Abstract

This study analyzes the impacts of ownership structure and business diversifications on the risk-taking behaviors of insurance companies in Vietnam. Foreign ownership and institutional ownership in the insurance sector are increasing significantly due to the privatization trend in Vietnam. Besides, business diversification allows insurance firms to maximize profits and reduce insolvency. Therefore, this study enriches the current literature because it is the first to examine how ownership and diversifications affect the risk-taking behaviors of insurance companies in Vietnam. We employ the Ordinary Least Squares, Fixed Effect Models, Random Effect Models, Generalized Least Squares, and dynamic system Generalized Methods of Moments to analyze 42 insurance companies from 2005 to 2020. Our findings indicate that business diversification increases the risk-taking behaviors of insurance firms. We also figure out a U-shaped relationship between institutional ownership and risk-taking behavior, with a turning point of 9.8%. This study also indicates an inverse U-shaped relationship between foreign ownership and insurers’ risk-taking behaviors, with a turning point of 20%. Thirdly, the interaction terms between ownership and diversification suggest the moderate role of business diversification in increasing the risk of insurance firms. Our findings align with agency theory, stakeholder theory, monitoring hypothesis, expropriation hypothesis, and prior literature. This study contributes practical implications for managers and policymakers to develop the insurance sector sustainably.

Keywords

Introduction

Reserve management refers to the process of effectively managing the reserves held by an organization. In the context of insurance companies, reserves are the funds set aside to cover future claims and other liabilities. The amount of reserves an insurance company holds is determined by various factors, such as the underwriting standards, the level of risk in its portfolio, and regulatory requirements.

Reserve management is essential for insurance firms because of the following reasons. Firstly, insurance companies collect premiums from policyholders and promise to pay out claims when certain events occur. These obligations are often spread out over many years. Therefore, effective reserve management ensures that the company has enough funds to meet these obligations when they come due. Secondly, reserves are critical for insurance firms to ensure financial stability. If a company has insufficient reserves, it may be unable to pay out claims, leading to financial instability. Third, insurance companies are subject to regulations that require them to maintain sufficient reserves to cover potential losses. Failure to comply with these regulations can lead to significant penalties and damage to the reputation. Fourthly, reserves can also provide insurance companies with investment opportunities to generate additional income. Effective reserve management involves balancing reserve needs with the opportunity for investment returns. Finally, insurance companies are exposed to a wide range of risks and uncertainties, such as changes in interest rates, natural disasters, and economic downturns. Effective reserve management helps companies manage these risks by ensuring they have sufficient funds to cover unexpected losses.

Odonkor et al. (2016) examine the determinants of insurance companies’ reserve adequacy in Ghana. The study found that reserve adequacy was positively related to firm size, profitability, and business growth. In contrast, leverage, liquidity, and insurance type negatively affect reserve adequacy. The study also highlighted the importance of reserve management in maintaining insurance companies’ financial stability. It noted that inadequate reserves could lead to insolvency and threaten the survival of insurance companies. Therefore, effective reserve management is crucial to ensure insurance companies can meet their financial obligations and remain solvent. In addition, the study found that regulatory requirements play a significant role in determining reserve adequacy. Insurance companies that complied with regulatory requirements had higher reserve adequacy than those that did not comply. This highlights the importance of regulatory oversight in ensuring insurance companies’ financial stability. Che (2019) conducted a study on the impact of reserve management on the profitability of life insurance companies in China. The study found that effective reserve management positively influenced the profitability of life insurance companies. The study also found that the impact of reserve management on profitability varied by company size. For small and medium-sized life insurance companies, effective reserve management positively impacted profitability more than for large companies.

Prior studies examine the trilogy between ownership structure, diversification, and risk management. Roberts and Yuan (2010) and Chou and Lin (2011) document that institutional investors have incentives to monitor strategic managerial actions and provide valuable resources for firms, such as information, knowledge, and experience, which help reduce the risk in a financial firm. Sakawa et al. (2021) proved that institutional investors increase firms’ risk to profit as shareholders by using their dominating power. In addition, Amor (2017) and Hammami and Boubaker (2015) suggest that foreign owners appoint new foreign managers who are often ill-informed about conditions in countries where they operate due to their limited knowledge, leading to higher risk. Ehsan and Javid (2018) found that foreign financial firms are better regulated and have better risk management experience. Recently, Sanya and Wolfe (2011) suggested that diversification helps insurance firms to reduce insolvency risk. Wu et al. (2020) argue that when financial firms expand their business into non-core activities, they encounter higher agency costs and information asymmetry. Besides, a lack of experience managing non-core activities increases insolvency risk.

We conduct this study in Vietnam because of the following reasons. In Vietnam, foreign ownership (FO) in the insurance sector is increasing significantly due to the privatization trend in the capital market. Our descriptive statistics report that foreign ownership in Vietnam has an average of 32.06%, which implies that foreign investor possesses, on average, 32.06% of the share outstanding of insurance firms. This ratio is higher than Huang et al. (2012) reported for Japanese (i.e., 23.4%). Chou and Lin (2011) find that foreign institutions have an effective governance mechanism to monitor the risk-taking behaviors of financial firms. Besides, the average institutional ownership in Vietnam is 23.92%, which is higher than Bangladesh’s insurers (Ullah et al., 2019). Institutional investors have incentives to monitor executive actions, which reduces the risk in financial firms (Roberts & Yuan, 2010). Unfortunately, prior studies have not examined the impact of institutional and foreign ownership on the risk-taking behaviors of insurance firms in Vietnam.

