and the variable name reflects the authors’ terminology. 1Mostly based on consumption or saving capacity, including some debt-related issues. 3A single measure that combines two items, one of them related to debt. 4A single measure that aggregates six questions related to debt. 5The specific details of the ordinal scale are not provided. 2Several models are estimated with different control variables and/or subsamples, yielding different results. +/–/N.S./N.C. indicate positive/negative/non-significant association / not considered relationship, respectively. OLS refers to Ordinary Least Square. Cont. stands for continuous variable; (0–1) represents dichotomous variables; and (#–#) represents scalar variables.

The second criterion distinguishes between objective and subjective measures of FV (Fasianos et al., 2014). While the former can be obtained from an outside source (e.g., savings, credit history, or financial assets), the latter requires the assessment of the individuals (O’Connor et al., 2019), as they refer to their self-perception of financial circumstances. Objective measures of FV have been the most widely used in existing literature (Fernández-López, Álvarez-Espiño, Rey-Ares, & Castro-González, 2023). However, considering objective and subjective measures together enriches the analysis, as individuals’ financial behavior is also influenced by their self-perception of the financial situation (Brüggen et al., 2017). Indeed, 7 out of the 23 studies summarized in Table 1 combine objective and subjective measures.

The third classification criterion deals with the number of items used to construct the FV measure. Most FV measures are derived from a single item, thereby identifying FV with a single debt or consumption/saving aspect, either objectively or subjectively. To account for the multidimensional nature of the phenomenon, some authors opt for using several measures of FV based on a single item (Allgood & Walstad, 2016; Chotewattanakul et al., 2019; Seldal & Nyhus, 2022), while others overlook this multidimensional nature and merely use a single measure of FV (Parise & Peijnenburg, 2019; Philippas & Avdoulas, 2020; Wiersma et al., 2020). As far as we know, only Anderloni et al. (2012) and Fei et al. (2020) have integrated several items that encompass debt and consumption and saving capacity into an index of FV.

The fourth criterion refers to the approach used to operationalize FV. As can be seen in Table 1, dichotomous variables are predominantly used (15 out of the 23 papers), resulting in households being categorized as either “financially vulnerable” or “not financially vulnerable,” rather than assuming that a household can be financially vulnerable to some degree (O’Connor et al., 2019). In the latter case, continuous variables are more appropriate (Abdullah Yusof et al., 2015; Anderloni et al., 2012; Disney & Gathergood, 2011). An intermediate approach involves creating an ordinal scale for FV, which has been done by nine of the studies analyzed, with five of them based on a single item, mostly subjective, and associated with consumption and saving capacity (Abdullah Yusof et al., 2015; Giannetti et al., 2014; Loke, 2017; McCarthy, 2011; Seldal & Nyhus, 2022).

In summary, the measurement of FV in the empirical literature has presented four main limitations: (1) it has mostly focused on a single household financial aspect (or item); (2) it has been based on debt-related issues or consumption or saving capacity issues, rarely considering both simultaneously; (3) it has been based on either objective or subjective measures without adequate integration of both; and (4) it has been operationalized as a binary distinction of being financially fragile or not. Only Anderloni et al. (2012), Daud et al. (2019), Fei et al. (2020), and Singh and Malik (2022) have attempted to construct a comprehensive FV index. Following their empirical approach this paper goes further, by considering subjective measures, while also balancing debt-based and consumption- and savings-based measures.

Measuring Financial Knowledge

There are numerous studies that analyze the driving forces of FV at the household level (see Fernández-López, Álvarez-Espiño, Rey-Ares, & Castro-González (2023) for a recent review). Among these factors, the role of financial literacy has been extensively researched (see Table 1), leading to several conclusions. Firstly, financial literacy has been consistently measured compared to FV. As objective financial knowledge serves as the core measure of financial literacy (Yuan et al., 2023), six studies use ordinal scale variables based on responses to the Big Three or Big Five financial literacy questions proposed by Lusardi and Mitchell (2011). These papers often report that financially illiterate households are more likely to be financially fragile; however, not all studies yield conclusive results (Disney & Gathergood, 2011; Wiersma et al., 2020).

