Abstract

This study aims to empirically examine the relationship between backdoor listing strategy, and the financial performance of companies in China. Two groups of control variables have been tested; the first group comprises firm characteristics, that is, firm size, growth, and leverage; the second group comprises macroeconomic factors, that is, inflation rate, gross domestic product growth rate, and interest rate. Using the Bloomberg database, a total of 10,775 firm-year observations are used in this study, which presents 2,155 non-financial companies for 5 years (2013–2017). The fixed-effect model is utilized to analyze the collected data. Tobin’s Q, return on assets, and return on equity served as measurements of the financial performance. The results show that the backdoor listing strategy has a positive correlation with the performance of companies in China. Firm size and interest rate show positive and significant relationships with returns on assets and equity, but a negative relationship with Tobin’s Q. Growth shows a positive and significant relationship with all financial performance indicators, however, leverage shows a negative and significant relationship with all three indicators. Finally, the inflation rate shows only a negative and significant relationship with Tobin’s Q but without returns on assets and equity. The results benefit companies’ managers by helping them figure out the impact of backdoor listing strategy on financial performance. The results may also benefit the policymakers who can regulate the backdoor processes and roles.

Plain language summary

This study aims to empirically examine the relationship between backdoor listing strategy, and the financial performance of companies in China. Using the Bloomberg database, a total of 10,775 firm-year observations are used in this study, which presents 2,155 non-financial companies for 5 years (2013–2017). The results show that the backdoor listing strategy has a positive correlation with the performance of companies in China. Firm size and interest rate show positive and significant relationships with returns on assets and equity, but a negative relationship with Tobin’s Q. Growth shows a positive and significant relationship with all financial performance indicators, however, leverage shows a negative and significant relationship with all three indicators. Finally, the inflation rate shows only a negative and significant relationship with Tobin’s Q but without returns on assets and equity. The results benefit companies’ managers by helping them figure out the impact of backdoor listing strategy on financial performance. The results may also benefit the policymakers who can regulate the backdoor processes and roles.

Introduction

With the COVID-19 pandemic, companies around the world are struggling to survive and enhance their financial performance. According to Bloomberg, 13.5% of Chinese industrial outputs dropped in the first 2 months of 2020, whereas 20.5% of the retailing sector’s revenue declined (Sun & Li, 2021). Over the past decade, a backdoor listing strategy has been adopted by companies to be listed on the stock exchange markets (D. C. J. Wang, 2018). Backdoor listing is a strategy that allows private and unlisted companies to enter the public stock exchange without the complicated process of an Initial Public Offering (IPO). Surprisingly, despite the high uncertainty and risk related to the backdoor listing strategy, it became the hottest mode on Wall Street, rapidly expanding to financial markets such as Canada, Germany, South Korea and the UK (Kim et al., 2021). According to Guo et.al., (2023), the number of companies that chose a backdoor listing strategy significantly increased in recent years those companies have successfully raised funds at substantial rates, as well as attracted more high-profile investors to invest in such an alternative scheme.

Earlier studies focussed on the motivations of companies to adopt this strategy, and they found easy and low-cost financing were the most motivational factors (Peng, 2011; Xu & Pei, 2011), this is because for a business to grow robustly, enterprises must obtain substantial financial support to fund strategic operations and production so that more profits can be gained (A. S. Alarussi & Gao, 2021). The Nobel prize-winning economist, Joseph Stiglitz once said, ‘Every large American firm grew up their business through mergers to a certain extent, and almost none of the large companies grew up through internal expansion’ (Zhang, 2015). Within this context, Essence Securities report showed that eight backdoor listed companies in 2016 raised $5.41 billion; nearly three times that raised from A-share IPOs in the first 3 months of backdoor listing (Shangjing, 2016). In addition, backdoor-listed companies enjoyed other advantages such as government support (S. Li, 2014); transforming companies’ operations (Feng & Shanthikumar 2016), getting superiority in the capital market (D. C. J. Wang, 2018), and increasing corporate visibility (Gao, 2018). Other studies focussed more on the impact of backdoor listing strategy on firms’ management earnings (Boubaker et al., 2017), governance quality (Brogi et al., 2020), and aftermarket performance (Cao-Alvira & Rodríguez, 2017). Few studies analyze the performance of backdoor listing firms, for example, Lin (2017), Shi (2018), Zhao (2018), Gahng et al. (2021), Kiesel et al. (2022), the results, however, are not consistent as most of these studies are case studies, and the results depend on the type of companies under study. Under this assumption, some studies confirmed a positive association between backdoor strategy and financial performance in the short run (Mengru, 2021; Peidong, 2014; Yuhong, 2020; Zhang, 2015; Zhao, 2018), other studies found a lower financial performance after adopting a backdoor strategy (Adjei et al., 2008; P. Brown et al., 2013; Greene, 2016). Pollard (2015) reported a lower earning quality of backdoor listing firms, especially firms with low institutional ownership (Shamki & Alarussi, 2017). Song et al. (2014) analyzed Korean companies’ data from 2000 to 2010, they reported that backdoor listing firms have higher leverage, lower profitability, and higher information asymmetry than those in IPO listing. Besides, the performance of backdoor listing firms was worse than IPO firms in the long term. A later study by Kim et al. (2021) reported that Korean backdoor listing firms neither generate marketing benefits nor get a significant change in their stock and operating performance in the long run. Dasilas et al. (2017) reported that backdoor listing firms in the European market receive significant wealth gains for their shareholders, the short-term gains seem to revert to substantial losses in the long term. Besides, their financial performance did not significantly improve. Similar results are found by Gleason et al. (2006) and Santoso (2016).

