Abstract

The graduate approach applied in China for the economic transition poses the risk of continued government influence on the market. The land reform and the following adjustment in China have introduced a seemingly complete market for residential land. However, a widely practiced coalition between the local developmental states and developers might impact residential land leasing in a more hidden way. Taking central Chengdu as the study area, this study takes the enterprise ownership and affiliations as two explanatory factors that impact the land leasing prices and builds an MGWR model to evaluate the premium of political connections for the developers to obtain the land. The result gives a clue to the local protectionism and preference for state-owned enterprises that might exist in land leasing in Chengdu. It is proved in this study that the average purchase price by state-owned enterprises is 8.9% lower than the prices that private enterprises could enjoy, and the average land leasing price by local enterprises is 14.2% lower than that enjoyed by non-local enterprises. The preceding conceptual and empirical discussion in this study advocates for a review and rethinking of the public sector’s intervention in China’s land market. In-depth analyses of the factors that define the land leasing behaviors of the local government are needed.

Introduction

The transition from a planned to a market economy is a fundamental social change, and different countries have taken different paths. Unlike the “shock therapy” style that marked the transitions in Russia and other Central and Eastern European countries (Sachs et al., 1994), China’s economic transition has been characterized by its gradualist approach (Xu et al., 2014). Starting in the 1980s, a series of market-oriented transformations were introduced in China to stimulate more economically intensive usage of urban land (Gaubatz, 1999; Leaf, 1998; Tang, 1994; Yeh & Wu, 1999). Prompted by the paid transfer of land use rights and the commodification of housing, dynamic forces to build cities have been generated, shifting dramatically from the former state-led, welfare-provision-oriented pattern to a more market-oriented approach (G. C. S. Lin, 1997; Y. Zhang & Fang, 2004; Zhu, 1999a). The institutional reform was pushed forward in 2002 when the Land Resource Ministry regulated that land for all profitable development (i.e., housing, offices, and commercial buildings) must be leased through auction or tender. A virtuous circle of market-based urban development seems to be reached.

However, although some have assumed that a free market economy is the destination of the transition, the lingering influence of the state may persist (N. Lin, 2011). Coexisting of state-owned enterprises (SOEs) and privately owned enterprises (POEs) does not mean equal opportunities to access land resources in the emerging land market. In a transitional economy, ownership and affiliation are helpful for enterprises to obtain trust and establish a relationship with the local government (G. L. Yang, 2018), resulting in a reduction of transaction cost (Leff, 1978), better material supplies and distribution networks (Luo & Tan, 1998), easier access to financing from state-controlled banks and government bailouts (Buckley et al., 2007; Faccio et al., 2006; Nguyen et al., 2013), or priority access to government grants and tax relief (Shleifer & Vishny, 1994). Existing studies have modeled the factors and mechanisms to define land prices, but seldom realize the possible impacts of political connections of the developers. In fact, the impacts of the political connections indicate the hidden control of the local government in defining the development of a city (F. L. Wu, 2016) and might hurt the efficiency of the urban resource distribution system as most empirical studies support the proposition that SOEs underperform POEs in a transitional economy (Tihanyi et al., 2019). It is worth evaluating the impact of the political connections of the developers to the land market. How do the political connections affect land leasing prices? How are such effects distributed in a city? An in-depth investigation of these questions could be helpful in understanding the logic behind land pricing and evaluating the efficiency of land management in Chinese cities.

By quantifying the political connections of developers and evaluating their impacts on the land leasing payment, this study tries to reveal the hidden intervention of the local government in the land market. This study compares three different models and chooses the Multiscale Geographically Weighted Regression (MGWR) model to map the spatial difference of such impacts. The following sections have been included. Political connections here refer to the real estate enterprise’s ownership and affiliation. Section 2 reviewed the literature about land pricing logic and the spatial-temporal heterogeneity of the impacts of various factors on the land price. Section 3 introduces the study area, the data and the methodologies for analysis. Section 4 presents the results, followed by the discussion and conclusions of the study in Section 5.

Modeling the Impact of Political Connections in Residential Land Leasing in Transitional China

Impacts of Developers’ Political Connections in the Transitional Land Market

Based on neo-classical economics, the market is viewed as the most powerful institution guiding capital circulation and society structuring in a city. Private sectors seek profit maximization in the land market, and would spontaneously allocate land resources most efficiently (Smith, 1776). However, the land market could be highly speculative and unpredictable since there are no substitutable goods and many attributes valued are not subject to formal contracts (Webster & Lai, 2003). The situation may even be complicated for land pricing in a transitional economy. The transitional economy here refers to an economy that has undergone a centrally planned era and is reforming toward market-oriented resource allocation. “The rejection of private ownership of capital and the means of production, including land, has been a central tenet of Marxist ideology” (Bertaud & Renaud, 1997, p. 137). Economic reforms reintroduced the land market and the land price gradients to the transitional economy, but could hardly eliminate government interference.

