Abstract

This research investigates whether institutional ownership contributes to enhancement of stock liquidity in emerging markets. The study examines data of listed companies on the Vietnamese stock market. Using a comprehensive data set for all stocks listed on Ho Chi Minh Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX) from 2008 to 2017, the statistical findings consistently demonstrate that institutional ownership has a negative impact on stock liquidity. In other words, the empirical evidence supports the adverse selection hypothesis that the upward trend of institutional ownership could reduce stock liquidity because the institutional investors with superior and advantageous information could exacerbate informational asymmetry issues. By using a case study in Vietnam, this research makes an original contribution to the academic literature by examining the relationship between institutional investors and stock liquidity in emerging markets. In addition, this study offers policymakers, authorities, agencies, and managers some insightful recommendations and implications that will help to not only promote the active participations of professional institutions but also improve stock liquidity, fairness, and efficiency.

Introduction

Liquidity is a fundamental characteristic of any financial market, and a liquid market plays pivotal roles in promoting efficacy of capital allocation. It has an exponentially crucial role in recent empirical research in finance, such as market efficiency (Chung & Hrazdil, 2010; Hodrea, 2015), asset pricing (Amihud et al., 2005; Lam & Tam, 2011), corporate finance (Amihud & Mendelson, 2008; Jiang et al., 2017; Li et al., 2012). Liquidity refers to speed and convenience with which an asset can be easily converted into money without significantly incurring a considerable transaction cost or unfavorable price impacts (Ince, 2022). In other words, it portrays the willingness of buyers and sellers who agree to exchange a specific quantity of securities at the stated price instantaneously, so it is considered as a major measure of how well the markets are working (Amihud et al., 2005). When it dries up, the market can be disruptive. Lack of abundant liquidity exacerbates market swings and makes it harder for market participants to fulfill unforeseen financial needs with the risk of higher losses. In contrast, firms with more liquid stocks could mobilize capital more efficiently at lower costs as well as achieve better market values (Amihud & Mendelson, 2008; Li et al., 2012). In addition, the presence of liquid markets would boost investor confidence, improve market efficiency, and thus enhance market resilience (Hodrea, 2015; Thapa & Poshakwale, 2012). Subsequently, liquidity is of prime importance to not only the market functioning and stability but also the growth of the whole economy.

There are two main gaps exerted from existing literature:

Firstly, there are insufficient and inharmonious empirical findings on the role of institutional ownership in enhancing stock market liquidity, and especially in emerging and developing countries. Emerging capital markets are frequently associated with substantial returns, considerable volatility, and diversification benefits, so they are regarded as highly potential profit-making opportunities for institutional investors (Barry et al., 1998). In recent years, the institutional investors have become pivotal actors in financial markets and gained increasingly important position in public listed firms because they usually have informational advantages and higher trading frequency than other groups of investors (Dang et al., 2018). The enormously rising participation of the institutional investors during the current decade paves the wave for enhancing a stable investor base for the emerging securities market, and then contributing to emerging market liquidity and efficiency. Therefore, it is crucial to look into whether institutional influences market liquidity, a key sign of how well and smoothly emerging capital markets are functioning and operating.

Compared to developed markets, institutional investors in emerging markets like Vietnam might have access to a narrower range of investment opportunities and the ability to enter and exit positions more challengingly due to lower market liquidity and smaller market sizes. As a result, institutional investors in developed markets often have access to more sophisticated and diversified investment strategies, whereas those in emerging markets have a trend of dominantly rely on traditional investment approaches due to limitations in market infrastructure and sophistication. Besides that, there are stricter limitations on the foreign investors in emerging markets compared to developed markets, affecting the investment strategies of international institutional investors. Additionally, emerging markets are often in a phase of rapid growth and development, so the institutional investors’ actions have a more pronounced impact on the still-evolving infrastructure and liquidity dynamics of these markets compared to more mature and developed markets. Subsequently, examining the impacts of institutional investors on stock market liquidity in emerging markets is crucial due to the unique characteristics and the growth potential of these markets, and this investigations aids in understanding how these markets can efficiently channel capital for economic development.

Secondly, the impacts of the institutional investors on the liquidity in different countries could be dissimilar due to some unique attributes, so it is vital to thoroughly research a particular market individually to draw essentially rational implications. In recent years, the Vietnamese stock market with two major trading platforms, Ho Chi Minh Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX), recently takes the lead in ASEAN stock market in terms of growth in trading value and market capitalization and names among Top 10 fastest growing markets in the world (The World Bank, 2022). Thereby, it boosts investor confidence and attracts both domestic and international investors, especially institutional investors. One of the uniqueness of this emerging market refers to the fact that the institutional traders only account for 15% of the traded value. Nevertheless, these institutions have more prominent role in this emerging stock market because they are active players with a vast wealth of value-enhanced and private information as well as their trading activity decisively influences on the individual investment. Additionally, the market witnesses a tremendous growth of the institutional participants in the current years. As of December 2021, there was over 17,000 institutional investors, equivalent to an increase of 92.15% compared to 2015 (Vietnam Securities Depository, 2021). The active participation of the domestic and foreign investors contributed to improving the market value and liquidity. From 2008 to 2021, the trading value massively grew by nearly six times to reach the value of approximately 5,500 trillion VND (Vietnam Securities Depository, 2021). On November 3, 2021, the stock market liquidity reached a new high, with approximately 52 trillion VND (more than 2.2 billion USD) worth of shares traded across all bourses. (Hanoi Stock Exchange, 2021; Ho Chi Minh Stock Exchange, 2021). While the Vietnam stock market may not represent all aspects of every emerging economy, its growth trajectory, regulatory improvements, attraction of foreign investment, and economic development align with many characteristics commonly associated with emerging markets. Studying the Vietnam stock market provides valuable insights into the dynamics and challenges faced by these economies as they continue to evolve and integrate into the global financial landscape. However, there is scant empirical research considering the mentioned relationship in the Vietnamese stock market, one of the outstandingly potential emerging markets during the past decade.

