Abstract

Microfinance has gained significant importance in supporting the livelihoods of individuals in developing economies. This paper examines the influence of self-employment on preferences for microfinance, based on the hypothesis that self-employment choices and participation in microfinance share the same decision-making ability. The analysis utilizes data from a recent survey conducted in rural China, employing a generalized multinomial logit model (GMNL) to account for both preference heterogeneity and scale heterogeneity. This model allows us to investigate the choice probabilities and the impact of different types of self-employment on preferences for microfinance attributes. The empirical findings indicate that engaging in self-employment contributes to a sense of reassurance regarding preferences for microfinance among rural respondents. Specifically, non-agricultural self-employment has a positive effect on this preference, whereas agricultural self-employment has a negative effect.

Plain Language Summary

This article focuses on examining the impact of self-employment on preferences for microfinance, using data from a discrete choice experiment conducted in rural China. We present a conceptual framework that uses the generalized multinomial logit model, which effectively captures both preference heterogeneity and scale heterogeneity. This model allows us to analyze the choice probabilities and the impact of different types of self-employment on preferences for microfinance attributes. Our findings yield the following insights: self-employment and paid employment exhibit similar preferences for microfinance, but there are notable differences across various attributes. In particular, the preference for microfinance attributes is more pronounced among self-employed individuals compared to those in paid employment, and the preference for microfinance attributes is stronger among agricultural self-employed individuals compared to non-agricultural self-employed individuals.

Introduction

Self-employment, as a form of employment opposite to wage employment, has been an important engine for optimizing the allocation of labor resources and an important way to withstand employment pressures in economic development. This is especially true for a transitional economy like China, whose industrial structure is constantly adjusting and which has also been affected by the Covid-19 pandemic. As a result, a large number of migrant workers have either initiated or returned to rural areas. In 2020, more than 10.1 million people returned to rural areas to start businesses, an increase of 1.6 million over 2019 (The data is compiled from the State Council, the People’s Republic of China.). Self-employment in rural areas has become one of the main breakthroughs for promoting employment and revitalizing the rural economy. In order to encourage working people to start their own businesses, the Chinese government has introduced a series of policies, including innovative policy measures and financial services, to promote the high-quality development of self-employment. It is estimated that the number of self-employed individuals in rural China was 60 million in 2019, accounting for 19.87% of the total rural employment, more than double the 25.4 million in 2010 (6.13% of the total rural employment) (The data was compiled from the National Bureau of Statistics of China.).

Factors influencing the propensity to become self-employed are various, including personal attributes, characteristics of personal behavior, and institutional environment (Luo & Chong, 2019). Specifically, self-employment means that people change production factors such as industrial structure, business models, and production technology through investment behavior. In this investment behavior, finance plays a key role in boosting entry into self-employment (Dunn & Holtz-Eakin, 2000; Pham et al., 2018). However, an unavoidable challenge is that China’s economy has a dual urban-rural structure, and various factors of production are unevenly distributed. In particular, financial resources are concentrated in cities, and rural financial constraints are severe, making self-employed individuals face the bottleneck of financing difficulties. In order to promote rural households’ self-employment and alleviate loan difficulties, China has introduced a series of policy measures to increase credit supply, including fiscal discounts, financing guarantees, and expanding the scope of collateral, etc. aiming to enhance the distribution of financial resources to both crucial and underdeveloped aspects of rural development, while also effectively addressing the diverse financial requirements of rural households. With the rapid growth of self-employment and the continuous strengthening of rural financial supply, little is known about whether there are differences in the preferences of self-employed and non-self-employed individuals for microfinance, and how microfinance benefits rural self-employed.

Understanding the origins that influence the microfinance preferences of households is important because households are the decision-makers in pursuit of utility maximization, and a utility function is represented or summarized by preference order. Previous studies have suggested that the preferences of decision-makers strongly influence decision-making outcomes (Mishra et al., 2018), and institutions could respond to consumer preferences for improved quality (Khanal et al., 2020). Therefore, the aim of the present paper is to contribute to our understanding of microfinance preferences and offer insights into the impact of self-employment on such preferences.

The contribution of this study to the literature is threefold. First, we address an under fully researched topic: the impact of self-employment on microfinance preferences. Although some studies have examined the impact of microfinance on employment (Augsburg et al., 2015; Ćumurović & Hyll, 2019; Nitani et al., 2020), little is known about the extent to which self-employment influences preference for microfinance attributes. In addition, self-employment itself holds importance. The new agricultural operating entities, such as professional farmers, family farms, rural cooperatives and agricultural industrialized leading enterprises, play a crucial role in China’s rural economic development. As self-employed leaders of these entities, their financial needs require attention to ensure effective financial supply. Therefore, our focus in on employment within the rural labor market, distinguishing between self-employment and paid employment, and further categorizing agricultural employment and non-agricultural employment. The second contribution involves recognizing employment type as a latent variable that significantly impacts the total utility of rural households, influencing their decision-making regarding microfinance. We establish a conceptual framework grounded in McFadden’s Random Utility Theory and Bayesian inference. We present a parsimonious approach to control for the effect of decision-making ability on preference uncertainty, taking into account individuals as Bayesian learners. The third contribution of this study is the use of an experimental approach, enabling us to examine ex-ante microfinance products with hypothetical attribute combinations. This approach is novel in the research filed of employment and microfinance preference, particularly due to the limitations of cross-sectional studies.