Especially for countries implementing gradual reforms such as China, institutions are evolving in a path-dependent way (Arthur, 1994; North, 1990), suggesting that lock-in effects and sub-optimal behavior may persist (David, 1994; Hall, 1986). In China, the government still retains ultimate ownership of urban lands, and the local governments play as the direct agents in leasing the land (J. Wu et al., 2012). The forces of decentralization and marketization have endowed Chinese local governments with a strong development impulse, resulting in a much closer relationship between the local government and developers (Zhu, 2004). partnerships of private- and public-sector interests were widely observed and studied as “urban regime,”“growth coalition,” and “developmental state” (Oi, 1996; Zhu, 1999b). Those developers who have a close relationship with the government would generally enjoy priority and discount in obtaining the land. This could be lower land prices in return for public facilities construction or flexible planning control in case of financial problems during the transition (Liu et al., 2019). Most of such developers are either SOEs or locally registered since the ownership and affiliation are helpful for enterprises to obtain trust and establish a relationship with the local government (G. L. Yang, 2018). Such enterprises generally have lower production and operation efficiency (Brandt et al., 2012; Ma et al., 2006), but may work with local governments to achieve specific social goals, such as selling housing at a discount (Monkkonen et al., 2019). SOEs often build on land acquired years ago, often converted from industrial uses that SOEs previously engaged in (X. Yang, 2009). SOE developers might be more likely to build above the Floor Area Ratio (FAR) limits, enabling them to sell units at a lower price without harming their profitability (Cai et al., 2017). Still, much more is left unexplored about the value of the political connections of the developers in land prices.

Modeling the Impact of Political Connection of Developers

Factors to Define Residential Land Prices

As shown in Table 1, locational characteristics are generally regarded as the most important factors that affect residential land prices. The locational characteristics refer to the accessibility of a site and local purchasing power (Benjamin et al., 1990; Gatzlaff et al., 1994; Hardin et al., 2002). A frequently used variable to evaluate the locational advantages is the distance to the city center (Benjamin et al., 1990; Chai et al., 2021; Garang et al., 2021; Jiang et al., 2022; Shen et al., 2022). Besides, the transportation facilities—such as subway stations—provided within a threshold could also indicate the accessibility of a site (Chai et al., 2021; Farber & Yeates, 2006; Kim & Yoon, 2023; Shen et al., 2022; Sisman & Aydinoglu, 2022; Zhou et al., 2022).

Common Factors to Define Residential Land Prices in Literature.

Scholars have also attributed the influence on residential land prices to various econometric variables: services provided within the neighborhoods, expectations of property value change and individual characteristics of land plots (Glumac et al., 2019). Services provided within the neighborhoods mainly highlight the premium of various services nearby to the land prices as services help in attracting people to agglomerate. Such services generally include the agglomeration patterns of commercial services and public facilities such as schools, parks and hospitals (Garza & Lizieri, 2016). In recent 3 years, more researches have highlighted the distance to the nearest supermarket (Chai et al., 2021; Jiang et al., 2022; Shen et al., 2022; Zhou et al., 2022), to the nearest school (Jiang et al., 2022; Shen et al., 2022; Zhou et al., 2022), and to the nearest hospital (Jiang et al., 2022; Shen et al., 2022).

Individual characteristics refer to the impact of the features of the land plots as well as the developers on the land price. It has been widely accepted that the allowed plot ratio, required portion of green land and parking lots could all affect the land price (McMillen & Redfearn, 2010; Panduro & Veie, 2013). Plot ratio is believed to be the most important one as it defines the building area for sale (Chai et al., 2021; Garang et al., 2021; Z. Huang & Du, 2021; Shen et al., 2022; Zhou et al., 2022). Besides, some countries publish Housing Price Index (HPI) to measure the changes in residential housing prices and indicate house price trends. With hedonic regression, HPI removes the influence of individual factors on real estate prices and can shed light on the economic situation (Hill, 2013). HPI is also an indicator of the market expectations in land market. An increase in the housing price index would inevitably stimulate the enthusiasm of the developers to obtain land for development and impact the land prices (Hjalmarsson & Österholm, 2020).

