Abstract

This research explores the moderating effect of institutional ownership on the relationship between audit committee attributes and audit report lag. The paper sampled data from 102 Saudi non-financial listed firms from 2012 to 2021. The data was analyzed using a fixed effect regression, while the generalized method of moments approach (GMM) was employed for robustness check. The research finding strongly suggests that the audit committee size may increase audit report lag. In contrast, it was found that audit committee independence and financial expertise may reduce audit report lag. In addition, the interaction effect reveals that the impact of audit committee financial expertise and the committee meetings on reducing audit report lag may be higher as institutional shareholding rises. Thus, the outcome validates the agency theory perspective that the active monitoring of institutional investors may shape firms’ internal governance systems. More importantly, the finding implies that firms should prefer a smaller audit size with a higher ratio of independent directors and financial experts to improve financial reporting quality. They should also embrace institutional shareholding to reduce audit report lag. Thus, lowering audit report lag may mitigate information disparity between firms and prospective investors, reducing agency conflicts and boosting firm value.

Introduction

Audit report lag is the time between a firm’s financial year end and the auditor’s report date (Agyei-Mensah, 2018; Farumi et al., 2023). It is regarded as one of the qualitative characteristics of financial reporting, which means making information available to the accounting information users when due (Abernathy et al., 2017; Ishak & Nugraha, 2023). Companies should have a shorter audit report lag because timeliness appears to be an essential determinant of firms’ governance quality (Singh et al., 2022). This information should be timely, enabling financial statement users to make informed decisions. Similarly, financial reporting guidelines globally have emphasized the significance of minimizing audit report lag in enhancing transparency in firms’ governance (Oradi, 2021; Singh et al., 2022). Importantly, investors, regulators, policymakers, and academics have given much attention to audit report lag because of the need to minimize information asymmetry and promote corporate disclosure. Therefore, understanding the factors influencing companies’ audit report lag remained crucial.

Furthermore, one of the oversight duties of the board of directors is to oversee companies’ financial reporting system through an audit committee (Alsheikh & Alsheikh, 2023; Alzeban, 2020; Chronopoulos et al., 2024; Klein, 2002). In particular, the studies reported that audit committee mechanisms might enhance the internal control system and minimize external auditors’ queries, leading to shorter audit report lag (Al-ahdal & Hashim, 2022; Alqatamin, 2018; Farumi et al., 2023). However, a strand of the literature on this context document contradictory findings (Abernathy et al., 2017; Al-ahdal & Hashim, 2022; Alfraih, 2016; Buallay & Al-Ajmi, 2019; Chen et al., 2022; Lee & Park, 2019; Oussii & Boulila Taktak, 2018).

These inconsistent empirical findings have made researchers and policymakers raise further questions about when the audit committee influences firms’ audit report lag. This research finds it compelling to explore what may likely account for these divergent views. Therefore, based on the agency argument, this study exploits institutional ownership as a moderator variable. This perspective believes that institutional investors may complement the board of directors’ monitoring role because of their expertise and financial skill, particularly in an environment with ineffective markets for corporate control (Boshnak, 2023b; Gillan, 2006; Guo & Platikanov, 2019; Jensen, 1989). Hence, this study examines the moderating effect of institutional ownership on the relationship between audit committee composition and audit report lag of Saudi non-financial listed firms.

Consequently, the study contributes to the literature in different ways. First, this research strongly suggests that Saudi firms may reduce audit report lag as the number of independent directors and financial experts on their audit committees rises. This evidence provides additional insights into the ongoing arguments on how board financial expertise may influence audit report lag, thus contributing to the board diversity literature. Most importantly, the moderation analysis reveals that the impact of audit committee meetings and financial experts in minimizing audit report lag may be greater as institutional shareholding increases. This implies that interaction between the audit committee and institutional investors may yield a robust control mechanism that can compel firms to minimize audit report lag. This approach may enhance financial reporting quality, particularly in emerging economies with less developed institutional frameworks. Therefore, the evidence provides new insight into the factors improving corporate governance quality.

This paper proceeds as follows: Section two focuses on the Saudi institutional background, and the next part presents a literature review, followed by the research methodology, discussion of regression results and robustness check. Finally, the last segment concludes the paper.

Saudi Institutional Background

Saudi is an emerging country, and it is located in the Southwest of the Asian region. The country practices Islamic teachings and a kingship political system, in which the King is the prime minister and head of state (Albassam, 2015; Tawfik et al., 2022). The oil sector is the pillar of the Saudi Arabian economy, and some studies estimated that the nation supplies about 35% of the international oil market (Bajaher et al., 2022; Sulimany, 2023). Also, the country’s stock market seems to be the biggest and the most liquid among the Middle East and North Africa (MENA) countries (Boshnak, 2023b; Sarhan et al., 2019). Government and family ownership are prevalent in the Saudi corporate environment, thus indicating lesser involvement of institutional investors (Al-Bassam et al., 2018; Boshnak, 2023a). The country adopted a corporate governance code (CGC) in 2006, and further amendments were made in 2017 to align with internal best practices, attract more foreign direct investment and enhance capital market performance (Al-Bassam et al., 2018; Sulimany, 2023).

