Abstract

This study explores the effect of R&D expenditure on firms’ exports and examines whether the CEO’s foreign experience moderates the nexus. Employing a large sample of 1,206 listed companies in China from 2012 to 2021, this study applies the fixed-effect panel regression to validate the relationship between R&D expenditure and the proportion of foreign sales to total sales. Further, the results are also checked for robustness using 2SLS instrumental variables (IV) and propensity score matching (PSM) to control endogeneity. Panel regression results reveal a significant effect of R&D expenditure on firms’ exports following the competitive advantage theory. The findings also show that CEOs with foreign experience can strengthen the competitiveness of Chinese firms in foreign sales, which supports the resource-based view. The heterogeneity test shows that R&D significantly improves the firm exports of non-state-owned, eastern region, and processing trade companies, due to policy pressures, locational advantages, and global value chain differences. The findings bear significant implications for policymakers, investors, and corporations endeavoring to comprehend the importance of innovation and human capital in international markets.

Introduction

In 2010, China became the world’s second-largest economy (Leung, 2011), making China’s development attractive to the world. However, the initial emphasis of Chinese firms on penetrating international markets is cost advantage due to inexpensive labor (K. Li & Song, 2011; Sun et al., 2021). Most firms in China adopt a low-price strategy (Ouyang et al., 2015; B. Yang, Liu, et al., 2022) in commissioned processing and assembly, and hence, China is known as the “world factory” with labor-intensive products and modest innovation capabilities (H. Yang, Zhao, & Cai, 2022; X. Zhang et al., 2016). Thus, China’s success in becoming a leading exporter is primarily due to its abundant, low-cost labor supply, not its innovation and independent research capabilities (Huang et al., 2021). The decline in exports became the factor that significantly impacted China’s Gross Domestic Product (GDP) growth (Iqbal et al., 2023). S. J. Wei et al. (2017) suggest that while cyclical factors contribute to the decline, structural and competitive causes are also significant.

Research and development (hereafter R&D) activities boost firms’ competitive advantage (Bleaney & Wakelin, 2002; Penner-Hahn & Shaver, 2005) As Y. Li et al. (2022) argues, while leveraging on low labor costs, Chinese firms increase their R&D expenditures to bolster technical competitiveness and facilitate the local production of pivotal components. At the same time, the Chinese government has taken measures to encourage companies to enhance international competitiveness, for example, intellectual property protection (H. Deng et al., 2019), tax incentives (Chen & Yang, 2019), and industry-university-research co-operation (Cui & Li, 2022). In 2021, as shown in Figure 1, China’s National R&D Funds amounted to 2.7864 trillion yuan, equivalent to 2.44% of GDP, a significant increase compared to 2016.

National R&D funds and input intensity from 2016 to 2021 of China

Although the significance of R&D expenditure in shaping corporate export behavior has been extensively documented in the literature (Azar & Ciabuschi, 2017; Barrios et al., 2003; Caldera, 2010). However, there is controversy in the results of existing studies, and related heterogeneity analyses have seldom been addressed (Dai et al., 2020; Inui et al., 2017; Roper & Love, 2002; D. Zhang et al., 2018). Given the limited empirical evidence and heterogeneity analysis, as well as the lack of consensus on the impact of R&D expenditure on corporate exports (Z. Deng et al., 2014; Kafouros et al., 2008), the first objective of this research is to investigate the impact of R&D expenditure on the exports of Chinese firms and exams heterogeneity for firm ownership, location, and trade mode.

Chinese enterprises face new hurdles in exporting their products due to lack of knowledge about local regulations and inexperience in international brand management (L. Wang et al., 2021). The outsider disadvantage caused by information asymmetry and cultural barriers has also become increasingly prominent in Chinese firms’ exports (Jia et al., 2020; Y. Li et al., 2022). Managers with foreign experience have become an essential human resource for Chinese firms (Cooke et al., 2020; Warner, 2020). As a result, Chinese firms increasingly employ professionals with foreign education degrees to assist their exports (M. Guo et al., 2019).

Some studies suggest that foreign experience is a vital resource that helps firms overcome difficulties and obstacles (e.g., multilingualism and customs) in internationalization (e.g., Buckley et al., 2016; Chandra et al., 2020). Conversely, some scholars believe that senior managers’ foreign experience may negatively impact their inability to adapt to localized management practices in China (Rui et al., 2017). Thus, the second objective of this study is to examine the moderating influence of CEO foreign experience on the relationship between R&D expenditure and firms’ exports.

In view of the above, employing a sample of Chinese non-financial listed firms from 2012 to 2021, this study applies Fixed Effects Model (FEM) and Two-Stage-Least-Squares (2SLS) estimation techniques to investigate the influence of R&D on firm exports. Furthermore, this study further explores whether the R&D expenditure–export nexus is moderated by CEO’s foreign experience. In particular, heterogeneity is examined for firm ownership, location, and trade mode.

This study contributes to the existing literature and body of knowledge in the following respects. First, this study extends the theoretical literature by suggesting whether R&D expenditure affects firms’ exports. The result of this study deepens our comprehension of the technological innovation dimension that influences export performance in developing economies. Further, we test the heterogeneity of enterprise ownership, location, and trade mode to conduct a comprehensive exploration of the influence of R&D on firm exports. Second, compared to preceding studies that predominantly examined the influence of innovation on exports (Azar & Ciabuschi, 2017; Bıçakcıoğlu-Peynirci et al., 2020), this study contributes to the ongoing debate by investigating the moderating impact of CEO foreign experience on the relationship between R&D and firms’ exports. A detailed exploration of this moderating mechanism is instrumental in enhancing our comprehensive understanding of corporate behavior, shedding light on why certain companies exhibit distinct behaviors in the face of decisions related to innovation and exports. The result suggests that CEO foreign experience is a critical resource that enhances the positive impact of R&D expenditure on firms’ exports in a competitive environment. Finally, this study contributes by focusing on the Chinese business context. Given China’s unique position in the global economy, this research provides crucial insights for understanding the internationalization strategies of Chinese enterprises. The study helps to inform the policy of overseas executive talent acquisition in developing countries and enriches the research on the factors influencing firms’ overseas strategy.

