Abstract

This paper investigates the mechanisms of tax incentives and R&D investments on employment absorption, constructs a panel data model with a sample of 4,255 Chinese technology-based SMEs, and adopts a random effect model for empirical evidence after various tests. The research results show that tax incentives and R&D investments of technology-based SMEs positively affect their employment absorption. The positive effect not only exists in the current period but also remains valid in the next period. R&D investment, operating profit margin, and remuneration have more significant positive impacts on employment absorption, while we should pay attention to control and reduce overhead costs. Finally, this paper gives corresponding suggestions and countermeasures from three levels: government, enterprises, and society.

Introduction

The Chinese 20th Party Congress report proposes to “strengthen the employment priority policy, improve the employment promotion mechanism, promote high-quality and full employment.” At the same time, it pointed out that “strengthening the status of enterprises as the main body of scientific and technological innovation, and creating a favorable environment conducive to the growth of technology-based small and medium-sized enterprises.”

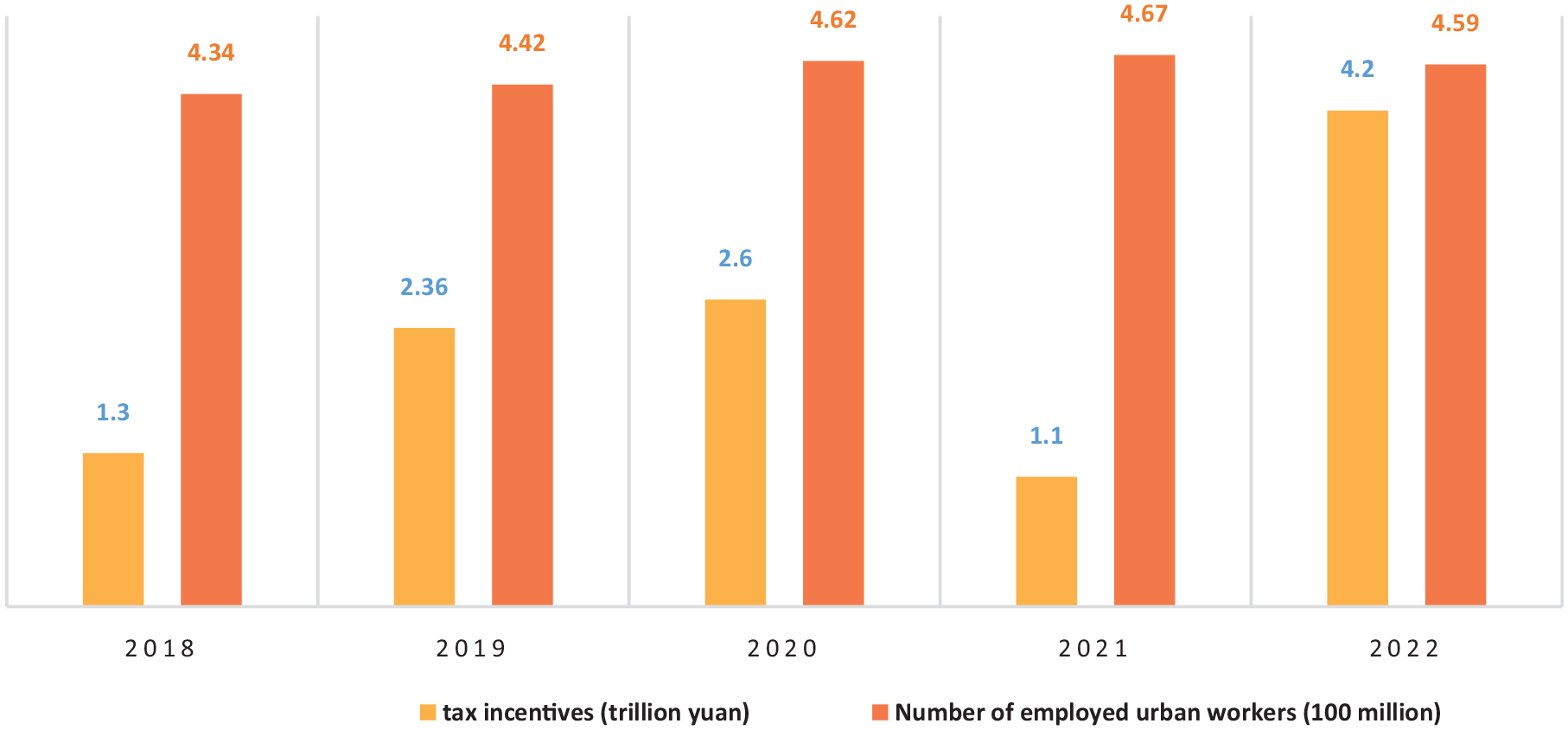

Taxation plays a vital role in employment absorption. In recent years, with the gradual deepening of China’s tax and fee reduction policies, labor and employment have also undergone corresponding changes. In 2018, the amount of China’s tax and fee cuts totaled 1.3 trillion yuan, and by 2022, the amount has reached 4.2 trillion yuan. In the same period, China’s urban employment numbers have also been changing. In 2022, 459 million people were employed in urban areas, compared with 438 million in 2018. Figure 1 shows the changes in tax and fee reductions, compared with urban employment in China during 2018 to 2022. As shown in Figure 1, from 2018 to 2022, China’s tax and fee reduction showed an upward trend. In the same period, China’s urban employment has also risen.