The Vietnamese government holds substantial ownership and exerts significant control over strategic industries, impacting decision-making and policies, whereas other markets dominantly have a more extensive representation of private companies. Comparatively, in other stock markets where foreign ownership restrictions are more relaxed than the Vietnamese stock market, the market liquidity might be higher due to more actively traded stocks, diverse investor interests, and greater international participation (Viet Nam News, 2021). Moreover, the majority is made up by individual traders who has inactive trading nature with a lack of essential knowledge, ability, and skills to capture and analyze information, thus it could lead to issues relating to crowd psychology and risk of contagion (Vietnam Securities Depository, 2021). The uniqueness of the Vietnamese ownership structure differentiates it from other markets, influencing investment strategies, business operations, and economic policies within the country. Understanding the uniqueness of ownership structure in emerging markets in general and Vietnam in specific is crucial in assessing and managing liquidity in this stock market.

Subsequently, this work will fulfill these existing gaps, and this research offers one general contribution that could be applied in not only Vietnam but also other countries and one specific contribution that focuses on the case study of Vietnam. Firstly, this research makes original contributions to the literature by shedding light on whether the institutional ownership has been beneficial effects on the stock liquidity, and it pursues investigation by taking a case study of Vietnam as an intriguing example for emerging countries. This research on the Vietnamese stock market could be utiilized as a basis for generalizing observations to other financial markets involves critical analysis, synthesis of information, and thoughtful consideration of the broader financial landscape. Secondly, it contributes to the literature by considering the above uniqueness of the institutional investors in the Vietnamese stock market when examining the impacts of the institutional investors on this emerging stock market liquidity. Additionally, it also provides implications for policy formation and practice to boost the Vietnamese market liquidity as well as bring more benefits for institutional investors.

The Amihud (2002) illiquidity measure has been employed as a legitimate and trustworthy proxy for liquidity. This research uses robust standard errors to solve issues related to heteroskedasticity as well as firm-level clustered standards errors in order to tackle autocorrelation issues. In addition, this research includes the year and industry fixed effects to control for the seasonality and variation across several years and industries. Further, this research performs various robustness tests on the statistical models used in the research to assess the stability of findings under different scenarios or alterations in variables to ensure the reliability of conclusions.

This research strives to study whether the relationship between stock liquidity and ownership structure in Vietnam over the years are dominantly based on the adverse selection hypothesis or trading hypothesis. The paper is structured as follows. The next section reviews recent research related to the relationship between institutional investors and liquidity. Section 3 presents the data sources, variable construction, and descriptive statistics. After that, the empirical findings are showed in Section 4. Finally, Section 5 draws conclusions as well as highlights the original contributions of this research and key implications.

Literature Review

Institutional investors generally obtain better information access and have more active trading activities than other investors. Both theoretical and empirical studies on how the institutional ownership affects the stock liquidity has been added to the literature recently. Since liquidity plays a significant role in the price discovery of assets, it has garnered a great deal of interest from investors and scholars worldwide. Numerous studies have laid the academic foundation of the relationship between stock liquidity and ownership structure over the years, and they are mainly based on two focal hypotheses—adverse selection hypothesis and trading hypothesis (Rubin, 2007).

According to the adverse selection hypothesis, when superior information was privately possessed by informed shareholders, they tend to have strategical and deliberate trading behaviors to maximize the value of private information (Kyle, 1985). Dominant institutional ownership could lead to higher conservatism in firms’ financial reporting, and thus entail a thorny issue of information asymmetry (Ramalingegowda & Yu, 2012). It could cause a decline in the number of uninformed traders in the market, boosting the inventory costs and average transaction costs per share of the investors (Easley & O’Hara, 1992; Glosten & Milgrom, 1985; Kyle, 1985). By that way, it contributes to the reduction of the market efficiency and liquidity.

