Abstract

The digital economy is a cornerstone of high-quality development and sustainability. This study employs a difference-in-differences approach to investigate how tax incentives, specifically those induced by the pre-tax deduction of employee education expenses, influence corporate digital transformation. We find that increasing the pre-tax deduction ratio for employee education expenses significantly promotes corporate digital transformation, with the effect being more pronounced in non-state-owned enterprises, start-ups, declining firms, companies with higher tax burdens, and firms facing severe financing constraints. Mechanism tests reveal that the policy primarily drives corporate digital transformation through three core channels: alleviating financing constraints, upgrading human capital, and fostering innovation-driven initiatives. These findings provide valuable policy insights for deepening supply-side structural reforms and achieving high-quality economic development.

Plain language summary

This study takes the implementation of the 2018 Employee Education Expenses Pre-tax Deduction Policy as a quasi-natural experiment and empirically examines the effect and heterogeneity of the tax incentive policy on enterprise digital transformation. The findings show that the Employee Education Expenses Pre-tax Deduction Policy significantly promotes digital transformation in enterprises, with more potent effects observed in firms with higher growth potential, industries with intense competition, and regions with higher degrees of marketisation. Furthermore, the policy indirectly fosters digital transformation by alleviating financial pressure, optimising human capital investment, and promoting enterprise R&D innovation. This study enriches the institutional mechanism literature on corporate digital transformation by examining how macro-level human capital tax incentives influence firm behaviour. It also this research contributes to the literature on tax policies’ microeconomic impacts by providing evidence of how human capital tax incentives specifically affect digital transformation.

Introduction

With the rise in labour costs and optimisation of industrial structures, the extensive economic development model has become outdated (Huang et al., 2023). Digitalisation is considered a new engine for the high-quality development of traditional industries. On the one hand, digital transformation brings new changes to enterprise production and operations, including real-time monitoring of production, procurement, consumption, transportation, and inventory. On the other hand, digital transformation enhances product quality and strengthens innovation capabilities. Currently, China is at a critical juncture in building a manufacturing powerhouse, optimising the supply side, and adjusting its industrial structure. Supporting the development of the digital economy has become an important lever for promoting economic growth (Qiao et al., 2024; Wang et al., 2024). Actively promoting the transformation of enterprise development models from factor-driven to innovation-driven has become a key task in economic development (Backman, 2014). Simultaneously, enterprises are vigorously undergoing digital transformation and gradually integrating traditional production methods with digital technologies. This integration drives broader economic growth and helps achieve high-quality economic development.

Digital transformation has also facilitated the development of flatter organisational structures, reducing traditional management hierarchies through automation and informatisation, thus improving decision-making efficiency. Furthermore, the widespread application of digital technologies stimulated increased demand for employee skills, with companies increasingly relying on highly skilled talent possessing technical abilities and innovative thinking. This shift in demand has not only transformed recruitment and training strategies but has also prompted companies to increase investments in human capital to adapt to technological changes and market competition (Chen et al., 2023). Simultaneously, the impact of digitalisation on business models has become increasingly profound. By establishing digital platforms, enterprises have effectively collaborated among suppliers, customers, and partners, creating new digital ecosystems (Maaz et al., 2022). This ecosystem not only strengthens the interaction between businesses and consumers but also drives business process optimisation and value chain extension, significantly enhancing the market competitiveness of enterprises.

However, enterprises face financial pressures and technological risks during digital transformation. Continuous digital investment requires stable financial support. As a key element of digital transformation, human capital places a higher demand on corporate resource allocation. Existing research indicates that companies can significantly improve their digital capabilities and innovation capacity by improving their capital-to-labour ratio, employee compensation, and human capital quality (Stanko & Rindfleisch, 2023). However, continuous financial investment in digital transformation poses risks, including long return cycles and uncertain outcomes. Technological innovation requires sustained and stable financial support. Some studies suggest that improvements in digital transformation through increased capital-to-labour ratios and higher employee wages are unsustainable, with effects varying across different stages of a company’s lifecycle. Improving human capital quality is an effective way to enhance the efficiency of a company’s digital transformation (Huang and Gao, 2023). Furthermore, owing to the positive externalities associated with human capital investment, if trained employees leave a company, the return on investment will be challenging to recover, reducing the incentive for firms to invest in human capital (Chhaochharia et al., 2024). This market failure makes government intervention particularly important, as it can help address long-term investment challenges, provide financial stability, and encourage greater investment in human capital to drive successful digital transformation.

To effectively incentivise digital transformation in enterprises, the government introduced a series of policy measures, among which providing financial subsidies or tax incentives for human capital investment is one of the most common external incentives. Existing research finds that policies such as the minimum wage system and social security contributions reduce the marginal cost of human capital investment and encourage enterprises to increase their on-the-job training efforts (Fairis & Pedace, 2004). Fiscal subsidies can motivate enterprises to make sustained and stable investments in human capital, thus promoting digital transformation. However, these subsidies face regulatory difficulties and inefficiency (Yu et al., 2023). In contrast, tax incentives have garnered more attention owing to their flexibility and wide coverage. Tax reduction policies lower operational costs and increase disposable income for enterprises, providing more financial support for digital equipment procurement, technology development, and employee skills enhancement (Orihara & Suzuki, 2023). Simultaneously, tax incentives offer a safety net for enterprises facing the risks of technological innovation, encouraging them to invest more in emerging technologies, such as big data, artificial intelligence, and the Internet of Things. In turn, this improves production efficiency and market competitiveness (Chen et al., 2023).

Chinese government increased the tax pre-deduction ratio for employee education expenses to alleviate the financial pressure on enterprises regarding human capital investment in 2018. This policy aims to boost enterprises’ investments in employee education and vocational training through tax incentives. Research has shown that this policy effectively reduces the tax burden on enterprises, thereby increasing funding for employee training, vocational education, and research and development (R&D) innovation. This, in turn, enhances employees’ skill levels and productivity, further promoting technological innovation and market competitiveness within enterprises (Negassi & Sattin, 2019). Moreover, raising the tax credit ratio alleviates the cost burden on enterprises’ human capital investment and sends a positive signal, attracting high-quality talent to join the company and driving the optimisation and upgrading of human capital (Tian et al., 2022). Although existing studies have focused on the impact of policies such as social insurance (Yang, Su, et al., 2024), fiscal subsidies (Duan et al., 2024; Wang et al., 2023; Yang, Zhang, et al., 2024; Yu et al., 2023), green finance policies (Li & Wang, 2023), digital tax enforcement (Chen & He, 2024), and public data availability (Chen & Zhang, 2024) on digital transformation, relatively little research has evaluated the effectiveness of tax incentive policies in this field. Specifically, the internal mechanisms through which human capital tax incentives affect enterprises’ digital transformation remain underexplored.

This study takes the implementation of the 2018 Employee Education Expenses Pre-tax Deduction Policy as a quasi-natural experiment and empirically examines the effect and heterogeneity of the tax incentive policy on enterprise digital transformation using data from Shanghai and Shenzhen A-share listed companies between 2015 and 2022. The findings show that the Employee Education Expenses Pre-tax Deduction Policy significantly promotes digital transformation in enterprises, with more potent effects observed in firms with higher growth potential, industries with intense competition, and regions with higher degrees of marketisation. Furthermore, the policy indirectly fosters digital transformation by alleviating financial pressure, optimising human capital investment, and promoting enterprise R&D innovation. This finding validates the importance of tax policies in guiding micro-enterprise behaviour and provides valuable insights for the government to optimise fiscal and tax policies.

This study offers three aspects of contributions. First, it enriches the institutional mechanism literature on corporate digital transformation by examining how macro-level human capital tax incentives influence firm behaviour. While prior research has explored the economic consequences of digital transformation, including the roles of government fiscal expenditures (Duan et al., 2024), digital finance (Zhang et al., 2023), and consumer demand changes (Hafezieh & Pollock, 2023), limited attention has been given to the effects of human capital tax policies. This study addresses this gap by focusing on the Employee Education Expenses Pre-tax Deduction Policy, highlighting its role in promoting corporate digital transformation through financial relief, human capital optimisation, and enhanced R&D investment.

Second, this research contributes to the literature on tax policies’ microeconomic impacts by providing evidence of how human capital tax incentives specifically affect digital transformation. While previous studies have examined the effects of such policies on corporate tax burdens, financing constraints, and innovation capabilities (Badel et al., 2020; Oyinlola & Adedeji, 2022; Tian et al., 2022), this study is among the first to investigate their direct impact on digital transformation. By demonstrating that tax incentives can alleviate financial pressure and encourage investment in human capital and innovation, this work advances the understanding of how fiscal policies can drive technological progress.

Third, in terms of methodology, this study employs a quasi-natural experimental design using data from A-share listed companies in China between 2015 and 2022. Through a difference-in-differences (DID) approach, the study provides robust empirical evidence of the policy’s effectiveness in promoting digital transformation. The findings reveal that the policy has stronger effects in firms with higher growth potential, industries with intense competition, and regions with greater marketization, offering nuanced insights into the heterogeneous impacts of tax incentives. Overall, this research advances theoretical and empirical understanding of the link between fiscal policy and digital transformation, providing actionable insights for policymakers seeking to design effective tax incentives to promote human capital investment and high-quality development.

