Abstract

In the context of emerging countries trying to attract foreign investors, building governance strategies and risk management of firms is an increasing concern. This study investigates the impact of financial flexibility strategies on the risk management effectiveness of firms and mechanism of these impacts by focusing on Vietnamese listed firms by applying the fixed effect and system GMM methods on a sample of 635 Vietnamese listed firms during the 2010 to 2021 period to derive empirical models under the high risk-high return approach. We also applied robustness tests to ensure that the results are reliable. We also investigate the level of risk management effectiveness among these firms during the 2010 to 2021 period. We found that financial flexibility strategies negatively impact risk management effectiveness of firms through reducing both firm risk and firm performance. Furthermore, we found that the degree of risk management effectiveness differs between low- and high-risk firms in Vietnam, with low-risk firms displaying more effective risk management compared to high-risk firms. Our research shows that financial flexibility strategies are not conducive to risk management effectiveness; however, firms can control the impact of flexibility strategies on risk management by controlling firm performance and risk.

Introduction

Financial flexibility strategies are aimed at helping a firm’s capacity to effectively, profitably, and immediately adapt to unforeseen changes in its cash flow or investment options. This strategy involves managing financial resources in a way that allows for agility and resilience in the face of economic uncertainties or unexpected expenses (Denis, 2011). Therefore, a financial flexibility strategy aims to reduce an financial management pressure, increase financial security, and take advantage of opportunities that may arise in various economic environments (Bonaimé et al., 2014). It is a dynamic approach to financial planning that recognizes the importance of adaptability and preparedness in the face of financial challenges and opportunities. Firms pursuing this strategy need to maintain a strong enough internal financial resource to cope with unusual fluctuations in cash flow and avoid using high-cost, short-term debt. These firms usually hold more cash and pay less dividends (Gamba & Triantis, 2008), which may affect firm value. Therefore, financial flexibility needs to be carefully considered by firms.

There is some evidence that financial flexibility strategies have several benefits for firms. Bancel and Mittoo (2011) found that firms that pursue financial flexibility were less severely impacted by the 2008 global financial crisis. Fahlenbrach et al. (2020) found that firms that were more exposed to the COVID-19 shock experienced greater benefits from cash holdings, and firms with high financial flexibility experienced lower stock price drops compared to firms with low financial flexibility. de Jong et al. (2012) found that firms with high unused debt capacity that pursue financial flexibility can invest more in the future compared to other firms. However, previous studies have also found that financial flexibility poses some disadvantages for firm activities. Mensah and Werner (2003) found a positive relationship between financial flexibility and cost inefficiency in the context of educational institutions. Bolton and Freixas (2000) provided evidence that financial flexibility is costly for banks, because banks face the costs of capital themselves, which can compromise their financial performance. Furthermore, Bonaimé et al. (2014) found that a flexible distribution that favors repurchases over dividends is negatively related to financial hedging within a firm, indicating that financial flexibility strategies increase firm risk. Therefore, pursuing a clear financial flexibility policy may not always be beneficial. Due to the complex impact of financial flexibility policy on firms’ operations, it is necessary to research the impact of financial flexibility policy on different aspects of firms’ operations.

Risk management effectiveness is also an area of concern for shareholders and managers in firms, but the subject has not received adequate attention from researchers. Few studies evaluated the factors that determine risk management effectiveness in previous studies. Accordingly, risk management effectiveness refers to the ability of an organization to identify, assess, mitigate, and monitor risks in a way that minimizes potential negative impacts on the firm’s objectives and operations. A high level of risk management effectiveness means that an organization is proficient at identifying, assessing, mitigating, monitoring, and reporting risks, as well as integrating risks with business strategy, compliance, and governance (Q. K. Nguyen & Dang, 2022b). Previous studies, such as Aljughaiman and Salama (2019) and Sun and Liu (2014), have evaluated risk management effectiveness based on overall results rather than evaluating each activity pertaining to risk management effectiveness. Aljughaiman and Salama (2019) and Sun and Liu (2014) state that a firm with effective risk management ensures a high-risk, high-return relationship during its operations. This approach is based on rational behavior theory (Morgenstern, 1976) that investors require a premium for the risks they are exposed to. Therefore, an investor or shareholder always wants a manager to manage risk in the direction that when accepting an increased level of risk, the expected return must increase accordingly. Therefore, a firm performs good risk management when ensuring that a high risk-high return relationship exists. Existing studies related to risk management effectiveness have focused only on banks and not considered non-financial firms.

In the rapidly evolving economic landscape of Vietnam, an emerging country, characterized by globalization, technological advancements, and dynamic market conditions, Vietnamese listed companies are trying to find ways to improve risk management effectiveness as well as choose appropriate financial flexibility strategies to become more attractive to foreign investors. Some previous studies find that the risk management effectiveness in emerging countries is not high Q. K. Nguyen and Dang (2022b), and which financial flexibility strategy is better for firms in Vietnam or emerging countries has no complete answer yet. Therefore, by using sample data from Vietnamese-listed companies, this study contributes to the literature in multiple ways.

