Abstract

This research aimed to provide a better understanding and analysis of consumer patterns relative to behavioral preferences in the Saudi cooperative motor insurance market. This aim was motivated by the fact that customers’ preferences have been underexplored in this market. Thus, this paper applied a multi-attributes decision analysis methodology to analyze the decision process of purchasing or retaining cooperative motor insurance based on a discrete choice experiment and a choice-based conjoint analysis. The methodology was conducted via a designed questionnaire that asked 385 customers in the Eastern Region to choose between a finite set of decision purchase options that varied along three key attributes: type of coverage, availability of discount, and insurance premium. Sample results showed that the most important attributes were the insurance premium, followed by the type of coverage. The availability of a discount was the least important attribute; however, compared with men, women placed a higher importance on coverage and discounts. The findings can be valuable to policymakers and managers of insurance companies in designing new characteristics for cooperative motor insurance products in Saudi Arabia in line with Saudi Arabia’s Vision 2030.

Plain language summary

This study aimed to enhance comprehension of consumer decision-making processes concerning cooperative motor insurance within the Saudi Arabian context, an area that has received limited investigation heretofore. Employing a multi-attribute decision analysis methodology, the research scrutinized the preferences influencing the purchase or retention of cooperative motor insurance, leveraging discrete choice experimentation and choice-based conjoint analysis. Through a structured questionnaire administered to 385 respondents in the Eastern Region, participants were tasked with selecting among predefined insurance options delineated by three pivotal attributes: coverage type, availability of discounts, and insurance premium. Results indicated that the foremost determinant of choice was the insurance premium, trailed by coverage type, while discount availability held lesser significance. Notably, gender discrepancies emerged, with female respondents attributing greater importance to both coverage and discount availability compared to their male counterparts. These findings hold considerable implications for policymakers and insurance industry stakeholders, furnishing insights conducive to the development of tailored cooperative motor insurance products aligning with the objectives outlined in Saudi Arabia’s Vision 2030 agenda.

Keywords

Introduction

The insurance sector contributes to the economy by supporting financial stability at national and sectoral levels; it mobilizes domestic savings, secures credit when borrowers default and supports international trade (Ansari, 2012; Arkell, 2011). The Islamic insurance sector (Takaful) emerged over the last three decades in Islamic countries and countries with clearly Muslim populations (Abdur Rehman et al., 2021; Alam et al., 2023; Hemrit, 2020). Takaful insurance is an alternative to conventional insurance; it must be compliant with Shariah principles, which include the prohibition of excessive doubt (gharar), gambling practices (maysir), and interest (riba; Abdur Rehman et al., 2021; Khan et al., 2020).

The Takaful market has the potential to become a significant player in the global insurance industry due to the expected population growth of Muslims, which was approximately 24% of the world population in 2017 (Khan et al., 2020). According to the Islamic Financial Services Board (2020), the contributions of the top five Takaful markets were as follows in 2018 (USD million): Iran (10,880), Saudi Arabia (9,463), Malaysia (1,856), United Arab Emirates (1,205) and Indonesia (1,057). In this regard, the Takaful markets continue to grow and become more competitive – particularly in Iran, Saudi Arabia, Pakistan and Malaysia, which are the largest Islamic insurance markets (Abdur Rehman et al., 2021; Hemrit, 2020; Mehboob Shaikh & Amin, 2024). Due to the growth of the Takaful insurance markets, customers can select from diverse Takaful products. Consequently, Takaful insurance markets have experienced the most growth of the Takaful products and services, particularly in Saudi Arabia. However, it is the least studied market. More work is needed to develop Takaful products that meet customers’ desires (Abdur Rehman et al., 2021; Saad et al., 2016).

The insurance industry has primarily been growing in the Kingdom of Saudi Arabia (KSA) because of rising demand due to high public and private sector outlays to achieve economic and social development in line with Saudi Arabia’s Vision 2030 (Akhtar, 2018; Almulhim, 2019). The Takaful sector in Saudi Arabia is a cooperative insurance model (Saudi Central Bank [SAMA], 2020). The cooperative insurance model is characterized by shared responsibility and cooperation, and it aims to promote welfare, solidarity and risk-sharing among all segments of society (Khan et al., 2020).

Royal Decree No. M/32 of 2003 basically enacted insurance law in the KSA. Regulations were implemented in 2004 that were entrusted to SAMA. Since then, the Saudi insurance market has become the largest Islamic insurance market in the Middle East and North Africa (MENA) region, with a gross written premium of USD 9.7 billion (Hemrit, 2020; Sallemi et al., 2021). The premium growth in the Saudi insurance market is also increasing, specifically in the motor and healthcare business lines (Hemrit, 2020, 2022; SAMA, 2020). In 2020, the combined motor and health insurance business lines constituted >80% of the total Saudi insurance market (SAMA, 2020). Consequently, they are considered to be the main drivers of the Saudi cooperative insurance industry. Nevertheless, the Saudi insurance market is in its early development stage, compared with other developing countries (Almulhim, 2019; Hemrit, 2020). Therefore, there is a need to improve insurance coverage schemes and product pricing, especially in the healthcare and motor insurance business lines, to ensure fulfilment of the sustainable economic and social development goals in Saudi Arabia’s Vision 2030.