The structure of this paper consists of the following: Section “Literature Review and Research Hypotheses” reviews relevant literature and develops the hypotheses. Section “Research Methodology” presents the variable design, models, and econometric models. Section “Empirical Results and Analysis” describes the empirical findings of this study. Section “Discussion” and “Conclusion” discuss the research results and provide the conclusions.

Literature Review and Research Hypotheses

The Nexus Between R&D Expenditure and Firms’ Exports

As international competition and globalization continue to rise, experts, and politicians worldwide stress the need for technological advancement to maintain export competitiveness (Archibugi & Michie, 1997). R&D promotes the expansion and application of technology, which can ultimately contribute to higher productivity (Melitz et al., 2007). Higher productivity improves the ability to enter new international markets and increase export market share (Krugman, 1979, 1991, 1995; Porter, 1990). Technologies enable innovative firms to enhance their processes and product quality to achieve a higher demand curve in foreign markets (Roper & Love, 2002). According to Welford et al. (1993), improved product quality, material efficiency, lower risk, reduced insurance premiums, and cheaper financing costs are significant components of competitive advantage. A productive firm can organize its export activities and adapt to the shifts in the global market, thus promoting export sales (Guan & Ma, 2003; Rodil et al., 2016; Wu et al., 2021). Better productivity can be achieved through innovation, lower production costs, and the introduction of quality goods and services (Yi et al., 2013). Productivity and economic growth rates are related to competitiveness (Schmookler, 1966; Segerstrom, 1991).

The Competitive Advantage Theory portrays the ability to attain a competitive edge and acquire new knowledge or capabilities (Furrer, 2008; Hoskisson et al., 1999). A competitive advantage is achieved when an organization develops or acquires a set of attributes (or performs actions) that enable it to surpass its competitors (H. L. Wang, 2014). A firm’s competitiveness can be strengthened through innovation, which can be advantageous in international markets (Dong et al., 2022). Innovation resources are critical to avoid damaging prices and vicious competition (Mendi & Costamagna, 2017; L. Xu et al., 2024) and are also essential to continued existence (Chatzoglou & Chatzoudes, 2018; Kirbach & Schmiedeberg, 2008). Firms with more R&D projects can operate the export market following high innovation (Aw et al., 2007, 2011). Thus, firm innovation may be related to the necessity to export (Grossman & Helpman, 1990; Krugman, 1979, 1991, 1995; Porter, 1990; Suarez-Villa & Fischer, 1995) and better adaptation to environmental uncertainty (Golovko & Valentini, 2011).

Firms can quickly recover R&D costs from exports and gain better profits from innovative products (Kotabe et al., 2002). This view is supported by most research examining the correlation between innovation and export growth (Ayllón & Radicic, 2019; Cassiman & Golovko, 2011). Innovative firms are found to be more likely to export than non-innovative firms of the same size (Wakelin, 1998). Similarly, Franko (1989) found inventive businesses are more likely to rush into international markets to improve or preserve profits.

According to a study on the connection between R&D expenditure and exports, an increase in a company’s R&D spending in 1 year is associated with a rise in exports the following year. It has been argued that an organization’s export growth is directly correlated with the R&D expenditure it makes in its business (Carboni & Medda, 2018). Amin and Thrift (1995) and Lall (1985) believe that R&D capabilities help export growth, whereas Dhanaraj and Beamish (2003) show a positive relationship between R&D expenditure and international market return. R&D expenditure creates a unique competitive advantage for the company. Thus, this study provides the following hypothesis.

Hypothesis 1: R&D expenditure positively affects the exports of Chinese firms.

The Moderating Effect of CEO’s Foreign Experience on the Nexus Between R&D Expenditure and Firm Exports

The Resource-Based View (RBV) posits that firm-specific resources and capabilities are fundamental to achieving and sustaining competitive advantage (Barney, 1991). Within this framework, CEO foreign experience is considered a critical resource (Le & Kroll, 2017). CEOs with foreign experience bring unique skills, knowledge, and networks that can enhance a firm’s strategic orientation and international competitiveness (Le & Kroll, 2017; L. Q. Wei & Ling, 2015). Their exposure to diverse markets and business practices equips them with a broader perspective and an ability to navigate complex international environments (Conyon et al., 2019).

Empirical evidence suggests that CEOs with foreign experience are better equipped to identify and exploit global opportunities, thereby facilitating firms’ entry and success in foreign markets (Criaco et al., 2022). Tihanyi et al. (2000) also found that CEO’s education level and foreign experience closely relate to the firms’ exports. Thus, understanding the link between R&D expenditure and firm exports is greatly helped by considering the CEO’s foreign experience (W. T. Hsu et al., 2013). Social networks are crucial resources that firms need in export activities (W. T. Hsu et al., 2013; Morgan et al., 2018; Rabbiosi et al., 2019). CEOs with foreign experience can tap into their formal or informal network in foreign markets (P. Y. Li, 2018). Executives with foreign experience can enhance human capital resources, prompting firms to make export decisions (Cerrato & Piva, 2012). Managers with cross-cultural knowledge effectively navigate language and cultural barriers (Selvarajah et al., 2019), enabling firms to accurately identify and capitalize on international market opportunities (Miocevic & Morgan, 2018). Foreign experience can help cultivate new international business relationships, leveraging external knowledge resources, even when they lack specific market partnerships (Miocevic & Morgan, 2018). Moreover, a competent CEO is a critical success factor in avoiding wasteful investment that can impede development (Müller & Zimmermann, 2009; Santarelli & Sterlacchini, 1990).