First, to the best of our knowledge, this is the pioneering study to investigate the impact of financial flexibility on firms’ risk management effectiveness. Our results indicate that financial flexibility strategies reduce risk management effectiveness. Second, we use a high risk-high return approach to investigate the mechanism of the effect of financial flexibility strategies on risk management effectiveness. We found that financial flexibility strategies negatively affect risk management effectiveness by reducing both firm risk and firm performance. Finally, we provide evidence that high-risk listed firms have less effective risk management compared to low-risk listed firms in Vietnam. Our results can help listed firms in Vietnam and other emerging countries determine their risk management effectiveness and adopt appropriate strategies to control the negative impacts of financial flexibility.

The rest of this paper is structured as follows. In the next section, we present the literature review and develop the hypotheses. In the following sections, we present the methodology and the research results. In the concluding section, we summarize our research and discuss the limitations of the study as well as provide suggestions for future studies.

Literature Review and Hypothesis Development

Although financial flexibility strategies can have several benefits for firm management, some economic theories have implied that it can reduce risk management effectiveness in certain contexts. Based on agency theory, managers can increase cash-holding and pay less cash dividends to reduce external financing costs to help firms reduce and manage risk easily (F. Chen et al., 2011). According to N. Chen and Hsiao (2014), a manager with higher insider ownership tends not to pursue financial flexibility strategies. However, higher internal financing puts pressure on managers to achieve promising levels of investment. This may lead to managers hastily accepting high-risk projects with inadequate returns (F. Chen et al., 2011). Therefore, financial flexibility strategies may cause managers to manage risk less effectively. Furthermore, asymmetric information in emerging countries might otherwise force firms in these countries to forego profitable growth opportunities (Marchica & Mura, 2010), and instead make investment decisions in projects with low profitable growth opportunities with high levels of risk. Financial flexibility can also encourage risk-taking behavior (Chortareas & Noikokyris, 2021; Duho, 2021) because it can lead managers to believe that their firms have a safety net in the form of available cash. This can further lead to the pursuit of riskier ventures or investments and overall reduced motivation to invest in risk mitigation. With abundant internal financial resources, managers also can become negligent when it comes to risk management.

Based on the financial constraints theory, Xiao et al. (2021) argue that firms with higher financial flexibility and financial slack resources have greater investment inefficiencies, that is, these firms can undertake high-risk projects with low returns. Some previous studies, such as Mensah and Werner (2003), Ali and Siddiqui (2020), and Färe and Yaisawarng (2008) provide evidence that a surplus of internal financial resources can lead to inefficient resource allocation, with funds being allocated to projects or investments that may not provide the best risk-adjusted returns. This can result in suboptimal use of capital. In addition, option theory suggests that managers often tend to accept high-risk projects with disproportionate expected returns for personal gain (Aljughaiman & Salama, 2019; Q. K. Nguyen & Dang, 2022b; Sun & Liu, 2014). In other words, managers can choose high risk but low return projects, thereby making risk management ineffective. This is especially true for businesses with high free cash flow and large cash piles. Based on the theories and findings from prior studies, we propose the following hypothesis:

H1: Financial flexibility reduces risk management effectiveness.

In this study, we consider risk management effectiveness to be the way a firm ensures high-risk, high-return operations. Existing literature has found that financial flexibility can impact firm risk and performance, but the effect of financial flexibility on firm performance remains unclear. Arslan-Ayaydin et al. (2014) found that firms that pursued a financial flexibility strategy during the 2008 financial crisis performed better than firms that did not pursue a financial flexibility strategy. Ma and Jin (2016) found that financial flexibility has a positive impact on firm performance during crises; that is, during a recession, financial flexibility appears to improve firms’ performance. However, de Jong et al. (2012) provided evidence that U.S. firms with above-median financial flexibility reported negative performance in 1990 and 1994. Ferrando et al. (2017) argued that financial flexibility is more valuable for firms in countries or times that have lower legal protection. Mensah and Werner (2003) used a sample of 200 institutions in the U.S. from 1996 to 1997 to indicate that financial flexibility may lead to cost inefficiency. Denis (2011) argued that excess cash holdings might be used for inefficient cross-subsidization and may lead to decreased performance. Therefore, for a developing country in general, and Vietnam in particular, pursuing a financial flexibility strategy may lead to cost inefficiency rather than improved investment efficiency. Moreover, Oded (2020) provided evidence that financial flexibility is positively related to agency cost and reduced profit. Based on these discussions, we expect that financial flexibility can reduce firm performance.

