Abstract

The dynamic trade-off model emphasizes that random shocks and other constraints may force firms to deviate from their optimum debt ratio. In addition, firms must incur adjustment costs for them to revert to their target level due to market frictions. However, prior literature in Saudi does not consider the effect of adjustment costs in determining how board governance mechanisms influence capital structure. By exploiting the generalized method of moments framework (GMM), this study analyzed the balanced panel of 100 Saudi non-financial listed firms covering the period from 2010 to 2019. The research found that Saudi firms observed a dynamic adjustment to attain their target leverage at 30.46% annually. Besides that, findings from the present study equally indicate strongly that board size and CEO tenure are negatively associated with leverage. There is also strong evidence that Saudi firms with a substantial number of independent directors pursue a more levered capital structure. Gender diversity appears insignificant in predicting the firms’ target debt ratio. Consequently, the Saudi board of directors and firms’ managers should consider the adjustment costs and other market frictions when designing the optimum debt-equity ratio.

Introduction

The board of directors is the apex body responsible for safeguarding firms’ internal governance (Fama & Jensen, 1983; Nwude & Nwude, 2021). The board can hire and fire entrenched managers who are unwilling to align with shareholders’ interests (Jensen, 1993). The function of a corporate board is to monitor management and oversee firms’ strategic policy initiatives (Fama, 1980). Agency theorists believe that the board of directors possesses exclusive control and can provide robust monitoring of top-level management. The board of directors discharges these functions through its mechanisms. These mechanisms include board size, board independence, CEO tenure, and board diversity. On the other hand, some studies suggest that the primary function of the board of directors is to provide guidance, expertise, and link firms to critical resources for their survival and growth (Hillman & Dalziel, 2003). This research focuses on board structure because the corporate board occupy the pinnacle position in ensuring the best corporate governance practices, and its decisions are directly related to various organizational outcomes (Nwude & Nwude, 2021; Zubeltzu-Jaka, Álvarez-Etxeberria & Ortas, 2020). Therefore, one may conclude that the corporate board is a platform for directors to deliberate and approve firms’ strategic policies, such as capital structure decisions. Capital structure is the mixture of different financing sources employed by a company to finance its investment (Myers, 2001). According to Abor and Biekpe (2009), a firm’s combination of debt and equity capital to fund its assets is known as a capital structure. Consequently, the ultimate goal of capital structure decisions is for firms to select a portfolio of financing sources that will ensure sustainability and enhanced profitability (Abor, 2007; Ardalan, 2017).

The novel study of Modigliani and Miller (1958) has contributed to the growing arguments on firms’ capital structure. These authors argue that the presence of a perfect market and no taxes, debt, or equity financing does not affect the value of any firm. This conclusion attracted widespread criticism due to its restrictive assumptions. Consequently, Modigliani and Miller (1963) demonstrated that capital structure is relevant to firms’ value considering the tax advantage of debt. This effort inspired many researchers and eventually led to the development of many theories on capital structure, such as the trade-off theory. This framework suggests that firms have a target or optimum debt-equity ratio that maximizes their value. The optimum point is where the benefits and costs of debt are equal (Kraus & Litzenberger, 1973; Shyam-Sunder & Myers, 1999). Accordingly, the dynamic trade-off model emphasizes that random shocks and other constraints may force firms to deviate from their optimum debt ratio. Hence, for firms to revert to their target level, they have to incur adjustment costs due to market frictions (Leary & Roberts, 2005). Given this review, it is paramount to analyze capital structure using a dynamic framework. Capital structure dynamics can be exploited effectively using the generalized method of moments (GMM) estimation procedure (Ozkan, 2001; Ramjee & Gwatidzo, 2012). GMM framework can effectively control endogeneity and reverse causality effect embedded in the board governance mechanisms-capital structure relationship.

Prior studies in this context mainly employed static estimation methods such as OLS and within estimators (Abor, 2007; Adusei & Obeng, 2019; Alves et al., 2015; Kyriazopoulos, 2017; Ngatno et al., 2021; Sheikh & Wang, 2012; Tarus & Ayabei, 2016). It may be possible that our explanatory variables (board governance attributes) might not be strictly exogenous in its relationship with the dependent variable (capital structure). This circumstance may induce endogeneity and thereby lessening the efficiency of the static estimators (Jebran et al., 2019; Ullah et al., 2018). By exploiting a dynamic panel technique, this research considers the effect of adjustment cost and other market imperfections that often prevent firms from rebalancing to their target debt ratio. Like most developing countries’ capital markets, the Saudi capital market is associated with high information asymmetry and high transaction costs (Bajaher et al., 2021). Most of the firms operating in the environment rely heavily on bank borrowing due to the difficulty in accessing long-term debt financing from the capital market (Rizvi & Hussain, 2022; Yıldirim et al., 2020). It may be interesting to provide further perspective on how the board of directors’ monitoring influences the attainment of optimum debt-equity ratio to enhance firm value. Therefore, this study examines the impact of board governance mechanisms on the capital structure of Saudi firms using a dynamic panel data framework. Accordingly, as observed by the dynamic capital structure model, empirical evidence from this paper indicates that Saudi firms observe a dynamic adjustment to attain their target leverage.