Several empirical studies reveal and demonstrate the valuable contributions of institutional ownership to the stock liquidity improvement. The outcome was in alignment with the results obtained from the studies of R. Almutairi (2013), Liu (2013), Boone and White (2015), Ali and Hashmi (2018), and Hunjra et al. (2020). The research of R. Almutairi (2013) shows that the participation of institutional shareholders contributes to improving the information transparency and the audit quality, so it demoralizes fraudulent practices and moral hazards. Furthermore, they could beneficially obtain internal information, thus the greater institutional ownership is associated with better management transparency, more efficient data analysis, and more aggressive actions for maximizing information advantages (Ali & Hashmi, 2018). As a result, the upward trends in institutional ownership would narrow spreads with a smaller proportion attributable to adverse selection, diminish the cost of liquidity-related services by amelioration of the informational asymmetry as well as lower transaction cost, thereby amplifying the liquidity (Ali & Hashmi, 2018; Boone & White, 2015; Liu, 2013; R. Almutairi, 2013). Consistent with this opinion, the research of Dang et al. (2018) reveals that better access to information, highly frequent trading activity and intense competition of the informed institutions could contribute to cutting transaction costs and lessening information asymmetry in the financial market. By that way, the institutional ownership exerts a profoundly positive impacts on the stock liquidity, and they could play a constructive role in diminishing stock illiquidity in the market with lack of fairly transparent information disclosure or inferior regulatory environments (Dang et al., 2018). The investigation of Blume and Keim (2012) for both NYSE and NASDAQ stocks also goes along with this idea and supports that the climb of institutional traders resulted in a downward trend of illiquidity, and the roles of institutional ownership become more crucial over time in explaining illiquidity from 1998 through 2010 (Blume & Keim, 2012). Ajina et al. (2015) investigates a sample of 162 listed companies in France and finds that the dominant ownership of the institutional investors performing high levels of transactions among their investment portfolios is positively aligned with the stock market liquidity. This confirms the signal theory and the trading hypothesis. Additionally, pension funds usually manage massive assets, which minimizes transaction costs and hence boosts liquidity (Ajina et al., 2015). Dyck et al. (2019) added that gaining favorable financial returns as well as social achievement are the motivations of institutional investors, one of the most crucial significant contributors of the market liquidity. In alignment with these opinions, Hunjra et al. (2020) studies 114 manufacturing listed companies in Pakistan, India, Singapore and Australia from 2010 to 2018 and concludes that the concentrated institutional ownership has a massively positive influence on the stock market liquidity because the institutional shareholders could monitor the corporate managers.

In contrast, the trading hypothesis posits that when the institutional investors increase trading frequency and rebalance their portfolios more often, it substantially brings down the transaction costs and supplies the stock liquidity (Demsetz, 1968; Merton, 1987; E. W. Sun et al., 2014). Furthermore, the proportion of stocks owned by institutional investors is much more massive than that of retail investors, so these institutional investors could react more promptly in trading volume of shares (El Ouadghiri et al., 2022). The rapt attention and intense competition of these informed traders stimulate the rate at which is reflected in prices, thereby enhancing the market efficiency and liquidity (Admati & Pfleiderer, 1988; El Ouadghiri et al., 2022; Holden & Subrahmanyam, 1992; Y. Sun & Ibikunle, 2017). Various researchers provide persuasive evidence for the inverse impacts of the institutional shareholders on stock liquidity. The empirical findings of Brockman et al. (2009) show that the institutional investors holding dominant shares in the listed companies exert a negative impact on their trading volume and stock liquidity. Some potential mechanisms could include their lack of informational advantage, or their stagnation even when having informational advantage due to legal framework and regulations, or the insufficiency of market consideration and matching even when they exploit value-enhancing information (Brockman et al., 2009). It entirely goes along with the study of Rhee and Wang (2009). These authors express that this problem could be explained as follows, higher level of information asymmetry caused by foreign institutional ownership, or more significant volatility given by their large trades, or reduction of competition in liquidity supply as there are dominant traders, or lack of the active trading by these institutional investors (Rhee & Wang, 2009). Additionally, the research findings are aligned with the studies of Boujelbene et al. (2011), Syamala et al. (2014), and Tran et al. (2018). Due to the existence of asymmetric information and preference to liquid stocks, the intensity of these institutional traders incurs escalating trading costs to uninformed investors (Syamala et al., 2014). Moreover, increasing percentage of shares by institutional investors could enlarge the adverse selection component (Boujelbene et al., 2011; Tran et al., 2018). Along with the views of previous researchers, the empirical findings in Vietnam of Tran et al. (2018) during and post the global crisis imply that their increasing participation could boost the price impact as well as decline the depth of stock. As a result, the institutional ownership alleviates the market liquidity.

Besides that, some studies show that the influence of institutional investors on stock liquidity depends on the degree of their ownership in the listed company as well as their holding period. It is evident from the empirical investigation of Rubin (2007) that institutional ownership in general favorably affects stock liquidity, but their concentrated ownership can have two-side effects on the liquidity. On one hand, concentrated ownership can strengthen liquidity by reducing the number of traders in the market and increasing the ability of large shareholders to coordinate their trades (Rubin, 2007). On the other hand, concentrated ownership could lead to insider trading, which discourages other investors from participating in the market and lowers overall liquidity (Rubin, 2007). The findings are consistent with the outcomes obtained from the study of Agarwal (2007). There is a U-shaped monotonous relationship between shares held by institutions and stock liquidity (Agarwal, 2007). Institutional ownership could boost liquidity by raising the number of the active traders and improving information quality in the market. However, high levels of institutional ownership could cause more price volatility and tighter liquidity due to their tendency to trade in large volumes. Furthermore, Wang and Wei (2021) added that the investment horizons of the institutions could yield mixed impacts of their ownership on stock liquidity. The short-term institutional ownership pushes up stock liquidity through highly trading activity (Wang & Wei, 2021). Nonetheless, due to high information asymmetry between firms and outside investors, the long-term investors tend to weaken their trading activity, thus generating more adverse selection and lessening stock liquidity (Wang & Wei, 2021). Therefore, the impacts of institutional investors on stock liquidity vary based on the ownership structure and investment horizon.