Tax incentives and employment absorption in China (2018–2022).

Among the vast number of small and medium-sized enterprises (SMEs), technology-based SMEs have strong potential for innovation and growth. In the process of development and growth, many small giant enterprises, invisible champion enterprises, and technology leaders have emerged and played essential roles in employment absorption. With the implementation of tax incentive policies, they are supporting policies including fully utilizing value-added tax exemptions, income tax incentives, and a 50% reduction of “six taxes and two fees,” covering various enterprises such as small and profitable enterprises, individual entrepreneurs, small and micro business entities, as well as covering the whole industrial chain of production, R&D, and innovation. Those policies have actively helped technology-based SMEs to stabilize and expand employment and played positive roles in achieving social stability and promoting high-quality economic development. According to statistics, in 2022 alone, tax policies to promote employment have benefited more than 80 million business entities, and more than 99% of SMEs and individual business owners have benefited from these policies.

The purpose of our study is to examine the impact of tax incentives on employment absorption using the microdata of technology-based SMEs. Our study is also motivated by the fact that previous literature primarily focuses on the economic consequences, and few studies examine the mechanism. By checking the mechanism and impact, we offer some findings: (1) tax incentives and R&D investments of technology-based SMEs have positive effects on their employment absorption; (2) the positive effect is not only reflected in the current period but also remains valid in the next period; (3) R&D investment, operating profit margin, and remuneration have more significant positive impacts on employment absorption, while we should pay attention to control and reduce overhead costs.

We make some economic policy contributions. This study not only provides more reliable evidence for solving academic differences in China but also explores the internal impact mechanism of tax incentives on employment absorption. Moreover, it also offers scientific suggestions for the improvement of China’s tax policy in order to manage unemployment issues more effectively.

This paper proceeds as follows. Section “Literature Review” introduces literature reviews. Section “Theoretical Analysis and Hypothesis” contains a theoretical analysis and hypothesis. Section “Research Design” explains the research design, including sample selection and data sources, the model setting, and variable definitions. Section “Empirical Analysis” contains the empirical analysis, including base regression analysis, endogeneity test, robustness test, and additional analysis. Section “Conclusions” concludes.

Literature Review

There has been much literature related to this topic, mainly focusing on each other’s relationships between tax incentives, innovation, and employment. Currently, the primary studies are:

(1) Studies on tax incentives and employment absorption. Scholars generally agree that tax incentives have a positive impact on employment absorption (R. Chen, 2023; Domguia et al., 2022; Hutton & Ruocco, 1999; Ma & Wang, 2020; Xiong & Liu, 2022). However, some scholars have drawn different research conclusions that tax incentives have no positive effect on employment absorption (Y. W. Chen & Xu, 2011). Some scholars believe that tax incentives have a positive effect on employment absorption for low-income employees, while they have little effect on the high-income employees ranked in the top 10% (Owen, 2019). In terms of how to bring into play tax incentives to enhance employment, most scholars believe that they should focus on SMEs, export-oriented economies, labor-intensive industries, industrial transformation, education and training of enterprise employees (Liu, 2003; Liu et al., 2022; Ma & Wang, 2020; S. Qu, 2005; C. Wang, 2007).

(2) Studies on tax incentives and R&D investment. Scholars generally agree that tax incentives have positive impacts on R&D investment (Bai et al., 2019; Feng et al., 2015; Kou et al., 2022; Shi et al., 2017; S. Wang & Hao, 2014; C. Zhang et al., 2021). The impact magnitude of different tax incentives on R&D investment varies, and some scholars found that by influence order, it is R&D expense accrual deduction > tax rate preference > accelerated depreciation of fixed assets (Han & Ma, 2019). Some scholars found that by influence order, it is R&D expense plus deduction > R&D expense plus deduction with tax rate preference > tax rate preference (Cheng & Yan, 2018). Some scholars found that the influence order is add-on deduction > accelerated depreciation and amortization > tax rate preference (X. Qu et al., 2022). Different types of enterprises can make tax incentives work differently for R&D investment, with some scholars arguing that tax incentives are more effective for high-productivity enterprises than for low-productivity enterprises by productivity (Almenar-Llongo et al., 2023). Some scholars argue that tax incentives are more effective for non-state-owned enterprises than for state-owned enterprises when differentiated by whether they are state-owned enterprises or not (C. Zhang et al., 2021). However, some scholars believe that tax credit refunds have a stronger positive effect on state-owned enterprises (Hou, 2023).

(3) Studies on R&D investment and employment. Most scholars believe that R&D investment can promote employment growth (Boeing et al., 2022; Fingleton et al., 2004; Meng, 2015; C.-G. Zhang & Guan, 2019; Zhao & Liu, 2009). Some scholars have studied R&D investment and employment in different types of enterprises, and the results show that R&D investment in services and high-tech manufacturing industries creates jobs. However, traditional industries have no such employment absorption effect (Bogliacino et al., 2012). It has also been argued that the employment effect of R&D investment is not significant because labor input may decrease with process innovation (Goel & Nelson, 2022), while an increase in R&D investment significantly increases labor force exits from employment in the group aged 41 to 59 (B. Zhang, 2022).

