Abstract

This study investigates whether enterprise risk management (ERM) functions as a mediating mechanism through which audit committee effectiveness (ACE) and internal audit (reflected by its arrangement and expenses) influence financial reporting lag (FRL). This study also tests (a) the nonlinearity of the ERM–FRL relationship and (b) the heterogeneity in the FRL that affects the relationship. The analysis is grounded in agency theory and the resource-based view and draws on 2,352 firm-year observations of companies listed on Bursa Malaysia from 2012 to 2015. The study employs panel static models to account for unobserved heterogeneity across firms alongside threshold regression and quantile regression methodologies. This approach captures nonlinear and distributional effects in the relationship between the variables. The findings indicate that investment in internal audit is essential to enhancing ERM effectiveness, which subsequently contributes to reducing FRL. Additionally, the results show that ERM mediates the relationship between ACE and FRL particularly at low levels of ERM effectiveness and when FRL is not excessively prolonged. The study highlights the importance of ERM in preparing financial reports, thus emphasising its role in ensuring a short FRL for timely decision-making by shareholders. It contributes to the financial reporting literature by offering novel insights into the nonlinear and heterogeneous effects of ERM on reporting timeliness.

Plain Language Summary

This study examines why some Malaysian public companies take longer to release their financial reports and how corporate governance practices can help mitigate these delays. We examine the role of audit committees, internal audit functions (including their costs and structure) and enterprise risk management (ERM). Using 2,352 company-year observations between 2012 and 2015, we found that spending more on internal audits can reduce reporting delays, especially when ERM is effectively implemented. However, this effect weakens when delays are already very high. We also found that in-house internal audits are linked to longer delays at moderate levels, but again, ERM helps mitigate this. Interestingly, the effectiveness of audit committees had no significant impact. This study is the first to examine how ERM mediates these relationships and how the effects vary depending on the duration of the delays. Our findings provide valuable insights for policymakers, regulators and companies seeking to enhance transparency and facilitate timely financial reporting.

Introduction

Timely financial reporting is vital for informed decision-making because it provides stakeholders with current insights into an organisation’s performance (Abdillah et al., 2019; Ashraf et al., 2020). As such, global exchange regulations require listed companies to meet strict filing deadlines. Financial reporting lag (FRL) refers to the time delay between the end of a reporting period and the availability of financial information to stakeholders, including shareholders, investors, regulators and the public (Owusu-Ansah & Leventis, 2006). It covers the preparation of financial statements and their internal validation at the company level as well as external audit processes and approvals, which is commonly referred to as audit report lag (Al-Ajmi, 2008; Lawal & Shinozawa, 2024). Although the literature has identified factors related to the timeliness (or lag) of financial reporting, little is understood about the role of enterprise risk management (ERM) in the process. Compliance risk is an important concern in organisations. Moreover, reporting lags beyond the stipulated timeframe is a serious threat because it can result in penalties and damage to companies’ reputations. For example, Bursa Malaysia, the regulator of the stock exchange in Malaysia, issued a public reprimand to Annum Bhd. and fined five of its directors RM31,000 each for failing to submit the company’s 2023 annual report on time. This study is motivated by the importance of this issue and the gap in the literature in examining how the ERM effectiveness of Malaysia-listed companies mediates the relationship between the audit committee effectiveness (ACE) and internal audit, which includes (a) investment in the internal audit function (IAF; cost) and (b) the arrangement (in-house or outsourced) with FRL. This investigation is conducted using agency and resource-based theories. Moreover, this study examines the nonlinearity of the relationships that arise from diminishing return effects. Specifically, incremental improvement in ERM effectiveness can lead to diminishing reductions in FRL, thus eventually reaching a point where further enhancements in ERM effectiveness do not substantially impact FRL. Our view is aligned with Kor and Mahoney (2004) and Penrose (1959) that firms with high FRL may face internal constraints that limit the gains from further ERM improvements, thereby reflecting a plateauing effect. Moreover, the ERM–FRL relationship weakens at low ERM effectiveness, which indicates that a threshold level is needed for meaningful FRL reduction. As such, the assessment of ERM on FRL involves analysing distinct FRL quantiles and acknowledging variations in their relationship especially when FRL levels are significantly higher than those of other companies.

Audit committees, internal audits and ERM are crucial corporate governance elements that ensure transparency, accountability and mitigation of potential risks within an organisation’s operations (Ghafran & Yasmin, 2018). Agency theory suggests that these three factors are important monitoring mechanisms that can control agents and ensure accountability to principals. The resource-based view suggests that allocating resources to monitoring mechanisms, such as audit committees, enhances financial reporting credibility and organisational governance (Baatwah et al., 2019; Bhuiyan & D’Costa, 2020; Rahaman & Bhuiyan, 2025). An internal audit with sufficient resources provides valuable insights, recommendations and assurance on internal controls, operational efficiency, risk mitigation and asset protection (AL-Qadasi et al., 2019). Resource dependence theory emphasises that the outcomes of internal audits depend on resource allocation, including outsourcing or internal resources and associated costs (Wan-Hussin & Bamahros, 2013). Additionally, ERM systematically identifies, assesses and manages risks, thus aiding organisational efficiency and objective achievement.