More specifically, the rest parts of this article continue as follows: the second part focuses on the literature review, whereas section three explains the research methodology. The fourth and fifth sections present analysis, discussions of results and conclusion, respectively.

Literature Review

Theory

This article exploits the agency and resource dependency framework as the theoretical base for linking board governance mechanisms and firms’ capital structure. Agency theory postulated that firms suffer from fundamental agency conflicts between managers (agents) and shareholders (principals) due to the separation between ownership and control (Jensen & Meckling, 1976). The theory’s critical issue is that shareholders should ensure that managers focus on profit maximization rather than engaging in an opportunistic goal to enhance their utility. In the same context, Jensen and Meckling (1976) provided further insight into this theory by defining agency relationships and identified agency costs. According to this perspective, the board of directors can minimize manager-shareholder agency conflicts through its governance mechanisms.

Additionally, the agency framework pointed out that board governance mechanisms such as board size, board independence, CEO tenure, and board diversity are essential for board monitoring (Adams & Funk, 2012; Fama, 1980). In particular, Jensen (1993) stressed that larger boards suffer from poor coordination and ineffective monitoring, and thus, firms should constitute a smaller board size with a substantial number of independent directors. Regarding CEO tenure, this perspective believed that CEO tenure should be moderate because a longer term in office makes the CEO to be more entrenched and that entrenched managers may override board decisions (P. G. Berger et al., 1997). Moreover, within the context of the agency literature, some studies explained that board diversity enhances board independence and monitoring. It is reported that gender diversity brings new perspectives and expertise to the boardroom deliberations and consequently shaping corporate boards’ monitoring (Adams & Ferreira, 2009).

In contrast, the resource dependency framework considered the board of directors a link companies can exploit to obtain valuable resources from the external environment (Pfeffer, 1973). This theory states that the corporate board’s primary role is to provide corporations with the resources, guidance, and expertise required for their growth and sustainability (Monem, 2013; Zahra & Pearce, 1989). Additionally, this perspective broadly focuses on the corporate boards’ networking influence, which is a strategic mechanism for gaining recognition and legitimacy for companies (Hillman & Dalziel, 2003). It is suggested that organizations gain acceptability by employing persons with high status and outstanding qualities on their boards to obtain broader community assistance (Singh, 2007). More importantly, the theory focuses on independent or outside directors’ critical functions in protecting firms against the external environment. These directors are purposely recruited to work on the board of directors because of their skills, expertise, and goodwill. The resource dependency framework also emphasized a positive relationship between board diversity and board size (Zahra & Pearce, 1989). Hence, organizations are expected to constitute large boards to secure diverse resources from the board of directors’ compositions. Accordingly, it is stated that board diversity enables companies to access social and human capital, thereby enhancing their ability to obtain funding from the external environment (Hillman et al., 2000).

In the same vein, the literature within the resource dependency theory also assessed women directors’ networking ability in securing resources to firms. In this regard, Miller and Triana (2009) described women as more accommodating; they practice participative leadership styles and have multiple viewpoints. In this way, female directors can quickly develop ties with external stakeholders to obtain valuable information and finances that an organization can use to grow and develop (Adams & Ferreira, 2009). In sum, the resource dependency theory provided insights on the pivotal functions of board size, independent directors, and boardroom diversity in assisting companies in overcoming the challenges of accessing vital resources from the external environment. According to the theory, the need for additional funding determines board composition. In this sense, as a matter of strategy, a firm may expand its board size to co-opt influential personalities from financial institutions with the view of securing additional capital to finance its investments.

Hypothesis Development

Board Size

Board size refers to the number of board members that constitute a corporate board. Studies pointed out that board size is an essential corporate governance mechanism that firms can use to mitigate agency conflicts between shareholders and managers (Dimitropoulos, 2014). Existing literature suggests that the higher the number of board members, the more powerful they are in ensuring intensive monitoring (Abor, 2007). As such, large boards may prefer a high debt policy to raise a firm’s performance. There is also empirical evidence that firms with larger board size are associated with lower borrowing costs due to their stringent monitoring (Anderson et al., 2004). In this regard, empirical studies showed that debt in firms’ capital structure increases and board size rises (Alves et al., 2015; Bokpin & Arko, 2009; Kyereboah-Coleman & Biekpe, 2006; Sheikh & Wang, 2012). Contrary to the above findings, a stream of the literature argued that smaller boards are bound to have effective coordination and facilitate robust management monitoring (Jensen, 1993; Lipton & Lorsch, 1992). Similarly, prior studies concluded that smaller boards paved the way for extensive deliberations of policies, greater cohesion in the boardroom and faster decision making (Pillai & Al-Malkawi, 2018). In this context, empirical findings showed that board size directly correlates with the total debt ratio (Dimitropoulos, 2014; Sewpersadh, 2019). Given this discussion, this article formulates the hypothesis that:

Board Independence

Another board governance attribute that can affect firms’ financing choice is board independence. Board independence can be achieved by setting up a corporate board with more external directors (Sheikh & Wang, 2012). In addition, both agency and resource dependency theories emphasised outside directors’ relevance in strengthening boards’ monitoring capacity and providing resources to firms. Hence, companies should employ more outside directors on their boards to boost their internal governance system (Hillman & Dalziel, 2003). Besides that, Fama (1980) pointed out that independent directors are regarded as professional referees because they can objectively assess the firms’ policy decisions due to their wealth of knowledge, expertise, and independence. Furthermore, a study by Wu et al. (2019) found that a higher proportion of independent directors on corporate boards promotes disclosure and mitigates information asymmetry.

Accordingly, empirical evidence showed that firms with a high number of outside directors on their boards are bound to have greater financial leverage measured by total debt (Abor, 2007; Kyriazopoulos, 2017; Tarus & Ayabei, 2016). This positive association supported the argument that outside directors are active monitors of management. Thus, these directors tend to compel managers to employ high leverage to boost firms’ value. On the contrary, some empirical evidence reported that firms with a large number of outside directors utilised low debt level in their capital (Dimitropoulos, 2014; Sani et al., 2020; Wen et al., 2002). One possible reason for this negative result between board independence and financial leverage is that firms with a high proportion of outside directors on their boards may likely utilise more equity than debt. More often, these directors take advantage of their pool of expertise, connections, and ties with the external environment to secure other funding sources to their firms other than debt capital. Given this presentation, the following hypothesis is stated:

CEO Tenure

CEO Tenure is another board governance mechanism that can affect companies’ capital structure choice. As defined by P. G. Berger et al. (1997), CEO tenure is the number of years a CEO has been holding his position. A CEO is the head of the top-management team and is also answerable to the board of directors regarding firms’ operational activities. Hence, his tenure may influence a firm’s decisions (Abor, 2007). The literature emphasised that the CEO’s ability to take more challenging decisions increases as his tenure lengthens (Orens & Reheul, 2013). As such, empirical evidence showed that firms’ leverage levels increases as CEOs’ tenure increases (Matemilola et al., 2018; Ndaki et al., 2018). However, P. G. Berger et al. (1997) buttressed that the higher the CEO’s tenure, the higher the CEO entrenchment level. Accordingly, some studies found a significant negative relationship between the CEO tenure and total debt ratio as a measure of capital structure (Ishak et al., 2011; Tarus & Ayabei, 2016; Wen et al., 2002). The negative association between CEO tenure and leverage can be interpreted based on the proposition of Fama (1980) that entrenched CEOs tend to employ lower debt level to minimise risk and safeguard their undiversified human capital investment. Likewise, Jensen (1986) emphasised that powerful CEOs dislike high debt because of its constraints on the managers’ desire to engage in empire-building. Based on the preceding arguments, this paper designed the following hypothesis:

Board Gender

There is a growing interest in the impact of women representation on corporate board decisions. One line of argument is that women have a peculiar attitude and diverse perspectives in organizational settings (Ain et al., 2021). Thus, their presence on the board of directors may promote sound corporate governance. Related to this view, Adams and Ferreira (2009) found that women participation in board meetings and other committee works is higher than men. By doing so, female directors are bound to monitor firms’ managers effectively. Prior studies also argued that female directors have a higher risk propensity than male directors (Adams & Funk, 2012; Chen et al., 2019). Hence, female directors are likely to subscribe to a riskier decision. In this regard, empirical evidence suggests that the higher the number of women on board, the higher the total debt ratio in firms’ capital structure (Jaradat, 2015; Nadeem et al., 2019). However, another school of thought concluded that women have lower risk propensity and less confidence in decision making. Therefore, a corporate board dominated by female directors is more likely to be risk-averse (A. N. Berger et al., 2014; Loukil & Yousfi, 2016). In the same context, some studies reported a negative association between the number of women on the board of directors and the total debt ratio (Adusei & Obeng, 2019; Custodio & Metzger, 2014). This adverse effect of board gender on debt financing implies that gender diversified boards focused more on internal sources in financing their investment opportunities, especially when the CEO is a woman. This conclusion is in tandem with the conjecture mentioned above that women propensity to risk is lower than men in decision making. Consequently, this research stated the following hypothesis:

Methodology

Data Source and Sampling

This study exploited a secondary data collection source by utilizing the sampled firms’ annual reports and accounts covering the period from 2010 to 2019 (Bazhair & Alshareef, 2022). The paper developed some filters to generate the requisite data for analysis: firstly, financial firms’ capital structure composition is substantially different (Rajan & Zingales, 1995). The study excluded Saudi financial companies due to their unique reporting system and regulations. Besides that, this research does not consider companies with substantial missing data during the study period. Moreover, this study considers only the companies that disclosed debt capital in their financial statements because it measured the firm’s capital structure using financial leverage. Hence, the final study sample comprises of a balanced panel data of 100 Saudi non-financial listed companies. Given that this article sampled the dataset of 100 firms over 10 years (2010–2019), panel data methodology is the most appropriate analytical framework to achieve the research objective.

Econometric Model

This article reasoned that to determine the relationship between board governance mechanisms and capital structure, the generalised method of moments (GMM) is more appropriate. Using static estimation methods such as OLS and within estimator to estimate parameters in a dynamic framework that includes lagged dependent variable and firm-fixed effect may yield bias estimates (Arellano & Bond, 1991). The GMM corrects endogeneity and reverse causality problems between variables using an instrumental variable approach (Ozkan, 2001). The GMM is of two dimensions: The Difference GMM and system GMM. The difference GMM estimator uses the first differencing approach to deal with the possible bias and inconsistency of the static estimation techniques (Arellano & Bond, 1991). The difference GMM deals with endogeneity and removes fixed effects by using the first difference transformation. However, the first differencing technique may result in data loss when one applies it in an unbalanced panel (Roodman, 2009). Simulation studies also indicated that difference GMM performs poorly and produces weak instruments when the observed time is short (Bun & Windmeijer, 2010).

Given the limitations of the difference GMM approach, Arellano and Bover (1995) and Blundell and Bond (1998) developed the system GMM estimator. The system GMM uses the lagged differences of a dependent variable as instruments for the equation in levels, and the estimator also employed the moment conditions of lagged levels as instruments for the differenced equation (Blundell & Bond, 1998). The system GMM is relatively more consistent and robust because the framework introduces more moment conditions. The technique also makes such instruments exogenous (uncorrelated) with the fixed effects. Thus, there are gains in precision when one applies the system GMM estimator to a panel with short time-series observations. Therefore, this paper used the two-step system GMM to estimate board governance mechanisms as determinants of firms’ capital structure. The two-step GMM procedure is chosen because the technique utilises the first-step errors to construct more consistent standard errors robust to heteroscedasticity (Blundell & Bond, 1998).

Furthermore, Arellano and Bond (1991) identified two specification tests applicable in ascertaining the validity of GMM estimation results. The first test is the Hansen / Sargan test of over-identifying restrictions. The test determines the efficiency of GMM estimates by checking for the absence of correlation between the instruments and the error term (Hansen, 1982). The null hypothesis (H0) of the test is that the instruments set are exogenous. Hence, the decision rule is that one may reject the null hypothesis when the p-value of the Hansen/Sargan statistics is insignificant. Accordingly, an insignificant p-value of the Hansen/Sargan test signifies that GMM instruments are valid and robust. Another essential parameter that reveals the validity of GMM results is the serial correlation in the differenced error term. As shown by Arellano and Bond (1991), a first-order correlation (AR1) is expected due to the inclusion of lagged dependent term in the first differenced equation. Therefore, the presence of first-order serial correlation in residuals does not render GMM estimates inefficient. However, the second-order test (AR2) condition is there should be no correlation in the disturbance term. If the p-value of AR2 is significant, it shows that the assumption of uncorrelated error terms in AR2 is violated. Thus, indicating some degree of misspecification and demonstrating that the GMM estimate in question suffers from the second-order serial correlation. Specifically, following Ozkan (2001), this research used a partial adjustment model to capture how board attributes influence the dynamic adjustment to the target capital structure, as shown in equation (1).

Where

Study Variables

The study variables are categorised into the dependent variable, the explanatory and control variables. The capital structure (TD) represents the dependent variable, and it is computed as the ratio of the book value of total debt over total assets. Also, for robustness check, the article used the book value of total debt over total capital ratio (TDTC). The book value of total debt is chosen because it is reported that managers focus mainly on book values when setting their capital structure (Graham & Harvey, 2001). Also, Kyriazopoulos (2017) emphasised that measuring leverage using book value is more consistent and reliable in decision making because book value is insensitive to price fluctuations. The main explanatory variables include board size (BS), board independence (BI), CEO tenure (CEOT), and Board Gender (BG). BS is measured as the number of board members, while board independence is determined as the number of independent directors divided by board size (Alves et al., 2015; Jebran et al., 2019). CEO tenure is calculated as the number of years a CEO has held his position (Abor, 2007; P. G. Berger et al., 1997). Finally, board gender represents the number of women directors over the total number of board members (Adusei & Obeng, 2019; Ain et al., 2021; Zaid et al., 2020).