Institutional Background and Hypothesis Development

Institutional Background

The pre-tax deduction policy for employee education expenses was introduced as part of China’s broader economic transformation, responding to changes in the labour market, evolving social demands, national strategies, and the refinement of policies and regulations. The primary aim of the policy is to encourage enterprises to invest in vocational education and improve their workforce’s skills. According to the Corporate Income Tax Law of the People’s Republic of China and its regulations, enterprises can deduct expenses related to employee education, including vocational and technical training fees, from their taxable income. This deduction also applies to training for vocational school students.

Since 1981, China has emphasised the importance of vocational education, stating that it should be consistently promoted. To support this, the Ministry of Finance allowed enterprises to deduct 1% of their payroll for employee education expenses in 1982, increasing it to 1.5% shortly thereafter. However, the application of this policy has varied by region, with no consistent deduction ratio nationwide.

With the implementation of the strategy to build a talent-strong nation, talent development has become a central component of national policy. As a result, the government introduced further supportive policies, adjusting the pre-tax deduction ratio for employee education expenses. The Corporate Income Tax Law and its regulations, enacted in 2008, provided a legal framework for these deductions, specifying that up to 2.5% of payroll could be deducted. As the demand for vocational education grew, the government increased its support for corporate participation in training. In 2012, the Ministry of Finance raised the deduction ratio to 8% for enterprises within national innovation zones.

Building on this, the ‘Notice of the Ministry of Finance and the State Administration of Taxation on the Pre-tax Deduction Policy for Employee Education Expenses of High-tech Enterprises’ (Cai Shui [2015] No. 63) extended the 8% deduction ratio to all high-tech enterprises while maintaining the ratio at 2.5% for other enterprises. In 2018, the Ministry of Finance standardised the 8% deduction ratio for all enterprises, including non-high-tech companies, allowing any excess amounts to be carried forward to subsequent tax years. In 2019, the State Administration of Taxation refined the procedure, clarifying that enterprises could deduct up to 8% of their payroll for employee education expenses, with excess amounts deductible in future years. These policy changes reflect China’s growing support for vocational education, as the deduction ratio gradually increased from 2.5% to 8%, alleviating the financial burden on enterprises, promote vocational education, and enhance workers’ skills.

Hypothesis Development

Pre-Tax Deduction of Employee Education Expenses and Digital Transformation of Enterprises

Tax reduction incentive policies are crucial in modernising the economy and enhancing corporate competitiveness, driving the digital transformation of enterprises. Tax relief measures help release company funds, providing essential support for investments in digital technologies and infrastructure (Fink et al., 2020). First, tax reductions alleviate the financial burden on enterprises, enabling them to respond flexibly to market changes and technological upgrade demands, thus creating additional funding sources for digital transformation. These funds can be used to purchase advanced digital equipment, software systems, and data analysis tools, thereby improving production efficiency, optimising supply chain management, and enhancing customer service levels, ultimately strengthening enterprises’ market competitiveness (Deng et al., 2024).

Furthermore, through digital transformation, enterprises can achieve automation and intelligence in business processes, reduce operational costs, and improve the quality of products and services. Moreover, tax reduction policies encourage increased investments in digital talent development, and R&D. Enterprises use tax incentives to conduct systematic employee training and enhance their digital skills and innovation capabilities. A highly skilled digital workforce contributes to driving technological innovation and supports the introduction and application of cutting-edge technologies. By continuously improving their employees’ technical expertise, enterprises can maintain technological leadership positions in a fiercely competitive market and promote continuous innovation (Tian et al., 2022).

However, the effects and pathways of digital transformation under tax reduction incentive policies may vary significantly across different types of enterprises. For instance, state-owned enterprises (SOEs) and private enterprises differ in ownership structures, which may influence their use of funds and capacity for innovation. SOEs often face higher tax burdens and stricter policy requirements, making tax-reduction policies effective in alleviating their financial pressure and enhancing investment in digital technologies. In contrast, private enterprises, which typically encounter greater financing constraints, may benefit more directly from tax reductions in the short term by relieving financial pressures and accelerating the procurement of digital equipment. Based on the above analysis, this study proposes the following hypothesis:

The Mechanism of Tax Incentives Promoting Corporate Digital Transformation

The pre-tax deduction policy for employee education expenses helps reduce the tax burden on enterprises, thereby releasing more funds for research and application of digital technologies. The availability of these funds enables enterprises to invest more flexibly in key areas, such as digital equipment, software systems, and employee training, thereby improving their overall level of digitalisation (Guariglia & Liu, 2014). Simultaneously, the optimised allocation of these funds further promotes technological innovation, enhancing a company’s competitive advantage in the market. The pre-tax deduction policy alleviates financial pressure on enterprises, allowing them to focus more on long-term strategic planning and technological innovation rather than being overly concerned with short-term liquidity issues.

Moreover, this policy helps enhance a company’s creditworthiness in financial markets, improves its financial condition, and reduces operational risks, thereby raising its credit rating. This facilitates access to more favourable financing conditions and may attract greater attention and investment from investors, promoting capital flow and further accelerating the company’s digital transformation. In short, the pre-tax deduction policy for employee education expenses alleviates financing constraints, providing enterprises with more financial support and flexibility, thereby creating favourable conditions for digital transformation and ensuring the digital upgrade of the overall economy.

Furthermore, the effects of tax reduction policies vary across enterprises at different life cycle stages. For startups, which typically face tighter financial constraints, tax reduction policies can directly alleviate their financial pressure, enabling them to allocate more funds toward digital technology research and development and equipment procurement. In contrast, although mature enterprises generally have more abundant financial resources, tax reduction policies may have more strategic significance. These policies can provide long-term support for technological upgrades, talent development, and innovation projects, thereby driving continuous innovation and technological leadership during the digital transformation. Based on this, the following hypothesis is proposed:

A pre-tax deduction policy for employee education expenses helps enterprises allocate more resources to digital training for employees, thereby facilitating their digital transformation. This policy alleviates the financial burden on enterprises by encouraging them to increase investments in employee training and skill enhancement, thereby improving their technical expertise. It fosters the development of a highly skilled digital workforce, creating favourable conditions for enterprises to introduce and apply advanced technologies (Tian et al., 2022).

As a significant tax incentive, the pre-tax deduction policy for vocational education encourages enterprises to implement systematic and long-term training programs, avoiding fragmented and short-term skill training. Through such structured education, enterprises can enhance employees’ overall quality and technical skills while stimulating their innovative thinking. A highly skilled workforce improves a company’s production efficiency and fosters innovation capabilities, helping it gain a competitive edge in the market. Additionally, the pre-tax deduction policy for employee education expenses contributes to transforming corporate culture, reinforcing a culture of employee training and development. In turn, this enhances employee loyalty and motivation. When employees feel that the company values their career development, they are more likely to actively engage in its digital transformation process, driving the company toward higher levels of digital operations.

Enterprises with different tax burdens may respond differently to the pre-tax deduction policy for employee education expenses. For enterprises with heavier tax burdens, the funds released by the tax reduction policy can support large-scale employee training and enhance digital skills more effectively, further driving their overall digital transformation. In contrast, enterprises with a lighter tax burden may allocate these funds to other areas of development, which could result in more limited investment in digital talent development. Based on this, the following hypothesis is proposed:

The pre-tax deduction policy for employee education expenses helps enterprises invest more resources in R&D and innovation, thereby promoting digital transformation. This policy reduces the financial burden on enterprises, encouraging them to offer higher quality and more comprehensive training programs. These programs help employees master emerging technologies, such as big data analytics, artificial intelligence, blockchain, and the Internet of Things, enhancing their innovation capabilities and driving technological progress and process optimisation within the enterprise (Howell, 2016). Moreover, systematic vocational education improves employees’ technical skills and stimulates innovative thinking. By engaging with the latest industry trends and technological developments, employees become more adept at identifying opportunities for digital transformation and proposing innovative business models and service solutions. This bottom-up innovation drive provides continuous momentum for the enterprise’s digital transformation (Uoshima et al., 2021).

Additionally, the pre-tax deduction policy for employee education expenses promotes collaboration between enterprises and universities, research institutions, and professional training organisations, helping companies quickly access cutting-edge technologies and innovation resources. For example, collaborating with universities on technology R&D projects allows enterprises to leverage their research strengths to solve technical challenges encountered during digital transformation. Cooperation with training institutions provides employees with the latest technical training, accelerates introducing and applying new technologies within a company, and drives digital transformation (Tian et al., 2022).