In general, the existing research mainly carried out from theoretical and empirical levels. At the theoretical level, the general concept is that tax incentives have both a promotion effect and a suppression effect on employment (Rosenzweig, 2014). On the one hand, the promotion effect suggests that tax incentives can improve enterprise profits, promote R&D investment, and scale growth to increase employment absorption (Garrett et al., 2020; Michaelis & Birk, 2006). On the other hand, according to the suppression effect, because capital can replace labor to a certain extent, tax incentives would drop the relative prices of capital and labor, thus increasing the capital demand, equipment investment, and R&D investment, and ultimately reducing the employment absorption (Z. Chen et al., 2021; Mughan & Propheter, 2017; Zwick & Mahon, 2017). In addition, the relative impacts of the promotion effect and suppression effect are often affected by many factors (Clausing, 2016). For example, there are differences in the final effect that tax incentives have on the employment of different ownership types of enterprises (Y. Wang et al., 2012). Tax law enforcement and enterprise asset structure also impact the employment absorption effect of tax incentives (Liu et al., 2022).

At the empirical level, current researchers have yet to reach a uniform conclusion on whether tax incentives can increase employment absorption. The key results of the empirical research are as follows: Most studies suggest that there is a positive correlation between tax incentives and employment absorption (Harden et al., 2003; Kakpo, 2018; Lars & Kirchgässner, 2003; Liu et al., 2022), while a small number of studies have found the opposite result (Corden & Garnaut, 2018; Lora & González, 2016). Other studies suggest that the effect of tax incentives on employment absorption needs to be clarified, which means no significant impact (Bettendorf et al., 2009; Jentsch & Lunsford, 2019; Mertens & Ravn, 2013).

The existing studies have provided a good foundation for this paper to study tax incentives, R&D, and employment absorption. However, there remain some topics to solve. For example, what kind of mechanism do tax incentives and R&D investment play in promoting the employment absorption of technology-based SMEs? Currently, with the employment pressure existing, how can we use the positive effects of various policies, including taxation, to promote R&D and enhance employment in technology-based SMEs? Besides, existing studies often need more research that puts tax incentives, R&D investment, and employment absorption into a unified framework. Regarding empirical research, the existing research data is primarily macro statistical data, and few pieces of research involve microdata. To address these limitations, we use a total sample of 4,255 Chinese technology-based SMEs from the Chinese Administration of Taxation, which is more sensitive than previous research data. By doing so, we can determine whether the tax incentives impact employment absorption and investigate the internal mechanism of how tax incentives, R&D investment, and employment absorption can work more accurately.

Theoretical Analysis and Hypothesis

In this paper, we build a framework to put tax incentives as a wedge in the R&D activities of technology-based SMEs, and Figure 2 shows the mechanism.

Mechanism of the role of tax incentives, R&D investment, and employment absorption.

Most of the literature divides the results of R&D investment into production innovation and process innovation. In terms of the impact of production innovation on employment absorption, firstly, production innovation can improve the quality of new products based on original products or enrich functional characteristics, further stimulate consumer demand, increase product sales, promote enterprises to expand production scale, and bring about an increase in labor demand and employment. Secondly, production innovation will bring derivative demand for intermediate products, promote the development of new production lines and new businesses of enterprises, promote the expansion of the overall production plan of enterprises, and bring about an increase in labor demand. Of course, when enterprises expand the consumer market of new products and expand the production scale of new products, they will cause a substitution effect on the original products, and the reduction or even suspension of the original production scale will correspondingly reduce the demand for labor and bring about employment destruction.

In terms of the impact of process innovation on employment absorption, firstly, from the perspective of price effect, process innovation improves the production efficiency of enterprises, decreases the per-production cost, and increases the profit margin of enterprises. Under the influence of enterprises’ price reduction strategy and market mechanism, the decline of product prices will stimulate the rise of consumer demand, and the expansion of the demand scale will promote the expansion of the enterprise production scale, bring about new labor demand, and thus form the employment absorption effect. Secondly, while improving enterprise productivity, process innovation contributes to the improvement of profit margins, the expansion of reinvestment scale, and the increase of labor demand. Of course, the improvement of labor production efficiency of enterprises may reduce the input of labor factors per unit of product or service and bring about a reduction in labor demand.

When enterprises carry out R&D activities, the tax incentives will help them reduce costs in terms of labor, capital, resource consumption, and the transformation of technological achievements. Firstly, in terms of labor cost, tax incentives such as increasing the proportion of pre-tax deductions for employee education expenses of high-tech enterprises will help reduce the labor cost of R&D investment. Secondly, in terms of capital cost, tax incentives such as granting high-tech enterprises foreign investment within a specific limit to offset the taxable income of venture capital enterprises will help reduce the capital cost of R&D investment. Thirdly, in terms of resource consumption, tax incentives such as adding depreciation and amortization to R&D expenses, in terms of resource consumption through the formation of fixed assets and intangible assets for additional depreciation, amortization, and other tax benefits will help reduce the consumption of resources for R&D investment. Fourthly, in terms of the transformation of technological achievements, through the income of related technical consulting services and technology transfer income exemption from value-added tax, enterprise income tax, or a 50% reduction in enterprise income tax and other tax incentives, it will help reduce the cost of transformation of technological achievements.