In addition, previous studies have also found that financial flexibility can reduce firm risk. When a company possesses financial flexibility, it is better equipped to address unexpected challenges, such as economic downturns or unforeseen market fluctuations. By using more cash and paying less cash dividends, a company pursuing a financial flexibility strategy can respond well to economic shocks such as financial crises (Arslan-Ayaydin et al., 2014; Bancel & Mittoo, 2011; Fahlenbrach et al., 2020) or periods of economic uncertainty (Dalwai, 2023; Yousefi & Yung, 2022). Yousefi and Yung (2022) also found that financial flexibility enables firms to avoid financial distress. With a financial flexibility strategy, a firm can diversify its risk exposure and avoid heavy reliance on a single financing method (Aydınoğlu, 2001). Based on these discussions above, we expect that financial flexibility can reduce both firm risk and firm performance. Therefore, we propose the second hypothesis:

H2: Financial flexibility reduces firm performance and firm risk.

Research Design

Data

In this study, we used financial data from 635 Vietnamese listed firms in the Ho Chi Minh and Ha Noi stock exchanges. The data was provided by FiinPro, a third-party platform that collects the financial data of Vietnamese listed firms. From the list of firms provided by FiinPro, we excluded firms that have less than 3 years of data in accordance with our financial flexibility calculations. We then manually collected corporate governance data from firms’ annual reports. This data is used as control variables in our models. Our data does not include financial firms due to unique risk environments. The remaining firms are classified into 10 different industries according to FiinPro (Appendix 3). After excluding missing data and outliers, our unbalanced dataset comprised 635 firms with 4,919 observations from 2010 to 2021. We excluded data before 2010 in order to exclude the effect of the 2008 financial crisis. The 2008 crisis period greatly affected the risk management activities of firms and the factors affecting the risk management activities became complex in this period (Ashby, 2011; Best, 2010). Including this period in the study data, therefore, may lead to biased results. Additionally, there are limited Vietnamese listed firms and published information.

Models and Estimation Method

Based on previous studies, such as Sun and Liu (2014) and Q. K. Nguyen and Dang (2022b), we determined risk management effectiveness through the high-risk, high-return relationship. Therefore, in order to test hypothesis H1 as well as verify the impact of financial flexibility on risk management effectiveness, we built the following model:

where PER is the bank performance variable measured by ROE and ROA ratios. These ratios were used as proxies of financial performance in large literature (Almustafa et al., 2023; Lee et al., 2016; Li et al., 2007). RISK is a risk variable which is measured as firm leverage (LEV), and CONT is a vector of control variables. As a robustness test, we also used stock price volatility (VOL) to measure firm risk, as recommended by Jo and Na (2012) and Guenther et al. (2017). FF signifies financial flexibility strategy as measured using the models of Yung et al. (2015) and Marchica and Mura (2010). We consider financial flexibility to refer to the extent to which a firm possesses unused borrowing potential. The following model was used to estimate financial flexibility:

Using this method, firms that demonstrate a discrepancy in leverage levels, with the actual level being lower than the predicted level, are recognized as having unused opportunities for borrowing. According to Marchica and Mura (2010) and Yung et al. (2015), a firm pursuing a financial flexibility strategy has a minimum of three consecutive years of unused debt capacity. Our first proxy of financial flexibility strategy (FF1) is a dummy variable that is 1 if a firm has a minimum of three consecutive years of untapped borrowing potential and 0 otherwise. As an alternative measure of financial flexibility strategy (FF2), we applied the following augmented model suggested by Marchica and Mura (2010) and Yung et al. (2015):

All variables used in Equations iEi and iiEii are defined in Appendix 1. The fixed-effect estimation methods were used for these equations, as suggested by Yung et al. (2015).

Based on previous studies, first, we used board size (BOZ) and board independency (BOI) to control for board structure, because board structure strongly affects firm performance (Bonn, 2004; Vafeas & Theodorou, 1998). Second, we controlled for other firm characteristics that may affect firm performance, including CEO age (CEOA), firm size (FSIZE), state ownership (STO), foreign ownership (FOW), market to book value (MTB), and firm growth (GROW). Belenzon et al. (2019) find that CEOA may reduce firm risk and firm performance. Ibhagui and Olokoyo (2018) provide evidence that positive relationship between leverage and firm performance depends on firm size. Kubo and Phan (2019) found that state ownership of Vietnamese listed firms is significantly related to firm performance because state shareholders have more power and better control over firms, and it is similar to state ownership (T. T. Nguyen & Nguyen, 2020; Q. K. Nguyen, 2023). Market to book value and firm growth are also likely to affect firm risk and performance as discovered by previous studies (Almustafa et al., 2023; Bonn, 2004; J. Chen et al., 2018).

The financial flexibility variable in (1) is used as an interaction variable to test the impact of financial flexibility on the relationship between firm risk and performance. Therefore, if the coefficients of FF*RISK are negative, it indicates that financial flexibility increases the high risk-high return relation, that is, increases risk management effectiveness. On the contrary, if the coefficients of FF*RISK are positive, it indicates that financial flexibility reduces risk management effectiveness. In addition, the sign of the RISK coefficient indicates the effectiveness of risk management. Specifically, the coefficients of RISK are positive and statistically significant with performance variables implying that firms have effective risk management and vice-versa (Aljughaiman & Salama, 2019; Sun & Liu, 2014).

