Abstract

This paper seeks to examine whether the characteristics of the audit committee impact the timely reporting represented by audit report lag (ARL), firm-based abnormal audit report lag (FAARL), and industry-based audit reports lag (IAARL). The sample of the study includes mostly hand-collected 2,284 firm-year observations obtained from Turkey’s listed non-financial companies. Main regression results show that audit committee gender diversity, meeting frequency, and independence are negatively associated with timely reporting. Furthermore, additional analysis indicates the negative association between timely reporting and the audit committee effectiveness indexes created by the coexistence of the audit committee. Also, an interaction effect between audit committee independence and gender diversity concerning the timeliness of financial reporting has been documented. The use of fixed effects estimators and two-step system GMM estimator also supported the main results. This paper aims to provide concrete contribution to the literature by examining timely reporting in an emerging market like Turkey. The results suggest that regulatory bodies and companies should review the audit committee structure to better timely reporting and reduce firm and industry-based abnormal delays.

Plain Language Summary

This study aims to understand how the characteristics of audit committee influence the timeliness of financial reporting, as represented by three measures: audit report lag, firm-based abnormal audit report lag, and industry-based audit report lags. The research is based on data from 2,284company-year observations, mainly collected by hand from non-financial companies listed in Turkey. To analyze the data, the study utilized regression models and other advanced statistical techniques. The findings show that more diverse (in terms of gender), frequent-meeting, and independent audit committees tend to report more promptly. Additionally, when certain audit committee characteristics combine, there is an even stronger tendency toward timely reporting. These results imply that for better and more timely reporting, companies, especially in emerging markets like Turkey, might benefit from audit committees that are diverse, independent, and meet frequently. Regulatory bodies might also consider these findings when setting guidelines for audit committee structures.

Keywords

Introduction

The concept of timeliness has been recognized in previous studies as an important proxy for financial reporting quality (Afify, 2009; Al-Ajmi, 2008; IASB, 2010). Financial reporting timeliness, also known as audit report lag or delay, is the time between the end of the fiscal year and the release of the financial report (Ashton et al., 1987). Previous studies have provided considerable empirical evidence on the determinants of timely reporting such as “firm-related, corporate governance-related and auditor-related characteristics” (Al-Ajmi, 2008; Bhuiyan & D’Costa, 2020; Daoud et al., 2014; Durand, 2019; Habib et al., 2019; Khlif & Samaha, 2014; Leventis et al., 2005; Munsif et al., 2012). The better understanding of these determinants may lead to a reasonable reduction of time needed to prepare and publicize financial reports. However, while the above-mentioned studies mostly cover developed countries, the number of studies regarding financial reporting timeliness is limited in emerging countries such as Turkey.

Audit committees play a critical role in corporate governance characterized by accounting scandals, economic crises, and increased investor attention (Beasley et al., 2009; Khatib et al., 2022). The literature has shown that the audit committee holds an important role in supervising management’s compliance with accounting regulations, disclosure of financial information, and timely financial reporting. The audit committee is responsible for overseeing the financial reporting process and ensuring that shareholders and other stakeholders receive accurate and timely financial information (Bédard & Gendron, 2010), and playing a crucial role in financial reporting timeliness where the corporate governance practices are not well established (Hassan et al., 2017). An ineffective audit committee may cause delays in the release of financial statements, which can in turn impact the ability of investors and other users of financial statements to make informed decisions (Chan et al., 2016). The increase in its responsibilities and roles has brought the regulators and researchers to dwelling on the characteristics of audit committee directors.

Our study aims to investigate the relationship between audit committee characteristics such as the number of members, independence, financial expertise, number of meetings, gender diversity and financial reporting timeliness. Financial reports in developing countries differ significantly from other developed countries in terms of preparation time as well (Ben Rejeb Attia et al., 2019). The corporate governance features of Turkey considered in this study provide significant information about the current environment of financial accounting system. Like other developing countries, the timeliness of financial reporting in Turkey should bear more importance compared to the developed countries because the information contained in financial reports provide the only reliable source (Basuony et al., 2016). In emerging economies, shareholder rights may not be well protected as in developed economies and well-regulated environments. Therefore, the audit committee should be comprised of skilled and knowledgeable individuals ensuring the compliance of organization with relevant laws and regulations. Our expectation from the study is finding a solution to suggest a new dimension and making contribution to the literature with new empirical evidence by investigating the determinants of timely reporting in a developing country like Turkey.

The Covid-19 pandemic and the resulting economic downturn have led to the transition of capital from developed stock markets to developing ones (Laghari & Xu, 2022). The incentive leading to such a transfer of capital is the belief that developing economies are more resilient to shocks and offer greater potential for growth (Samitas et al., 2022). The Russia–Ukraine War has also contributed to this trend, as investors seek to diversify their portfolios away from instability. Considering recent developments, providing accurate and up-to-date information on a company’s financial status poses great significance as investors can, accordingly, make informed decisions on whether to continue to invest in a certain company. Such, in turn, helps to ensure a stable capital flow, essential for the continued growth of an economy. The timely submission of reports to investors is therefore critical to the sustainable capital flow in emerging countries (Bajary et al., 2023). In conclusion, the role of the audit committee in timely reporting is also of vital importance to ensure the sustainability of capital flow.

Many studies have revealed that the competence of audit committee in financial, accounting, and audit is one of the key factors in timely reporting (Abernathy et al., 2015; Baatwah et al., 2019; Ghafran & Yasmin, 2018). Cohen et al. (2022) suggests that audit committee, expert in finance, may demand further explanations in suspected situations caused by the financial information provided by management. On the other hand, few studies dwell on other basic audit committee characteristics. Though there are some empirical findings regarding audit committee size, independence, meeting frequency, and gender diversity in backgrounds, it is inconsistent and contradictory. Sultana et al. (2015) found the result depicting that having at least one financial expert on the audit committee shortened the audit report delays but failed to find evidence pointing gender diversity, meeting frequency, and size. Naimi Mohamad-Nor et al. (2010) indicates that meeting more frequently and a larger audit committee shorten audit report delay, while Oussii and Boulila Taktak (2018) find no evidence for audit committee meeting frequency and size impacting financial reporting timeliness. In order to fulfill the audit committee’s responsibilities effectively, such characteristics also bear importance other than financial expertise.

A growing body of research on gender diversity in audit committees can be seen (Bravo & Reguera-Alvarado, 2019; Sultana et al., 2020; Thiruvadi & Huang, 2011). Diversity in audit committees will bring out new perspectives and experiences contributing to the value of decisions. There exists the evidence that companies with gender-diverse audit committees are more likely to have better financial results. For instance, a study by Oradi and Izadi (2019) revealed that companies with women on audit committees are less likely to re-state their financial results. Yami and Poletti-Hughes (2022) found findings that demonstrate independent female executives on the audit committee reduce the risk of financial fraud. Mnif Sellami and Cherif (2020) documented that audit fee is higher when female executives are included in the audit committee. Despite the findings suggesting that gender diversity in audit committees is associated with better financial outcomes, there are some shortcomings in Turkey environment. Recent empirical studies in Turkey have revealed that there is no significant relationship between financial results and gender diversity (Arioglu, 2020; Khan et al., 2022). In addition, Turkey stands at lower ranks in many gender inequality indexes. For illustration, in the Global Gender Gap Report published by the World Economic Forum (WEF, 2021), Turkey ranks 133rd among 156 countries. These statistics show that women are underrepresented in corporate senior positions and audit committees in Turkey, providing an opportunity to examine whether gender diversity plays a role in the financial reporting process.

About 2,284 observations were obtained from non-financial companies, with all data available, traded in Borsa Istanbul between 2009 and 2019. Three proxies have been identified to measure financial reporting timeliness: audit report lag (ARL), firm-based abnormal audit report lag (FAARL), and firm-based industry audit report lag (IAARL). Results indicate the negative and significant association between audit committee independence, meeting frequency, and gender diversity with timely reporting. The fact that these results are obtained in Turkey, which is criticized in terms of corporate governance structure, signifies the importance of the findings. Women have very little space in senior management positions in Turkey, however it has been documented that the presence of female members in the audit committee is associated with audit report lag. Finally, no findings show that audit committee size and financial expertise are significantly associated with timely reporting, and it can be attributed to the fact that Turkish companies generally prefer employing only two members in audit committees and that no legal obligation enforces these members to be financial experts. After controlling for firm-level fixed effects, year * industry fixed effects, and endogeneity issues, our main findings are robust.