Our study significantly contributes to the growing literature in the insurance field. Firstly, Roberts and Yuan (2010) and Hammami and Boubaker (2015) because they examined the effect of ownership on the financial firm’s risk. Roberts and Yuan (2010) employed the two-stage regression (TSR) and showed that institutional ownership is, to some degree, endogenously determined. In addition, prior insurance studies such as Che (2019) and Filasti and Risfandy (2021) employed the Fixed Effects Model (FEM). However, we followed Marie et al. (2021) to utilize the dynamic system Generalized Method of Moments (GMM) for some reasons. Firstly, GMM is generally more efficient than TSR and FEM. GMM uses all available moment conditions to estimate the parameters, which can help to reduce the bias. Secondly, GMM is more likely to produce consistent estimates than TSR and the FEM if the number of instruments is relative to the sample size. Third, GMM is more robust to misspecification of the model than both TSR and the FEM. GMM uses moment conditions derived from the data rather than relying on assumptions about the distribution of the errors. Finally, GMM is a more flexible method than TSR and the FEM because it can estimate a wide range of models with different specifications, including models with non-linearities and heteroskedasticity. Furthermore, Hammami and Boubaker (2015) compute different risk proxies, such as the standard deviation of Return on Equity (SDROE), the standard deviation of Return on Assets (SDROA), and default risk (Z-score). We employed Loss Reserve as proxies for insurers’ risk-taking behavior because insurers take more risk when loss reserves are low. The loss reserve also reflects insurance firms’ operation because they must maintain sufficient reserves for future claims.

We collect data from 42 insurance companies from the Finnpro database and annual financial reports to close the literate gap. The final sample consists of 309 annual observations of 42 Vietnamese insurers from 2005 to 2020. This study employs the Ordinary Least Squares, Fixed Effect Models, Random Effect Models, Generalized Least Squares, and GMM estimations to investigate the effect of institutional ownership, foreign ownership, and business diversifications on the risk-taking behavior of insurance firms.

This study contributes several striking results. Our findings indicate that business diversification increases insurance firms’ risk-taking. The findings show a U-shaped relationship between institutional ownership and risk-taking behaviors, with a turning point of 9.804%. Moreover, there is an inverse U-shaped relationship between foreign ownership and insurers’ risk-taking behaviors, with a turning point of 20%. In addition, our findings suggest a moderate role of business diversification in increasing risks for insurance firms. Finally, the robustness test reports the persistent impact of business diversification on risk-taking behaviors before and after the enactment of the Law on Insurance Business in 2016. While an inverted U-shaped relationship between foreign ownership and risk remained robust after 2016, a non-linearity relationship between institutional ownership and risks was not robust after 2016.

Our study is unique because of the following ways. Our study is similar to Roberts and Yuan (2010) and Amor (2017) because we employ the linear relationship between ownership structure and a financial firm’s risk. However, our study has contributed to extending the existing literature on ownership structure and business diversification on risks. Our study extends the literature by considering a nonlinear relationship between institutional ownership, foreign ownership, and insurance firms’ risk-taking behaviors. Specifically, previous studies have analyzed diversification’s effect on risks. Our study develops prior literature by testing the moderating role of business diversification in increasing the risk of insurance firms by adding interaction terms between business diversification and ownership structure. Finally, we examine whether our main findings are robust before and after implementing the Law on Insurance Business in 2016.

Literature Review

The Proxies of Risk-Taking Behaviors

Odonkor et al. (2016) indicate that financial firms take more risk when excess reserves are low, and financial firms take a lower risk when excess reserves are high. This result suggests that when insurance companies receive that the markets are at risk, they like higher excess reserves than lending to borrowers, reducing risks.

The loss reserve is gaining attention for the following reasons. Firstly, the loss reserve protects the insurance system and is the most significant liability on the balance sheet (Che, 2019). Secondly, loss reserves affect insurance firms’ risk-taking behaviors because insufficient reserves erode insurers’ financial stability or cause insolvency (Eastman et al., 2018). Hence, efficient loss-reserve management is essential for insurance firms. Prior studies employ risk proxies such as Z-score, RROA, RROE, and loss reserve (Che, 2019; Mondher & Lamia, 2016; Skała et al., 2018; Vo, 2016). Z-score reflects the downside insolvency risk, while RROA and RROE measure the volatility of profitability. The loss reserve measures the risk associated with insurance activities and claims settlements. Therefore, we use loss reserve to measure insurance company risk in this study.

Theories

Agency theory is a contractual engagement between principals and agents to fulfill the principal’s best interests. Agents include suppliers, creditors, shareholders, and managers. However, these parties’ interests may not be aligned, leading to agency costs (Waluyo, 2017). The separation of ownership and management induces managers to pursue their benefits. That is why supervision is essential to reduce agency costs. Various proxies can reflect the supervisory role, including lenders who require managers not to violate the debt covenants. Agency theory suggests that risk-taking behaviors in the financial industry are primarily affected by ownership structure (Lassoued et al., 2016). Agency theory suggests institutional investors can discipline managers by overseeing their practices, reducing the insurer’s risk (Tornyeva & Wereko, 2012). Foreign investors invest in insurers of another country for a good return and ensure effective management monitoring to avoid managerial expropriation (Tornyeva & Wereko, 2012). Therefore, foreign investors also help reduce risks.