In summary, CEO’s foreign experience enhances a company’s international perspective and strategic advantage. Based on the resource-based view, this study examines whether the CEO’s foreign experience moderates the relationship between R&D expenditure and firms’ exports. Thus, this study provides the following hypothesis.

Hypothesis 2: CEO’s Foreign Experience positively moderates the relationship between R&D expenditure and the exports of Chinese firms.

Research Methodology

Data Sources

From 2012, the 12th Five-Year Plan (2011–2015) placed a strong emphasis on innovation and technology development. This period marked the beginning of increased government support and funding for R&D activities, making it a relevant starting point for research. Hence, this study uses the data of A-share listed companies in China for 2012 to 2021 as the sample. All initial data are obtained from the CSMAR and WIND database. Following J. Xu et al. (2021), first, we remove financial institutions that are not related to R&D investments. Second, in accordance with guidelines from the China Securities Regulatory Commission (CSRC), companies recording net losses for two consecutive years are categorized as special treatment (ST) companies, and those with losses for three consecutive years are denoted as *ST companies, facing potential delisting after another year of losses. Consequently, ST and *ST companies are excluded from the sample, which means the listed companies have abnormal financial conditions. Finally, it disregards certain listed companies lacking complete or accessible data. The ultimate sample for this study consists of 1,206 companies with 11,971 firm-year observations during the 10 years from 2012 to 2021.

Selection of Variables

The dependent variable in this study is firm exports (FSTS). In line with previous studies (Berman et al., 2015; Sharma et al., 2020), we identify firm export as the ratio of foreign sales to total sales. Building upon the studies of Vithessonthi and Racela (2016) and Moradi et al. (2019), R&D expenditure (RDTA) as the independent variable is defined as the ratio of R&D expenditures to total assets. Existing studies have not adequately considered the impact of top executives’ background factors, especially their foreign experience, on firm exports (Oura et al., 2016; Ramón-Llorens et al., 2017). Therefore, this study introduces CEO foreign experience as a moderating variable to explore whether it enhances or attenuates the impact of national ownership on firm exports, thus filling a gap in the relevant literature. Following Le and Kroll (2017), this study adopts a dummy variable to represent CEO foreign experience (FOREIGN). One is assigned if the CEO has studied or worked overseas, and zero otherwise.

Following previous literature as empirical specifications, this study incorporates firm size (SIZE), leverage (LEV), gross profit margin (GPM), firm performance (ROA), and firm age (AGE) to control for firm characteristics that might create a competitive advantage to drive foreign sales (Kling & Weitzel, 2011). Firm size (SIZE) is crucial when choosing an export strategy (Zapletalová, 2015), and large companies have the advantage of resources and are more resilient to risk (Kumar et al., 2020). Highly leveraged enterprises have more severe financial constraints, which may limit their willingness to take risks and access international markets (Aivazian et al., 2005). Companies with high gross profit margins typically produce lower-cost goods or compete in less-saturated marketplaces. Low-profit companies may have higher production costs or operate in less favored product marketplaces (Abor, 2007). Return on assets (ROA) measures how effectively the assets are used, which might affect firms’ exports (C. Hsu & Boggs, 2003). Although older firms may benefit from the accumulation of assets (B. J. Liu, 2017), they may face the challenge of organizational inertia and, therefore, cannot adapt to new markets and technologies (Zahra et al., 2000). This study mitigates the simultaneity bias and endogeneity issues with a lag structure of variables (Aitken & Harrison, 1999). Except for Firm Age (AGE), all variables of firm characteristics are lagged by 1 year to minimize estimation biases that firms’ exports might affect their characteristics.

In addition to firm characteristics, internal corporate governance mechanisms can also favor export performance (Bilgin et al., 2017). Thus, this study controls the ratio of independent directors to board size (BIND) and the percentage of control owned by the beneficial owner minus the percentage of ownership owned by the beneficial owner (OWN; Lozano et al., 2016). This study also controls foreign exchange rates (EXRA), which can deter firms from entering a competitive foreign market due to exchange rate uncertainty (Lin & Chen, 2022). During the Renminbi (RMB) appreciation period, exports decreased significantly, with exporters facing more competitive pressure (Dai et al., 2018). Furthermore, macroeconomic shocks and individual factors were accounted for using time and firm-specific dummy variables. The definitions of these variables are summarized in Table 1.

Definition and Description of Variables.

Note. The table provides brief definitions of the main variables used in the study.

Model Specification

R&D expenditure can enhance enterprise innovation, thereby enhancing competitiveness through innovation, lowering production costs, and introducing quality goods and services. Thus, this study uses the following equation to examine the effect of R&D expenditure on firms’ exports.

Where FSTS is the ratio of foreign sales to total sales. RDTA is equal to the ratio of R&D expenditures to total assets. SIZE is the natural logarithm of actual total assets in millions of RMB. LEV is the ratio of total debt to total assets. Gross Profit Margin (GPM) is the ratio of gross profit to total sales. ROA is the ratio of EBIT to total assets. AGE is defined as the length of time that has passed since a firm was founded. The ratio of Independent Directors to board size is the proxy of a corporate’s governance. OWN is the percentage of control owned by the beneficial owner minus the percentage of ownership owned by the beneficial owner. The

The following equation is used to examine further the moderating effect of a CEO’s foreign experience on the nexus between R&D expenditure and firms’ exports.