However, it is reported that in Saudi, greater attention is attached to family values, informal relationships and Islamic teachings (Sulimany, 2023). In this way, the corporate bodies operating in the country may rely less on formal accountability mechanisms, such as the board of directors, when designing important decisions (Alregab, 2021; Sarhan et al., 2019). Although the capital market regulation in Saudi requires firms to disclose their audited financial statements within 3 months (90 days), but a substantial number of Saudi firms appear not to strictly adhere to this requirement (Borgi et al., 2021; Ebaid, 2022; Sulimany, 2023). Specifically, Alsheikh and Alsheikh (2023) reported that some Saudi firms have a lag of 197 days, while Borgi et al. (2021) stated that companies in Saudi have up to 323 lag period, which are far greater than the allowable time. This no-compliance reinforces the argument that the Saudi corporate sector is associated with ineffective markets for corporate control that can discipline managers and ensure strict adherence to corporate governance principles (Alregab, 2021; Ebaid, 2022). These instances may pave the way for managers to be highly entrenched, undermine corporate boards’ monitoring capacity and weaken the firms’ financial reporting system. Also, this low institutional quality suggests the need for a more robust control mechanism to complement the board of directors’ monitoring role for greater disclosure in firms’ governance in Saudi. Therefore, this study would serve as a research base framework that companies could utilize to reduce audit report lag, thereby strengthening financial reporting quality.

Importantly, the Saudi corporate sector is undergoing reforms to actualize its vision for 2030 aimed at revenue diversification and attracting more foreign direct investment (Alregab, 2021; Sulimany, 2023). Also, the reforms intend to salvage the country from heavy dependence on oil revenue. The stock market (Tadawul) is now open to foreign investors. Other essential bodies that support CGC compliance include the capital market authority (CMA) and the Saudi Organisation for certified public accountants (SOCPA). These organs regulate the Saudi stock market and monitor firms’ accounting and auditing activities for effective corporate disclosure (Boshnak, Alsharif, & Alharthi, 2023; Sarhan et al., 2019).

Literature Review

The literature review section is classified into theoretical framework and review of prior studies for hypotheses development.

Theoretical Framework

Agency theory predicts that conflict may arise due to the separation between owners and managers in the modern organizational set-up (Bathala & Rao, 1995; Jensen & Meckling, 1976). This dispute may create information disparity between shareholders and management, thus paving the way for incurring agency costs (Bazhair, 2023; Rashid, 2016). One of the control mechanisms suggested by this framework is constituting a board of directors to oversee firms’ internal governance (Alves, 2023; Fama & Jensen, 1983; Uĝurlu, 2000). The board of directors is to monitor management proposals to ensure that shareholders’ interests are protected (Thi, 2023). Accordingly, the audit committee is a sub-committee of the board of directors. Its primary purpose is to strengthen firms’ internal control system by enhancing the quality of their financial reporting system (Chronopoulos et al., 2024; Musallam, 2020). Effective monitoring from the audit committee may control managers’ opportunistic attitude and promote disclosure due to robust scrutiny (Abbas & Frihatni, 2023; Al-ahdal & Hashim, 2022). The committee control mechanisms may enable firms to design conservative accounting systems and detect internal control weaknesses, thereby reducing audit report lag (Alfraih, 2016; Durand, 2019; Farumi et al., 2023). In sum, sound control mechanisms from the audit committee composition may minimize agency conflicts and enhance financial reporting quality, thus boosting the external auditors’ confidence in firms’ internal control system.

Moreover, from the perspective of the resource dependency theory, the audit committee’s advisory role may influence audit report lag. According to this theory, the board of directors are composed to advise and link organizations to external resources they need for their growth and development (Di Vaio et al., 2023; Drees & Heugens, 2013; Pfeffer, 1973). Since the audit committee is a sub-committee of the board, its composition may provide an advisory role in its dealings with internal audit units. The committee may also mediate between internal and external auditors in the event of disagreements (Abbas & Frihatni, 2023; Baatwah et al., 2015). Further, several studies evaluated the audit committee’s role in providing valuable suggestions on external auditors’ engagement, and offering expert advice that can remedy internal control deficiencies (Chronopoulos et al., 2024; Mitra et al., 2012). Within this context, it is argued that an audit committee composition with a higher ratio of independent directors and financial experts is more likely to resolve financial reporting lapses due to the crucial advice from these directors (Abernathy et al., 2013; Alsheikh & Alsheikh, 2023; Baatwah et al., 2015). Overall, the audit committee advisory role may have a bearing on firms’ financial reporting systems and lowering audit report lag.

Empirical Review and Hypotheses Development

Audit Committee Size

The audit committee size is the number of persons that formed the committee (Fariha et al., 2022; Sulimany, 2023). It is stated that the audit committee is a determinant of corporate governance quality (Lajmi & Yab, 2022). A series of arguments were recorded regarding the nexus between audit committee size and audit report lag (Buallay & Al-Ajmi, 2019; Ishak & Nugraha, 2023). Within the resource dependency view, a larger audit committee may result in greater diversity and breadth of expertise that may enrich the decision-making ability of the committee (Detthamrong et al., 2017; Fariha et al., 2022; Othuon et al., 2023). Also, the advisory role of the committee may be enhanced due to the diverse skills and knowledge gained from large committee members (Ben Barka & Legendre, 2017). Given that, a larger audit committee may shape firms’ financial reporting systems and reduce external audit queries, leading to shorter audit report lag (Durand, 2019; Farumi et al., 2023; Oussii & Boulila Taktak, 2018).