Audit committees, internal audits and ERM collectively contribute to the accuracy and reliability of financial information, enhance stakeholder confidence and promote transparency, accountability and responsible management, thus ultimately supporting long-term success and organisational sustainability. We are also motivated to investigate this issue further because the IAF and the audit committee serve as parties that provide assurance and act as consultants on the effectiveness of risk management implementation (Ghaleb et al., 2020; Kaawaase et al., 2021; Tumwebaze et al., 2022). Given that the late submission of annual reports poses a serious risk to companies, we suspect that the influence of both parties on reducing FRL is through ERM. Thus, we question whether ERM mediates the relationship among IAF, ACE and FRL. In relation to this issue, we also question whether the ERM is associated with FRL and whether a relationship exists among ACE, IAF and ERM. In addition, we seek to answer whether these relationships are linear.

This study contributes to the literature in several ways. Previous studies have identified factors related to FRL, such as company demographics, external audit characteristics and corporate governance factors. Company demographics include size, industry, fiscal year-end, leverage, profitability and complexity (Alexeyeva, 2024; Lary & Taylor, 2012). External audit characteristics include audit firm size, audit technology, audit staff, audit work time, fees, auditor changes and audit reporting period (Habib & Bhuiyan, 2011; Owusu-Ansah & Leventis, 2006; Rahman et al., 2024; Salleh et al., 2017). Corporate governance includes several factors, such as CEO duality, board size, frequency of board meetings, board independence and board expertise (Mohamad-Nor et al., 2010). Past studies have also reported the roles of internal audits and audit committees in providing assurance and serving as consultants in assessing the effectiveness of risk management implementation and its impact on performance and internal control systems (Bananuka & Nkundabanyanga, 2023). Similarly, Wan-Hussin and Bamahros (2013) investigated the association between a company’s internal audit arrangements using either outsourcing or internal resources and costs incurred for IAFs with delays in audit reports. However, limited studies have assessed the role of the ACE and internal audit attributes, that is, the formation and cost of internal audit investments, concerning the effectiveness of ERM and their relationships with FRL. In contrast to past studies, this study examines the extent to which the success of audit committees and IAF contributes to the effectiveness of ERM, which can subsequently reduce FRL. This study is also the first to investigate the role of ERM in reducing FRL. In line with agency theory, effective ERM can reduce agency costs through its role as a monitoring mechanism within a company. The study also emphasises the importance of ERM in corporate governance to gain a competitive advantage based on the resource-based view. Finally, studies that have investigated this issue using threshold analyses and quantile regression approaches are lacking. Our methodology concurrently addresses two primary concerns: (a) nonlinearity of the ERM–FRL relationship and (b) heterogeneity in FRL, which affects the relationship. Initially, we address nonlinearity by computing static discontinuous nonlinear estimates of ERM effectiveness for our sample through panel threshold regressions. Next, we investigated FRL heterogeneity by assessing whether the previously derived estimates exhibit variations across the FRL spectrum using a quantile regression approach.

This study used 2,352 company-year observations of 571 listed companies on Bursa Malaysia from 2012 to 2015 and found that internal audit costs help reduce FRL with ERM partially mediating this effect. However, this relationship disappears at high FRL levels. At moderate FRL levels, in-house internal audits are linked to high FRL, which is also mediated by ERM. However, ACE shows no significant impact on ERM or FRL. Unlike previous studies, this study focussed on the unique characteristics of Malaysia, an emerging country with different corporate landscapes, for several reasons. Firstly, in this context, data on internal audits, such as investment costs and internal audit formation arrangements, are publicly available. Therefore, we could test how they affect the effectiveness of internal audits in FRL. Secondly, we selected a sample period before the revision of the Malaysian Code of Corporate Governance (MCCG) in 2017. After the revision, listed companies were specifically encouraged to implement ERM as the best practice. The data provided sufficient variability to test this mediating effect. The sample covers a period prior to the regulatory change that shortened the annual report submission deadline from 6 months to four. This strict requirement imposed great urgency on companies in terms of preparation and audit timelines, thus potentially altering the relationships among key variables during the period surrounding the change. Investigating this shift necessitated a distinct theoretical perspective and analytical framework. Finally, financial intermediaries and news outlets in Malaysia, as in other emerging economies, are not as effective as those in developed countries (Qasem, 2025). This aspect underscores the importance of timely reporting.

Addressing these questions is crucial for informing policymakers, publicly listed companies, investors and regulatory bodies to enhance ERM implementation through the development of policies and practices related to audit committees and internal audits, thereby reducing FRL.

The remainder of this paper is organised as follows. Section 2 reviews the related literature and develops the hypotheses. Then, Section 3 explains the research method and data analysis. The results are presented in Section 4. Finally, Section 5 concludes.

Literature Review and Hypotheses

The literature reveals the interrelationships among audit committees, IAFs and ERM. Despite considerable progress in understanding the relationships among FRL, audit committees, IAFs and ERM, several gaps persist.