In addition, only a limited number of studies have utilized theoretically and empirically plausible methods to examine the influence of various employment types on preferences for microfinance, and even fewer have considered the issue on rural households in China. China, as the largest developing country, had an estimated 40% of its total population living in rural areas in 2019 (The data was compiled from the China Statistical Yearbook 2020.). Rural microfinance is an important component of the financial system in China and has been strengthened for over 10 years. By the end of 2020, the balance of rural loans reached 32.27 trillion yuan and the balance of the rural household loan amounted to 11.81 trillion yuan. These figures represent a 270% and 370% increase, respectively, compared to the balance of rural loans of 9.8 trillion yuan and the balance of the rural household loan of 2.6 trillion yuan in 2010 (The data was compiled from the People’s Bank of China and Almanac of China’s Finance and Banking.). However, a major issue in microfinance, which is also significant in China, is the low participation rate. It is estimated that only 20% of rural borrowers borrowed money from financial institutions or used credit cards, while the majority still prefer informal financial sources (The data was compiled from the Global Findex Database 2017, the World Bank.). This indicates that their preferences do matter. In addition, as previously indicated, self-employment itself is important, particularly in the face of a downward economic environment, as the domestic economic cycle plays a leading role in boosting economic growth. Given the literature gap from these empirical analyses and the key challenges in the current situation, further research is needed to shed more light on this issue.

The rest of the paper is organized as follows: The next section presents the literature review. In section 3, we describe the data, measures, measures, and empirical methods employed. The empirical findings are then presented in section 4. Finally, the concluding section offers concluding remarks and implications.

Literature Review

Microfinance has gained significant importance in improving the livelihoods of people in developing economies. It serves as an essential element to stimulate the rural economy by providing rural households and micro-enterprises with more accessible cash flows and better market opportunities. Being a strategic financial service and a method of resource reallocation, microfinance has proven to be an effective approach in alleviating poverty and promoting welfare growth over the past decade. Several studies have supported the positive impacts of successful rural microfinance services on various aspects of rural livelihoods, including income, consumption, food security and quality of life (e.g., Agbola et al., 2017; Attanasio et al., 2015; Lahkar & Pingali, 2016). However, findings from other empirical analyses have indicated that microfinance schemes do not necessarily produce such positive effects. For example, Banerjee et al. (2018) found that neither business outcomes nor household consumption outcomes were affected by microfinance. Moreover, evidence from the studies on microfinance suggests that the impact of microfinance is unlikely to be homogenous across the entire population or among potential borrowers (Dahal & Fiala, 2020).

Although various programs and pilot schemes of microfinance are commendable, their impacts are mixed and inconclusive, largely contingent on the extent to which they are embraced by rural households. The decision-making process of households regarding microfinance participation is intricate, as it depends on their individual characteristics, including financial literacy, assets endowments, risk attitude and social networks (Berge et al., 2016; Warsame & Ireri, 2018). In addition, participation decisions are influenced by attributes associated with microfinance that govern their willingness to pay (Barboni, 2017; Ding & Abdulai, 2018). These factors and attributes, in return, reflect the performance of microfinance. Among them, employment type is presumed to be of particular significance but has not been fully considered.

First, the purpose of developing microfinance goes beyond the immediate provision of financial services to low-income individuals. As the saying goes, “Give a man a fish and you feed him a day; teach a man to fish and you feed him for a lifetime.” Access to finance can lead to a long-term increase in income by facilitating investments in income-generating activities and potentially diversifying sources of income (Hermes & Lensink, 2011). Therefore, it is more sustainable to enhance the employability of farmers, encompassing both wage-employment and self-employment opportunities. As Buera et al. (2021) pointed out that microfinance targeted toward small-scale entrepreneurial activities has become a pillar of economic development policies.

Second, just as the decision to participate in microfinance is a rational choice, the decision to become self-employed is also a product of individual rational decision-making. The factors that contribute to the growth of non-farm employment are likely interconnected with the factors that lead to variations in microfinance outcomes (Merfeld, 2020). Both decisions are influenced by utility-maximization functions that consider factors such as endowments, constraints, perceptions, attitudes, and preferences. Risk or risk attitude, for instance, plays a role in both decisions. Douglas and Shepherd (2000) argued that individuals tend to opt for self-employment when the anticipated overall utility derived from self-employment surpasses that of the alternative employment options available to them, incorporating factors like income and risk into a job utility function. Ahunov and Yusupov (2017), Brachert et al. (2020) confirmed a significant positive relationship between risk-taking propensity and the likelihood of being self-employed. Likewise, the number of microcredit borrowers depends on borrowers’ attitude toward risk (Thanh et al., 2019). Possner et al. (2021) found a noteworthy association between an individual’s risk attitude and their selection of a microfinance source. In particular, individuals with lower levels of risk aversion are inclined to choose riskier options, such as informal loans, which often come with higher costs. In addition, financial literacy is supposed to enhance credit availability and displace a positive effect on the probability of being self-employed (Ćumurović & Hyll, 2019; Grohmann et al., 2018). In other words, a significant barrier to self-employment is the acquisition of sufficient financial knowledge to guide financial practices (Nitani et al., 2020). This may result in households being unable to effectively employ capital (Blattman et al., 2014; Merfeld, 2020). However, there is a scarcity of research examining the influence of self-employment on households’ preferences for microfinance.

Third, the development of employment must be complementary to that of microfinance. The investment decisions made by individuals in developing countries are conditioned by their financial environment (Karlan et al., 2014). In a study conducted in Bangladesh, Imai and Azam (2012) have pointed out that microfinance helps in poverty reduction by promoting business activities and creating employment opportunities. In Ethiopia, Tarozzi et al. (2015) discovered that regions receiving microfinance interventions experienced a general rise in earnings derived from self-employment activities. Similarly, in Morocco, Crépon et al. (2015) and Dahal and Fiala (2020) found that individuals who accessed microcredit loans observed significant impacts on self-employment investments, sales and profits. Notably, improved access to collateral enabled individuals to initiate small businesses or pursue self-employment opportunities (Adelino et al., 2015). Moreover, various studies have indicated that self-employment and firm ownership are positively associated with availability of credit (Augsburg et al., 2015; Herkenhoff et al., 2021). Erhardt (2017) and Justo et al. (2021) emphasized the significantly positive impact of microfinance on job creation. On average, firms that participate in microfinance programs tend to have a higher number of employees compared to non-participating firms in matched comparisons. Therefore, analyzing the microfinance attributes preferred by these self-employers is worthwhile.

