Abstract

Even though audit committee (AC) characteristics and corporate social responsibility (CSR) relationship has long been well investigated, scarce research on committee leadership is observed in the literature. Considering the growing emphasis on the potential role of the audit committee chair (ACC) on financial and non-financial reporting, the current study aims to fill this literature gap by analyzing the influence of ACC characteristics on the level of CSR. Using a Jordanian sample of 475 firm-year observations over the period 2014 to 2018, this study employs content analysis to quantify CSR disclosure and ordinary least squares (OLS) regression to test the proposed hypotheses. The study findings show that ACC independence, legal expertise, and education level are positively and significantly associated with CSR reporting. However, ACC age has a significant inverse relationship with CSR reporting, suggesting that older ACC perform more poorly in a committee function. Importantly, ACC tenure and financial expertise have an insignificant relationship with CSR reporting. These findings are robust under a battery of sensitive tests such as employing OLS with robust standard errors and using alternative measurements of ACC features. The sub-sample analysis results also show that ACC characteristics predominantly enhance CSR reporting in large firms but not in small firms, implying that firm size strengthens the relationship between ACC characteristics and CSR reporting. The current study provides new evidence of the significant role of ACC on non-financial reporting in an emerging economy, Jordan. Policymakers, researchers, and stakeholders may benefit from these results in recognizing the potential role of ACC in advancing CSR reporting.

Keywords

Introduction

The relationships between corporate social responsibility (CSR) and corporate governance (CG) have been widely investigated in recent decades. Today, corporations work in a multifaceted environment, deal with diverse stakeholders, and are increasingly required to be more responsible to society and the environment (Arif et al., 2021). Thus, CSR activities and CG systems have become an essential component of firms’ strategy to reduce management conflicts with these stakeholders. Consequently, CSR practices have become a part of the board function (including audit committee) to align management concerns with stakeholders. Accordingly, researchers are reporting CSR activities are associated with greater dividend payments (Badru & Qasem, 2021), favorable stock recommendations (Wan-Hussin, Qasem, Aripin, & Ariffin, 2021), higher financial performance (Akben-Selcuk, 2019; Nour et al., 2021), higher customer loyalty and satisfaction (Galbreath & Shum, 2012; Ibrahim & Hanefah, 2016), low cost of equity capital (El Ghoul et al., 2011), low earnings management (Ghaleb, Qaderi, Almashaqbeh, & Qasem, 2021; Kim et al., 2012), corporate credibility and legitimacy (Garcia et al., 2020), and enhancing a firm’s reputation (Valls Martinez et al., 2019). These findings show that involvement in CSR activities reflects good health for firms. However, Galant and Cadez (2017) reported that the relationship between CSR and firm financial performance is equivocal, as several studies also have reported negative impact of CSR.

Even though several empirical studies have examined the impact of CG mechanisms (e.g., audit committee [AC]) on CSR reporting, these studies mainly focus on the AC features rather than on leadership. For example, Appuhami and Tashakor (2017) provide evidence that AC size, gender diversity, independence, and meetings are highly and significantly associated with the CSR disclosure level in the Australian market. However, independent ACC and AC members’ financial expertise do not affect CSR reporting. Further, Qaderi et al. (2020) report that independent AC and AC ownership have a significant association with higher CSR discourse in Jordan.

Indeed, the AC effectiveness depends significantly on the chair’s skills and dedication (Bromilow & Keller, 2011). An audit committee chair (ACC) with deep knowledge, expertise, and skills is necessary for maintaining the control and monitoring functions of an influential AC. The ACC is the formal head of the firm’s committee, responsible for ensuring the reporting quality and AC effectiveness (Chaudhry et al., 2020; Dwekat et al., 2020; Ghaleb, Al-Duais, & Hashed, 2021; Tanyi & Smith, 2015). The ACC has the power to set and manage the agenda for AC meetings, and to build a good relationship with AC members, management, and external auditors (Abernathy et al., 2014; Ghaleb, Al-Duais, & Hashed, 2021), thus providing additional insight into sustainable performance and reducing agency problems and agency costs (Chaudhry et al., 2020). Regarding non-financial reporting, researchers assert that the position of the ACC can play an essential role in increasing the transparency in firms’ reported CSR information (Appuhami & Tashakor, 2017; Dwekat et al., 2020). Indeed, the ACC has a great responsibility in monitoring both financial and non-financial reporting. He/she is mainly responsible for failures in corporate reporting (Bromilow & Keller, 2011; Schmidt & Wilkins, 2013). Thus, the current study proposes that competent ACCs can lead AC members, encouraging them to monitor the financial and non-financial reporting process effectively.