Two main studies have been conducted to understand the factors that influence FRL. The first stream, which is rooted in the resource-based view, explores how company demographics, such as size, performance, financial condition, industry, leverage and complexity, impact FRL. These factors were discussed in the studies summarised by Abernathy et al. (2017). The second stream, which draws from agency theory, focuses on the role of the board as a monitoring mechanism for shareholders over management. This perspective highlights corporate governance mechanisms, such as ownership concentration, board and audit committee composition, family ownership, CEO duality and external auditors, in reducing the FRL (Al-Mulla & Bradbury, 2020; Kaaroud et al., 2020; Lajmi & Yab, 2022; Sultana et al., 2015). Some studies also consider external governance mechanisms, such as governmental regulation, accounting standards and analyst forecasts, along with internal controls and Big Data within organisations, as determinants of FRL (Ahmed et al., 2023; Habib, 2015; Khlif & Samaha, 2016). Furthermore, Alexeyeva (2024) established that board independence, gender diversity and board size are negatively associated with financial reporting delays (Alexeyeva, 2024; Hassan, 2016). Some studies combine both perspectives, thus suggesting that resources can enhance the effectiveness of monitoring mechanisms in reducing FRL (Sultana et al., 2015).

Many studies examine the effect of external audit firm characteristics on FRL (Wan Hussin et al., 2018). Situated within this body of literature, this study extends the understanding of the role of key governance mechanisms in financial reporting, that is, ACE, internal audit and ERM. The audit committee plays a crucial role in determining the quality of corporate governance (Lajmi & Yab, 2022). Moreover, it oversees financial reporting and ensures its integrity and transparency. Reduced FRLs are found to be associated with independent audit committees in the United States (Abernathy et al., 2014) and Australia (Sultana et al., 2015). Although the combined results were provided by Habib et al. (2019), the mixed results that emerged require a re-examination of the issue in a specific context using a detailed threshold regression and quantile regression approach.

ERM involves the systematic identification, assessment and management of risks across an organisation. Effective ERM practices integrate risk considerations into strategic decision-making processes, thus ensuring a proactive and holistic approach to risk management. Companies with robust ERM practices may experience short FRLs based on several factors. Firstly, companies may proactively identify and address risks that may affect reporting (Pierce & Goldstein, 2018) to ensure a smooth process. Secondly, the literature may be viewed from a risk perspective. Long FRL is associated with the manipulation of earnings (Asthana, 2014), bankruptcy and leverage (Al-Mulla & Bradbury, 2020), restatement (Skomra et al., 2023), financial crisis (Bajary et al., 2023), contingencies and industry risks. Thus, an effective ERM that can manage and reduce these risks may improve the FRL. The unique characteristic of ERM, which is tailored to meet the needs of each organisation, serves as a vital resource which is distinct for the firm.

ACE and ERM are interconnected. Effective audit committees, which are characterised by their independence, size and frequent meetings, are crucial for robust risk management (Sulimany, 2024; Yatim, 2009). ERM enhances timely financial reporting by ensuring effective internal controls. Thus, without effective ERM, FRL will be difficult to reduce. As a resource, ERM also lowers agency costs and information asymmetry between owners and management, which is aligned with agency theory. Thus, based on preceding discussions, further research is needed to explore the mediating effects of ERM effectiveness on the relationship between ACE and FRL. The first hypothesis (

The IAF is another important mechanism for corporate governance that is related to financial reporting and can reduce agency costs. However, few studies have examined the relationship between IAF and reporting lag. The IAF provides independent assurance and consulting services that can reduce FRL by improving internal controls, risk management and operational efficiency (Bajary et al., 2023; Harymawan & Putri, 2023; Ismail et al., 2022). Wan-Hussin and Bamahros (2013) found that outsourced IAFs, which are independent and knowledgeable, typically lower FRL compared with in-house IAFs, which benefit from strong organisational knowledge and relationships. A well-funded IAF can hire skilled internal auditors to detect and prevent financial misstatements, thus further reducing FRL. This study explores the impact of the costs and arrangements of IAF, which is viewed as an important resource, on FRL and its components. This study differs from other studies in that we considered the effect of ERM as another important resource in the model.

In line with the internal audit tasks of monitoring financial reporting, which is a company’s internal control system and assessing the effectiveness of ERM, the IAF, that is, arrangement (in-house or outsourced) and cost, is expected to help improve the quality and efficiency of audit work, thus reducing FRL. In other words, an effective IAF reduces FRL. The second hypothesis (

Figure 1 presents the conceptual framework. Grounded in agency theory, ACE and the internal audit function are identified as key governance mechanisms, which emphasise the board’s role in monitoring management. Their independent monitoring roles are further supported by the resource-based view, which highlights the importance of organisational resources in enhancing oversight, accountability and governance capacity. ERM is introduced as a mediating variable because it systematically manages risks and strengthens internal controls, thereby facilitating timely financial reporting and reducing FRL.

Conceptual framework.

Methods

Sample

The study sampled active listed companies on Bursa Malaysia from 2012 to 2015. From 2015, Bursa Malaysia shortened the annual report publication deadline from 6 to 4 months. The sample period included the post revision phase of the MCCG 2012, which emphasises the significance of risk management in financial reporting and adds responsibilities to the audit committee.

The study sourced active data for the observation year from the Bursa Malaysia website, financial data from the Datastream database by Thomson Reuters and nonfinancial data from annual reports. As of November 21, 2016, Bursa Malaysia had 904 active publicly listed companies. The sample excluded 34 finance-based companies, 75 companies with mid-year changes, 14 newly listed companies and 210, that is, 193 plus 17 companies with incomplete or inaccessible reports from 2012 to 2015. The final sample included 571 companies, which is about 63% of the total listed companies (Table 1).

Sample.