This study is based on the premise that individuals possess similar decision-making capabilities when it comes to selecting between self-employment and accessing microfinance. Despite considering standard observables, decision-making ability is an important factor that contributes to heterogeneity in outcomes. It captures individual differences in preferences, constraints, information, or beliefs that are not directly observed (Choi et al., 2014). Dohmen et al. (2010) pointed out that lower cognitive ability is associated with higher risk aversion and greater impatience. Agarwal and Mazumder (2013) found that cognitive ability is the most significant factor in financial decision-making and financial wealth. Although it is challenging to make definitive assess the quality of decision-making in specific choices or determine individuals with inferior decision-making ability, this latent ability is assumed also be functioning in maximizing the utility of employment choices.

To conclude, previous studies have highlighted the significance of self-employment and the preference for microfinance. However, no existing literature has investigated the impact of self-employment on microfinance preferences. This paper makes a valuable contribution to the existing literature by investigating the influence of employment type on rural households’ preferences for different aspects of microfinance. It utilizes a discrete choice experiment (DCE) dataset obtained from rural China to analyze this relationship. To capture both preference and scale heterogeneity, a generalized multinomial logit model is employed. This model enables the estimation of choice probabilities and the assessment of the impact of self-employment on preferences.

Data and Model Specification

Data

We draw links between self-employment and microfinance using a dataset from a field survey in rural China. The sampling process for identifying rural households commenced by selecting sample areas where microfinance is widely implemented and holds significant importance in the daily life of rural households. Sichuan, Chongqing and Guizhou provinces (with Chongqing being a province-level municipality) were then selected as appropriate study areas, considering their diverse agricultural practices and economic statuses. To be more specific, Sichuan, Chongqing and Guizhou provinces have a large rural population of 38.70, 10.37, 18.47 million accounting for 46.21%, 33.20%, and 50.98% of the total population, respectively. Their agricultural-related loan balances were 1,739, 579, and 1222 billion yuan in 2019 (The data was Complied form China Statistical Yearbook 2020 and Almanac of China’s Finance and Banking.).

To select representative regions and respondents, a multistage random sampling approach was employed. We firstly selected 12 regions from the provinces, taking into consideration the availability of participation in various microfinance sources. Then, a random selection process was employed to choose 40 households from each region, resulting in a total of 447 valid households sampled from 27 villages. Information was gathered through face-to-face interviews conducted between July and August 2020, including households’ characteristics and a discrete choice experiment. To facilitate the interview process, enumerators proficient in the local language were recruited to assist in conducting the interviews.