Since China became a member of the World Trade Organization (WTO) in 2001, IPO in China still adopts the approval system, and hence, the listing requirement is relatively stringent and requires a longer processing time. According to X. Wang (2015), almost 840 companies in the capital market are queueing up to get listing status. Nevertheless, with the rapid growth of the Chinese capital market, especially the establishment of the Small and Medium Enterprise (SME) board, the Growth Enterprise Market (GEM) has gradually increased the opportunities for enterprises to go public (T. Nguyen et al., 2019). However, since the IPO listing requirements are complicated, many companies choose the alternative route to going public through a backdoor listing in the securities trading market. The backdoor listing of China’s inland companies first started on the Hong Kong Stock Exchange.

The current study intends to empirically examine whether adopting a backdoor strategy improves firm performance by using data from many companies, from different industries in China. This study differs from previous studies in various aspects: first, this study adds value to the extant literature on backdoor strategy. Although the backdoor listing is gaining popularity, and research on this scheme is relatively scarce compared to the huge number of studies on IPO. Second, previous studies have used Buy-and-Hold Abnormal Return (BHAR) and Cumulative Abnormal Return (CAR) to measure firm performance, however, this study uses Tobin’s Q (TOBINSQ), return on equity (ROE) and return on assets (ROA) to measure firm performance, so the results of this study are solid and concrete. The majority of studies have used one or more of these measurements for firm performance (e.g., Alarussi et al., 2009; P. R. Brown et al., 2010; Lindrud et al., 2014). Finally, previous studies have focussed more on the characteristics of backdoor listing companies (Arellano-Ostoa & Brusco, 2002; Aydogdu et al., 2007; Greene, 2016), or the factors that motivate companies towards backdoor listing (Adjei et al., 2008; Beerannavar et al., 2015; Z. D. Wang, 2019) or the performance of backdoor listing firm – case based (J. N. Li, 2019; Miao, 2019; W. B. Yang, 2018).

Thus, the inconsistent results of the relationship between adopting a backdoor strategy and firm performance complicate the task of management in companies, regulators, and related parties to make the right decision, which opens the door for a further and comprehensive investigation. Thus, the current study aims to empirically examine this relationship by utilizing the data of many Chinese companies (constituting 62% of the total Chinese listed companies) for a 5 year period (2013–2017), covers different sectors, and includes more control variables to come up with concrete results that enhance in-depth understanding for stakeholders regarding whether firm performance differs after taking part in backdoor listing activities. In essence, this study aims to answer the following question: what is the impact of adopting a backdoor strategy on Chinese firms’ performance?

The results show a significant improvement in Chinese firms’ performance after adopting a backdoor strategy, however, the control variables show different influences on firm performance. The rest of the paper is structured as follows: Section 2 explains previous studies and hypotheses development; section 3 presents the methodology, data collection, and analysis; Section 4 discusses the results, and Section 5 concludes the study.

Literature Review

Previous Studies

The IPO means a previously unlisted company or private company sells new or existing securities and offers them to the public company for the first time. Before the IPO practice, the company has a limited number of shareholders and accredited investors, including high-net-worth individuals and the founder. After an IPO, the issuing company becomes a publicly listed company on a recognized stock exchange. There are many advantages of being a public company such as fundraising (Loughran & Ritter, 2002), accessing lower cost of capital for new investment plans or to repay outstanding loans (Ljungqvist, 2007), and enhancing the market reputation of a company (Demers & Lewellen, 2003). However, being a public company is not an easy task; some disadvantages of IPO listing are loss of control by business founders and current shareholders (Dolvin & Jordan, 2008; Smart & Zutter, 2003); following strict rules and regulations of transparency and disclosure requirements, which may affect a company’s competitive advantage (Habib & Ljungqvist, 2001); last but not least, being a public company is very costly and a company has to bear different costs such as listing fees, underwriting fees, and brokerage, legal and accounting fees, share registry costs, and other related costs of regulations compliance (Loughran & Ritter, 2002). Hence, companies found the backdoor listing strategy a good alternative to benefit from the advantages of being public and avoid the disadvantages.