The interaction term assesses whether the CEO’s foreign experience affects the relationship between R&D expenditure and firms’ exports. The dummy variable

The models are regressed using pooled ordinary least square (pooled OLS) estimation before considering cross-sectional or temporal differences. The F-test, the Breusch and Pagan Lagrangian Multiplier (LM) test, and Hausman’s test are performed for each individual proposed model to determine the most appropriate method of regression analysis.

Empirical Results and Analysis

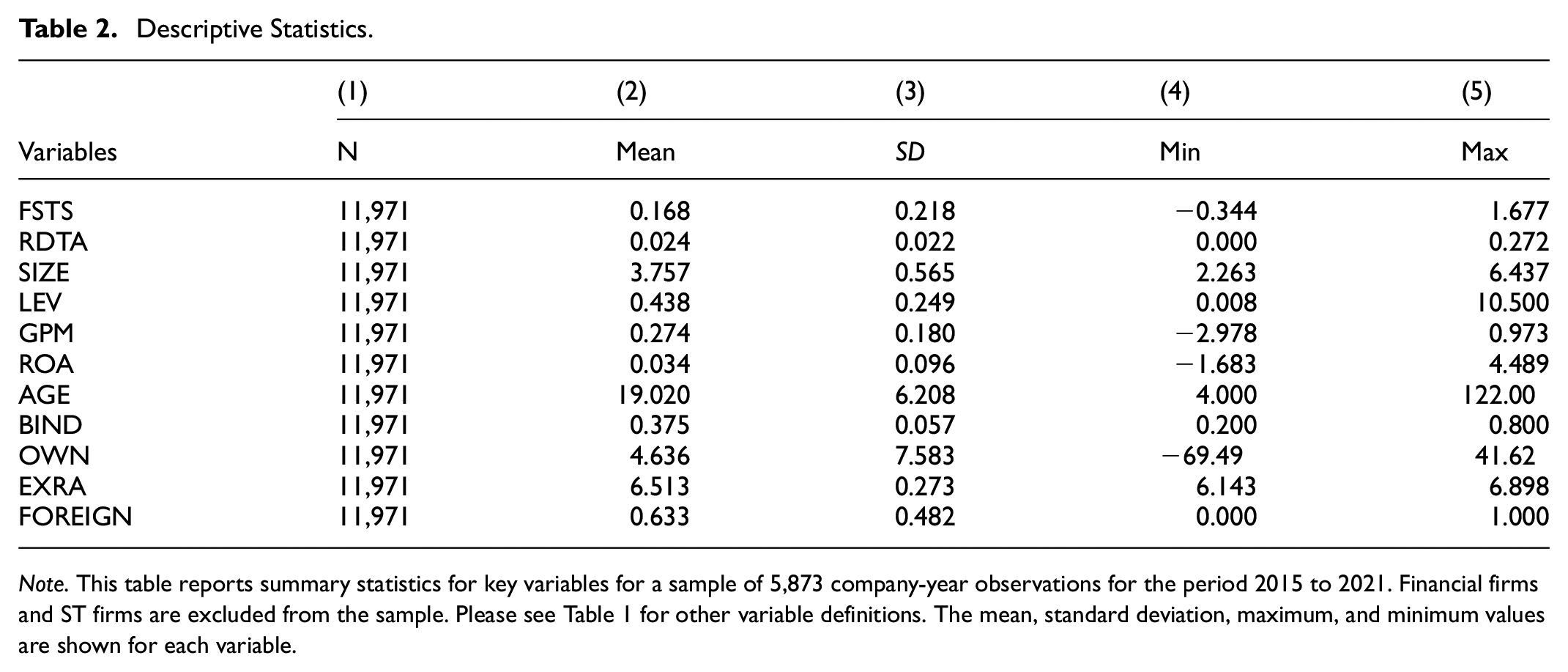

Descriptive Statistics

Table 2 shows the mean of FSTS is 16.8%, with a standard deviation of 21.8%. The high deviation among export levels among enterprises suggests a divergence that may stem from the diverse business strategic choices made by these firms. The RDTA exhibits notable heterogeneity across companies, with a maximum value of 0.272 and a minimum value of 0.000, which means that R&D expenditure varies dramatically. The mean ROA was 3.4%, indicating that firms exporting from China have weaker profitability on average. That shows most Chinese products were still at the lower end of the global value chain, lacking competition, and bargaining power. The average age of Chinese listed companies was 23 years old, indicating that Chinese listed companies started late and may have the problem of insufficient resources and experience in internationalization.

Descriptive Statistics.

Note. This table reports summary statistics for key variables for a sample of 5,873 company-year observations for the period 2015 to 2021. Financial firms and ST firms are excluded from the sample. Please see Table 1 for other variable definitions. The mean, standard deviation, maximum, and minimum values are shown for each variable.

Table 3 reports correlations for the variables used in the analysis. The correlation coefficients are relatively minor (less than .5). The mean VIF is 1.21, and the minimum and maximum values of VIF are 1.02 and 1.62, respectively. The VIF of all the variables is significantly below the acceptable threshold of 5, as G. James et al. (2013) suggested. Hence, the dataset has no concerns of multicollinearity (Callen & Fang, 2013).

Correlation Matrix.