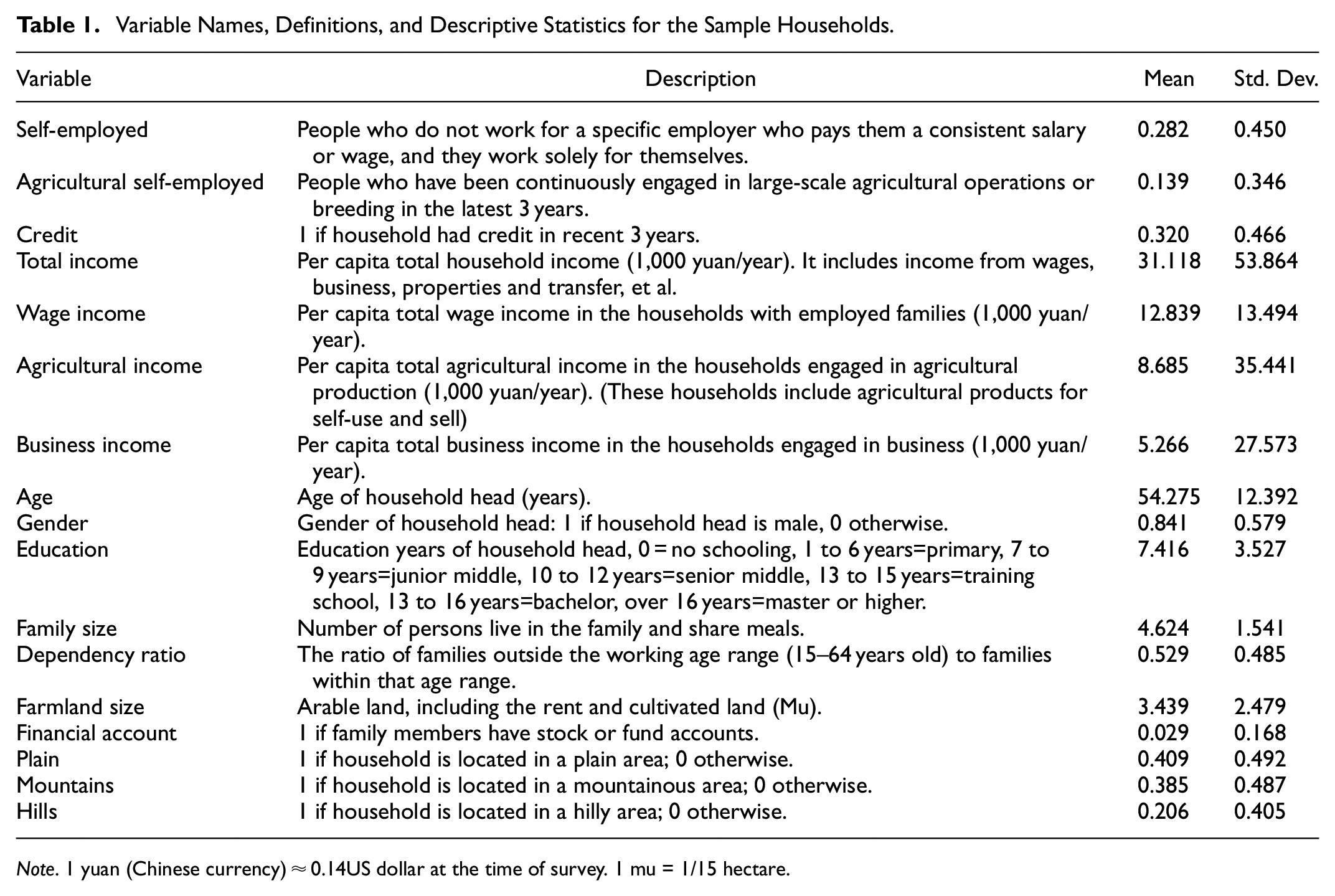

Table 1 presents the major characteristics of the sample households. The table reveals that out of the total sample, 126 respondents were self-employed, with 62 of them being agricultural self-employed, accounting for 28.2% and 13.9% of the sample, respectively. In this study, self-employed individuals refer to those who reported that they are not employed by a specific employer and instead work solely for themselves for the past 3 years. This includes those who have been continuously involved in industrial and commercial operations, as well as various types of large-scale farming and breeding. Agricultural self-employed individuals specifically refer to those who have continuously engaged in large-scale agricultural operations or breeding. The total income considered in this study comprises wage income, agricultural income, business income, and other income sources, such as pensions, subsidies, compensations. In addition, the majority (84%) of the sample household heads in the sample were male, with an average age of 54 years. The education of the household head is measured as the number of years of education, which is a continuous variable. According to the education system in China, in general, 1 to 6 years refer to primary school, 7 to 9 years refer to the junior middle, 10 to 12 years refer to the senior middle, 13 to 15 years refer to training school, 13 to 16 years refer to undergraduate and over 17 years refer to master or higher. The average household size was more than four persons, with a dependency ratio of approximately 0.5. The sampled households predominantly consisted of smallholders, with an average farmland size of 3.4 mu. Financial account reflects the level of financial participation, with an average of 2.9% of the sample households having stock or fund accounts. The topographic variables show that 41%, 38%, and 21% of the samples were located in plain, mountain and hilly regions, respectively.

Variable Names, Definitions, and Descriptive Statistics for the Sample Households.

Note. 1 yuan (Chinese currency)≈0.14US dollar at the time of survey. 1 mu = 1/15 hectare.