The importance of the political connections of the developers has been highlighted recently. Political connections refer to the real estate enterprise’s ownership and affiliation. Existing studies proved a negative effect of affiliation on firm performance as resources are unevenly distributed (Monkkonen et al., 2019; L. Zhang et al., 2021). However, the definition and quantification of the political connections have long been a problem for modeling. Political connections may refer to the relationship with a Parliament member or the parties (Faccio, 2006; Ferguson & Voth, 2008), or the political experiences of enterprise operators (Li et al., 2008). A transitional economy such as China offers a more straightforward way to quantify political connections. With the establishment of the State-owned Assets Supervision and Administration Commission (SASAC) in each city, SOEs are the enterprises with shares of SASAC or companies wholly owned by SASAC exceeding 50%, according to the regulation of the National Statistics Bureau. A rich collection of data on the economic weight of SOEs allows more practices to model the role of SOEs in land pricing (Anderson et al., 2015; Cai et al., 2017; Szarzec et al., 2021; J. Wu et al., 2012).

Modelling Residential Land Pricing With Spatio-Temporal Heterogeneity

There has been a tremendous effort among economists, planners, and policymakers to model the land pricing. Lancaster’s (1966) insight that a commodity is a good is formed and valued with various attributes and Rosen’s (1974) analysis of choice in characteristic space have laid the theoretical foundation for the empirical research model of heterogeneous commodities—the hedonic price model (HPM). HPM manipulates a property as a mixture of a bundle of attributes that meet the different needs of people and provides an effective way to estimate the price of each attribute (Nelson, 1978). The traditional ordinary least squares (OLS) estimator applied in HPM assumes no spatial autocorrelation among the observations (Glumac et al., 2019). However, the residential market in a region is not homogenous, and housing units located in different geographic locations are likely to have different hedonic price combinations. This led to adjustments to the model, such as the application of HPM in sub-divided markets (Schnare & Struyk, 1976) or taking into consideration of the heteroscedasticity problems of factors such as the residential age and number of rooms in the OLS regression model (Fletcher et al., 2000; Goodman & Thibodeau, 1997).

Together with the advancement of spatial econometrics and spatial statistics, new mathematical tools were applied to address spatial autocorrelation in models (Brunsdon, 1996; Cao et al., 2018; Diao, 2015; Fotheringham et al., 2015; Helbich et al., 2014). The geographically weighted regression (GWR) and the multiscale geographically weighted regression (MGWR) model were proposed as further efforts to improve the accuracy of modeling the land prices. GWR explores the potential spatial nonstationarity of relationships and provides a measure of the spatial scale at which processes operate through the determination of an optimal bandwidth. MGWR further allows different processes to operate at different spatial scales, and provides a more flexible and scalable framework to examine multiscale processes (Fotheringham et al., 2017). This means that for some explanatory variables, the neighborhood can be larger or smaller than for other variables. By allowing the scale of analysis to vary between explanatory variables, MGWR fits better for the analysis of datasets in which the dependent variable exhibits spatial heterogeneity. Applications of the MGWR model in the study of geographical changes of the impacts of various factors on real estate prices in Istanbul (Sisman & Aydinoglu, 2022), the study of the premium of the road network on real estate prices in Chengdu (Wang et al., 2022) and Chen and Luo (2022) have proved that the MGWR model could offer better performance.

In summary, the nature of the transitional economy of China determines that China’s land market is inevitably subject to government interference and a common effect is that local governments will give different preferential treatment to enterprises of various ownerships and affiliations. Such preferences will be shown in land prices, but have yet to be quantified and evaluated in existing studies. However, in detail, the political connections of the developers affect the residential land leasing prices in Chinese cities still needs more in-depth investigation. Furthermore, existing studies have suggested technologies that were more suitable for real estate price studies than HPM which is commonly used for land price modeling and could be applied for spatial heterogeneity analysis of the influence of various factors.