Specification Model

This study consists of three main models. Model 1 examines the relationship involving FRL without considering ERM. Then, Model 2 tests the direct effect of ERM on FRL. Meanwhile, Model 3 sets ERM as the dependent variable to evaluate its role as a mediator in the relationship between other variables and FRL. The three-step modelling approach is based on Baron and Kenny (1986). The following regression models are used to test the hypotheses:

Model (1)

Model (2)

Model (3)

Where FRL refers to financial reporting lag, ACE represents audit committee effectiveness, IAF_ARG denotes the internal audit function arrangement and IAF_COST is the cost associated with the internal audit function. Additionally, control variables include Size, which indicates company size. LEV represents company leverage. ZMJ measures bankruptcy propensity. LOSS indicates companies reporting losses. Meanwhile, CFO refers to cash flow from operations. BUSY is a dummy variable for the busy audit season. In addition, AUD_FEE represents audit fees. BIG4 is an indicator for companies that were audited by one of the Big Four audit firms. OPINION controls for variations in FRL due to the nature of the audit opinion. In addition, i denotes the company, t represents the year (2012–2015), and the equation includes an intercept term, which is denoted as β0. The coefficients β1, β2,…, βn™ represent the slopes or regression coefficients. The term ε it captures the error component.

Variable Measurement

The variables used in this study include FRL, ACE, IAF attributes, ERM effectiveness and company-specific characteristics. The primary dependent variable in this study is FRL, which is measured as the number of days between the fiscal year-end and the release date of financial statements. The ACE is determined by its size, independence, member expertise, number of meetings held and chairperson expertise (Abdillah et al., 2019; Al-Ajmi, 2008; Rusmin & Evans, 2017; Appendix A). The IAF attributes are (a) the investment in the IAF and (b) the arrangement, whether in-house or outsourced (Wan-Hussin & Bamahros, 2013). The ERM effectiveness is measured following Gordon et al. (2009), as presented in Appendix B. Table 2 presents the measurements of the company-specific variables.

Descriptive Statistics.

Note. FRL is the number of days between the end of the financial year and the date the financial report is submitted to Bursa Malaysia. ACE is the sum of the ACE index score, where all components of ACE are described in Appendix A. IAF_COST is the original logarithm of investment costs for internal audit incurred by company i in the year t. ERM is the total ERM effectiveness index score, where all indicators are described in Appendix B. SIZE is the natural logarithm of the total assets of the company i in year t. LEV is the ratio of debt per total assets of company i in year t. ZMJ is the probability score of bankruptcy using the Zmijewski model for nonfinancial companies, where Zmijewski score = −4.336 − 4.513 × (Return on Assets) + 5.679 × (Leverage) + 0.004 × (Current Ratio). AUD_FEE is the original logarithm of the audit fee paid to the auditor. CFO is the ratio of operating net cash flow per total assets of the company i in year t. IAF_ARG is a dummy variable for the formation of an internal audit encoded as 1 for the formation of an internal audit using internal resources (in-house) and 0 if the formation of an internal audit using external sources (outsourcing). BUSY is a dummy variable encoded as 1 if the company has a financial year ending December 31/January 31. Otherwise, the value is 0. LOSS of the dummy variable Net Income less than 0 is encoded as 1. Otherwise, the value is 0. BIG4 variables for companies that are clients of Big Four audit firms, namely, PricewaterhouseCoopers, Ernst & Young, KPMG and Deloitte, are encoded as 1. Otherwise, the value is 0. OPINION is a dummy variable encoded as 1 for the unconditional audit report (unqualified) and 0 for the conditional audit report (qualified).

Static Analysis

This study used panel static analysis, which includes the pooled, fixed effects and random effects models. Organisations may experience a diminishing rate of reporting lag reduction beyond a certain level of ERM effectiveness, thus leading to a nonlinear relationship. This study analysed the possible existence of nonlinearity in the relationship between ERM effectiveness and FRL by using Hansen’s (1999) threshold regression technique. The panel threshold regression shows the distinction between the two coefficients for the other half of the turning (threshold) point, beyond which the relationship between ERM effectiveness and FRL changes. The procedure that helps to determine the threshold point that divides the data into two regimes (with a single threshold) can be specified as follows:

where

The threshold parameter was estimated using the least squares approach, which is presented as follows:

We computed the critical values for the threshold effect via a bootstrap procedure to test the null hypothesis of no threshold effect, which is presented as follows:

where SSEa is the sum of squares error of the linear model and SSEb is the sum of squares error of the threshold model. The statistical significance of the F-test indicates the rejection of the null hypothesis of no threshold effect, which demonstrates that the relationship is nonlinear. Following Hansen’s (1999) recommendation to obtain asymptotically valid p-values, we bootstrapped our estimate. The null hypothesis of the nonidentification of g (no threshold effect → linear relation) and its accompanying alternate hypothesis of the existence of at least one threshold are as follows:

Under the null hypothesis of no threshold effect, the model specified in Equation 3 was reduced to the linear model specification given in Equation 2. In this study, the threshold estimator was obtained using the STATA command ‘xthreg’.

Subsequently, this study analysed the differences in the impact of FRL using a newly developed technique for unconditional fixed-effects quantile estimation for panel data.