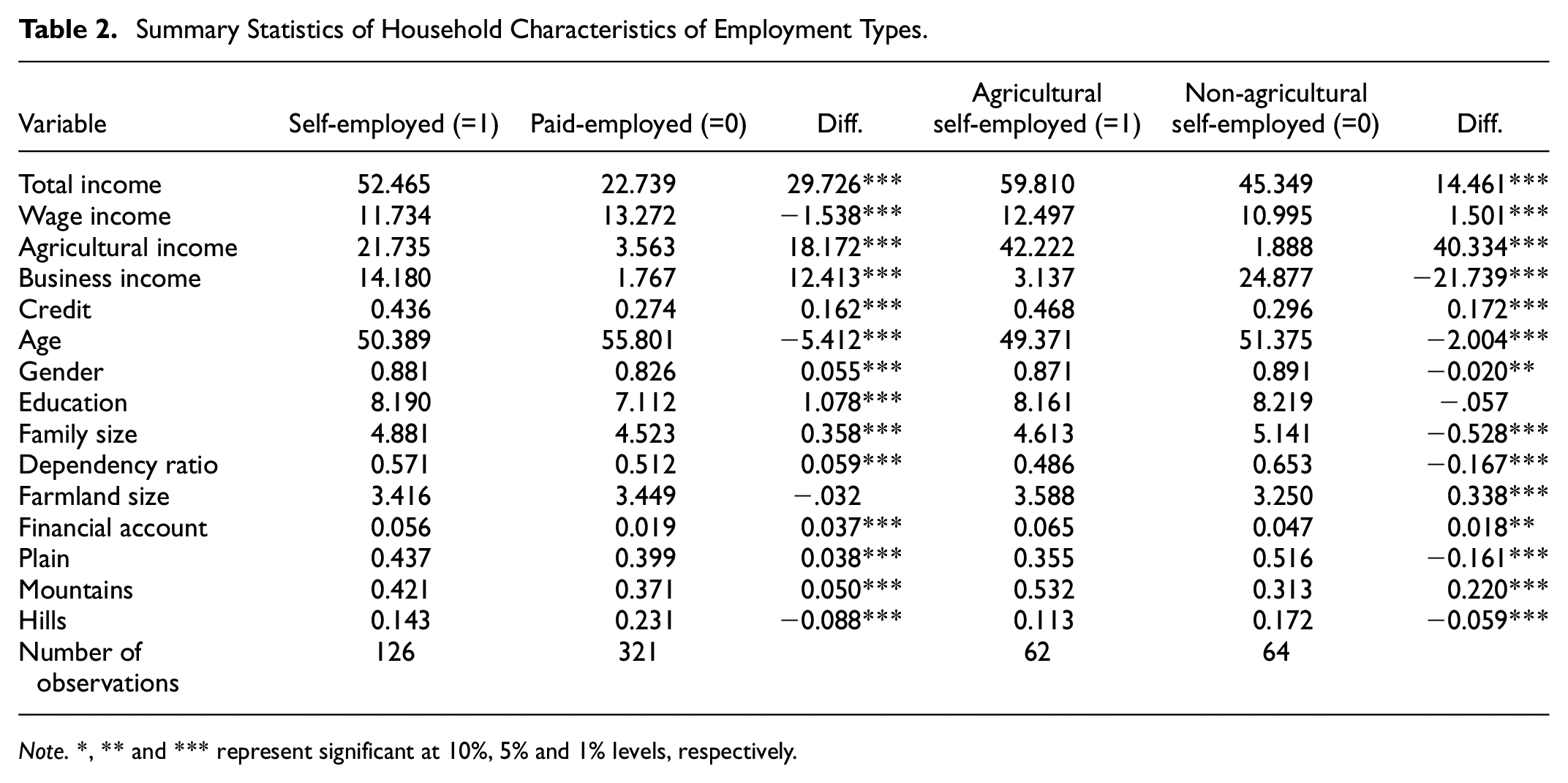

Table 2 presents the differences in household characteristics between self-employed and non-self-employed individuals, along with their corresponding t-values. The categorization of households into different employment types is based on their primary sources of income. The t-values suggest that there are notable differences in household characteristics between self-employed and wage-employed individuals, as well as between agricultural self-employed and non-agricultural self-employed individuals. The average total income for self-employed individuals was 29.726 higher than that of wage-employed individuals, and the average total income for agricultural self-employed individuals was 14.461 higher than that of non-agricultural self-employed individuals. In particular, the average agricultural income for agricultural self-employed was 40.334 higher than that of non-agricultural self-employed, and the average business income for non-agricultural self-employed was 21.739 higher than that of agricultural self-employed. These differences indicate that self-employed plays a significant role in increasing family income. Although the variable of credit shows that more self-employed and agricultural self-employed respondents had access to credit compared to their counterparts, these differences do not provide a clear indication of actual preferences between these groups. In addition, there appear to be significant differences between self-employed and paid-employed in age, gender, education, family size, dependency ratio and financial account. Similarly, differences between agricultural self-employed and non-agricultural self-employed individuals are observed in age, gender, family size, dependency ratio, farmland size, and financial account ownership. Nevertheless, the aforementioned comparisons are in sufficient to determine whether there are differences in the preferences for microfinance between self-employed and non-self-employed individuals. Therefore, the study utilizes a discrete choice experiment methodology to investigate choice probabilities and evaluate the influence of various employment types on preferences regarding microfinance attributes, and aims to develop strategies to address the diverse credit needs of the self-employed population.

Summary Statistics of Household Characteristics of Employment Types.

Note. *, ** and *** represent significant at 10%, 5% and 1% levels, respectively.

Discrete Choice Experiment

The discrete choice experiment is a valuable stated preference approach that allows for the examination of hypothetical choices. This methodology has been widely employed in many studies to explore the behavior aspects of microfinance (Bauer et al., 2012; Ding & Abdulai, 2018; Sagamba et al., 2013), where participants were invited to select their preferred combination of attributes from various options (Apostolakis et al., 2018). The primary objective of this choice experiment was to evaluate the responses of self-employed individuals toward different levels of microfinance attributes within the rural areas of China.

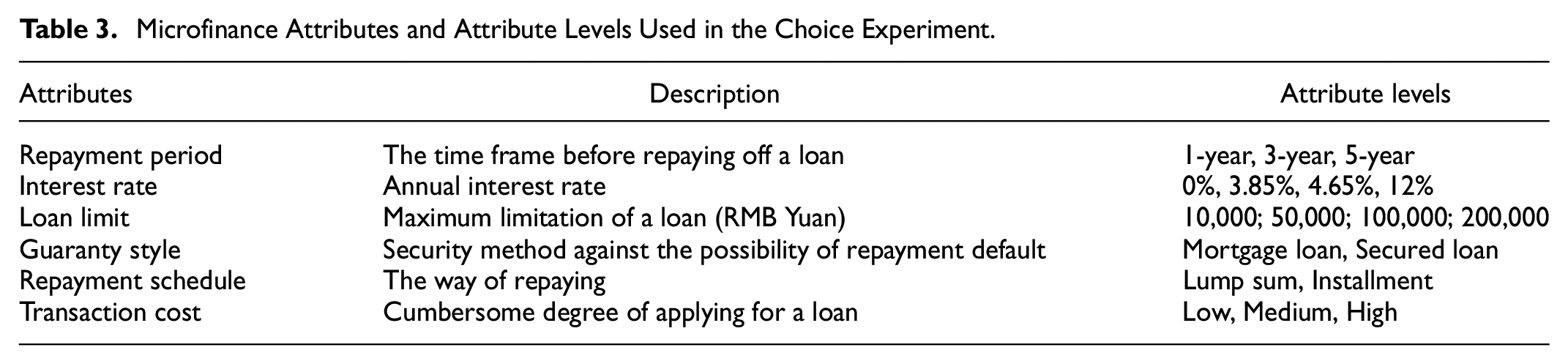

This specific group of respondents is expected to be significantly affected by microfinance since many of the attributes which the choice experiment focuses on are those linked to the costs of borrowing. The attributes we chosen for the choice experiment included six aspects of microfinance: repayment period, loan limit, guaranty style, repayment schedule, transaction costs and interest rate. These attributes represent terms are the key and noticeable components of microfinance loans and are known to influence customers’ preferences (Al-Azzam et al., 2012; Banerjee et al., 2015; Cerqueiro et al., 2016; Giné & Karlan, 2014). The levels assigned in the choice experiment were determined based on the existing microfinance products and the corresponding regulations. This ensured that respondents had the option to choose from existing alternatives or select a range from a small level to a large level for each aspect.