Subsequently, the empirical investigations on relationship between liquidity and ownership structure offer inconsistent findings as dissimilar ownership proxies in different countries and especially in emerging markets might vary their suitability of capturing the two mentioned hypotheses. More precisely, there is insufficient and inharmonious research on the emerging stock markets. In addition, it is vital to study whether the institutional ownership has profound effects on the stock liquidity in the emerging countries, and this study pursues investigation by taking a case study of Vietnam due to the unique nature and impressive growth of the Vietnamese stock market. Based on the above discussion, this study strives to examine whether the Vietnamese stock market follows adverse selection hypothesis or trading hypothesis.

Sample and Methodology

Our primary variables of interest refer to institutional ownership and we focus on its impact on stock liquidity in emerging countries. To examine whether the Vietnamese stock market follows adverse selection hypothesis or trading hypothesis, Ordinary Least Square (OLS) and Fixed Effects Model (FEM) regression models are used to investigate statistical analysis on the data sample of the listed companies on the two major stock exchanges in Vietnam. We account for the year and industry fixed effects, and statistical tests are based on standard errors clustered at the firm level.

Measurement of Variables

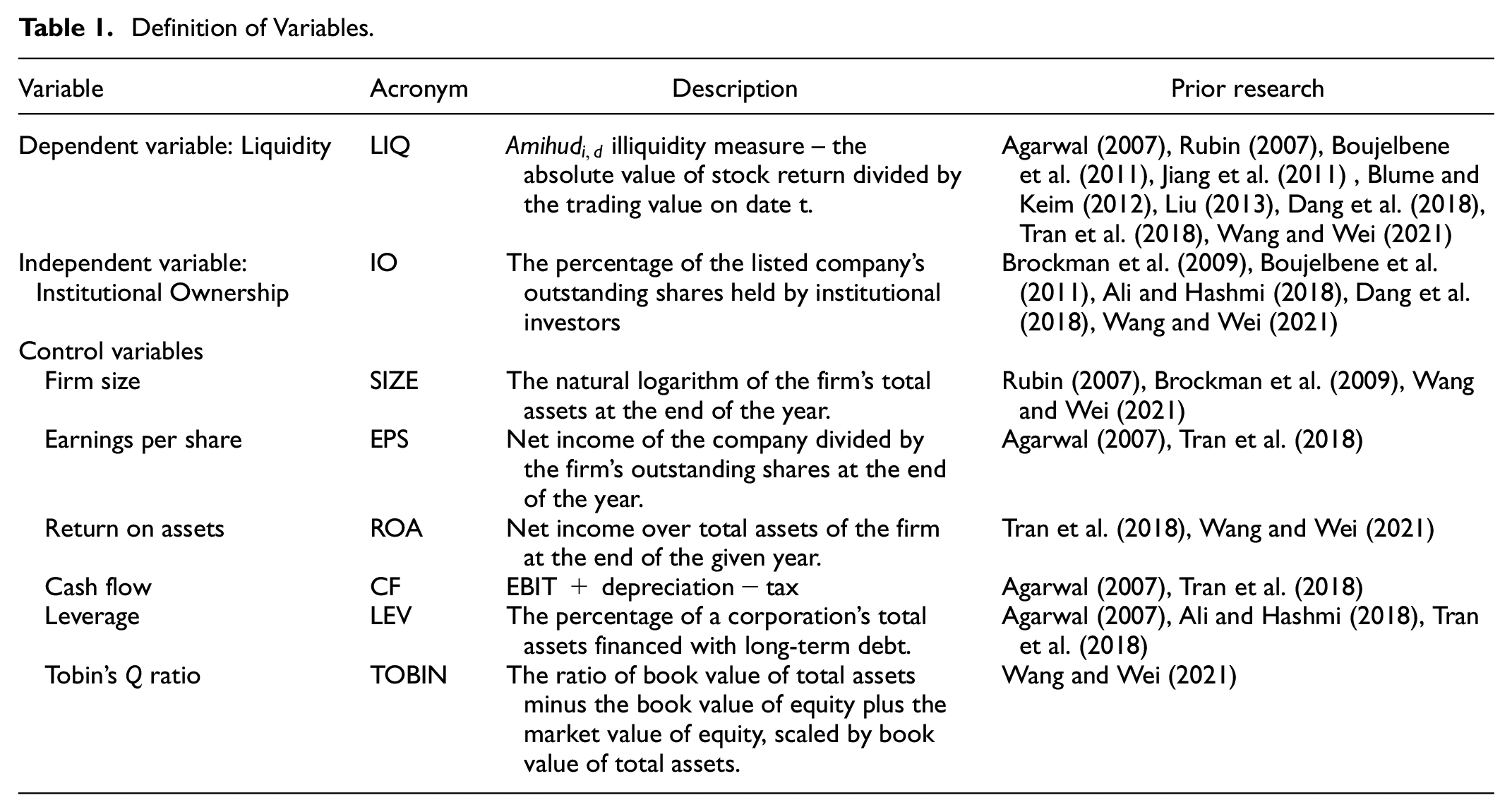

According to Table 1, the Amihud (2002) illiquidity measure has been commonly employed as a legitimate and trustworthy proxy for liquidity in prior research since there is a substantial association between this variable and other liquidity proxies based on microstructure metrics. Goyenko et al. (2009) support that this illiquidity ratio is a good proxy for price impact of the order flow. Following the prior research, this Amihud measure is employed in this study. According to Amihud (2002), stock illiquidity refers to the ratio of the daily absolute value of returns to the daily trading value for each stock on a given day, and it is calculated as follows:

where

Definition of Variables.