Although production innovation leads to the substitution effect of the original products, due to the improvement of the quality or functional characteristics, it can further stimulate the consumer demand on the basis of the consumer market size of the original products, thus bringing about the expansion of the production scale of the products. In addition, the production of new products has the potential to open up new markets for intermediate goods, so the overall effect of production innovation is job creation. As mentioned above, most scholars believe that R&D investment can promote employment absorption. At the enterprise level, the enhancement of R&D innovation will lead to reinvestment and reproduction, and enterprises will have more labor demand, thus promoting employment absorption. At the industry level, the technological spillover effect, industry multiplier effect, and wealth effect of R&D innovation will lead to the expansion of production and promote employment absorption. In addition, although the increase in production efficiency will reduce employment, it will have a different impact on all enterprises. Comparatively, the lower the enterprise productivity, the more they will be affected. Combined with the production and process innovation effects, this paper holds that the combined impact on employment is the job creation effect.

Based on the above analysis, this paper puts forward the following research hypotheses.

H1: Enterprise R&D investment contributes positively to employment absorption.

H2: Tax incentives affect employment absorption by influencing enterprises’ R&D investment.

Research Design

Sample Selection and Data Sources

The technology-based SMEs referred to in this paper are consistent with the “Evaluation Measures for Science and Technology-based SMEs,” which is issued by the Chinese Ministry of Science and Technology, and refer to SMEs that rely on technology personnel to engage in science and technology research and development activities, acquire independent intellectual property rights and transform them into high-tech products or services, thus achieving sustainable development. The research sample of this paper comes from the Chinese Administration of Taxation, and the period is 2018 to 2022, with a total sample of 4,255 enterprises, and all data are desensitized, without involving sensitive information such as enterprise names.

Overall, among the 4,255 technology-based SMEs, the number of enterprises distributed in the first, second, and third industries are 11, 2,143, and 2,101, respectively, which roughly coincides with the ratio of three industries in 2022.

According to the type of industry, 407 technology-based SMEs are distributed in the software and information technology service industry, and 386 and 363 technology-based SMEs are distributed in the wholesale industry and the general equipment manufacturing industry. Only one technology-based SME is distributed in the health industry. The industry distribution is consistent with China’s high-quality development.

The data covers the COVID-19 epidemic, and therefore, the epidemic’s impact on technology-based SMEs can also be described. In the 3 years affected by the epidemic, 53 industries had negative gross profit growth, and only 11 industries had positive gross profit, while most of them were related to the epidemic and consumption, especially the pharmaceutical industry. Forty-two industries have enjoyed the tax incentives, of which the most significant reduction in tax burden are instrumentation manufacturing, special equipment manufacturing, and other manufacturing industries.

Data integrity determines the result’s reliability. In this paper, we take four steps to process data. Firstly, data matching is performed, and essential data items are checked and matched individually. Secondly, data standardization is taken, the Z-score method is used to standardize the data, and the newly generated variable names start with Z_ to show the difference with the original variables. Thirdly, data cleaning is performed, and essential data items are compared carefully. For those missing or unreasonable data items, they are deleted directly. Fourthly, to eliminate extreme values and outliers, this paper makes a 1% and 99% winsorize shrinkage of all continuous variables. Stata 16.0 is used to calculate the data.

Model Setting and Variable Definitions

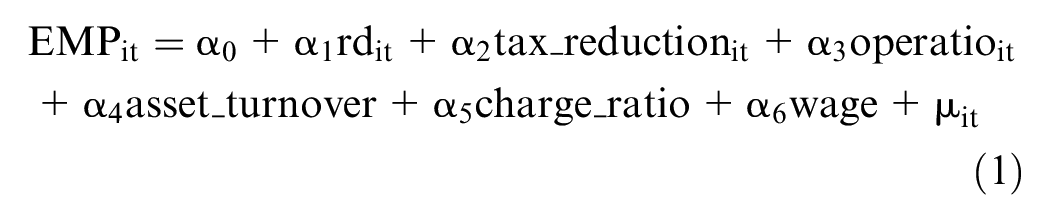

Referring to Li et al. (2021), based on the research hypothesis above, the following model is developed:

Here, the subscript i represents the i-th firm, and the subscript t represents the year t; employment absorption (EMP) is the explanatory variable, R&D investment (rd) and tax incentives (tax_reduction) are the explanatory variables; the remaining variables are the control variables, and μit is a random disturbance term.

Referring to Zuo et al. (2023), we define the explained variable, explanatory variables, and control variables as follows.

1. Explained variable: employment absorption. Employed absorption refers to employees aged 16 or above who engage in specific social labor and obtain certain labor remuneration or business income, and the number of employees at the end of the current year is chosen to measure employment absorption and taken as a logarithm.

2. Explanatory variables:

(1) R&D investment. R&D investment refers to the depreciation of the assets used in the process of research and development, the raw materials consumed, the salaries and welfare expenses of the personnel directly involved in the development, the rent and borrowing costs incurred during the development process, and take the ratio of R&D expenditure to primary business income is selected to measure R&D investment.

(2) Tax incentives. Tax incentives refer to measurements that the state adopts tax policy to provide for a particular part of specific enterprises and tax objects in tax laws and administrative regulations to reduce or exempt tax burden, including value-added tax, enterprise income tax, consumption tax, and land use tax, which are reduced by policy, are expressed as the ratio of total annual tax reduction to total profit.

3. Control variables. Based on previous studies, operating profit margin, total asset turnover ratio, overhead rate, and remuneration are selected as control variables.