Customers have a significantly important position for developing and improving policies and products in the insurance market (Ali & Rumzi Tausif, 2018; Liao et al., 2009). Therefore, exploration and understanding regarding customer behavior (e.g., satisfaction, participation, preferences) is needed in order to develop policies and improve certain characteristics of insurance products. Moreover, a better understanding of customer behavior could provide significant insights that insurers need in order to acquire and retain customers. In this context, very few prior works in empirical and analytical literature explore the Saudi cooperative insurance industry about this subject.

Researchers who have turned their attention toward understanding customer behavior in the cooperative insurance market have primarily focused on risk perception (Akhter & Hussain, 2012), customer knowledge and loyalty (Alawni et al., 2015; Saad et al., 2016), service characteristics and national culture (Alharbi, 2017), profitability of insurance companies and quality of service (Ali & Rumzi Tausif, 2018) and marketing and service quality dimensions (Abdur Rehman et al., 2021). However, studies about customer behavior concerning future insurance products that would incorporate new variables (such as discount and coverage attributes) to meet their changed motives and diverse preferences are still missing in the context of cooperative insurance. Hence, the proposed models fill the gap in the existing literature by revealing how attributes of insurance products influence customers’ decisions when they select insurance products and provide average predicted values that customers are willing to pay for cooperative insurance products based on certain characteristics.

For multiple reasons, the empirical focus of this study is to investigate and analyze customer behavior toward newly developed insurance products in the motor insurance business line. First, the motor insurance sector is likely to remain the main driver of Saudi cooperative insurance industry growth because this type of insurance has been mandatory for citizens and residents since 2001 (Alshammari et al., 2018; SAMA, 2020). Indeed, the increased premium growth and retention ratio is notable. For instance, motor insurance’s gross written premiums (GWP) accounted for 21.6% of the 2020 total GWP market with SR 8.36 billion in 2020 in underwritten premiums (SAMA, 2020). Furthermore, retention for motor insurance classes remained high, at 93% (SAMA, 2020). Secondly, women have been allowed to drive in Saudi Arabia since 2018 (Basaffar et al., 2018; Williams et al., 2019); Consequently, there is a new segment benefiting from motor insurance, and policymakers and insurers in this new segment need to monitor customer behavior to ensure optimal development or reformatting of motor insurance products. Third, the lack of empirical data regarding customers’ preferences for characteristics that customers desire needs to be available for motor insurance products in the Saudi market. Fourth, some insurers in the KSA might have massive expenses due to their smaller size and high underwriting losses (Akhtar, 2018). Those insurers might have limited resources to allocate to research activities that would cover customers’ needs, especially regarding motor insurance research, which should cover a large population. There is a need to carry out empirical grounds in the context of the cooperative insurance industry products in Saudi Arabia to increase decision makers’ knowledge and awareness about customers’ buying habits associated with risk mitigation trough the available motor insurance products. Therefore, a guideline for understanding motor insurance market customer behavior based on empirical research will be valuable for small-sized insurers.

In order to extend the understanding of customer behavior in the Saudi motor insurance sector, this research conducts an empirical study addressing the following objectives:

To inform marketing managers and decision-makers in the cooperative insurance industry about the most important insurance attributes for Saudi customers and to discover the most preferred and least preferred insurance product profiles from customer perspectives.

To measure customers’ marginal willingness to pay for various cooperative motor insurance products.

To highlight and offer valuable findings associated with the cooperative motor insurance industry in Saudi Arabia and other emerging cooperative insurance markets for policymakers, regulators and managers.

In accordance with the purpose of this research and in order to address the corresponding objectives, a multi-attribute decision analysis methodology is conducted based on a discrete choice experiment (DCE) and a choice-based conjoint analysis (CBCA). The DCE is a method that is used when the customer under investigation faces quantifiable alternatives. It is a stated preference method in the field of decision-making that uses a survey to analyze and investigate customer preferences and demand regarding product characteristics (Bansal et al., 2024; Cantillo et al., 2020; Sagebiel, 2017). It uses the design and analysis of experiments to characterize the relationships between product attributes and consumer preferences (Li et al., 2013). Moreover, the DCE is valuable for including new products or attributes that do not exist in the real market (Cantillo et al., 2020). The CBCA is an appropriate method to determine the customers’ choices from the rank order of the alternatives – it provides information about which alternatives and attributes exert the highest and the lowest amount of influence on the decisions of the participants (Na et al., 2023). Thus, it helps by sorting alternatives from the least to the most favorable option in customers’ point of view. The authors believe this is the first study to apply DCE and CBCA in the analysis and understanding of customers’ preferences for purchasing or retaining products in the cooperative motor insurance field, in general, and specifically in Saudi Arabia. The main idea behind DCE and CBCA is that each customer is given a hypothetical cooperative motor insurance product with various attributes, and they are asked to select one or none (opt-out) of the offered products. This examines and reveals how motor insurance product characteristics influence customers’ purchase decisions. Correspondingly, it examines how customers’ socioeconomic characteristics such as income, gender, age and marital status affect their purchase decisions.

The findings of this research have relevant contributions in terms of practical implications and theoretical perspectives. This research employs a multi-attribute methodology, namely the DCE and CBCA, based on the qualitative choice behaviors and judgments of the customers. Moreover, this study examines the customers’ behaviors regarding motor insurance products; it will inform insurers about customer preferences and requirements and highlight the characteristics that encourage their acquisition decisions. It will also provide recommendations, guidance and future aspects to the cooperative insurance industry in terms of individual characteristics that impact their selection of motor cooperative insurance products. Finally, this study will enable the marketing managers in Saudi cooperative insurance companies to make informed decisions that are supported by empirical evidence when offering insurance quotes to potential customers.