Next, to test hypotheses H2, we investigated the impact of financial flexibility strategies on firm risk and firm performance using the following models:

where PER, RISK, FF, and CONT are performance, risk, financial flexibility, and control variables, respectively. The selection of control variables in (Equations 2 and 3 are based on previous studies that can affect firm risk and performance (Almustafa et al., 2023; Cai et al., 2016; Jo & Na, 2012; Lee et al., 2016; Li et al., 2007). α, β, and γ are coefficients that need to be estimated, and ε is the error term.

To estimate models 1, 2 and 3, we applied the fixed-effect method after performing the Hausman test. We also controlled for year and industry fixed effects in the model. As a robustness test, we applied the system GMM estimation method in a dynamic framework, in accordance with Bond et al. (2003), to control for a potential endogeneity problem. We also performed Hansen’s J test and the AR(2) test to ensure that the instruments are valid and that the system GMM results are reliable. The fixed-effect and system GMM are effective estimation methods for unbalanced panel data that have been recognized in many previous studies (Fernández-Val & Weidner, 2018; Judson & Owen, 1999).

Research Results and Discussion

Descriptive Statistics and Correlation Matrix

Table 1 presents the descriptive statistics of the main variables. The mean of ROA and ROE are 1.7% and 12.8%. These values are significantly lower than those of other samples in countries such as Malaysia (Subramaniam & Wasiuzzaman, 2019), Thailand, and Singapore (Elmghaamez & Gan, 2023). There are also significant differences between the min and max values of these variables. The mean values of the LEV and VOL variables are also high; the mean of LEV is 47.1% and the mean of VOL is 0.081, indicating that the listed companies in the sample use significant financial leverage and have a fairly high level of risk. The min and max values of risk variables also display considerable differences. These are characteristics of an emerging market like Vietnam. We also reported the correlation matrix of the main variables to indicate the relationships between variables. The correlation matrix is presented in Appendix 2. This appendix shows that there exists a statistically significant correlation between risk and performance variables but is not consistent, so we need to continue to perform multivariate analysis. The highest values are the coefficients of ROA and ROE (0.846), and FF1 and FF2 (0.814). However, these variables are not estimated in the same model, so multicollinearity is not a concern in our models.

Descriptive Statistics of Main Variables.

Note. This table reports the descriptive statistics of main variables. See Appendix 1 for variable definitions, variable measures and sources.

Financial Flexibility and Risk Management Effectiveness

The estimation results of Equation 1 using the fixed-effect estimation method are presented in Table 2. The coefficients on LEV and VOL are negative and statistically insignificant (at 10% level or better) with both ROA and ROE in all regressions, indicating that Vietnamese listed firms may have a low level of risk management effectiveness, since there is no evidence of a high-risk, high-return relationship in these firms. Second, the coefficients on FF1*LEV and FF1*VOL are negative and significant (at 10% level or better) with ROA and ROE in regressions 1 to 2 and regression 3, respectively, indicating that financial flexibility reduces the high-risk, high-return relationship. Therefore, we found evidence that financial flexibility strategies reduce firms’ risk management effectiveness. This result supports hypothesis H1 and is consistent with previous studies, which state that financial flexibility can reduce investment efficiencies and result in inefficient resource allocation (Ali & Siddiqui, 2020; Färe & Yaisawarng, 2008; Mensah & Werner, 2003; Xiao et al., 2021), which then reduces risk management effectiveness. In the context of Vietnam, an emerging country with a high level of information asymmetry, financial flexibility easily creates conditions for managers to make ineffective investment decisions with high risks, thereby affecting shareholder value. This is consistent with previous studies.

Multivariate Analysis Results of Financial Flexibility and Risk Management Effectiveness.

Note. The data presented in this table apply LEV and VOL as proxies of firm risk in regressions 1 to 2 and 3 to 4, respectively. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

Pursuing financial flexibility may lead to a decrease in risk management effectiveness, as firms might prioritize short-term liquidity and accept higher costs. In the context of the Vietnamese stock market, where there might be a desire for quick returns and liquidity, firms could be sacrificing risk management quality. Furthermore, in emerging markets such as Vietnam, where agency problems and information asymmetry are persistent concerns, financial flexibility can induce managers to accept high-risk projects with disproportionate returns. In the context of regulations related to risk management in Vietnamese listed companies are still not many. Vietnamese listed firms do not have many risk management tools nor are regulations required to disclose risk management tools. Therefore, our research contributes an important new aspect to the risk management of listed companies in Vietnam and other emerging countries. Our results are consistent with the option theory as proven through previous studies. Regarding other control variables, we found that some firm characteristics, such as firm size, ownership structure, debt structure, and growth, affect firm performance, which is consistent with findings in previous studies that were performed in different countries (Almustafa et al., 2023; Bonn, 2004; Zeitun & Goaied, 2022).