(1) Operating profit margin. Operating profit margin refers to operating profit from operations as a percentage of net sales and takes the ratio of annual operating profit to operating income to express it.

(2) Total assets turnover ratio. The total assets turnover ratio is an indicator that measures the ratio between the scale of asset investment and the level of sales, and it is expressed as annual sales revenue and its annual average total assets.

(3) Overhead rate. Overhead rate is an essential factor that affects the profitability of enterprises and reflects the level of enterprise management. It is expressed as the ratio of annual administrative expenses to operating income.

(4) Remuneration. Remuneration is the various forms of compensation that employees receive for providing services to their organizations, and it is expressed as the average salary at the end of the year.

Table 1 illustrates the variable definitions.

Variable Definitions.

Empirical Analysis

Descriptive Statistics

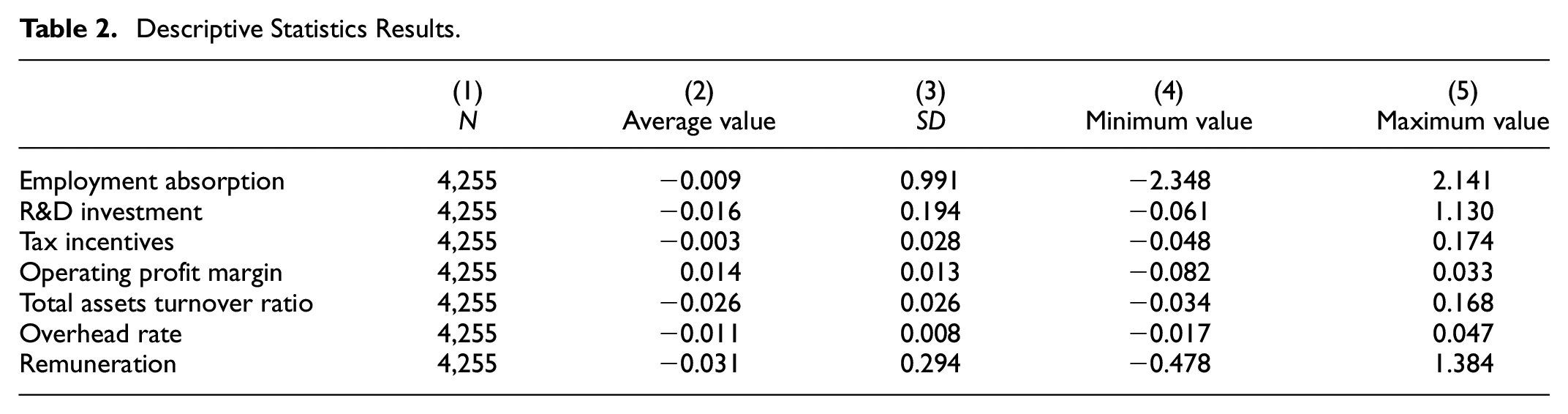

Table 2 represents the descriptive statistics results.

Descriptive Statistics Results.

As seen in Table 2, after standardization, the mean value of employment absorption in technology-based SMEs is −0.009, the maximum value is 2.141, the minimum value is −2.348, and the standard deviation is significant, indicating a large dispersion in employment. The mean value of R&D investment is −0.016, the maximum value is 1.130, and the minimum value is −0.061. The difference between the maximum and minimum values is significant. However, the standard deviation is 0.194, which is not a high degree of dispersion, indicating that the R&D investment interval is relatively concentrated. The minimum value of tax incentive is −0.048, which may be that some enterprises need to pay back taxes. In addition, the standard deviations of operating profit and management expense ratio are minor, indicating that the values of these two indicators are more concentrated in the sample enterprises.

Individual Effect Test

The original hypothesis is to use an OLS mixed effects model. Table 3 reports the individual effect results.

Individual Effect Results.

p < .01. **p < .05. *p < .1.

As seen in Table 3, the p-value is 0, which indicates that the fixed effects are better than the mixed effects model.

Time Effect Test

The LM test is adopted to test between mixed and random effects. Table 4 reports the time effect results.

Time Effect Results.

p < .01. **p < .05. *p < .1.

As seen in Table 4, the p-value is 0, indicating that the random effects are better than the mixed effects model.

Hausman Test

The Hausman test compares fixed effects (FE) and random effects (RE). Table 5 reports the Hausman test results.

Hausman Test Results.

Note. Standard errors in parentheses.

p < .01. **p < .05. *p < .1.

As seen in Table 5, the p-value is .463, which is greater than .05, indicating that the random effect is better than the fixed effect, and the random effect should be selected.