Also, the control variables are firm size (FS) and profitability (ROA), Tangibility (TANG), and GROWTH. Firm size is measured as the logarithms of the total assets (Abor, 2007; Agyei et al., 2020). Larger companies are associated with a higher debt level because they are relatively more diversified and have various return streams, stable earnings, and less vulnerability to bankruptcy (Sani & Alifiah, 2020; Titman & Wessels, 1988). In this way, leverage rises as firm size increases. Profitability (ROA) stands as the ratio of net profit before interest and taxes to the book value of total assets (Agyei et al., 2020; Zaid et al., 2020). In this context, the capital structure theories document contradictory views on the effect of leverage on firms’ profitability. For instance, the agency theory suggested that profitable companies are bound to have free cash flow (Jensen, 1986). Thus, firms with a high profitability ratio should take on more debt to control managers-shareholders agency conflicts. On the other hand, Myers and Majluf (1984) argued that given the relative information costs of external funding, profitable firms might likely employ lower debt in their capital structures (Appiah et al., 2020; Ngatno et al., 2021). As such, there will be a negative relationship between profitability and leverage. This measure of profitability appears to be more appropriate for us to gauge the tax advantage of debt financing (Moradi & Paulet, 2019). Tangibility is the net non-current assets over total assets (Agyei et al., 2020; Rajan & Zingales, 1995). Firms with a high proportion of tangible assets tend to have higher liquidation value and utilise more debts (Sani & Alifiah, 2020). Consequently, lenders will be relatively more willing to extend loans to firms with high tangible assets. GROWTH is calculated as capital expenditure divided by total assets (Appiah et al., 2020; Moradi & Paulet, 2019). Companies with high growth are embedded with underinvestment and assets substitution problems, and lenders may be less willing to supply loans to such firms (Agyei et al., 2020; Rajan & Zingales, 1995).

Results and Discussion

This section shows the empirical results that this research generated. It starts with demonstrating the descriptive analysis shown in Table 1, followed by the correlation results, which is contained in Table 2. Lastly, Table 3 displays the GMM regression estimates.

Descriptive Statistics.

Note. TD is the book value of total debt divided by the book value of total assets, TDTC is the ratio of total debt over total capital, BS is the total number of board members, BI is the number of independent directors over the total number of board members, CEOT is calculated as the number of years a CEO has been occupying his position, BG is the number of female directors divided by the total number of board members, FS is the logarithms of the total assets, ROA is the net profit before interest and taxes divided by total assets, TANG is the net non-current assets over total assets, and GROWTH is calculated as capital expenditure divided by total assets.

Correlation Results.

Note. TD is the book value of total debt divided by the book value of total assets, TDTC is the ratio of total debt over total capital, BS is the total number of board members, BI is the number of independent directors over the total number of board members, CEOT is calculated as the number of years a CEO has been occupying his position, BG is the number of female directors divided by the total number of board members, FS is the logarithms of the total assets, ROA is the net profit before interest and taxes divided by total assets, TANG is the net non-current assets over total assets, and GROWTH is calculated as capital expenditure divided by total assets.

Indicate significance at 1%, 5%, and 10% respectively.