Note. This table reports the correlation coefficients between key variables for 11,971 company-year observations covering 2012 to 2021. Please see Table 1 for other variable definitions.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Analysis of Regression Results

Table 4 presents the empirical results of the two hypotheses formulated for our study. Model 1 reports results from estimating Equation 1 using an ordinary least squares (OLS) regression. Results support the hypothesis that R&D expenditure increases the firms’ exports. However, F-test results indicated that Fixed-Effects Panel Regression analysis is more appropriate than ordinary Pooled-Ordinary Least Squares (OLS) regression analysis. The null hypothesis of the Breusch and Pagan Lagrangian Multiplier (LM) test is rejected, indicating that a Random-Effects Panel Regression analysis is more appropriate than the standard OLS regression analysis. Model 2 repeats the estimation using Random-Effects Panel Regression. The null hypothesis in the Hausman test is rejected, indicating that the Fixed-Effects Panel Regression is more appropriate (Greene, 2005).

Regression Results of R&D Expenditure on Exports and the Moderating Effect of CEOs’ Foreign Experience.

Note. RDTA × FOREIGN is the moderating effect of the CEO foreign experience. Industry and year fixed effects are included in all regressions. Robust standard errors grouped at the firm level is reported in parentheses. Please see Table 1 for other variable definitions.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Models 3 and 4 are the results of the Fixed-Effects Panel Regression analysis. Model 3 shows that R&D expenditure is significant at the 1% level. The positive coefficient of 0.920 implies that for one standard deviation increase in R&D expenditure to total assets, the firms’ foreign sales to total sales rise by 8.43% ceteris paribus. The result supports Hypothesis 1, which is that R&D expenditure can boost firms’ exports by strengthening international competitiveness. The competitive advantage theory (F. Wang, 2014) demonstrates that increased in R&D expenditure is a compelling strategic choice for firms seeking international competitive advantage. It is consistent with prior studies that emphasize the critical role of R&D expenditure in the long-term competitiveness of firms (Ayllón & Radicic, 2019; Bleaney & Wakelin, 2002; Cassiman & Golovko, 2011; Penner-Hahn & Shaver, 2005). Similarly, it is argued that innovation can generate or maintain a competitive advantage (Dereli, 2015; Yu et al., 2017), and technological innovation strategies significantly impact firms’ exports (Becker & Egger, 2013; Edeh et al., 2020).

Model 4 shows that the interaction term (RDTA × FOREIGN) is significant at a 1% level. The positive coefficient supports Hypothesis 2, indicating that foreign experience enhances the positive effect of R&D expenditure on firms’ exports. The result proves that executives with foreign experience might have network resources or the ability to handle complex business overseas, which benefited the firms’ exports (Carpenter & Fredrickson, 2001). It is argued that CEOs with foreign experience have more resources under intense international competition, including broader international social networks (Suutari & Mäkelä, 2007), deep cross-cultural knowledge (Black & Duhon, 2006), and richer business insights (Quan et al., 2021). These resources endow them with stronger strategic tools that help firms to better cope with the challenges of the international market (Quan et al., 2021). CEOs with foreign experience, being a strategic resource, can bring unique competitive advantages to the company from the perspective of Resource-Based View (Kraaijenbrink et al., 2010).

Some corporations may avoid expanding into foreign markets due to additional export costs (Chang & Rhee, 2011) and higher business risk (Gulamhussen et al., 2014). Firm size (SIZE) is negatively linked to firms’ exports, suggesting that smaller businesses are more agile in penetrating international markets than their bigger counterparts (Zapletalová, 2015). International markets increase corporate risks (Kwok & Reeb, 2000), and the negative association between leverage and foreign sales suggests that companies with higher debt ratios are hesitant to expand into these markets for fear of going bankrupt (Chen & Zhao, 2007). Moreover, coordination and oversight issues may exist in internationally expanding enterprises (Boeh & Beamish, 2012) and higher liability of foreignness (Johanson & Vahlne, 2009; Zaheer, 1995). A smaller gross profit margin is associated with more foreign sales, indicating that Chinese firms focus on a lower price strategy for conquering international markets (Ouyang et al., 2015). Firm age (AGE) is negatively associated with firms’ exports, indicating that older firms are more likely to experience organizational inertia, making it more challenging to adapt to complex and changing international markets (Zahra et al., 2000). In contrast, board independence (BIND) positively correlates with the firms’ exports, suggesting that good corporate governance leads to better exports.

Endogeneity Test

Results of Two-Stage-Least-Squares (2SLS)