The study is organized as follows. Section 2 provides the background and related work. The methodology, study design and data are provided in Section 3. Section 4 presents data collection, results and findings. Implications of the research are provided in Section 5. Finally, Section 6 provides the conclusion, limitations, and future work.

Background and Related Work

Overview of the Saudi Motor Insurance Market

Motor insurance has been compulsory since 2001, based on Rule No. 222 issued by the Ministries Council (Alshammari et al., 2018). Based on SAMA regulations, the compulsory motor insurance policy (third-party insurance) covers damages caused to individuals and property by a driver of the insured’s vehicle for a premium paid by the insured (SAMA, 2019). An insured is a natural or juristic person who has entered into an insurance contract and whose name is stated in the policy schedule. This policy does not cover the damages to the driver of the insured’s vehicle or to his or her vehicle when driving. Conversely, comprehensive motor insurance policies cover both the insurance company’s liability for the insured’s car (the vehicle is covered against fire, theft and incidental accidents) and the insured’s liability toward a third party (property and individuals). According to SAMA’s insurance rules and regulations (2011), the third party is any natural or juristic person who sustains loss or damage covered under the provisions thereof, excluding the insured and/or the driver. In this case, the insurer should pay all of the charges to repair the insured’s vehicle, repairing and compensating for all of the damages to the third party that they caused and are responsible for. The comprehensive motor insurance policy can be expanded with an additional premium to cover renting a substitute vehicle for the insured while the damaged vehicle is being repaired, roadside aid service and repairing the damaged vehicle at the dealer or a local garage (SAMA, 2019).

By 2022, the Saudi insurance industry had 29 cooperative insurers and reinsurance companies licensed by the Central Bank of Saudi Arabia (SAMA, 2020). The companies operate in diversified insurance business lines; one is motor insurance. By reviewing the companies’ products for motor insurance, we concluded that there are three main products offered in the Saudi motor insurance market. They are the Third-Party Liability Motor Insurance Program, the Comprehensive Motor Insurance Program and the Comprehensive Third-Party Liability Motor Insurance Program with added coverage.

Review of the Related Literature

The earlier researches on the behavioral factors of the Takaful cooperative insurance market have been concentrated on Islamic countries: Gulf countries (e.g., Saudi Arabia, United Arab Emirates), Southeast Asia (e.g., Malaysia, Indonesia), South Asian (e.g., Pakistan) and the Middle East and North African (MENA) regions (Md Husin & Ab Rahman, 2013; Nasir et al., 2021). Many authors have begun exploring Takaful cooperative insurance attributes to understand consumer patterns relative to preferred products (Abdur Rehman et al., 2021; Akhter & Hussain, 2012; Alawni et al., 2015; Alharbi, 2017; Ali & Rumzi Tausif, 2018; Khan et al., 2020; Saad et al., 2016).

Customer perceptions were found as a literature stream within the works regarding the demand and purchasing of Takaful products. Akhter and Hussain (2012) studied Takaful standards and customer perceptions affecting Takaful practices. They conducted a survey on customer perceptions in Pakistan and concluded that the education level is an important factor that affects customer perceptions and levels of Takaful awareness. Similarly, other authors found that the customers’ education levels had significantly positive and long-run impacts on purchases of Takaful products in Malaysia (Gustina & Abdullah, 2012; Hawariyuni, 2006; Redzuan, 2011; Sherif & Azlina Shaairi, 2013) and Turkey (Ustaoğlu, 2015). Other socio-demographic variables for customers, such as gender and income, have important impacts on behavioral intentions to participate in Takaful purchases (Md Husin & Ab Rahman, 2013).

Another stream within this literature focused on customer loyalty and satisfaction and consumer patterns in relation to preferences of Takaful products. Shukor (2020) studied the knowledge and communication skills of Takaful agents in Malaysia and found that trust in the agents affected customer loyalty and intentions to continue service with the existing agents. Ali and Rumzi Tausif (2018) studied both the profitability of companies and the quality of service and attempted to relate it to customer satisfaction in the Saudi insurance market. They found that there is no definite relationship between service quality, customer satisfaction and profitability in the insurance sector of Saudi Arabia. Another study by Alawni et al. (2015) tested the association between communication, customer knowledge and customer loyalty in the Saudi insurance market. This study found that customer knowledge had a positive and significant effect on customer loyalty. Abdur Rehman et al. (2021) proposed a model based on a combination of the relationship marketing and the service quality dimensions to examine corporate image and customer loyalty through corporate reputation. They conducted their research via a survey-based study from Takaful customers in Saudi Arabia and Malaysia. Based on the research results, they recommended that Takaful operators from Malaysia and Saudi Arabia needed to put maximum effort on customer loyalty by bringing the dimensions of service quality and the relationship marketing in compliance with the principles of Islamic business transactions.