On the other hand, some studies stated that a smaller audit committee size is more suitable for minimizing audit report lag. According to the agency theory, a larger audit committee may lead to conflicts and a lack of cohesion among the members because of communication differences and cognitive conflict (Alfraih, 2016; Ishak & Nugraha, 2023). These instances may lessen the committee’s effectiveness in scrutinizing financial reports, thereby widening the scope of the external audit work. Hence, the external auditor may require a longer time to examine financial records, resulting in a longer audit report lag (Farumi et al., 2023; Oradi, 2021). More importantly, the Saudi corporate governance framework suggests that an audit committee should have a minimum of three and a maximum of five members (Y. A. Al-Matari, 2022). This pronouncement implies that the code supports a smaller audit committee size due to its effectiveness in strengthening firms’ internal control systems. Based on the agency framework, a smaller audit committee size may be more efficient due to lesser conflict and greater cohesion among members (Chronopoulos et al., 2024; Klein, 2002). This effectiveness associated with a smaller audit committee may ensure careful monitoring, minimize financial misstatements, and reducing audit report lag. Therefore, as audit committee members increase, the time taken to release financial information (audit report lag) may be longer due to the inefficiency associated with a larger audit committee. Given that, the following hypothesis is stated:

Audit Committee Meetings

Audit committee meetings refer to the number of meetings members hold in a particular accounting year (Bazhair, 2022; Ishak & Nugraha, 2023). Audit committee meetings frequency indicates the involvement level of the committee in firms’ financial reporting processes (Chronopoulos et al., 2024; Klein, 2002). According to agency literature, frequent meetings may help audit committee members understand firms’ internal control strength and financial reporting quality (E. M. Al-Matari, 2019; Alsheikh & Alsheikh, 2023). Also, it is reported that regular meetings may help reduce financial reporting errors or misstatements, thus strengthening internal governance mechanisms (Alfraih, 2016). Similarly, prior studies indicated that audit committee diligence makes the committee more active in detecting earning management practices and internal control weaknesses (Oussii & Boulila Taktak, 2018). Therefore, studies found that regular meetings may lessen audit queries due to frequent monitoring from the audit committee (Alfraih, 2016; Ishak & Nugraha, 2023). Thus, audit committee monitoring may be enhanced due to regular meetings, which may boost internal control quality. Consequently, robust internal control may increase the confidence of external auditors in firms’ financial systems. This improved confidence may lead to lower audit report lag because auditors require less time scrutinizing financial records. Based on these discussions, the following hypothesis is designed:

Audit Committee Independence

Audit committee independence is also another attribute that can influence audit reporting lag. Independent directors are members of the board of directors who are not under the control of managers (Bazhair, 2023; Kallamu & Saat, 2015). Independent directors are usually employed due to their goodwill and reputations (Musallam, 2020; Sani, 2020). Hence, many studies emphasized that an audit committee tends to be more robust and effective when composed of more independent directors (Klein, 2002; Shan, 2019). Based on the resource dependency perspective, these directors provide an essential advisory role to firms (Nwude & Nwude, 2021; Othuon et al., 2023). In addition, within the context of the agency theory, it is argued that the presence of these directors on the audit committee may enhance the committee’s monitoring capacity and boost firms’ internal control (Dang & Nguyen, 2022; Haji, 2015). Accordingly, prior studies indicated a negative relationship between audit committee independence and audit report lag (Abernathy et al., 2017; Chen et al., 2022). Drawing from these theories, stringent monitoring and strategic advice from a highly independent audit committee may shape firms’ internal control systems and minimize audit queries, leading to shorter audit report lag. Given this presentation, the following hypothesis is formulated:

Audit Committee Financial Expertise

The literature argues that financial expertise involves acquiring knowledge or experience in finance and accounting-related jobs (Ali et al., 2022; Sani, 2021). Accordingly, it is reported that one of the audit committee’s primary mandates is overseeing organizations’ accounting systems and financial reporting processes (Abbas & Frihatni, 2023; Klein, 2002). Studies indicated that an audit committee with accounting and finance experts might likely be more effective and robust in discharging its duties (Baatwah et al., 2015; Özer & Merter, 2023). The agency and resource dependency theories emphasize that financial experts in the audit committee have the incentives to evaluate the weaknesses and strengths of firms’ internal control systems of their educational backgrounds (Alcaide-Ruiz & Bravo-Urquiza, 2023; Davidson et al., 2004). Their presence may assist the committee in designing appropriate policies to enhance financial reporting quality (Buallay & Al-Ajmi, 2019). In addition, it is reported that audit committees with financial experts usually adopt conservative accounting policies, and their monitoring capacity may mitigate earning management practices (Lee & Park, 2019). Therefore, these particular attributes of financial experts may enhance the reliance and confidence of external auditors on firms’ internal control (Abernathy et al., 2013). Thus, auditors require a shorter time to evaluate firms’ financial position, resulting in lower audit report lag. Given that, the following hypothesis is derived:

Institutional Ownership

The literature considers institutional ownership as an important corporate governance mechanism. Examples of these investors include banks, insurance firms, investment companies and pension funds. These investors are relatively more active in monitoring the actions of managers because of their keen interest in maximizing their investment value (AbdulJalil & AbdulRahman, 2010; Boshnak, 2023b; Jensen, 1989). These investors closely monitor managers’ policies and scrutinize their proposals extensively due to their sophisticated financial expertise and management skills (Ledi & Ameza – Xemalordzo, 2023; Switzer & Wang, 2017). They usually design prudent investment strategies and monitor managers to ensure their plans are actualized. In this context, Agency literature suggests that institutional investors play a vital role in remediating firms’ internal control lapses and improving internal control quality (Le & Nguyen, 2023; Ma, 2020; Tee, 2019). Consequently, companies with a higher ratio of institutional investors may minimize financial misstatements, thus reducing financial reporting lag (Basuony et al., 2016; Mitra et al., 2012). Given this explanation, the following hypothesis is designed:

Moderating Role of Institutional Ownership

The justification for choosing institutional ownership as a moderator variable is based on the agency theory argument that these investors may shape firms’ internal governance system (Boshnak, 2023b; Jensen, 1989). According to this perspective, institutional investors’ presence in a firm can mitigate managers’ opportunistic behavior because of their active monitoring (Y. A. Al-Matari, 2022; Al-Sartawi & Sanad, 2019). Institutional investors usually pressure managers to disclose vital information to the public and exercise due diligence when scrutinizing management proposals (Basuony et al., 2016; Le & Nguyen, 2023). This high disclosure may reduce the information gap between firms and outsiders, thereby mitigating agency conflicts (Ledi & Ameza – Xemalordzo, 2023). They have a fiduciary role in firms’ governance and may use their voting power to influence board compositions (Boshnak, 2023b; Thi, 2023). In addition, many studies reported that institutional investors preferred investing in firms with sound corporate governance (Switzer & Wang, 2017; Wang & Shailer, 2018). Similarly, studies showed that audit committee oversight functions are more likely to be robust because of the active involvement of institutional monitoring (Bataineh, 2021; Guo & Platikanov, 2019). Therefore, an audit committee is a crucial governance mechanism that may shape firms’ internal audit functions and lead to a lower audit report lag (Abernathy et al., 2017; Chen et al., 2022; Özer & Merter, 2023). On the other hand, it is established that stringent monitoring from institutional investors may equally minimize financial misstatements, lower audit queries, and thus reducing financial reporting lag (Basuony et al., 2016; Mitra et al., 2012). Given these findings, this paper assumes that the audit committee’s effectiveness may likely increase as institutional ownership increases. Hence, the following predictions are stated:

Methodology

Sample Size and Data Gathering

The population of this research covers 198 Saudi-listed companies as of 31st December 2021. The research data spanned from 2012 to 2021 because, within this period, the Saudi stock market experienced several transformations that may impact financial disclosure. For instance, the Saudi corporate environment adopted international financial reporting (IFRS) and other capital market reforms (Alregab, 2021; Ebaid, 2022). Moreover, the paper focuses on the non-financial listed firms, and its sample was created in the following manner. Firstly, financial companies were excluded from the selection because of their peculiar financial reporting systems (Ebaid, 2022; Rajan & Zingales, 1995). Given that, a total of 42 Banks and insurance firms were dropped. Further, 22 companies with substantial missing data were step-downed from the study sample. Also, companies listed after 2012 and those that merged within the study period were not considered, leading to the exclusion of other 32 firms from the sample. Hence, Table 1 displays the sample distribution across the companies from 2012 to 2021.

Sample Distribution.

Overall, the final sample comprised the data of 102 Saudi non-financial companies from 15 sectors. Additionally, the data for this research was gathered from three sources. More specifically, the firm-level data were obtained from the Saudi stock exchange website and the Eikon data stream. Likewise, the corporate governance-related data were generated from the sampled firms’ annual reports.

Study Variables and Their Measurements

The main explanatory variables in this article are audit committee size (ACS), audit committee meetings (ACM), Audit committee independence (ACI) and audit committee financial expertise (ACFE). This study focuses on these attributes because they are the most common proxies used when examining the effectiveness of audit committee oversight duties. The dependent variable is audit report lag (ARL). Also, the research employed institutional ownership (IO) as a moderating variable. The justification for using this variable as a moderator is to test its monitoring capacity, as advocated by the agency literature (Jensen, 1989). This theory argues that institutional investors might shape firms’ internal governance systems due to their financial expertise and management skills (Bataineh, 2021; Guo & Platikanov, 2019). Thus, this study expects that the audit committee oversight functions are more likely to be robust because of the stringent monitoring of these investors.

Moreover, the study employed firm size (FS), leverage (LEV), profitability (ROA) and audit type (AT) as control variables. Previous studies indicated that these variables might influence audit report lag (Al-ahdal & Hashim, 2022; Basuony et al., 2016). Therefore, using these variables in this research may reduce specification bias and assist in empowering the specified model. In particular, it is argued that larger companies may have more robust internal control systems because of their track records that external auditors may rely upon, resulting in shorter audit report lag (Alfraih, 2016; Oussii & Boulila Taktak, 2018). Hence, a negative association between FS and audit report lag is anticipated. Also, leverage may influence audit report lag. In this regard, studies reported that creditors pressure firms to embrace high disclosure as a monitoring mechanism (Basuony et al., 2016; Ebaid, 2022). Therefore, high leverage may constrain companies to release their financial position timelier to boost creditors’ confidence. Hence, this research expects a negative association between LEV and audit report lag.