Secondly, few studies consider self-perceived financial knowledge, alongside objective one (i.e., Allgood & Walstad, 2016; Lee et al., 2018; Loke, 2017; Wiersma et al., 2020). These studies reveal a negative relationship between the former and FV. This empirical evidence supports the inclusion of the self-perceived dimension of financial literacy since it may impact financial behavior through mechanisms that go beyond objective financial knowledge (Allgood & Walstad, 2016; Wiersma et al., 2020). Thus, individuals need objective financial knowledge and a sense of confidence in their ability do make smart financial decisions (Ghadwan et al., 2023).

Thirdly, there is a limited number of studies that consider additional aspects to complement the assessment of financial literacy, such as financial inclusion (Friedline & West, 2016), investment skills (McCarthy, 2011), behaviors and attitudes (Chotewattanakul et al., 2019; Daud et al., 2019), or mathematics skills (Lee et al., 2018). These studies consistently show a negative relationship between financial literacy and FV, regardless of how the latter is measured. In this regard, a particularly relevant study is that of Friedline and West (2016), which aligns with a recent strand of financial literacy research advocating for the joint consideration of financial knowledge and its practical application (Sherraden, 2013; Sherraden & Ansong, 2016), rather than analyzing these two factors separately. This approach involves combining measures of “objective financial knowledge” with measures of “access to and use of financial services and products” (Sherraden & Ansong, 2016) into a unified index that captures “financial capability.” Indeed, Friedline and West (2016) find that, compared to financially excluded millennials, those who are financially capable are three times more likely to be able to cope with an unexpected expense and, therefore, they are less financially vulnerable.

Hypothesis Development

The arguments behind the influence of financial literacy on FV are grounded within the theory of bounded rationality (Simon, 1956, 2000). This theory proposes that individuals face limitations in their ability to make optimal decisions due to the increasing complexity of the financial environment (Ibrahim & Khaimah, 2009), information asymmetries (Simon, 1956), and scarcity of resources such as information, time, or money (Schneider & Angelmar, 1993). Thus, the vast array of choices, considering the numerous decisions humans make daily (Riaz et al., 2022), contrast with the limited time for reflection and the unavailability of up-to-date information (Simon, 1956).

In this context, people rely on heuristics and animal spirits (Keynes, 1936) as an alternative when confronted with complex and uncertain decisions (Simon, 1956). However, they must acknowledge the potential for assessment errors driven by cognitive biases (Slovic, 1972). Consequently, people need tools to analyze the available information and make decisions that can address their financial limitations (Sherraden & Ansong, 2016). Financial literacy enables individuals to evaluate complex financial products or services (Riaz et al., 2022), such as loans or saving plans (Bayar et al., 2020), and make decisions that are in their best long-term interests (Kim et al., 2019). Therefore, financial knowledge may be positively related to financial resilience. Hence, we propose the following hypothesis:

H1: Financial literacy is negatively related to household FV.

In sum, the aim of this paper is to analyze the relationship between the relationship between financial literacy and FV while addressing the limitations in how each variable is measured in existing literature. To measure FV, we construct an index that encompasses objective and subjective factors, along with aspects related to debt and consumption and saving capacity. Additionally, we go beyond examining solely objective financial knowledge, as commonly done in previous studies on FV, by considering self-perceived financial knowledge and financial capability. This approach offers a more comprehensive view of FV and a better understanding of its relationship with different dimensions of financial literacy.

Data and Variables

The Sample

Data are extracted from Survey of Financial Competences (ECF by its Spanish acronym), a joint initiative developed by the Bank of Spain and the National Securities Market Commission (Banco de España and CNMV, 2018). The survey was conducted between 2016 and 2017 to assess the financial competences of the adult population in Spain. It contains 10 questions on financial knowledge, three of which coincide with those proposed by Lusardi and Mitchell (2011) and are commonly used in existing literature (Table 1). The ECF also includes socio-demographic, economic, and behavioral characteristics of Spanish households. Additionally, the ECF provides cross-sectional weights to account for the potential bias stemming from stratified sampling and item non-response (Bover et al., 2019). These sample weights have been employed in all subsequent calculations.