For example, the interest rate was assigned a level of 0% to account for governmental interest-free loans such as poverty alleviation microcredit and individual interest-free informal loans. The levels of 3.85% and 4.65% represented the 1-year and above-5-year LPR (Loan Prime Rate) set by the People’s Bank of China at the time of the survey. The highest interest rate level of 12% was selected, which is commonly quoted by microcredit companies. Guarantees were classified into mortgage loans and secured loans. A mortgage loan implies that the borrower must provide specific collateral as a guarantee for loan repayment when it is due. On the other hand, a secured loan is granted on the condition that someone provides a corresponding guarantee for the borrower. Transaction cost was used to indicate the ease or complexity of applying for a loan, ranging from the easiest (Low) to the most complex (High). These attributes and their respective levels were thoroughly discussed with rural households to ensure a common understanding of the descriptions. The attributes and levels used in this study are presented in Table 3 below.

Microfinance Attributes and Attribute Levels Used in the Choice Experiment.

The choice experiment was designed using efficient design principles to ensure optimal efficiency. In order to create manageable choice sets, a combination of D-optimal and blocked designs was implemented through JMP 10 (SAS), incorporating second interactions and powers. The efficient design resulted in 72 sets, which were further organized into three blocks of 24 sets each. Each set included an opt-out option. For further details on the total sets, please refer to the attached appendix. During the field experiment, each respondent was randomly assigned to only one of the blocks and presented with eight choice cards. Each choice card consisted of four alternatives, and respondents were asked to select their preferred option. Overall, the respondents provided responses for a total of 14,304 alternatives.

Econometric Model Specification

The conceptual framework employed in this study draws upon Lancaster’ model of consumer choice and random utility theory. In this framework, the utility experienced by individual

where

In the decision-making process, individuals are assumed to maximize their expected utility. The probability

where Y represents the alternative variable, which takes the value 1 when alternative

Following the approach proposed by Maddala (1983) and Train (2009), the logit model is derived by assuming that each

Mixed logit model (MIXL) is then normally employed to estimate the utility weight since it avoids the independence of irrelevant alternatives (IIA) assumption by allowing random preference variation for attributes. The utility weight

where

Despite the mentioned advantages of the mixed logit, it does not account for heterogeneous correlation in preferences across different attributes. To address this limitation, Fiebig et al. (2010) have introduced a generalized multinomial logit model (G-MNL), building upon the scaled multinomial logit model (S-MNL) proposed by Louviere et al. (2008). According to Fiebig et al. (2010), the G-MNL outperforms MIXL in terms of its ability to explain the behavior of extreme consumers with nearly lexicographic preferences and highly random consumers whose choices are relatively insensitive to attributes.

In addition, the G-MNL model not only incorporates preference heterogeneity but also captures scale heterogeneity. Scale heterogeneity is particularly pertinent in this study as it provides information that varies across households while remaining consistent across different choices. This aspect is crucial because the preferences of households, influenced by diverse employment types in this study, are expected to exhibit significant variation.

In G-MNL model, the utility that individual

where

In despite of these two specifications, the utility weight

where

In order to effectively capture the preferences associated with each attribute and personal characteristic, the natural normalization is to set