In addition, several studies reported that profitable companies have lower audit report lag because disclosing higher profitability is good news to the public (Baatwah et al., 2015; Ebaid, 2022). In this way, this paper supports a positive relationship between ROA and audit report lag. Concerning auditor type (AT) and audit report lag, empirical evidence suggests that companies audited by the Big 4 may have shorter audit lag because of the efficiency and expertise of these audit firms (Alfraih, 2016; Chen et al., 2022). These audit firms are more experienced, employ more staff, and have better access to resources and audit technology than their counterparts (Al-ahdal & Hashim, 2022; Basuony et al., 2016). So, they are more likely to complete their assignment faster, thus reducing audit report lag. Therefore, this study expects a negative link between AT and audit report lag. Table 2 displays the measurements of these variables as used by prior studies.

Measurement of the Variables.

Analytical Model

The structure of the research data makes it imperative to employ the panel data method. Panel data involves an examination of the behavior of cross-sectional units over many periods (Pesaran, 2015; Wooldridge, 2002). This methodology generates more data points, reduces multicollinearity and improves the econometric estimations’ efficiency (Hsiao, 1985). The commonly used panel data methods include Pooled OLS, random and fixed effects. However, OLS may be associated with omitted variable bias because the estimator ignores firm-specific effects (Wooldridge, 2002). Thus, it may yield an inconsistent estimate. Given that, this study conducted a Hausman test to determine the proper panel data method for this research besides OLS. The condition for this test is that if the p-value of the Hausman test is statistically significant at 5%, then the fixed effects model is more appropriate. However, the random effects estimator is more robust if the Hausman test is insignificant at that level. The Hausman test results show a significant p-value (prob > chi2 = .000). Hence, the Hausman test supports the suitability of the fixed effects technique in this study.

Model Development

This study adopts a fixed effect framework based on the Hausman test specification. The baseline mode for the fixed effects model is given as follows:

Fixed Effects

The subscripts i and t capture the cross-sectional and time-series dimensions, respectively. The variable

Hence, by applying the study variables into Equation 1, the following model is specified for the direct relationship:

Furthermore, to measure the moderating effect, we employed the standard moderation model developed by Fairchild and Mackinnon (2009), which is given as follows:

Where: Y represents the dependent variable,

Thus, according to Aguinis et al. (2017), the moderation effect arises when the interaction term coefficient is statistically significant.

Empirical Analysis and Discussion

This section shows the results generated. First, the presentation starts with a descriptive analysis in Table 3, then the correlation results in Table 4. Further, Table 5 displays the main regression results, and finally, Table 6 contains additional regression analysis using the GMM technique for robustness check.

Descriptive Analysis.

Note. ARL = audit report lag; ACS = audit committee size; ACM = audit committee meetings; ACI = audit committee independence; ACFE = audit committee financial expertise; AT = auditor type; FS = firm size; LEV = leverage; ROA = return on assets; IO = institutional ownership.

Correlation Results.

ARL = audit report lag; ACS = audit committee size; ACM = audit committee meetings; ACI = audit committee independence; ACFE = audit committee financial expertise; AT = auditor type; FS = firm size; LEV = leverage; ROA = return on assets; IO = institutional ownership.

Indicate significance at 1%, 5%, and 10%, respectively.

Regression Results (Fixed Effects).

Note. Model (1) presents the regression estimates of the direct relationship between audit committee attributes and financial reporting lag, while model (2) displays the interaction effect results. The numbers in parentheses are standard errors robust to heteroscedasticity. See Table 2 for variables definitions. ARL = audit report lag; ACS = audit committee size; ACM = audit committee meetings; ACI = audit committee independence; ACFE = audit committee financial expertise; AT = auditor type; FS = firm size; LEV = leverage; ROA = return on assets; IO = institutional ownership.

, **, & * Indicate significance at 1%, 5%, and 10% respectively.

Regression Results (2-Step System GMM).

Note. Model (1) presents the regression estimates of the direct relationship between audit committee attributes and financial reporting lag, while model (2) displays the interaction effect results. The numbers in parentheses are standard errors robust to heteroscedasticity. See Table 2 for variables definitions. ARL = audit report lag; ACS = audit committee size; ACM = audit committee meetings; ACI = audit committee independence; ACFE = audit committee financial expertise; AT = auditor type; FS = firm size; LEV = leverage; ROA = return on assets; IO = institutional ownership.

, & *** Show significance level @ 1%, 5%, and 10%, respectively.

Descriptive Analysis

Table 3 presents the study variables’ descriptive statistics. ARL represents the firms’ audit report lag in days and has a mean value of 58 days with a minimum and maximum of 5 days and 209 days, respectively. The average lag period reported in this study appears consistent with Ebaid (2022), who also revealed an average of 58 days for Saudi firms. However, it is slightly higher than the 74 days average recorded by Alsheikh and Alsheikh (2023) in the country, and 69 lag period on the average for firms in Kuwait (Almutawa & Suwaidan, 2022). The audit committee size (ACS) indicates an average of approximately four persons, with a maximum and minimum of five (5) and three (3) members, respectively. Concerning the audit committee meetings (ACM), the statistics indicate that the firms held six meetings per annum on average. Audit committee independence (ACI) is the ratio of independent directors on the firms’ audit committees, revealing a mean of 52.6%. Therefore, it implies that, on average, independent directors dominate the audit committees of Saudi non-financial companies. Audit committee financial expertise (ACFE) registers a mean of 56.9%. Firm size (FS) discloses a maximum and minimum ratio of 14.040 and 7.290, respectively.