Stakeholder theory suggests that financial firms should consider the interests of all stakeholders, including foreign investors, in managing their risk. Applied stakeholder theory to examine the impact of foreign ownership on risk-taking behavior in financial firms. The study found that foreign-owned tend to take more risk due to their focus on maximizing shareholder value, which can lead to conflicts with other stakeholders. Foreign ownership can affect financial firms’ risk in several ways. For example, foreign investors may have different risk preferences than domestic investors. They may also have different expectations regarding performance and may require higher returns on their investment. As a result, foreign ownership can affect risk-taking behavior, such as underwriting and investment decisions. Stakeholder theory suggests that financial firms should consider the interests of foreign investors as one of many stakeholders in their risk management decisions. Insurers may need to balance foreign investors’ interests with other stakeholders, such as policyholders and regulators, in managing their risk. Moreover, foreign ownership may also affect the financial firm’s ability to manage risk. For example, foreign investors may have different risk management practices or be unfamiliar with local regulations, which could lead to increased risk. Financial firms may need to implement additional risk management measures, such as conducting more extensive due diligence on foreign investors or requiring them to follow certain risk management practices.

Wu et al. (2020) document that insurers expand their business lines to generate revenue from non-core activities. However, diversification theory suggests that expanding non-core business weakens the enterprise’s human and financial resources, leading to higher financial risk.

The Relationship Between Institutional Ownership and Risk-Taking Behaviors

Previous studies report mixed relationships between institutional ownership and the firm’s risk-taking. Sakawa et al. (2021) proved that institutional investors increase firms’ risk to profit as shareholders by using their dominating power. Therefore, we propose the following hypothesis:

H1: There are positive and significant relationships between institutional ownership and insurers’ risk-taking.

Conversely, Roberts and Yuan (2010) document that institutional investors have incentives to monitor strategic managerial actions and provide valuable resources for firms, such as information, knowledge, and experience, which help reduce the risk in a financial firm. In addition, Chou and Lin (2011) argue that foreign institutions have a dominant governance effect in monitoring the risk-taking behaviors of financial firms. Roberts and Yuan (2010) conclude that institutional investors help reduce a firm’s risk. Therefore, we propose the following hypothesis:

H2: There are negative and significant relationships between institutional ownership and insurers’ risk-taking.

According to the monitoring and expropriation hypotheses, there may be a nonlinear relationship between ownership concentration and the firm’s risk (Ehsan & Javid, 2018). The monitoring hypothesis documents that the concentration of ownership increases the financial firm’s risk-taking while the dispersion of ownership decreases the financial firm’s risk-taking. The expropriation hypothesis documents that ownership concentration may cause an agency problem. Besides, prior studies have a mixed relationship between institutional ownership and insurers’ risk-taking behaviors.

Conversely, Roberts and Yuan (2010) document that institutional investors help reduce the risk in a financial firm. Besides, institutional investors reduce firm risk by effectively monitoring management. This effect is even more pronounced when the fraction of institutional ownership is below the turning point. For firms below this point, institutional ownership risk is monotonically decreasing. Beyond the turning point, the gains from having higher institutional ownership are decreasing. Based on controversial results, we propose the following hypothesis:

H3: There is a U-shaped relationship between institutional ownership and the risk-taking behaviors of insurers.

The Relationship Between Foreign Ownership and Risk-Taking Behaviors

Previous studies report mixed relationships between foreign ownership and the risk-taking behaviors of insurance companies. Amor (2017) and Hammami and Boubaker (2015) found foreign ownership with a high insolvency risk. They explain that foreign owners will appoint new foreign managers who are often ill-informed about conditions in countries where they operate due to their limited knowledge, leading to higher risk. Lassoued et al. (2016) state that foreign investors encounter information asymmetry and agency costs. Therefore, foreign ownership may increase the risk to insurance firms if there are no efficient corporate governance mechanisms. Therefore, we propose the following hypothesis:

H4: There are positive and significant relationships between foreign ownership and insurer risk.

Conversely, Ehsan and Javid (2018) find that financial firms with foreign ownership also have a lower risk. Foreign investors offer innovative business models and develop human resources by training their branch employees. Especially foreign financial firms are better regulated, so they have better risk management experience. Foreign ownership reduces risk-taking behaviors, consistent with agency and information asymmetry theories. There is a conflict of interest between foreign investors and the firm’s managers. Therefore, we propose the following hypothesis:

H5: There are negative and significant relationships between foreign ownership and insurer risk.

However, Nguyen (2020) argues that foreign ownership can increase risk-taking in high-risk financial firms and reduce risk-taking in low-risk financial firms. Foreign owners can efficiently diversify risk, willing to take higher risks. Foreign shareholders also effectively control management activities, making managers more risk-averse. Therefore, ownership structure does not affect risk because the relationship depends on each financial firm’s risk level. Kim (2011) fails to support a non-linearity between foreign ownership and risk. In addition, prior studies document a mixed relationship between foreign ownership and risk-taking behaviors. Ehsan and Javid (2018) find that financial firms with foreign ownership also have a lower risk.