Methodology

Study Area and Samples

In this study, central Chengdu (an area within the outer ring road in Chengdu) was selected as the research area. Chengdu is the capital of Sichuan Province. With its priority in the national development plan, and by leading regional development, Chengdu was approved as a National Central City in 2016. It also witnessed a fast population increase in recent decades and now has a population of around 21.192 million. Economic as well as population growth boost the demand and supply for housing in Chengdu. New buildings have sprung up like mushrooms in Chengdu even since 2000. This study takes the area inside Outer Ring Road as the study area (Figure 1). Enjoying a fast speed of economic and urban development, the area inside Outer Ring Road is the main area where land transfers have occurred in this decade. The area outside Outer Ring Road includes too many non-urban built-up areas where there are few residential land leasing cases during the research period. Besides, the distance measurements, such as the distance to CBD or the nearest subway station, could become problematic as the majority of the area outside Outer Ring is rural area which is remote from and incomparable with urban areas. Most residential land plots enjoy relatively similar geographical advantages inside the Outer Ring. Outside the Outer Ring, on the contrary, factors such as the entrance of expressways to the city, commercial centers in suburban counties and urban planning have significantly increased their influence on land prices. Significant needs for accommodation and dense development of housing inside the Outer Ring Road could also provide a sufficient sample size for the research on land leasing prices in Chengdu. We used Python to collect the land lease data in Chengdu from 2009 to 2019 from the 3fang.com-Land Cloud section (https://land.3fang.com/). Information collected about the status of the land plots includes the coordinates of the centroid for the land parcel, land use type, transaction method, land area, planned construction area, plot ratio, transaction date, transaction price and buyer (developer).

The study area.

As the epidemic of covid-19 and the subsequent lockdowns since 2020 have greatly distorted land leasing behaviors of the local governments in China, land leasing cases in 2020 and 2021 are not included. As shown in Figure 2a, there were 474 residential land leasing cases in Chengdu from 2009 to 2019. Most land leasing cases are concentrated between the Second Ring and the Outer Ring. The boxplot of the price of floor area (see Figure 2b) shows that the floor area price of the residential land sold in Chengdu generally showed an upward trend from 2009 to 2019. Two small peaks of the prices exist for the years 2013 and 2017. After 2017, the growth slowed down. The market fluctuations of the land leasing prices indicate the impact of macroeconomic and political instability in a city and conversions of the prices according to the time of sale are thus needed. Referring to the method introduced by Feng (2011), this study takes the land price index for 2019 as the benchmark and converts the land prices of floor area from 2009 to 2018 to what the prices would be in 2019. Equation 1 is applied in this study to achieve this task.

In this equation,

Distribution of the land leasing cases: (a) the land leasing cases with price labeled and (b) box plot of price distribution.