Baseline Regression

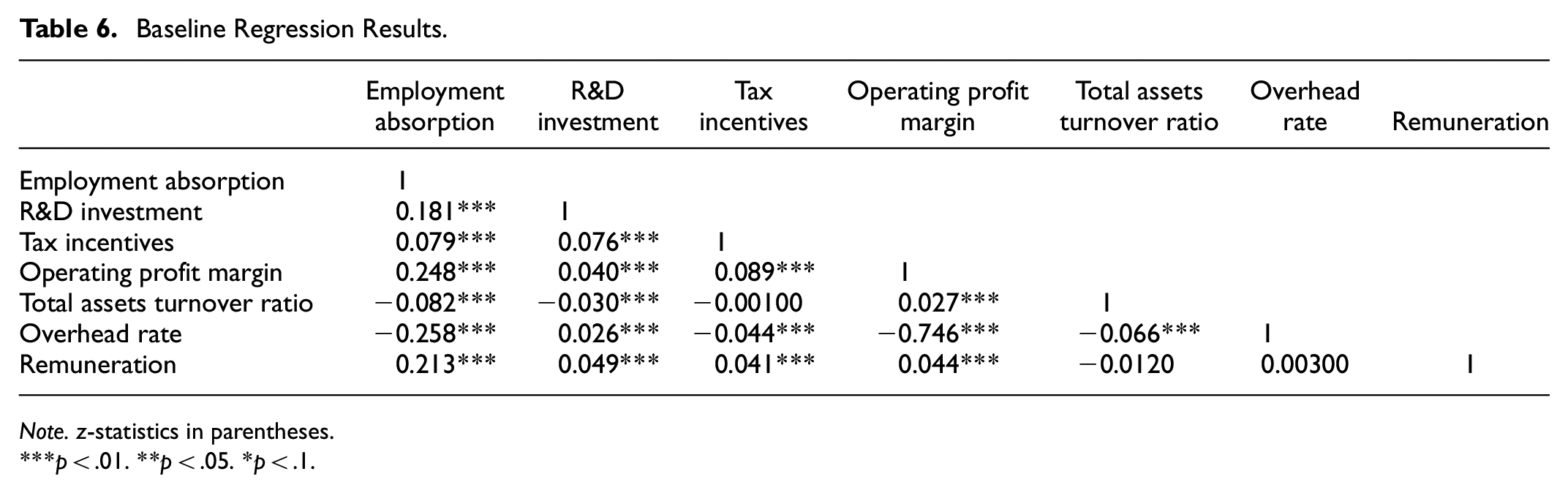

Table 6 reports the baseline regression results.

Baseline Regression Results.

Note. z-statistics in parentheses.

p < .01. **p < .05. *p < .1.

As seen in Table 6, the employment absorption of technology-based SMEs is significantly related to R&D investment, tax incentives, operating profit margin, total asset turnover, overhead rate, and compensation at 0.01.

The model can be formulated as follows.

The model implies that with every one percentage increase in R&D investment, the employment absorption of technology-based SMEs will increase by 0.181%. In contrast, for every one percentage increase in tax incentives, the employment absorption of technology-based SMEs will increase by 0.079%, with other factors held constant. Similarly, with other factors unchanged, each one percent increase in operating profit margin and salary will impact 0.248% and 0.213%, respectively, on the employment absorption capacity of technology-based SMEs. Total asset turnover ratio and overhead rate hurt employment absorption capacity, that is, each percentage point increase in both will reduce the employment absorption capacity of technology-based SMEs by 0.082 and 0.258 percentage points, respectively, with all other factors remaining unchanged.

Endogeneity Test

The endogeneity of this paper mainly comes from two aspects. On one hand, there exist causal relationships between each other. Technology-based SMEs with R&D investment will send positive signals to the outside world, making it easier for them to obtain tax incentives. On the other hand, although we control those essential characteristics of technology-based SMEs in the regression model, some variables may need to be added to affect employment absorption. The above situations may lead to endogeneity issues, resulting in biased estimation results. So, this paper adopts a two-stage least squares method to solve endogeneity.

Referring to Yao et al. (2022), this paper uses tax incentives with a lag of one period as instrumental variables (IV) to control endogeneity. Table 7 reports the results.

Instrumental Variables (2SLS) Regression.

p < .01. **p < .05. *p < .1.

As can be seen from Table 7, the Durbin test and Wu-Hausman test show that all explanatory variables are exogenous. Besides, the p-value of the Sargan statistic fails to pass the significance test at the 10% level, indicating there exists no overidentification problem.