More reviews of Takaful literature have been conducted regarding consumer patterns in relation to behavioral preferences in demand and purchasing Takaful products; for instance, the studies by Md Husin and Ab Rahman (2013), Khan et al. (2020), Nasir et al. (2021) and Mehboob Shaikh and Amin (2024). However, studies on customer behavior regarding development of insurance products that incorporate new variables such as discount and coverage attributes to meet their changed motives and diverse preferences are still missing in the context of Takaful insurance. In other words, there is a lack of research that includes products, alternatives or attributes that do not exist in the current Takaful products. Moreover, there is no previous study that examines and understands the issue about the entry of a new benefit segment of customers into the motor insurance market. This is the case in the Saudi cooperative insurance market due to the sudden entry of women into the market. Therefore, our study fills the gap in the existing literature by providing an insightful framework to understand customers’ behavior patterns concerning hypothetical Takaful products in the Saudi motor insurance market. This aim is achieved with a multi-attributes decision analysis methodology based on integrated DCE and CBCA.

Methodology and Study Design

In accordance with the purpose of this study, a multi-attributes decision analysis methodology based on integrating a DCE and a CBCA was utilized. The DCE is also recognized as a stated preference survey; it is a decision-making method of understanding consumer demands for products where it is not possible to use revealed preference data on the real selections made by individual customers. It is a proper method for eliciting customers’ preferences and expected selection behaviors that has recently been widely used in insurance (Akaichi et al., 2020; Bannor et al., 2023; He et al., 2021; Wang et al., 2021). The main advantage of the DCE is that a hypothetical new product can be characterized by multi-characteristics that do not exist in the real market – normally denoted as ‘multi-attributes’– and consumers can assess the overall desirability of the product based on these multi-attributes (Bansal et al., 2024; Cantillo et al., 2020; He et al., 2021). Thus, the DCE was utilized in this study to measure and understand the pattern of preferences of customer purchasing for hypothetical cooperative motor insurance products in the Saudi insurance market.

The CBCA was the other method that was adopted in the multi-attributes decision analysis methodology. There are numerous methodologies within the stated approach, such as conjoint techniques that collect consumer preferences for identification of a best- and worst-case scenario and ranking alternatives (Arning et al., 2021; Chen et al., 2024; Lebeau et al., 2012). Among the conjoint techniques, the CBCA is considered to be more realistic, and it provides a better predicted accuracy, particularly in market simulations (Lebeau et al., 2012). Compared with other conjoint techniques, the CBCA allows a holistic examination of decision purchase scenarios where multi-attributes are weighed against each other (Arning et al., 2021). Furthermore, choice-based tasks are easy for participants to understand and are less time consuming than more traditional forms of conjoint analysis – for example, ranking profiles (Wallner et al., 2022). Consequently, the CBCA was employed in the methodology for the following purposes: (1) to infer the customer’s choice from the rank order of the alternatives as specified by the customer, and (2) to calculate customers’ preferences for the purpose of measuring the importance of attributes in the selection of cooperative motor insurance products.

In order to apply the multi-attributes decision analysis methodology, the collected data must be cross-sectional to elicit consumers’ preferences and choices on motor insurance products. Thus, a survey design via online platform was chosen to serve the purpose of the study for the following reasons. First, data from design surveys are often the core inputs to performing DCE (Cantillo et al., 2020; Mariel et al., 2021) and CBCA (Arning et al., 2021). Second, the method is also used to collect information to describe, compare and explain the behavior of the study respondents. Third, the method has advantages related to the speed and cost of data collection, in addition to data quality (Heiervang & Goodman, 2011).

Discrete Choice Experiment

The DCE is a commonly stated preference statistical technique theoretically grounded on random utility theory and Lancaster’s theory, which is the basis of several models and theories of decision-making in psychology and economics (Lancaster, 1966; McFadden, 1973; Thurstone, 1927; Uncles et al., 1987). It has become an integral tool for researchers and policymakers to understand and model patterns in customers’ choices between pairs of hypothetical products and services (alternatives), and it can be described using a set of tangible and intangible characteristics (attributes) (Mariel et al., 2021). Thus, the DCE assumes that any product or service is defined as a combination of di levels of multiple attributes that can be both quantitative and qualitative (Cantillo et al., 2020; Mariel et al., 2021). Furthermore, the DCE is valuable because it allows for the inclusion of new products, alternatives or attributes that do not exist in the real market, and for which there is no data available (Cantillo et al., 2020). It builds upon the design of the experiment, including the identification of key attributes and the specification of their levels, the design of the survey for collection of proper data and the model to predict the probability that any alternative is selected from a set of alternatives.

This research methodology considers that

The utility given by equation 1 can be divided into two components: the first component is the observable or systematic component (

Since

where a choice set in this paper consists of two insurance products with varying attribute levels and an opt-out option.

Choice-Based Conjoint Analysis

The traditional conjoint analysis is an empirical quantitative research method that integrates psychological measurement theory with a statistical estimation process (Green & Rao, 1971; Green & Srinivasan, 1990). In 1983, Louviere and Woodworth extended conjoint analysis to choose evaluations and multinomial logit analysis. It enables the examination of variations in the likelihood of individual purchases and the determination of trade-offs. The CBCA tasks are similar to DCE in that the participants/customers are asked via a survey to choose the most preferred set of choice configurations, which consist of different choice parameter ‘attributes’ and parameter characteristics (attribute levels). Compared with other surveys, the CBCA allows a holistic examination of decision purchase scenarios where several attributes are weighed against each other (Arning et al., 2021). Moreover, the CBCA’s preference patterns allow for the identification of a best- and worst-case scenario (Arning et al., 2021). In this research analysis, the CLM was applied to calculate the likelihood of choice based on respondents’ choices, and then choice decisions were decomposed into the relative importance of attributes together with separate utilities of all attribute levels. In this regard, this analysis offers information about which attributes can affect the purchase decisions of the customers the most or the least.