Results and Discussion

Descriptive Statistics and Correlation

On average, a company’s FRL for publishing audited financial statements to the public after the end of financial year is 132.4 days with a 49-day low and a 289-day high (Table 2). This average period did not exceed the 6-month regulatory period set by Bursa Malaysia before 2015. However, the average FRL for companies listed on Bursa Malaysia is long compared with the average of 106.95 days reported by Leventis et al. (2005) and the average of 113 days by Owusu-Ansah and Leventis (2006). Meanwhile, listed companies in Indonesia take 98 days on average to release audited financial statements to the public after the end of their financial statements. (Rochmah Ika & Mohd Ghazali, 2012). The average ACE is 2.62 out of the five maximum ACE scores. These numbers show that the average ACE score for the sample companies is approximately 52.4% of the maximum requirement. Of the sample of companies in Malaysia, 37% formed an in-house IAF, whereas 63% formed IAF_ARG using outsourced sources, namely, services from outsourced companies. The average cost incurred for IAF (IAF_COST) is RM401,388 compared with Wan-Hussin and Bamahros (2013), where average IAF cost amounted to RM371,590. The ERM effectiveness was measured using the ERM effectiveness index developed by Gordon et al. (2009). The results show that the average value of the ERM effectiveness index is −0.116 compared with Gordon et al. (2009), where the average ERM value for the high-performing group was −0.067.

The Pearson correlation values shown in Table 3 indicate that SIZE and AUD_FEE have a correlation of .80 (p < .01). However, the VIF analysis shows no value exceeding 10, suggesting that the model has no serious multicollinearity problem (Gujarati, 2004). Therefore, size was retained in the model.

Correlation Matrix.

Note.***, **, and * indicate significance at the .01, .05 and .10 levels, respectively, using two-tailed tests.