Factors Impacting Residential Land Leasing Price in Chengdu and Quantification

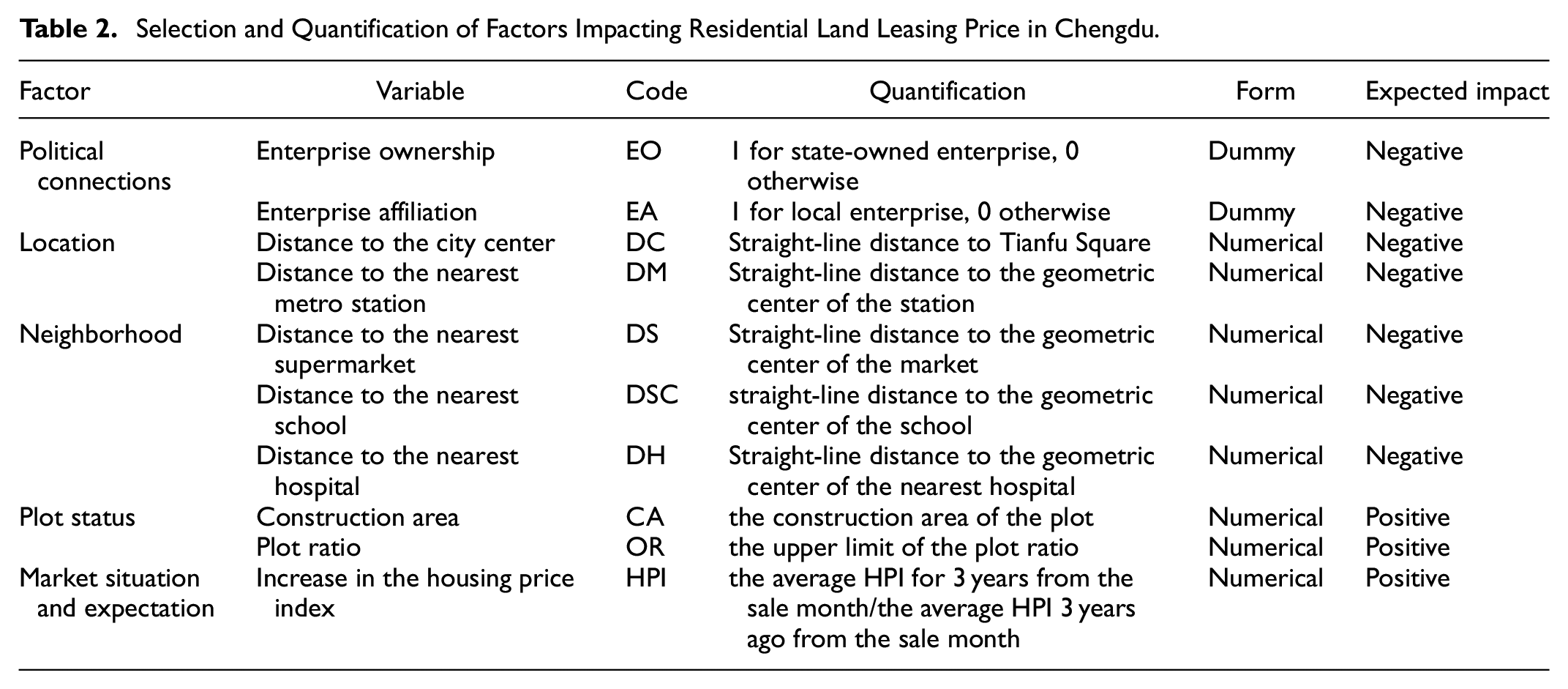

Based on the literature and preliminarily thoughts about political connections, this study aims to identify some variables to reflect and evaluate the impacts of the developer’s political connections. Together with the variables to define land prices that were selected based on the literature and availability of the data, all variables are shown in Table 2.

Selection and Quantification of Factors Impacting Residential Land Leasing Price in Chengdu.

The research data used in this study came from open data sets available online. This procedure reduces the data acquisition costs and provides larger numbers of research samples. The data collected covers the following four aspects.

Point of Interest (POI) Data

POI data offer an excellent resource for collecting data about services, with labels for service types and locations. In this research, the Python crawler program was used to obtain POI data from the Baidu Map open platform. POI data collected includes the location of the city center (Tianfu Square in Chengdu), subway stations, shopping malls, primary and secondary schools, and hospitals. This data is used to calculate the variables of location and neighborhood.

Enterprise Status Data

The enterprise status data is obtained from Qixinbao (https://www.qixin.com/), which is a data provider tracing all the basic information of enterprises in China, including the name, identity number, registration date, shareholder, registration address, and so on. These data provide two variables that indicate the political connections of the developers: ownership and affiliation, as shown in Table 3. Due to the limited information openly provided for enterprises, this study matches the name of developers and labels their political connections in a relatively simple way: 1) If the shareholder of the enterprise is a local State-owned Assets Supervision and Administration Commission, or if the state-owned institution holds more than 50% of the shares of a mixed-ownership enterprise, the enterprise will be recognized as an SOE. This standard is defined by the National Bureau of Statistics in the “Opinions of the National Bureau of Statistics on the Identification of State-owned Companies” in 2003. 2) Non-state-owned enterprises mainly include private enterprises, Hong Kong, Macao and Taiwan enterprises and natural persons, and so on. 3) If the enterprise is registered in Chengdu, it is recognized as a local enterprise.

Statistics of Developers’ Political Connections to Samples.

Housing Price Index of Chengdu

The monthly housing price index is collected from the China Real Estate Index System (https://www.cih-index.com), provided by China Index Academy. It refers to the weighted average of new housing prices with the calculation formula as follows:

In the formula,

Comparison and Selection of Models

HPM

According to Lancaster’s (1966) theory, the application of the HPM is based on the hypothesis that various attributes contribute to the value of goods, and land is exactly such a heterogeneous good. The HPM is often solved with the regression equation, so the choice of the specific form of equation will directly affect the analysis results. Existing literature has applied linear, logarithmic, and semi-logarithmic functions, and semi-logarithmic functions generally could better alleviate the problem of heteroscedasticity. It refers to the weighted average of new housing prices with the calculation formula as follows:

HPM applies the traditional ordinary least squares (OLS) estimator. In Equation 3,

GWR

GWR produces the spatial weight matrix that admits varying spatial relationships. Generally, the nearer the observations are, the higher the impact on the local set of coefficients would be for the point-based calibration around each regression point (Cao et al., 2018). The GWR model used in this research can be written as:

Here

MGWR

Differ from the GWR which uses a fixed bandwidth for all variables to calculate their parameters, MGWR advances the approach by allowing conditional relationships between the dependent variable and independent variables to vary at different spatial scales, which can better capture the spatial non-stationarity for different variables (Fotheringham et al., 2017). Similar to Equation 4, the equation for MGWR in this study can be written as follows:

Here

Comparison

As shown in Table 4, the fitness R2 and adjusted R2 of the MGWR model are higher than those of the OLS and GWR models. MGWR model also enjoys lower AIC and AICc values than the other two models. Taking into consideration of the excellent performance of the MGWR model, the results of this study are mainly analyzed with the MGWR model.