The study sample comprises 8,554 individuals. The average age is approximately 47 years, and the sample is gender balanced (Table 2). Most of the sampled households consist of individuals living together (65.11%), without cohabiting with children under 18 years old (68.87%). As regards the educational attainment, almost 50% of the respondents have attained at least upper secondary education. Regarding economic features, most individuals (53.07%) are employed and/or self-employed. About one third of the sample (36.97%) report an annual household income below €14,500, whereas a smaller percentage (13.60%) report an annual household income exceeding €45,000. Regarding risk preferences, 43.92% of respondents are risk averse, as they agree or fully agree that they are not “prepared to risk some of their money when saving or making investments.” The remaining 56.08% of individuals could be considered riskier investors.

Descriptive Statistics: Respondents’ Profiles.

The Dependent Variable: The FV Index

Similar to Anderloni et al. (2012), Daud et al. (2019), Fei et al. (2020), and Singh and Malik (2022), we propose an index of FV that addresses certain limitations found in previous FV measures. Our approach involves constructing a continuous index that encompasses multiple dimensions of FV. Table 3 shows six variables available in the ECF, which have been widely used in the literature as proxies for FV. These variables refer to issues related to consumption and saving capacity (i.e., perception of current financial situation, timely bill payment, overspending, or lack of emergency funds) and debt-related concerns (i.e., perception of indebtedness and delays in debt payment). Half of these variables rely on self-reported data, capturing the subjective perception of households’ financial difficulties, while the other half can be considered objective measures of an individual’s financial circumstances. By considering various dimensions, the FV index offers a comprehensive view of this multidimensional phenomenon, measured in terms of levels or degrees of FV. This approach acknowledges that every household can experience some degree of FV.

FV Variables: Definition, Mean Values, and Studies.

Note.*indicates that in the NLPCA the items of answers have been reversely ordered, from the lowest to the highest, in terms of their potential impact on FV.

Regarding individuals’ perceptions of their financial situation (i.e., subjective measures), over 90% of the respondents consider that they pay their bills on time, and approximately 13% feel excessively indebted. Also, half of the sample (50.99%) reports that their current economic circumstances restrict their ability to do things they consider important. Zooming on the objective measures of FV, Spanish households seem to manage their finances by avoiding household deficits (71.50%) and delays in debt payment (87.88%). However, around 8% of households do not have enough savings to cover their current expenses for a week if they were to stop receiving their primary source of income. Moreover, only 66.82% have a “financial cushion” for more than 3 months.

To provide a comprehensive and gradual measure of FV, we apply the Nonlinear Principal Components Analysis (NLPCA) to “summarize” these six items. This statistical method aims to reduce the dimensionality of data by delving into the relationships of the variables (J. F. Hair et al., 2006). NLPCA has proved to be a more appropriate method than traditional PCA when dealing with non-continuous variables (Anderloni et al., 2012; J. F. Hair et al., 2006). The Bartlett’s test of sphericity rejects the null hypothesis of no correlation among the variables (p < .000), while the Kaiser-Meyer-Ohlin (KMO) measure of sampling adequacy yields a value of .778, indicating that the data are suitable for factor analysis (Mishra et al., 2021).

The six items form three dimensions in the NLPCA, which account for 71.43% of the total variance (Table 4). In addition, the model demonstrates a high level of reliability, with Cronbach’s alpha value being close to 1 (α = .920). This value exceeds the threshold of 0.6 (J. F. Hair et al., 2006). Although Cronbach’s alpha for some components falls below this threshold, the results are similar to those obtained by Anderloni et al. (2012) and Singh and Malik (2022). Table 4 displays the factor loadings obtained using varimax rotation, which relate each original item to the different FV dimensions. In detail, component 1 primarily considers parameters related to consumption or saving capacity issues (i.e., perception of current financial situation, overspending and no emergency funds). Component 2 represents delays in bill and debt payment, while component 3 refers to an individual’s perception of being over-indebted.

Summary of NLPCA.

Note. The highest loadings for each factor are highlighted in bold.