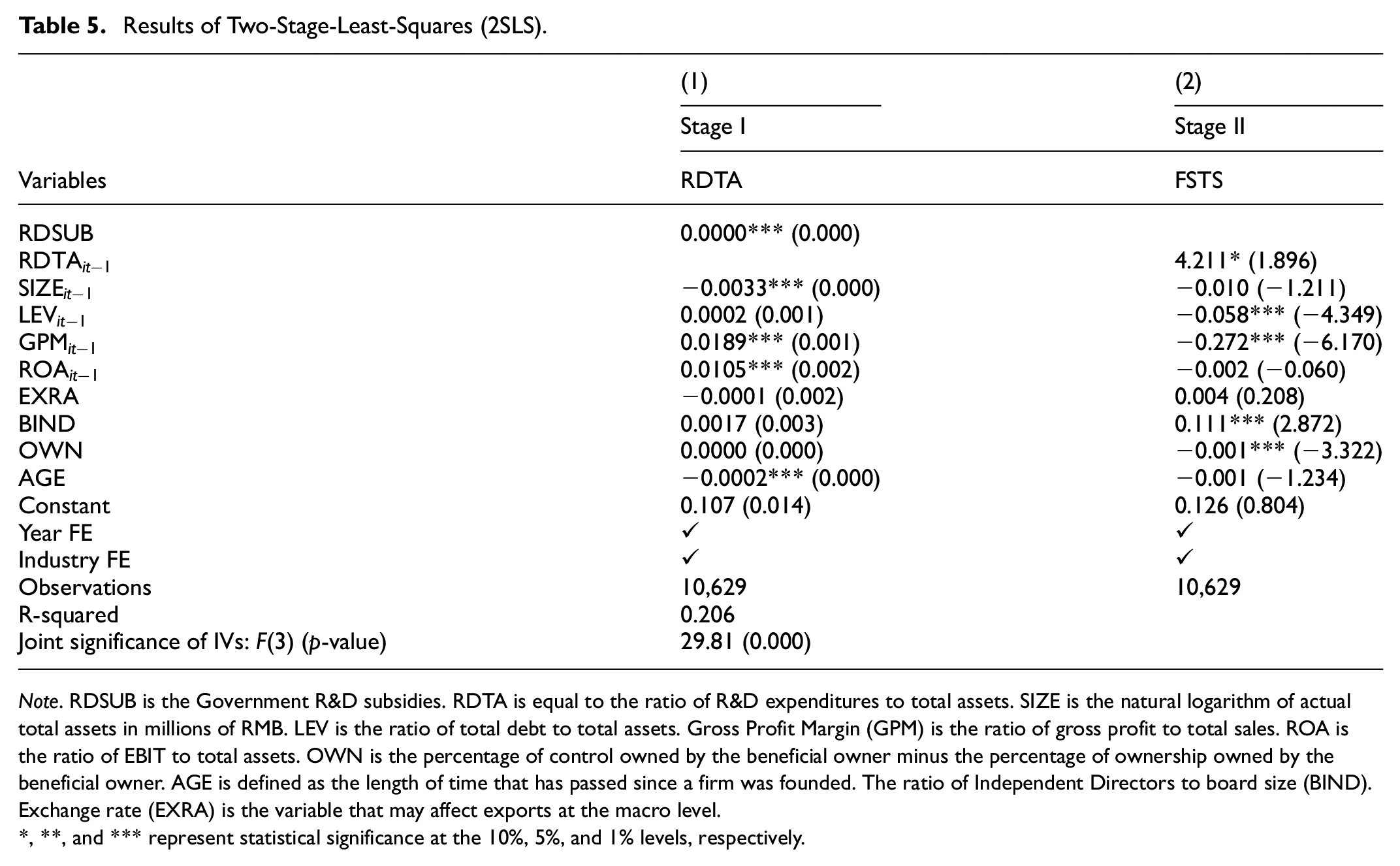

The main challenge in estimating exports is the endogeneity of R&D attainment, which is subject to self-selection, ability bias, and measurement errors (Esteve-Pérez & Rodríguez, 2013). Government R&D subsidies are typically allocated based on policy objectives and criteria, rather than the specific characteristics and short-term performance of individual firms (Boeing, 2016). Consequently, Government R&D subsidies is considered exogenous, as it is not correlated with unobserved firm characteristics (i.e., it is uncorrelated with the error term). Furthermore, government R&D subsidies have a direct impact on firms’ R&D expenditures, establishing a strong correlation between government R&D subsidies and R&D spending (D. Guo et al., 2016; X. Liu et al., 2016). Therefore, this study adopts the 2SLS method and exploits the government R&D subsidies (RDSUB) as a source of exogenous variation in R&D expenditure to generate an instrumental variable and conduct a regression using Two-Stage-Least-Squares (2SLS). As indicated in the first column of Table 5, the coefficient of the Government R&D subsidies is positively correlated with R&D expenditure at 1% significance. Regarding the explanatory power of the instrumental variable, the F value is 29.81 (p = .000), rejecting the null hypothesis that “the instrumental variable has no explanatory power.” The problem of weak instrumental variables is not severe. The results in the second column indicate that the coefficient of R&D is significantly positive at the 10% significance level, which is consistent with the results in Table 3.

Results of Two-Stage-Least-Squares (2SLS).

Note. RDSUB is the Government R&D subsidies. RDTA is equal to the ratio of R&D expenditures to total assets. SIZE is the natural logarithm of actual total assets in millions of RMB. LEV is the ratio of total debt to total assets. Gross Profit Margin (GPM) is the ratio of gross profit to total sales. ROA is the ratio of EBIT to total assets. OWN is the percentage of control owned by the beneficial owner minus the percentage of ownership owned by the beneficial owner. AGE is defined as the length of time that has passed since a firm was founded. The ratio of Independent Directors to board size (BIND). Exchange rate (EXRA) is the variable that may affect exports at the macro level.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Robustness Test

Testing Robustness Using Output Value of the New Products as a Dependent Variable

Following the literature (Coad & Rao, 2010; Wignaraja, 2012), we consider the ratio of R&D-to-Sales (RORS) of the firm as R&D expenditure for checking robustness. Because it directly reflects the a demonstration of the firm’s R&D expenditure (Wignaraja, 2012). This data come from the CSMAR database. The results stated in Table 6 support the prior findings reported in Table 3, indicating that R&D expenditure positively affect firm exports, and CEO’s Foreign Experience also positively moderates the relationship between R&D expenditure and the export. The findings of the control variables likewise persist, confirming that our results are unaffected by a different R&D proxy.

Robustness Test Alternative Proxy for R&D.

Note. OVNP is the output value of the new products of the firm. OVNP × FOREIGN is the moderating effect of the CEO foreign experience. Industry and year fixed effects are included in all regressions. Please see Table 3 for other variable definitions.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Testing Robustness Using Propensity Score Matching

To further address the potential endogeneity issues arising from selection bias related to firm-specific characteristics, this study employs a widely used technique—propensity score matching (PSM; Sarang et al., 2021, 2024). This paper utilizes PSM to mitigate the impact of selection bias on the regression results. Firms with R&D expenditure above the mean were designated as the treatment group, while the remaining firms constituted the control group. The matching process employed a 1:1 matching ratio, with the control variables serving as the matching covariates and the nearest neighbor matching method being applied (Table 7).