The firm performance presents the results obtained by management, economics, and marketing in providing competitiveness, efficiency, and effectiveness to the company (A. S. Alarussi, 2021; A. S. A. Alarussi, 2021; Taouab & Issor, 2019). Several studies have been conducted to study the firm performance of the backdoor listing; Yuhong (2020) studied the changes in corporate financial performance due to adopting a backdoor strategy, by using a case study (SF Express). The findings showed improvement in the financial performance of SF Express, however, he recommended that companies should choose suitable listing schemes according to their financial characteristics, and realize the related risks before deciding to join the backdoor listing. These findings are supported by Z. D. Wang (2019) when he studied the impact on Y.T. Express’s financial performance after joining the backdoor listing. He reported that the capital of the company increased by almost 200% within a couple of months of joining. Similarly, Yao (2021) compared the performance of Aiko Solar before and after the backdoor listing, and found after joining, the shareholders obtained additional income, increasing their wealth significantly. However, Gleason et al. (2006) distributed a questionnaire survey to compare the operating performance of the companies listed through IPO versus through backdoor listing. The questionnaire survey was based on several core indicators, including the company’s assets, cash-to-asset ratio as well as ROA and ROE. Their analysis concludes that the operating performance of companies through backdoor listing is lower than the performance of companies that choose IPOs, and the former companies have a higher probability of bankruptcy. He also argued that most of the merged companies that chose the backdoor strategy to qualify for listing have not shown significant improvement in operations and profitability after the merger, as evidenced by only 46% of the sample companies that could sustain profitability for more than 2 years. P. Brown et al. (2013) and Greene (2016) reported that private firms have lower shareholder returns after engaging in backdoor listing compared to shareholders’ returns in private firms with IPO listing. Carpentier et al. (2012) argued that the long-term average returns on investment of backdoor-listed companies are lower than that of companies listed through IPOs, whereby the long-term performance of the former cannot reach an optimal level. Arellano-Ostoa and Brusco (2002) implied that 32.6% of companies listed through reverse acquisitions were delisted in less than 3 years in both the biggest stock markets in the United States; the New York Security Exchange (NYSE) and Nasdaq. A later study by Adjei et al. (2008) reported that 42% of sample companies that engaged in backdoor listing chose to delist, as compared to 27% of sample companies that listed through IPO in less than 3 years of listing. This implies that the performance of backdoor listing companies is relatively poor, and they cannot sustain or achieve increasing shareholders’ wealth in the long term, ultimately leading to financial distress. Furthermore, Santoso (2016) stated that firm performance has no apparent deviation in terms of current ratio, asset turnover ratio, debt-to-equity ratio, and return-to-equity ratio, regardless of prior, during or after backdoor listing. This is supported by Masulis (1983) that backdoor listing does not influence financial performance, especially in the short run, and any change in firm performance may have been caused by other reasons, such as the company’s debt level.

For a country like China, which has an immature economy as well as an imperfect capital market, it is relatively reliable to use financial indicators to study the performance because of the backdoor listing. Yuhong (2020) examined the impact of backdoor listing on corporate financial performance. He used the case analysis method and measured financial performance via financial indicators, that is, debt-paying ability, operating ability, profitability and growth ability. The findings display a general improvement in all firms’ financial performance due to adequate capital and broader business scope. Yuhong (2020) supported these results and found that the changes in the operating performance of the firms in the short term are apparent, but in the long term, there is not enough evidence to show that it has an upward trend. However, Zhou (2013) argued that the performance of the sample companies after the reverse takeover is greater than the performance before the reverse takeover in the short, or long term in China. Moreover, Lee et al., (2014) found backdoor listing companies significantly increased their overall operating performance and argued that joining backdoor listing can have a positive effect on stock prices. Huang and Yin (2007) found that the initial shareholders mostly obtained high investment value-added gains after the backdoor listing of security companies. Similar results were found by M. X. Yang (2000). Furthermore, P. C. Li (2010) argued that backdoor listing is important to enhance the economic efficiency of companies. In short, most of the existing studies have shown mixed and inconsistent results which justify further investigation of the impact of backdoor transactions on firm performance. For measurement purposes, Sauaia and Castro (2014) explained that TOBINSQ is the ratio of the market value of the company’s assets and the replacement value of its assets to indicate the value of the firm, and Samiloglu et al. (2017) asserted that both ROA and ROE are accounting-based indicators that bring income statements and balance sheets together to measure the performance of a company, although income statements and balance sheets are different performance indicators, whereby ROA measures amount of earnings generated from assets, and ROE measures how much profit a firm generates as a percentage of shareholders’ equity (Hannagan, 2008). So, despite their differences, TOBINSQ, ROA, and ROE are all in fact measurements of firm performance.

Selection of Variables, Hypothesis Development

Backdoor Listing Strategy

The backdoor listing strategy is a unique type of merger and acquisition and an alternative route to going public without an IPO. Gleason et al. (2005) argued that the backdoor listed companies have inferior operating performance through reverse acquisition. Similar results were found by P. Brown et al. (2013) and Greene (2016) that private firms have lower shareholder returns after participating in reverse takeovers. However, Yuhong (2020) indicated that companies showed significant improvements in their overall operating performance after carrying out backdoor listing. These results are supported by Zhou (2013), Lee et al., (2014), and Huang and Yin (2007), who reported a positive effect of the backdoor listing on stock prices, and the initial shareholders mostly obtained high investment, value-added gains after the transaction. Based on the management synergy theory, before the execution of mergers and acquisitions, the target companies often have poor management, resulting in the firms having to face the dilemma of unsatisfactory performance. In line with the management synergy theory, when two business units with different management efficiency levels incorporate as one, the acquiring firm which has higher capabilities in management tends to have control of the poor management firm (A. S. Alarussi, 2021; A. S. A. Alarussi, 2021; Servaes, 1991). This will lead the target companies to take advantage of good management firms to maximize the utilization of their management resources, thereby creating potential value growth for both parties and improving society’s welfare. Based on the above discussion, it is expected that backdoor listing strategy and firm financial performance have a positive relationship. Hence the hypothesis is drawn as follows:

H: There is a positive relationship between backdoor listing strategy and the financial performance of firms in China.