The next step is to calculate the FV index as the sum of the values of each original variable, weighted by their respective factor loadings. The obtained values are then rescaled between 0 (minimum FV) and 1 point (maximum FV). As depicted in Figure 1, the index has a right-skewed distribution. Descriptive statistics indicate that Spanish households have a relatively low average level of FV (0.243) with a notable degree of dispersion (0.2105). Nevertheless, households with values above the median (0.1796) display noticeable symptoms of FV across the original variables. Specifically, nearly 77% of respondents perceive that they are limited by their current financial situation, more than half overspend, 56.42% have emergency funds lasting less than 3 months, and 23.17% experience delays in debt repayment.

FV index: Histogram.

The Key Independent Variables: Financial Literacy Measures

The key independent variables are referred to three dimensions of financial literacy. Firstly, an objective financial knowledge index is constructed based on the number of correct answers to the Big Three financial literacy questions on the concepts of inflation, compound interest, and portfolio diversification. This variable ranges from 0 (no knowledge) to 3 (the highest level of knowledge). Secondly, subjective or self-reported financial knowledge is measured through a single item question: “How would you qualify your general knowledge on financial matters compared with other adults in Spain?” Responses to this question are rated on a Likert scale ranging from (1) very poor to (5) very high.

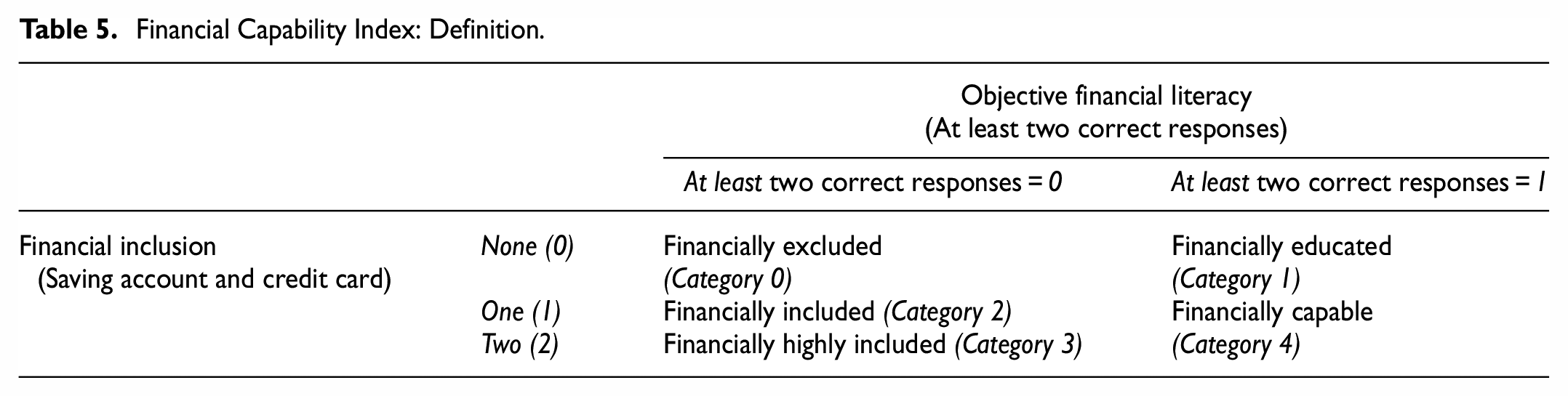

Thirdly, following Friedline and West (2016), a financial capability index is constructed by combining the individual’s level of objective financial knowledge and his/her banking inclusion (see Table 5). While the former variable captures the “ability to act,” the latter represents the respondents’“opportunity to act” (Sherraden, 2013). Hence, the objective financial knowledge variable is dichotomized to indicate whether (or not) the individual is financially literate (i.e., two or more correct responses to the Big Three questions). Then, this dummy variable is combined with several questions capturing the individual’s banking inclusion through holding either saving accounts and/or credit cards (Friedline & West, 2016). As a result, the financial capability index can take up to five values: 0 (“financially excluded”) and 1 (“financially educated”) for financially illiterate and financially literate individuals, respectively, who do not possess the two considered banking products; values 2 (“financially included”) and 3 (“highly financially included”) for financially illiterate individuals who have, respectively, one of the two products or both; and 4 (“financially capable”) for financially literate individuals who have at least one of the two banking products.

Financial Capability Index: Definition.

