Abstract

Haze pollution not only affects the quality of economic growth and the image of the government, but also seriously affects public health. With the improvement of climate risk perception, the public is actively seeking all kinds of risk management measures to combat the hazards of haze pollution. The study of the relationship between haze pollution, climate risk perception and the development of commercial health insurance is of great significance to the formulation of haze control policies and the improvement of social security system. This paper attempts to explore the relationship between haze pollution, climate risk perception and commercial health insurance demand by establishing static and dynamic models based on panel data from 31 provinces in China from 2005 to 2022. Also, the spatial spillover effects of haze pollution in different regions on the development of commercial health insurance in other regions are investigated by establishing a spatial Durbin model. It is found that (1) haze pollution has a lagged positive effect on the demand for commercial health insurance; (2) haze pollution has a significant spatial spillover effect on the development of commercial health insurance; (3) this study used Python technology to construct a climate risk perception index, and found that the moderating effect of the residents’ perception of climate risk existed significantly, and that the residents might take other measures to manage the risk in the short term, but in the long term, the climate risk perception showed a positive correlation with the level of education. This paper provides implications for government departments and social media to strengthen education and publicity, improve residents’ awareness of risk diversification, and deepen the concept of commercial health protection.

Plain Language Summary

This paper attempts to explore the relationship between haze pollution, climate risk perception and commercial health insurance demand by establishing static and dynamic models based on panel data from 31 provinces in China from 2005 to 2022. Also, the spatial spillover effects of haze pollution in different regions on the development of commercial health insurance in other regions are investigated by establishing a spatial Durbin model. It is found that (1) haze pollution has a lagged positive effect on the demand for commercial health insurance; (2) haze pollution has a significant spatial spillover effect on the development of commercial health insurance; (3) this study used Python technology to construct a climate risk perception index, and found that the moderating effect of the residents’ perception of climate risk existed significantly, and that the residents might take other measures to manage the risk in the short term, but in the long term, the climate risk perception showed a positive correlation with the level of education.

Keywords

Introduction

China’s economy has witnessed a period of rapid development, but the haze pollution problem has become increasingly serious behind the rapid economic growth, which has become a great obstacle to the construction of ecological civilization (Bai & Nie, 2017). In 2016, the haze pollution problem was particularly serious, even covering 17 provinces and cities in the central-eastern region of China. By 2010 PM2.5 index began to be published, and the central media began to alert the health problems caused by haze pollution, haze pollution once caused widespread concern throughout society (Shao et al., 2016). The haze will not only affect the living environment, the image of the city, and the development of the economy, but also seriously affect the health of residents and cause an increase in the incidence of diseases. The problems brought about by haze pollution have raised the health care costs of residents and increased the demand for commercial health insurance (S. Chen & Chen, 2018).

In 2010, the World Health Organization released the Global Burden of Disease Assessment project, which showed that haze pollution was predicted to cause 1.2 million premature deaths from lung cancer, sudden death, and other diseases in China, with children being the most severely harmed by haze pollution. The China Environment Report (2020) (Ministry of Ecology and Environment, 2021) white paper shows that haze pollution is a serious impediment to China’s economic development and an increasingly serious public health hazard to the population (J. Wu et al., 2017). It is evident that the haze pollution problem continues to worsen and may pose a great danger to the health and lives of the residents. Therefore, the excessive burden of personal health care has become one of the major social conflicts in China, and the problem of how to reduce the cost of health care for residents has become a challenge to be solved in the new era.

Commercial health insurance in China started in 1982 with 40 years of development history so far. The development time is relatively short, but it has developed rapidly with the support of many policies in China (B. Chen et al., 2019). Commercial health insurance has always played an indispensable role in the reform of China’s health insurance system. The State Council of the People’s Republic of China issued 《The Outline of the “Healthy China 2030” Plan》 (“The Outline”),which clearly puts forward the requirement of “actively developing commercial health insurance,” encouraging individuals and enterprises to actively participate in commercial health insurance, and enriching the existing health insurance products. In addition, the Outline further specifies that by 2030, there will be further development of commercial health insurance in China, and significantly increase the ratio of commercial health insurance claims expenditure to the total cost of medical and healthcare expenditure. The release of the Outline confirms the importance of commercial health insurance in serving the “Healthy China” strategy and improving the medical security system in the form of a national strategy for the first time. The release of these documents catered to the current demand of Chinese residents for health protection and fully reflected the important status and good development trend of commercial health insurance in China’s insurance industry (He et al., 2019).

There has been literature on the elements of commercial health insurance development to make relevant exploration, still there are many shortcomings in the development of the domestic commercial health insurance market, specifically as follows: insufficient perception of the climate risk of the residents, the lower degree of specialization, and the lack of effective supply, etc.; There is also a large amount of literature analyzing the causes and impacts of haze pollution, but it is worth noting that haze pollution is not a purely local environmental problem, but can spread or be transferred to other regions through natural factors such as atmospheric circulation and economic mechanisms such as industrial transfer (L. Ma & Zhang, 2014; Shao et al., 2016). However, existing studies have only studied the impact of haze pollution on commercial health insurance purchasing behavior decision-making from single enterprise perspective at the micro level, and there is little literature on the impact of haze pollution and residents’ risk perception on the demand for commercial health insurance, which ignores the spatial spillover effect of haze pollution, possibly leading to biased empirical findings and affecting the state’s targeted haze-control policies. In this context, it is necessary to analyze the demand for commercial health insurance for haze pollution and climate risk perception. In addition, climate governance requires in-depth public participation, and the public’s perception of climate risks will influence the development of climate governance. Meanwhile, the public’s perception of climate risk will also affect their motivation to take protective measures for their own health, thus the government needs to take into account the information conveyed to the public as well as the possible feedback from the public when setting policies. Therefore, this paper incorporates haze pollution, residents’ climate risk perceptions and commercial health insurance consumption into the one analytical framework by attempting to address the following questions: How does haze pollution affect commercial health insurance consumption? What is the difference between short-term and long-term impacts? Does residents’ perception of climate risk moderate these effects? The aim is to provide reference for insurers’ product design and business development, assist insurers in developing haze-pollution and geographically-specific products, give full scope to the economic protection function of commercial health insurance, and stabilize the livelihood of the society.