Previous studies have emphasized the importance of ACC independence leadership and accounting expertise in driving AC effectiveness (Khemakhem & Fontaine, 2019; Tanyi & Smith, 2015). Importantly, ACCs with well-developed leadership features beyond financial expertise and independence will be an advantage in securing high AC quality. This is because these other features, such as educational level, legal expertise, age, and tenure, are more useful in monitoring the more complicated transactions and providing the information required by the firms’ stakeholders. Recent empirical research has explored the effect of the ACC on different aspects of accounting, such as financial reporting quality (Abernathy et al., 2014; Bajra & Čadež, 2018; Tanyi & Smith, 2015); firm’s financial performance (Chaudhry et al., 2020); earnings quality (Ghaleb, Al-Duais, & Hashed, 2021; Jalan et al., 2020); audit report lag (Al-Qublani et al., 2020; Ghafran & Yasmin, 2018); and internal audit practice (Wan-Hussin, Fitri, & Salim, 2021), the relationship between the ACC’s characteristics and CSR practices has not yet been investigated in prior studies but is worth exploring here, since ACC play a vital role in leading and guiding the committee to improve CSR practice more effectively. Therefore, this study bridges the research gap by examining the relationship between ACC leadership attributes (independence, educational level, legal expertise, age, financial expertise, and tenure) and the CSR disclosure level.

Jordan is a suitable environment for conducting this research for various reasons. First, CSR activities and CG rules have received attention from regulatory bodies such as the Jordan Securities Commission (JSC). For example, the JSC introduced the Jordanian Corporate Governance Code (JCGC) in 2009, which recommends that listed firms provide information about their social activities (i.e., policy in preserving the environment, awarding grants to human resources, serving the community and charitable involvement) (Abu Qa’dan & Suwaidan, 2019). Second, related to CG, JCGC 2009 recommended that the board members of listed firms establish ACs consisting of three non-executive directors; at least two should be independent directors. Third, JCGC 2009 emphasized that all members of the AC should have accounting and financial literacy, at least one having accounting and audit qualification or financial expertise (JSC, 2009). Unlike many countries that emphasis the role of the ACC, regulators in Jordan have yet to mention any requirements related to this post. Thus, outcomes from this study may benefit regulators in Jordan and similar developing countries on improvements to CG rules.

The study uses a sample of 95 non-financial listed Jordanian firms (475 firm-year observations) over a 5-year period from 2014 to 2018. The results show that an independent ACC, the education level, and legal expertise are significantly associated with a higher CSR disclosure level. However, ACC tenure and financial knowledge have no impact on CSR reporting. Furthermore, a younger ACC produces richer information on CSR than an older ACC. A battery of sensitivity tests, such as applying OLS regression with robust standard errors and using alternative measurement of ACC features, lead to the same conclusions. Notably, the study finds that ACCs in large firms are more effective than in small ones, suggesting that firm size significantly enhances the negative relationship between ACC characteristics and CSR reporting.

This study contributes to the literature on CG and CSR in the following ways. We add further evidence to the limited research in CSR reporting among developing markets (mainly in Jordan), supporting the claim that CSR reporting in these markets is still at a low level compared with developed markets. Our study fills an important literature gap by investigating the impact of AC leadership on CSR disclosure; to the best of our knowledge, this study is among the first to address this neglected area. Thus, our results are consistent with the notion that the ACC is a substantial contributor to AC success in driving the quality of financial and non-financial reporting. Our study also contributes to the governance research by presenting new perceptions into the effect of firm size on the ACC’s role. The outcomes of the current study have implications for firms’ management, shareholders, regulators, and other stakeholders in an emerging economy (in this case, Jordan) about the urgency of ACC features in improving the level of CSR reporting.

The remainder of this paper is arranged as follows: Next section presents the literature review and the hypotheses development, which is followed by section ‘Research Design.” Sections “Results and Discussion” and “Additional Robustness Checks” discuss the main empirical results and further robustness analysis, and finally, Section “Conclusions” presents the study’s conclusion and directions for future research.

Literature Review and Hypotheses Development

Theoretical Background

CSR disclosure is a contemporary topic of debate in the accounting literature (Velte, 2019). Various theories are applied in addressing the relationship between internal governance monitoring tools and CSR disclosure, but stakeholder and agency theories are the most commonly used. Stakeholder theory is principally based on the idea of an implicit social contract between stakeholders and firms (Freeman, 1984). Nevertheless, firms face greater pressure from various stakeholder groups (e.g., customers, environmental lobbyists, investors, and employees) to disclose CSR information (Cadez et al., 2019; Fernandez-Feijoo et al., 2014), thus improving the transparency of CSR activities. This means that managers are required to reduce the conflicts with shareholders, leading to the need to broaden the disclosure of non-financial information. Therefore, CSR’s objective is to meet all the stakeholders’ information needs (Alazzani et al., 2019). Stakeholder theory is frequently applied in the CSR reporting literature (Fahad & Rahman, 2020; Garcia et al., 2020). Fernandez-Feijoo et al. (2014) suggest that CSR initiatives help firms reduce stakeholder pressure as they connect all the information ranging from firm strategy to performance. Valls Martinez et al. (2019) and Matuszak et al. (2019) stress that the stakeholder theory proposes that internal CG mechanisms improve CSR disclosure.