Table 6 presents the descriptive statistics for the key independent variables. Most of the Spanish population has a low or moderate level of objective financial knowledge. Notably, 13.59% of respondents are unable to answer any of the three financial literacy questions correctly. In contrast, 18.04% of the respondents answer all three questions correctly. The mean values of self-perceived financial knowledge indicate that 17.50% and 28.64% of respondents rate their knowledge on financial matters as very poor and poor, respectively. Comparing these results with those obtained for the objective financial knowledge variable suggests a potential perceptual bias. Thus, while 18.04% of respondents demonstrate a high level of objective financial knowledge, only 1% of them self-report a very high level of financial knowledge. Regarding financial capability, 51.40% of the respondents can be considered financially capable, indicating that they have at least one of the considered banking products and a medium level of objective financial knowledge. In contrast, 12.16% of the respondents can be classified as financially excluded. Furthermore, 11.71% of the sample lack both baking products despite having a medium level of objective financial knowledge.

Mean Values of Financial Literacy Variables.

Multivariate Analyses

Financial Literacy and Financial Vulnerability: OLS Analyses

To explore the relationship between various dimensions of financial literacy and FV, we use ordinary least squares (OLS) regressions, which are suitable for continuous dependent variables (Dismuke & Lindrooth, 2006) such as the FV index. Following Anderloni et al. (2012), we employ the inverse hyperbolic sine transformation to the dependent variable, as the FV index takes values that are practically equal to zero for certain observations. Thus, the basic specification of the models can be expressed as follows (Equation 1):

where i denotes the observation,

To assess the multicollinearity among the variables, we compute the Variance Inflation Factors (VIF). The highest VIF value (1.52) is considerably lower than 6, indicating the absence of multicollinearity (J. Hair et al., 1998).