Control Variables

Firm-specific

Firm Size

Dang et al. (2018) suggested that scholars must consider the impact of firm size on firm performance. A. S. Alarussi and Alhaderi (2018) found a significantly positive relationship between firm size and profitability in Malaysian companies. Similar results were found by Lee (2009), who concluded that firm size plays a significant role in profitability, which in turn, affects firm performance. Hashmi et al. (2020) utilized the data of 25 companies from Brazil, Russia, India, China, and South Africa, for 10 year period from 2006 to 2015. He found a positive association between firm size, measured by the log of total assets, total sales, the market value of equity and number of employees, and financial performance, measured by ROA and ROE. Hence, without confounding the results, firm size is used in this study as one of the control variables to effectively indicate the performance of backdoor listing firms. In brief, firm size is considered a control variable because it may influence the results of firm performance.

Growth

Rahim (2017) argued that firm growth is relatively significant in different aspects, as it can sustain the firm’s business towards making more profit than the previous year. This, in turn, can improve firm performance to prevent financial distress. Since there is a significant relationship between company growth and performance, it is expected that this relationship would be true when assessing backdoor listing. Therefore, firm growth is included in the model to control for the variability in firm performance. Zhang (2015) stated that net income growth can be applied to determine firm growth, by using the formula of deducting the net income growth of the previous year from the current year, dividing it by the net income growth of the previous year, then multiplying by 100. In short, this paper looks at the effect of backdoor listing while holding firm growth as constant.

Leverage

Many studies have concluded that leverage is a significant indicator of many management decisions that (directly or indirectly) affect companies’ financial performance. Liargovas and Skandalis (2012) found that leverage affects firm performance. Obradovich and Gill (2013) argued that companies with high financial leverage may affect firm performance by increasing the probability of bankruptcy, thus increasing agency costs. Similar findings were reported by A. S. Alarussi and Alhaderi (2018). This study sets leverage as a constant so that it does not affect the results throughout the research. The asset-liability ratio, which is also known as the debt ratio, is applied to measure leverage, that is, the proportion of total assets financed through total liabilities (Enekwe et al., 2014). In brief, leverage acts as a control variable in the regression of firm performance on the backdoor listing.

Macroeconomic Factors

Inflation Rate

The inflation rate is one of the macroeconomic variables that may influence a company’s future profitability, and indisputably, is beyond the control of the firm (Issah & Antwi, 2017). Hence, Broadstock et al. (2011) suggested that it is needed to know the effect of the inflation rate on firm performance and to examine the results without heterogeneous impact. To clarify, the inflation rate refers to the percentage of increase as well as a decrease in prices in a certain period. It also implies how fast prices go up throughout the period (Amadeo, 2020). This study keeps the inflation rate constant to minimize the impact on firm performance.

Interest Rate

Odalo et al. (2016) revealed that the interest rate has a significant relationship with ROA and ROE, whereby both are indicators of firm performance. Furthermore, Loveland (2018) indicated that the GDP growth rate can influence the interest rate, in that the interest rate may also have an indirect effect on firm performance. Since the interest rate is not the emphasis of this study, it is controlled in this study model.