Moreover, Table 3 indicates that debt financing (LEV), representing the firms’ total debt ratio, has a mean value of 0.220. This finding suggests that 22% of the firms’ total assets were financed by debt. On average, the return on assets ratio (ROA) displays 5.5% profit before tax across the sampled firms. Further, the variable auditor type (AT) shows a mean of 0.553. This evidence indicates that Big Four audit firms audit 55.3% of the Saudi firms, while the non-Big Four audited about 44.7% within the period under analysis. Lastly, institutional ownership (IO) reveals a mean value of 0.114, thus showing that the firms’ institutional shareholding stood at 11.4% on average.

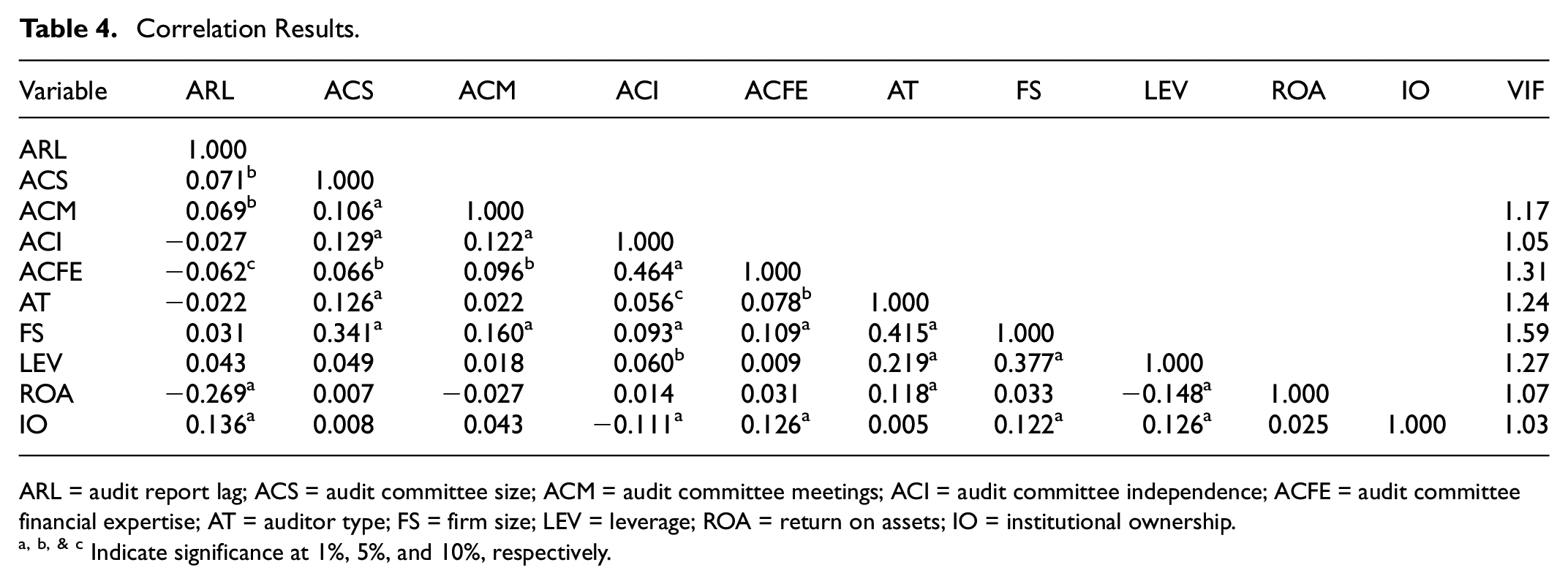

Correlation Analysis

On the other hand, Table 4 reveals the correlation analysis of the variables in the specified model. According to Gujarati and Porter (2010), multicollinearity arises when the correlation between explanatory variables is above 80%. Accordingly, the evidence from Table 4 illustrates that the variables in the specified model are not highly associated with each other. Furthermore, the results show 46.4% as the highest correlation among the explanatory variables between audit committee financial expertise (ACFE) and independence (ACI). Hence, the outcome discloses that the multicollinearity issue is absent in this study.

Regression Analysis

Some diagnostics tests were conducted before running the fixed effect in order to generate a more robust and reliable regression outcome. First, the multicollinearity among the variables was tested using the variance inflation factor (VIF). The VIF values in this study ranged from 1.03 to 1.59, suggesting the non-existence of multicollinearity in the specified model (Gujarati & Porter, 2010). Further, this study employed a Breusch-Pagan test to investigate whether heteroscedasticity exists in the specified model. The p-value of this test exhibits significant results (Prob > chi2 = .000), indicating the presence of heteroscedasticity in the research model (Baltagi, 2005; White, 1980). Also, this research applied a Wooldridge Lagrange-Multiplier (LM) test to detect whether the research model suffers from a serial correlation problem. The p-value of this test appears significant (Prob > f = .004), showing the existence of serial correlation in the model (Drukker, 2003; Hoechle, 2007). Consequently, this study applied robust regression to address these statistical issues.