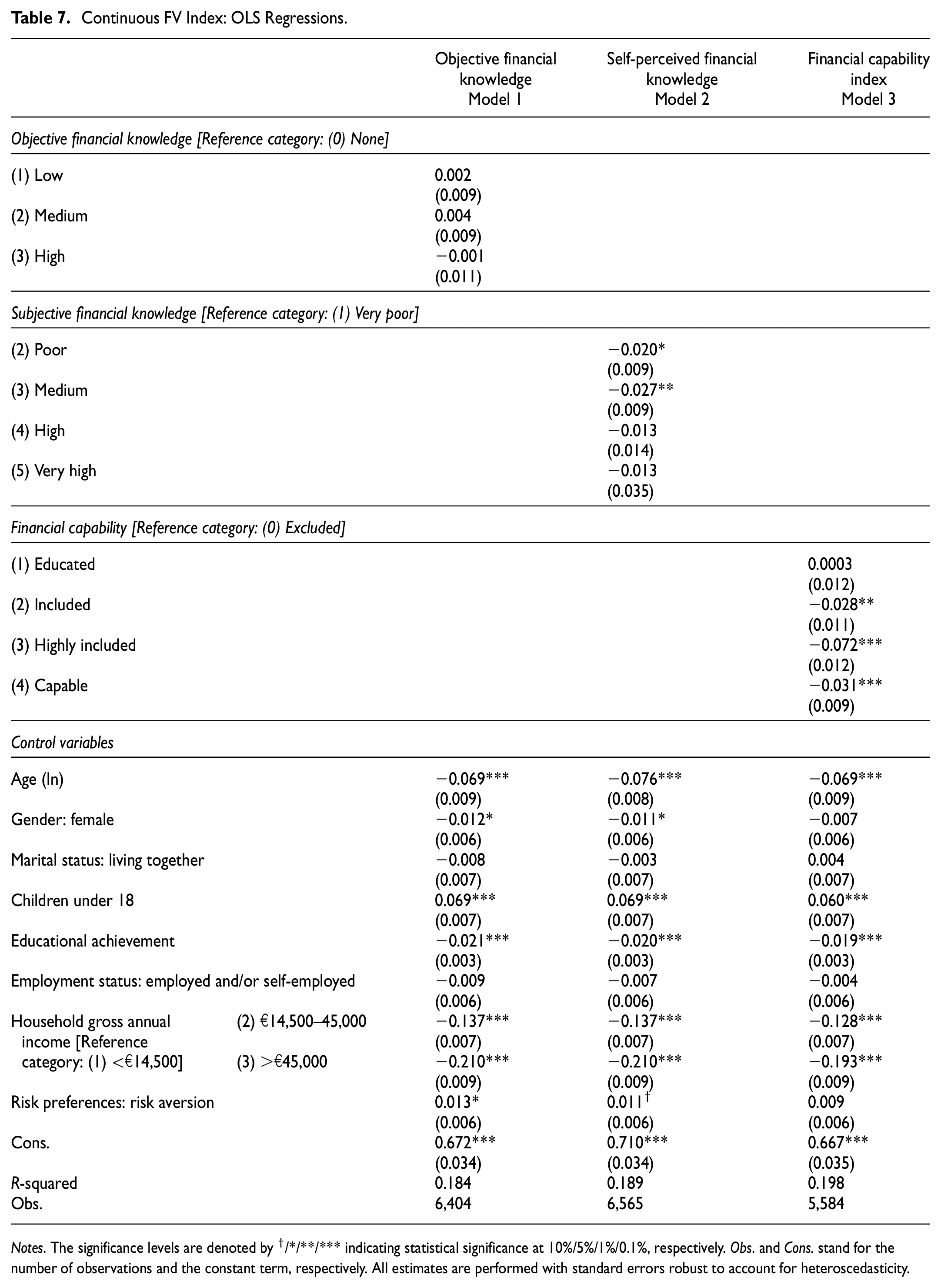

Several conclusions can be drawn from the estimates in Table 7. Firstly, a negative but non-statistically significant relationship is observed between high levels of objective financial knowledge and household FV. This finding is consistent with previous research (Abdullah Yusof et al., 2015; Loke, 2016, 2017; Philippas & Avdoulas, 2020; Wiersma et al., 2020), which also yielded inconclusive results when relying solely on objective financial knowledge to capture individuals’ financial literacy. It is worth noting that some studies have pointed out that commonly used financial literacy questions, such as the Big Three or Big Five, have a theoretical bias and fail to encompass the specific financial knowledge required for effective day-to-day household management (Loke, 2016). This could potentially explain the unreliability of objective financial knowledge as a driver of individuals’ savvy financial behavior (Mutsonziwa & Fanta, 2019).

Continuous FV Index: OLS Regressions.

Notes. The significance levels are denoted by †/*/**/*** indicating statistical significance at 10%/5%/1%/0.1%, respectively. Obs. and Cons. stand for the number of observations and the constant term, respectively. All estimates are performed with standard errors robust to account for heteroscedasticity.

Secondly, evidence points to a significant relationship between self-perceived financial knowledge and FV. Specifically, individuals who perceive their financial knowledge as poor or medium have lower levels of FV than those who self-report very poor levels of financial knowledge. These findings are similar to those of Allgood and Walstad (2016). Moreover, these results suggest that the underlying mechanisms through which financial knowledge attenuates FV may differ between objective and self-perceived financial knowledge (Allgood & Walstad, 2016; Ghadwan et al., 2023).

Thirdly, financial capability does also matter. When employing a more comprehensive definition of financial literacy that encompasses both the “ability to act” (i.e., objective financial knowledge) and the “opportunity to act” (i.e., banking inclusion), it is observed that “financially capable” individuals show lower FV than “financially excluded” individuals. These results are in line with those of Friedline and West (2016), although direct comparison is not feasible as the authors measure FV using a single dichotomous item (i.e., the holding of emergency funds). Additionally, the estimated coefficient for “financially capable” individuals is half that of “highly financially included” and illiterate individuals, suggesting that that the “opportunity to act” is a more important driver of FV than the “ability to act.”

Finally, the control variables help in building up the demographic and socio-economic profile of individuals/households most prone to experiencing FV. The evidence for these variables is consistent with prior research. Thus, older individuals tend to have lower values of FV (Disney & Gathergood, 2011; Loke, 2017; Seldal & Nyhus, 2022), as do those with higher levels of education (Anderloni et al., 2012; West & Mottola, 2016), and women (Abdullah Yusof et al., 2015; Singh & Malik, 2022). Households with dependent children tend to be more financially vulnerable compared to those without dependents (Anderloni et al., 2012; Friedline & West, 2016). The findings also indicate that higher income levels are negatively associated with FV (Daud et al., 2019; Friedline & West, 2016; Seldal & Nyhus, 2022). Additionally, more conservative attitudes toward financial risk-taking are positively related to FV, although the statistical significance of this relationship is weak.