On the other hand, Amor (2017) and Hammami and Boubaker (2015) report a positive relationship between foreign ownership and insolvency risk. Therefore, we propose a U-shaped relationship between foreign ownership and risk-taking behaviors. Risk first decreases with foreign ownership at a decreasing rate to reach a minimum, after which risk increases at an increasing rate as foreign ownership continues to rise. Based on the above discussion, we have the following hypothesis:

H6: There is a U-shaped relationship between foreign ownership and risk-taking behaviors.

The Relationship Between Non-Core Activities and Risk

The core activities of insurers include insurance underwriting, reserving, claims settlement, reinsurance, and the non-core or banking activities engaged by some insurers. Non-core activities such as providing financial guarantees, asset lending, issuing credit default swaps (CDSs), investing in complex structured securities, and excessive reliance on short-term sources of financing (Bierth et al., 2015; Chang et al., 2018). Insurers can expand their business by getting diversification benefits from non-core activities (Chang et al., 2018; Sanya & Wolfe, 2011; Wu et al., 2020).

Prior studies show that insurers gain benefits from diversified activities. For example, Sanya and Wolfe (2011) suggest that diversification helps insurance firms to reduce insolvency risk. Conversely, Wu et al. (2020) argue that diversification increases agency costs and risks. When financial firms expand their business into non-core activities, they encounter higher agency costs and information asymmetry. As a result, shareholders are difficulties in monitoring managers and, thus, may intensify the agency cost. In addition, a lack of experience managing non-core activities leads to higher insolvency risk. Chang et al. (2018) also report that non-core activities increase systemic risk. Therefore, we propose the following hypothesis:

H7: There is a relationship between non-core activities and risk-taking.

Institution Ownership, Non-Core Activities, and Risk-Taking Behaviors

DeYoung and Torna (2013) suggest that diversification of the firm’s risk is more potent for larger institutions. Conversely, Saghi-Zedek (2016) finds that institutional investors’ presence has much expertise, assisting financial firms in reaping the benefits from more sophisticated activities. They conclude that financial firms involved as institutional investors benefit from diversification activities and will have higher profits and lower insolvency. Deng et al. (2013) also find that diversification helps financial institutions reduce risk. Based on the above discussions, we propose a hypothesis:

H8: Insurers with non-core activities and institutional ownership take additional risks.

Foreign Ownership, Non-Core Activities, and Risk-Taking Behaviors

Pennathur et al. (2012) examine the impact of ownership structure on diversification and risk. They figure that shifting to fee-based activities benefits financial firms by reducing default risk. Still, the impact of diversification is quite different between domestic and foreign financial institutions. M. Chen et al. (2017) report that foreign financial firms can benefit from diversification. In contrast, Berger et al. (2010) find a more substantial diversification discount for domestic financial firms than foreign ones. They explain this diversification discount by the shortage of managerial expertise in the management teams. Based on the above discussions, we have a hypothesis:

H9: Insurers with non-core activities and foreign ownership have a higher risk.

Other Determinants of Risk-Taking Behaviors

Filasti and Risfandy (2021) examined the relationship between leverage ratio and risk. They suggest that higher leverage discourages firms from taking higher risks. Conversely, Chang et al. (2018) and Bierth et al. (2015) find that leverage is the primary driver of insurers’ contribution to systemic risk.

There is growing literature exploring the effects of CEO gender on the risk-taking of financial firms. Some find that CEO gender negatively affects risk-taking (e.g., Marie et al., 2021; Skała & Weill, 2018). On the other hand, Othmani (2021) demonstrates that women on board are less conservative in monitoring risk and make more risky decisions.

Data and Methodology

Data

Our data sample includes 42 insurance companies in Vietnam. We collect data from insurance financial statements and Finnpro, the leading data provider in Vietnam (Fiinpro, 2020). Following Eastman et al. (2016), we exclude insurers reporting written non-positive assets, capital, or net premiums. We also screen insurers with extreme errors in their loss reserves (Che, 2019). We exclude observations that do not have sufficient information to calculate variables. We follow Grace and Leverty (2012) to keep observations with positive reserves. The final sample is a balanced panel with 363 firm-year observations from 2005 through 2020.

Our study uses several financial indicators such as loss reserve, foreign ownership (FO), institutional ownership (IO), non-core activities (Non-core), equity/asset (Leverage), and gender of the CEO (Gender). These variable definitions are explicitly described in Appendix A.

Estimation Methods

Initially, this study employed OLS, FEM, and REM. After employing required tests such as the Hausman test, and the Breusch-Pagan test, we choose the Pool regression model (OLS) as a suitable method for models 1, 2, 3, and the FEM for model 4 because OLS and FEM meet all the requirements of selection methods. Unfortunately, OLS and FEM may violate the autocorrelation and heteroskedasticity assumptions. Therefore, we employ the Generalized Least Squares (GLS) to mitigate the autocorrelation and heteroskedasticity issue. However, GLS is endogenous, so we use the GMM method to mitigate the above issues. Marie et al. (2021) suggest that GMM estimations mitigate endogeneity, unobserved heterogeneity, and autocorrelation problems. We also test the robustness of the main results before and after enacting the Vietnamese Insurance Business regulation in 2016.