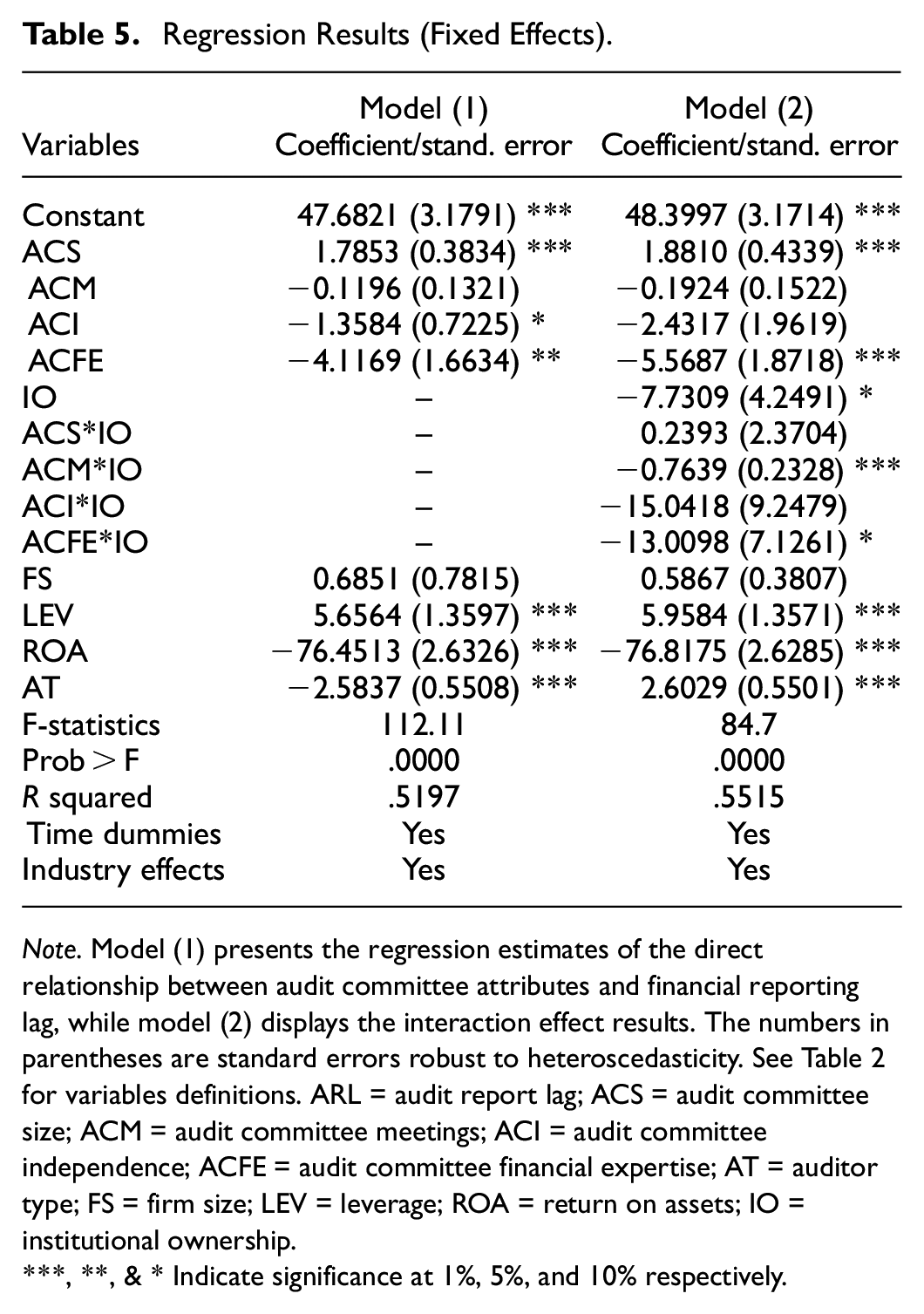

Table 5 shows the main regression results using the fixed effect technique. Model (1) focuses on the direct relationship between audit committee attributes and audit report lag. Model (2) is on the moderating effect, where the moderator variable and interaction terms were inserted. According to the model (1) results, audit committee size is positively associated with audit report lag at a 1% significance level. Thus, the evidence supports

Furthermore, the control variables in the model (1) indicate that firm size exerts an insignificant positive impact on audit report lag. This evidence suggests lesser support for the proposition that larger companies may possess more robust internal control systems that external auditors may rely upon, resulting in lower audit report lag (Alfraih, 2016; Oussii & Boulila Taktak, 2018). In contrast, this research found a strong positive relationship between leverage and audit report lag. This finding implies that high gearing may increase the Saudi companies’ audit report lag. The result contradicts Basuony et al. (2016) and Ebaid (2022), who emphasize that high leverage may pressure companies to release their financial statements timely to boost creditors’ confidence regarding their ability to repay such debts. The regression results also reveal that profitable firms may have a shorter audit report lag because disclosing higher profitability is good news to the public (Baatwah et al., 2015; Ebaid, 2022). Finally, this study found that Saudi firms audited by the Big Four are likelier to have shorter audit lag. The evidence supports the conclusion that Big Four audit firms are relatively more efficient, employ more staff, and have better access to resources and audit technology than their counterparts (Al-ahdal & Hashim, 2022; Basuony et al., 2016). Therefore, firms audited by the Big Four may have lower audit report lag.