Methodology and Data Collection

Data, Sample, and Model Specification

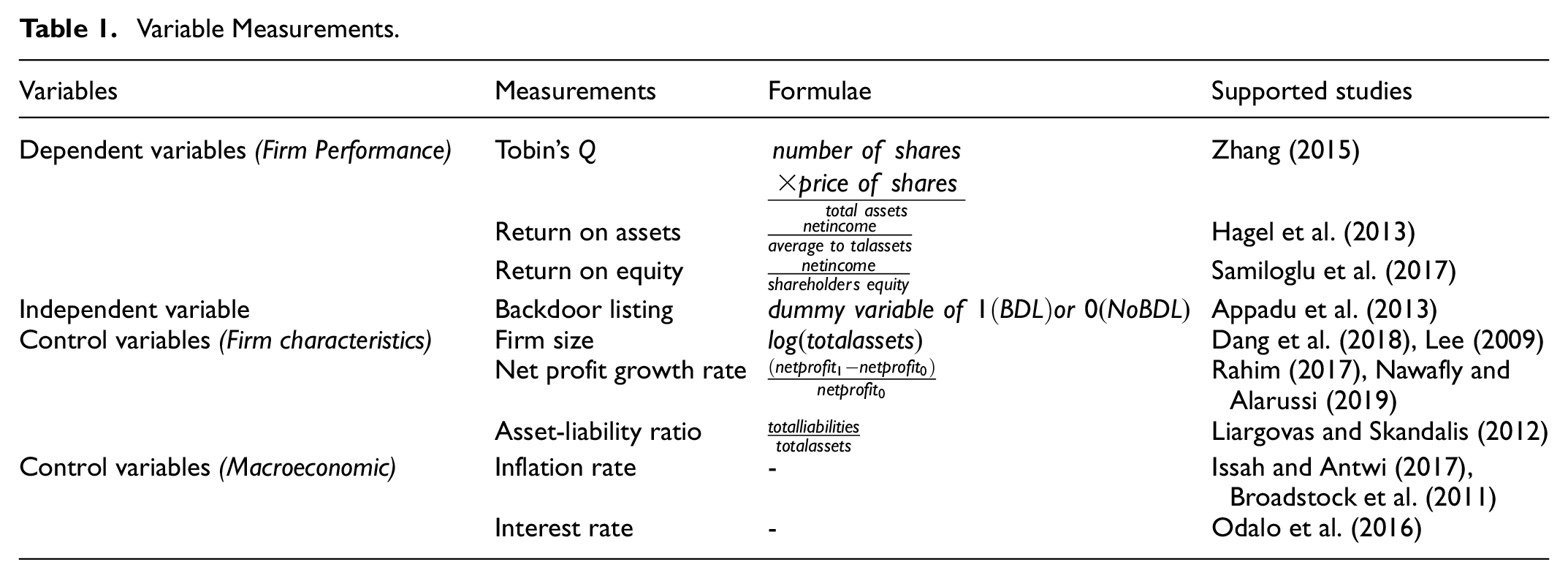

This empirical study used secondary data collected from companies listed on both the Shanghai Stock Exchange and Shenzhen Stock Exchange in China. The sample size of this study is 2,155 non-financial listed companies, constituting 62% of the total listed companies in China. The data was derived from a secondary source, that is, the Bloomberg Database, for 5 years from 2013 to 2017, which was the available completed information at the time of conducting the study, and so, the total firm-year observations are 10,775. The researchers chose a large sample size and 5 years to come up with robust results, which can help the users to make the right decisions. The years between 2013 and 2017 were chosen, as these 5 years include the period when the Chinese government devalued the Yuan currency, and they were the recent data available at the time of conducting this study. This study has one independent variable, which is backdoor listing strategy, and one dependent variable, which is financial performance. Two groups of control variables were examined in this study: the first group comprises firm characteristics, that is, firm size, growth, and leverage; and the second group comprises macroeconomic factors, that is, inflation rate and interest rate. The variables and their measurements are elaborated in Table 1.

Variable Measurements.

Variable Measurements

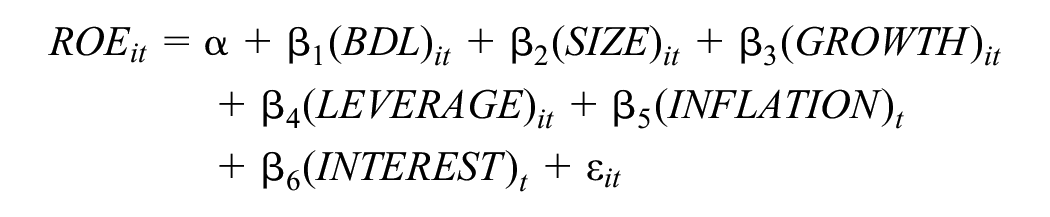

Since this study is a longitudinal study, fixed-effect models were used to analyze the data to interpret the results of the analysis. Therefore, the following equations present the three models to measure performance:

where:

the Tobin’s Q of a firm in year t is

Results and Discussion

Descriptive Statistics

Table 2 shows that TOBINSQ has a mean of 2.3037 and a standard deviation of 2.0449. The mean and standard deviation of the other two financial performance measurements, namely ROE and ROA, were also determined.

Descriptive Statistics of Variables.

N = 10,775.

The central tendency of ROE is 6.357%, whereas ROA has an average value of 3.95%, showing that ROE has a higher mean than ROA. Therefore, the descriptive statistics imply that the public firms listed on both the Chinese Exchanges are performing better in the aspect of ROE compared to ROA. As for the measures of dispersion, ROE has more variability as it has a standard deviation of 16.80 compared to the standard deviation for ROA at 5.99 The backdoor listing strategy is a dummy variable, and the mean and standard deviation are just mathematical functions that do not mean anything in this case.

Furthermore, the firm characteristics are control variables, that is, firm size (SIZE), firm growth (GROWTH) as well as leverage (LEVERAGE), which were also tested for their mean value and variability. To clarify, SIZE conveys that the listed firms in both Exchanges in China average 22.297, with a dispersion of 1.318. GROWTH denotes that the 2,155 sampled companies have an average increase in sales of 18.90% per annum, with a standard deviation of 16.37. LEVERAGE has an average value of 43.36% with a standard deviation of 20.81, representing that listed firms in China’s Exchanges rely heavily on debt financing and have huge volatility. Thereafter, for control variables from the aspect of macroeconomic variables, inflation rate (INFLATION) signifies a mean value of 1.898 with a dispersion of 0.359, while interest rate (INTEREST) indicates an average value of 4.93 with a 0.7216 standard deviation.