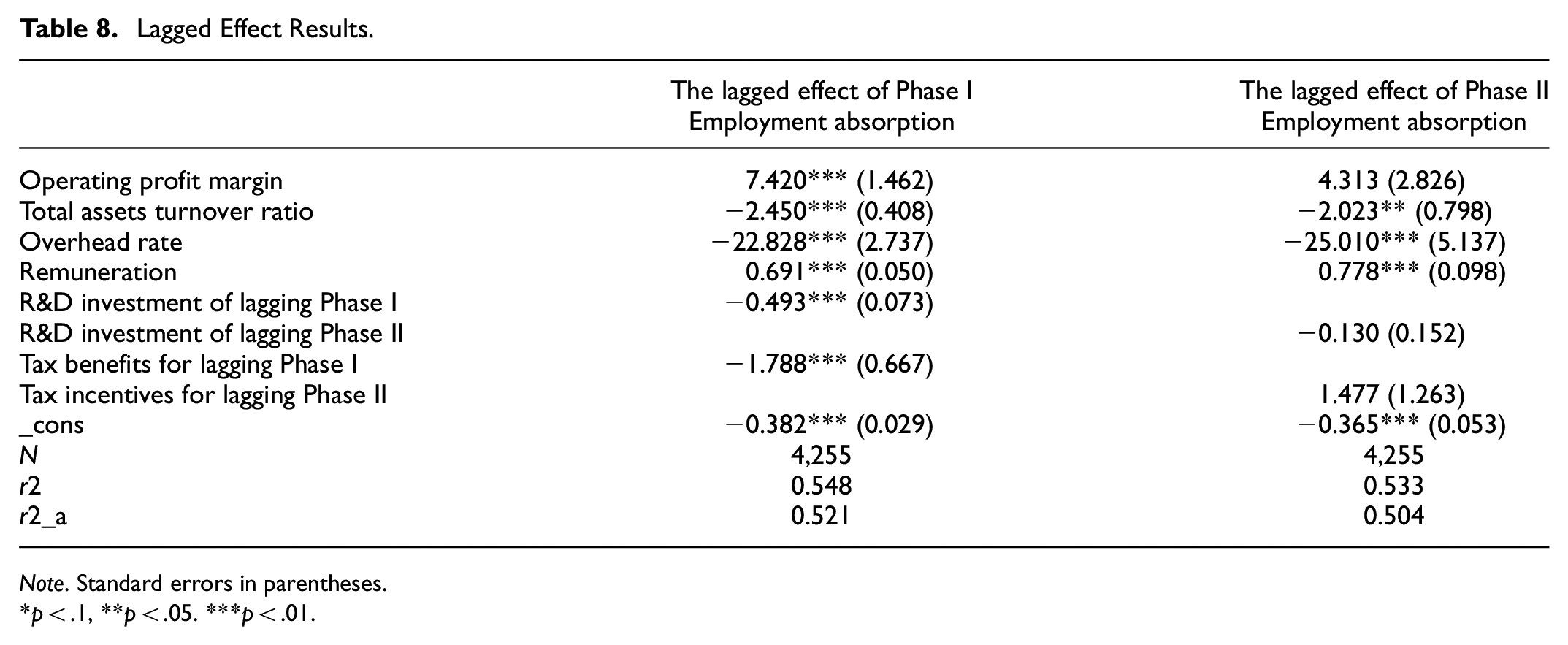

Lagged Effects Test

Tax incentives and R&D investment have created positive incentives for employment in technology-based SMEs in the current period, but will they continue to work in the subsequent period? Regarding the lag and continuity of policy implementation, tax incentives and R&D investment will likely remain effective on the employment absorption of technology-based SMEs in the following period. To this end, this paper tests the employment absorption effects of tax incentives and R&D investment on technology-based SMEs with one and two lagged phases. Table 8 reports the results.

Lagged Effect Results.

Note. Standard errors in parentheses.

p < .1, **p < .05. ***p < .01.

The first lagged phase results report that tax incentives and R&D investment are still significant for the employment absorption in technology-based SMEs at the 0.01 level. The second lagged phase shows they no longer have significant incentive effects on employment absorption. The results indicate that the effects of tax incentives and R&D investment on employment absorption of technology-based SMEs are significant in the current period and the next period, but the effects are no longer significant in the following two periods.

Robustness Analysis

This paper transforms the variables and makes another regression. Table 9 reports the results.

Robustness Test Results.

Note. t-Statistics in parentheses.

p < .01. **p < .05. *p < .1.

Replace the explanatory variables and replace the number of employees at the beginning with EMP (number of employees at the end of the period with logarithm) for another regression analysis.

EMP_2 = ln (number of employees at the beginning of the period)

Vary the operating margin and replace the operating margin (operatio) with the sales margin (operatio_2) for another regression analysis.

operatio_2 = net profit/main business income

As seen in Table 9, after changing the variables for regression, the model is still significantly correlated at the 0.01 level, which proves the robustness of the model.

Research Findings

This paper analyzes the tax incentives, R&D investment, and employment absorption of 4,255 Chinese technology-based SMEs from 2018 to 2022 and draws the following conclusions.

(1) The employment absorption dispersion in technology-based SMEs is significant, while the R&D investment interval is relatively concentrated.

(2) There is a positive employment absorption correlation between tax incentives and R&D investment in technology-based SMEs, which is significant at 1%. The implementation of tax incentives and R&D investment have a significant promoting effect on employment absorption. This conclusion plays a vital role in the implementation of preferential tax policies, the promotion of R&D and innovation, and the enhancement of employment absorption capacity.

(3) Tax incentives and R&D investment positively impact employment absorption. The positive impact does not only exist in the current period but also remains valid in the following periods. From the comparison of the degree of positive impact, R&D investment exceeds tax incentives, and the former has more than twice the degree of impact than the latter, with all other factors remaining unchanged.

(4) Compared with external influences, the self-development of technology-based SMEs has more significant impacts on employment absorption. The self-development factors, such as R&D investment, operating profit margin, and remuneration, have more positive impacts on employment absorption. At the same time, technology-based SMEs should also pay attention to controlling and reducing overhead costs to play a better role in employment absorption.

(5) Although the tax incentives have been widely implemented, there are still some technology-based SMEs that still need to enjoy them. Therefore, other kinds of policies, together with tax incentives, should be effectively implemented to increase policy synergy and comprehensive support so that more policy dividends can better benefit technology-based SMEs.

Conclusions

Based on literature review and empirical studies, this paper proposes that three levels of government, enterprise, and society should work together to promote technology-based SMEs to achieve better employment absorption.