Models Construction

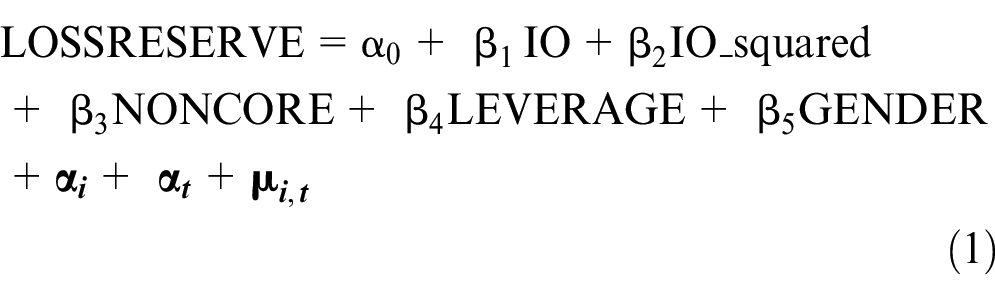

Following previous studies, we have four models to analyze the determinant variables’ effect on insurers’ risk-taking behaviors. Following Rober and Yuan (2006), we employ model (1) to estimate the effect of institutional ownership on insurers’ risk-taking in Vietnam insurers. Following Deng et al. (2013), we employ model (2) to estimate the effect of insurers’ institutional ownership and non-core activities on risk-taking in insurers in Vietnam. Following Hammami and Boubaker (2015), we employ model (3) to estimate the effect of foreign ownership on insurers’ risk-taking in Vietnam. Following M. Chen et al. (2017), we employ model (4) to estimate the effect of insurers’ foreign ownership and non-core activities on risk-taking in insurers in Vietnam.

In addition, we use models 1 and 2 to test the non-linearity between institutional ownership on insurers’ risk (Ehsan & Javid, 2018). We also employ models 3 and 4 to test the nonlinear relationship between foreign ownership on insurance risk-taking. Nguyen (2020) and Kim (2011) argue that foreign ownership can increase risk-taking in high-risk financial firms and reduce risk-taking in low-risk financial firms. This relationship depends on the level of risk of each financial firm. The econometric form of these models is stated as the following specifications:

Where LOSS RESERVE proxies for insurers’ risk-taking, insurers take more risk when loss reserves are low. The explanatory variables are Institutional ownership (IO), Foreign ownership (FO), Non-core activities (NON-CORE), and control variables, including Equity/Asset (LEVERAGE), Gender of the CEO (GENDER); the sign of “i” indicates cross-sections; the notation of “t” is time; “α” stands for intercept; and ε is the error term. The

Results and Discussion

Descriptive Statistics

Table 1 presents the descriptive statistics of the sample. Table 1 reports that the average loss reserve in our sample is 0.09. Thus, similar to prior studies (e.g., Che, 2019; Grace & Leverty, 2012), insurers in our sample are more likely to over-reserve. The average IO is 23.92%, implying that institutional investors have 23.92% of the total share outstanding of insurance firms. The institutional ownership in Vietnam’s insurers is higher than in Bangladesh’s (Ullah et al., 2019). The average FO in Vietnam is 32.06%, higher than in Japan (Huang et al., 2012). The mean of non-core activities in Vietnamese insurers reached 0.18, much higher than the average in Taiwan insurers, only 0.14 (Chang et al., 2018). Finally, Table 1 reports that the mean LEVERAGE is 0.41, and 91% of CEO is female in the Vietnamese insurance sector. These figures align with Filasti and Risfandy (2021) and Skała and Weill (2018).

Descriptive Statistics of Variables.

Note. It presents the sample descriptive statistics. The sample covers 42 Vietnamese insurers from 2005 to 2020. All variable definitions are in Appendix A.

Pearson Correlation Matrix

Table 2 presents the Pearson correlation matrix of the independent variables. This table shows that the correlations between variables are moderate. The maximum correlation between NON-CORE and IONO is 0.695, indicating a possible multicollinearity issue. Therefore, we test the variance inflation factor (VIF), the mean VIF is 1.635, and the maximum value of VIF is 2.182. The VIF of all the variables is less than five, so we conclude that there is no multicollinearity issue in our sample data (Callen & Fang, 2013).

Pearson Correlation Matrix.

Note. Table 2 presents the correlation matrix among independent variables. The sample has 42 Vietnamese insurers from 2005 to 2020. All variable definitions are reported in Appendix A.

p Values are in parentheses. The symbol ***, **, and *represents the significant level at 1%, 5%, and 10%, respectively.

Impact of Foreign Ownership, Institutional Ownership, and Non-Core Activities on the Risk-Taking Behaviors of Insurance Companies in Vietnam

Table 3 represents the regression results from OLS and FEM estimation. After employing required tests such as the Hausman test, and the Breusch-Pagan test, we choose the Pool regression model (OLS) as a suitable method for models 1, 2, 3. and the Fix Effects Model (FEM) for model 4 because OLS and FEM meet all the requirements of selection methods. The adjusted R2 of all models is above 30%, indicating that institutional ownership, foreign ownership, and non-core activities explain more than 30% of the variation in loss reserve. F-statistics is significant in that joint variables are all significant. The results show that regression results from FEM and OLS have a low p-value (<.001%), indicating the model’s suitability. However, OLS and FEM violate the hypothesis because the Wald test probability is less than .001. Hence, we re-estimate our results by the GLS method.

Regression Results From OLS and FEM Estimation.

Note. It represents the regression results from OLS for models 1, 2, 3, and FEM for model 4. The sample covers 42 Vietnamese insurers from 2005 to 2020. All variable definitions are reported in Appendix A.

p Values are in parentheses. The symbol ***, **, and *represents the significant level at 1%, 5%, and 10%, respectively.