Main Model

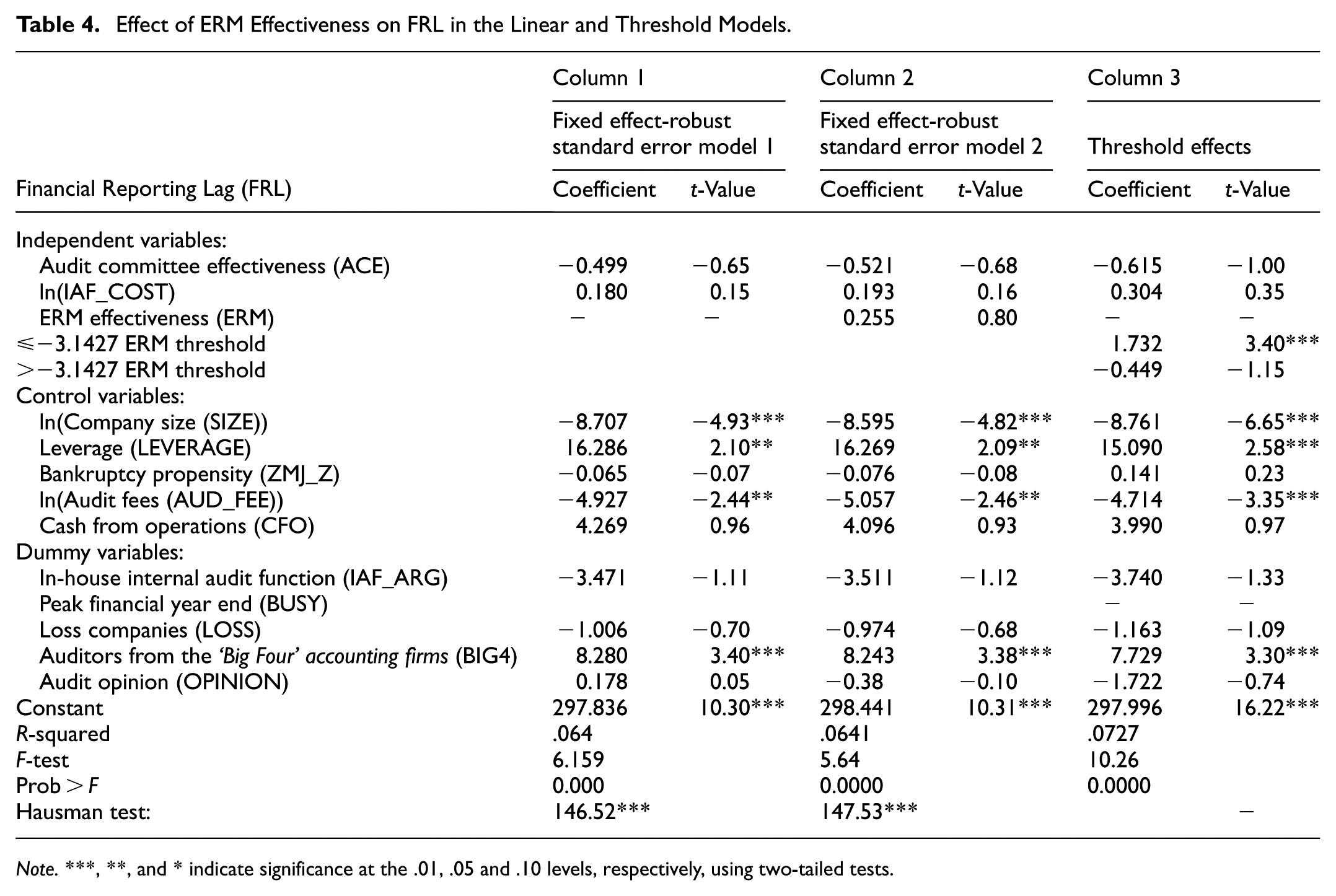

Models 1 and 2 in Table 4 show the results of the panel fixed effects with statistically significant Hausman and F tests. Among the variables, only the control variables and the dummy variable demonstrate significance, including company size, audit fees, leverage and auditors from Big Four accounting firms (BIG4). These findings suggest that internal audit arrangements and costs are not linked to FRL, thus indicating that ERM does not mediate this association. We explore the nonlinearity of these relationships further by determining the existence of a threshold that establishes the connexion between ERM and FRL. Beyond a certain point of optimal ERM effectiveness, further enhancements may not significantly reduce FRL. This concept aligns with the idea of diminishing returns, which is common in economics and various disciplines. This argument is also consistent with the existence of constraints on resources in achieving competitive advantage (Kor & Mahoney, 2004; Penrose, 1959). Beyond a certain threshold, the additional input leads to progressively marginal increases in the output until it reaches a plateau.

Effect of ERM Effectiveness on FRL in the Linear and Threshold Models.

Note.***, **, and * indicate significance at the .01, .05 and .10 levels, respectively, using two-tailed tests.

For threshold regression, a test is conducted to determine the presence of a single threshold and ensure that the selection of thresholds is not arbitrary. The null hypothesis

Tables 5 and 6 present the results of the threshold analysis. The calculated F statistic surpassed the critical value of 21.14 (p-value <5%), thus indicating the existence of one threshold in the model (Table 4). The null hypothesis of linearity was rejected in favour of nonlinearity. In Table 6, a single threshold occurs when the ERM effectiveness is −3.1427 with a 95% confidence interval between −3.2200 and −3.0558.

Test for the Unitary Threshold Model.

Estimation of a Model with a Unitary Threshold.

Note. Threshold estimator (95% CI) with 1,000 bootstrap estimates. CI = confidence interval.

We further examined the relationship between the predictor variables and the dependent variable in the threshold regression model (Table 4, Column 3). The main variable of interest was the effectiveness of the ERM. When ERM was less than or equal to −3.1427, a significant positive relationship with FRL was observed, as evidenced by a coefficient of 1.732 and a t-value of 3.400. When the ERM falls below a specified threshold, an increase is noted in the FRL. By contrast, when the ERM exceeds −3.1427, the relationship with FRL becomes insignificant. However, we also suspect that the result is contingent upon the heterogeneity of the FRL. Thus, additional testing is necessary.

Unconditional Quantile Regression

Issues that are not directly related to ERM but are associated with FRL also arise. ERM usually detects anticipated risks and manages them by taking measures to reduce them. However, some issues may have already occurred, such as forensic investigations of dubious financial transactions, which may increase FRL to an unprecedented level. This fact introduces heterogeneity in FRL. We tested this effect according to different quantiles of FRL. We suspected that, when FRL is unusually long, ERM may no longer affect FRL because of the major issues faced by companies.

In the quantile regression, 1,000 bootstrap replications were employed to calculate estimates and standard errors. The results are presented in Table 7. Notably, when ERM effectiveness surpasses −3.1427, the relationship between ERM and FRL exhibits negativity at the 0.25 and 0.50 quantiles and becomes insignificant at the 0.75 quantile. This outcome suggests that while the relationship is inconsequential at low levels of ERM effectiveness, it becomes notably negative and statistically significant beyond the threshold of −3.1427. This result indicates an enhancement in reporting timeliness with increasing ERM effectiveness at quantiles of 0.25 and 0.50, thus contradicting the notion of diminishing returns. However, this significant inverse relationship is only apparent when considering FRL variability across quantiles. Conversely, the previously reported positive relationship between ERM and FRL at low ERM thresholds loses statistical significance across all the FRL quantiles. These findings imply that a minimum threshold of ERM effectiveness is necessary to influence FRL substantially, thus suggesting that a sufficiently effective ERM can significantly reduce FRL. The findings indicate that the ERM cannot further decrease FRL for quantiles surpassing 0.75.

Quantile Regression on FRL.

Note.***, **, and * indicate significance at the .01, .05 and .10 levels, respectively, using two-tailed tests.

Additionally, this study reveals that the IAF_COST is inversely associated with FRL across all quantiles, which implies that allocating costs to IAF can mitigate FRL. However, the variables IAF_ARG are only significant at the 0.50 and 0.75 quantiles of FRL, thus suggesting that an in-house IAF and high-quality external audit from Big Four firms are effective in reducing reporting delays especially in categories with prolonged FRL.

Mediating Effect

Table 8 displays the regression outcomes of quantile regressions concerning ERM determinants. Sample companies with ERM effectiveness surpassing the minimum threshold of −3.1427 were exclusively considered. The significance of ACE, IAF_COST and IAF_ARG on ERM effectiveness was examined across various FRL quantiles except for the 0.75 quantile, which was deemed insignificant. Notably, IAF_COST was found to enhance ERM effectiveness at the 0.25 and 0.50 quantiles, thus suggesting that investing in the IAF can bolster ERM effectiveness. However, IAF_ARG does not exhibit significance at the 0.25 quantile of FRL but diminishes ERM effectiveness at the 0.50 quantile of FRL. This outcome implies that an outsourced IAF may be advantageous for ERM effectiveness when FRL is moderately prolonged possibly because of its independence or specialised knowledge. Conversely, ACE shows no association with ERM effectiveness across any FRL quantile, thus contradicting Yatim’s (2009) emphasis on the importance of audit committee characteristics in determining effective ERM implementation. Additionally, no significant relationship was observed between ACE and FRL at any quantile. However, further exploration of this issue is constrained by the limited availability of detailed data on the audit committee processes that influence ERM implementation.