Then,

As a result, an increase in

Then, given

where

Empirical Results

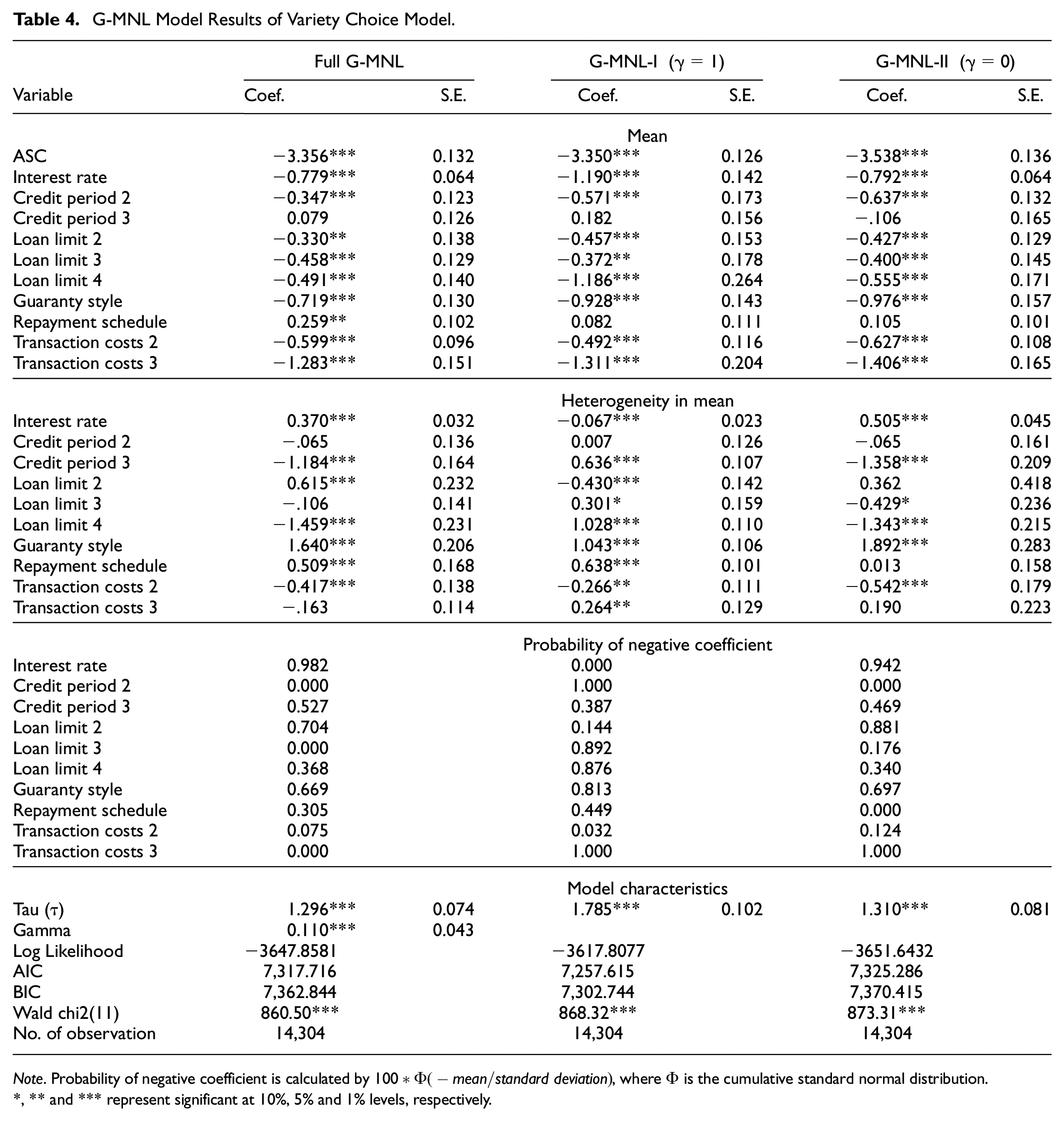

This section presents the estimates regarding the influence of self-employment on microfinance preferences. Dummy codes are utilized to represent each attribute, with the base levels set as follows: credit period 1 (1-year), loan limit 1 (10,000 yuan), transaction costs 1 (low), secured loan, and lump sum repayment.

The results, as presented in Table 4, indicate that different formulations of the G-MNL models yielded highly similar preferences for each attribute. In particular, the mean values of the taste parameters indicate that respondents tend to exhibit a preference for lower prices, longer credit periods, smaller credit sizes, lower transaction costs, secured loans, and installment repayment methods. Moreover, there were observed variations in taste parameters for credit period, loan limit, guaranty style, repayment schedule, and transaction cost, indicating the presence of unobserved heterogeneities among the respondents.

G-MNL Model Results of Variety Choice Model.

Note. Probability of negative coefficient is calculated by

*, ** and *** represent significant at 10%, 5% and 1% levels, respectively.

The goodness of fit for the model is evaluated using Akaike’s Information Criterion (AIC) and Bayesian Information Criterion (BIC). Based on the results presented in Table 4, it can be observed that the G-MNL-I model performs slightly better compared to the Full G-MNL and G-MNL-II models, despite the less precise coefficient estimates. Consequently, the subsequent discussion will focus on this specific specification, wherein the prior distribution of individual-level parameters is a mixture of normals with different means but equal variances. The scale parameter

Estimates of the G-MNL-I model in Table 4 indicate that long-term and small loans with mortgages are the attributes that have significantly negative effects on the choice of microfinance. To be more specific, the probability of negative coefficient in the G-MNL-I model indicate that all the rural households prefer less than a 3-year loan. The results also suggest that rural households prefer smaller credit sizes, as the loan limit of 50, 100, and 200 thousand yuan satisfy only roughly 14%, 11%, and 12% of them, respectively. Differences in guaranty style and repayment schedule reveal that more than 81% of respondents prefer secured loans, and more than 55% of them prefer installment repayment. Although lower transaction costs are generally preferred, over 3% of respondents are willing to accept higher transaction costs.

The estimates of microfinance attributes for different types of employment are presented in Table 5. The results of the G-MNL-I model are displayed, as it exhibits better performance in terms of AIC and BIC. The mean values in all specifications show that there are no apparent differences in preferences for microfinance attributes.

Heterogeneity in Mean Taste Parameters Models.

Note. *, ** and *** represent significant at 10%, 5% and 1% levels, respectively.

Looking at the scale-related parameters. The statically significant coefficients of the employment type indicate that the distinct employment statuses significantly influence individuals’ preferences for microfinance. In particular, the negative and significant coefficients of the self-employment, agricultural self-employment and paid employment in Table 4 indicate that individuals engaged in these types of employment are less likely to participate in microfinance. Conversely, the positive coefficient of non-agricultural self-employment indicates that this group of people are more likely to borrow funds from microfinance.

The coefficients of the scale parameter

An interesting observation is that the coefficient associated with agricultural self-employment is found to be significantly negative. This suggests that individuals engaged in agricultural self-employment are less inclined to participate in microfinance and exhibit a high level of confidence in their decision-making. On the other hand, the coefficient for non-agricultural self-employment is significantly positive, making it a unique case. Although the associated scale variance parameter

The sociodemographic variables used to control for the effects of self-employment indicate that participants in microfinance are more likely to be female and older household heads. It is noticeable that a higher educational level does not contribute to microfinance participation to some extent. This may be because individuals with higher education level typically have better employment opportunities and higher incomes. As a result, this group may rely more on self-accumulation or have access to traditional large commercial banks, reducing their demand for microfinance.

Conclusion

Many governments have implemented policies to promote self-employment as a means to stimulate economic growth. However, little is known about how to address the specific needs of the self-employed through financial product innovation. This article aims to investigate the influence of self-employment on preferences for microfinance, utilizing data obtained from a discrete choice experiment conducted in rural China. We introduce a conceptual framework based on the generalized multinomial logit model, which effectively incorporates both preference heterogeneity and scale heterogeneity. Through this model, we examine choice probabilities and assess the impact of various types of self-employment on preferences for microfinance attributes. Although the results demonstrated that the G-MNL-I model slightly outperforms the full G-MNL and G-MNL-II models, across all three specifications, there is a consistent preference among respondents for lower prices, longer credit periods, smaller credit sizes, lower transaction costs, secured loans, and installment repayment methods. The scale heterogeneity captured from the G-MNL model indicates that engaging in self-employment instills a sense of assurance among rural respondents regarding their preferences for microfinance.

Our findings yield the following insights: self-employment and paid employment exhibit similar preferences for microfinance, but there are notable differences across various attributes. In particular, the preference for microfinance attributes is more pronounced among self-employed individuals compared to those in paid employment, and the preference for microfinance attributes is stronger among agricultural self-employed individuals compared to non-agricultural self-employed individuals.