Agency theory explains the existence of agency problems in principal–agent relationships (Jensen & Meckling, 1976). An agency conflict occurs when the goals of the shareholders differ from managers due to the presence of managerial opportunistic behavior and information asymmetry problems (Jensen & Meckling, 1976; Speziale, 2019). It posits that the AC plays the main role in monitoring and oversight of top management to align their interests with shareholders and minimize agency problems and costs (Fama & Jensen, 1983; Jensen & Meckling, 1976) by engaging in more socially responsible activities, thus mitigating information asymmetry problems (Appuhami & Tashakor, 2017). The agency theory perspective is the most prominent in investigating the impact of Inside CG on CSR reporting (Katmon et al., 2019; Mohammadi et al., 2021; Qaderi et al., 2020; Setiany et al., 2017). Zaid et al. (2019) assume that CG has a monitoring role over agency problems, reducing information asymmetry, enhancing the disclosure quality, and making a firm more transparent. Therefore, the current study adopts these two theories to develop the following hypothesis pertaining to investigate how ACC attributes affect CSR reporting.

Hypothesis Development

The chair is the formal head of the firm’s audit committee, responsible for ensuring the AC’s effectiveness and reporting quality (Chaudhry et al., 2020; Tanyi & Smith, 2015). The ACC has the authority to set and manage the agenda for the meeting and build a good relationship with AC members, management, and external auditors (Bédard & Gendron, 2010). Dwekat et al. (2020) assert that the ACC can play an essential role in advancing the CSR reporting level. Thus, this study fills the research gap by investigating the effect of ACC attributes (independence, educational level, legal expertise, age, financial expertise, and tenure) on CSR reporting.

AC chair independence and CSR disclosure

AC independence is one of the CG mechanisms frequently identified in the CSR voluntary disclosure literature (Arif et al., 2021; Mohammadi et al., 2021). Buallay and Al-Ajmi (2020) believe that the independence of the AC can affect its effectiveness in monitoring management and overcoming agency conflicts, increasing CSR voluntary disclosure. In addition, an independent ACC has a greater capacity to perform the committee’s duties and functions in an improved manner (Appuhami & Tashakor, 2017; Dwekat et al., 2020). Accordingly, JCGC 2017 states that the AC members should be independent (JSC, 2009). From agency theory, Dwekat et al. (2020) claim that a greater level of AC independence can determine the implementation of sustainable strategic decisions about socially responsible activities and can thus influence CSR disclosure.

Several studies conducted around the world have investigated the impact of AC independence on CSR disclosure level. Researchers provide evidence that an AC consisting of independent members promotes the CSR disclosure level (Arif et al., 2021; Fallah & Mojarrad, 2019; Mohammadi et al., 2021). Qaderi et al. (2020) provide evidence from the Jordanian market that independent AC members improve the CSR disclosure level. However, other empirical studies by Musallam (2018) show that AC independence has no impact on CSR disclosure.

Studies examining ACC independence are rare. For example, Dwekat et al. (2020) provide evidence that an independent AC engages more in social responsibility activities in the European context, suggesting that the ACC’s independence is the most significant factor affecting the committee’s effectiveness on the monitoring function. Nevertheless, Appuhami and Tashakor (2017) find no direct relationship between an independent ACC and voluntary CSR disclosure in Australian firms. Based on the agency theory and the mixed empirical result, this study predicts that the levels of CSR disclosure are higher for firms with a greater ACC independence. Thus, the following research hypothesis is proposed:

AC chair educational level and CSR disclosure

One criterion for assessing board members’ ability is educational level (Khan, Khan, & Saeed, 2019); educational level diversity may play a crucial role in improving the board’s performance, including increasing managerial monitoring, providing different perspectives of supervision, and hence enhancing the CSR disclosure quality (Elmagrhi et al., 2019; Katmon et al., 2019). Based on agency theory, a board with more educated directors affects firms’ sustainable behavior (García Martín & Herrero, 2020), which could strengthen the firm’s reputation by enhancing CSR disclosure.

Empirically, studies have discussed the impact of board educational level on non-financial reporting such as CSR disclosure. For instance, Harjoto et al. (2019) find a significant association between board educational level and firms social performance in the US market, suggesting that directors with a high educational level may use their expertise to make effective decisions related to CSR disclosure. Likewise, Katmon et al. (2019) used 200 Malaysian listed firms for the period 2009 to 2013 to examine the board diversity-CSR disclosure quality nexus. They reported a significant positive effect, suggesting that directors with high education levels may be more efficient in making decisions related to firm performance and non-financial disclosure. Conversely, Elmagrhi et al. (2019); Hassan et al. (2020) and Khan, Khan and Senturk (2019) find no relationship between board educational level and CSR information disclosure. However, all these studies have ignored the effect of the ACC’s educational level on CSR disclosure. Based on the agency theory and limited literature, this study consequently assumes that at higher levels of education, the role of ACC will be more effective in improving CSR issues. Thus, the following research hypothesis is formulated:

AC chair age and CSR disclosure

Directors’ age is perceived as one of the important features of a firm’s human capital (Katmon et al., 2019). It plays a vital role in strategic leadership by enhancing knowledge and creativity and generating competitiveness in board value creation (Åberg & Shen, 2020). From the agency theory perspective, diversity in the age of directors improves monitoring quality. This may be because older directors often have more experience and knowledge in dealing with social and ethical issues (Katmon et al., 2019). Elmagrhi et al. (2019) argue that older directors with greater experience and knowledge are more inclined to divulge information on non-financial issues, more willing to increase transparency and reduce information asymmetry.