Study Design

The required data for this type of research is primary data collected through a designed survey. The survey was designed via SurveyKing, which is the perfect platform for market research and customer satisfaction. Informed consent was obtained from all subjects before the study. Researchers informed all participants why the research was being conducted and anonymity was assured; this was included in the introduction of the designed survey.

The survey consisted of two parts. Whilst the first part was a general socioeconomic questionnaire, the second part was a DCE and CBCA questionnaire. The second part of the survey offered alternatives of cooperative motor insurance products and new characteristics (attributes) for the existing motor insurance products in the Saudi market.

The identification and selection of attributes and levels is the most important step in the empirical research design of the DCE and CBCA analyses. In the survey design, each respondent was given two hypothetical alternatives and an opt-out choice. Each alternative consisted of three attributes: type of coverage, availability of discount and insurance premium. Furthermore, each of these attributes had three levels, as shown in Table 1.

Number of Attributes and Levels for the Saudi Cooperative Motor Insurance (Source: authors’ design).

For the study addressed here, the three attributes were selected based on literature review and Saudi motor insurance market analysis. The first attribute was the type of motor insurance coverage, which is considered a significant characteristic for purchasing a cooperative motor insurance product (Akhter & Khan, 2017; Hemrit, 2022). Motor insurance coverage means the coverage under the policy shall include loss or damage to the insured motor vehicle and third-party civil liability (SAMA, 2020). Three levels of this attribute were identified based on the available coverage and information from SAMA and Saudi motor insurance companies’ websites. The second attribute in this study was the availability of a discount. From previous studies and from analyzing the cooperative insurance markets, some new characteristics were observed, such as no accident record, loyalty, age and level of education (Abdur Rehman et al., 2021; Ab Rahman et al., 2008; Akhter & Hussain, 2012; Bhatti, 2018; SAMA, 2020; Shukor, 2020). Thus, the levels of the second attribute were identified: no discount, no accident record, loyalty discount, age and level of education, as shown in Table 1. In this study, new attribute levels that are not available in the existing Saudi cooperative motor insurance products were considered, such as age, level of education, no accident record and loyalty discount. Eventually, the insurance premium was selected to be the third attribute. Previous research on insurance proved that lower premium rates make the insurance products more attractive to customers (Alharbi, 2017; Hemrit, 2020). The premium (or contribution) is defined as the amount paid by the insured to the insurer in exchange for the insurer’s acceptance to indemnify the insured for loss/damages resulting directly from a covered risk (SAMA, 2019). In this study, the premium attribute was associated with three levels. The premium levels were determined and calculated based on the range of potential insurance premiums in the Saudi market, as illustrated in Table 1.

The choice sets in this study were designed using the mix-and-match method (Enneking, 2004; Orme, 2010). Thus, respondents to the survey questions were given nine choice sets that contained the three attributes and random combinations of their levels. Table 2 shows an example of the choice preference question.

Example of DCE Questions (Source: Authors’ Design) Which of the Following Insurance Products Would You Select?.

Since DCA calculates the preferences for each single respondent, no large sample is required for the results to be valid (de Bekker-Grob et al., 2015; Kuzmanović & Vukić, 2021). There are several techniques to calculate the sample size for the DCA. This study adopted the rule of thumb for an acceptable sample size proposed by Orme (2010) i.e., given by

Data Collection and Analysis of Results

This section discusses data collection and implements the DCE and CBCA analyses, the findings of which are also presented.

Data Collection

The data collection was a fundamental phase to conduct the experiment and the DCE and CBCA analyses. The survey was distributed randomly to consumers living in the Eastern Province of Saudi Arabia via various distribution techniques, such as social media, email and by directly asking customers in cooperative insurance firms’ offices to complete the survey. After incomplete and unreliable responses were removed, the total number of observations was 385. Table 3 illustrates the summary of the statistics of the customers’ socioeconomic characteristics.

Summary of Socioeconomic Variables (Source: Authors’ Calculations).

Women are considered as new customers in the Saudi motor insurance sector, and their representation in the sample of this study was of high importance. Indeed, 68% of the respondents were men and 32% were women. We noted that almost half of the respondents were married. Most respondents lived in a city, held a bachelor’s degree, owned a Japanese car and parked their vehicles in the street. Furthermore, 53.51% of the respondents purchased their cars through cash payment, 27.27% through personal loans and 19.22% through auto-leasing. The average respondent’s age was 31, and the average monthly income was SAR 9,031.

CBCA Results

The conjoint utilities were estimated using R software via the ChoiceModelR package (Sermas & Colias, 2014). The results of the CBCA (the relative importance scores of attributes and utilities of all attribute levels) are reported in Table 4.

Conjoint Utilities (Source: Authors’ Calculations).

It was noted that the survey respondents placed the highest importance on insurance premium rates. Indeed, customers exhibited the largest utility when the premium amounts were SAR 900. Furthermore, SAR 2,200 gave customers more utility compared to SAR 3,800. Coverage type was the second most important attribute for customers, followed by discount. Comprehensive coverage gave customers the greatest utility compared to other coverage types. Moreover, discounts that were given to customers due to their loyalty to an insurance company or the customers’ accident-free record gave customers more utility, compared with other types of discounts.