However, the degree of financing constraints faced by different enterprises may affect the effectiveness of the pre-tax deduction policy for employee education expenses. Enterprises with more substantial financing constraints are more directly motivated by tax reduction policies because these policies alleviate their financial pressures and encourage innovation activities and the introduction of new technologies. These enterprises can use tax savings to invest in R&D or technology acquisition, accelerating their digital transformation. Based on this, the following hypothesis is proposed:

Research Design

Data

This study employs a dataset from Chinese firms listed on the Shanghai and Shenzhen Exchanges from 2015 to 2022, with an initial sample size of 17,186. The dataset is strategically segmented into two distinct periods, with 2018 as the critical division point. This approach facilitates a comprehensive analysis that captures 4 years of data before and after the pivotal year. To enhance the reliability of the sample, several methodological precautions were taken. First, data from the financial sector were excluded to avoid sector-specific biases. Second, firms with abnormal listing statuses, such as ST, *ST, or PT, were removed to ensure stability and representativeness. ST refers to stocks that are specially treated due to the company’s financial or operational issues, typically involving consecutive losses or financial reporting problems. *ST indicates that the company has incurred losses for three consecutive years and is at risk of delisting, warranting special treatment. PT denotes that the company is in a special risk status, which may involve major asset restructuring, financial issues, or significant challenges. Third, observations with missing values for key variables, including total assets, profits, and liabilities, were excluded to preserve data integrity. Lastly, continuous variables were winsorised at the 1% level to address extreme outliers. The data used in this study were sourced from the CSMAR and RESSET databases, both well-regarded for their comprehensive coverage and reliability in Chinese financial markets. The final sample comprises 16,836 observations.

Model

To examine the impact of tax incentives arising from the pre-tax deduction of employee education expenses on corporate digital transformation, we use the policy differences between non-high-tech and high-tech enterprises to construct a baseline regression model.

The prerequisite for employing the DID model is that the experimental and control groups satisfy the parallel trends assumption. To address this issue, drawing on Ferrara et al. (2012), this study uses an event study approach to conduct a parallel trends test; the specific model is as follows:

Furthermore, to verify the mediation mechanism and analyse how the pre-tax deduction policy for employee education expenses affects human capital upgrading, this study establishes the following models for examination:

In Equation (1), the subscripts i and t represent the firm and year, respectively. The dependent variable DIGITALi,t indicates the digital transformation of firm i. The mediating variable Finance represents financing constraints, human capital structure, and R&D innovation. Treati is a dummy variable indicating whether firm i is a pilot enterprise for the 2018 pre-tax deduction policy for employee education expenses, taking the value of 1 if the firm is a pilot (not previously benefiting from the 8% pre-tax deduction) and 0 otherwise. Aftert is a dummy variable for the policy implementation period, taking 1 for 2018 and beyond and 0 for years prior. To eliminate the interference of other factors on the parameter estimation, a series of firm-level control variables Xi,t are included. μi represents firm fixed effects, controlling for time-invariant firm characteristics that influence digital transformation. γt represents time-fixed effects, controlling for variables that change over time and affect digital transformation. εi,t is a random error term. When estimating the model, the standard errors of the coefficients are clustered at the firm level.

Variables

Firm’s Digital Transformation (DIGITAL)

Drawing on Yu et al. (2023), Chen and He (2024), Chen and Zhang (2024), and Yang, Su, et al. (2024), this study systematically identifies pertinent information related to digital transformation within corporate annual reports. This study uses advanced text analysis techniques to extract critical terms such as big data applications, artificial intelligence, cloud computing, and blockchain from these reports. These terms are then subjected to frequency analysis and synthesis to construct a comprehensive index quantifying the degree of digital transformation within a corporation. This methodological approach captures the extent of investment in and application of digital technologies across enterprises and provides a solid empirical basis for further research. The constructed index serves as a crucial tool for measuring digital transformation, offering a quantitative dimension to what has traditionally been a qualitative assessment. The dictionary for words related to digital transformation can be seen Appendix (Table A1).

We fully recognise the significant variation in the length of corporate annual reports and that absolute word frequency alone cannot provide an accurate comparison. Therefore, in the robustness analysis, we use the ratio of digital word frequency to total word frequency as an alternative proxy variable for digital transformation. This approach draws on another methodology which incorporates the ratio of digital intangible assets to total intangible assets disclosed in the financial reports of corporate annual reports as another proxy variable for a company’s digital transformation, as can be seen in robustness tests.

Treat × After

In 2008, the Ministry of Industry and Information Technology, in conjunction with the Ministry of Science and Technology, issued the ‘High-tech Enterprise Recognition Opinion’, which mandates that the recognition period for high-tech enterprises be limited to 3 years, with a required review every 3 years. Using data from the CSMAR, this study classifies companies that consistently received high-tech enterprise recognition from 2015 to 2018 as the control group. Conversely, companies that were never recognised as high-tech enterprises during this period are categorised as the experimental group. To facilitate the analysis, a dummy variable indicates whether an enterprise’s industry qualifies for the pre-tax deduction policy for employee education expenses, serving as the core interaction term, denoted as Treat × After. In this framework, Treat is assigned a value of 1 if the enterprise had not achieved high-tech enterprise recognition before the policy’s implementation; otherwise, it is assigned a value of 0. Similarly, the variable After is assigned a value of 1 if the observation pertains to 2018 or later; otherwise, it is assigned a value of 0. This interaction term allows us to rigorously assess the impact of the policy on corporate behaviour, that is, digital transformation.

We also consider several control variables: firm size (Size), firm age (Age), debt-to-asset ratio (Lev), management expense ratio (Gl), profitability (Roa), managerial ownership proportion (Ms), CEO duality (Dual), Tobin’s Q (Tobinq), nature of ownership (Soe), operating leverage (Op), and the proportion of independent directors (Indir). Including these control variables aims to enhance the explanatory power of the model and the reliability of the results, ensuring the scientific rigour and robustness of the study, as shown in Table 1.

Definition and Measurement of Variables.

Result

Descriptive Statistics

Table 2 presents the results for descriptive statistics. The sample mean of digital transformation, denoted as DIGITAL, is 2.4690. The mean of the treatment variable, Treat, is 0.2434, suggesting that policy implementation influenced 24% of the sample observations. The mean of the variable, After, is 0.6019, indicating that the sample is divided into 39.81% and 60.19% before and after the policy shock, respectively.

Descriptive Statistics of the Main Variables.

Main Analysis

Baseline Results

Table 3 presents the baseline regression results. Column (1) considers only firm and year-fixed effects. The estimated coefficient of the interaction term Treat × After is 0.082, statistically significant at the 5% level. This indicates that the policy has a significant positive effect on promoting digital transformation across the sampled firms. Column (2) introduces additional controls for firms’ financial indicators; however, the coefficient for the interaction term remains significantly positive, affirming the robustness of the initial findings. Column (3) expands the model by incorporating variables related to corporate governance structure, which further increases the estimated coefficient of Treat × After to 0.112, which is significant at the 1% level, suggesting that the pre-tax deduction policy has a consistent and positive influence on a firm’s digital transformation (Hypothesis 1).

Main Analysis for Pre-Tax Deduction of Employee Education Expenses and Digital Transformation.

Note. Robust standard errors clustered at the firm level in parentheses.

p < .05. ***p < .01.

From an economic perspective, the results indicate that firms affected by the policy experienced a 4.5% increase in digital transformation relative to the average level (0.112/2.4690) compared to those unaffected by the policy. Several factors contribute to this effect. First, the pre-tax deduction reduces the tax burden, thereby increasing firms’ disposable cash flow, which can be directed towards investments in digital technology research and application. Second, by incentivising firms to invest in employee education, the policy enhances employee skillsets, better preparing them to adopt and leverage digital technologies effectively. Furthermore, the policy encourages firms to allocate more resources to employee training, thereby fostering the development of internal talent and creating an organisational environment conducive to digital transformations.

Parallel Trend Assumption Test

Figure 1 presents the 95% confidence intervals and estimated coefficients, providing a visual analysis of whether the degree of digital transformation in firms varied over time between the treatment and control groups before and after the implementation of the policy. The results indicate that from 2015 to 2018, the differences between the treatment and control groups were not significant at the 10% level. This suggests that the digital transformation trends for firms in both groups remained relatively consistent before policy implementation, satisfying the parallel-trend assumption. This finding is crucial as it validates the use of the DID approach by confirming that any observed changes in digital transformation after policy implementation can be attributed to the policy itself rather than to pre-existing differences in trends between the two groups.

Parallel trend test.