Robustness Analyses

Additional analyses were conducted to check the robustness of our findings. To do so, we transformed the FV index from a continuous variable into three categorical variables by grouping the percentile scores of the FV index into tertiles (Arellano & Cámara, 2021; Loke, 2017), quartiles (McCarthy, 2011; Valdes et al., 2021), and quintiles (Abdullah Yusof et al., 2015; Daud et al., 2019). Then, we re-run the models detailed in Table 7 using ordered probit regressions. This allowed us to check whether the results were robust to different definitions of the dependent variable and to alternative estimation methods.

Figure 2 illustrates the distribution of the categorical FV measures. the statistics indicate that a small percentage (2%–4%) of Spanish households can be classified as highly financially fragile. In contrast, a notable percentage of households (22%–40%) can be classified as moderately (low and intermediate) financially vulnerable, consistent with the gradual approach outlined by O’Connor et al. (2019).

Categorical FV measures: Histograms and cumulative frequencies. (a) FV index: tertiles, (b) FV index: quartiles, and (c) FV index: quintiles.

As previously mentioned, we re-run the estimates detailed in Table 7 using ordered probit regressions. Unlike classical linear regression, ordered probit models do not assume equal intervals between levels of the dependent variable (Liddell & Kruschke, 2018), nor that two individuals with the same value of FV index have the same level of FV (Daykin & Moffatt, 2002). Then, ordered probit approach performs better than OLS, as the latter assumes linear probability relationships that could generate problems of heteroskedasticity for ordinal variables (Dismuke & Lindrooth, 2006).

The results remain largely unchanged: objective financial knowledge still show a non-statistically significant relationship with FV, while subjective financial knowledge reveals a negative association for individuals with low and medium levels of self-perceived financial knowledge. Additionally, Figure 3 displays the estimated probabilities of being categorized into each FV level based on the financial capability index. It allows us to read the results in terms of marginal effects.

Average adjusted predictions of categorical FV measures by financial capability index. (a) FV index: tertiles, (b) FV index: quartiles, and (c) FV index: quintiles.

Thus, Figure 3a shows that the probability of being highly financially fragile is approximately three times higher when respondents who are “financially excluded” compared to those who are “highly financially included” (6%vs. 2%). As financial capability increases, this estimated probability decreases by up to 4% points. In contrast, 73% of “financially capable” individuals have a low level of FV compared to 68% of those who are “financially excluded.” It should be noted that the greatest differences in relation to “financially excluded” individuals are consistently observed among those who are “highly financially included.” These findings indicate that the reduction in FV is higher among individuals who are “highly financially included” than among those who are “financially educated.” In other words, the “opportunity to act” seems to hold greater importance than the “ability to act” in reducing the level of FV. Therefore, “learning by doing” emerges as the most effective way for promoting financial literacy among the Spanish population.

Discussion

The COVID-19 pandemic has further intensified the economic and financial difficulties faced by households, who were still grappling with the aftermath of the 2007-08 financial crisis. An increasing number of households are struggling to pay debts or meet unexpected expenses, leading to an alarming increase in financial vulnerability (FV), which has become a pressing concern for public authorities and the financial sector. In response, one proposed solution has focused on promoting financial literacy. Therefore, this paper investigates the relationship between financial literacy and FV, aiming to address the limitations in previous literature regarding the measurement of both variables.

Overall, empirical evidence has showed a negative relationship between FV and financial literacy, thus supporting the hypothesis of this paper. Nevertheless, it is essential to recognize that not all dimensions of financial literacy play an equal role in mitigating FV. Specifically, while objective financial knowledge does not have a statistically significant relationship with FV, self-perceived financial knowledge shows a negative association, indicating that higher levels of self-perceived financial knowledge can reduce the risk of FV.

Furthermore, financial capability also holds a leading role in decreasing household FV. Generally, “financially capable” individuals tend to experience lower levels of FV. Moreover, our findings suggest that the “opportunity to act” (or banking inclusion) is a more relevant factor in improving households’ financial resilience than the “ability to act” (or objective financial knowledge).