Table 4 reports the estimation results from the GLS method. The Chi-square statistic for all models is smaller than 0.23; there is no overdispersion. Table 4 shows that the interaction term that insurers have non-core activities and institutional ownership increase risk. Besides, we also find that the other interaction term that insurers have non-core activities and foreign ownership increase risk. Higher business diversification increases the risk in all models by reducing the loss of reserves. Akbar et al. (2017) suggest that GLS is endogenous. Marie et al. (2021) recommend that GMM control endogeneity unobserved heterogeneity and eliminate autocorrelation problems. Therefore, we perform the dynamic system GMM to analyze our main findings.

Regression Results From GSL Estimations.

Note. It represents the regression results from Generalized Least Squares estimations. The sample consists of 42 Vietnamese insurers from 2005 to 2020. All variable definitions are reported in Appendix A.

p Values are in parentheses. The symbol ***, **, and * represents the significant level at 1%, 5%, and 10%, respectively.

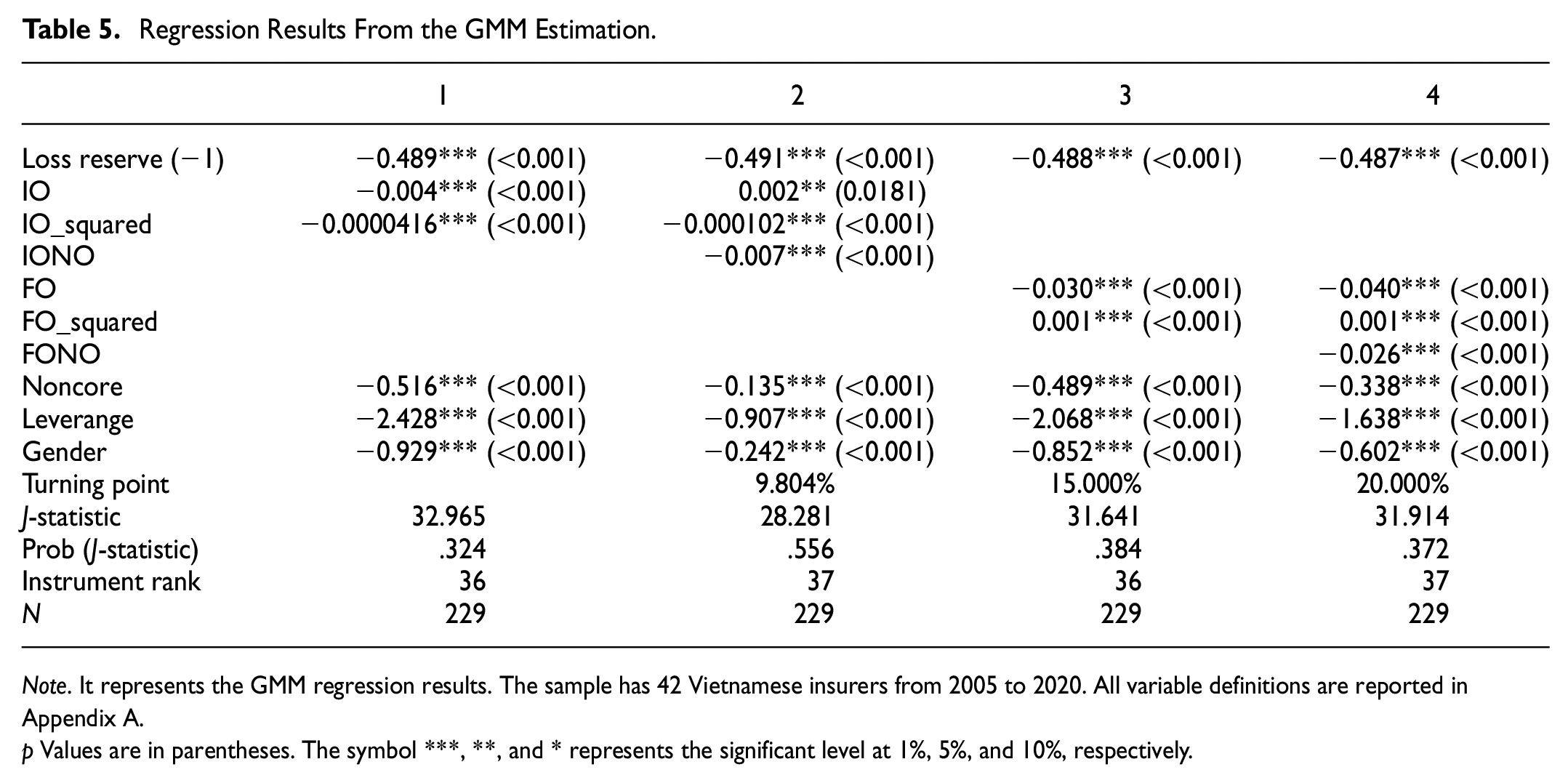

Table 5 reports a positive relationship between institutional ownership and loss reserve. Specifically, a percentage increase in institutional ownership reduces risk by 0.002%. Roberts and Yuan (2010) explained that institutional investors have incentives, monitor strategic managerial actions, and provide valuable resources for firms, such as information, knowledge, and experience, which help reduce the risk in a financial firm. Our results are consistent with the agency theory. Agency theory documents institutional investors can discipline managers by overseeing their practices, reducing the insurer’s risk. While our findings do not support hypothesis 1, they support hypothesis 2.