The current study is expected to provide several key contributions. First, the findings highlight the importance of audit committee characteristics in financial reporting timeliness, an essential requirement in emerging economies such as Turkey, to provide well-founded and timely accounting information to investors. Especially nowadays, when the economic impact of Covid-19 and the Russia-Ukraine war continue, capital flows from developed countries to developing countries, making it even more important to determine the factors affecting financial reporting timeliness. Second, our study may fill a literature gap by providing empirical evidence on how audit committee characteristics affect timely reporting. Furthermore, it may contribute to the financial reporting timeliness literature by investigating the effects of audit committee characteristics on firm and sector-based reporting delays in the analyses. Third, by including audit committee gender diversity to the audit committee effectiveness index developed by Rochmah Ika and Mohd Ghazali (2012), a new modified index was created. The modified index provides a more comprehensive evaluation of the effectiveness of audit committees. Finally, the findings depict that the presence of female members on the audit committee is an essential determinant of financial reporting timeliness in Turkish companies. Unfortunately, there is no legal regulation or advice regarding the employment of female audit committee members in Turkey. If the current guidelines provided by the Capital Markets Board (CMB) are not found sufficient to encourage firms to enhance diversity in company boards, we recommend, imposing further legal interventions.

Theoretical Background and Hypothesis

The Turkish Audit Environment is supported by an active and well-developed audit committee system. During the 1990s, the Istanbul Stock Exchange Market experienced a surge in the number of companies being traded. This growth, coupled with the need for Turkish companies to adhere to international financial reporting standards, led to the establishment of audit committees. Although in the early years, audit committees were characterized by several challenges, such as lack of understanding their role and purpose, and a lack of clarity in their mandate and responsibilities, today they have become an established and essential bodies in Turkish corporate governance environment. The legal framework for audit committees in Turkey was established by the Capital Markets Board of Turkey (CMB) in 2009. The CMB requires all public companies to have an audit committee in place. In addition, it has become obligatory for the audit committee to be composed of at least two members, all of whom are independent members of the board of directors, and to meet regularly, at least four times a year.

The timeliness of financial reporting is another important consideration in the Turkish audit environment. As per the regulations set forth by the Capital Markets Board (CMB), it is mandatory for all publicly traded companies to release their financial statements within a period of 2 months from the conclusion of the respective fiscal year. The aforementioned requirement guarantees that investors and other relevant parties are provided with precise and current financial data, imperative for making well-informed judgments, regarding commercial activities within Turkey. Failure to comply with this requirement can result in penalties and damage to a company’s reputation.

Financial reports must be disclosed quickly to decrease uncertainty in investment decisions and prevent the asymmetrical spread of financial information among stakeholders. As the timely information reporting contributes to the economic value of companies, determinants of delay are a worldwide concern for researchers, regulators, policymakers, and practitioners. Previous studies investigating the determinants of timeliness generally can be sorted into three categories: firm-related, audit-related, and corporate governance-related. Firm-related factors are firm size, financial condition, profitability, leverage effect, firm age, and industry type that effectively prepare and publish financial reports. Audit-related factors include the auditor size, auditor opinion, audit risk, auditor change, and internal audit. To illustrate, Habib et al. (2019) reports that audit reports are more delayed in companies with high financial risk. Bonsn-Ponte et al. (2008) found that larger companies demonstrate a tendency to disclose their financial reports earlier because they have easier access to resources. Leventis et al. (2005) document that assigning higher-quality auditors or paying extra audit fees may reduce audit report delays. Al-Ajmi (2008) demonstrates that company size, profitability, and leverage are associated with audit report lag.

Generally, corporate governance-related determinants receive the most excellent attention in studies of financial reporting timeliness (Bhuiyan & D’Costa, 2020; Firnanti & Karmudiandri, 2020; Khlif & Samaha, 2014; Lajmi & Yab, 2022; Munsif et al., 2012). Previous studies have shown that crucial corporate governance components, such as the board of directors and audit committee, are linked to critical financial accounting issues (Sultana et al., 2019; Turley & Zaman, 2004). However, evidence showing their impact on financial reporting timeliness is inconsistent. For example, Firnanti and Karmudiandri (2020) and Afify (2009) found that the number of independent board members is associated with lower audit delay. Lajmi and Yab (2022) and Naimi Mohamad-Nor et al. (2010) found no evidence indicating any association between audit committee independence, board size, board independence and audit report delay. Chalu (2021) and Afify (2009) showed that duality had a positive effect on audit report lag. However, Kawshalya and Srinath (2019) and Naimi Mohamad-Nor et al. (2010) report no findings indicating that duality is associated with audit report delay.

Recently, the use of modern approaches such as Audit 4.0 and blockchain in the audit process has become increasingly common (Elommal & Manita, 2022). Such techniques have revolutionized the way audits are conducted by introducing automation, real-time monitoring, and enhanced accuracy (Dai et al., 2019), allowing auditors improve the accuracy and efficiency of their work, as well as to increase transparency, accountability and timeliness in financial reporting. In contrast, traditional auditing techniques rely on manual processes and demand individual expertise. Developing countries, where traditional auditing techniques are predominantly used, often face challenges such as limited resources and inadequate audit infrastructure which may impede the ability to report financial information in a timely manner. In this respect, determining the factors affecting financial reporting timeliness in developing countries is comparatively more vital. Y. M. Hassan (2016) investigated the determinants of audit report delay for companies traded in the Palestine Stock Exchange Market and found that audit reporting delay was affected by factors such as the number of board members, audit quality, company complexity, audit committee presence, and ownership structure. Maranjory and Kouchaki Tajani (2022) reported that the independence of the audit committee of Iranian companies was negatively associated with audit report lag, while audit committee gender diversity was positively associated. Ahmed and Hossain (2010) found that auditor type, profitability and company size were associated with less delay of audit report in publicly traded companies in Bangladesh. The above-mentioned findings demonstrate that factors affecting audit report lag may vary across different countries and regions, highlighting the importance of considering local contexts and audit techniques used when examining audit committee effectiveness.

The audit committee’s research is based on the agency theory (Fama & Jensen, 1983). According to agency theory, the audit committee is a monitoring body that ensures the objectivity and reliability of financial information and accounting practices presented through financial statements in the capital market (Beasley et al., 2009) The audit committee protects the interests of shareholders by overseeing the quality of declared earnings and preventing misrepresentation of earnings (Fama & Jensen, 1983; Klein, 2002; Turley & Zaman, 2004). For the audit committee to fulfill these responsibilities properly, the audit committee must combine and utilize the necessary characteristics correctly and function effectively.

Previous studies have focused on the four central audit committee characteristics: size, independence, financial expertise, meeting frequency. The literature emphasizes that these four audit committee features are essential for the effectiveness of the audit committee because having an audit committee in a company is necessary but insufficient to improve financial reporting quality (Bajra & Čadež, 2018). With the increasing popularity of audit committee literature, it is not surprising to see that more studies have considered the audit committee’s effect on financial reporting timeliness. Previous studies suggest that there is a positive relationship between financial expertise and timely reporting of financial statements. However, findings showing how independence, size, and frequency of meetings affect financial reporting timeliness are scant and inconsistent. In addition, it is surprising that these studies did not report the relationship between audit committee gender diversity, a popular research topic, and audit report lag. This paper is expected to add empirical evidence showing the impact of audit committee characteristics on timely reporting. The following are hypotheses developed to be tested in this study.

Independence

Besides the financial expertise, audit committee independence is critical as audit committee independence improves committee effectiveness and financial reporting quality (Klein, 2002; Mardessi, 2022). The expectation from the independent members of the audit committee is to act independently and impartially while fulfilling their responsibilities and duties. In contrast, lack of independence may lead to impairment of financial reporting quality (Salehi & Shirazi, 2016), increased information asymmetry (Kao & Chen, 2020), and agency problems. Klein (2002) report that most independent members in audit committees have a restrictive effect on earning management. Abbott et al. (2004) found that the existence of audit committees composed of independent members is negatively related to financial restatements. Kamarudin et al. (2012) state the empirical findings that suggest audit committee independence positively impacts earning quality. Sultana et al. (2015) indicate that audit report delays are reduced if most audit committee members are independent. Therefore, we hypothesize that:

H1: There is a negative relationship between audit committee independence and timely reporting.