Comparison of HPM, GWR, and MGWR Models.

Results

Factors Impact Land Leasing Prices in Chengdu

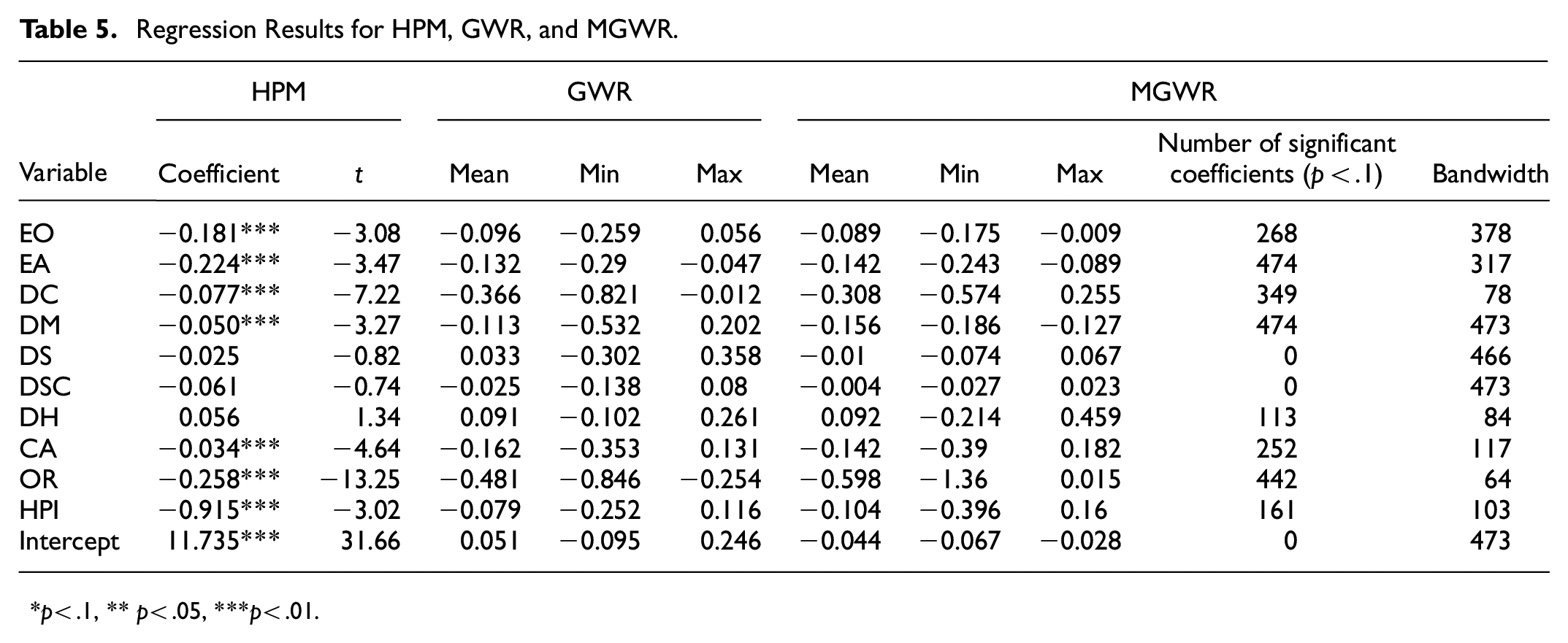

As shown in Table 5, the results of three different models are consistent with expectations. Since MGWR is a local regression model with individual coefficients and significance tests for each observation (the price of land leasing case), this study calculates the mean value of the coefficients of all observations to indicate the average strength of the influence of the coefficient on all observations. The bandwidth defines the spatial scale of different influences. The larger the bandwidth, the larger the spatial scale of the influencing factor. In other words, the factor can affect land prices on a larger spatial scale or even a global scale. The spatial heterogeneity of factors affecting land prices can be mapped by the intensity of impact and visualized within the spatial range of the trend to further analyze the spatial pattern of impact distribution. As shown in Table 3, the distances to the nearest large shopping mall and the nearest primary and secondary schools are not significant in the model, and these two factors are not considered in the spatial mapping of the coefficients that describe the spatial heterogeneity of the impacts of various factors.