High Amihud value implies a significant change in the share price even with a small transaction. In other words, greater Amihud ratio for a specific stock indicates that it is less liquidity. To de-emphasize outliers in the regression model, the authors transform the daily Amihud liquidity measure of a stock i into its annual measure by taking the natural logarithm of the simple average of its daily measures in each year.

In regard to the independent variable, the institutional ownership is defined as the ratio of the total shares held by institutional investors over the total number of the firm’s outstanding shares at the end of a given year (Boujelbene et al., 2011; Brockman et al., 2009). Furthermore, the extant literature implies that some firm-specific traits may influence the effects of institutional ownership on stock liquidity (Brockman et al., 2009; Rubin, 2007). Following the previous research, this regression analysis employs several firm-specific control variables to separate the net impact of the independent variable on the dependent variable with the aim of alleviating the dominant impacts of firm-specific factors on the relationship between the institutional ownership and the stock liquidity. The firm-specific control variables comprise: Firm size (SIZE), Earning per share (EPS), Return on assets (ROA), Cash flow (CF), Leverage (LEV), and Tobin’s Q ratio (TOBIN). Detailed information is provided in Table 1. In order to reduce possibly malign influences from outliers, the authors winsorize the sample distribution of each continuous variable excluding the variables transformed by logarithm all continuous variables at the 1% and 99% levels.

To examine the impacts of institutional ownership on stock liquidity of companies listed in HOSE and HNX while controlling for other factors, this research estimates numerous forms of the provided cross-sectional regression:

Where: LIQi: the variable measuring liquidity of stock i; IOi: the institutional ownership, the percentage of the listed company’s outstanding shares held by institutional investors; Controlsi: the control variables for firm-specific characteristics (explained in Table 1).

All the variables in the formula (2) are calculated on an annual basis. Furthermore, this research model also encompasses industry-fixed effects (θi) and year-fixed effects (δy) to control the significant effect of the industry and the year on the relationship between the institutional ownership and the stock liquidity. Additionally, all the independent variables are employed in the regression model in a one-lagged version. Thanks to the lagged independent variables in the regression, the impacts of reverse causality between stock liquidity and institutional investors could be mitigated.

In the financial panel data set, there could be correlation of regression disturbances over time and across firms by using OLS estimation, thereby causing biased statistical inference or unreliable t-statistics confidence intervals and hypothesis results. To address this issue, this research uses robust standard errors to solve issues related to heteroskedasticity as well as firm-level clustered standards errors in order to tackle autocorrelation issues. In addition, this research includes the year and industry fixed effects to control for the seasonality and variation across several years and industries.

Data Sample

Various relevant data, including closing stock price, daily trading volume, financial data, and data for ownership structure provided in their annual reports and financial statements, are gathered to effectively capture the impacts of the institutional ownership on the stock liquidity. This research employs the dataset of all non-financial firms listed in the two major stock exchanges, HOSE and HNX, between 2008 and 2017. The data is obtained from FiinGroup, a top integrated platform providing a wide range of data, including financial data, business information, industry and market research as well as other relevant data in Vietnam. Therefore, by evaluating cross-sectional data across time series, the panel data analysis in this work offers more valuable and profound information with less variability and less multicollinearity. This sample could be considered reasonably representative of the Vietnamese stock market. Because this research encompasses all non-financial firms listed on these two major exchanges to provide a comprehensive insight of various industries, company sizes, and market capitalizations within the Vietnamese stock market. Furthermore, analyzing data from all listed non-financial firms reflects the overall market behavior, performance, and trends of these companies within the Vietnamese economy during the study period.

Results, Findings and Discussion

Descriptive Statistics

Table 2 provides descriptive statistics for dependent variable—stock liquidity—measured by Amihud’s illiquidity ratio, independent variable—institutional ownership, and control variables in the regression for the research sample in the Vietnamese stock market from 2008 to 2017. The results show that institutional investors hold approximately 31.43% of the total outstanding shares of the listed companies in the market. In other words, institutional investors do not account for the dominant proportion, and individual ownership is significantly greater than the institutional ownership in this emerging market with over 68%.

Summary of Statistic Variables.