Regression Results From the GMM Estimation.

Note. It represents the GMM regression results. The sample has 42 Vietnamese insurers from 2005 to 2020. All variable definitions are reported in Appendix A.

p Values are in parentheses. The symbol ***, **, and * represents the significant level at 1%, 5%, and 10%, respectively.

Table 5 reports a U-shaped relationship between institutional ownership and the risk-taking behavior of insurance firms in Vietnam. The coefficient of IO_squared is negative and significant, implying that excess institutional ownership increases the risk-taking behavior of insurance firms. Table 5 also shows that the turning point of institutional ownership is 9.8%, implying that a percentage increase toward 9.8% reduces the risk of insurance firms. However, insurance firms risk higher when their institutional ownership exceeds 9.8%. Our findings also support hypothesis 3, which indicates a U-shaped between institutional ownership and the risk-taking behavior of insurance firms in Vietnam.

Table 5 reports a negative relationship between foreign ownership and loss reserve. Specifically, a percentage increase in foreign ownership increased risk by 0.040%. Hammami and Boubaker (2015) and Amor (2017) explained that foreign ownership would appoint new foreign managers who are often ill-informed about conditions in countries where they operate due to their limited knowledge, leading to increased risk. While our findings support hypothesis 4, they do not support hypothesis 5. Our results are consistent with the stake theory that foreign-owned tend to take more risk due to their focus on maximizing shareholder value, which can lead to conflicts with other stakeholders.

In addition, Table 5 indicates an inverse U-shaped relationship between foreign ownership and risk-taking. The coefficient of squared FO is significant, implying that excess foreign ownership reduces the risk-taking behavior of insurance firms. Table 5 also shows that the turning point of foreign ownership is 20%, implying that insurance firms take a higher risk when their foreign ownership increases to 20%. However, a percentage increase in foreign ownership excess of 20% reduces the risk of insurance firms. Ehsan and Javid (2018) suggested that foreign ownership helps reduce financial institutions’ risk because foreign investors develop human resources by training their employees. Especially foreign financial firms are better regulated and supervised and have better risk management experience. Lassoued et al. (2016) also suggested that foreign ownership discourages risk-taking. Information asymmetry and agency costs are possible explanations for this risk aversion. Besides, Our results are consistent with the agency theory that foreign investors invest in insurers of another country for a good return and to ensure effective management monitoring to avoid managerial expropriation (Tornyeva & Wereko, 2012). Therefore, foreign investors also help reduce risks. Our findings do not support hypothesis 6.

Table 5 also documents that business diversification increases the risk-taking behavior of insurance firms in Vietnam. For example, the percentage increase in non-core revenues leads to an increase of 0.516% in risk-taking behavior. Chang et al. (2018) and Wu et al. (2020) suggest that insurers expand their business lines to generate extra revenue from non-core services. However, the non-core business also erodes the enterprise resources, leading to higher financial risk. Therefore, our findings support the diversification theory that expanding non-core business weakens the enterprise’s human and financial resources, leading to higher diversification and financial risk. Our findings support hypothesis 7.

Table 5 reports all interaction variables with a higher risk that moderates the role of business diversification in increasing risk. Our results show that insurers with institutional ownership and business diversification risk more. DeYoung and Torna (2013) document that higher diversification positively increases the risk for larger institutions. Hence, our findings support hypothesis 8 that insurers with non-core activities and institutional ownership take additional risks, suggesting a moderating role of business diversification in increasing risks.

Table 5 also indicates that insurers with foreign ownership and business diversification have a higher risk. Our result is consistent with M. Chen et al. (2017). While foreign financial firms gain diversification benefits, they face substantial agency costs and information asymmetry problems, leading to additional risk. Hence, our findings support hypothesis 9 that insurers with non-core activities and foreign ownership take additional risks, implying a moderating role of business diversification in increasing risks.

Table 5 indicates that the coefficients of leverage in all models are negative and significant, implying that a higher leverage ratio causes a higher risk for insurance firms. Chang et al. (2018) and Bierth et al. (2015) report that leverage is the primary driver of systemic risk. Finally, the CEO gender is positive and significant with risk-taking behaviors in all models. Our result is consistent with Othmani (2021), demonstrating that women on board are less conservative in monitoring risk and make more risky decisions to improve financial performance.

Robustness Tests Before and After Implementing Law on Insurance Business in 2016

We employ the robustness check to confirm that our results remain robust before and after implementing the Law on Insurance Business in 2016. The Vietnamese government enacted Decree No. 73/2016/ND-CP detailing the Law on Insurance Business, dramatically affecting the insurance industry, especially performance riskiness. Thus, we divide the sample into pre-enactment (2005–2015) and post-enactment (2017–2020) and estimate the results using dynamic system GMM estimations.

Table 6 reports the persistent impact of business diversification on risk-taking behaviors. Table 6 indicates that interaction variables between business diversification and ownership structure remain robust. Insurers with institutional ownership and non-core activities take a higher risk before and after implementing the Law on Insurance Business. Insurers with foreign ownership and non-core activities take a higher risk before and after implementing the Law on Insurance Business.

Robustness Test Results From GMM Estimations Before and After Implementing the Law on Insurance Business in 2016.