Based on the above research motivation, this paper takes haze pollution as the research object and explores the relationship among haze pollution, climate risk perception and commercial health insurance on the basis of the panel data of 31 provinces in China from 2005 to 2022, with empirical tests conducted by static and dynamic panel models respectively, which investigate the direct effect of haze pollution on the demand for commercial health insurance and the moderating effect of climate risk perception of residents. The main findings of the study are as follows: firstly, haze pollution promotes the demand for commercial health insurance from the perspective of the provincial level; secondly, we tested the channels through which haze pollution promotes the demand for commercial health insurance by using the moderating effect model, and found that the climate risk effect caused by haze pollution plays a major role. This paper enriches the current research literature on the impact of haze pollution on commercial health insurance demand, and has certain theoretical value.

The possible marginal contribution of this paper lies in the following four aspects: first, in terms of perspective, there are existing studies analyzing the impact of environmental pollution on commercial health insurance. However, there is less research literature from the perspective of haze pollution. The existing foreign research involving haze pollution and commercial health insurance also mainly focuses on the relationship between haze pollution and residents’ health, or mainly focuses on the relationship between insurance claims and medical expenses. Therefore, there are few studies taking haze pollution as an entry point to study the relationship between the two sides from both domestic and foreign, and most studies adopt methods and select variables that are quite different from those in this paper.

Second, on the empirical research method, this paper takes residents’ climate risk perception as a moderating variable in the relationship between haze pollution, residents’ risk perception and demand for commercial health insurance. In the existing literature, most of the studies are based on the relationship between haze pollution and commercial health insurance, mostly analyzing with static models. Instead, this paper not only introduces the cross-sectional term of residents’ climate risk perception, but also adopts static and dynamic models to further analyze the relationship between the haze pollution, climate risk perception and commercial health insurance by incorporating the time span based on the existing literature. Third, this paper proposes a four-dimensional index system based on the process of climate risk perception, using Python technology to extract the web search volume of keywords related to climate risk, and then, adopting the Generalized Dynamic Factor Model (GDFM) for key factor extraction to construct a comprehensive index of climate risk perception to portray the public’s sensitivity to climate risk. Finally, considering the spatial mobility of haze pollution, a spatial Durbin model is used to explore the spatial spillover effect of haze pollution on the demand for commercial health insurance.

Literature Review

This paper is concerned with the impact of haze pollution and climate risk perception on the demand for commercial health insurance. It can be categorized into two main groups: the health risk of residents caused by haze pollution and the influence of climate risk perception on the demand for commercial health insurance. Among the above two categorizations, this paper builds a logical framework by reviewing and sorting out the relevant literature and research results in order to target the problems and solve them.

The Impact of Haze Pollution on Residents’ Health

Haze pollution refers to the air pollution phenomenon formed when the economic and social activities of high-density population emit a large amount of fine particulate matter (PM2.5), and the concentration of fine particulate matter will continue to accumulate when the emission exceeds the capacity and carrying capacity of atmospheric circulation. Since 2010, scholars at home and abroad have conducted a lot of research on the health problems caused by haze pollution to residents. Scholars have pointed out through their studies that haze can cause great adverse effects on the human cardiovascular system, nervous system, immune system, etc., especially on the human respiratory system (He et al., 2019; M. Li & Du, 2018; Lv et al., 2017; Sun et al., 2016).

Moreover, many studies in the literature have found that air quality significantly affects the potential life expectancy of Chinese residents, in other words, the life expectancy of residents is significantly correlated with the concentration of air pollutants, the welfare loss of residents caused by haze pollution is increasing rapidly, and the increasing concentration of PM2.5 has caused significant health economic losses to Chinese residents, and the medical costs of residents are increasing (Y. Chen et al., 2013; W. Li et al., 2016; Xie et al., 2014) considered the fact that centralized heating is provided in the north of China during winter, and the burning of large amounts of fuel can lead to excessive emissions of pollutants, which can cause significant differences in haze pollution between regions in China. Therefore, the authors used the Huai River as a dividing line and found that haze pollution reduces the life expectancy of northern residents by 5 years. Other qualitative studies have found a relationship between haze pollution and respiratory diseases, cardiovascular diseases, and female mortality (Xie et al., 2014; Zhou et al., 2014). Some scholars have even found that the effects of haze pollution on public health in large and medium-sized cities in China are long-term and do not disappear in the short term (Huang & Zhang, 2013; Kan & Wu, 2013; Qu & Yan, 2015).

Economic Effects of Haze Pollution on the Health of the Population

From a macro perspective, S. Chen and Chen (2018) point out that haze pollution has a significant negative effect on the economic growth of society, and the negative effect of haze pollution on the economic development of large cities is higher than that of small cities. The increasing problem of haze pollution may lead to an increase in the cost of foreign investment, which in turn makes foreign investment decrease and affects the economic development of the region (Shi, 2014). From a microscopic perspective, haze pollution can affect the efficiency of individuals and cause a decrease in individual productivity (Ebenstein et al., 2015; He et al., 2019; Wei et al., 2017). Even haze pollution may affect investors’ judgment on the stock market by affecting individuals’ emotions and expectations, resulting in a decline in stock returns (Guo & Zhang, 2016).