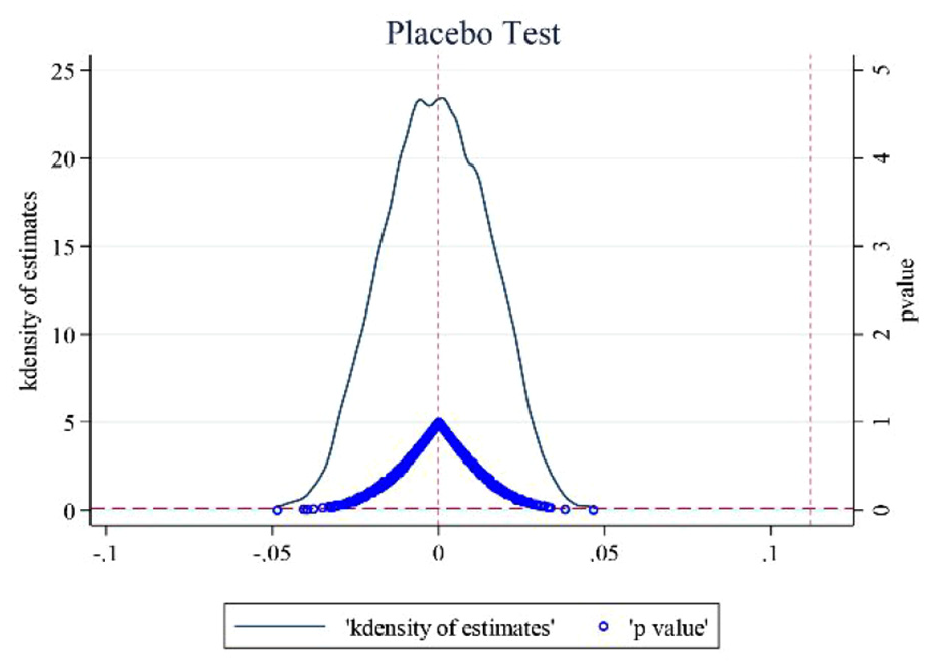

Placebo Test

We employ the methodology proposed by Moon (2022) to consider potential biases due to random factors. In this approach, a false treatment group was randomly generated, and an interaction term Treat × Afterfalse was created using the time dummy variable, resulting in the corresponding estimated coefficients (repeated 500 times). Theoretically, the regression coefficients of the falsely constructed core explanatory variable Treat × Afterfalse should be statistically insignificant. The distributions of the estimated coefficients are then plotted. As illustrated in Figure 2, the coefficients of Treat × Afterfalse are concentrated around zero and follow a normal distribution. Notably, the true estimated coefficient of Treat × After (0.112) lies entirely outside the distribution of the coefficients from the random experiments. This finding indicates that the baseline regression results are not driven by random factors.

Placebo test results.

Robustness Tests

Alternative Measurements of Dependent Variables

We also construct several indicators to assess a firm’s digital transformation, enabling robust testing of the main findings. On the one hand, recognising the potential variations in the length of corporate annual report texts, we adopt the methodology proposed by Hou (2023) to remeasure digital transformation by calculating the ratio of digital word frequency to total word frequency within these texts (column (1) of Table 4). Second, following the measurements by Huang and Gao (2023), the ratio of digital intangible assets to total intangible assets is used as a potential proxy for digital transformation (column (2) of Table 4). These findings confirm that the primary conclusions of this paper are robust across different measurement approaches, reinforcing the validity of the results after using alternative indicators of firms’ digital transformation.

Alternative Measurements of Dependent Variables.

Note. Robust standard errors clustered at the firm level in parentheses. Control variables are included but not reported for saving space.

p < .05. ***p < .01.

Exclusion of Specific Industries

Given the distinct characteristics of certain industries, particularly those with a high concentration of digital-related intangible assets, such as the information transmission, software applications, and Internet technology sectors, additional analyses were conducted to further validate the robustness of our regression results. Specifically, we exclude these industries from the overall sample, concentrating on sectors such as technology promotion and application services, software and information transmission, professional skills, and Internet-related services. Table 5 shows that after excluding industries characterised by a high concentration of intangible assets, the estimated coefficient for Treat × After remains significant at 1%. The robustness of these results across different industry subsets further substantiates the validity of our initial conclusions, highlighting the broader applicability of the policy’s effects beyond sectors traditionally associated with digital technologies.

Exclusion of Specific Industries.

Note. Same as Table 4.

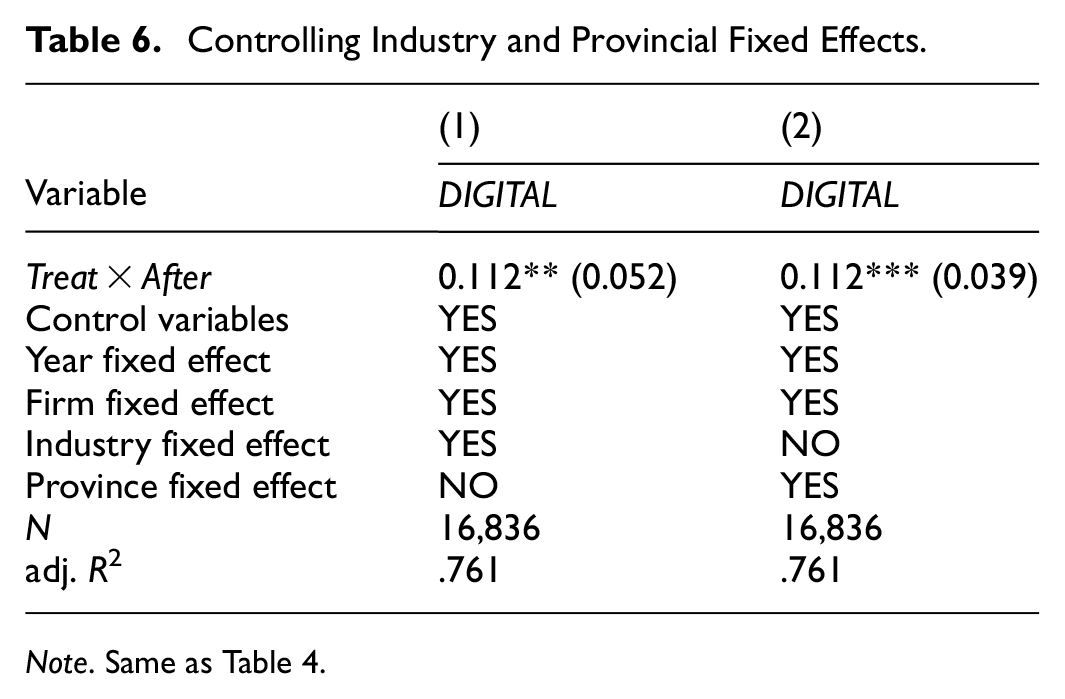

Considering more fixed effects

To eliminate the interference of industry and provincial-level factors that do not vary over time in the empirical results, we further controlled for industry and provincial-fixed effects. The regression results presented in Table 6 strongly support the baseline regression findings.

Controlling Industry and Provincial Fixed Effects.

Note. Same as Table 4.

Propensity Score Matching-Difference-in-Differences

To mitigate the interference of selection bias in parameter estimation, this study employs the Propensity Score Matching (PSM) method to identify suitable control group firms for the experimental group before conducting a DID estimation. Specifically, key firm characteristics such as firm size, debt-to-asset ratio, management expense ratio, profitability, growth potential, managerial ownership proportion, fixed asset ratio, operating cash flow, and firm age are selected as covariates. A logit model calculates the propensity scores, followed by various matching methods, including 1-to-1 nearest neighbour matching, 1-to-2 nearest neighbour matching, 1-to-3 nearest neighbour matching, and kernel density matching, to match the experimental and control group samples. Subsequently, the matched sample that satisfies the common support assumption is used as the basis for DID estimation to assess the net effect of the pre-tax deduction policy for employee education expenses on human capital upgrading.

Columns (1) to (4) of Table 7 correspond to the results of 1-to-1 nearest neighbour matching, 1-to-2 nearest neighbour matching, 1-to-3 nearest neighbour matching, and kernel matching, respectively. The estimation results indicate that the coefficients, signs, and significance levels obtained using the PSM-DID method are consistent with those from the baseline regression, reaffirming the positive role of the pre-tax deduction policy for employee education expenses in driving corporate digital transformation. This consistency underscores the robustness of the conclusions of this study. Balance tests are conducted to further evaluate the quality of the matching results, and detailed outcomes are presented in Figure 3a–d. These results demonstrate that the standardised biases of most variables are significantly reduced after matching, indicating an effective balance of the matched data.

Propensity Score Matching-Difference-in-Differences.

Note. Same as Table 4.

Balance test. (a) Calliper matching (1:1). (b) Calliper matching (1:2). (c) Calliper matching (1:3). (d) Kernel matching.