Regression Results for HPM, GWR, and MGWR.

p< .1, **p< .05, ***p< .01.

Role of Political Connections

According to the results, both enterprise ownership and affiliation of the buyers, who are also the developers, play essential roles in defining the land leasing prices in central Chengdu. As far as the ownership of enterprises is concerned, state-owned enterprises have a relatively significant price advantage in purchasing residential land when Chengdu. The average land leasing price per floor area decreases by 8.9% for state-owned enterprises. The bandwidth of the coefficient is as wide as 378, indicating a great impact throughout central Chengdu. As shown in Figure 3a, the northern part of central Chengdu has witnessed the most substantial impact from the enterprise’s ownership. In the southern part of central Chengdu, whether it is a state-owned enterprise has no significant impact on the land leasing prices. Similarly, local enterprises have obvious price advantages over non-local enterprises when purchasing land (Figure 3b). The value range of the coefficient of enterprise affiliations is −0.243 to −0.089, and the average coefficient is −0.142, indicating that the average purchase price by local enterprises is 14.2% lower than that of non-local enterprises. The bandwidth attributable to the enterprise is 317, which is also a large scale covering most of the study area. The coefficients of enterprise affiliations decrease spatially from southeast to northwest, which also shows more advantages held by local enterprises in the northeast part of central Chengdu.

Impacts of the political connections on the land leasing prices: (a) enterprise ownership and (b) enterprise affiliation.

Impacts of Factors Other Than Political Connections

The result doesn’t challenge the traditional emphasis on the location to define the land price. The value range of the coefficient of the distance from the city center is −0.574 to 0.255, with a mean value of −0.308, indicating that, in general, for each standard deviation increase in the distance from the city center, the land price per floor area will drop by 30.8% (see Figure 4a). From the perspective of spatial heterogeneity, the coefficient of the distance from the city center shows a trend of decreasing from the middle to outer space. However, its bandwidth is 78, indicating that distance from the city center only plays a role on small spatial scales. The distance from the nearest subway station shows a broader adoption. The bandwidth of the coefficient of the impact of the distance from the nearest subway station is 473, which means an impact on almost a global scale (see Figure 4b). The value range of the coefficient of the distance between the site and the nearest subway station is between −0.186 and −0.127, with a mean value of −0.156, which means that for each standard deviation increase in the distance to the nearest subway station, the land price per floor area will drop by 15.6%. The overall coefficient of this variable decreases from the southeast to the northwest, indicating that this variable has a greater impact on land leasing prices in the northeast part of Chengdu. This may be because the construction of the Chengdu subway in the northeast has lagged behind that in the south for years and increased the premium of subway stations for the development and sale of housing products.

Spatial patterns of the distribution of the coefficients in the MGWR model: (a) distance to city centre, (b) distance to the nearest subway station, (c) distance to the nearest hospital, (d) construction area, (e) plot ratio, and (f) market Expectation.

Neighborhood characteristics mainly refer to the degree to which land leasing prices are affected by its surrounding public amenities and commercial services. In the regression results of MGWR, the coefficients of the variable of the distance to the nearest shopping mall and the variable of the distance to the nearest center do not significantly affect the land leasing prices at the 10% significance level for all land plots, indicating a possible even distribution of school and commercial service supply throughout Chengdu. The distance from the nearest hospital has a greater impact, with a bandwidth of 113 (see Figure 4c). Although the scale of the impact of the distance from the nearest hospital might not be significant, the way it impacts the land leasing prices is worth discriminating against. The impacts of hospitals on land leasing prices vary in different locations: in the east and southwest, hospitals can positively affect land leasing prices, indicating a greater need for hospitals. However, a negative impact is observed for the northeast part of Chengdu, which may be partially due to the relatively lower quality of the hospitals in this area.

The coefficients of individual characteristics reflect the impacts of the land plots’ structural attributes (such as area and shape) on the land leasing prices. The coefficient of construction land area ranges from −0.39 to 0.182 in the regression results of MGWR, with a mean value of 0.142 (see Figure 4d). The plot ratio has the greatest influence among all factors, and its coefficient ranges from −1.36 to 0.015, with a mean value of −0.598 (see Figure 4e). However, the bandwidths of the coefficients of the construction area and plot ratio are 117 and 64, respectively, indicating that the individual characteristics could only impact land leasing prices on small geographic scales. From the perspective of the spatial distribution of the coefficients, the coefficients of the construction area decreased from southeast to northwest as a whole, and the impacts on most of the land plots in the southwest are insignificant. The overall distribution of the plot ratio coefficient shows a trend of decreasing values from the city center to the urban periphery, indicating that an increase in the plot ratio of land closer to the city center will increase land leasing prices more significantly. This study also controls the housing price market expectations at the time of land transactions as the macro background of land transactions in the model. The model shows drastic changes in the impacts of the expectations of housing prices on the land leasing prices at different locations (see Figure 4f). The coefficient ranges from −0.396 to 0.16, with a bandwidth of 103, indicating that the expectations of housing prices could only have impacts on land leasing prices on small geographic scales. Recently, the housing prices in different parts of Chengdu have shown different paces of the price increase. This has also led to a weakened impact on land prices of the expectation of the housing prices when it is calculated with the housing index of the whole city.