Mechanism of the Impact of Financial Flexibility on Risk Management Effectiveness

Table 3 presents the estimation results of Equations 2 and 3 using the fixed-effect method. The results indicate that financial flexibility can reduce firm performance, because the coefficients on FF1 in regressions 1 and 2 are negative and statistically significant at 10% level of better. Additionally, the coefficients on FF1 are negative and statistically significant (at 10% level or better) with both risk variables in regressions 3 and 4, indicating that financial flexibility strategies reduce firm risk. These results strongly support hypothesis H2 and indicate that financial flexibility strategies can reduce both firm risk and performance and therefore reduce risk management effectiveness. These results are consistent with some previous studies which indicate that financial flexibility strategies can result in inefficient resource allocation (Ali & Siddiqui, 2020; Färe & Yaisawarng, 2008) and increase risk-taking behavior (Chortareas & Noikokyris, 2021; Duho, 2021). Our findings are relevant in the context of developing countries like Vietnam, where agency problems are considered serious and control mechanisms are not effective (Agyei-Mensah, 2016; Dang & Nguyen, 2024).

Multivariate Analysis Results of Financial Flexibility, Firm Risk, and Firm Performance.

Note. This table presents the estimation results for Equations 2 and 3 in regressions 1 to 2 and 3 to 4, respectively using the fixed-effect estimation method. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

These results imply that companies in developing countries in general and Vietnam in particular will have difficulty enhancing risk management effectiveness if they pursue a financial flexibility strategy. Firms that pursue flexible financial strategies may hoard cash or avoid taking on reasonable levels of debt due to a fear of financial risk. While this reduces the risk of financial distress in the short term, firms that overly prioritize financial safety may not invest in projects that could enhance their performance and profitability. Maintaining excessive financial flexibility can lead to missed opportunities for growth and expansion, which ultimately affects firm performance (Bancel & Mittoo, 2011). Overall, we found that, while financial flexibility can increase an organization’s ability to identify, assess, mitigate, and monitor risks, it also has potential negative impacts on the organization’s objectives and operations. Therefore, our research results provide important implications for firms pursuing financial flexibility strategies to have solutions in place to improve firm performance, thus mitigating the negative effects of financial flexibility.

Robustness Test

In this study, we performed three robustness tests. First, we investigated the impact of financial flexibility on risk management effectiveness as well as its mechanism in two groups of low and high risk firms separately. The risk-taking behavior of firms is believed to depend on the risk level of the firms (Q. K. Nguyen, 2022a; Wellalage & Locke, 2014). Furthermore, firm performance also depends on the risk propensity of firms (Boermans & Willebrands, 2017). Therefore, the impact of financial flexibility on risk and performance may differ between firms with risk levels. Although splitting the research data will cause the models to have fewer observations, analyzing the experiments for two different groups of firms will help us control for changes in the research results when applied to different groups of firms. To address these discrepancies, we estimated Equation 1, 2, and 3 for two separate groups. High-risk firms include firms with above-average LEV, while low-risk firms comprise the remaining firms. Second, we also used an alternative measure of financial flexibility (i.e., the FF2 variable) as an additional robustness test to ensure research results do not change when using different measurement methods. Finally, we treated the potential endogeneity problem to avoid biased results due to such problems by applying the system GMM estimation method for Equation 1, 2, and 3.

In Table 4, we present the estimation results for Equation 1 for sub-sample of high and low risk firms. The coefficients on LEV and VOL are negative and statistically significant with both ROA and ROE in regressions 1 to 4, while most of the coefficients are insignificant in regressions 5 to 8. This indicates that low-risk firms in Vietnam have better risk management effectiveness compared to high-risk firms. Second, financial flexibility reduces risk management effectiveness in both high- and low-risk firms, as indicated by the coefficients of FF1*LEV and FF1*VOL, which are negative and statistically significant in regressions 1 to 4 and 5 to 8.

Financial Flexibility and Risk Management Effectiveness in Low- and High-Risk Firms.