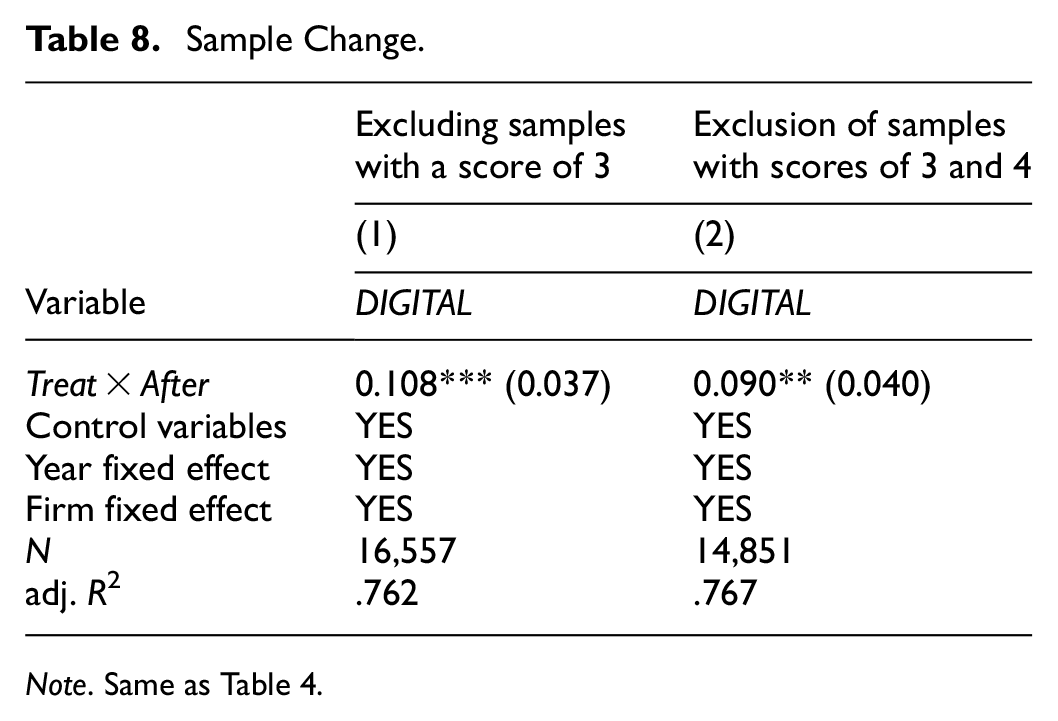

Sample Change

Given that the metrics for firms’ digital transformation are derived from corporate annual report texts, there is an inherent risk of discrepancies, which may lead to inaccuracies in interpreting these texts and result in measurement bias when evaluating firms’ digital transformation. This study assesses the quality of disclosures in annual reports to construct a more accurate digital transformation index. This assessment is based on analyst attention, information disclosure levels, and the internal disclosure control index. The quality of the disclosures is scored on a scale from 1 to 4, with 1 indicating excellent quality, 2 good, 3 satisfactory, and 4 unsatisfactory. Samples with scores of 3 and 4 were excluded, leaving only higher-quality samples for regression analysis. The results in Table 8 remain stable compared to the primary analyses above.

Sample Change.

Note. Same as Table 4.

Exclusion of Other Interfering Policies

The baseline regression results may be partially driven by these concurrent policies from 2015 to 2022 rather than solely by the pre-tax deduction policy for employee education expenses. A systematic approach is adopted to exclude potential confounding effects of other policies. First, we considered the impact of the reduction in social insurance fees. In 2019, the Ministry of Finance lowered the corporate pension insurance contribution rate, effectively increasing disposable funds for enterprises, alleviating financing constraints, and potentially influencing digital transformation. To control this confounding factor, we followed the methodology of Liu et al. (2021) by measuring the social insurance contribution rate (sb) as the ratio of newly added social insurance contributions in the current year to employee wages and salaries in the previous year. The results in column (1) of Table 9 remain robust after controlling for the effects of reduced social insurance fees.

Exclusion of Other Interference Policy Interpretation I.

Note. Same as Table 4.

Second, considering the impact of personal income tax reform, the State Council introduced a reform policy in 2018 that could have affected employee compensation, thereby influencing motivation and digital transformation. To control for this effect, we followed the methodology of Sandvik et al. (2021), measuring the average wage level (pw_after) as the ratio of total employee compensation to the number of employees. After including this variable, the results in column (2) of Table 9 remain unchanged.

Third, we address the influence of bank credit support policies. Financial departments have increased bank credit support to help enterprises alleviate financing constraints and resolve liquidity issues which may affect firms’ digital transformation. To control this, we follow Léon and Weill’s (2024) approach using the natural logarithm of the firm’s bank loans for the current year to measure access to credit (loan). This variable is included as a control in the baseline model, and the results are shown in column (3) of Table 9. The estimated coefficient of the interaction term Treat × After remains significantly positive.

Fourth, we considered the impact of the VAT refund reform. The Ministry of Finance issued the ‘Notice on the Tax Policies for Refunding VAT Retained in Certain Industries’ (Caishui [2018] No. 70) to support high-quality economic development by refunding VAT retained in specific industries, which could influence firms’ digital transformation by reducing operating costs and alleviating financing constraints. A dummy variable (ts_after) indicates whether a firm is affected by the VAT refund policy, with a value of 1 if affected and 0 otherwise. Column (4) of Table 9 still supports the baseline findings.

Fifth, China has implemented a series of VAT rate reductions since 2017, which may have affected firms’ digital transformation. We followed the approach of Chen (2017), including the actual VAT rate (vtax) of enterprises in the baseline model. The results in column (1) of Table 10 still support our hypothesis.

Exclusion of Other Interference Policy Interpretation II.

Note. Same as Table 4.

Sixth, considering the ‘Business Tax to Value-Added Tax’ (BT to VAT) reform from 2012 and 2016, the 2015 sample was excluded, and the regression was re-run. The results in column (2) of Table 10 indicate that the estimated coefficient of Treat × After remains significantly positive, which supports our findings above.

Seventh, considering the impact of the accelerated depreciation policy for fixed assets initiated in 2014, which aims to reduce costs for high-tech firms and may stimulate investment and promote digital transformation. In 2015, the policy was gradually extended to key industries in light, textiles, machinery, and automobiles and further extended to all manufacturing industries in 2019. We follow the approach of Du et al. (2023) and include a dummy variable (cv_after) to indicate the impact of the accelerated depreciation policy. The results in column (3) of Table 10 remain unchanged compared with our main analysis.

Eighth, we exclude the impact of the R&D expense super deduction policy, which reduces R&D costs and promotes technological innovation, potentially influencing digital transformation. To control for this effect, we follow the methodology of Oswald et al. (2022), using the natural logarithm of the enterprise’s ‘R&D expense super deduction amount’ to measure the actual R&D super deduction situation. The regression results in column (4) of Table 10 confirm that the positive impact of the tax policy for employee education expenses on firms’ digital transformation is not driven by other concurrent policies, further validating the baseline results.

Further Analysis

Mechanism Analysis

Financing Constraint

The tax-deductible employee education expenses policy is a strategic tax incentive aimed at reducing the tax burden on enterprises and alleviating their financing constraints. Digital transformation often requires significant financial investment, and by lowering the tax burden, this policy can effectively mitigate the financial risks associated with such transformative processes. To delve deeper into the underlying mechanism and draw on the work of Hadlock and Pierce (2010), an internal and external financing constraint indicator for enterprises is constructed. This indicator facilitates a more nuanced analysis of whether the tax-deductible employee education expenses policy aids digital transformation by easing these financing constraints.

In Equation (3), Financei,t represents enterprises’ external financing constraints (sa) and internal financing constraints (cf). The definitions and symbols of the remaining variables are consistent with those used in the baseline regression. External financing constraints (sa) are measured using the absolute value of the SA index; the larger the value, the smaller the external financing constraints faced by the enterprise. The SA index is typically calculated based on a company’s financial data, particularly factors such as capital structure, liquidity, and profitability. The standard calculation formula is as follows: SA = (B−A)/C, where: B represents the company’s external financing needs, typically measured by financial indicators such as capital expenditures and debt repayment requirements. A refers to the company’s internal funding sources, such as retained earnings or cash flow. C represents the company’s overall financing capacity, generally including factors such as leverage and the availability of bank credit. The higher the value of the SA index, the stronger the external financing constraints faced by the company, indicating lower flexibility in obtaining financing.

Columns (1) and (2) of Table 11 present the regression results for external financing constraints. In column (1), the estimated coefficient of the interaction term Treat × After is 0.007 and significant at the 5% level, indicating that the tax incentive induced by tax-deductible employee education expenses can reduce enterprises’ external financing constraints. In column (2), the estimated coefficient of external financing constraints (sa) is significantly positive, suggesting that a tax-deductible employee education expenses policy can promote digital transformation by improving external financing constraints for enterprises.

Mechanism Analysis: Financial Constraints.

Note. Same as Table 4.

Internal financing constraints (cf) are measured by the ratio of cash holdings to total assets (Feng et al., 2022), with higher values indicating smaller internal financing constraints. The specific regression results are presented in columns (3) and (4) of Table 11. In column (3), the estimated coefficient of the interaction term Treat × After is significantly positive, suggesting that a tax-deductible employee education expenses policy can effectively alleviate internal financing constraints. The results in column (4) further support this finding, with an estimated coefficient of Treat × After being 0.108 (p < .01). These results demonstrate that a tax-deductible employee education expense policy significantly improves enterprises’ external and internal financing constraints, facilitating their digital transformation. The consistent findings across columns (1) to (4) of Table 11 support Hypothesis 2, indicating the role of financing constraints in mediating the relationship between tax incentives and digital transformation within firms.