Financial Expertise

The audit committee substantially performs its oversight role in financial reporting process through its financial expert members. The presence and the quality of financial expert members help companies build a reputation, both in the eyes of independent audit firms and capital markets (DeFond & Francis, 2005). A lack of financial experts may lead to failures in financial reporting process. Thus, critical financial accountings figures, important for companies, may be disclosed to investors biased or delayed. Agyei-Mensah and Yeboah (2019) report that audit committees’ members who are not financial experts have difficulty in preventing aggressive earnings management practiced by managers. J. Krishnan and Lee (2009) found that companies with a high risk of litigation prefer employing more audit committee financial professionals. El Mahdy et al. (2022) suggest that information asymmetry will decrease if there is at least one financial expert member in the audit committee. Mah’d and Mardini (2022) suggest that audit committee financial expertise has a positive relationship with the level of disclosure of key audit matters. Financial expertise provides managers with an understanding of each role within financial reporting structures, helping to shorten the preparation of financial reports and facilitate timely disclosure of reports. Considering the above arguments, the hypothesis to be tested is formed as following.

H2: There is a negative relationship between audit committee financial expertise and timely reporting.

Size

Regulators emphasize that an audit committee must contain adequate members; otherwise, it might not be able to carry out its duties. There are two opposing views on audit committee size in the literature. Rochmah Ika and Mohd Ghazali (2012) argue that the number of audit committee members is one of the determinants of audit committee effectiveness and proposes that the higher in members presence will yield a better effectiveness. Raimo et al. (2021) claim that a larger audit committee significantly affects its activities in a positive manner and enables it to monitor financial reporting more effectively. An increase in the number of audit committee members reduces earnings restatement (Wan Mohammad et al., 2018) and restricts earnings management (Agyei-Mensah & Yeboah, 2019; Ngo & Le, 2021).

On the other hand, Collier and Gregory (1999) argue that a smaller committee will better perform its controlling and monitoring functions. Furthermore, large committees may be confronted with communication and coordination issues, and small boards will be agile in the decision-making process; thus, auditing activities will be accomplished in a shorter time. Aldamen et al. (2012) find empirical evidence that smaller audit committees are positively associated with firm performance during the 2008 crisis. Gao and Huang (2018) report that odd and smaller audit committees improve earnings quality. Based on these two opposing views, we formulate the below undirected hypothesis:

H3: There is a relationship between audit committee size and timely reporting.

Meetings Frequency

The number of audit committee meetings is a proxy of audit committee diligence that demonstrates the audit committee’s effort to discharge its responsibilities effectively. The audit committee must meet regularly to minimize overlooked errors in financial reports (Stewart & Munro, 2007; Vafeas, 1999) and to secure overall audit activities (G. V. Krishnan & Visvanathan, 2008). As audit committee members meet more frequently, communication among committee members, board and auditors strengthens (Cziffra et al., 2021), and audit quality improves (Sharhan & Bora, 2020), thus reducing the time necessary to prepare audit reports (Bédard & Gendron, 2010). The literature provides evidence for more meetings prevent management’s opportunistic behavior, thereby improving financial reporting quality (S. Hasan et al., 2020; Kent et al., 2010). The audit committee should meet more frequently, given its oversight responsibility in preparing and publicly disclosing financial reports. Accordingly, we effectuate the following hypothesis:

H4: There is a negative relationship between audit committee meeting frequency and timely reporting.

Gender Diversity

The recent growing stream of empirical research shows that the existence of female directors in the board and audit committee contributes to enhancing the effectiveness and monitoring activities (Francis et al., 2015; Strydom et al., 2017; Thiruvadi & Huang, 2011; Zalata et al., 2019). The psychology and management literature state that female members differ from men in basic communication, decision-making, and leadership (Arora, 2022; Hillman et al., 2007; Kirsch, 2018). Some studies show that women have more tendency toward financial conservatism, ethical behavior, and risk-averse (Briano-Turrent, 2022; Powell & Ansic, 1997). Prior research shows that gender diversity has led to more conservative reporting (Francis et al., 2015), lower earnings management (Gull et al., 2018), and reduced fraudulent and misleading financial statements (Capezio & Mavisakalyan, 2016). Based on such, we assume that audit committee gender diversity will affect the timely disclosure of financial reports. The hypothesis is as follows:

H5: There is a negative relationship between audit committee gender diversity and timely reporting.

Research Design

Sample

Table 1 shows the sample selection and industry breakdown. The sampling methodology includes a stratified-randomly selected sample of all firms actively listed on the Istanbul Stock Exchange Market (ISE) from 1 January 2009 to 31 December 2019. The initial sample comprises of 4,657 firm-years observations. The sample is chosen according to the following two criteria. Firstly, similar to the literature, financial companies are excluded from the study sample because of their different financial statement structures and processes (Baatwah et al., 2019; Sultana et al., 2015). The sample has been reduced to 4195 firm-year observations. Secondly, companies without any audit committee and that lack audit committee and financial data have been excluded.

Sample Selection and Industry Breakdown.

The companies that voluntarily established an audit committee before 2009 did so without any obligation. Therefore, companies made their audit committee-related data public voluntarily. With the establishment of the Public Disclosure Platform (KAP) in 2009 and the obligation to disclose the financial reports of listed companies in this electronic system, audit committee data of companies became available to the public. In this manner, the data used in the study was based on financial reports made public in 2009 and onward. The last year of our sample has been determined as 2019 because the global epidemic has damaged the financial structure of many companies.

The final sample consisted of 2284 firm-year observations, accounting for 49% of all market-listed companies. Data were obtained using a comprehensive database (FINNET) and manually collected data (annual reports). In addition to these data sources, Google search, investor relations pages on companies’ and directors’ websites were used simultaneously. Panel A of Table 1 shows the sample selection process, Panel B of Table 1 shows the distribution of the sample by sectors, excluding the financial services sector.

Research Model and Variables

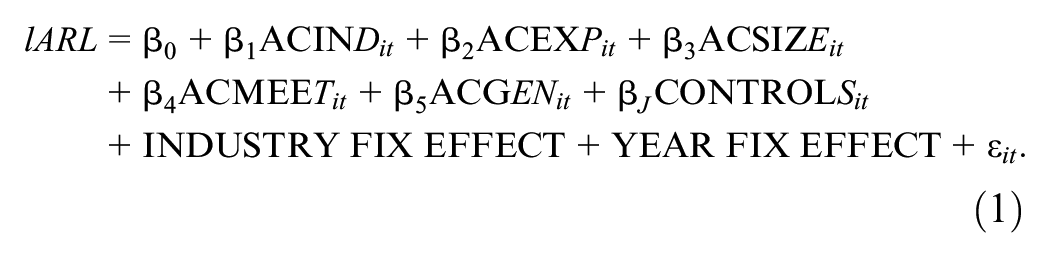

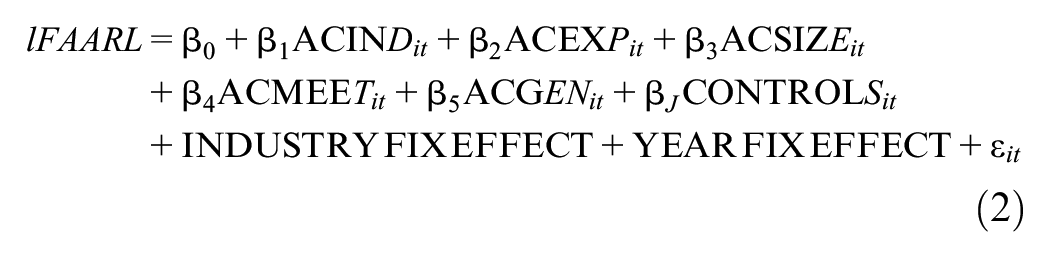

Audit committee features employed as independent variables are financial expertise, independence, size, meeting frequency, and gender diversity. Three proxies used are the audit report lag (ARL), firm-based abnormal audit report lag (FAARL), and industry-based abnormal audit report lag (IAARL)—for measuring financial reporting timeliness as a dependent variable. The Ordinary Least Squares (OLS) regressions with cluster-robust standard errors is utilized to provide empirical results. To mitigate the impact of outliers, the continuous variables were winsorized at the 1st and 99th percentile. Appendix A. shows how all the variables used in the analysis have been measured. The structural equation of the three models is:

Equation 1 depicts the first regression model investigating the relationship between independent variables and ARL. ARL is calculated by the difference between a company’s financial year-end and the date the company publicly releases its audit reports. ARL is consistent with most prior literature and is quite popular (Ashton et al., 1987; Knechel & Payne, 2001; Sultana et al., 2015). Equation 2 shows the second regression model investigating the relationship between independent variables and FAARL. FAARL is calculated by the difference between the actual ARL and the firm’s median ARL. This model examines the possible impact of audit committee characteristics on abnormal audit report lag that may occur on a firm-by-firm basis (Habib & Huang, 2019). Finally, Equation 3 shows the third regression model investigating the relationship between independent variables and IAARL. The IAARL is calculated to show the difference between the company’s actual ARL and the median ARL of the industry the company is in. IAARL is used to measure the impact of audit report delays on industries to which firms belong (Baatwah et al., 2015; Mande & Son, 2011).