Note. This table presents the estimation results for Equation 1 by using the fixed-effect estimation method for low- and high-risk firms in regressions 1 to 4 and 5 to 8, respectively. We applied LEV and VOL as risk variables in regressions 1, 2, 5, and 6; and 3, 4, 7, and 8, respectively. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

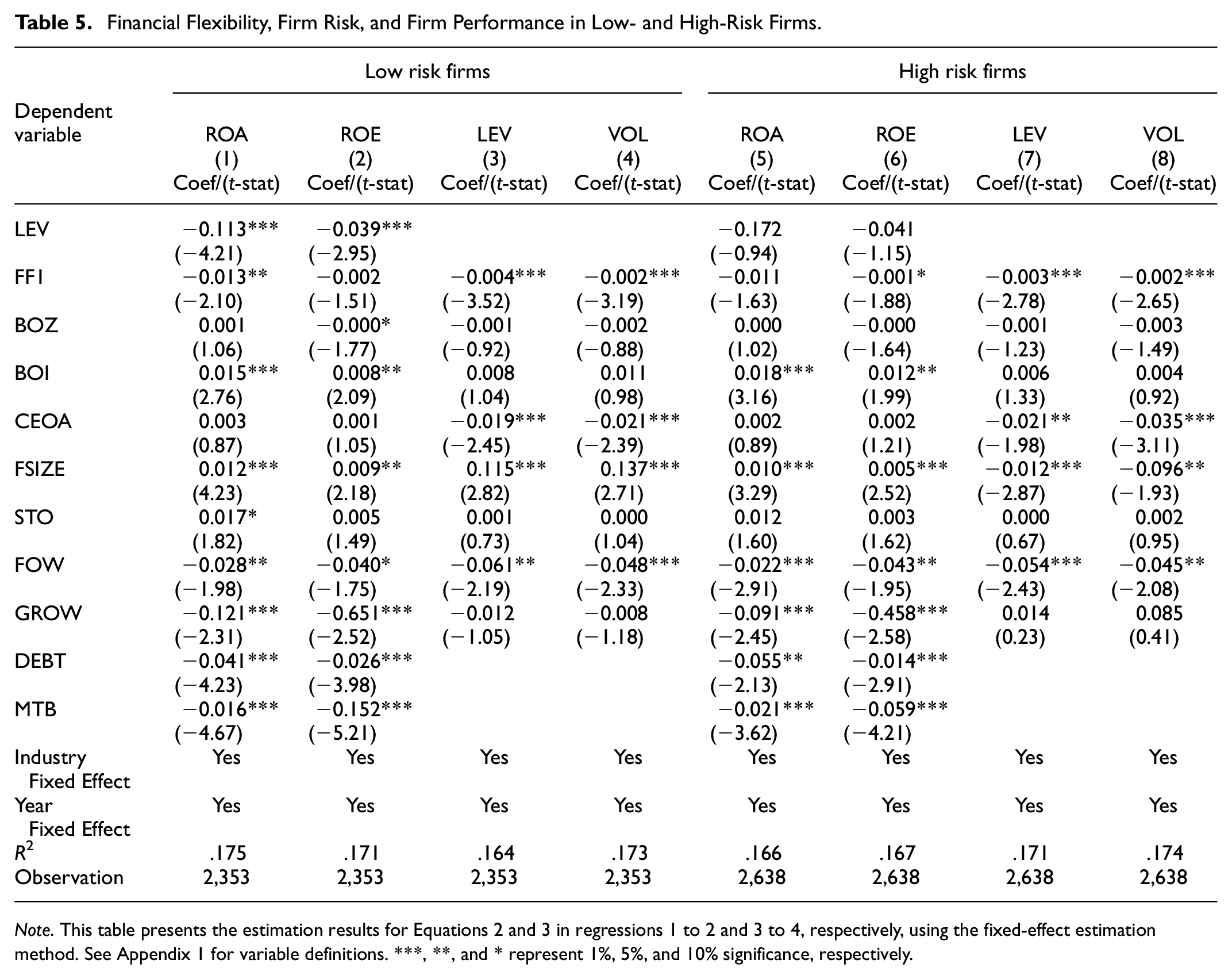

Table 5 presents the estimation results for Equations 2 and 3 for low- and high-risk firms. The coefficients are only negative and statistically significant with ROA and ROE in low-risk firms. The coefficients of FF1 are negative in all regressions and significant in most regressions, indicating that financial flexibility reduces firm risk and firm performance in both low- and high-risk firms. Therefore, the mechanism of the impact of financial flexibility on risk management effectiveness remains the same between low- and high-risk firms. This supports hypothesis H2 and is consistent with the initial results presented in Table 3.

Financial Flexibility, Firm Risk, and Firm Performance in Low- and High-Risk Firms.

Note. This table presents the estimation results for Equations 2 and 3 in regressions 1 to 2 and 3 to 4, respectively, using the fixed-effect estimation method. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