The literature on the directors’ age-CSR practices relationship is limited. For example, Ibrahim and Hanefah (2016) show that young directors have a higher tendency to disclose CSR information. Elmagrhi et al. (2019) report a significant association among older female directors and the information disclosed within environmental reporting. On the other hand, Katmon et al. (2019) and Khan, Khan, and Senturk (2019) demonstrate that higher board age lowers the quality of CSR disclosure, which might result from weak governance. In contrast, some studies conducted by Cucari et al. (2018) and Giannarakis (2014) find that firms with older directors are insignificantly associated with the CSR information disclosure level. Building on the agency theory and considering the scarcity of empirical evidence, the present study expects that ACCs age influence higher CSR disclosure practices. The following research hypothesis is thus posited:

AC chair legal expertise and CSR disclosure

ACCs with legal expertise may play a significant role in monitoring and enhancing the financial reporting quality (Ghaleb, Al-Duais, & Hashed, 2021; Krishnan et al., 2011), as they can understand legal liability to counter the risk of litigation. Furthermore, de Villiers et al. (2011) argue that the lawyers on the board have better analytical skills to evaluate opportunities in the environment and be fully aware of the impacts of environmental decisions on stakeholders. Limited empirical studies have examined the role of the directors’ legal expertise in reporting quality. For instance, Krishnan et al. (2011) indicate that board legal experts are perceived as essential for firms with legal risk concerns. Alhababsah and Yekini (2021) expect that firms with more AC members with legal expertise to be knowledgeable about the legal liability implications resulting from the misrepresentation of financial statements. However, Ghaleb, Al-Duais and Hashed (2021) find that an ACC with legal expertise is correlated with higher real earnings management practices. They justified this result by the nature of real earnings management, which makes it less detectable, more related to discretionary decisions, and may be considered as a normal business activity. Dharwadkar et al. (2021) demonstrate that a director with legal expertise is likely to reduce corporate socially irresponsible activities related to the perceptions of investors and firms’ outcomes (such as the quality of financial reporting, market valuation, performance of analyst forecast, financial risk, and tax avoidance). Importantly, Bozanic et al. (2019) confirm that legal experts may improve the quality of disclosures, which in turn strengthens the CG system.

Some of the previous studies address the role of board legal expertise in non-financial reporting. For example, de Villiers et al. (2011) find that directors with legal expertise improve environmental performance, suggesting that legal expertise on the board is considered as an additional resource for fostering sound environmental policy (Kassinis & Vafeas, 2002). However, no empirical study addresses the direct relationship between the ACC’s legal expertise and CSR disclosure. Therefore, this study anticipates that ACCs who possess a legal background and expertise are more likely to improve non-financial performance and thus increase the firms’ CSR disclosure information. Thus, the following research hypothesis is posited:

AC chair financial expertise and CSR disclosure

AC members’ financial expertise is one of the important factors influencing CSR disclosure, and numerous scholars have used it as a proxy for the AC’s competencies (Raimo et al., 2020; Setiany et al., 2017). Chaudhry et al. (2020) assert that ACCs with financial expertise are more efficient in improving reporting quality and decreasing agency problems. JCGC 2009 in Jordan emphasizes accounting and financial literacy of all AC members or that at least one has an accounting and audit qualification or financial expertise (JSC, 2009). Agency theory postulates that an AC with financial expertise is more efficient in performing its monitoring role, ultimately promoting the dissemination of more information in CSR reporting (Dwekat et al., 2020; Musallam, 2018).

Several empirical studies have examined the impact of AC financial expertise on CSR disclosure, with inconclusive results. Studies conducted by Dwekat et al. (2020) and Mohammadi et al. (2021) show that financial experts on the AC could enhance CSR disclosure. They suggest that an AC with financial expertise performs with more capacity and confidence when providing external information to stakeholders. Another study conducted by (Chan et al., 2021) indicates that AC members’ financial expertise improv CSR information disclosure. On the other hand, Musallam (2018) provides evidence that firms with AC financial expertise are less likely to report socially responsible activities. However, Appuhami and Tashakor (2017) and Qaderi et al. (2020) reveal that the AC’s financial expertise does not influence CSR information disclosure. Based on agency theory and contradictory findings, the current study predicts that an ACC with financial expertise affects higher CSR disclosure. Hence, the following research hypothesis is posited:

AC chair tenure and CSR disclosure

Tenure is another essential indicator of voluntary disclosure (Othman et al., 2014). Researchers use it as a proxy for various values, such as duration of service (Åberg & Shen, 2020), expert dimension (Velte, 2020), and director’s reputation (Bouaziz et al., 2020). AC members with longer tenure are more likely to perform an influential monitoring role as they are expected to monitor management decisions, thus increasing voluntary ethics disclosure (Othman et al., 2014). Khan, Khan, and Saeed (2019) indicate that directors’ tenure improves creative activities, and monitoring skills, resulting in efficient decisions on the CSR disclosure quality. According to agency theory, long-tenured AC members become closer with the board, more familiar with the firm’s management strategy and less efficient in monitoring them (Hafsi & Turgut, 2013; Vafeas, 2003), which increases the agency problem and decreases disclosure.