Corporate Human Capital

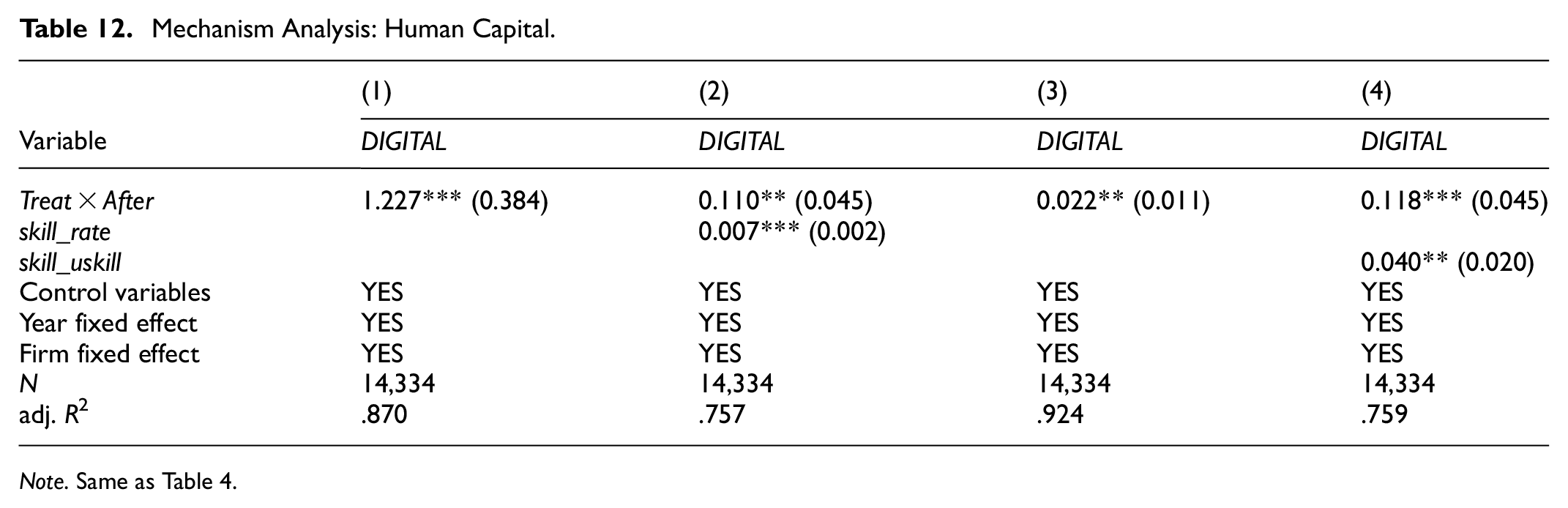

Given that digital transformation requires the substantial involvement of multiskilled talent, adjusting talent quality and structure becomes a key driver of this transformation. To further elucidate the mechanism by which the tax deduction policy for employee education expenses promotes corporate digital transformation through the enhancement of human capital, this study adopts Abraham and Mallatt’s (2022) methodology, utilising both education and job structures to measure the human capital structure within enterprises.

Employee positions include administrative management, technical R&D, marketing and sales, production operations, and financial auditing. Labour is divided into skilled and unskilled categories based on skill levels, with skilled labour comprising technical R&D personnel and unskilled labour including all other employees. The ratios of skilled labour to total labour (skill_rate) and skilled labour to unskilled labour (skill_uskill) are included. The results in columns (1) and (3) of Table 12 indicate that the tax deduction policy for employee education expenses significantly increases the demand for skilled labour within enterprises. Additionally, the results in columns (2) and (4) of Table 12 demonstrate that the tax deduction policy for employee education expenses facilitates corporate digital transformation by enhancing the human capital structure within enterprises. These findings confirm Hypothesis 3.

Mechanism Analysis: Human Capital.

Note. Same as Table 4.

Corporate Innovation

Tax incentives are crucial in promoting corporate innovation and providing essential technical support for digital transformation. Building on Kong et al. (2022), this study measures corporate innovation output using the number of patent applications as an indicator. Innovation is the natural logarithm of the total number of corporate patent applications. Innovation_f, Innovation_x, and Innovation_w represent the natural logarithms of the number of inventions, utility models, and design patent applications, respectively.

The results in columns (1) and (2) of Table 13 indicate that the tax deduction policy for employee education expenses significantly enhances corporate digital transformation by boosting overall innovation levels. Further analysis disaggregates patent applications into different types—namely, invention, utility model, and design patents. The regression results, detailed in columns (3) through (8) of Table 13, reveal that the estimated coefficients of the interaction term Treat × After are significantly positive across all types of patents. Additionally, the coefficients of the corporate innovation variables (Innovation_f, Innovation_x, and Innovation_w) are significantly positive, underscoring the critical role of innovation in facilitating digital transformation.

Mechanism Analysis: Corporate Innovation.

Note. Same as Table 4.

These findings reaffirm the mechanism by which the tax deduction policy for employee education expenses drives digital transformation through enhanced corporate innovation. The consistent positive impact across different types of patent applications confirms Hypothesis 4, highlighting the importance of fostering innovation to achieve digital transformation within firms.

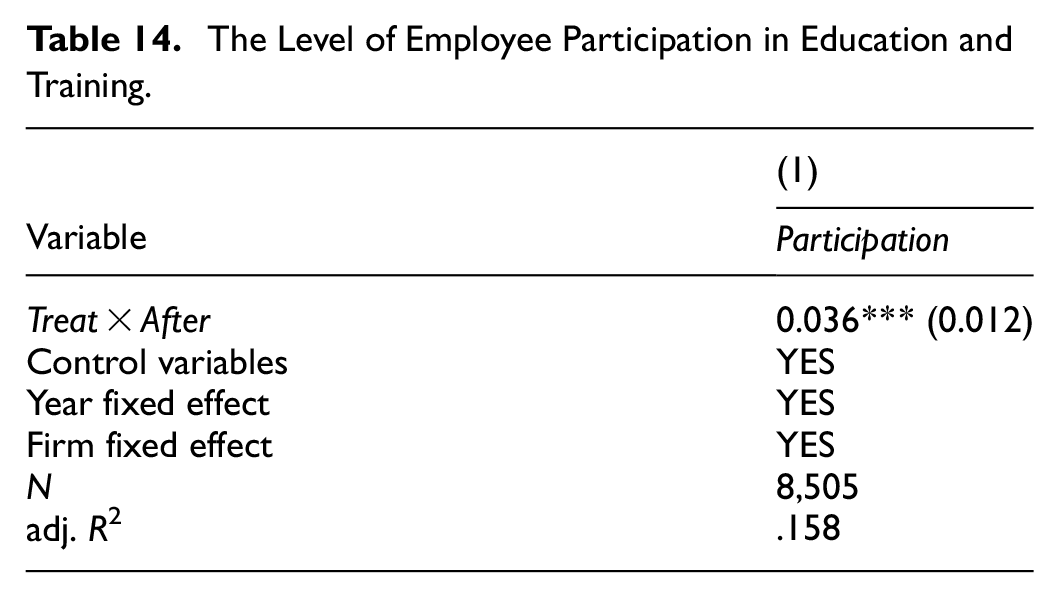

Direct Impact of Pre-Tax Deduction Policy on Employee Participation in Training and Education

We further examine whether the 2018 pre-tax deduction policy for employee education expenses increased employee participation in training and education. Considering the methodology of Guo (2018) to measure the extent of enterprise utilization of training subsidies, we calculate the ratio of total government training subsidies to the total assets of the enterprise as a proxy for employee participation. Given the absence of a centralised database for government training subsidies in our country, we manually extracted relevant data from the ‘Government Subsidies’ section under ‘Union and Employee Education Fund-Related Subsidies’ in the ‘Financial Report Notes’ of the ‘Company Research Series’ within the CSMAR database. This approach enables us to indirectly represent the level of employee participation in training and education. Using a difference-in-differences (DID) model, our empirical results, presented in Table 14, confirm that the implementation of the pre-tax deduction policy significantly increased employee engagement in training and education.

The Level of Employee Participation in Education and Training.

Heterogeneity Analysis

Non-SOEs face more limited access to credit than SOEs, and firms in the growth stage are more likely to encounter financing constraints than those in the maturity stage. Similarly, firms with heavier tax burdens tend to have less liquidity available. Additionally, it is crucial to further consider the heterogeneous impacts arising from factors such as firm type, the direction of digital transformation, and the degree of market-oriented development.

Property Right (State-Owned vs. Non-State-Owned Enterprises)

The impact of tax incentives on digital transformation can differ significantly depending on the nature of corporate ownership. SOEs generally have greater access to credit channels and face fewer obstacles in securing external funding. Consequently, increased cash flows resulting from tax incentives may provide relatively less motivation for digital transformation in SOEs, as suggested by Lv & Wu (2024). By contrast, non-SOEs, which typically experience more severe financing constraints, may benefit more from the pre-tax deduction policy for employee education expenses (Xiang et al., 2023). This policy enhances cash flow, promotes talent structure upgrades, and drives technological innovation, likely leading to a more pronounced effect on the digitalisation efforts of non-SOEs.

The results presented in columns (1) and (2) of Table 15 reveal that the policy has a significantly greater impact on the digital transformation of non-SOEs than on SOEs. Specifically, the interaction term Treat × After exhibits a stronger positive coefficient in the non-SOE group, indicating that the policy’s effect on enhancing digital transformation is more substantial among firms with more constrained access to external funding. These findings suggest that ownership structure plays a critical role in determining the effectiveness of tax incentives in promoting digital transformation.

Heterogeneity Analysis Considering Property Right (State Ownership vs. Non State Ownership).