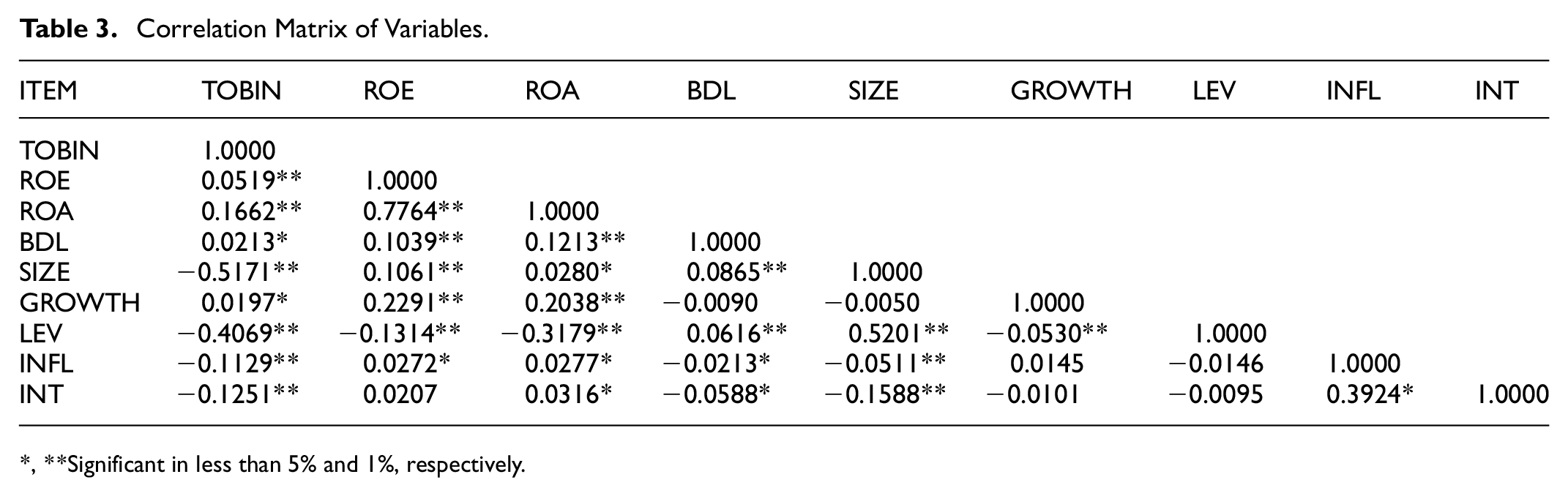

Correlation Analysis

Table 3 shows the correlation matrix that was performed to test the correlation among all variables. Ratner (2009) suggested that coefficients that lie between 0 and .3 (0 to −.3) imply a weak and positive (negative) correlation; coefficients between .3 and .7 (−.3 to −.7) show a moderately positive (negative) correlation, and coefficients that lie between .7 and 1.0 (−.7 to −1.0) are viewed as strongly positive (negative) correlation. This empirical study examines the correlations among the three measures of financial performance and a relatively low correlation of TOBINSQ with ROE and ROA is observed at the values of .0519 and .1662, respectively. The weak correlation entails an essential understanding that TOBINSQ is different from ROE and ROA, justifying the study on the effect of backdoor listing which involves the independent examination of each firm performance indicator. However, it is found that ROA and ROE have a great correlation of .7764 and this is a normal correlation since both present the measurements of firm performance.

Correlation Matrix of Variables.

*, **Significant in less than 5% and 1%, respectively.

Table 3 also shows that the three measurements of financial performance, TOBINSQ, ROE, and ROA, have positive correlations with BDL, with the correlation coefficients at .0213, .1039, and .1213, respectively. Further, from the aspect of firm-related control variables, SIZE has the greatest negative correlation with TOBINSQ, which conflicts with Dang et al. (2018).

A positive correlation is detected between GROWTH and TOBINSQ, ROE, and ROA; however, LEVERAGE has a negative association with each indicator, which concurs with Obradovich and Gill (2013). Further, in similarity to Broadstock et al. (2011) and Odalo et al. (2016), this correlation matrix demonstrates that the macroeconomic control variables of INFLATION and INTEREST have significant relationships with financial performance. Additionally, the control variables, in general, have a weak correlation with each other as well as with the independent variable of BDL, since all their correlation coefficients fall below .3. Nevertheless, one of the exceptions is the correlation between SIZE and LEVERAGE as there is a significant coefficient of .5201 between them, as supported by Marete (2015), who suggested that there is a significant link between firm size and financial leverage. Besides, another exception is the correlation between INFLATION and INTEREST, with a value of .3924, which is because both variables are macroeconomic variables, and so, it is common to be correlated.

Soliman (2013) recommended that since no correlation value exceeds .8 among the independent and control variables, it implies that there is no multicollinearity. As a result, no adjustments had to be made; Pooled OLS Regression is widely used and recommended for panel studies because it generates unbiased and consistent estimates of parameters even when time-constant attributes are present (Zariyawati et al., 2009; Zhou, 2013). Moreover, pooled OLS regression is favored for data without dummy variables, which is the case of this study to obtain robust results, a fixed-effects model was run. The fixed-effect model has no bias and is statistically adequate for this empirical research. It has been argued that the significance of using the fixed-effect estimator is to limit any endogeneity issue by controlling firm characteristics that are not included in the regression model although they may have some connections with the model (Lazar, 2016).