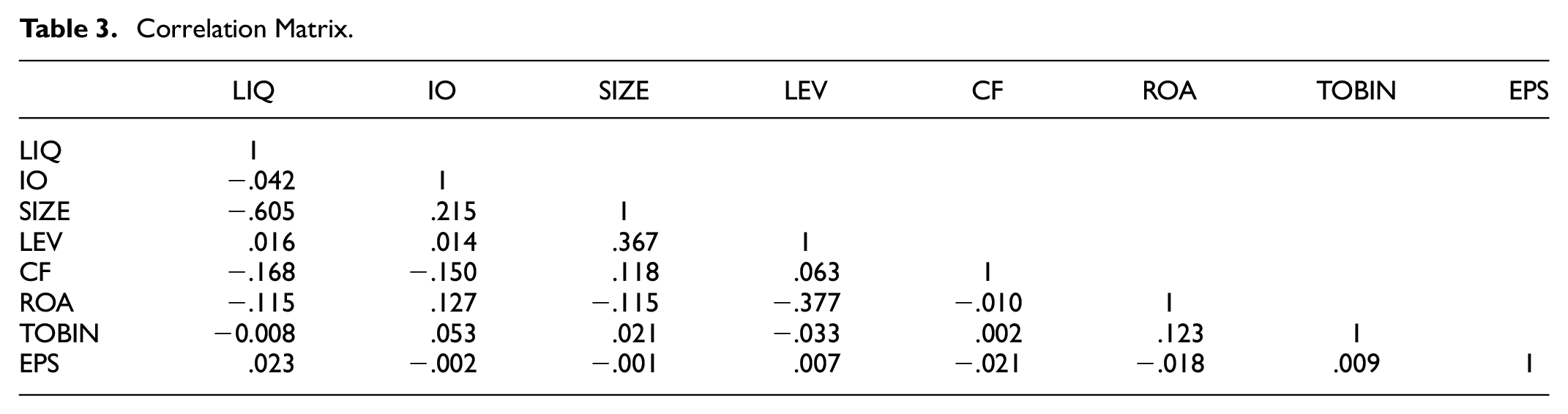

Table 3 presents the correlation matrix of these mentioned variables employed in this research. There are quite low Pearson correlation coefficients between the variables, thereby mitigating concerns related to multicollinearity in this regression analysis.

Correlation Matrix.

Institutional Ownership and Stock Liquidity

Our primary variables of interest refer to institutional ownership and we focus on its impact on stock liquidity in emerging coutries. In this study, OLS and FEM regression models are used to investigate statistical analysis on the data sample of the listed companies on HOSE and HNX over 10-year period from 2008 to 2017. The authors account for the year and industry fixed effects, and statistical tests are based on standard errors clustered at the firm level.

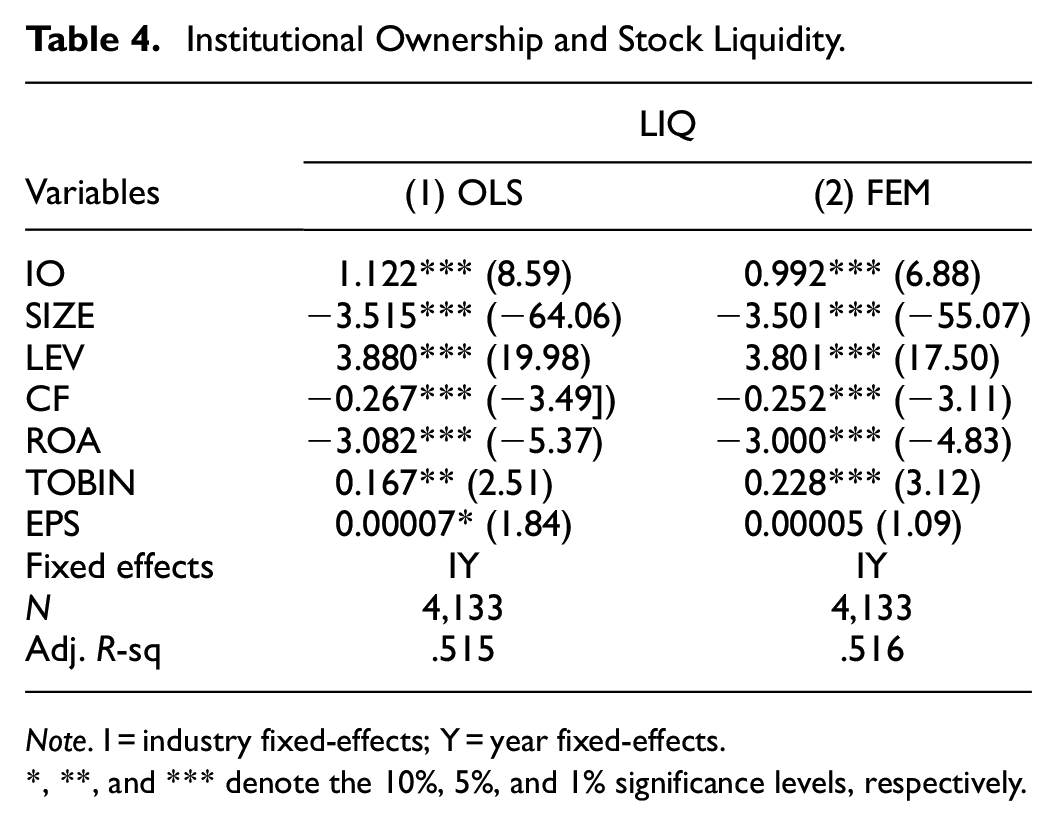

As reported in Table 4, the regression estimated coefficient of institutional ownership is 1.122 (t-stat = 8.59) and 0.992 (t-stat = 6.88) for OLS (1) and FEM (2) respectively at the significant level of 1%. The positive coefficient estimates of institutional ownership intimate that the stock illiquidity is significantly positively correlated to institutional ownership. More precisely, the growth of institutional ownership could exert devastating impacts on stock liquidity. Furthermore, the R2 values from the regression analysis are relatively high, which indicates that the selected variables and fixed effects could considerably explain the variation in the stock liquidity.

Institutional Ownership and Stock Liquidity.

Note. I = industry fixed-effects; Y = year fixed-effects.

, **, and *** denote the 10%, 5%, and 1% significance levels, respectively.

Robustness Test

In this section, various robustness tests are performed to assess whether our findings in the previous section are reliable. Further investigations include regression model with the addition of the lagged dependent variable (LagLIQ), the controls of firm-fixed effects, and the exclusion of the financial crisis period of 2008.