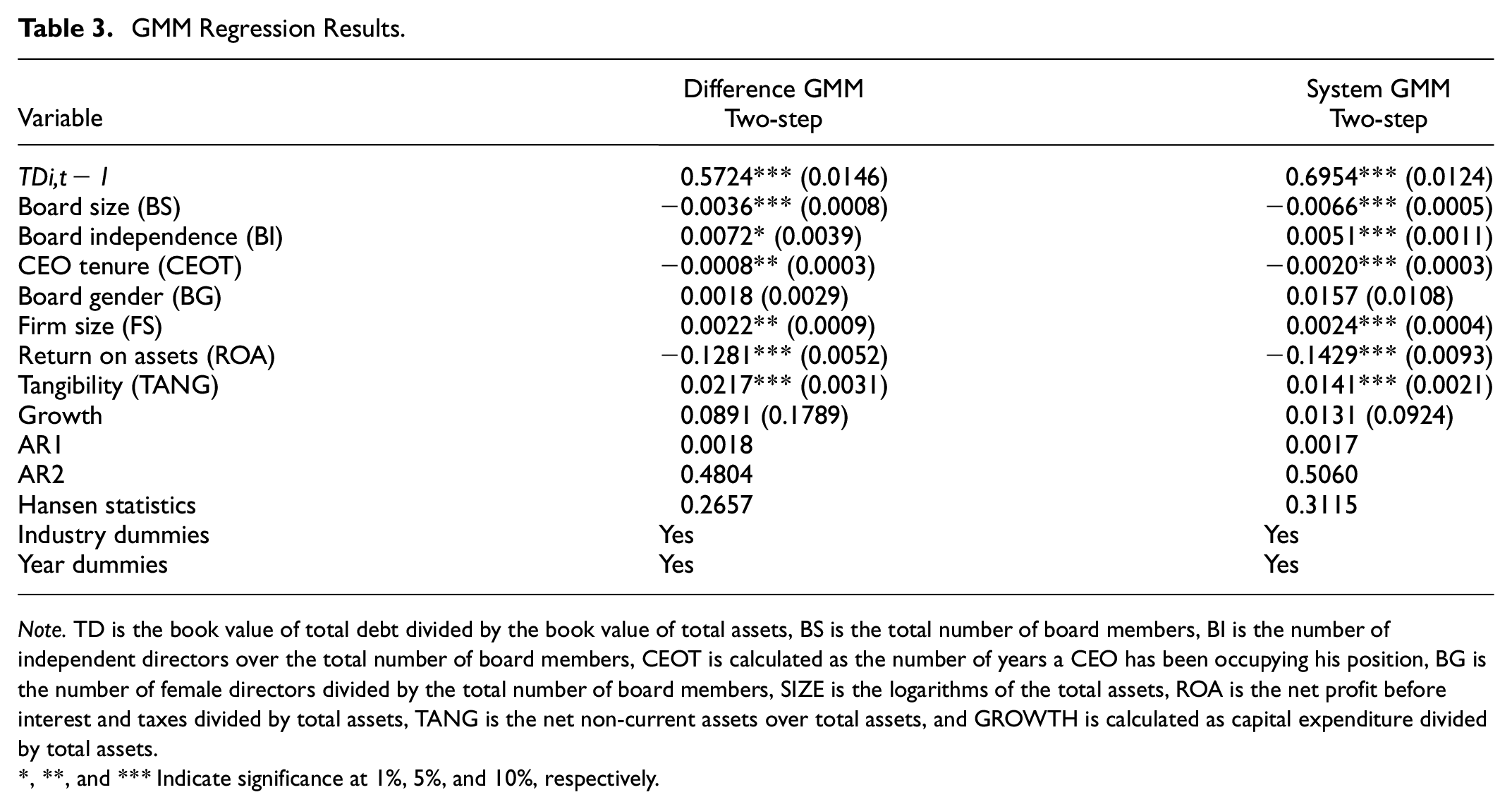

GMM Regression Results.

Note. TD is the book value of total debt divided by the book value of total assets, BS is the total number of board members, BI is the number of independent directors over the total number of board members, CEOT is calculated as the number of years a CEO has been occupying his position, BG is the number of female directors divided by the total number of board members, SIZE is the logarithms of the total assets, ROA is the net profit before interest and taxes divided by total assets, TANG is the net non-current assets over total assets, and GROWTH is calculated as capital expenditure divided by total assets.

, **, and ***Indicate significance at 1%, 5%, and 10%, respectively.

Table 1 presents the descriptive statistic of the study variables. The variable (TD) stands for the ratio of total debt over total assets, and its average value is 0.224. This result suggests that 22.4% of the firms’ total assets were financed by debt. Also, the TDTC ratio shows that debt represents 24.3% of the total capital the companies employed on average. Thus, the evidence implies that the Saudi non-financial listed firms rely heavily on equity financing in funding their assets. The board size (BS) of the firms indicates an average of eight members approximately, with a minimum and maximum of 3 and 13 members, respectively. Also, board independence (BI) shows that 44.4% of the board members are independent directors. CEO tenure (CEOT) registers a mean of about 4 years, with a maximum period of 10 years. Board gender (BG) stands as the proportion of women in the board of directors of these firms reveals a mean of 9.3% and therefore implies that, on average, men dominates the boards of Saudi non-financial firms. According to the statistics, the variable firm size (FS) measured as the logarithms of the firms’ total assets reveal a minimum and maximum ratio of 5.670 and 14.040, respectively. The return on assets (ROA) shows that the firms recorded a profitability ratio of 5.32% on average. This research attributes this low profitability level to the inability of the firms to obtain a substantial amount of borrowings, which in turn leads to a lower return on assets. The tangibility ratio (TANG) reveals a mean value of 0.434, thereby showing that the firms’ fixed assets investment stood at 43.4% on average. Lastly, the GROWTH indicator variable recorded a minimum and a maximum value of 0.006 and 0.620, respectively.