If ACEXP, ACIND, ACMEET, and ACFEMALE affect financial reporting timeliness as predicted, the coefficients β1, β2, β3, and β5 (equating to H1, H2, H3, and H5) should be negative and statistically significant. As H4 is non-directional, If ACSIZE affects financial reporting timeliness as predicted, the coefficient β4 should be statistically significant.

To measure audit committee financial expertise, an indicator variable ACEXP is defined assigning 1 as the value for cases where at least one audit committee member has expertise in accounting and finance; otherwise 0. Concerning audit committee independence, another variable ACIND is defined as the proportion of independent members on the audit committee and, a variable ACSIZE, concerning audit committee size to indicate the total number of audit committee members. To measure audit committee meetings, a variable, namely, ACMEET to point the number of audit committee meetings held during the financial year; finally, an indicator variable ACGEN, concerning audit committee gender diversity is defined, assigning 1 as the value if at least one audit committee member is a female director; otherwise, 0.

Control variables are used to increase the predictive power of the model and to minimize the omitted-variable bias. Twelve control variables are housed in our models, empirically proven to affect financial reporting timeliness. The control variables are sorted into three categories: corporate governance-related, auditor-related, and firm-related. Control variables related to corporate governance include the total number of executives in the board of directors (BSIZE), The proportion of independent members on the board (B_IND), and assignment of the CEO and board chairman of different individuals (DUALITY). A larger board enables more directors to get involved in managerial processes and hence increases the quality of management decisions. Basuony et al. (2016) show that larger boards are significantly associated with shortened audit report lag. Independent board directors are considered tools for efficient management monitoring, making the financial reporting process more transparent and reliable (Afify, 2009; Fama & Jensen, 1983). Prior research shows a strong link between board independence and shortened audit report lag (Habib et al., 2019). A CEO or Chairman with a dominant personality may result in weak monitoring and audit quality. Such may lead to corporate governance practices that jeopardize the interests of shareholders. In this situation, the audit will take a long time to be completed (Forker, 1992). Previous research indicated that differentiation of people in chairman and CEO positions is associated with lower audit report lag (Basuony et al., 2016).

Control variables related to auditor include the auditing of company’s reports by Big 4 audit firms (BIG4), given an unqualified opinion on the company’s financial reports by audit firm (AOPIN), and audit firm rotation in the current year (AUDITCH). Auditing plays an essential role in reporting timeliness since it is a function of the financial reporting process (Türel, 2010). Prior research claims that auditing of financial reports by Big 4 audit firms is related to a shorter audit reporting lag because these audit firms have greater resources and well-programed audit procedures, thereby providing a higher-quality audit (Afify, 2009; Ocak & Ozden, 2018; Shukeri & Nelson, 2011). Long-tenured auditors are likely to have problems with objectivity and independence. On the other hand, short-tenured auditors cannot get fully familiar with firms’ business operations and financial reporting systems. Indeed, prior research shows that companies that changed their auditors in the current period had more delays in the audit report (Azami & Salehi, 2017). Because qualified reports may lead to misleading reporting, auditors are likely to spend more time on the audit process (Habib, 2013). In addition, prior research shows that qualified audit opinion leads to higher audit report lag (Dong et al., 2018; Ocak & Ozden, 2018; Shukeri & Nelson, 2011).

Finally, control variables related to the firm include gross revenue (SALES), the book value of total assets (SIZE), market-to-book ratio (M/B), debt/asset ratio (LEV), the proportion of net profit to total assets (ROA), proportion of net profit to shareholders’ equity (ROE), natural logarithm of firm age (AGE), receivables and inventory to total assets (INVREC) and being a multinational firm (MULTI). Larger firms can access more resources, more robust internal control systems, and more qualified accounting professionals. Also, larger firms are more demanding higher quality external audits. The literature indicates that firm size negatively relates to audit report lag (Al-Ajmi, 2008; Ashton et al., 1987; Owusu-Ansah, 2000). Sales growth is used as a measure of good and bad news. Prior research has reported that annual sales growth is considered good news for the investors and shortened the audit report lag (Knechel & Payne, 2001). The higher the leverage, the riskier the company’s financial situation, resulting in a longer audit process and indirectly delayed audit reports. Several empirical studies reported a positive relationship between leverage and audit report lag (Al-Ajmi, 2008; Owusu-Ansah, 2000). The market-book ratio, return on equity and return on assets are considered measures of firm performance. When the company is at a high loss, this is perceived as bad news, and audit report delays may be lengthened. On the other hand, this is perceived as good news when the company is highly profitable, and audit report delays may be shortened (Al-Ajmi, 2008). Older firms tend to have shorter audit report lags compared to younger firms, possibly due to the former’s more established and structured internal control systems. Additionally, younger firms may have less experience with the audit process and may require more time to gather and prepare the necessary documentation for the auditors. It is also possible that older firms have stronger relationships with their auditors, which can lead to a more efficient audit process (Efobi & Okougbo, 2014). A firm’s liquidity, effectiveness, and overall financial performance can be usefully understood by looking at the ratio of receivables and inventory to total assets, a proxy for corporate complexity (Durand, 2019; Habib et al., 2019). For example, it is possible that a high ratio of receivables and inventories to total assets could lead to delays in the audit process if there are discrepancies or issues with the accuracy of these metrics. Audits can be complex and time-consuming, especially for large multinational firms with operations in multiple countries. On the other hand, multinational firms may be more responsive to the demands of global investors demanding timely and accurate information to make informed decisions. Lee et al. (2008) gathered empirical proof that managers of multinational companies submit their financial reports earlier than other firms.