Although previous studies have researched the bond between AC tenure and voluntary disclosure (Bravo & Reguera-Alvarado, 2019; Setiany et al., 2017), evidence for the effect of ACC tenure on CSR disclosure is non-existent in either developed or developing countries, so further investigation is needed. Othman et al. (2014) show that a longer AC tenure is related to greater voluntary information disclosure. Other empirical evidence from Setiany et al. (2017) concludes that AC members with longer tenure tend to produce more voluntary disclosure. However, Bravo and Reguera-Alvarado (2019) fail to find a correlation between the AC members’ tenure and the quality of the information disclosed within ESG reporting. In light of the agency theory argument and given the lack of empirical studies, this study expects that ACCs with long tenure will lead to decreased CSR disclosure . Hence, the following research hypothesis is proposed:

Research Design

Sample and Data

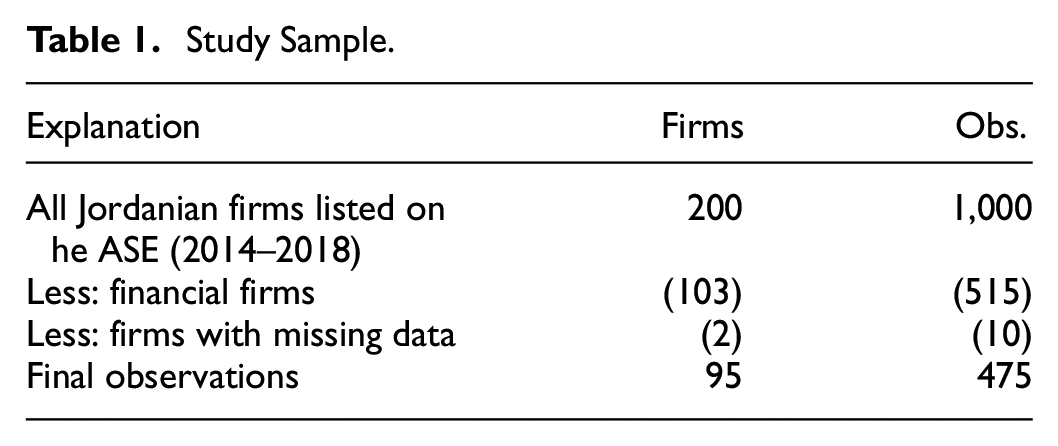

The sample in this study consists of non-financial Jordanian listed firms during 2014 to 2018. Financial firms are excluded (e.g., banks, diversified financial services, and insurance) due to the specific regulations of CG and the financial reporting structure (Al Fadli et al., 2020). Their different capital structure compared to the non-financial firms make them incompatible to be included in our sample. As presented in Table 1, the final sample includes 95 firms (475 firm-year observations). Regarding the information about the names of AC members, data were obtained from the Amman Stock Exchange website under disclosures categories (board of directors & ownership, and general assembly meetings & decisions). After determining the names of AC members, data on ACCs were manually collected by analyzing the 1,490 AC members’ biographies from the selected firms during the study period. These biographies were collected from the firms’ annual reports. Finally, CSR and financial data were extracted from firms’ annual reports and the Securities Depository Centre of Jordan.

Study Sample.

Measurement of CSR Disclosure

CSR disclosure level (CSRDL) is measured by the CSR index using content analysis. In line with the prior literature (Haniffa & Cooke, 2005; Qaderi et al., 2020), the disclosure index of CSR was adopted to determine the score of the CSR disclosure level. In addition, this study uses the unweighted scoring method (binary approach) as it is more appropriate, reduces the subjectivity problem, and suggests that each disclosure item is equally relevant (Chau & Gray, 2002; Cooke, 1989). Under the CSR index, the four types of activity (environmental activities, products/services to customers, community involvement, and human resources) are reported by 42 items. Following prior studies, a binary approach was used such that a firm is scored “1” if a CSR item is disclosed and “0” otherwise (Abu Qa’dan & Suwaidan, 2019; Qaderi et al., 2020). Consequently, the CSR disclosure level is obtained by dividing the sum of the actual number of items disclosed by the maximum possible CSR score for the firm (42 items).

Measurements for ACC Characteristics and Control Variables

ACC characteristics are the independent variables of the current research, namely: ACC independence (ACCIND); ACC educational level (ACCEDU); ACC age (ACCAGE); ACC legal expertise (ACCLEG); ACC financial expertise (ACCFEXP); and ACC tenure (ACCTEN). ACCIND is measured as a binary variable that equals “1” if the ACC is independent and “0” otherwise (Appuhami & Tashakor, 2017; Dwekat et al., 2020). ACCEDU is quantified as a binary variable that equals “1” if the ACC has a postgraduate degree (e.g., master or doctorate) and “0” otherwise (Elmagrhi et al., 2019). ACCAGE is measured by the ACC’s age in years (Tanyi & Smith, 2015). ACCLEG is computed as a binary variable that equals “1” if the ACC has a law qualification or expertise and “0” otherwise (Ghaleb, Al-Duais, & Hashed, 2021). ACCFEXP is assessed as a dummy variable that equals “1” if the ACC holds financial qualifications or has previous financial experience (e.g., accounting or auditing), and “0” otherwise (Chaudhry et al., 2020). Finally, ACCTEN is measured using the number of years that the present ACC has been serving in this position (Al-Qublani et al., 2020; Ghafran & Yasmin, 2018).