Factors Influencing Climate Risk Perceptions and Management Measures

In the existing literature and theoretical findings on the impact of risk perception on the demand for commercial health insurance, most of them use the level of education to measure the level of risk perception. The results of these studies show that the more educated an individual is, the more risk-averse he or she is and the more likely he or she is to purchase insurance against risk (Browne & Kim, 1993; Kjosevski, 2012; D. H. Li et al., 2007; Truett & Truett, 1990; Ward & Zurbruegg, 2002; Yuan & Jiang, 2015). Among domestic scholars, Hu et al. (2018) showed that as residents’ education level deepens, their knowledge of insurance products becomes more comprehensive, their demand for insurance increases, and they are more inclined to use insurance to diversify risks. The public’s demand for insurance increases in the long run as their education level increases, thus driving the development of commercial health insurance. However, Millo and Carmeci (2015) suggest that as individuals become more educated, they acquire more favorable ways to spread risk and are not limited to purchasing insurance, and that more educated individuals are better equipped to spread risk in different ways and tend to show a preference for risk. Domestic and international studies have shown that when the public has a clear understanding of the health damage caused by pollution, they are generally willing to pay the corresponding financial cost to spread the risk and mitigate the health loss caused by pollution (Cuñado & de Gracia, 2013).

Spatial Spillover Effects of Haze Pollution on Commercial Insurance

In general, most spatial data have spatial correlation (Fang et al., 2017; J. Wu et al., 2017), and haze pollution has significant spatial flow and diffusion effects (Shao et al., 2016). The haze pollution in one region will spread to other regions through spatial gas flow, and there is a high concentration of highly polluting enterprises in China, and the haze pollution is likely to move to other regions along with the migration of highly polluting enterprises (S. Chen & Chen, 2018; L. Ma & Zhang, 2014). Currently, China is in the era of rapid development of information technology, and the public can easily learn about the pollution status of high-risk areas of haze pollution through online media, so even people in low-risk areas will increase their risk perception level and risk aversion after being exposed to pollution information, and they will purchase corresponding insurance products to manage risks in order to effectively reduce the impact of haze (Cheng & Zhu, 2021; Guo & Zhang, 2016). At the same time, China is a country with a high mobility rate between regions, and commercial health insurance has the feature of cross-regional insurance, along with the mobility of labor across regions, commercial health insurance also shows spatial spillover effects (Jia & Ma, 2015).

In summary, existing studies have analyzed the impact of haze pollution from macro and micro perspectives as well as the factors affecting the development of commercial health insurance from the supply and demand side. Existing related studies at home and abroad mainly focus on the impact of haze pollution on residents’ health risks, health insurance expenditures, or the impact of health insurance in mitigating the impact of haze pollution on residents’ health costs, and so on, with less literature directly exploring the specific impact of haze pollution on commercial insurance. However, the residents’ climate risk perception has been more often used as a control variable in the study of factors influencing insurance consumption, and few studies have dealt with the analysis of its role in coping with the impact of haze pollution. Moreover, both haze pollution and residents’ climate risk perception have an impact on commercial health insurance consumption, which is not isolated. Therefore, this paper attempts to analyze haze pollution, residents’ climate risk perception and commercial health insurance consumption in a unified framework, not only to explore the direct impact of haze pollution on commercial health insurance, but also to further analyze the moderating role played by residents’ climate risk perception.

Theoretical Hypothesis

The substantial impact of haze pollution on the development of commercial insurance has not received enough attention from scholars, much less to form a theoretical consensus. Combined with existing research, this paper argues that the mechanism of haze pollution on commercial health insurance includes the following three aspects.

The Direct Impact of Haze Pollution on Commercial Health Insurance

Existing research has proved that haze pollution is extremely hazardous to human health, and it has a great impact on the lives of residents. The main component of haze pollution is particulate matter in the atmosphere with a diameter of no more than 2.5 μm. Firstly, haze affects the physiology of residents; PM2.5 not only affects the respiratory system and causes various diseases, but also its components have carcinogenic effects on the human body (Y. Chen et al., 2013); secondly, haze also affects the psychological condition of residents. Individuals’ negative emotions, such as irritability, reduced control, and frustrated confidence, which are closely related to local air pollution levels (Mehta et al., 2015; H. Zhang et al., 2013). With so many adverse effects of haze pollution on human health, people should also have the willingness to avoid or minimize the harm caused by haze pollution. Numerous studies at home and abroad have shown that people are indeed willing to pay a premium to ward off the health risks associated with air pollution (van Rhyn & Barwick, 2019; Shao et al., 2018; H. Zhang et al., 2013).

In fact, there are various ways for residents to increase their health investments, which mainly include two major types of risk management methods: ex ante management for loss prevention and reduction and ex post management for loss financing from the perspective of risk management. In this regard, loss prevention and mitigation refer to the increase in various types of ex-ante preventive measures taken by residents to reduce the hazards of haze pollution on the human body, commonly including the purchase of purification products, donations to environmental organizations, medical checkups, and fitness. For example, households invest more in masks and air filter products when haze pollution levels exceed critical alert thresholds (Chang et al., 2018). And the most important way of loss financing is to increase the purchase of commercial health insurance under the premise of social security coverage, which is one of the effective means for the population to invest in health and enhance mental health expectations. However, it is clear that the method of loss prevention and reduction will lead to relatively less money for the purchase of insurance, causing a decline in the effective demand for commercial health insurance by the population (Bordalo et al., 2013). In addition, excessive rise in medical costs will lead to an imbalance between the revenue and expenditure of medical insurance premiums, as well as possible moral hazards such as over-consumption of medical services from the perspective of insurance company supply. These will affect the pricing strategy of insurance companies by adjusting premiums upwards in actuarial pricing, thus increasing the financial burden on policyholders, some of whom may choose to reduce the level of coverage or even delay purchase.