Accordingly, the findings of this study provide some policy implications for enhancing rural microfinance strategies. Firstly, recognizing that self-employed individuals constitute a significant driving force for rural economic development, financial institutions should develop microfinance products that align with their preferences. To cater to the preferences of respondents, it is recommended that these microfinance products incorporate longer repayment periods, smaller loan sizes, easy accessibility, a guarantor system, and installment repayment schedules. In addition, although the negative scale-related parameter of agricultural self-employment suggests a lower likelihood of microfinance engagement among this group, the mean coefficients indicate their sensitivity to microfinance attributes. For example, due to the vulnerability and higher risks associated with agriculture, they are less inclined toward loans with high interest rates and complex processes. However, this does not imply that they do not require microfinance. On the contrary, agricultural financial institutions should design products that are tailored to the specific needs of self-employed individuals in the agricultural sector. Secondly, in addition to addressing interest rates and simplifying procedures, attention should be given to the issue of guarantee methods. The government should strengthen the credit system to promote credit loans, enhance the risk-sharing mechanism, and expand the range of available guarantee systems. Thirdly, it is encouraged for self-employed individuals to integrate into the rural industrial ecosystem. Through value chain finance, they can leverage the contractual relationships among economic entities to establish a credit community. This can lead to reduced financing and transaction costs, as well as improved effectiveness of financial support.

The results reported in this paper are based on a discrete choice experiment, which has been extensively used to investigate hypothetical choices. As our primary objective is to explore the impact of self-employment on preferences, we did not delve into the issue of attribute non-attendance phenomenon. The study was unable to analyze the exact investment amounts made by self-employed individuals; instead, they were categorized based on types. It is highly probable that the various categories of self-employed individuals with different investment levels also influence financial preferences. We believe exploring these aspects would add intriguing refinements to the research.

Footnotes

Appendix

Probability of Negative Coefficient of the Results in Table 5.

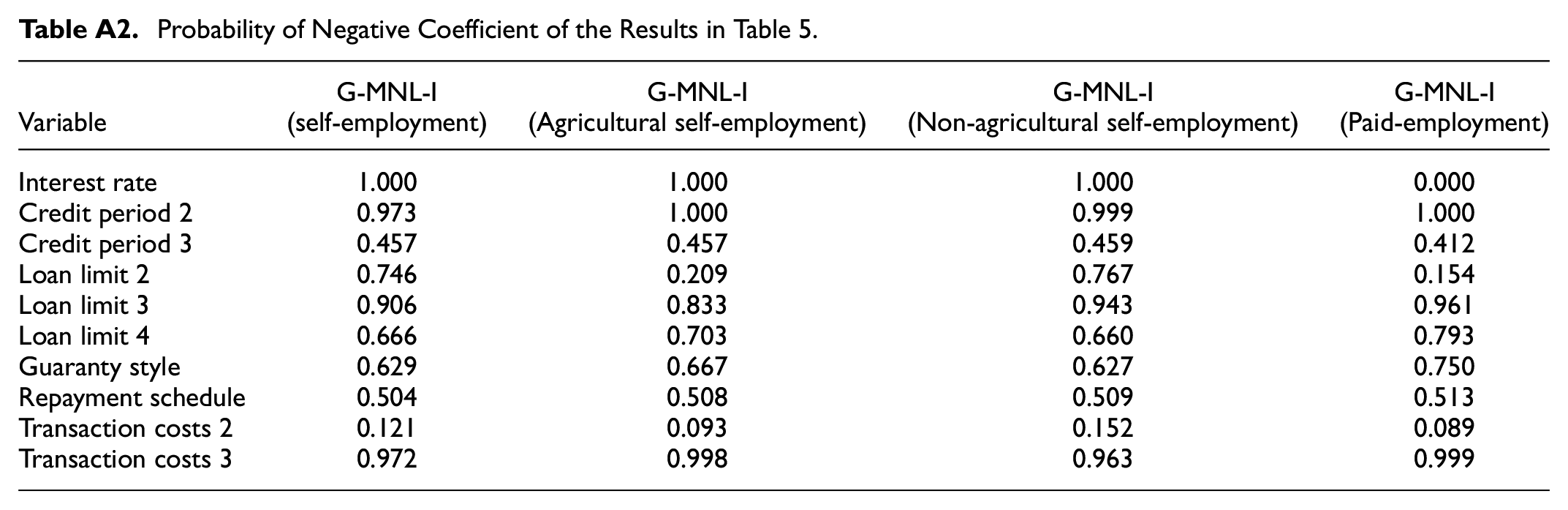

| Variable | G-MNL-I (self-employment) | G-MNL-I (Agricultural self-employment) | G-MNL-I (Non-agricultural self-employment) | G-MNL-I (Paid-employment) |

|---|---|---|---|---|

| Interest rate | 1.000 | 1.000 | 1.000 | 0.000 |

| Credit period 2 | 0.973 | 1.000 | 0.999 | 1.000 |

| Credit period 3 | 0.457 | 0.457 | 0.459 | 0.412 |

| Loan limit 2 | 0.746 | 0.209 | 0.767 | 0.154 |

| Loan limit 3 | 0.906 | 0.833 | 0.943 | 0.961 |

| Loan limit 4 | 0.666 | 0.703 | 0.660 | 0.793 |

| Guaranty style | 0.629 | 0.667 | 0.627 | 0.750 |

| Repayment schedule | 0.504 | 0.508 | 0.509 | 0.513 |

| Transaction costs 2 | 0.121 | 0.093 | 0.152 | 0.089 |

| Transaction costs 3 | 0.972 | 0.998 | 0.963 | 0.999 |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Supported by the Sichuan Province Science and Technology Support Program (2021JDR0305), and the National Social Science Fund of China (21CGL026).

Data Availability Statement

Data will be available on reasonable request