On the other hand, Table 2 contains the correlation results among the study variables. According to Gujarati and Porter (2010), multicollinearity arises when the correlation between explanatory variables is above 80%. Accordingly, the evidence from Table 2 shows that there is no strong relationship between the independent variables. Furthermore, the results show that the highest correlation among the explanatory variables is 31.4% between firm size (FS) and board size (BS). Therefore, the outcome reveals that the research model specification is free of the multicollinearity problem.

Table 3 exhibits the regression results using the two-step difference and system GMM approaches. The estimates for the system GMM represent the main results for the analysis, while the difference GMM regression result is presented for robustness check. According to both specifications, the lagged total debt ratio (TDi,t − 1) coefficient is positive and significant at the 1% level. This significant finding provides evidence that the specified model is dynamic and confirms that the firms adjust their capital structure to achieve a target leverage ratio. The P-value of the Sargan test and AR2 indicate that the GMM instruments used herein are valid, and equally, the model does not suffer from the second-order serial correlation. Based on the system GMM estimates, the adjustment speed (1 − 0.6954) indicates that board governance mechanisms influence the firms to close the gap between their actual leverage to their target debt ratio at the rate of 30.46% annually. That is to say, the effect of board monitoring will enable the firms to move to the optimum total leverage in about 3.3 years (100%/30.46%). This estimated adjustment for Saudi listed firms seems to be faster in comparison with Buvanendra et a. (2017) that found an annual adjustment speed of 26% for Indian firms. In contrast, this evidence suggests that Saudi are associated with high adjustment costs compared to Ramjee and Gwatidzo (2012) that reported an annual adjustment of 1.5 years for South African listed companies.

Moreover, the system GMM regression results in Table 3 indicate that board size is negatively related to the total debt ratio at the 1% significance level, thereby not supporting H1. This finding implies that firms with higher board members might be associated with slower adjustment to the target leverage due to the absence of stringent monitoring from larger boards. Thus, the result aligns with the agency theory argument that leverage in firms’ capital structure decreases as board size increases (Alves et al., 2015; Sheikh & Wang, 2012). On the contrary, the coefficient of board independence appears positive and significant at the 1% level. This evidence demonstrates that as the proportion of independent directors on the Saudi board of directors rises, leverage in their capital structure increases and supports H2. The empirical result agrees with the proposition that independent board members monitor managers vigorously due to their wealth of experience and expertise (Abor, 2007; Kyriazopoulos, 2017; Tarus & Ayabei, 2016). Such stringent monitoring from independent directors may pressure managers to rebalance firms’ capital structure with more debt to raise firm value. Thus, leading to this estimated significant positive association between board independence and optimum total debt ratio. CEO tenure is negatively related to total debt. Hence, the finding does not support the H3 that a positive relationship exists between CEO tenure and capital structure measured by total debt. This negative effect contradicts Orens and Reheul (2013) and Ndaki et al. (2018). The negative association between CEO tenure and target leverage reinforces the agency theory’s argument that CEOs with longer-term pursued a less levered capital structure (P. G. Berger et al., 1997). Perhaps, to avoid the performance pressure of debt financing. Thus, the result aligns with Wen et al. (2002) and Tarus and Ayabei (2016) who argued that CEO tenure is inversely related to debt financing.

Furthermore, board gender exhibits an insignificant coefficient, thereby contradicting H4 that board gender is positively related to leverage. The empirical evidence implies that gender may not explain target debt ratio adjustments across the Saudi listed firms. This estimated weak association may be attributed to the fewer female directors in Saudi firms. Again, the results disagree with prior studies that reported that the higher the number of women on board, the higher the total debt ratio in firms’ capital structure (Jaradat, 2015; Nadeem et al., 2019). Moreover, the control variables demonstrate signs consistent with the existing literature. Accordingly, the empirical results show that Saudi firms with larger size are associated with faster adjustment to the optimum leverage ratio. This finding supports the conjecture that bigger companies take on a higher debt level because they are relatively more diversified and have various return streams and stable earnings (Sani & Alifiah, 2020; Titman & Wessels, 1988). The coefficient of return on assets appears negative and significant at the 1% level. This result underscores the conclusion that profitable firms might likely employ lower debt in their capital structures given the relative information costs of external funding (Moradi & Paulet, 2019). This evidence implies that Saudi firms with higher profitability rebalance their capital structures with lesser debt. Also, the empirical findings demonstrate that Saudi firms with substantial investment in tangible assets are more likely to have higher adjustments to the optimum debt-equity ratio. The result supports the argument that firms with high fixed assets are better positioned to provide collateral to secure debt financing (Agyei et al., 2020; Sani & Alifiah, 2020). Also, this study found a positive association between Growth and debt financing. The finding implies that Saudi companies with high growth prospects maintain a levered capital structure to finance their growth opportunities. However, the growth coefficient appears insignificant in predicting the firms’ adjustment to the target capital structure ratio.