Regression Analysis

The results of the Pooled OLS regression and fixed-effect model for the three different firm performance indicators of TOBIN’S Q, ROA, and ROE are computed in the following Tables 4 and 5. From Tables 4 and 5, it is noted that the F-test indicates the overall significance of the regression models by examining all model terms to assess the fit of the corresponding linear models. It is observed that Prob > F, which means the p-value of the F-test is smaller than the significance level of 1% and 5% in all three models. In addition, it can be said that overall, the three regression models are highly significant, as both independent and control variables can improve the fit of the models since they are jointly significant in predicting Tobin’s Q, ROA, and ROE. The adequacy of the experimental results is R-squared, as it exposes how well the regression model fits the sample data by revealing the intensity of the relationship between the models and financial performance.

Regression Results Model 1 (TOBIN’S Q).

Note. TOBINSQ = Tobin’s Q; ROA = Return on Assets; ROE = Return on Equity; BDL = Backdoor listing; SIZE = Firm size; GROWTH = Growth rate; LEVERAGE = Leverage; INFLATION = Inflation rate; INTEREST = Interest rate of the country.

**, ***Significant in less than 5% and 1%, respectively.

Regression Results Model 2 (ROA) & Model 3 (ROE).

Note. TOBINSQ = Tobin’s Q; ROA = Return on Assets; ROE = Return on Equity; BDL = Backdoor listing; SIZE = Firm size; GROWTH = Growth rate; LEVERAGE = Leverage; INFLATION = Inflation rate; INTEREST = Interest rate of the country.

Significant in less than 1%, respectively.

From the findings in Tables 4 and 5, the regression models indicate that the R-squared values are equal to 0.3401, 0.2077, and 0.1204, respectively, which are good. The adjusted R-squared values for the three models are not that much different from the R-squared values, which are 0.3397, 0.2072, and 0.1199, respectively, signaling that 34%, 21% and 12% of the variance in the financial performance indicators are justified by the individual models. Torres-Reyna (2007) argued that when there is only a small number of variables with a relatively large sample size, the values of the R-squared and the values of the adjusted R-squared are close, which is the case in this study. Disclosing that the model is considered statistically significant.

Tables 4 and 5 show positive and significant relationships between backdoor listing (BDL) and the firm performance indicators of Tobin’s Q, ROA, and ROE in the three models, retaining a p-value of 0 at the significance level of 1%. Moreover, the firm-specific and macroeconomic control variables are incorporated in this study to precisely assess the relationship between the dependent and independent variables. The firm-related control variables are established since they may lead to some plausible effects on firm performance, that is, firm size, growth, and leverage. The findings show that firm size (SIZE) has a negative correlation with Tobin’s Q, but is positively related to ROA and ROE, at the significance level of .01. To explain, a unit increase in firm size of listed companies will lead Tobin’s Q to decrease by −.85 units, while ROA and ROE will each increase by 1.20% and 2.68% respectively. Apart from that, the growth (GROWTH) of companies has a significantly positive effect on ROA and ROE at the significance level of 1%. It is anticipated that a 1 -unit increase in firm growth, will increase 0.006 and 0.0184 units in ROA and ROE, as demonstrated in Table 5.

Firm leverage (LEVERAGE) demonstrates negative relationships with each of Tobin’s Q, ROA and ROE with a significance level of 1%. When leverage increases by 1 unit, Tobin’s Q will decrease by .0200 units, while ROA and ROE will drop by 13.04% and 17.84%, respectively. Tables 4 and 5 also show the findings of the macroeconomic control variables: inflation rate (INFLATION) has a negative effect on Tobin’s Q, ROA, and ROE at the 1% and 5% significance levels. To make it clear, a 1% increase in the inflation rate will lead Tobin’s Q to drop 0.49 units at the same time as the ROA and ROE fall to 07.56% and 46.72%. Besides, the interest rate (INTEREST) shows a negative correlation with Tobin’s Q but a positive relationship with ROA and ROE. A 1 -unit increase in interest rate will result in Tobin’s Q dropping by 0.56519 units, whilst leading to both ROA and ROE increasing by 63.94% and 102%, respectively.

The relationships between the control variables and financial performance cannot be compared to previous studies as these studies have not paid attention to this aspect. In conclusion, backdoor-listed companies perform better than non-backdoor-listed companies in terms of Tobin’s Q, ROA, and ROE, even after considering all the firm-specific and macroeconomic control variables.

Discussion of Results

The study examines the association between backdoor listing strategy and companies’ financial performance. Firm size, growth, leverage, inflation rate, gross domestic product growth rate, and interest rate are the control variables in this study. The results of the regressions are elaborated on as follows:

Backdoor Listing Strategy

The backdoor listing strategy is a unique type of merger and acquisition, and an alternative route to go public without an IPO. Tables 4 and 5 show positive and significant relationships between backdoor listing strategy and firm performance measurements Tobin’s Q, ROA, and ROE. The coefficients t-value = 0.7251492, 3.907861 and 7.666335 respectively at p < .001 which confirms these positive and significant relationships. This indicates that companies adopting the backdoor listed strategy, are expected to perform .54 units better than companies that do not carry out backdoor listing in terms of Tobin’s Q, 3.4 units better in terms of ROA, and 6.3 units better in terms of ROE. Despite ROA and ROE being positively correlated to backdoor listing, the coefficient of the latter is larger than the coefficient of the former, inferring that backdoor listing has a more significant influence on ROE. In general, all these findings evidence there is a positive and significant association between backdoor listing strategy and firms’ financial performance in China, which supports the hypothesis of this study. Hence the study hypothesis is accepted. This result is in line with Feng and Sun (2001), and Zhou (2013).