Note. It represents the robustness test results from GMM estimations. The sample has 42 Vietnamese insurers from 2005 to 2020. All variable definitions are reported in Appendix A.

p Values are in parentheses. The symbol ***, **, and * represents the significant level at 1%, 5%, and 10%, respectively.

Table 6 shows that institutional ownership negatively correlates with loss reserve after 2016. There is an inverse U-shaped between institutional ownership and risks, implying that institutional ownership increased by the turning point at 167.192%, and risk increased. The turning point is 167.192%, which means institutional ownership increases, and the risk increases before the turning point. After the turning point, the risk decreases. Therefore, these findings differ from our main findings.

Table 6 shows that after 2016, FO is negative with loss reserve. There is an inverse U-shaped between foreign ownership and risk, implying that institutional ownership increased by the turning point at 31.219%, and risk increased. The turning point is 31.219%, which means foreign ownership increases, and the risk increases before the turning point. After the turning point, the risk decreases. Our robust findings are consistent with our main findings.

Conclusion

Previous studies report the linear relationship between institutional ownership, state ownership, and risks. This paper contributes to the literature by testing a nonlinear relationship between these ownerships and risk-taking behaviors in the insurance sector. Besides, previous research has examined how business diversifications affect insurance firms’ risk. This study adds the interaction term between ownership and business diversification to test the moderating role of business diversification in increasing risk-taking behaviors.

We employ the OLS, FEM, GLS, and GMM to analyze a sample of 42 insurers from 2005 to 2020 in Vietnam, a transition market in Asia. The main findings indicate that business diversification increases the risk-taking behaviors of insurance firms in Vietnam. Secondly, this study shows a U-shaped relationship between institutional ownership and risk-taking behaviors, with a turning point of 9.804%. The findings report an inverse U-shaped relationship between foreign ownership and insurers’ risk-taking behaviors, with a turning point of 20%. In addition, the interaction term between ownership and diversification also suggests that business diversification increases risks. Finally, our findings are robust before and after implementing the Law on Insurance Business in 2016.

Our findings suggest the following implications for policymakers to develop the insurance sector sustainably. Diversification requires significant resources, both financial and human. Policies and managers should allocate resources effectively to ensure the new ventures have the resources they need to succeed without neglecting the core business. This may involve reallocating resources from existing businesses or raising additional capital to fund the new ventures. Besides, policies and managers should develop a clear strategy for diversification that outlines the desired outcomes, the markets or industries to target, the resources needed, and the risks to be managed. The strategy should be flexible enough to adapt to changing market conditions and should be communicated clearly to all stakeholders. Furthermore, one way to mitigate diversification risks is to identify potential synergies between the core business and the new ventures. Synergies can arise from shared capabilities, customer bases, distribution channels, or other resources that can be leveraged across the organization. By identifying and leveraging these synergies, policies, and managers can increase the chances of success in new ventures. In summary, insurance managers should also consider other factors such as risk, return, strategic fit, regulatory requirements, and reliable information to make informed and sound investment decisions. Policymakers must closely monitor insurance firms’ business diversification and significantly restrict them from investing in securities and real estate markets via a cross-ownership approach.

In addition, our study shows that the average value of institutional investors in insurance firms in Vietnam is 23.92%, which is higher than the turning point. Moreover, the average value of foreign investors in insurance firms in Vietnam is 32.06%, which is also higher than the turning point. Therefore, managers and policymakers should readjust institutional and foreign ownership toward turning points to minimize risk.

Although this study contributes to the growing literature in insurance fields, it also has data limitations. The number of publicly-traded Vietnam insurers is relatively small compared to developed countries. The latter study may overcome data limitations by employing cross-countries analysis. Future studies may intensively examine non-core activities such as financial guarantees, asset lending, issuing credit default swaps (CDSs), and investing in complex structured securities. Finally, future research should compare the impact of business diversification and ownership structure between life insurance and non-life insurance firms.

Footnotes

Appendix

Variables Definition.

| Variables | Notation | Variable descriptions |

|---|---|---|

| Dependent variable | ||

| Loss reserve | Loss reserve | Loss reserve is measured by the difference between total incurred losses and the revised estimate of incurred losses in 5 years scaled by total net admitted assets (Che, 2019). |

| Independent variables | ||

| Institutional ownership | IO | The ownership of institutional investors (Callen & Fang, 2013). |

| Foreign ownership | FO | The ownership of foreign investors (Huang et al., 2012). |

| Non-core activities | Non-core | Non-core activities are the ratio of total on-balance sheet liabilities minus total insurance reserves to total liabilities (Chang et al., 2018). |

| Insurers have non-core activities and institutional ownership | IONO | Financial firms have diversification and institution ownership (Deng et al., 2013) |

| Insurers have non-core activities and foreign ownership | FONO | Financial firms have diversification and foreign ownership (M. Chen et al., 2017) |

| Equity/asset | Leverage | The total owner’s equity ratio to total assets (Filasti & Risfandy, 2021). |

| Gender of the CEO | Gender | A dummy variable equals one if the CEO is a woman and zero otherwise (Skała & Weill, 2018). |

Acknowledgements

We also thank anonymous reviewers for their constructive feedback, which helps us revise our manuscript

Author Contributions

Khoa Dang Duong (

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Ton Duc Thang University, Van Lang University, and Ho Chi Minh City Open University.

Ethical Approval

This study does not involve animals or humans.