To improve the research model’s goodness and to isolate the impact of other factors affecting CSR disclosure, we also add control variables that may affect the correlation between ACC attributes and CSR disclosure. The first set is linked to the CG characteristics included: ownership concentration (OWNC) is measured by the proportion of firm shares held by the five largest shareholders (Adel et al., 2019; Qaderi et al., 2020). Board size (BSIZE) is computed by the number of directors on the board (Mohammadi et al., 2021). The second set is related to the firm’s characteristics included: audit firm size (BIG4) is computed as a dummy variable taking a value of “1” for firms with a BIG4 auditor and “0” otherwise (Ghaleb, Al-Duais, & Hashed, 2021). Finally, firm size (FSIZE) is computed by the natural logarithm of a firm’s total assets; firm leverage (LEVE) is calculated by the ratio of total liabilities to firm size and market to book value ratio (MTBV) (Chandren et al., 2021; Gal & Akisik, 2020; Ting, 2021). These variables included in our regression model because firms’ CSR investment could be impacted by financial conditions and resource availability. The regressions, in addition, include industry type and year indicator variables. Definitions of the variables considered in this study are shown in Table 2.

Variable Definitions.

Empirical Model

The current study applies the ordinary least squares (OLS) model to examine the impact of ACC attributes on CSR disclosure. This model is suitable for our study to “assess the changes in the dependent variable in response to the changes in the independent variables” (Hair et al., 2014). Further, majority of previous CSR studies applied OLS regression as reported in Dwekat et al. (2021) study. The regression model that we propose is presented in the following equation:

Results and Discussion

Descriptive Results and Correlation Matrix

Table 3 shows the descriptive data statistics of 95 Jordanian firms for the period 2014 to 2018 (475 observations). The mean (median) value of CSR disclosure (CSRDL) is about 34% (33%). This value is similar to those found in recent Jordanian empirical studies (Abu Qa’dan & Suwaidan, 2019; Ghaleb, Qaderi, Almashaqbeh, & Qasem, 2021). This indicates that, on average, Jordanian listed firms disclose 34% of their socially responsible activities in their annual reports. As for the independent variables, the average of ACC independence (ACCIND) among the AC members is 55.6%. Regarding the ACC educational level (ACCEDU), the results indicate that 32% of the ACCs have a postgraduate degree. The mean (median) of ACC age (ACCAGE) is 58.444 (57.999 years). Approximately 4.2% of ACCs have legal expertise (ACCLEG). The mean ACC financial expertise (ACCFEXP) is around 28.4%, which is slightly low. This could be because companies not yet to consider the anticipated role of the AC chair with financial expertise. Finally, the average of ACCs tenure (ACCTEN) is 2.455 years.

Descriptive Statistics.

Note. Number of observations = 475. Variable definitions are reported in Table 2.

For the control variables, the results show the average ownership concentration (OWNC) is 63.1%, suggesting that the largest shareholders own the majority of Jordanian firms. About 41.5% of the firms have hired Big4 firms. The average (median) value of the board size (BSIZE) is 7.901 (7 members), in line with prior studies (Abu Qa’dan & Suwaidan, 2019). The mean for firm size (FSIZE) is 17.148, and the average of firm leverage (LEVE) and market-to-book value ratio (MTBV) are 6.323 and 1.711%, respectively, similar to the findings described by previous studies (Ghaleb, Qaderi, Almashaqbeh, & Qasem, 2021).

Concerning the Pearson correlations matrix for all research variables, the untabulated results indicate the absence of multicollinearity issues. The highest coefficient of Pearson correlation observed across all variables is between FSIZE and CSRDL (correlation coefficient = 0.524). This value is lower than the threshold of more than 80%, confirmed by Gujarati and Porter (2009). Further, the Variance Inflation Factor (VIF) is applied to check for multicollinearity problems. Unreported results show that all values of VIF are below the informed threshold of 10 (Hair et al., 2014), indicating that multicollinearity problem is not existed in our regression model.

Multivariate Analysis

Following the CG and CSR literature (Ghaleb, Qaderi, Almashaqbeh, & Qasem, 2021; Katmon et al., 2019), this study applies OLS regression. Several regression assumptions (such as normality of error term, multicollinearity, heteroscedasticity of residue, and autocorrelation) are tested to strengthen the research model’s reliability and validity. Untabulated results confirm that these assumptions are not of concern in this study.

Table 4 presents the regression results of the direct relationship between ACC attributes and CSR reporting. In particular, the results show that the adjusted R-squared has a value of 0.600, implying that the six independent variables can explain approximately 60% of the variance in CSRDL. Further, the results indicate that the OLS regression model is statistically significant in explaining the CSRDL of Jordanian listed firms (p = 0.000) at the 1% level, implying that the model is statistically valid.

Regression Results of the Relationship Between ACC Attributes and CSR Disclosure.

Note. Variable definitions are reported in Table 2.

p < .01. **p < .05. *p < .10.