Firm Size

Tables 4 and 5 show mixed results regarding the relationships between firm size and firm performance indicators; in Table 4, the results show a significant but negative association between firm size and Tobin’s Q. the coefficient t-value = −0.8525856 and p < .001. Badri Shah et.al. (2021) found a negative and significant relationship between firm size and Tobin’s Q. This result suggests that bigger firms have lower growth potential than that smaller ones. Similar results were found by P. Nguyen et al. (2015) and Coles et al. (2008). For the second and third models of ROA and ROE, the coefficient t-value = 1.206527 and 2.688073 respectively at p < .001. Hence, if enterprises in China are expanded, their profitability will be improved as indicated by the empirical results, which support the resource-based view theory, that is, the bigger the firm, the more the financial resources accessible, leading to lower cost of capital and higher return in asset and equity. The result is like the findings of Gaio and Henriques (2018) and Sritharan (2015). Overall, the result shows Chinese companies’ significance in increasing and expanding to different territories and places.

Growth

The results of Tables 4 and 5 show a positive and significant association between growth and both ROA and ROE. The coefficient t-value = 0.0006194 and 0.0018426 respectively and p < .01 prove these significant relationships. Hence, if Chinese firms maintain continuous growth, they can avoid financial distress, which, in turn, enhances the firms’ performance and profitability (Rahim, 2017). Similar results are also found by Zhang (2015).

Company Leverage

The results of Tables 4 and 5 show negative and significant relationships between Leverage and all financial performance indicators (Tobin Q, ROA, and ROE). The coefficient t-value = −0.0200422, −0.1304018 and −0.1784163 respectively, and the p < .001. This can be explained by Chinese companies relying heavily on debt financing and have huge volatility. When the level of financial leverage is high, the cost of this borrowing will be high and this, in turn, negatively affects the firm’s profitability. Similar results were found by Aryantini and Jumono (2021) and Andersson and Minnema (2018).

Inflation Rate

It was expected that the inflation rate negatively affect the firm performance indicators, but the results from Tables 4 and 5 show a negative and significant relationship between the inflation rate and Tobin Q, but not with ROA or ROE. The coefficient t-value = −0.4861078 and the p < .001. This means when the inflation rate increases, it negatively affects the purchasing power of money which leads to increased prices over consumers, and therefore lowers the volume of sales of companies which negatively affects their performance. The Similar results are reported by Frimpong and Oteng-Abay (2010) and Moyo and Head (2020).

Interest Rate

Tables 4 and 5 show mixed results regarding the relationships between interest rate and firm performance indicators; in Table 4, the results show a significant but negative association between interest rate and Tobin’s Q. The coefficient t-value = −0.5651984 and p < .001. For the second and third models of ROA and ROE, the coefficient t-value = 0.6394742 and 1.235121 respectively at p < .001, which proves the positive and significant relationships between interest rate and ROA and ROE. The explanation for this mix results is any increase in the interest rates will raise the company’s cost of capital and therefore, a company should struggle harder to generate higher returns by increasing the sales volume (this leads to higher ROA and ROE) to pay a high-interest environment, If not, then interest expense will take its profits and lead to lower profits, lower cash inflows, and a higher required rate of return for investors, which all negatively affect a company fair value and therefore its Tobin’s Q ratio. Similar results were reported by Odalo et al. (2016) and Kanwal and Nadeem (2013).

Conclusion

The effect of the backdoor listing strategy on firm performance in China has not been fully explored yet; therefore, this research focuses on and examines this relationship by using the data of 2,155 non-financial companies listed on the Shanghai and Shenzhen Stock Exchanges of China from 2013 to 2017. With a total of 10,775 firm-year observations, the fixed-effect model in STATA was used to analyze the collected data. Three different types of financial performance measurements were used (Tobin’s Q, ROA, and ROE) to assess the impact of a backdoor listing strategy on financial performance. The findings show that backdoor listing is positively correlated to all three firm performance indicators. This suggests that companies that carry out backdoor listing strategies have better financial performance indicators (Tobin’s Q, ROA, and ROE) than companies that do not carry out such a strategy. In addition, the results show that firm size, growth rate, leverage, inflation rate, and interest rate of the country, have significant relationships with financial performance indicators. The findings provide a basis for the operating managers and executives to consider whether to adopt this strategy as well as whether it can bring any improvement to the firm performance, especially with the negative impact of the COVID-19 pandemic. Besides, since the public and investors may be suspicious that the market has inadequate information, through the findings of this study, the public can raise their awareness of backdoor listing companies, while investors can observe how these companies perform in the Chinese market. Lastly, this research paper can support and serve as a reference for future research on the state of affairs of backdoor listing companies in the market. However, there are several limitations in this study as it only focuses on the contemporaneous firm performance after adopting the backdoor strategy. There is a lack of investigation into the changes before and after adopting the backdoor listing of both shell and backdoor companies which can be considered by future studies. Finally, this study did not focus on the reasons for successful factors of backdoor listing in different countries, future research may consider this in the future study.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data is available with the authors.