Further, the tendency to avoid harm is one of the main drivers of human behavior, and the public’s first consideration in haze pollution is how to avoid risk and loss (Yi & Sun, 2006). Behavioral finance research has shown that the public’s internal trade-offs between benefits and harms when making decisions about whether to purchase commercial health insurance are uneven, with the “harm avoidance” factor given twice as much weight as the “benefit seeking” factor (Yi & Sun, 2006; Zeng, 2003). In order to avoid risks and damages, the public’s level of haze pollution control feeling is relatively high, and people are more willing to buy commercial health insurance than those who buy health insurance in a state of severe haze pollution. At the same time, the public’s subjective perception of the impact of haze pollution on health has a time lag, only by fully recognizing the impact of haze pollution on health and improving the level of the sense of haze pollution control will the purchase of commercial health insurance decisions be made, which in turn will have an impact on the development of commercial health insurance. Therefore, on the one hand, haze pollution will prompt residents to purchase or increase the purchase of commercial health insurance, on the other hand, it may also have an impact on the demand for commercial health insurance because of the diversity of the residents’ coping measures and the changes in the decision-making. Based on the above analysis, this paper proposes the following hypotheses:

H1: Haze pollution contributes to the development of commercial health insurance

Moderating Effects of Climate Risk Perceptions

Public perceptions of climate risk are multifaceted (B. Chen et al., 2019). Behavioral finance theory integrates the disciplines of modern financial theory, psychology, and decision science into the analysis of investment behavior, its theory is based on the assumption that people make decisions on the basis of psychological factors (Zeng, 2003). This theory assumes that the public’s decision-making is not always rational due to the differences and imprecision of the information they possess and the assumption of limited rationality (Zeng, 2003). According to the above definition, the formation and improvement of residents’ climate risk cognition requires continuous learning and correction of climate risk event information, which is highly related to residents’ acceptance and discrimination of new information. Generally speaking, individuals with a higher level of education are more capable of recognizing and measuring risks in a comprehensive manner, and have a deeper perception of pollution risks. Families with a higher degree of climate risk perception will pay more attention to the hazards caused by haze pollution, rationally and objectively analyzing the various aspects of its impact on themselves in the future, such as earlier foreseeing and considering the possibility of future illnesses and the rise in medical expenditures, and the concern about future uncertainty will prompt them to arrange better risk management measures and reinforce family health and economic insurance (Chang et al., 2018). And the multiple specific methods of risk management range from various types of measures to directly reduce the harms of haze pollution on the human body to commercial health risks to finance losses for actual medical expenses. Residents with higher levels of climate risk perception will do a better job than those with lower levels of climate risk perception, both in terms of purchasing commercial health insurance and taking other risk-prevention measures (L. Cai, 2017; Chang et al., 2018). Therefore, in general, an increase in the level of residents’ climate risk perception will further amplify the impact of haze pollution on commercial health insurance.

In the short run, residents with higher climate risk perception will be more receptive and invested in preventive measures such as installing purifiers than those with lower climate risk perceptions, which will further amplify the dampening effect on commercial health insurance consumption in the current period. However, the investment in preventive measures is mainly concentrated in the early stage. In the long run, residents with a higher level of climate risk perception will be more active in purchasing commercial health insurance because they are better than those with a lower level of climate risk perception in terms of insurance awareness and economic income (Bai & Nie, 2017; Yi & Sun, 2006), in addition to the fact that most of the commercial health insurance available in the market is a long-term contract and is paid by installments, which further contributes to the further promotion of its premium income of continuous growth, and in turn amplifies the lagged positive impact of haze pollution on commercial health insurance consumption. Based on this, this paper proposes the following research hypotheses:

H2: Climate risk perceptions have a moderating effect on haze pollution and commercial health insurance

Spatial Spillover Effects of Haze Pollution on Commercial Health Insurance

According to the first law of geography, which states that everything may be correlated, most spatial daters exhibit spatial correlation (Fang et al., 2017; Tobler, 1970; J. Wu et al., 2016, 2017). Haze pollution has obvious spatial diffusion and transfer effects (Shao et al., 2016). Haze pollution is not a localized environmental problem, but will spread to other areas through atmospheric circulation, atmospheric chemistry and other natural factors. Moreover, haze pollution in Chinese provinces and regions shows obvious characteristics of high-emission club agglomeration, and regions with high haze pollution emission club agglomeration may “leak” haze pollution to other regions through the transfer of high-pollution industries (S. Chen & Chen, 2018; L. Ma & Zhang, 2014; Shao et al., 2016). At the same time, in the age of informationization, if a certain area, especially a landmark city suffers from persistent or severe haze pollution, the public outside the area may quickly capture the information through media dissemination and other public opinion campaigns. The risk of haze has been enlarged from a purely physical risk to a common risk for the whole society, so that even the public in non-haze-prone areas can have a real sense of the hazards of haze risk, increasing the level of control of haze pollution as well as the aversion to risk. In order to avoid the health risks brought about by haze pollution, they are still equally willing to purchase commercial health insurance and pay some attention to it (B. Chen et al., 2019; Guo & Zhang, 2016). Haze pollution has a significant spatial spillover effect, any public can not be alone, the public will also be concerned about the neighboring areas or other areas of haze pollution, increasingly become a “community of destiny” in which you have me, I have you. Along with labor mobility, commercial health insurance is “portable,” when participants’ workplaces change, the insurance benefits they receive can be retained or transferred to avoid damage to their benefits, and commercial health insurance may also spill over across regions (Jia & Ma, 2015; Tang & Yao, 2011).

In response to the reality of health threats caused by haze pollution and the increasing public demand for commercial health insurance, some local governments have introduced policies to encourage the development of commercial health insurance. For example, in 2017, the Shenzhen Insurance Supervision Bureau launched the Guiding Opinions on Accelerating the Reform and Innovation of Shenzhen’s Insurance Industry, which proposes to allow the usage of individual medical insurance account balances to purchase various types of commercial health insurance, and to innovate and develop various types of commercial health insurance products to realize the convergence with basic medical insurance. These regional policies may have spillover effects on the development of commercial health insurance in other regions. There is a high degree of interaction between the relevant government departments, the foreign public and the local public, with a certain degree of intersectionality and coupling. For example, the worsening haze pollution may also directly affect the formulation and implementation of policies, and their policies may have spillover effects, thereby affecting the willingness of the public in the field to purchase commercial health insurance, and having an impact on the development of commercial health insurance in other regions (Guo & Zhang, 2016).