Results and Discussions

Univariate Tests

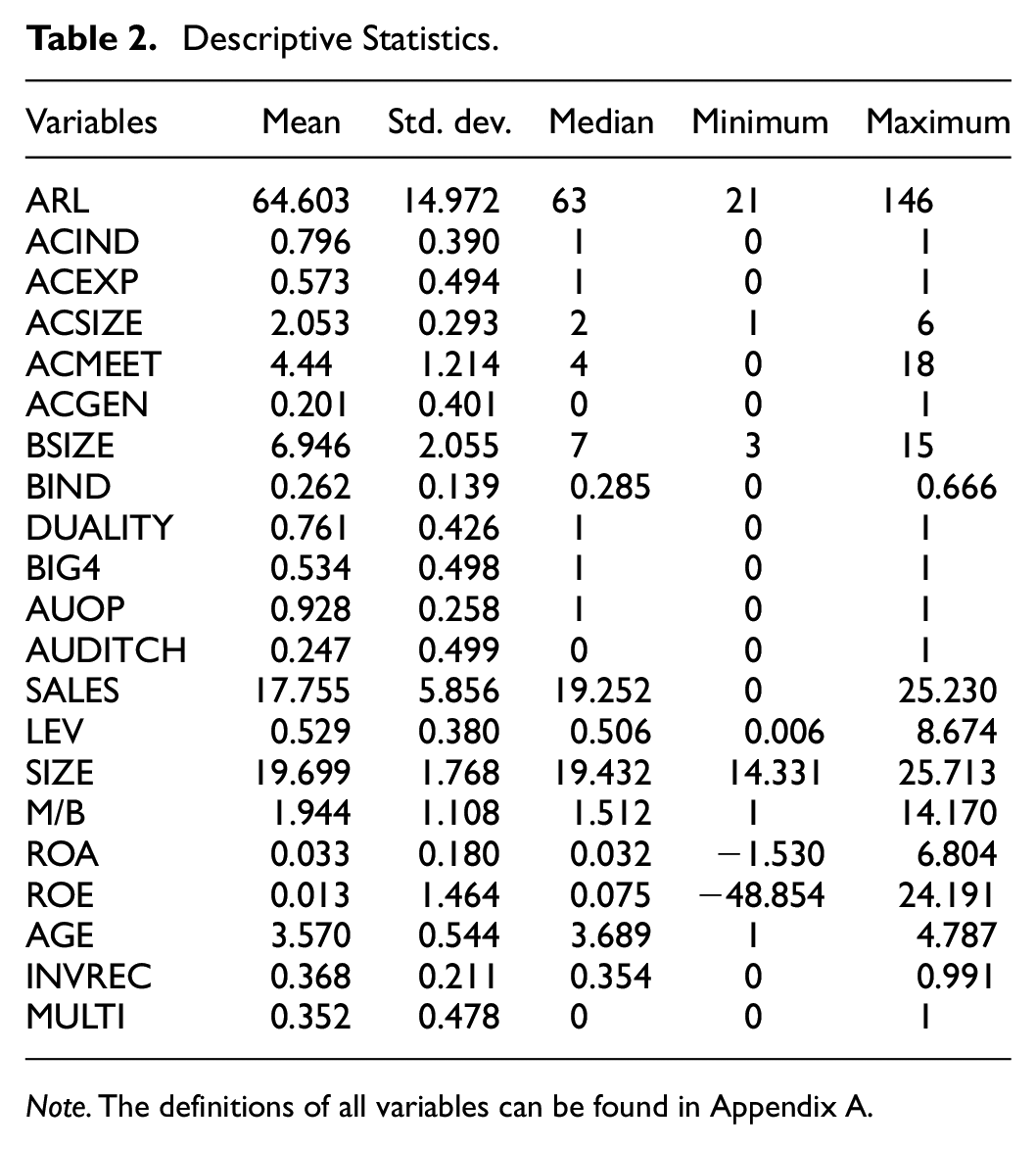

Table 2 shows the mean, standard deviation, median, maximum, and minimum values of the regression model variables. The mean-median-value for ARL is 64 to 63-days, indicating that the companies in the sample release their financial reports approximately 2 months from the end of the fiscal year. This period is relatively short compared to other countries; for example, 55 to 70 days in the United States (Abernathy et al., 2015), 64 days in the UK (Ghafran & Yasmin, 2018), 88 days in France (Khoufi & Khoufi, 2018), and 80 days in Australia (Sultana et al., 2015). The minimum and maximum ARL values are 21 and 146 days, respectively.

Descriptive Statistics.

Note. The definitions of all variables can be found in Appendix A.

Audit committees of companies usually consist of two members, and the number of members does not exceed six members. About half of our sample (0.537) includes at least one financial expert member on the audit committee. The proportion of independent members on the audit committee is 0.796, and this value shows that firms strive for their audit committees to be independent. Audit committee members meet four times during the reporting period (4.44), and the number of meetings does not exceed 18. Finally, one out of every five audit committees has at least one female member. This statistic shows that the audit committee gender diversity has not yet become fully widespread in Turkish companies.

Table 3 provides the Pearson correlation matrix correlation results for all variables. All independent variables are significantly correlated with timely financial reporting, except for the audit committee gender diversity. Table 3 also indicates several significant correlations involving control variables. Some of the correlation coefficients among the variables are well above .7 (e.g., the correlation between ACIND and BIND is .85). The computation of the variance inflation factor (VIF) is a reliable method for testing multicollinearity. The mean of VIFs is 1.47, the largest VIF factor observed for the full model was 3.54 (BIND) and the VIFs of all other independent variables are below 2.0 (Results have not been presented in tabular form in order to maintain conciseness.). VIFs are well below the commonly accepted threshold of 10, indicating that multicollinearity does not pose a problem for our study.

Pearson and Spearman Correlation Analysis.

Note. The definitions of all variables can be found in Appendix A. The symbols a and b denote statistical significance at the 1% and 5% levels of confidence, respectively.

Multivariate Tests

Table 4 shows the regression analysis results involving independent and control variables expected to affect financial reporting timeliness. The results for Equation 1 are reported in column1, for Equation 2 in column 2 and for Equation 3 in column 3. The results indicate that ACIND is negative and significantly associated with ARL (t = −3.66, p < .01), FAARL (t = −9.77, p < .01), and IAARL (t = −3.60, p < .01), confirming for H1. Whereas there is an extensive literature on audit committee independence and financial reporting timeliness, evidence is quite limited. While some studies report a significant relationship between audit committee independence and financial reporting timeliness (Naimi Mohamad-Nor et al., 2010; Oussii & Boulila Taktak, 2018), on the other hand, other studies find a negative and significant relationship between audit committee independence and financial reporting timeliness (Lajmi & Yab, 2022; Sultana et al., 2015). Our findings are consistent with Lajmi and Yab (2022) and Sultana et al. (2015). Agency theory suggests that audit committee independence is crucial for ensuring effective corporate governance and reducing the likelihood of financial fraud or misreporting. The independence of audit committee is expected to serve as a mechanism for better auditing the financial reporting process and ensuring that it is carried out in a timely and efficient manner. Our findings support the agency theory perspective.

Audit Committee Characteristics and Timely Reporting.

Note. The definitions of all variables can be found in Appendix A. The symbols ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels of confidence, respectively.

The results indicate that ACMEET is negative and significantly associated with ARL (t = −2.76, p < .01), FAARL (t = −2.05, p < .05), and IAARL (t = −2.91, p < .01), providing support for H4. While previous studies have provided evidence of a relationship between the frequency of audit committee meetings and the timeliness of financial reporting, this evidence has been inconsistent and contradictory. Lajmi and Yab (2022) state that the problems encountered in the financial reporting process can be identified at the audit committee meetings and if the frequency of the meetings is higher, there may occur some problems with the quality of the financial statements and the publication of the audit report may be delayed. In another study, Naimi Mohamad-Nor et al. (2010) state that more frequent audit committee meetings increase the likelihood of the audit committee reaching a resolution of financial matters and directing auditors to report on time. Our findings are consistent with Naimi Mohamad-Nor et al. (2010). According to the agency theory, meeting frequency is important to aligning their interests, as managers may prioritize their own interests over those of the shareholders. The audit committee must meet frequently in order to identify any potential conflicts of interest or unethical behavior within the organization (Stewart & Munro, 2007). More frequent meetings can enable members to be more successfully discharge their obligations, identify and eliminate financial problems faster, and thus shortening the audit process. The study’s empirical result is consistent with the theoretical framework of agency theory, indicating a negative association between the frequency of audit committee meetings and timely reporting.

The results show that ACGEN is negative and significantly associated with ARL (t = −1.97, p < .05), FAARL (t = −2.06, p < .05), and IAARL (t = −2.08, p < .05), providing support for H5. Given the potential benefits of gender diversity, it is not surprising to see that there has been an increased focus on increasing the representation of women on audit committees. However, there is still a lack of empirical evidence of the impact of gender diversity on audit committees. Few studies conducted have yielded mixed results. Some studies have found a positive relationship between gender diversity and financial reporting timeliness (Alkebsee et al., 2022), while others have found no significant impact (Sultana et al., 2015). Our findings are consistent with Alkebsee et al. (2022). The agency theory suggests that gender diversity in corporate boards can lead to better decision-making and performance due to a wider range of perspectives and experiences (Arvanitis et al., 2022; Carter et al., 2010). The presence of female directors is more likely to contribute to identifying potential conflicts of interest, developing a culture of discussion, improving transparency and ethical practices, and faster resolution of financial reporting problems. Our empirical findings are in line with agency theory perspective regarding the positive effect of gender diversity in audit committee functioning, which in turn may drawn on enhancing financial reporting timeliness.

The results indicate that the coefficients of ACEXP and ACSIZE are positive but insignificantly associated with ARL, FAARL, and IAARL, not providing adequate support for H2 and H3. These results are surprising because prior research have proven that the financial expertise of audit committee directors is an essential determinant of timely reporting (Abernathy et al., 2015; Baatwah et al., 2019; Ghafran & Yasmin, 2018). The empirical findings should be evaluated in the light of certain characteristics of the management styles and institutional context of Turkish listed companies. For example, regulatory bodies in Turkey do not make listed companies to have financial expertise for members of their audit committees obligatory, leaving it to the discretion of the companies. However, these companies are obliged to employ at least two members in the audit committees and generally prefer not to have more than two members. Insufficient financial expertise or lack of competence and the committees with less members, vital for audit committees to fulfill their duties, may increase the disruptions in the financial reporting process. These disruptions may also result in delays in the disclosure of financial reports. According to agency theory, larger audit committees are believed to provide better oversight and monitoring of financial reporting, leading to higher quality financial statements. However, some studies have found that larger committees have more resources and expertise to oversee financial reporting and reduce agency costs. Besides, agency theory suggests that audit committee financial expertise is positively associated with financial reporting quality, as financial experts are better equipped to understand and scrutinize complex financial information and identify potential misstatements or errors. Insignificant relationship between audit committee financial expertise, size and timely reporting shows that audit committee size and financial expertise are not consistent with the agency theory framework.