1. At the government level, various policies, including tax incentives, should be optimized to form a policy synergy. Human capital is particular to enterprises; a long-term employment system can effectively lower the human capital flow frequency and reduce the cost of hiring employees. At present, most preferential tax policies have implementation time limitations, and these time limitations depend on the issuance of new policies to replace the original policies. As one of the market economy central bodies, technology-based SMEs need a certain amount of time from receiving policies to adjusting their production and operation behaviors. There exists a time lag in the appearance of the effect of tax policies.

Meanwhile, the lack of continuity of tax policies will increase the cost of tax payments for enterprises and cannot provide stable expectations. Therefore, when formulating tax policies, it is necessary to plan the application period of policies reasonably, ensure the continuity of policies, formulate preferential tax policies with a relatively long period, stabilize enterprise expectations, and better achieve incentives for long-term employment. Firstly, the government should actively reduce the burden on technology-based SMEs, support them to increase R&D investments in research infrastructures and equipment, and fully implement preferential policies such as tax rebates, pre-tax deduction of R&D expenses, and preferential income tax for high-tech enterprises. Also, the government should comprehensively reduce the labor costs of technology-based SMEs and dynamically adjust the social security levy standards. Secondly, the government should cultivate the innovation momentum of technology-based SMEs, promote technology-based SMEs to realize the concentration of capital, workforce, and other complete elements, deepen the application of the industrial Internet of Things, and promote the complete opening of industrial application scenarios for technology-based SMEs, with corresponding subsidies.

2. At the enterprise level, technology-based SMEs should continuously strengthen their construction and achieve internal development. Firstly, they should enhance innovation capability, actively grasp new technology trends, new models, and new business trends, raise awareness of the importance of investment in research and development, and enhance the skeleton staff in research and development projects, talent pool. They should actively lead and participate in developing various standards and apply for international and national invention patents. Secondly, technology-based SMEs should accelerate innovation developments by integrating them into the industrial chain, and they should carry out upstream and downstream docking, realize various business synergies and resource integration with the industrial chain, and strive to realize their system integration and added value in the industrial chain. Thirdly, they should tap into the potential to reduce management costs, refine the accounts, avoid double counting of costs, eliminate gray costs, strengthen budget management, and implement strict control of management costs and accountability for overspending to reduce the generation of management costs effectively. Fourthly, financial personnel should pay close attention to tax law and regulation changes in time and choose the most advantageous tax planning methods for enterprises. Besides, they should make reasonable use of various preferential tax policies to help enterprises maximize the preferential benefits, increase the tax revenue of enterprises as much as possible, and reduce the negative impact of the tax burden on enterprises’ employment absorption.

3. At the social level, society should create a better business environment to encourage technology-based SMEs to invest in research and development, pay more attention to the improvement of the skills and quality of employees, and carry out social training courses and vocational education classes, to continuously cultivate professional talents needed in various fields, promote the matching of employees with jobs, and alleviate the structural unemployment problem. Firstly, they should support technology-based SMEs to gather talent, encourage technology-based SMEs to adopt more flexible ways to widely employ high-end talents both at home and abroad, optimize the permission of foreign high-end talents to work in China, support high-end talents to lead and undertake science and technology projects and provide high-quality services for high-end talents in education and medical service. Also, they should explore optimizing the market evaluation of talent mechanism, R&D talents, and R&D teams of technology-based SMEs with broad market prospects and high development potential to provide a certain amount of personal income tax incentives and give them priority support in R&D projects. Secondly, they should strengthen financial support, effectively use various governmental investment funds, and encourage social capital to strengthen support for technology-based SMEs’ R&D investment. Also, the financing guarantee system of technology-based SMEs should be constructed to guide bank credit funds, financing guarantee funds, and other types of funds to support technology-based SMEs in R&D investment to provide them with financing credit support. Thirdly, the entrepreneurial spirit should be vigorously promoted to strengthen strategic guidance and services for technology-based SME entrepreneurs and support their continuous implementation of exploratory development and innovative development, empowering them with decision-making power in constructing fundamental science and technology innovation projects and facilities.

Footnotes

Acknowledgements

We would like to thank the editor and anonymous reviewers for their helpful remarks.

Author Contributions

Conceptualization: Yanhua Mao. Data curation: Yanhua Mao. Formal analysis: Yanhua Mao. Funding acquisition: Yanhua Mao. Investigation: Yanhua Mao. Methodology: Yanhua Mao. Project administration: Yanhua Mao. Resources: Yanhua Mao. Software: Yanhua Mao. Supervision: Yanhua Mao. Validation: Yanhua Mao. Visualization: Yanhua Mao. Writing—original draft: Yanhua Mao. Writing—review & editing: Yanhua Mao.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is founded by National Social Science Foundation Key Project (22ATJ003) “Research on consensus mechanism of group evaluation based on trust relationship”; National Key Project of Statistical Research (2021LZ33) “Comprehensive evaluation technology and intelligent application based on social network,” and “Tax incentives, R&D investment and employment: An empirical study of innovative start-ups in Ningbo City”(Project of 6th Ningbo Philosophy and Social Science Research Base).

Ethical Approval

I certify that this manuscript is original and has not been published and will not be submitted elsewhere for publication while being considered by you. And the study is not split up into several parts to increase the quantity of submissions and submitted to various journals or to one journal over time. No data have been fabricated or manipulated (including images) to support our conclusions. No data, text, or theories by others are presented as if they were our own.

This paper does not contain any studies with human participants or animals performed by any of the authors.

Informed Consent

Informed consent was obtained from all individual participants included in the study.