Firstly, the previous section presents that institutional ownership would lessen stock liquidity by increasing the information asymmetry and imposing adverse selection costs. It is also assumed that institutional ownership is an exogenous set. However, the empirical study of Liu (2013) in the U.S. indicates that institutional investors generally prefer listed stocks with more sufficient liquidity. Thus, there is our possible concern related to endogenous issue that time-invariant and unobservable firm-specific characteristics could drive effect of stock liquidity on institutional investors. To address this issue, we add a 1-year lagged value of the dependent variable (LIQ) into the regression model. By that way, the time-series covariation between the variables could also be examined. Evidence from Table 5 shows that the coefficient estimates of institutional ownership are significantly positive. The coefficient estimates of the institutional ownership for the Amihud’s illiquidity measure are 0.451 (t-stat = 5.69) and 0.355 (t-stat = 3.93) for (1) and (2) at the significant level of 1%, correspondingly.

Institutional Ownership and Stock Liquidity (Lagged Dependent).

Note. I = industry fixed-effects; Y = year fixed-effects.

, **, and *** denote the 10%, 5%, and 1% significance levels, respectively.

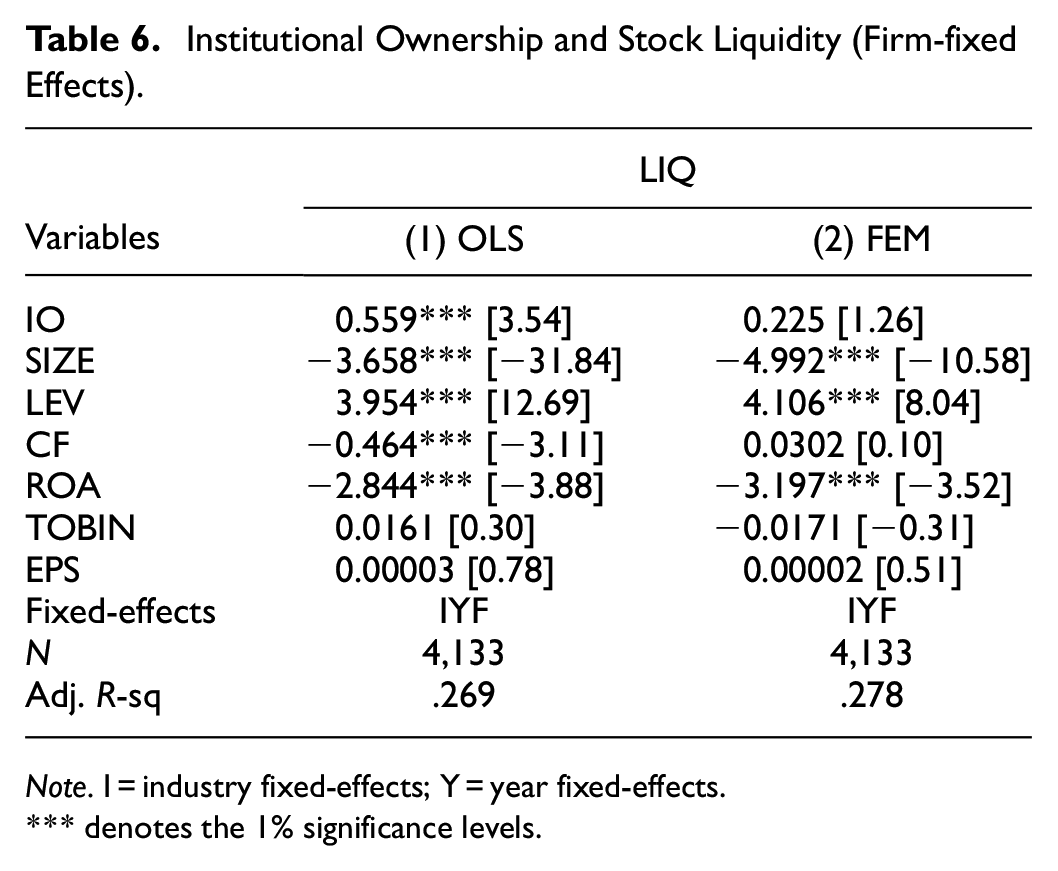

Secondly, the relationship between institutional ownership and stock liquidity could be influenced by unobservable firm-specific factors referring to time invariance or infrequent changes over time. To alleviate this heterogeneous concern, it is important to incorporate firm-fixed effects into the regression model. Table 6 exhibits that the coefficient estimates for the institutional ownership variable are 0.559 (t-stat = 3.54) and 0.225 (t-stat = 1.26) for (1) and (2), correspondingly. These findings demonstrate that institutional ownership has a detrimental effect on stock liquidity.

Institutional Ownership and Stock Liquidity (Firm-fixed Effects).

Note. I = industry fixed-effects; Y = year fixed-effects.

denotes the 1% significance levels.

Thirdly, the research period was between 2008 and 2017, including the time during the global financial crisis. To mitigate the influence of the global financial crisis on the overall findings for the detrimental impacts of institutional ownership on stock liquidity, the observation time was adjusted to start from 2009 until 2017 in Table 7. The Adjusted R-square coefficient of 52.8% and 52.1% corresponding to (1) and (2) indicate that the variability in the outcome data is still significantly explained by the model. The coefficient estimates of institutional ownership are statistically significant at the significant level of 1% with 1.157 (t-stat = 8.60) and 1.026 (t-stat = 6.87) for OLS and FEM. In other words, institutional investors would make notable contributions to the increasing illiquidity even when excluding the financial crisis period.