Our results show that most control variables are significantly related to financial reporting timeliness as expected (p < .05). The coefficients BSIZE, BIND, DUALITY, BIG4, AUOP, M/B, ROA, and ROE have been found to be negative and significantly associated with ARL, FAARL, and IAARL; and the coefficients LEV, INVREC, and MULTI to be positive and significantly associated with ARL, FAARL, and IAARL. These results are not surprising; thus, firms with a higher profitability level, more effective boards, and audit quality are expected to have no delay in the timeliness of financial reporting. In other words, the results suggests that companies with strong financial performance, good governance practices, and high-quality audits are more likely to report their financial information in a timely manner.

Additional Analyses

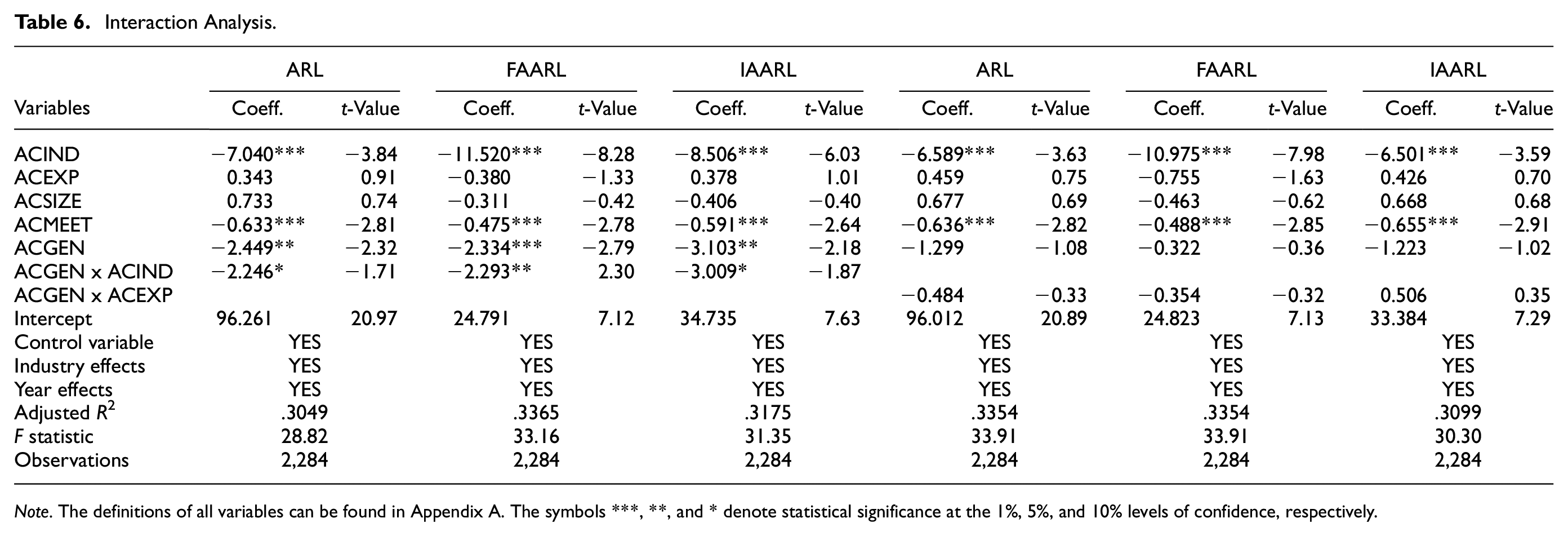

Our initial regression model used ACEXP, ACIND, ACSIZE, ACMEET, and ACFEMALE as audit committee characteristics. It has been argued by many authors that combining audit committee characteristics recommended by academic and regulatory bodies will increase audit committee effectiveness. Firstly, adhering to Rochmah Ika and Mohd Ghazali (2012), the audit committee effectiveness index (ACEFFECT4) is used and the relation to our dependent variables (ARL, FAARL, IAARL) is tested. The resulting assumption is that the characteristics of each audit committee are equally important. We create an audit committee effectiveness variable that takes a value between 0 and 1 by assigning values of zero or one for each of the audit committee characteristics. Second, we add audit committee gender diversity to this index (ACEFFECT5) and test whether it is related to ARL, FAARL, and IAARL.

The results of Table 5 depict that ACEFFECT4 is negative and significantly associated with ARL, FAARL, and IAARL, consistent with Rochmah Ika and Mohd Ghazali (2012). Furthermore, ACFEMALE is negative and significantly associated with ARL, FAARL, and IAARL. Besides, Table 6 indicates that ACEFFECT5 is negative and significantly associated with ARL, FAARL, and IAARL. The findings suggest that combining audit committee characteristics is a significant factor in ensuring timely reporting and reducing the lag of abnormal and industry-adjusted audit reports. Moreover, our findings suggest that even when audit committee characteristics are combined, they do not alter the significant association between gender diversity and ARL, FAARL, and IAARL as evidenced in the main regression results. This result supports the argument that gender diversity is a significant determinant of financial reporting timeliness. And accordingly, companies should review how to strengthen audit committee effectiveness further to shorten audit report delays.

Audit Committee Effectiveness and Timely Reporting.

Note. The definitions of all variables can be found in Appendix A. The symbols ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels of confidence, respectively.

Interaction Analysis.

Note. The definitions of all variables can be found in Appendix A. The symbols ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels of confidence, respectively.

Our main findings show that audit committee independence and gender diversity are negatively associated with financial reporting timeliness. Also, no significant relationship between audit committee financial expertise and timely reporting has been revealed. This phase is assigned to investigate whether there is a change in our primary findings by including interaction variables in the regressions. Table 6 shows the regression results with the interaction variables ACIND * ACFEMALE and ACIND * ACFEMALE. ACIND * ACFEMALE is negatively and significantly associated with ARL, FAARL, and IAARL accordingly. On the other hand, we figured out that no significant evidence that ACEXP * ACFEMALE is related to ARL, FAARL, and IAARL. These results support the evidence we obtained in our primary findings. Moreover, our results support the arguments that audit committee independence and gender diversity increase audit committee effectiveness and reduce audit report lag. However, although there is much empirical evidence in the literature (Abernathy et al., 2015; Baatwah et al., 2019; Ghafran & Yasmin, 2018), we could not find evidence that audit committee financial expertise is a determinant of reporting timeliness for Turkish firms.