Discussion

The impacts of political connections of enterprises on the costs to obtain all types of resources and enterprise performance have attracted scholars’ attention in economics and political sciences for decades. Land is the most crucial resource for both production and living. Its distribution could hardly escape from the impacts of enterprises’ political connections and is worth closer investigation. With the established SOE supervision system, there are precise dimensions for the political connections in China: ownership and affiliation. In this study, the definitions of ownership and affiliation by the official authorities are applied, but the political connection could be more hidden and subtle. Studies also indicate that whether the leader in charge of the company was transferred from the government or served as an official of the local government when the land was sold also has a particular influence (Zhao & Yang, 2015). Moreover, Chengdu has a population of more than 20 million, and the population distribution is uneven. Although the economic development within the Outer Ring Road is relatively balanced, there are still subtle differences in the economic conditions of different districts. Due to data availability, these have not yet been included in the model applied in this study.

Further adjustment of the methodology to reflect the temporal changes could also be suggested: the MGWR model focuses on the analysis of the spatial differentiation of impacts, with few studies of the temporal characteristics of the impacts. However, the reform of China’s land market is gradual, and the influence of political connections on land leasing has changed over time. Considering the spatio-temporal changes of political connections is conducive to better understanding the macroscopic impact of land market reform on enterprises’ land purchase behaviors. Taking the temporal differences of the impacts of various factors with new methodologies could thus achieve more accurate results for the analysis of the mechanism of land pricing.

Conclusion

Taking enterprise ownership and affiliations as two explanatory factors that impact the land leasing prices in central Chengdu, this study builds an MGWR model to evaluate the premium of political connections for the developers to buy the land in a transitional economy. The MGWR model not only reveals spatial differences in the relationship between land leasing prices and impact factors, but also defines a spatial bandwidth for each factor that impacts the land leasing prices in this study. It reflects the local, regional or global patterns of the change of the influences, and offers a new way to understand and react to the land leasing market precisely. With the MGWR model, it is proved in this study that both the enterprise ownership and affiliation of the developers play important roles in defining the land leasing prices in central Chengdu. In general, the average purchase price by state-owned enterprises is 8.9% lower than the prices that private enterprises could enjoy, and the average land leasing price by local enterprises is 14.2% lower than that enjoyed by non-local enterprises.

Studies of the roles played by the political connections of the developers offer a new way to better understand land marketization and the business environment in China. Compared with the advantages that state-owned and local enterprises hold in land leasing, private enterprises and non-local enterprises have to bear higher land lease payments. This gives a clue to the local protectionism and state-owned enterprises’ preference that might exist in land leasing in Chengdu. Such trends have regional differences. The southern part of the study area, where the south part of the National Hi-tech Zone locates, obviously has a better business environment and fair competition conditions for land use. On the contrary, the northern part of central Chengdu is affected more by administrative forces in land allocation. Further investigation of the institutions is still needed: the northwest part also suffers from a relatively higher bias in the chances for fair land leasing payments for enterprises with different ownerships and affiliations, although this area – known as the west part of the National Hi-tech Zone—actually shares similar institutional guidelines for land leasing as the southern part.

In broader theoretical terms, the preceding conceptual and empirical discussion in this study advocates for a rethinking of the intervention of public sectors in the land market in China. The results about the impacts of political connections on land leasing prices indicate that although land reform has successfully built a frame for an open land market, administrative preferences could still distort the market mechanism of resource distribution. Such choices may come from the protection for local enterprises or growing audit requirements from higher-level governments and result in the advantages of state-owned and local developers having to obtain trust and establish a relationship with the local government. To maintain the land market, there needs close monitoring of the way of land leasing and the role of the government. In-depth studies of the factors that define the land leasing behaviors of the local government are needed.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by National Social Science Foundation of China (NSSFC) Key Project [grant number 23AGL037].

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.