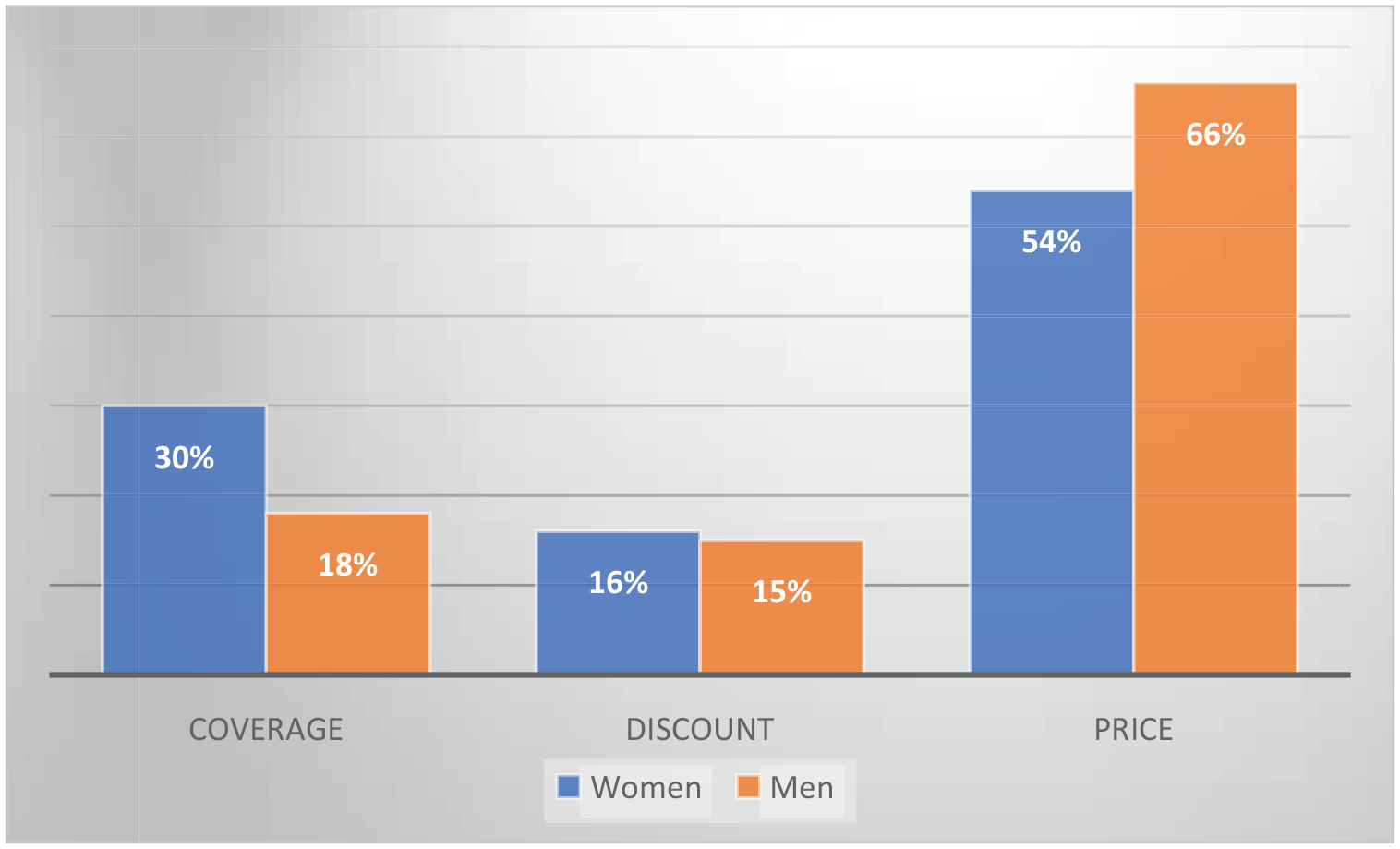

Figures 1 and 2 show the attribute importance and levels of utilities according to respondents’ gender. This result is very informative, since women are new entrants into the Saudi auto insurance sector. Thus, it is critical to compare which attributes men and women place importance on and their utilities.

Attribute importance according to sex of respondents.

Utilities according to sex of respondents.

Women placed greater importance on coverage than men. This was expected, since the women were new drivers, and the collision risk was higher. Women and men were almost in agreement on the importance placed on a discount. Nonetheless, men placed greater importance on the price than women.

Figure 2 shows that the only level where women obtained higher utility than men was with the comprehensive coverage, confirming the fact that women were concerned with collision risks resulting from being unexperienced drivers.