Robustness Analyses

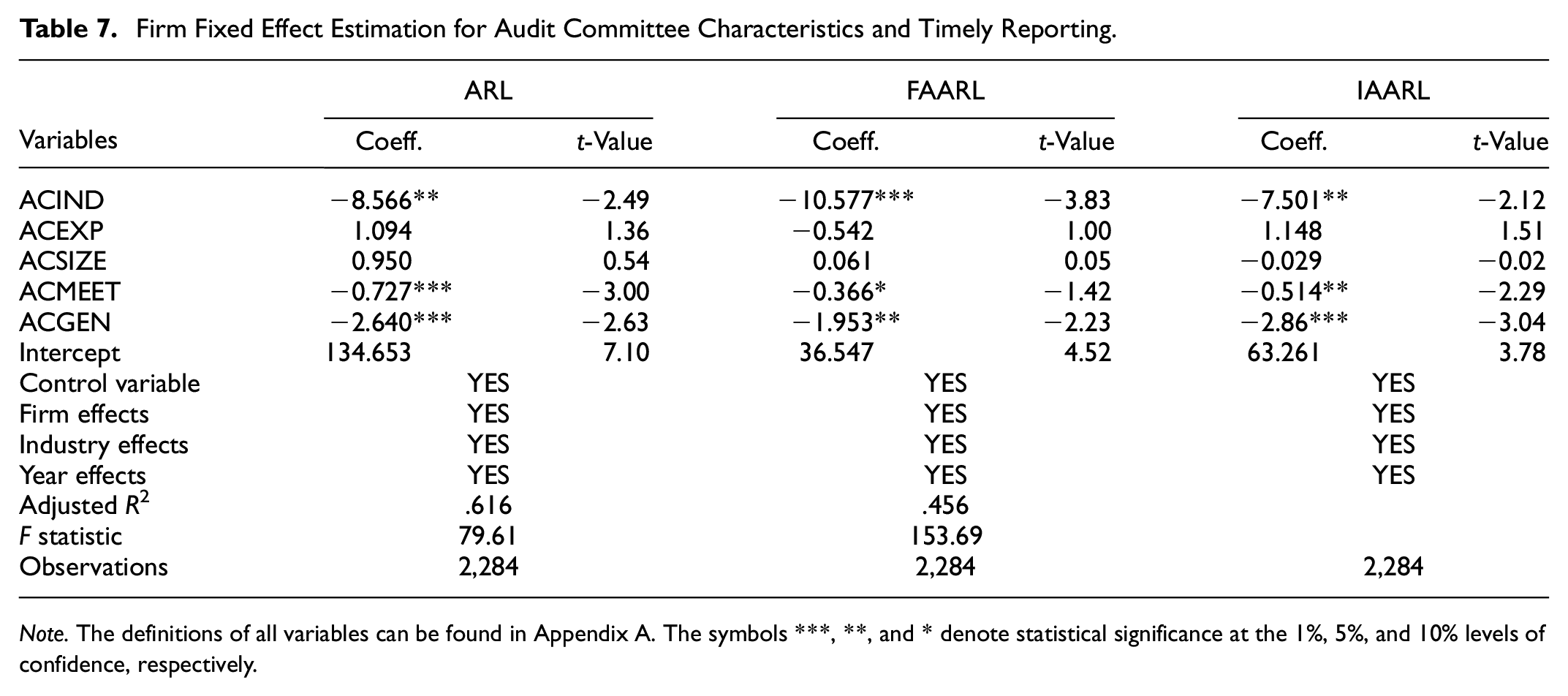

We extend our main findings by including two fixed effects in our regressions to account for time-invariant and unobserved heterogeneity. Table 7 shows results when firm fixed effects are included. There is a number of reasons why firm fixed effects are important. Firstly, they allow us to control for time-invariant factors that may be affecting our results. Secondly, they help us to avoid the issue of omitted variable bias. Thirdly, they allow us to capture the true within-firm effects, as opposed to the between-firm effects. Particularly in emerging markets, time-invariant firm-level effects can easily affect financial reporting timeliness. Table 8 also contains dummies of year * industry interaction. The year-industry fixed effect can be used to remove unobserved heterogeneity both across year and industry (Gormley & Matsa, 2014). Year * industry interaction dummies are tested for differences in the effect of changes over time in unmeasured determinants on financial reporting timeliness across industries. While industry fixed effects might capture these on average, a better-identified model would control for the interactive fixed effects. We re-estimate Equations 1, 2, and 3 using both firm and year * sector fixed effects. Based on the results in Tables 8 and 9, we found that audit committee independence, meeting frequency and gender diversity are negatively and significantly associated with ARL, FAARL, and IAARL even after including firm and year * industry fixed effects. The results in Tables 7 and 8 robust our main findings shown in Table 4.

Firm Fixed Effect Estimation for Audit Committee Characteristics and Timely Reporting.

Note. The definitions of all variables can be found in Appendix A. The symbols ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels of confidence, respectively.

Industry x Year Fix Effect Estimation for Audit Committee Characteristics and Timely Reporting.

Note. The definitions of all variables can be found in Appendix A. The symbols ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels of confidence, respectively.

Two-Step System GMM Estimation for Audit Committee Characteristics and Timely Reporting.

Note. The definitions of all variables can be found in Appendix A. The symbols ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels of confidence, respectively.

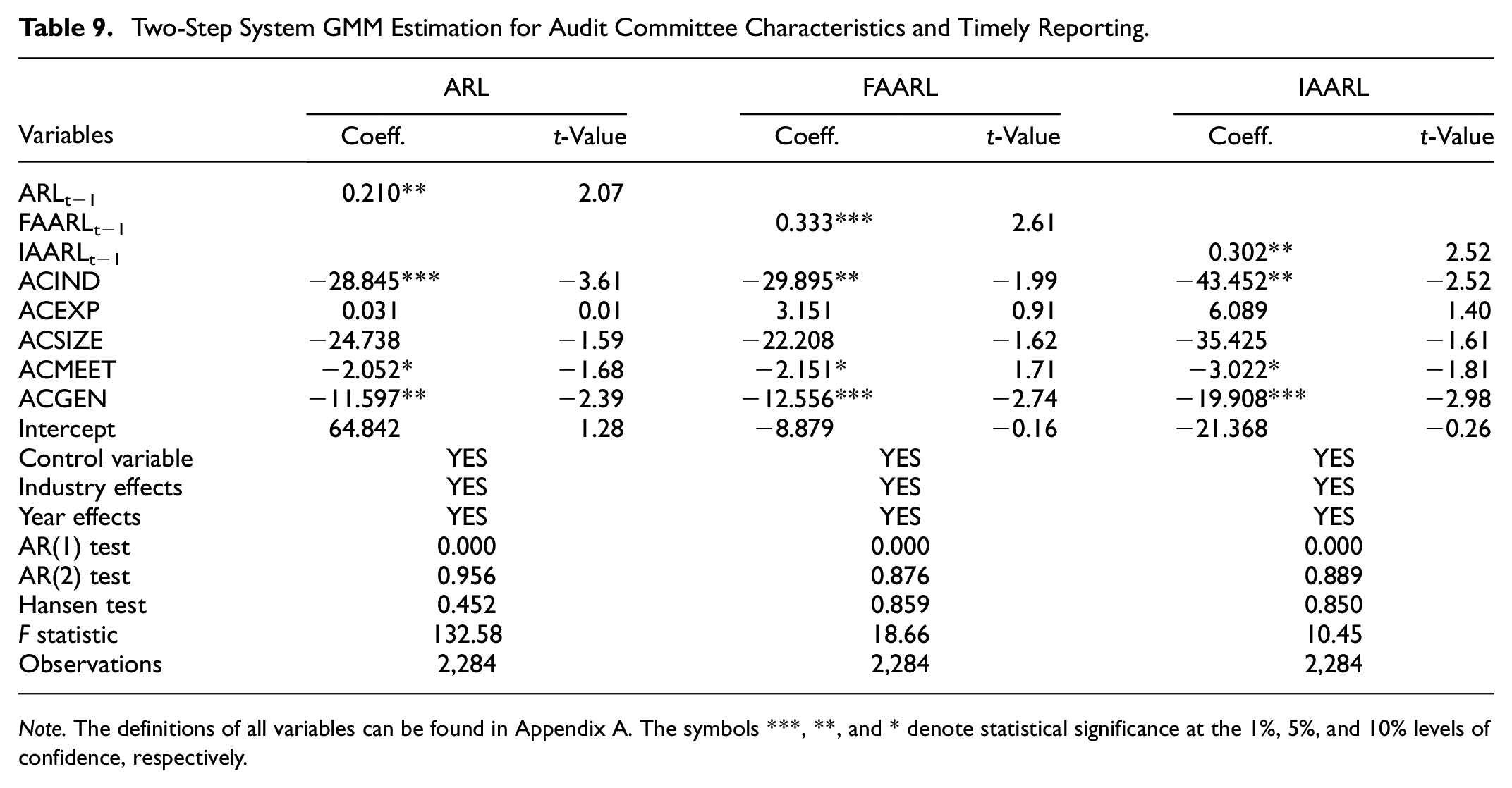

Some potential concerns may show up when researchers study corporate governance. One of the most significant concerns is endogeneity, the possibility that the variables being studied are not truly independent of each other. Vafeas (2001) and Carcello and Neal (2003) also point out that it is probably not random that a company selects audit committee members with certain characteristics. It is very well possible that the timeliness of financial reporting has an impact on the choice of the audit committee or in other words, endogeneity causality. For example, firms with certain characteristics may be more likely to have both diverse audit committees and lower financial reporting lag. Alternatively, external factors such as industry trends or economic conditions may influence both variables simultaneously. The arguments imply that factors affecting financial reporting timeliness and audit committee characteristics may be endogenously determined, which can bias our regression analysis results, resulting in simultaneous causality. Fixed effects estimators control for firm-specific heterogeneity but not endogeneity. The GMM estimator is more robust at correcting for varying variance and autocorrelation (Roodman, 2009) and proved great potent to address different sources of internality, such as unobserved panel heterogeneity, concurrency, and dynamic endogeneity (Ullah et al., 2018). Regressions are tested utilizing a two-step system GMM estimator to control for this problem and to obtain consistent and efficient estimates.