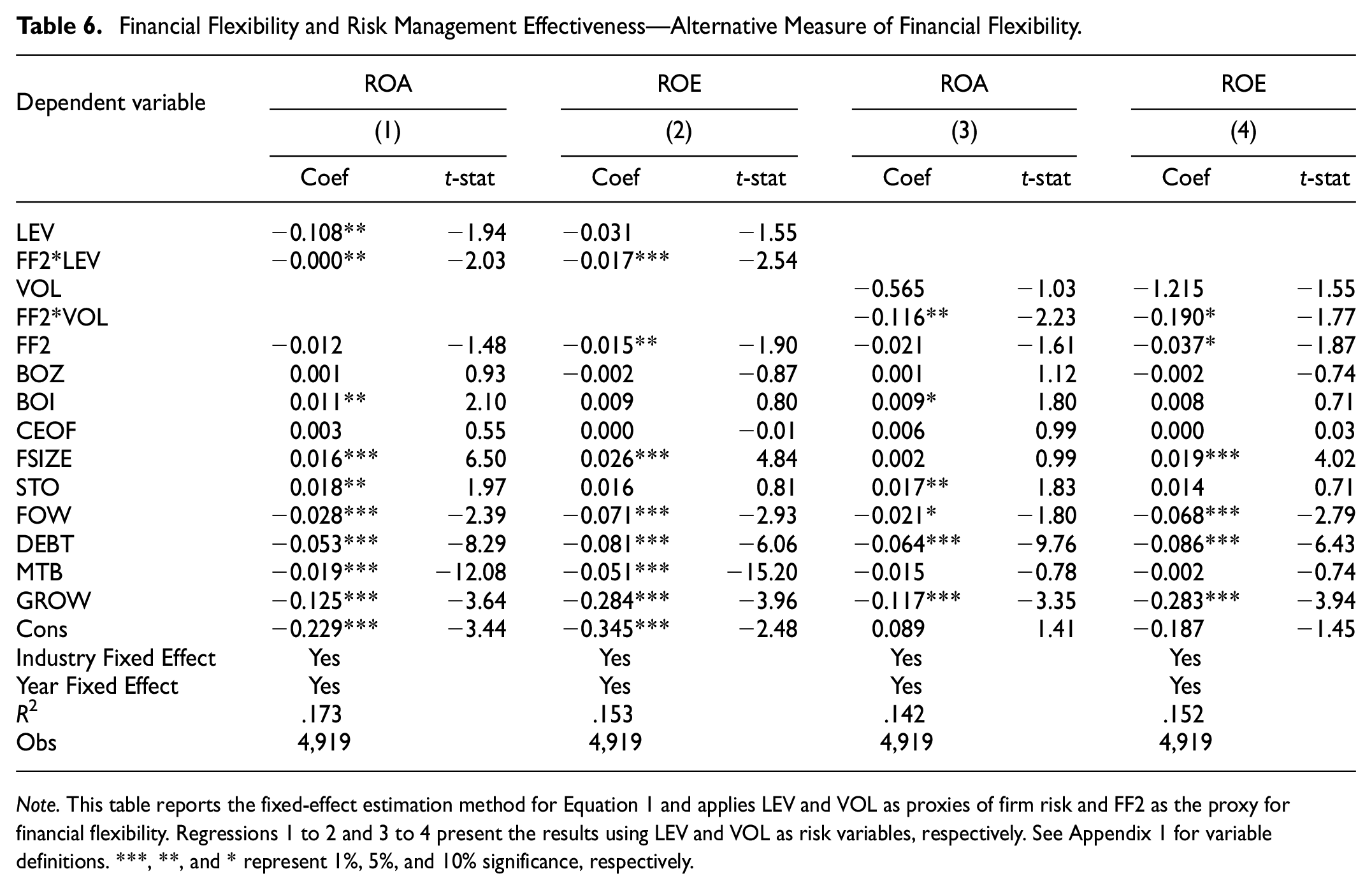

Tables 6 and 7 report the results of the alternative robustness test, wherein Equation 1, 2, and 3 were estimated using an alternative measure of financial flexibility (FF2). Table 6 displays the estimation results of (1) using fixed-effect estimation method, which is similar to the results in Table 3. The coefficients of FF2*LEV and FF2*VOL are negative and statistically significant. Therefore, hypothesis H1 continues to be supported and is consistent with our initial expectations.

Financial Flexibility and Risk Management Effectiveness—Alternative Measure of Financial Flexibility.

Note. This table reports the fixed-effect estimation method for Equation 1 and applies LEV and VOL as proxies of firm risk and FF2 as the proxy for financial flexibility. Regressions 1 to 2 and 3 to 4 present the results using LEV and VOL as risk variables, respectively. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

Financial Flexibility, Firm Risk, and Firm Performance—Alternative Measure of Financial Flexibility.

Note. This table presents the estimation results for Equations 2 and 3 in regressions 1 to 2 and 3 to 4, respectively, using the fixed-effect estimation method and using FF2 to measure financial flexibility. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

Table 7 reports the estimation results for Equations 2 and 3 using FF2 as the proxy of financial flexibility. The coefficients of FF2 are negative and significant in all regressions, indicating that financial flexibility strategies reduce firm risk and firm performance. The results in this table are consistent with our initial results and continue to support hypothesis H2. The other results related to control variables are also similar to our initial results.