Moreover, the moderation analysis is presented in the model (2). The essence of this analysis is to examine how the moderator variable and the interaction terms may influence financial reporting lag. The evidence suggests that the moderator variable (institutional ownership) exerts a significant adverse effect on audit report lag, supporting

Additional Analysis

This study provides further empirical analysis for robustness check using the generalized method of moments (GMM). This analysis is also classified into model (1) for the direct relationship and model (2) for moderating effects. Specifically, GMM was employed because the technique is relatively more robust than the fixed effect approach (Blundell & Bond, 2000; Fitzgerald & Ryan, 2019; Habimana, 2017). GMM is a dynamic panel data estimator that uses an instrumental variable approach to address causality effects and control unobserved heterogeneity (Arellano & Bover, 1995; Ozkan, 2001). Also, this regression technique utilizes the lag-dependent variable as an instrument, thereby enhancing the consistency of the econometric estimates (Roodman, 2009). It is a dynamic model because the regression approach assumes that a dependent variable’s past is an essential explanatory variable in determining its present behavior (Habimana, 2017). The paper used the system GMM because it is more efficient and consistent than the difference GMM (Arellano & Bover, 1995; Ozkan, 2001). Notably, the Sargan / Hansen statistics and AR (2) are parameters widely used to gage the validity and reliability of GMM estimates (Arellano & Bond, 1991). The GMM results in Table 6 have satisfied these basic assumptions because the Hansen statistics and AR (2) appear insignificant. This evidence indicates that the instruments used are robust, and the specified model is free of the second-order serial correlation. Furthermore, the GMM results suggest that the lagged dependent variable (ARLi, t-1) coefficient is positive and significant at the 1% level. This finding indicates that the specified model is dynamic, thus confirming that Saudi companies adjust their financial reporting processes to lower audit report lag.

Additionally, the GMM estimates in Table 6 look consistent with that of the fixed effect results in Table 5. The direct relationship in the model (1) still suggests that audit committee size exerts a strong positive effect on audit report lag. Also, audit committee independence and financial expertise maintain their negative impact. The interaction effects results in model (2) equally indicate that institutional ownership moderates the effect of audit committee meetings and financial expertise on audit report lag. Overall, the empirical evidence using fixed effects and GMM regression methods appears robust.

Conclusion

This study explores the moderating role of institutional ownership on the relationship between audit committee attributes and audit report lag. The study sampled data from 102 companies from 2012 to 2021 and analyzed it using a fixed effect approach, whereas the GMM method was used for robustness check. The evidence strongly suggests that audit committee independence and financial expertise adversely affect audit report lag. In contrast, it was found that audit committee size exerts a significant positive influence on audit report lag. Additionally, the moderating effect shows that as the proportion of institutional ownership rises, the impact of the audit committee meetings and financial expertise on reducing audit report lag may increase. Also, the research findings suggest that leverage, profitability and auditor type are essential variables in explaining Saudi firms’ audit report lag.

Furthermore, the results from this investigation have crucial implications for the financial reporting system of Saudi firms. First, the firms should design smaller audit committees with more independent board members and financial experts to strengthen their internal governance quality, thereby lowering financial reporting lag. Also, the moderation analysis suggests that institutional investors may complement the audit committee’s oversight duties. Thus, Saudi firms should embrace institutional shareholding to empower their internal control systems, thereby enhancing internal audit functions. The findings also indicate that applying the prepositions of agency and resource dependency frameworks may be relevant to the Saudi corporate environment. Similarly, the research findings may serve as inputs for standard setters and policymakers in charge of reviewing corporate governance codes and regulatory frameworks to enhance financial reporting quality.

Overall, this study contributes to the ongoing debates on the impact of board diversity on organizational outcomes by analyzing how audit committee financial expertise may influence audit report lag. Also, the moderation analysis unveils a new approach that may yield a robust control mechanism that can compel firms to minimize audit report lag. Thus, the research provides further insights that may enhance financial reporting quality, particularly in emerging economies with less developed institutional frameworks.

Although this research provides further insights into the audit report lag determinants, some limitations must be acknowledged. Firstly, this research concentrates on non-financial companies. Therefore, future studies may focus on financial firms to confirm the reported empirical results. Also, future should focus on other audit committee attributes not covered in this study. The moderation analysis is based on institutional ownership. Thus, future research may explore the moderating role of family and government ownership. The research used one approach for measuring audit report lag, and upcoming studies may employ other measures of financial reporting lag for comparison purposes. Moreover, a similar analysis may be conducted in other emerging economies to confirm the findings of this study. Finally, future studies may specifically analyze the impact of Covid 19 on audit report lag for comparison purposes.

Footnotes

Acknowledgements

The authors extend their appreciation to Taif University, Saudi Arabia, for supporting this work through project number (TU-DSPP-2024-303).

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with ror publi/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by Taif University, Saudi Arabia, Project No. (TU-DSPP-2024-303).

Data Availability Statement

Data for this research can be obtained from the official website of the Tadawul website.