Theoretical Implications

Household FV is a multidimensional phenomenon, and currently, there is no universally accepted definition for it (Fernández-López, Álvarez-Espiño, Rey-Ares, & Castro-González, 2023; Seldal & Nyhus, 2022; Singh & Malik, 2022). As a result, there is a lack of consistent measures for FV. In this context, researchers have developed FV measures based on available information. However, almost of the FV measures in the literature suffer from a major drawback -they focus on a single aspect of the phenomenon (such as debt or savings/consumption) and may be either objective or subjective in nature. Moreover, dummy measures are frequently used, which hampers the analysis of household FV as a gradual process. Therefore, future research should employ comprehensive and gradual FV index, which is essential to capture the nuanced nature of this multifaceted phenomenon.

Similarly, financial literacy entails different dimensions, and their roles in mitigating FV are not equal. These results support the notion that the commonly used Big Three or Big Five financial literacy questions may be insufficient in measuring financial literacy comprehensively. Additionally, the findings highlight the difference in how objective and self-perceived financial knowledge contribute to reducing the risk of FV. The evidence also emphasizes the importance of considering the dimension of financial inclusion. Further research on FV could benefit from separately incorporating measures of both objective and self-perceived financial knowledge, as well as financial capability.

Practical Implications

As mentioned, not all dimensions of financial literacy play an equal role in mitigating FV. With self-perceived financial knowledge proving to be more important than objective financial knowledge, governments and financial institutions should actively encourage individuals to evaluate their own financial knowledge and skills. This recommendation aims to enhance individuals’ awareness of their actual level of financial knowledge and boost their self-confidence. Technology, such as mobile apps, can be valuable in this regard by providing self-assessment tools, interactive exercises, and quizzes.

Also, policymakers and financial institutions should prioritize efforts to improve access to financial services, especially for underserved populations. This entails promoting financial inclusion initiatives and reducing barriers to entry, such as simplifying account opening procedures.

Moreover, when formulating and implementing financial education initiatives, governments should take previous findings into consideration. This will contribute to the development of more action-oriented programs. Instead of solely focusing on objective financial knowledge, financial education programs should emphasize practical skills, decision-making, and the utilization of available financial opportunities. These programs should focus on creating budgets, tracking expenses, saving strategies, and debt management. Moreover, they should provide individuals with practical tips and tools that can be readily applied in their daily lives.

Contributions and Limitations

The first contribution of this paper involves the development of a comprehensive FV index that encompasses both objective and self-perceived financial features of households. Thus, FV is conceptualized as a multidimensional and gradual phenomenon. The second contribution is the consideration of three dimensions of financial literacy, namely objective and self-perceived financial knowledge, as well as financial capability. To date, only Friedline and West (2016) have explored the relationship between financial capability and FV; however, their FV measure was limited to a single item assessing the ability to handle unforeseen expenses. The third contribution centers around studying a South-European country characterized by relatively low financial literacy levels (Arrondel et al., 2021) and moderately high levels of FV (Arellano & Cámara, 2021), making it an interesting case for the analysis.

The paper also has limitations that can guide the development of future research lines. Firstly, the cross-sectional nature of the sample presents a challenge in studying potential causal relationships. This limitation could be addressed when more waves of the ECF are completed. Secondly, the obtained evidence is restricted to Spain. As noted by Anderloni et al. (2012), future research would benefit from design of harmonized FV measures across countries. Moreover, the absence of quantitative data represents an important limitation of the FV index. Thus, the survey prevents the consideration of aspects such as the financial burden loans impose on household income, which would further contribute to a better understanding of household FV.

Footnotes

Acknowledgements

Not applicable.

Author Contributions

All authors make the same contribution to the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Marcos Álvarez-Espiño acknowledges financial support from the Spanish Ministry of Universities through the FPU grant (Ayudas para la Formación del Profesorado Universitario) [FPU grant: FPU21/03287]. The authors acknowledge the support of the Consellería de Cultura, Educación e Universidade through the “Axudas para a consolidación e estruturación de unidades de investigación competitivas”.

Ethics Statement

Not applicable.