Finally, we applied the system GMM method for Equation 1, 2, and 3 to treat the potential endogeneity problem and the results are presented on Table 8. The coefficients of FF1*LEV and FF1*VOL in Panel A as well as the coefficient of FF2*LEV and FF2*VOL in Panel B are negative and significant with both ROA and ROE in regressions 1 to 4, which indicates that financial flexibility reduces risk management effectiveness, thus strongly supporting hypothesis H1 and meeting our initial expectations. Furthermore, the coefficients on FF1 and FF2 are negative in regressions 5 to 8 in both Panel A and Panel B. Most coefficients of FF1 and FF2 are statistically significant, implying that financial flexibility reduces both firm risk and firm performance. Financial flexibility reduces risk management effectiveness through reducing both firm risk and firm performance. The robustness test results meet our initial expectations and strongly support hypothesis H2. The p-value of the AR(2) test and Hansen’s J test are higher than 10%, implying that the instruments are valid and the results are reliable. In addition, the number of instruments is lower than the number of firms, implying that Hansen’s J test is reliable.

System GMM Result for the Relationship between Financial Flexibility, Firm Risk, and Firm Performance.

Note. This table presents the estimation results for Equation 1, 2, and 3 in regressions using the system GMM method. Regressions 1 to 4, 5 to 6, and 7 to 8 present the estimation results for Equation 1, 2, and 3, respectively. Panel A and Panel B present the results by using FF1 and FF2 to measure financial flexibility, respectively. See Appendix 1 for variable definitions. ***, **, and * represent 1%, 5%, and 10% significance, respectively.

Overall, after performing some robustness tests, the robustness test results are consistent with our initial results and strongly support hypotheses H1 and H2. Therefore, there is strong evidence that financial flexibility strategies reduce risk management effectiveness and this impact is through the mechanism that reduces both firm risk and firm performance.

Conclusion

Our study aims to evaluate the level of risk management effectiveness and sheds light on the impact of financial flexibility strategies on risk management effectiveness as well as its mechanism within the context of Vietnamese listed firms for the period 2010 to 2021. We performed empirical analysis and robustness tests to derive important findings. First, there are significant variations in the degree of risk management effectiveness between low- and high-risk firms in Vietnam, with low-risk firms displaying more effective risk management compared to high-risk firms. Second, financial flexibility strategies have a negative impact on risk management effectiveness. Finally, this negative effect is mediated by the observation that while financial flexibility may reduce firm risk, it also reduces firm performance. Therefore, it is crucial for organizations to recognize the potential disadvantages of relying solely on financial flexibility as a risk-management strategy.

Our study contributes to the existing literature by providing empirical evidence on the impact of financial flexibility strategies on risk management effectiveness—an area that has not been extensively explored before. Our findings challenge conventional wisdom regarding financial flexibility as a panacea for risk management and highlights the need for firms to consider a more nuanced approach to risk mitigation.

Our results provide important implications for shareholders and managers of firms in Vietnam as well as in other emerging countries in the context of ineffective risk management by firms in these countries. The differences in risk management effectiveness between low- and high-risk companies require managers in high-risk firms in Vietnam need to adopt risk-management strategies to improve their risk-management activities. While pursuing financial flexibility strategies can have several advantages for firms, such strategies can also reduce risk management effectiveness through reducing both firm risk and firm performance. Therefore, if a company pursues a financial flexibility strategy, shareholders need to pay closer attention to agency issues, control the selection of investment projects, and prevent managers from choosing high-risk projects that have inadequate return levels.

Our study also has some limitations. This study used samples from only an emerging market, that is, Vietnam, and the assessment of risk management effectiveness may differ in other countries. Future studies can use similar methods to evaluate risk management effectiveness in other countries and regions. Furthermore, our study did not consider crisis periods such as wartime and COVID-19. Future studies can therefore examine the impact of financial flexibility on risk management effectiveness during different periods, specifically during recession periods.

Footnotes

Appendix

Data Distribution by Country.

| No | Industries | Firms | % | Observations | % |

|---|---|---|---|---|---|

| 1 | Warehousing and transportation | 66 | 10.39 | 514 | 10.45 |

| 2 | Agriculture forestry seafood | 17 | 2.68 | 147 | 2.99 |

| 3 | Construction | 120 | 18.90 | 1,108 | 22.52 |

| 4 | Information, communication | 35 | 5.51 | 216 | 4.39 |

| 5 | Industry | 136 | 21.42 | 965 | 19.62 |

| 6 | Health | 25 | 3.94 | 175 | 3.56 |

| 7 | Trading, service | 120 | 18.90 | 1,019 | 20.72 |

| 8 | Science and Technology | 36 | 5.67 | 196 | 3.98 |

| 9 | Mining and Petroleum | 41 | 6.46 | 325 | 6.61 |

| 10 | Real estate | 39 | 6.14 | 254 | 5.16 |

| Total | 635 | 100 | 4,919 | 100 |

Source. FiinPro database.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by Ho Chi Minh City Open University

Data Availability Statement

Data is available on request