Note. Same as Table 4.

Firm lifecycle

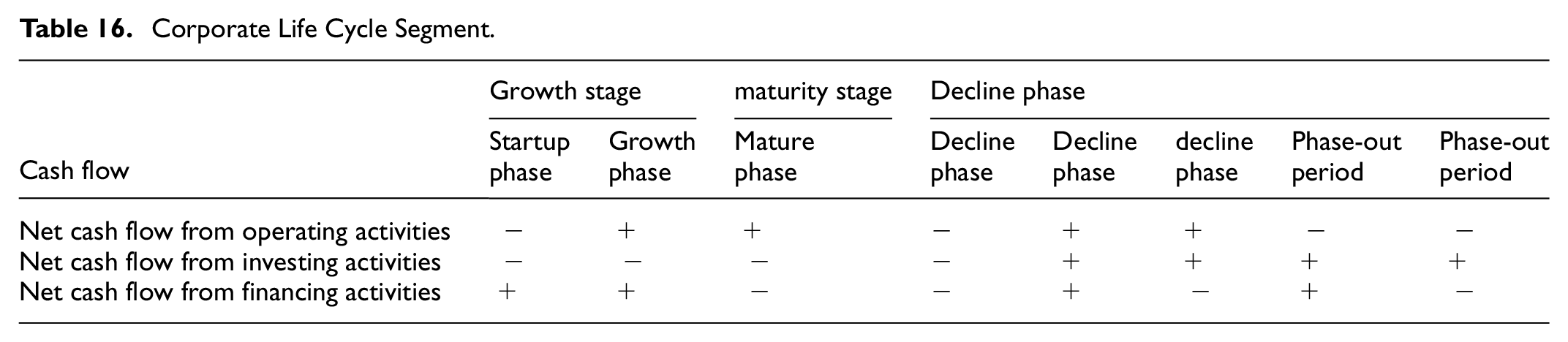

An enterprise’s stage of development plays a crucial role in determining its financing constraints. Mature enterprises generally have more robust financial resources than firms in the start-up or decline stages (Furceri et al., 2021). Consequently, the pre-tax deduction of employee education expenses, aimed at alleviating financing constraints, is more likely to foster digital transformation in startups and declining firms, where financial limitations are more pronounced.

Following the methodology proposed by Dickinson (2011), this study employs a cash flow approach to categorise firms into different life cycle stages (see Table 16). Dickinson’s method identifies the stage of a company’s lifecycle by analysing the trends in various financial indicators, such as net operating cash flow, net investing cash flow, and net financing cash flow. It is typically positive during the startup phase and negative during the maturity and decline phases. By examining these cash flow patterns, this method helps in determining the specific stage of a company’s lifecycle.

Corporate Life Cycle Segment.

Based on this approach, the sample enterprises are divided into three groups: startup, mature, and declining stages. Grouped regressions are then conducted to assess the impact of the pre-tax deduction policy across these different stages of a firm’s life cycle. The results are summarised in Table 17. The estimated coefficient of the interaction Treat × After in column (1), which pertains to mature firms, is not statistically significant. This suggests that, for mature enterprises, which generally face fewer financing constraints, the tax deduction policy does not significantly affect their digital transformation efforts.

Heterogeneity Analysis Considering Enterprise Lifecycle.

Note. Same as Table 4.

In contrast, the coefficients in columns (2) and (3), which correspond to firms in the startup and decline stages, respectively, are significantly positive. This finding indicates that the pre-tax deduction policy for employee education expenses has a substantial positive effect on promoting digital transformation in these firms. The results highlight that the policy is particularly effective in stimulating digital transformation in enterprises that are either in their early stages of development or facing decline, where the alleviation of financing constraints is more critical.

Firm Tax Burden

Varying tax burdens across enterprises can lead to differential impacts of tax incentives on their digital transformation efforts. Specifically, for enterprises with a high tax burden, a pre-tax deduction policy for employee education expenses is likely more effective in alleviating financing constraints, thereby exerting a more significant influence on their digital transformation.

To examine this, this study follows the methodology of Chen et al. (2018) and constructs a tax burden indicator measured as the ratio of corporate income tax expenses to operating revenue. Based on this indicator, the sample is divided into two groups–high- and low-tax-burden enterprises–using the median tax burden as the dividing line. The results presented in columns (1) and (2) of Table 18 provide clear evidence that pre-tax deductions for employee education expenses have a more pronounced effect on the digital transformation of high-tax burden enterprises than on their low-tax burden counterparts. The estimated coefficients for the interaction term Treat × After are significantly positive in the high-tax burden group, indicating that these enterprises benefit more from the policy promoting digital transformation.

Heterogeneity Analysis Considering Tax Burden.

Note. Same as Table 4.

This outcome is consistent with theoretical expectations because enterprises with higher tax burdens experience greater relief from financing constraints when their tax liabilities are reduced. This relief allows them to allocate more resources toward digital initiatives, accelerating their transformation. Conversely, for low-tax burden enterprises, the marginal benefit of the tax deduction policy is less impactful, resulting in a comparatively smaller influence on their digital transformation. The results suggest that tax policies promoting innovation and digitalisation may be particularly beneficial for enterprises facing higher tax burdens because they are more likely to leverage the financial relief provided by such policies to enhance their technological capabilities and digital infrastructure.

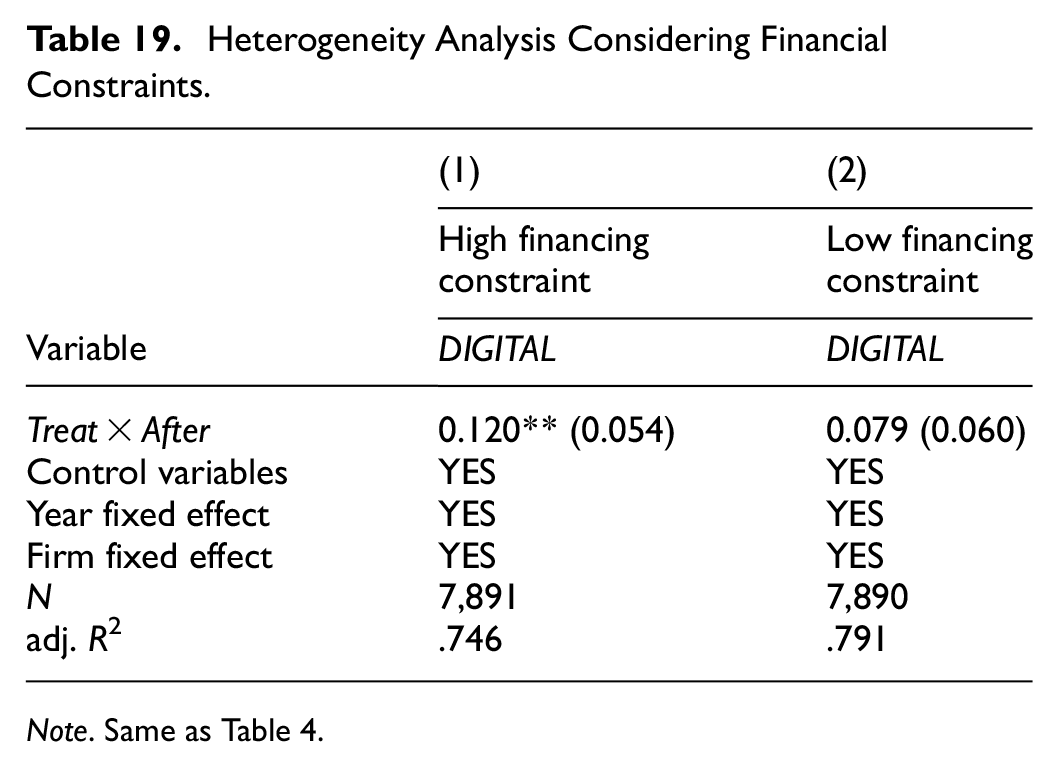

Financial Constraints

The pre-tax deduction policy for employee education expenses enables enterprises to benefit from tax reductions, thereby increasing disposable cash flow for firms facing high financing constraints and promoting their digital transformation. To further validate this theoretical hypothesis, we follow Mertzanis et al. (2024) by dividing the sample into high and low financing constraint groups based on the median SA index of the enterprises. The SA index is a well-established measure of external financing constraints, with higher values indicating greater financial difficulty.

As shown in columns (1) and (2) of Table 19, in the high financing constraint group, the estimated coefficient of the interaction term Treat × After is significantly positive. This finding indicates that the pre-tax deduction policy for employee education expenses is particularly effective in releasing liquidity for firms with high financing constraints, making their impact on digital transformation more pronounced. In contrast, for firms with relatively easier access to external financing, the additional liquidity provided by the tax deduction policy does not substantially influence their digital transformation efforts.

Heterogeneity Analysis Considering Financial Constraints.

Note. Same as Table 4.

Policies play a crucial role in alleviating financial pressure and enabling greater investment in digital technologies for firms with high financing constraints. Conversely, for firms with low financing constraints, the policy’s impact is less pronounced because these firms already have adequate access to financial resources. Overall, the study confirms that the pre-tax deduction policy is most beneficial for enterprises that face significant financial challenges, as it helps unlock the liquidity necessary to support their digital transformation initiatives.