Propensity Score Matching Test.

Note. Please see Table 3 for other variable definitions.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels.

To examine whether the differences in firm exports are driven by R&D expenditure, we re-estimated the matched sample presented in Columns 3 to 4 of Table 4. Subsequently, we matched the treatment and control groups based on the explanatory variables in Equation 1 to ensure a high degree of similarity between the two groups. We found that the coefficient for R&D was positive and significant. These results are consistent with our baseline findings, indicating that increased R&D expenditure tends to enhance firm export performance. The results ensuring the quality of PSM are reported in Table 8 and 9. These findings suggest that the treatment and control groups are comparable in terms of firm-level factors, as there are no significant differences in the control variables between the two groups. As shown in Figure 2, it is evident that the two groups are better matched after the PSM.

Student’s t-Test.

Balance Test of PSM.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels.

Standardized deviation of each variable.

Heterogeneity Analysis

Following the benchmark regression, this study examines the impact of R&D on firms’ exports from the perspectives of ownership type (state-owned, private, foreign-owned enterprises), geographical location (eastern, central, western regions), and trade mode (ordinary trade and processing trade).

The sample companies are categorized into state-owned and non-state-owned firms based on whether state ownership exceeds 50%. Additionally, we adhere to the classification established by the National Statistical Bureau of China in 2003, which considers economic development and geographical factors, resulting in the division of mainland China into three economic zones: eastern, central, and western (Nie et al., 2019). Furthermore, these companies are segmented according to their trade mode (primary business) into trading companies and processing companies (Fang et al., 2014).

Table 10 presents the test results for the impact of R&D on firm exports in different ownership enterprises in columns (1) and (2). The regression outcomes indicate that the influence of R&D expenditure on exports is significantly more pronounced in non-state-owned enterprises than in state-owned enterprises. This result substantiates the findings of G. Hu and Yue (2021) and Fang et al. (2014), highlighting that the impact of R&D is more significant for non-state-owned enterprises in China. This distinction arises because Chinese state-owned enterprises have closer ties with the government, and their investment motivations align with government intentions rather than purely economic objectives (Zang & Jiang, 2020). Consequently, their export motivations are contingent on government intentions, and the opportunities to acquire technology through R&D spending are limited, factors that are not conducive to enhancing export activities. In contrast, non-state-owned enterprises prioritize economic benefits in their R&D investments, demonstrating higher capabilities for imitation, learning, absorption, and transformation (L. Li et al., 2017; B. Wang et al., 2022). As a result, R&D spending has a more pronounced impact on improving exports. This suggests that non-state-owned enterprises in China exhibit higher innovation effectiveness and dynamism compared to state-owned enterprises. R&D plays a crucial role in elevating the technological prowess of non-state-owned enterprises, thereby driving export growth. This finding aligns with the results of the study by W. Liu and Huang (2018).

Heterogeneity Test Results.

Note. Please see Table 1 for other variable definitions.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Columns (3) and (4) present the results of the heterogeneity analysis based on the geographical location of firms. The impact of R&D expenditure on enhancing firms’ exports is more pronounced in enterprises located in the eastern region compared to those in the central and western regions. This disparity can be attributed to the advantages that the eastern region holds in economic development, market systems, human capital, and R&D investments. Additionally, the proximity of the eastern region to coastal cities facilitates greater access and interaction with international markets. This heightened sensitivity to global market demands prompts eastern enterprises to better align with international requirements by augmenting R&D investments. These findings are consistent with established R&D practices and policies in China (Lin & Qin, 2022).

Lastly, columns (5) and (6) reveal the test outcomes for companies engaged in different trade modes. The regression coefficient for processing trade surpasses that of ordinary trade. 1 This divergence is attributed to the fact that companies involved in processing trade in China often occupy the lower end of the global value chain, necessitating more technological support to increase value addition. By increasing R&D expenditure, these enterprises can introduce more advanced technologies and production methods, thereby enhancing product quality and technological sophistication (X. Xu, Xia, & Li, 2017). Consequently, the competitive advantages generated by R&D have a more pronounced impact on firms’ exports in enterprises engaged in processing trade. This conclusion finds support in the studies conducted by J. Zhang et al. (2020) and Peng and Zhang (2022).

Discussion

By fostering innovation, enhancing capabilities, and enabling the creation of unique value propositions, R&D expenditure equips firms with the necessary tools to succeed in market competitions (Rajapathirana & Hui, 2018). R&D expenditure is a key driver of innovation, leading to the development of new products, processes, and technologies that enhance a firm’s competitiveness (Akinwale et al., 2017; Ciocanel & Pavelescu, 2015). By investing in R&D, firms can create unique products that meet the specific needs of foreign markets, thus differentiating themselves from competitors (W. Liu & Atuahene-Gima, 2018; Papanastassiou et al., 2020). This differentiation provides a competitive advantage that can translate into increased export performance (Tan & Sousa, 2015). Thus, R&D expenditure can be seen as enhancing innovation capabilities while expanding the competitive advantage of its products or services in international markets. The finding also strongly confirms Edeh et al. (2020) that innovation, as a crucial source of competitive advantage for businesses, positively impacts firms’ exports and prompts them to pursue an international strategy through export activities.