Robustness Check

To further confirm the robustness of the regression results in Table 3, this study employed the ratio of total debt over total capital (TDTC) as another proxy variable for measuring firms’ capital structure. The robustness analysis is provided in Table 4.

GMM Regression Results.

Note. TD is the book value of total debt divided by the book value of total assets, BS is the total number of board members, BI is the number of independent directors over the total number of board members, CEOT is calculated as the number of years a CEO has been occupying his position, BG is the number of female directors divided by the total number of board members, SIZE is the logarithms of the total assets, ROA is the net profit before interest and taxes divided by total assets, TANG is the net non-current assets over total assets, and GROWTH is calculated as capital expenditure divided by total assets.

and *** Indicate significance at 1% and 5%, respectively.

Table 4 provides additional evidence of the GMM estimates using a different measure of capital structure. Again, these results suggest an autoregressive coefficient similar to the earlier finding in Table 3. In other words, the lagged total debt over total capital ratio (TDTCi,t − 1) coefficient is positive and significant at the 1% level. This significant result implies that the Saudi firms adjust their capital structure to achieve a target leverage ratio. The p-value of the Sargan test and AR2 are insignificant, indicating that the GMM instruments used are valid, and the model does not suffer from the second-order serial correlation. More importantly, the coefficients of the explanatory variables are consistent with that of total debt divided by total assets ratio (TD) in Table 3. According to these results, board size and CEO tenure have negative and significant coefficients, whereas board independence remains positive and board gender still shows an insignificant coefficient. Therefore, the study findings appear robust using total debt divided by total assets ratio (TD) and total debt over total capital ratio (TDTC).

Conclusion

This research examined board governance mechanisms as the capital structure determinant of Saudi non-financial listed firms from 2010 to 2019. The paper exploited the GMM framework to effectively control endogeneity and reverse causality effects embedded in the relationship between board mechanisms and firms’ capital structure decisions. The analysis from the present paper strongly suggests that board size is negatively related to leverage. The evidence from this research supports the agency and resource dependency perspectives that independent directors provide effective monitoring and link firms to diverse resources, including leverage. More specifically, this article found that Saudi firms with more independent board members take on greater debt capital to raise their performance level. There is also evidence that significantly showed that CEO tenure and total debt are negatively related. However, board gender appears insignificant in predicting the Saudi listed firms’ borrowing decisions. The research findings also suggest that firm size and profitability are equally important determinants of Saudi listed firms’ leverage.

More importantly, the findings emanating from this research have some bearings on the financing decisions of Saudi firms. First, the firms should design their boards with a smaller board size with more independent board members to attract creditors. Attracting creditors may enable the firms to secure substantial leverage to operate an optimum debt-equity ratio. The preceding results support the arguments of the agency and resource dependency perspectives that stringent monitoring may enhance firms’ ability to secure debt finances at favorable terms. Hence, the findings imply that applying the prepositions of these frameworks may be quite relevant to the Saudi corporate environment. In addition, regulatory authorities should formulate a moderate tenure for CEOs because longer CEO tenure appears to be negatively associated with the supply of leverage to Saudi firms. Also, the empirical results generated on adjustment speed indicate the presence of adjustment costs in the Saudi stock exchange market. Therefore, the Saudi corporate boards and firms’ managers should consider the adjustment costs and other market frictions when designing the optimum debt-equity ratio. Although this research provides further insights on capital structure determinants, further studies can be undertaken to validate the findings of this article. Given that this study measured capital structure using the book value of debt, future studies should employ other capital structure measures like the market value of leverage to provide further empirical evidence. Likewise, upcoming research should attempt to generate predictions on how ownership structure and audit committee attributes may impact firms’ dynamic capital structure determination.

Supplemental Material

sj-xlsx-1-sgo-10.1177_21582440231172959 – Supplemental material for Board Governance Mechanisms and Capital Structure of Saudi Non-Financial Listed Firms: A Dynamic Panel Analysis

Supplemental material, sj-xlsx-1-sgo-10.1177_21582440231172959 for Board Governance Mechanisms and Capital Structure of Saudi Non-Financial Listed Firms: A Dynamic Panel Analysis by Ayman Hassan Bazhair in SAGE Open

Footnotes

Acknowledgements

The author acknowledges the contribution of Tadawul for providing data needed for this research work.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research work supports funding from Taif University, Saudi Arabia.