The results in Table 4 demonstrate that ACCIND has a positive and significant connection with greater CSR disclosure (t-value = 1.86, p = 0.064), providing support for H1. This finding reveals that firms with more independent ACCs are more likely to provide greater CSR disclosure. Our finding is consistent with the agency theory postulation and the evidence of Dwekat et al. (2020), which found that an independent ACC does motivate firms to publish socially responsible information, mitigating agency conflict and information asymmetry problems. These findings suggest that ACC independence is one of the internal governance monitoring mechanisms in solving conflicts between management and stakeholders, therefore, increasing CSR reporting (Buallay & Al-Ajmi, 2020; Dwekat et al., 2020). However, this result contrasts with prior disclosure studies from Australia (Appuhami & Tashakor, 2017), which indicate that CSR disclosure is not affected by ACC independence.

The results also indicate that ACCEDU is positively and significantly associated with CSR reporting (t-value = 2.67, p = 0.008). Therefore, H2 is accepted. The result suggests that ACCs with a high educational level may engage in more CSR-related activities. This result supports the view that educational level plays a crucial role in constructing and applying the firm’s strategic decision on disclosure of CSR (Katmon et al., 2019). This is because an educated ACC have broader perspective, superior pattern of thinking, and better CSR knowledge, thereby engaging in strategic decisions like CSR disclosure, which helps to understand the wider interests of various stakeholders and maintain a good corporate image. These findings are aligned with the agency theory and similar to the findings of Harjoto et al. (2019) and Katmon et al. (2019), who reveal that directors’ education level is related to higher CSR disclosure quality. However, the results are inconsistent with some previous studies that reported an insignificant association between directors’ educational level and CSR reporting (Elmagrhi et al., 2019; Hassan et al., 2020; Khan, Khan, & Senturk, 2019).

ACCAGE is inversely and significantly associated with socially responsible activities (t-value = −2.54, p = 0.011), and therefore H3 is not supported. This indicates that ACC age is related to lower CSR disclosure. The reason for this result may be younger director are more risk takers, more enthusiastic, and attracted toward emerging innovative business ideas (Fahad & Rahman, 2020); consequently, these directors strategically decrease the engagement in CSR practices. This result is inconsistent with the agency theory. This result confirms those of Katmon et al. (2019) and Khan, Khan, and Senturk (2019), who demonstrated that younger directors are likely to contribute to CSR disclosure. However, this result is inconsistent with Ibrahim and Hanefah (2016), which found that directors’ age is essential in enhancing CSR-related information disclosure. This could be because older directors are more willing to increase transparency and diminish agency problems and information asymmetry (Elmagrhi et al., 2019).

As shown in Table 4, the relationship between ACCLEG and CSR activities is positively significant (t-value = 1.80, p = 0.072), hence H4 is accepted. The result implies that the greater the extent of the ACC’s legal expertise, the higher the CSR disclosure. A possible explanation is that directors with legal expertise has a significant governance role due to the legal and regulatory environment’s rising complexity (Dharwadkar et al., 2021). This result is consistent with (de Villiers et al., 2011) findings which indicate that ACCs with legal expertise are associated with increased environmental performance, suggesting that board legal experts have a significant role in expanding the quality of corporate disclosure (Bozanic et al., 2019).

Table 4 also shows that ACCFEXP is negatively but insignificantly related to CSR disclosure (t-value = −1.34, p = 0.180), and therefore H5 is not supported. That is, the ACC’s financial expertise fails to increase social responsibility disclosure. One possible explanation for the insignificant relationship is that only one third of ACCs has financial expertise because the Jordanian regulations has pay little attention to AC experience. This finding is inconsistent with the agency theory. The result is similar to those of Qaderi et al. (2020), who show that CSR disclosure is not affected by the financial expertise of AC members. However, this result is inconsistent with other authors (Chan et al., 2021; Mohammadi et al., 2021), who found firms with AC financial expertise have better CSR disclosure.

Finally, results indicate that ACCTEN has no significant relationship with social responsibility disclosures (t-value = −0.24, p = 0.810). Hence, H6 is not supported. A possible explanation is that ACCTEN is not influenced as critically as other attributes of the ACC. This finding contradicts agency theory. Our finding is in line with Bravo and Reguera-Alvarado (2019) study, which reveals that AC’s longer tenure discourages the disclosure of environmental and social responsibility information. However, our evidence is inconsistent with other disclosure studies (Othman et al., 2014; Setiany et al., 2017), which found that long-serving AC members tend to increase firm’ voluntary disclosure, because AC tenure plays a crucial role in increasing corporate transparency, and thus non-financial reporting quality.

The results of the control variables reveal that ownership concentration is negatively associated with CSR reporting, suggesting that highly concentrated ownership firms are less likely to disclose CSR activities. Likewise, consistent with the disclosure studies (Abu Qa’dan & Suwaidan, 2019; Katmon et al., 2019), BIG4 audit firms positively impact the disclosure of socially responsible practices. BSIZE is positively associated with higher CSR engagement, implying that firms with a large board of directors are expected to provide a higher level of CSR disclosure; this is similar to the findings (Abu Qa’dan & Suwaidan, 2019). FSIZE positively affects the level of CSR-related information disclosure, in line with the study of Appuhami and Tashakor (2017), who found that larger firms are more committed to investing in socially responsible activities as they have more resources. LEVE insignificantly and positively affects the CSR activities of the selected firms, contrasting with the results of other studies (Abu Qa’dan & Suwaidan, 2019; Fallah & Mojarrad, 2019). Finally, MTBV is significantly positively associated with CSR-related activities, similar to the evidence in prior studies (Qaderi et al., 2020).