Table 9 presents the two-step system GMM estimation results for audit committee characteristics and timely reporting. The p-values of the Hansen test are statistically nonsignificant, and therefore our instruments are valid in all our regression analyses. Having checked that the first-order serial correlation is insignificant (AR (1)), we can safely conclude that the regression model is properly specified because the second-order serial correlation (AR (2)) doesn’t appear and, therefore, we can both white noise processes for the errors of regression can be omitted. The tables show that our primary conclusions in Table 4 regarding the effects of audit committee independence, meeting frequency, and gender diversity indicators on financial reporting timeliness remain valid when we use the two-step system GMM approach.

Conclusion

The overall goal of the current study is to investigate the effect of audit committee characteristics on financial reporting timeliness. Delays in financial reporting may lead to higher risks, missed opportunities, and more information asymmetry for decision-makers and undermine confidence in financial reports overall. The importance of financial reporting timeliness is comparatively higher in developing countries as opposed to developed countries. This is because developing countries often have weaker regulatory frameworks and less mature financial markets, making timely financial reporting fragile for maintaining investor confidence and attracting foreign investment. Additionally, the significance of timely financial reporting has been amplified for developing nations considering worldwide crises, such as the Covid-19 pandemic and the Russia-Ukraine conflict. The economic instability, uncertainty and capital flow caused by these crises have made timely financial reporting a crucial source of valuable information for investors and stakeholders. It is should be noted that investigating the determinants that affect the timeliness of financial reporting to make financial information available for those demanding as soon as possible is of crucial importance. Previous studies have emphasized that the audit committee members with specific roles and responsibilities in preparing complete, reliable, and quality financial reports establish a significant determinant of financial reporting timeliness. However, these studies focused commonly on the relationship between audit committee financial expertise and timeliness, leading to neglect of other audit committee characteristics. Our effort in this study has been aimed at seeking any possible contribution, with all respect to the previous studies, to the limited literature, by focusing on audit committee financial expertise as well as independence, meeting frequency, gender diversity, and size.

According to the regression analysis conducted employing 2,284 firm-year data obtained from publicly traded firms in the ISE from 2009 to 2019, audit committee gender diversity, meeting frequency, and independence are negatively related to financial reporting timeliness. The lack of diversity in committees may lead to groupthink and a failure to consider alternative perspectives, which can slow down decision-making processes. Similarly, infrequent meetings may result in delayed discussions and resolutions, while the absence of independent members can lead to conflicts of interest and biased decision-making. These factors may contribute to shortening the audit report’s delay, which can positively impact investor confidence and stock prices.

No evidence pointing a relation between audit committee financial expertise, size and reporting timeliness is found. The findings are robust as they are consistent even when proxy measures of financial reporting timeliness are used, such as ARL FAARL and IAARL. Moreover, additional analysis indicates that the audit committee effectiveness indexes are negatively related to timely reporting. Finally, we examined whether there is a change in our primary findings by including interaction variables in the models. It has been found that ACIND * ACGEN are negatively and significantly associated with financial reporting timeliness. Additional analysis results support our main findings, proving the findings are robust after controlling for firm-level fixed effects, year * industry fixed effects, and endogeneity issues.

The results demonstrate that in developing countries such as Turkey, the audit committee, overseeing the financial reporting process and ensuring compliance with regulations, plays a significant role in the timely disclosure of financial reports. It provides an additional layer of accountability and transparency, important especially in countries where technological support and skills may be lacking. The increasing importance of real-time financial data enables the use of artificial intelligence tools in auditing and timely reporting to financial statement users (Zhao et al., 2004). Accordingly, developed countries, where modern tools such as artificial intelligence and audit 4.0 are extensively used, house the habitat for audit and financial reporting processes (Hasan, 2021). However, in developing countries, the utilization of traditional auditing tools remains prevalent in the preparation of audit reports. This can be attributed to various factors, including the absence of a strategic approach to embracing available technological resources, the need to cultivate the requisite proficiencies to leverage these advancements, and limitations in terms of time and resources allocated for education and training (Mustapha & Lai, 2017). By utilizing traditional auditing tools and implementing strong corporate governance mechanisms effectively, developing countries can improve their financial reporting practices and reduce delay of financial reporting timeliness.

Practical and Theoretical Implications

Our findings are expected to make several significant contributions. First, the investigation of possible enhancement regarding timely reporting through audit committee characteristics, especially gender diversity may be considered as a possible contribution to limited existing valuable literature. The finding showing the negative effect of audit committee gender diversity on delays of timely reporting makes a significant contribution as no such a finding was found in prior studies. Furthermore, the finding regarding independence and meeting frequency supports prior literature. Second, elucidated by the findings, we tried to provide some recommendations to managers and policymakers. There is a critique proposing that the corporate governance implementations in Turkey are relatively weak and a better understanding of the concept should be deviced. Regulatory bodies in Turkey do not impose employing members of financial experts and a gender diversity policy on the audit committees in listed companies. Better functioning of the capital markets can be ensured as regulating bodies and policymakers implement possible new standards and legal regulations regarding the audit committee structure. Third, our results offer a new paradigm for managers. In overall, the results show that in Turkey, the audit committee’s characteristics yield great significance in the timely presentation of financial reports and, consequently, in the quality of financial reports. The reduction of abnormal delays will enable the managers to have the investors to invest in their own zone of activities leaving the competitors behind.

Limitations and Future Research

Our study has some limitations. Firstly, the sample comprises of only the non-financial companies in the Istanbul Stock Exchange Market considering the financial companies have different regulatory environments and reporting processes. Secondly, while all control variables in regression models are corroborated by previous literature, other variables may also impact timely reporting. Thirdly, the independent variables that we investigate, whether associated with financial reporting timeliness or not, are the ones instrumentalized most in previous efforts in literature. Finally, as mentioned above, Audit 4.0, Blockchain and other modern techniques offer a great potential to solve any problems in timely reporting of audit activities. Future studies may explore the effects of the use of modern techniques on the relationship between the audit committee and timely reporting.

Footnotes

Appendix

Variable Measurement and Definition.

| Variable name | Variable measurement and definition |

|---|---|

| ARL | Difference between a company’s financial year-end and the date the company publicly releases its audit reports; |

| FAARL | Difference between the actual audit report lag and the firm’s median audit report lag |

| IAARL | Difference between the company’s actual audit report lag and the median audit report lag of the industry the company is in |

| ACIND | ACIND is defined as the ratio of the total number of audit committee members to the number of independent members. |

| ACEXP | An indicator variable ACEXP is defined assigning 1 as the value for cases where at least one audit committee member has expertise in accounting and finance; otherwise, 0. |

| ACSIZE | ACSIZE is defined the total number of audit committee members. |

| ACMEET | ACMEET is defined the number of audit committee meetings held during the financial year. |

| ACGEN | ACGEN is defined, assigning 1 as the value if at least one audit committee member is a female director; otherwise, 0. |

| BSIZE | The total number of executives in the board of directors. |

| BIND | The proportion of independent members in the board. |

| DUALITY | DUALITY is defined, assigning 1 as the value if CEO and board chairman is different individuals; otherwise, 0. |

| BIG4 | BIG4 is defined, assigning 1 as the value if the auditing of company’s reports by Big 4 audit firms; otherwise, 0. |

| AUOP | AOPIN is defined, assigning 1 as the value if an audit firm gives an unqualified opinion on the company’s financial reports; otherwise, 0. |

| AUDITCH | AUDITCH is defined, assigning 1 as the value if an audit firm rotation in the current year; otherwise, 0. |

| SALES | Natural logarithm of the gross sales. |

| LEV | Total assets divided by total assets minus total liabilities. |

| SIZE | Natural logarithm of the book value of total assets |

| M/B | Ratio of market value of equity and book value of equity. |

| ROA | Proportion of net income to total assets. |

| ROE | Proportion of net income to shareholders’ equity. |

| AGE | Natural logarithm of firm age. |

| INVREC | Receivables and inventory to total assets. |

| MULTI | MULTI is defined, assigning 1 as the value if firm is a multinational firm (i.e., foreign sales are greater than 20%); otherwise, 0. |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was financially supported by the scientific research project fund of Gebze Technical University (Funding Number: 2021-A-102-1)

Ethics Approval Statement

Ethics approval was not required for this study.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.