Quantile Regression on ERM Effectiveness (>−3.1427).

Note.***, **, and * indicate significance at the .01, .05 and .10 levels, respectively, using two-tailed tests.

Table 9 presents the formal tests for mediation. The results indicate that ERM partially mediates (complementary mediation) the relationship between IAF_COST and FRL at the 0.25 and 0.50 quantiles of FRL. These findings suggest that the effectiveness of ERM serves as a significant mediating factor, thereby complementing the direct impact of investment in the IAF on FRL. Essentially, this result implies that investment in the IAF can directly reduce reporting lags. Meanwhile, the lags can be indirectly diminished through the effectiveness of ERM. The table also reveals that ERM only partially mediates the relationship between IAF_ARG and FRL (competitive mediation) at the FRL quantile of 0.50 but not at other quantiles. This result indicates that an in-house (outsourced) internal audit arrangement reduces (increases) ERM effectiveness at a moderate level of reporting lag, thereby increasing (reducing) the lags.

Mediating Effect.

Note.***, **, and * indicate significance at the .01, .05 and .10 levels, respectively, using two-tailed tests.

Discussions

This result implies that the effectiveness of ERM prolongs FRL and reduces the ERM threshold. This finding contradicts our initial belief, as implied by Abernathy et al. (2014) and Sultana et al. (2015), that an effective mechanism for corporate governance shortens reporting lags. At a low level of ERM effectiveness, as the effectiveness increases, additional internal control issues are highlighted, thus leading to increased substantive tests by auditors. Consequently, the FRL is prolonged. This evidence supports the importance of ERM in agency relationships. The findings also reveal a behaviour that is characterised by diminishing returns. As ERM effectiveness increases, the reduction in FRL decreases in significance, which eventually reaches a plateau where additional improvements yield minimal impact. This outcome aligns with Kor and Mahoney (2004) and Penrose (1959), who suggested that internal firm constraints can limit the benefits of further ERM enhancements. Additionally, the relationship between ERM and FRL is weak at low levels of ERM effectiveness, thereby indicating that a minimum threshold must be reached before meaningful risk reduction occurs.

The results may also suggest that companies with exceptionally high FRL may encounter severe issues beyond typical ERM processes, such as uncovering material misstatements in previous financial statements or encountering unresolved disputes between auditors and clients regarding impairment values. This outcome suggests that improvements in ERM effectiveness are associated with shortened reporting lags (i.e., enhanced timeliness) among firms with low to median FRL levels. However, this benefit diminishes among firms that already have high reporting delays. This pattern may indicate that the impact of ERM is pronounced in firms that already report relatively fast, whereas firms with high FRL may face other structural or organisational constraints (Penrose, 1959) that limit the effectiveness of ERM improvements. Moreover, the positive relationship between ERM and FRL at low levels of ERM effectiveness becomes statistically insignificant across all quantiles. This correlation reinforces the notion that a minimum threshold of ERM effectiveness is required before any meaningful reduction in FRL is observed.

The inverse relationship between IAF_COST and FRL reflects that allocating additional costs to the internal audit function means increasing resources that can enhance efficiency by hiring additional or highly skilled staff, investing in advanced technology and audit tools, providing ongoing training and strengthening risk management support. This notion is consistent with the role of IAF in agency relationships and leads to accurate, timely and effective internal audits. Regarding internal audit arrangement, in contrast to Wan-Hussin and Bamahros (2013), the result supports the view that familiarity with organisational knowledge and internal relationships by having an internal audit unit within the company can streamline the internal audit process, thus enhancing its efficiency and timeliness. Overall, these findings provide an explanation for the divergent results observed in prior literature (Ismail et al., 2022; Sultana et al., 2015). Furthermore, the conditional nonlinearity of the relationship extends the recent work of Nguyen and Nguyen (2023) regarding the impact of ERM on reporting lags as well as the contributions of Harymawan and Putri (2023) and Ismail et al. (2022) on the role of IAF.

Regarding the insignificant role of the audit committee in influencing ERM effectiveness, although this finding is not consistent with Yatim (2009), it may be explained by the audit committee’s limited operational involvement. Audit committees typically evaluate the overall effectiveness of the ERM function but are not directly engaged in identifying, analysing, managing or reporting risks.

Further results also suggest that an in-house internal audit arrangement is associated with reduced ERM effectiveness at a moderate level of reporting lag, thus leading to prolonged lags. By contrast, an outsourced arrangement enhances ERM effectiveness, thereby contributing to short reporting lags. The findings suggest that the effectiveness of ERM is more sensitive to the structure and investment in the internal audit function than to audit committee characteristics especially at varying levels of financial reporting lag. These results contribute to the growing literature on the conditional and context-specific nature of governance mechanisms in supporting ERM effectiveness.