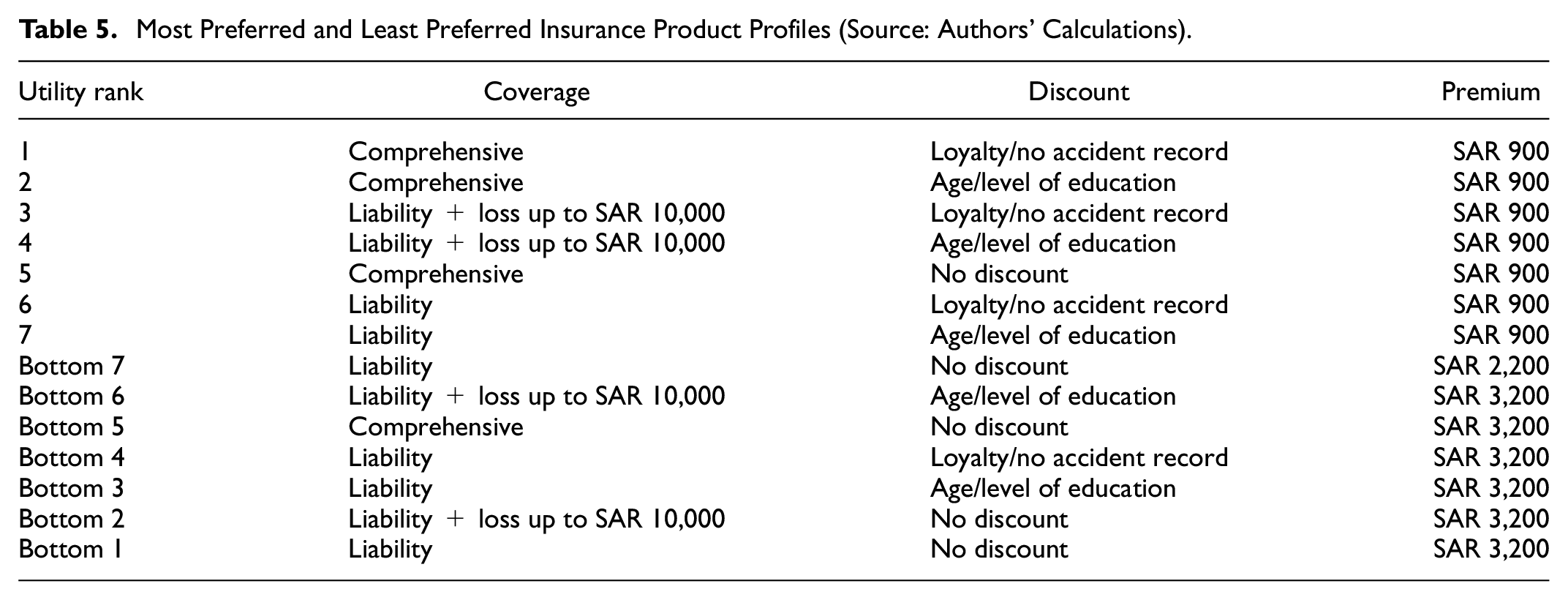

The most and least preferred insurance product profiles are reported in Table 5. This information should give decision-makers in the cooperative auto-insurance industry in Saudi Arabia an abstract overview so they can tailor informed decisions when designing their insurance products for Saudi customers.

Most Preferred and Least Preferred Insurance Product Profiles (Source: Authors’ Calculations).

The top seven insurance products’ profiles that gave customers the highest utility had a common factor of the SAR 900 premium rate. Comprehensive insurance was ranked first and second, respectively, if it included a discount for loyalty/no accident record or age/level of education. Liability + compensation up to SAR 10,000 was ranked third and fourth if the customers were given the same discounts as with the comprehensive insurance. Moreover, liability-only insurance was ranked sixth and seventh if its premium was SAR 900 and included a discount on the premium.

On the other hand, insurance liability products with no discount and a premium of SAR 2,200 were ranked seventh in terms of customers’ utility. The other lowest insurance product, regardless of coverage or discounts, was linked with a price premium of SAR 3,200. The results confirmed that insurance customers selected insurance policies that gave them the greatest utility in terms of the premiums, coverage and discount availability. The results showed that the greatest utility in the respondents’ points of view was obtained through an insurance policy that gave them the lowest possible premium, the highest possible coverage and any type of discount on their premium.

DCE Results

We estimated CLM (2) using R software. Since women are considered new entrants into the Saudi cooperative motor insurance sector, two were run models. The first model was the original model with no interaction term, and the second model included women’s interaction terms with liability and comprehensive insurance. Table 6 shows the obtained results of the two models.

Estimated Parameters for the Discrete Choice Model (Source: Authors’ Calculations).

Note: ***, **, and * indicate significance levels at 1%, 5%, and 10%, respectively. Figures in round brackets () are standard error, and figures in square brackets [ ] are odds ratio.

Both models showed that we rejected the null hypothesis of the likelihood ratio test that all coefficients were equal to 0 at the 1% level. The results in the first model showed that customers valued liability plus loss coverage up to SAR 10,000 more than the liability-only insurance coverage. However, the coefficient was not significant in the second model. In addition, the comprehensive insurance’s coefficient was significant in both models, indicating that customers were more likely to select comprehensive insurance coverage than the liability plus loss up to SAR 10,000 coverage. Furthermore, customers valued insurance products that gave them a discount on their premium for either age or level of education more than insurance products with no discount. The price coefficient in both models was negative, indicating that customers in Saudi Arabia preferred cheaper insurance products. The odds ratio in the second model showed that women, compared with men, had 36% higher odds of purchasing comprehensive insurance compared to liability plus loss up to SAR 10,000. In addition, women, compared with men, were indifferent about liability-only insurance versus liability with loss coverage up to SAR 10,000.

Table 7 shows customers’ marginal willingness to pay (MWP) to upgrade their insurance products. Explicitly, MWP reveals how much more cooperative insurance customers would be willing to pay (on average in Saudi Riyal) to upgrade from liability insurance to other insurance policies with more coverage, such as liability plus loss up to SAR 10,000 or comprehensive coverage. The MWP in DCE studies is used to assign a monetary value for nonmonetary attributes.

Customers’ Marginal Willingness to Pay for Insurance Products (Source: Authors’ Calculations).