In conclusion, the development of local commercial health insurance is not only affected by local haze pollution, but may also be affected by the overflow of haze pollution from other regions, thus, this paper proposes the following hypotheses:

H3: Haze pollution has positive spatial spillover effects on commercial health insurance

Data and Model Construction

Data Sources

As China carried out a reform of social medical insurance in 2005, which promoted the development of Chinese commercial health insurance to a certain extent and had an impact on the future direction of Chinese commercial health insurance. Therefore, this paper selects the data year sample from 2005 to 2022, at the same time, due to Hong Kong, Macao and Taiwan and the mainland statistical caliber is not the same, in order to ensure the accuracy of the results, we selected the regional samples of 31 provinces in the mainland, without Hong Kong, Macao and Taiwan. The data on haze pollution level comes from the National Air Quality Real-time Release Platform of the Ministry of Ecology and Environment of the People’s Republic of China; the data on the demand for commercial health insurance comes from the Chinese General Social Survey (CGSS2005-2022), and the data on the level of medical and healthcare resources and the per capita medical cost come from the China Health Statistics Yearbook, and other data come from the China Statistics Yearbook. This paper uses Stata 15 to process the model.

Variable Selection

(1) Dependent variable: commercial health insurance demand

This paper investigates the impact of haze pollution and residents’ risk perception on commercial health insurance demand. Based on the fact that the consumption of commercial health insurance in China is mainly concentrated in towns and cities, while the penetration rate in villages is not high, thus this paper takes the urban population as the research object. Referring to the method of Suo & Wanyan (2017), the dependent variable refers to the commercial insurance purchase indicator (CHID) in the CGSS 2005-2022 database, that is, “Whether you are currently purchasing commercial insurance,” with the value of 0 assigned to non-purchase, and the value of 1 assigned to purchase.

(2) Independent variable: haze pollution level

The Independent variable selected for this paper is PM2.5, a haze representative, and this paper draws on the study of W. Li et al. (2016) to use the air quality index as a measure of haze pollution. The air quality level is divided according to the size of the index: 0–50 points, 50–100, 100–150, 150–200, 200–300, and more than 300 represent the six levels of haze pollution: excellent, good, light pollution, moderate pollution, heavy test pollution, and severe pollution, this paper will take the natural logarithm of the haze pollution index to deal with the index. The larger the index value, the more serious the haze pollution in the region.

(3) Moderating Variables: Climate Risk Perception

Often, the occurrence of a climate risk event and a series of emergency response measures will lead to emotional panic among the public. The level of people’s perception of climate risk is directly related to the severity of climate risk events. Therefore, in order to accurately portray climate risk perception, this paper constructs a comprehensive index system of climate risk perception based on the process of climate risk perception, from the four dimensions of the name of climate disasters, the heat of climate disaster authorities, the way of coping with climate disasters and the consequences of climate disasters, extracting keywords from the Internet search volume by python technology, in order to construct a comprehensive index. Keywords can reflect human perception, preference and personality (Webb et al., 1966), and researchers can capture human traits by analyzing the type and frequency of words used in the language of experimental subjects (Miller & Ross, 1975). And python technology is an automated data collection technology that extracts information from web pages by simulating the behavior of manual web browsing, parsing and extracting the required data. Specifically, the process of constructing the climate risk perception indicator (RS) is as follows:

First, before the arrival of a weather disaster, people may search for information about the disaster directly through search engines or social media. Dou et al. (2021) found that during the impacts of Typhoon Pigeon and Paka in 2017, “rainstorm” and “typhoon” became hot topics on social media. “rainstorm” and “typhoon” became hot topics in social media. Therefore, the Baidu index of disaster names can be considered to capture people’s weather risk perception behavior. According to the “Measures for Issuing and Disseminating Early Warning Signals for Meteorological Disasters” published by the China Meteorological Administration (CMA), meteorological disasters in China mainly include: typhoons, rainstorms, snowstorms, cold waves, gusty winds, sandstorms, high temperatures, droughts, thunder and lightning, hailstorms, frosts, fogs, haze, and road icing. Second, the meteorological department is an important channel for people to obtain meteorological information and be informed of weather risk warnings. Ryan (2018a, 2018b) found through interviews that visiting the website of the Australian Bureau of Meteorology is an important way for people to be informed of disaster warnings and to confirm the authenticity of disaster rumors. Boas et al. (2020) also found that during meteorological disasters, information released by official agencies is more likely to be trusted by the public and more widely disseminated. The Central Weather Bureau (CWB) is the national center for weather forecasting, climate prediction, and meteorological information collection and distribution services in China. Therefore, this paper uses the Baidu index of “Central Weather Station” to capture people’s perception of access to information. Similarly, “Weather station” can also be used as keywords; third, before the arrival of a meteorological disaster, the public may use search engines to learn how to respond to it, S. Y. Ma et al. (2021) found that before Typhoon Nepartak happened, people were not aware of its impact on the weather. Therefore, we use the Baidu index of “emergency” to capture the degree of urgency of the public in responding to climate risks; finally, meteorological hazards may interfere with transportation systems, and the public will pay attention to flights, trains, and other dynamics after perceiving the risk of meteorological hazards, For example, before the landing of Typhoon Niburt, the term “stopping transportation” was used the topics of “stopping transportation” and “stopping sales” became hot topics (S. Y. Ma et al., 2021). Therefore, in this paper, we chose the keywords “train suspension” and “ticket refund” etc.to measure the consequences of climate risk. Through the above four dimensions, we finally selected 18 keywords for Baidu search volume extraction. In order to avoid the difficulty of dimensionality disaster and information overlapping, this paper adopts the Generalized Dynamic Factor Model (GDFM) for information extraction and synthesis, and constructs a comprehensive Climate Risk Perception Index (RS).

According to the Generalized Dynamic Factor Model proposed by Forni and Lippi (2001). The model is used to analyze the dynamic relationships and co-movements between multiple observed variables, a set of high-dimensional smooth time series can be decomposed into a common becoming

Here,

(4) Control variables

As for the factors affecting the demand for commercial health insurance, in addition to climate risk perception and haze pollution, the following factors have been confirmed in the literature:

Income level of residents (Y): the income of urban population residents, the higher the income of residents, the higher the demand for commercial health insurance. The relevant data are taken as logarithm.