Additional Robustness Checks

To confirm the robustness of our main results, we re-run OLS regression with robust standard errors, consistent with prior disclosure literature (Adel et al., 2019; Ghaleb, Qaderi, Almashaqbeh, & Qasem, 2021; Katmon et al., 2019). The findings in Table 5 (Model 1) show that the impacts of almost variables remain unchanged compared to those previously reported in Table 4, indicating that ACC attributes (ACCIND and ACCEDU) are significantly associated with higher CSR disclosure, and that an older ACC is related to lower CSR-related information disclosure. Thus, these findings indicate that our main results are robust across the OLS with robust standard errors regression estimation.

Regressions Result for Additional Tests.

Note. Variable definitions are reported in Table 2.

p < .01. **p < .05. *p < .10.

In this additional test, we re-estimate our regressions model by including alternative measures of ACC attributes. ACCEDU is measured alternatively as a continuous variable: secondary school or below = 1, diploma = 2, bachelor’s degree = 3, master’s degree = 4, and doctorate = 5 (Katmon et al., 2019; Khan, Khan, & Senturk, 2019). The natural logarithm of ACC age alternatively measures ACCAGE (Chandren et al., 2021). The results presented in Table 5 (Models 2 and 3) reveal that the findings remain consistent with our preliminary results, thus confirming the model’s robustness.

Additionally, extensive studies have found that large firms are more likely to engage in CSR-related information disclosure than small firms (Katmon et al., 2019; Ting, 2021). To investigate the potential influence of firm size on the relationship between the ACC characteristics and CSR disclosure, this study divides the sample into large and small firms. We define large firms as those with total assets higher than the sample’s median and small firms with total assets equal to or less than the sample’s median. Table 5 (Models 4 and 5) presents the subsample (large and small firms) regression results: ACC attributes in large firms are more likely to improve socially responsible disclosures compared to small firms.

Conclusions

Motivated by the absence of studies that examine the effect of AC leadership on CSR reporting, the current study aimed to investigate the impact of ACC characterizes on CSR reporting in Jordan. The analysis is performed using a Jordanian sample of 475 firm-year observations from 2014 to 2018. We began by measuring the CSR reporting level in Jordan using an index established and applied by previous studies. Then, we performed an empirical examination to assess the effect of the ACC characteristics (independence, education level, legal expertise, age, tenure, and financial expertise) and CSR reporting level. The results show that ACC education level, independence, and legal expertise positively and significantly affect CSR reporting, but ACC age is negatively and significantly related to CSR reporting. However, ACC financial expertise and tenure do not affect CSR reporting. We conclude that firms that appoint an independent ACC with legal expertise and a high education level are more likely to have a high level of CSR reporting, while older ACCs are associated with a lower level of CSR reporting. Additional analyses have corroborated our results.

This study contributes to support the stakeholder and agency theories by identifying the relationship between ACC attributes and the CSR reporting, especially in an emerging economy. Agency theory suggests that the AC can affect its effectiveness in monitoring management and overcoming agency conflicts, increasing CSR voluntary disclosure. In addition, our study has important practical implications for firms’ management, policymakers, researchers, and society. First, unlike many countries that emphasize the role of the ACC, in Jordan, the regulators have yet to mention any requirements related to the ACC. Thus, the outcomes from this study may be timely in encouraging regulators in Jordan and similar developing countries to improve the CG rules concerning the ACC’s role. Second, CSR reporting level is directly affected by ACC characteristics. Thus, firms’ management may consider the findings from this study and pay more attention to specific features that help report high CSR activities, consequently helping to produce high-quality financial and non-financial information. Our results have implications for the effect of firm size on the effectiveness of CG tools (including ACC) as the effect of the ACC features is more pronounced in large firms than in small ones. Thus, small firms may improve their effort in adopting good CG. Third, our paper adds to the literature by extending the debate on the monitoring role of CG by investigating the relationship between AC leadership and CSR reporting. In addition, it examined the role of firm size on the effectiveness of CG. Thus, our findings lead to a better understanding of how the leadership of the AC may improve CSR reporting. Further, the effect of firm size on this relationship is also addressed. Finally, our findings may help enhance the value of social life, as involvement in social responsibility by firms may directly affect people’s lives and allow firms to reach sustainable development targets.

The study’s results are subject to some limitations that lead to future research. The study examined only six of the ACC characteristics. However, attributes other than those examined (such as gender, religion, CSR training or expertise, and social ties) may significantly impact CSR reporting. Thus, future studies may address these limitations. Further, CSR disclosure is reported in the previous studies using various measurements; thus, the validity of our findings is subject to similarity with the measures applied in this study. Finally, valuable insights may be gained through qualitative research, such as interviews with ACCs and top management.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.