The results show that the average insurance customer was willing to pay SAR 321 to upgrade their insurance from liability to liability plus coverage up to SAR 10,000. Furthermore, the average customer was willing to pay SAR 652 for comprehensive insurance compared to liability plus coverage up to SAR 10,000. In addition, model (2) shows that women, compared with men, were willing to pay, on average, SAR 824 more to obtain comprehensive coverage rather than liability plus coverage up to SAR 10,000.

Implications of the Research

Theoretical Implications

For theoretical implications, this research provides a new insight of analysis to explore how research performed in the cooperative motor insurance market may inform researchers and decision-makers about how customers make selection decisions. The proposed multi-attribute decision analysis methodology offers insurance decision-makers novel insights into the prioritized factors relevant to individuals presently seeking cooperative motor insurance products or anticipated to do so in the future. Integration of this fresh perspective with additional insights from diverse angles within the insurance industry endows discerning decision-makers with hitherto undiscovered, practical knowledge, thereby enhancing motor insurance outcomes and contributing to enhancements in various facets of quality of life. In addition, this research methodology assists in explaining how choice modelers in the cooperative motor insurance market may contribute to a better understanding of customer choice behavior by using preference statistical techniques.

Managerial/Practical Implications

With respect to the practical implications, this research provides several plausible findings that could be valuable for policymakers and managers in the Saudi cooperative motor insurance industry. Therefore, the significant research results are recapped to be helpful in consideration of reforming and developing the cooperative motor insurance industry. Saudi consumers sampled in this study were strongly willing to purchase or retain cooperative motor insurance products with insurance premium rate attributes, followed by the type of covering attribute and the availability of the discount attribute. In terms of the insurance premium rate attribute, this research found that the willingness to purchase or retain cooperative motor insurance products depended on the amount of money to be paid, which was between SAR 900 and a maximum of SAR 2,200. Regarding the type of coverage and the availability of discount attributes, the comprehensive coverage type and the discount based on either age/level of education or loyalty/no accident record contributed positively to the decision process during purchase and retention of cooperative motor insurance products. The previous findings support the fact that the best choice for Saudi consumers sampled in this study is a cooperative motor insurance product with comprehensive coverage, the SAR 900 premium and the loyalty/no accident record discount. The worst choice is a product with a liability coverage type, the SAR 3,200 premium and no discount. Interestingly, further analysis indicates that Saudi customers are willing to pay, on average, SAR 321 to upgrade their motor coverage insurance from liability to liability plus coverage up to SAR 10,000, and they will pay SAR 652 to get comprehensive coverage insurance instead of liability plus coverage up to SAR 10,000.

Since the women are the most recent segment benefit from motor insurance in Saudi Arabia, the analysis in this study focused on investigating their preferences in purchasing a motor insurance product. The study reveals that the women, compared with men, have 36% higher odds of purchasing comprehensive insurance products than the other products in the market. Moreover, the results show that women place greater importance on coverage than men. Indeed, women obtained greater utilities from comprehensive insurance, compared with men, proving their unwillingness to take any collision risks resulting from being new drivers.

The results of this research should be useful to policymakers of cooperative insurance for redesigning their portfolios and raising the diversification benefits. The newly designed products should have diversity in insurance coverage with advantages given according to educational levels, age or gender. This could be done by offering a comprehensive product with a discount for customers with doctoral degrees, for example, which does not exist in the market. Moreover, offering new products requires action to be taken. For instance, for portfolio managers, it is important to recalculate premiums with actuarial research in proportion to the preference of customers that vary with time.

Regulatory authority should monitor the competition and market analysis. In other words, it should check whether the cooperative insurance companies are constantly conducting market research analyses to keep pace with changing customer preferences. Moreover, it should continue with legislative analysis and the development of regulations to align with the inclusion of new features in motor cooperative insurance products.

Conclusion, Limitations, and Future Work

In this study, a multi-attribute decision analysis based on DCE and CBCA was utilized in the context of customer choice behavior in the Saudi cooperative motor insurance market. The present analysis explores the association between the relative importance of different attributes and their different levels, in general, and similarly by gender, in a sample of 385 customers, covering a range of the Eastern Region in the KSA. Eventually, it reveals customers’ marginal willingness to pay.

The current multi-criteria decision analysis results significantly contribute to new understanding for policymakers and managers about which attributes affect the preferences of customers when purchasing or retaining motor insurance. Additionally, the present results add to cooperative motor insurance literature and consumer choice behavior by adding new insights.

In this study, there are some limitations that can be improved by future research. First, the choice questionnaire was applied to a limited number of respondents; it considered one region in Saudi Arabia. In addition, the attributes in the choice set were three attributes obtained from previous studies. Thus, academicians could extend future research with a larger sample study and consider more attributes in the choice decision process. Second, this study did not address the issue of uncertainties associated with customer choice behavior. This would be an interesting task to undertake in future research by employing a fuzzy set theory to tackle the uncertainty in customer decision judgment. Third, the present study investigated the customer preference model based on gender. Thus, future work can be examined with the segmentation preference model based on customers’ different socioeconomic characteristics. Eventually, the research methodology can be readily applied in future research domines to investigate customers’ priorities.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper was funded by the Saudi Central Bank. The funder played no role in topic selection, study design, and study results.

Ethical Statement

The survey in this paper was approved by the ethical committee at King Faisal University, and it was assigned the following reference number: KFU-REC-2021-NOV-EA000201.

Data Availability Statement

All the data used in this study are available from the authors upon request.