Institutional Ownership and Stock Liquidity (excluding Financial Crisis Period).

Note. I = industry fixed-effects; Y = year fixed-effects.

, **, and *** denote the 10%, 5%, and 1% significance levels, respectively.

In summary, the statistical results from these mentioned robustness tests strongly confirm the previous findings that an enlargement in institutional ownership could cause an unfavorable rise of stock illiquidity. The empirical evidence amplifies that institutional ownership has an adverse association with stock liquidity, therefore it is consistent with the adverse selection effects of institutions.

Discussion

This research findings are in harmony with the empirical results supporting the adverse selection hypothesis as proposed by Rubin (2007) of prior researchers (Boujelbene et al., 2011; Syamala et al., 2014; Tran et al., 2018). Compared to existing studies in emerging countries, this research findings concur with the studies of Rhee and Wang (2009) in Indonesia, Boujelbene et al. (2011) in Tunisia, Syamala et al. (2014) in India, and Tran et al. (2018) in Vietnam. It implies that the upward trend of institutional ownership could lessen stock liquidity. This seems to stem from the fact that institutional investors with superior and advantageous information could exacerbate problems of informational asymmetry (Easley & O’Hara, 1992; Glosten & Milgrom, 1985; Kyle, 1985). The amplification of information asymmetries and the intensity of the institutional traders causes the escalation of trading costs for uninformed investors, the rise of price volatility, as well as the reduction in total trading volume in the market, thereby contributing to lower stock liquidity.

On the contrary, this study dissent from the works of Boone and White (2015) in Russell, Ali and Hashmi (2018) in Pakistan, Dang et al. (2018) in 20 emerging markets as well as Hunjra et al. (2020) in Pakistan, India, Singapore and Australia. The finding that institutional ownership has a negative impact on stock liquidity in the Vietnamese stock market, contrary to findings in some other emerging markets, could stem from various factors unique to Vietnam’s market context. In specific, the presence of state-owned ownership in Vietnam could crucially influence market dynamics, whereas other markets are mostly less pronounced due to limited state ownership and control in most industries. Furthermore, foreign ownership restrictions in Vietnam are more stringent than others (Viet Nam News, 2021). Moreover, the majority is made up by individual traders with inactive trading nature who usually consider the investment trends of the institutional investors as their guidelines and benchmarks, so it is associated with crowd psychology and risk of contagion (Vietnam Securities Depository, 2021). Subsequently, these unique characteristics of the Vietnamese ownership structure differentiate it from the previous studies in the other mentioned emerging markets.

Conclusions

In this paper, we investigate the role of institutional ownership in the stock liquidity in Vietnam—a representative example of emerging markets. The research examines data of listed companies on the two key trading platforms, HOSE and HNX, between 2008 and 2017. The statistical findings through the analysis consistently supports that the institutional ownership exerts adverse effects on the stock liquidity. The original contribution of this study to academic literature refers to offering a profound insight of the relationship between the institutional investors and the stock liquidity in emerging markets by taking a case study of Vietnam. This research on the Vietnamese stock market could be utiilized as a basis for generalizing observations to other financial markets involves critical analysis, synthesis of information, and thoughtful consideration of the broader financial landscape. Moreover, it contributes to the literature by considering the above-mentioned uniqueness of the institutional investors in the Vietnamese stock market when examining the impacts of the institutional investors on this emerging stock market liquidity.

Based on the findings, the impact of institutional investors on Vietnamese stock market liquidity carries some valuable recommendations and implications for stakeholders such as policymakers and regulators, market participants, and corporate managers. Firstly, we commend that the policymakers and regulators should protect the rights of all market participants fairly. Encouraging higher transparency and disclosure requirements could help mitigate adverse effects of informational asymmetry. Regulatory bodies might reassess policies related to institutional investor activities to foster fair and efficient markets and they could involve revisiting trading practices, ownership limitations, or disclosure norms. Secondly, in the light of the current ownership structure in the Vietnamese stock market and this research findings, it is necessary to diversify the investor base. Besides that, educating and incentivizing both institutional and retail investors to engage in fair and transparent trading practices as well as encouraging their responsible and ethical investment behavior might mitigate adverse impacts on liquidity. Thirdly, for listed companies, strengthening information disclosure and transparency, better reporting practices, and emphasizing investor relations could improve market perception and liquidity. Another implication of this research for financial management refers to determining the optimal ownership structure to enhance their stock liquidity and build more effective investment portfolios. In conclusion, implementing these implications would require collaborative efforts from various stakeholders to address challenges associated with the impact of institutional investors on Vietnamese stock market liquidity. Policymakers, regulators, market participants, and corporations need to work together to create an environment conducive to fair, efficient, and liquid markets.

Our research is, however, subject to limitations owing to the challenges of accessing more updated and comprehensive information sources. Based on this research, we hope that future studies will investigate ownership structures more thoroughly and extensively, considering more detailed types of owners, such as government and foreign investors. This exploration should encompass financial industry groups and extend across more developing and emerging markets.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the Foundation for Science and Technology Development - The University of Danang, under grant number B2019-DN04-29.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.