Conclusion

Timeliness in publishing financial reports (reduced FRL) is crucial to ensuring that shareholders and investors continue to receive information when they want to make decisions. Delays in publishing financial reports can cause financial information to lose relevance. Hence, effective corporate governance mechanisms, such as the characteristics of audit committees and internal audits, are important in determining the smoothness of the financial reporting process to be published on time and ensuring that the listing requirements are met. Effective audit committees and internal audits reduce risk, thus simplifying external audit processes and ultimately reducing FRL. Therefore, the main objective of this study is to examine the mediating effect of ERM effectiveness on the relationship between corporate governance mechanisms (ACE, internal audit cost and internal audit arrangement) and FRL. This study tested the nonlinearity of the relationships that depend on the levels of ERM effectiveness and FRL. In addition, this study investigated a new relationship between ERM effectiveness and FRL.

We used 2,352 observations of Malaysia’s publicly listed companies and found evidence that internal audit costs are related to reduced FRL and that ERM partially mediates this relationship. However, such relationships are absent at high FRL levels. At a moderate level of FRL, an in-house internal audit arrangement is related to high FRL with ERM mediating this relationship. Moreover, ACE is not associated with improved ERM or FRL effectiveness.

This study addresses a gap in the literature by demonstrating the impact of internal audit costs and arrangements as well as effective audit committees on FRL through strong ERM as a mechanism. Our study is one of the first works to highlight ERM effectiveness as a key factor that influences FRL. It also reveals two main effects: (1) the direct impact of in-house and investment in the IAF on FRL and (2) the indirect effect of in-house and investment in the IAF through effective ERM on FRL.

Although ERM, internal audits and audit committees are theoretically connected through the concept of risk, their roles and practices appear distinct. The IAF assesses the effectiveness of ERM in identifying and managing company risks and ensuring that actions align with reported risk responses. The intensity of the internal audit processes is influenced by the risk rating report that is produced by the ERM function. Then, the results of these internal audit processes are reported to the company’s audit committee. Although the internal audit, audit committee and ERM functions are separate, they are interconnected.

Our study highlights the importance of internal audit costs and arrangements in influencing the reporting lag particularly when they are considered in conjunction with ERM effectiveness. We find evidence that suggests that ERM effectiveness has a minimum threshold rather than a diminishing return effect, thereby indicating its potential to reduce the reporting lag significantly. This condition only occurs when the FRL is not excessively long. However, while ACE is important, our findings suggest that it may not be sufficient on its own to mitigate the reporting lag significantly.

Theoretically, this study contributes to agency theory and the resource-based view by providing additional evidence that the effectiveness of monitoring mechanisms in agency relationships depends on the resources allocated to them. Moreover, it deepens the understanding of the inherent limitations of these resources, which impose boundaries on their effectiveness. These findings also have significant implications for companies and regulators especially in emerging economies. Companies need to understand and address the key factors that affect the reporting lag to ensure compliance with shortened publication periods for financial reports. Regulators may need to focus on enhancing governance practices, such as internal audit arrangements and ERM implementation, to improve the timeliness of financial reporting.

However, the limitations of our study, including the lack of longitudinal data to assess relationship dynamics over time and the absence of granular data, must be acknowledged to understand the internal audit, audit committee and ERM processes fully. Additionally, the cultural context of the actors and institutions was not explored, which can have significant implications for effectiveness and efficiency. In Malaysia, the mix of religious and ethnic groups, which includes mostly Malay-Muslims but also a large number of Chinese, Indian and indigenous people, can affect the values, morals and institutional logic of businesses. These cultural dimensions can influence managerial perspectives towards accountability, risk management and regulatory compliance, thereby subsequently shaping the design and operation of ERM systems and internal audit practices. Additionally, future research can extend the sample period to examine the impact of increased urgency following the change in the deadline for the submission of financial statements. Thus, future research can address these limitations and provide additional insights into these areas.

Footnotes

Appendix

ERM Effectiveness Index.

| Indicator | Definition |

|---|---|

| (ERM_SCORE) | |

| Strategy1 |

= sales of a firm for the year, , = average industry sales in the year, and = deviation of sales standards for all companies in the same industry. |

| Operation1 | |

| Operation2 | |

| Reporting1 | Reporting1 = (significant weakness) + (audit results) + (restatement)

Significant Weaknesses are reported as −1 if significant weaknesses are reported in the Internal Control and Risk Management System Statement and 0 otherwise. Audit findings are set as 0 if the firm’s audit findings are unconditional and −1 otherwise. Restatement is set as −1 if the firm reports a restatement and 0 otherwise. |

| Compliance1 | Compliance1 = auditor’s fee/total assets |

Note. Each indicator is standardised before being incorporated into the equation. Therefore, the average value of the ERM score for the entire sample is −0.116.

Ethical Considerations

This study did not require ethical approval, as it did not involve any interaction with human participants, the collection of personal or sensitive data or the use of identifiable private entities. The research was based entirely on publicly available secondary data. As such, ethical permission was not sought, in accordance with standard academic and institutional guidelines.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We acknowledge generous funding from Faculty of Economics and Management, UKM, FEP1.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The financial data supporting the findings of this study are available from the Datastream database by Thomson Reuters. The non-financial data, manually collected from annual reports, are available from the corresponding author upon request.