Gender ratio (GR): the ratio of male and female population (female = 100), according to Peng et al. (2021) through the study found that compared to men, women will be more risk averse, so the more inclined to buy insurance.

Price index (INF): the consumer index of the population (with 2000 as the base period), taking into account the change in the monetary value of assets and the influence of the time factor, this paper takes the price index into account, aiming to reduce the uncertainty of consumers’ income and consumption in different periods.

Mortality rate (DR): The higher the mortality rate, the higher the demand for commercial health insurance in the region. This paper uses the population mortality rate of each region as the mortality rate measure.

Urbanization level (UR): it refers to the degree of urbanization achieved by a region, that is, the proportion of the population living in towns and cities to the total population of the region. A high level of urbanization in a region has a positive impact on the development of commercial health insurance in that region.

Elderly dependency ratio (OL): the proportion of the elderly population to the youth population, the higher the demand for insurance among the elderly relative to the youth population. The specific variables are illustrated in Table 1.

Description of Variables.

Descriptive Statistics

Table 2 shows the descriptive statistics of each variable, in which the mean of the logarithm of commercial health insurance density is 6.87 and the standard deviation is 0.84, which shows that the development of commercial health insurance density in China is fast, and there is a large difference in the consumption of commercial health insurance between different regions at the same point in time. Other indicators, such as PM2.5 emissions, climate risk perception, and income level, show similar characteristics to commercial health insurance density, that is, the difference between the maximum and minimum values is large, which also reflects the disparity between different regions in China in terms of economic development level.

Descriptive Statistics of the Sample Data.

Model Construction

Static Model

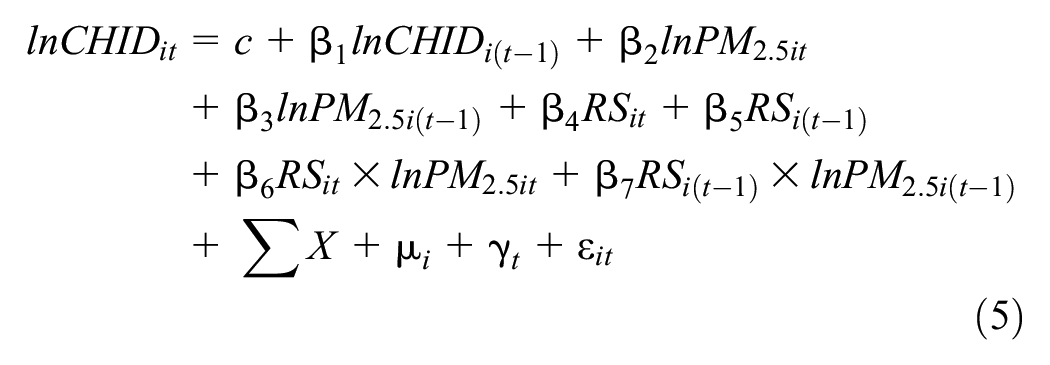

According to the previous analysis, it is known that the information impact of haze pollution will have an impact on the residents’ climate risk perception, so this paper introduces the cross term of climate risk perception and haze pollution indicators (

Since the empirical research in this paper is based on 18 years of data from 31 provinces, the data capacity is small, moreover, there is heterogeneity in the data between provinces and years, so the model setting is uncertain. This paper adopts Hausman test to screen more effective model, by comparing whether there is a significant difference between random effect and fixed effect, if they are significantly the same, then use the random effect model; otherwise, we use the fixed effect model. The results of the Hausman test can be seen, the P-value is 0, indicating that it is very significant, so we should reject the original hypothesis and choose the fixed effect model. The fixed regression model constructed in this paper is as follows:

here, c denotes the constant term;

Dynamic Models

Dynamic model can respond to the main explanatory variables lag one on its own role, can effectively make up for the shortcomings of static model. This paper firstly adopts differential generalized moment estimation (GMM) to reduce the endogeneity problem and solve the interference of the lagged term in the disturbed term, but due to the fact that the generalized differential moment estimation often has the problem of weak instrumental variables in the process of empirical analysis, which is easy to cause the results to be biased. Therefore, this paper solves the problem of weak instrumental variables and reduces the bias of empirical results by making the systematic generalized moments estimation for further empirical analysis. Meanwhile, we adopt the Sargan test to judge the validity of the instrumental variables of Differential GMM and System GMM. The dynamic panel estimation model is as follows:

here c denotes the constant term;

Empirical Analysis

Fixed Effects Regression Results Analysis

Hausman test results Show that p = .0001, so we reject the original hypothesis and adopt the fixed effect model, at the same time, in order to carry out the robustness test, we analyze the model again by using the generalized least squares method (comprehensive FGLS), and the specific results are compared as follows, as shown in Table 3:

Fixed Effects Regression Results.

Note. 1. Stata15 was used for analysis; 2. *, **, and *** indicate passing the significance test at the 10%, 5%, and 1% levels, respectively; t-values in ( ).

In Table 3, according to the regression results analysis, although there are individual differences in both static and dynamic model regression results, the overall are relatively significant. The coefficient of haze pollution (

In addition, climate risk perception is significant for the demand for commercial insurance in both least squares and fixed effects models without cross terms. The estimated coefficient of least squares is 0.225 and the estimated coefficient of fixed effects is 0.031, both significant at the 1% level. This indicates that with the improvement of residents’ climate risk perception, the level of residents’ risk perception will significantly increase, and the demand for commercial health insurance will continue to increase, which is also consistent with the direction of the research findings of Chang et al. (2018): When the level of haze pollution is high, people tend to buy commercial health insurance, that is, haze pollution increases the demand for commercial health insurance. Climate risk perception in this paper refers to a kind of concern and prediction of climate risk events. In the network era, the Internet has changed the way the public obtains and transmits information, especially the use of big data technology has increased dramatically, and the public is able to obtain all kinds of information from the Internet more actively, anytime and anywhere (F. Li & Wang, 2014). The search behavior of residents using internet search engines for certain events or concepts can then be used to measure the level of concern for certain climate risk phenomena and certain concepts. However, it can be seen that the coefficient of climate risk perception is small because of the large order of magnitude difference compared to the insurance purchase index, and therefore the coefficient of climate risk perception is relatively small. The coefficient for PM2.5 emissions is 0.152, a negative coefficient, which is not in line with the current research results and needs to be studied in more depth.