Conclusion

Findings

This study uses data from Chinese A-share listed companies on the Shanghai and Shenzhen stock exchanges, covering 2015 to 2022, and uses the 2018 pre-tax deduction policy for employee education expenses as an exogenous shock event. By employing a DID model, this study examines the impact of this policy on corporate digital transformation, yielding the following key conclusions. (a) The pre-tax deduction policy for employee education expenses significantly promotes corporate digital transformation. (b) Heterogeneity analysis reveals that the policy’s impact is more pronounced in non-SOEs, startups and declining firms, high tax-burden companies, and firms facing high financing constraints. (c) From the perspective of the impact mechanism, the pre-tax deduction policy primarily facilitates digital transformation by alleviating financing constraints, enhancing human capital, and incentivising corporate innovation. The findings offer important policy implications for optimising the role of tax incentives in promoting corporate digital transformation.

Implications

Our research indicates that the pre-tax deduction policy for employee education expenses significantly alleviates financing pressures, particularly for small and medium-sized enterprises (SMEs) and labour-intensive businesses facing financial difficulties. First, government should consider including digital transformation-related employee training programs such as courses in data analysis, artificial intelligence, and big data applications within pre-tax deductions for employee education expenses. This would encourage enterprises to increase their investment in digital technology training and ensure their employees possess essential digital skills. Next, support for enterprises with high financing constraints should be increased. Particularly for SMEs and local enterprises with significant financing difficulties, the government should consider increasing the pre-tax deduction ratio for employee education expenses. For example, the government could establish a dedicated tax-reduction fund to support digital skills training and technological upgrades. By offering tax relief, enterprises can ease their financial pressure, enabling them to focus more on technological R&D and innovation, thereby accelerating digital transformation.

The government should establish an innovation incentive mechanism to drive the digital transformation of enterprises. The pre-tax deduction policy for employee education expenses can facilitate this transformation by promoting innovation-driven development and enhancing human capital. To refine this policy, the government could create an innovation reward system for enterprises that achieve significant advancements in their digital transformation. These rewards could include financial subsidies and tax reductions, with incentives based on various factors such as technological R&D outcomes, human resource investments, and progress in digital transformation. This would encourage enterprises to invest more in technological innovation and the development of employee skills. Moreover, the government should increase support for high-tech enterprises. For those that have made notable progress in digital transformation, expanding the scope of pre-tax deductions for employee education expenses would further incentivise deeper technological breakthroughs. For example, businesses involved in cutting-edge technologies like big data and artificial intelligence could benefit from tailored tax policies that promote innovation and boost their competitiveness in the market. Additionally, the government should strengthen collaboration between enterprises and research institutions by establishing joint ‘industry-university-research’ platforms. These platforms would facilitate digital technology R&D through partnerships with universities and research organisations. Enterprises participating in these projects should be eligible for pre-tax deduction benefits for employee education expenses, supporting both R&D and the practical application of emerging technologies. Such tax incentives would foster an environment conducive to technological advancement and the widespread adoption of digital innovations.

Third, the government should implement differentiated tax incentives to support the digital transformation of enterprises at various stages of their lifecycle. The impact of the pre-tax deduction policy for employee education expenses varies depending on the stage of the enterprise. Mature enterprises typically benefit more from these deductions than growth-stage companies. Therefore, the government should tailor tax incentives to the specific needs of enterprises at different development stages to encourage digital transformation across the entire lifecycle. For startups, especially those in the technology sector, the government could consider increasing the pre-tax deduction ratio for employee education expenses or offering additional tax reductions. Since startups often face financial constraints, establishing special funds or providing low-interest loans would help these companies improve their employees’ digital skills and enhance their technological innovation capabilities. For growth-stage enterprises, the pre-tax deduction policy should be combined with additional incentives for R&D expenses. These enterprises often experience rapid growth and have significant technological innovation needs. By increasing the pre-tax deduction rates for both R&D and employee training, the government can help these businesses leverage technology and human capital more effectively, thus driving the development and application of digital technologies. For mature enterprises, the pre-tax deduction policy should further encourage investment in areas such as smart manufacturing, information systems, and digital management. This would help these enterprises continue innovating and enhance their employees’ skills, ensuring ongoing improvements in digital transformation.

Limitations and Future Orientation

Although we provide serval implications on corporate digital transformation, limitations warrant further exploration in future research. First, it relies primarily on data from companies listed on the Shanghai and Shenzhen A-shares market. While the data are relatively rich, due to its limitations, the analysis does not include data from non-listed firms or SMEs. Future studies could extend this research to cover a broader range of company types, particularly SMEs and regional enterprises, which would provide a more comprehensive assessment of the impact of the Employee Education Expense Pre-Tax Deduction Policy on digital transformation. Second, this paper mainly explores the policy’s direct impact on corporate digital transformation. Future research could delve deeper into the indirect effects of the policy on corporate innovation capabilities, market competitiveness, and other related areas as well as the underlying mechanisms.

Footnotes

Appendix

Construction of Corporate Digital Transformation Index and Keyword Selection.

| Dimension | Categorised idioms | High-frequency text combinations | Word segmentation dictionary |

|---|---|---|---|

| Digital Technology Application | Data, Digital, Digitalisation | Data Management, Data Mining, Data Networks, Data Platforms, Data Centres, Data Science, Digital Control, Digital Technology, Digital Communication, Digital Networks, Digital Intelligence, Digital Terminals, Digital Marketing, Digitalization | Data Management, Data Mining, Data Networks, Data Platforms, Data Centres, Data Science, Digital Control, Digital Technology, Digital Communication, Digital Networks, Digital Intelligence, Digital Terminals, Digital Marketing, Digitalization, Big Data, Cloud Computing, Cloud IT, Cloud Ecosystem, Cloud Services, Cloud Platforms, Blockchain, Internet of Things (IoT), Machine Learning |

| Internet Business Model | Internet, E-commerce | Mobile Internet, Industrial Internet, Industrial Internet of Things (IIoT), Internet Solutions, Internet Technology, Internet Thinking, Internet Initiatives, Internet Operations, Mobile Internet, Internet Applications, Internet Marketing, Internet Strategy, Internet Platforms, Internet Models, Internet Business Models, Internet Ecosystem, E-commerce, Electronic Commerce | Mobile Internet, Industrial Internet, Industrial Internet of Things (IIoT), Internet Solutions, Internet Technology, Internet Thinking, Internet Initiatives, Internet Business, Mobile Internet, Internet Applications, Internet Marketing, Internet Strategy, Internet Platforms, Internet Models, Internet Business Models, Internet Ecosystem, E-commerce, Electronic Commerce, Internet, ‘Internet +’, Online and Offline, Online-to-Offline, Online and Offline Integration, O2O, B2B, C2C, B2C, C2B |

| Smart Manufacturing | Smart, Intelligent, Automation, CNC (Computer Numerical Control), Integration, Integrated | Artificial Intelligence, Advanced Intelligence, Industrial Intelligence, Mobile Intelligence, Intelligent Control, Intelligent Terminals, Intelligent Mobility, Intelligent Management, Smart Factories, Smart Logistics, Smart Manufacturing, Smart Warehousing, Intelligent Technology, Smart Equipment, Smart Production, Smart Connectivity, Intelligent Systems, Automation, Automatic Control, Automatic Monitoring, Automatic Surveillance, Automatic Detection, Automatic Production, CNC (Computer Numerical Control), Integration, Integrated Solutions, Integrated Control, Integrated Systems | Artificial Intelligence, Advanced Intelligence, Industrial Intelligence, Mobile Intelligence, Intelligent Control, Intelligent Terminals, Intelligent Mobility, Intelligent Management, Smart Factories, Smart Logistics, Smart Manufacturing, Smart Warehousing, Intelligent Technology, Smart Equipment, Smart Production, Smart Connectivity, Intelligent Systems, Intelligence, Automation, Automatic Control, Automatic Monitoring, Automatic Surveillance, Automatic Detection, Automatic Production, CNC (Computer Numerical Control), Integration, Integrated Solutions, Integrated Control, Integrated Systems, Industrial Cloud, Future Factories, Intelligent Fault Diagnosis, Lifecycle Management, Manufacturing Execution Systems (MES), Virtualization, Virtual Manufacturing |

| Modern Information Systems | Information, Informatization, Networking | Information Sharing, Information Management, Information Integration, Information Software, Information Systems, Information Networks, Information Terminals, Information Centres, Informatization, Networking | Information Sharing, Information Management, Information Integration, Information Software, Information Systems, Information Networks, Information Terminals, Information Centres, Informatization, Networking, Industrial Information, Industrial Communication |

Acknowledgements

We thank insightful comments from the editors and reviewers.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We acknowledge financial support from Shanxi Province Philosophy and Social Sciences Special Project (Grant No. 2024WZ030), National Social Science Fund of China (Grant No. 21&ZD096), Research foundation of Jiangsu Ocean University ‘Haizhou Bay Talents’ Innovation Program Project (PD2025015).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.