However, the efficacy of R&D investments in driving export performance may be contingent upon complementary managerial resources, such as the foreign experience of the CEO. CEOs with substantial international exposure bring a wealth of knowledge and insights from diverse markets, enabling them to steer R&D efforts in directions that align with global trends and demands (Heyden et al., 2017). Their understanding of international market dynamics, regulatory environments, and consumer preferences can significantly enhance the effectiveness of R&D investments, translating into superior export performance (Arunachalam et al., 2022). This aligns with Ying et al.’s (2019) view that the managerial resources of a firm, including the expertise and background of its top executives, are critical determinants of its growth and competitive positioning.

The integration of the CEO foreign experience into the firm’s strategic framework serves as a crucial moderating factor (Le & Kroll, 2017). It not only compensates for potential gaps in market knowledge but also amplifies the impact of R&D activities by aligning them with international standards and opportunities (Mostafiz et al., 2023). Our findings highlights that a dynamic interplay where the foreign experience acts as a catalyst, transforming R&D investments into tangible competitive advantages in export markets. The alignment between R&D expenditure and CEO foreign experience exemplifies a strategic fit that enhances the firm’s ability to navigate and succeed in complex international markets. This synergy between competitive advantages and resource allocation is crucial for achieving sustained competitive advantage.

Our results of heterogeneity analysis also open up intriguing questions about the potential limits of such complementarities. The R&D have higher quality improvement effects on firm exports in the eastern region than in the central and western regions, and on processing trade firms than on ordinary trade firms. This aligns with the policy of the State Council of China, which released guiding opinions aimed at advancing innovative trade development (S. J. Wei et al., 2017). These results acknowledge the challenges posed by different factors that Chinese firms face in their pursuit of innovation, considering industry and regional variations along with the uncertainties in institutional frameworks (K. Wang & Jiang, 2021; Yi et al., 2017). It serves as a comprehensive response to the unique heterogeneous characterizing Chinese exports, where dominance in processing trade, active participation of non-state-owned enterprises, and a heightened proclivity for enterprises in the eastern region to engage with international markets are notable features.

Conclusion

This study explores the impact of R&D expenditure on firms’ exports and examines whether the CEO’s foreign experience moderates the nexus, and performs heterogeneity tests for different types of firms. The findings indicate that R&D expenditure positively impacts firms’ exports by enhancing firms’ competitiveness. CEO foreign experience significantly enhances the positive impact of R&D expenditure on firm export performance by leveraging international insights and networks to better navigate and penetrate global markets. The findings also reveal that the impact of R&D is more pronounced in enhancing the exports of non-state-owned enterprises compared to their state-owned counterparts. The R&D have higher quality improvement effects on firm exports in the eastern region than in the central and western regions, and on processing trade firms than on ordinary trade firms. That means policy pressures, locational advantages, and global value chain differences significantly impact the effectiveness of R&D expenditure.

This study provides a novel perspective on understanding the critical role of R&D investment and CEO foreign experience in enhancing firm export performance and hold significant implications for government policymakers, corporate managers, and investors. First, policymakers should prioritize policies such as tax incentives, grants, and subsidies to incentivize R&D investment as a key driver of export performance. Such measures would encourage firms to innovate, leading to the development of competitive products and services that can succeed in international markets. Secondly, businesses need to leverage the international vision and experience of their CEOs to formulate globalization strategies aligned with corporate development goals, select appropriate market entry modes, and identify expansion pathways. Additionally, they should capitalize on the business networks established by their CEOs abroad to acquire more market information and cooperation opportunities, thereby enhancing their competitiveness in the international market. Firms also should be encouraged to diversify their leadership teams by including executives with foreign experience and resources.

Furthermore, to maximize the benefits of foreign experience, policies should focus on facilitating knowledge transfer and the establishment of international networks. Governments can support initiatives that promote collaboration between domestic firms and international partners, including joint ventures, strategic alliances, and international R&D consortia. These collaborations can provide domestic firms with access to global knowledge, markets, and technologies, thereby enhancing their competitive edge in the export sector. Finally, a heterogeneity analysis of firm ownership structure, firm location, and trade mode is conducted in this study. This segmentation provides a more refined perspective on the differential outcomes of R&D efforts to capture the multifaceted dynamics shaping the impact of R&D across diverse dimensions within the business landscape.

Limitations and Future Directions

Despite the valuable insights provided by our study, several limitations should be acknowledged. First, our analysis primarily relies on data from firms operating in a specific economic context, potentially limiting the generalizability of our findings to different geographical regions or industries with varying regulatory and market conditions. Future research should consider cross-country comparative studies to validate and extend our findings in diverse economic environments.

Second, while we focused on CEO foreign experience as a moderating factor, there are other potentially influential variables, such as the CEO’s educational background, industry experience, and the firm’s internal R&D capabilities, that were not considered in our model. Including these variables may provide a more comprehensive understanding of the dynamics between R&D expenditure and export performance.

Lastly, our study uses a static approach to assess the impact of R&D expenditure on export performance, which might not fully capture the dynamic nature of R&D investments and their long-term effects on firm international competitiveness. Longitudinal studies could offer deeper insights into how sustained R&D investments and evolving CEO experiences influence export outcomes over time.

Footnotes

Acknowledgements

This work was supported by the Ministry of Higher Education Malaysia (MOHE) under the Fundamental Research Grant Scheme (Project Code: FRGS/1/2020/SS01/USM/02/6). We acknowledge the support of School of Management, Universiti Sains Malaysia. Thanks for the joint efforts of the creators and editors.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Ministry of Higher Education Malaysia (MOHE) under the Fundamental Research Grant Scheme (Project Code: FRGS/1/2020/SS01/USM/02/6).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The publications analyzed in this study can be accessed from the publicly available databases using the query provided under the methodology section of this paper. Data will be made available on request.