The income level of residents (Y), urbanization level (UR), and population mortality rate (DR) have significant positive driving effects on the demand for commercial health insurance, and the three reflect the influence of income level, climate risk perception, and medical coverage level on the development of commercial health insurance.

The results of the least squares and fixed effects regressions with cross-sectional terms show that climate risk perception is still significant at the 1% level and the coefficient of PM2.5 emissions (

Differential GMM and System GMM Regression Results Analysis

As shown in Table 4, through the generalized difference moment estimation (Difference GMM) model, the coefficient of the lagged first order(

Parameter Estimation Results.

Note. 1. Stata15 was used for analysis; 2. *, **, and *** indicate passing the significance test at the 10%, 5%, and 1% levels, respectively; t-values in ( ).

In summary, the level of climate risk perception as measured by python technique plays a moderating role between haze pollution and the demand for commercial health insurance, and this mechanism well explains the statistical phenomenon that there is a correlation between the demand for commercial health insurance and haze pollution. Specifically, when haze weather occurs frequently, on the one hand, people are exposed to haze pollution, due to the impact of haze pollution and directly increase the demand for commercial health insurance; on the other hand, people through the reptile technology to obtain the knowledge of climate risk, to understand that climate change to the human body brought about by the adverse effects of the awareness of the risk, and ultimately, in order to avoid the health risks, to reduce the economic losses, people are more proactive and motivated to buy commercial health insurance, indirectly increasing the demand for health insurance. The finding of this mechanism is of great significance in promoting the development of China’s commercial health insurance market. Currently, China has fully built a moderately prosperous society, and with the income level of the residents stepping onto a new level, the purchasing power will no longer be the main bottleneck restricting the development of the commercial health insurance market in the future, while strengthening the residents’ awareness of commercial insurance and climate risk prevention will prompt people to utilize commercial insurance as a tool to defend against health risks (J. Cai & Song, 2017).

Spatial Analysis

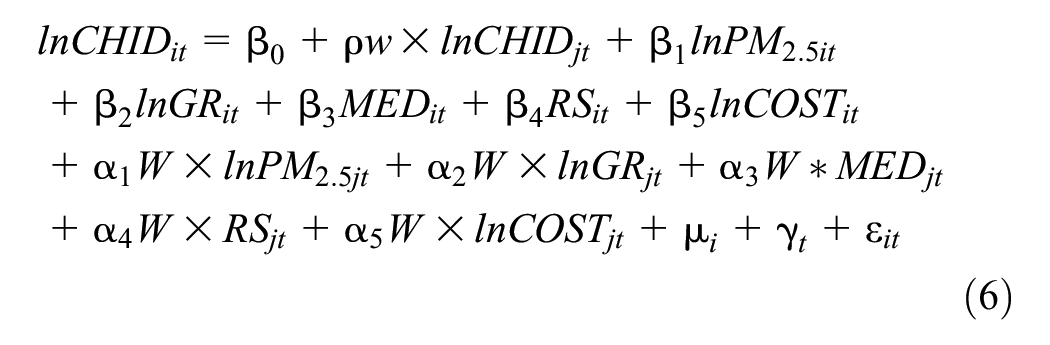

Given the differences in economic level, degree of haze pollution, per capita medical capital in urban areas, and degree of population aging, this paper not only explores the impact of haze pollution on local demand for commercial health insurance, but also further investigates whether there is any spatial interaction of haze pollution on commercial health insurance between regions in China. This paper attempts to construct a spatial Dubin model to further investigate and analyze this issue (Lesage & Pace, 2009). Therefore, this paper adopts the spatial Dubin model constructed by Lesage and Pace (2009), which is a combined extended form of the spatial error model and the spatial lag model. The model has the following advantages: first, as a standard starting point for spatial econometric modeling, the spatial Dubin model is a standard framework for capturing various types of spatial spillovers, and it can be morphed into common spatial lag and spatial error models under different coefficients setting conditions, which makes it more general (Shao et al., 2019; Tian & Zhang, 2013; second, no matter whether the real data generation process is in spatial lag form or spatial error form, the modeler guarantees unbiased estimation of the coefficients; thirdly, it does not impose any limitations on the magnitude of potential spatial spillovers in advance (J. Wu et al., 2017).

The spatial Dubin model for this paper Is as follows:

here

In the selection of spatial matrix, most of the previous literature constructs spatial matrix for geographic distance, this paper draws on B. Wu et.al (2022) in constructing spatial matrix by constructing economic spatial matrix through the inverse of the square of the difference of the mean of capital stock GDP samples. According to the previous section, the impact of haze pollution on the demand for commercial health insurance is closely related to the degree of economic development among regions. Therefore, in this paper, the spatial matrix was constructed by using the economic differences among provinces. Model regression results as shown in Table 5:

Model Estimation Results.

Note. 1. Stata15 was used for analysis; 2. *, **, and *** indicate passing the significance test at the 10%, 5%, and 1% levels, respectively; t-values in ( ).

As can be seen from Table 5, for the nation-wide sample, the direct effect of haze pollution on the development of commercial health insurance is not significant (CHID* is the density of commercial insurance: the ratio of commercial insurance purchases to the population) . From the previous results, it is clear that there is a lagged effect of haze pollution on the development of commercial health insurance. And the spatial spillover effect is significant at 1%, proving that there is a positive spatial spillover effect of haze pollution on the development of commercial health insurance, which is in line with the conclusion of Shao et al. (2016) and verifies hypothesis H3.

The reason may be as follows: in recent years, haze pollution frequently affects the health of residents, and haze pollution in Chinese provinces and regions shows obvious spatial spillover effects and the characteristics of high-emission clubs (Huang & Zhang, 2013), and the areas of high-emission clubs may “leak” haze pollution to other areas through the transfer of high-pollution industries. At the same time, haze pollution will also produce diffusion effects through atmospheric circulation, atmospheric chemistry and other natural factors, and the development of commercial health insurance policies introduced by some local governments as well as the dissemination of media, meanwhile other public opinion to publicize the negative news of haze pollution will produce spatial diffusion, which will result in subsequent spatial spillover effects (Shao et al., 2016). The haze pollution overflow from other regions will have an impact on the development of commercial health insurance in the region, and the development of commercial health insurance in the region will be affected by haze pollution in other regions. Therefore, haze pollution information will be transmitted between regions and indirectly have an impact on the demand for health insurance in other regions.

At the same time, it can be seen from Table 5 that there are differences in the direct impact and spatial spillover effects of the different impacts of haze pollution on the development of commercial health insurance in various regions of China, which is similar to the conclusion of Chang et al. (2018). In the central and western regions, the direct impact of haze pollution on commercial health insurance is not significant in terms of demand of insurance purchase, while the eastern region shows significant demand of insurance purchase. The differences between the three regions may be due to the fact that the eastern region is more economically developed and has a higher demand for insurance, and that residents in the eastern region have a higher level of education and a higher level of knowledge about insurance than the public in the central and western regions. From the point of view of spatial spillover effect, the spatial spillover effect is more significant in the eastern and central regions than in the western region, especially in the central region where the spatial spillover effect of haze pollution on the development of commercial health insurance is the most significant. This may be due to the following reasons: firstly, the economic development level of these two regions is more developed than the western region, the residents have higher income and higher education level, and the insurance market is more mature, therefore, the residents’ climate risk perception and risk aversion are higher; secondly, the industries in the central and eastern regions are more developed than the western region, and there are more polluting enterprises, and the haze pollution is relatively more serious, causing a greater impact on the physical health of residents, which is similar to the conclusion of Chang et al. (2018).

Conclusions and Policy Recommendations

Conclusion

The current haze pollution has had a significant impact on public health in China. Along with the improvement of climate risk awareness, Chinese residents have a more objective understanding of commercial health insurance and their willingness to purchase it is increasing rapidly. Based on the panel data of 31 provinces from 2005 to 2022, this paper concludes that (1) haze pollution has a significant lagged positive effect on the demand for commercial health insurance, and inhibits the consumption of commercial health insurance in the current period. (2) Further, residents’ climate risk perception plays a moderating role between haze pollution and commercial health insurance demand; (3) there is a positive spatial spillover effect between haze pollution and commercial health insurance development among provinces. In terms of regions, the central and eastern regions are more seriously affected by haze than the western region, so the spatial spillover effect in the eastern and central regions is larger than that in the western region.

Policy Recommendations

Combined with the above research conclusions, the haze pollution has already had a certain impact on the health of Chinese residents, although the risk perception ability of Chinese residents has been greatly enhanced, and the demand for commercial health insurance has been strengthened, but there is still a huge potential for the development of commercial health insurance. As far as the current commercial health insurance market is concerned, commercial health insurance has a huge space for development, but it needs the joint efforts of many parties. In order to promote the importance of commercial health insurance in maintaining social stability, improving the healthcare system, and supporting and supplementing social healthcare insurance, etc., this paper combines the findings of the empirical research and puts forward the following policy recommendations from three levels: the public, insurance companies and the government:

(1) From the public aspect. On the one hand, the education of the population on health risk management should be strengthened, and the public media should intensify their publicity efforts on the concept of commercial health protection. The results of this study show that in the long run, increased perception of climate risk can strongly stimulate the growth of Chinese residents’ commercial health insurance consumption, so it is particularly important to strengthen publicity, enhance residents’ perception of climate risk, and provide residents with health risk management products and information; On the other hand, in the highly connected information era, people are more sensitive to the perception of climate risk, and we should accurately grasp the characteristics of residents’ needs, make full use of the advantages of the information age, and strengthen the popularization of science and education, so as to further promote the enthusiasm of the residents to safeguard own health through the insurance .

(2) From the insurance company aspect, on the one hand, the insurance market is an “invisible” hand that allows commercial insurance companies to add vitality to China’s health insurance market, for example, through the construction of a medical data platform, medical institutions and insurance companies can realize data co-building, -sharing, and -utilization, so as to provide a decision-making basis and data support for the insurance company’s development. On the other hand, precise design and development of health products. Research results show that in the long run, haze pollution has a significant positive driving effect on commercial health insurance demand, and may gradually differentiate by regional geography and industries. Thus, precisely customized regional products may gain advantages in market segments.

(3) From the national and local government aspect, the government needs to improve the top-level design in the system. Therefore, on the one hand, a haze pollution prevention and control system should be established. The significant spatial spillover effect of haze pollution on the demand for commercial health insurance warns us that ignoring the spillover effect between regions will seriously underestimate the adverse health impacts of haze pollution on the human body, haze management should be a joint prevention and control system, insisting that provinces and cities develop a highly efficient mechanism of coordinated management, so as to avoid being trapped in a “each one for himself” dilemma and jointly win the “battle to protect the blue sky”; On the other hand, the government needs to change the economic development mode to solve the increasingly serious haze pollution problem, . It should establish market-incentivized environmental regulations to promote the upgrading of industrial structure, set up corresponding long-term mechanisms to maintain the consistency of environmental regulation policies, increase environmental protection investment, improve the compensation system for ecological damages.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is supported by “Research Center for Ecological Civilization and Green Development of Shenzhen University,” the key research base of humanities and social sciences in Shenzhen (project number: 2020001); This paper is supported by the National Social Science Foundation “Research on the Thought of Ecological Civilization” (Project No.: 18ZDA004).

Consent to Publish

All the authors are consent to publish.

Data Availability

The data can be got on the request of the author.