Abstract

The purpose of the current study is to investigate the influence of corporate and foreign ownership structures on the timeliness of financial reporting. The sample of the study consists of 2,204 observations obtained from 208 companies trading in Borsa Istanbul between 2008 and 2019. Multiple regression analysis was conducted, and the relationship between ownership structure and financial reporting timelinesses was investigated. The findings indicate that corporate and foreign ownership are significantly and negatively associated with financial reporting timeliness. Robustness analysis was carried out using the two-stage GMM method, and it was determined that there was no endogeneity problem. The results provide valuable information for financial reporting users, such as investors, companies, regulators, policymakers, and auditors, and will aid them in their decision-making processes as it reduces information asymmetry and contributes to the improvement of the financial reporting quality.

Introduction

Financial reporting timeliness is an important factor affecting investor decisions since it contributes rapidly and efficiently to the pricing and valuation performance and functions of stock markets (Daoud et al., 2014). The timeliness of financial reports holds significant sway over investment decisions, as investors understand a company’s failure to publish its financial statements in a timely manner as a negative signal (Chambers et al., 1984). The timeliness is one of the qualitative characteristics of financial reporting because it determines the appropriateness of information and affects the decisions made by the users and beneficiaries of financial reports (Daoud et al., 2014). The investigation of the factors that impact the timeliness of financial reporting is a significant field of study (Mouna & Anis, 2013). Identifying these factors will help companies develop corporate governance policies to reduce delays in financial reporting timeliness. The most important source of information about companies in developing countries is their financial statements. Investors demand to rely on companies’ financial statement information when making their decisions (Al Daoud et al., 2015). Through identifying these characteristics, investors will be able to make the best choice and will have access to information that will boost the financial statements’ credibility.

Despite the existence of a considerable and comprehensive corpus of literature concerning the determinants of financial reporting timeliness, a noteworthy segment of antecedent scholarly work has focused on audit-related characteristics, including audit committee, audit firm, audit firm size, and auditor opinion. The extent of research investigating the influence of a company’s ownership structure on the timeliness of financial reporting is relatively restricted. The ownership structure of companies exhibits significant variation. The ownership structure is referred to by different ownership structures such as family ownership, foreign ownership, state ownership, employee ownership, managerial ownership, and institutional ownership. According to Yurtoglu’s (2000) research, the predominant ownership structure in Turkey is that of a family company, which exhibits a complex and pyramidal arrangement. It is needed to examine the ownership structure in emerging economies like Turkey from this perspective. Research has revealed that ownership structure has an impact on corporate performance (Thomsen & Pedersen, 2000), corporate management performance (Xu & Wang, 1999), agency costs (Ang et al., 2000), financial reporting quality (Yasser et al., 2017), and earnings management (Aygun et al., 2014). The timeliness is deemed to be a measure of the quality of financial statements. The present context suggests that a correlation may exist between ownership and timeliness, particularly in light of the influence of ownership structures on the financial reporting timeliness. Several studies have examined the relationship between ownership structure and the timeliness of financial reporting (Al-Ajmi, 2008; Albawwat et al., 2020; Apadore & Mohd Noor, 2013; Habib et al., 2019). Several studies have examined the relationship between ownership structure and the timeliness of financial reporting (Al-Ajmi, 2008; Albawwat et al., 2020; Apadore & Mohd Noor, 2013; Basuony et al., 2016; Habib et al., 2019; Ishak et al., 2010). Ishak et al. (2010) found that foreign ownership was negatively associated with audit report lag. Basuony et al. (2016) revealed findings that institutional and foreign ownership are negatively associated with audit report lag. Upon examination of studies conducted in Turkey, only one study has been found that investigates the effect of corporate and foreign ownership structures on financial reporting timeliness. The findings of Aksoy et al. (2021) show that there is a insignificant relationship between foreign ownership structure and financial reporting timeliness. This result contrasts with previous literature and highlights the lack of clarity regarding the determinants of financial reporting timeliness. Further extensive research is required to address the issue of financial reporting timeliness in Turkey. The dearth of research in the field of interest within Turkey serves as a significant impetus for our investigation.

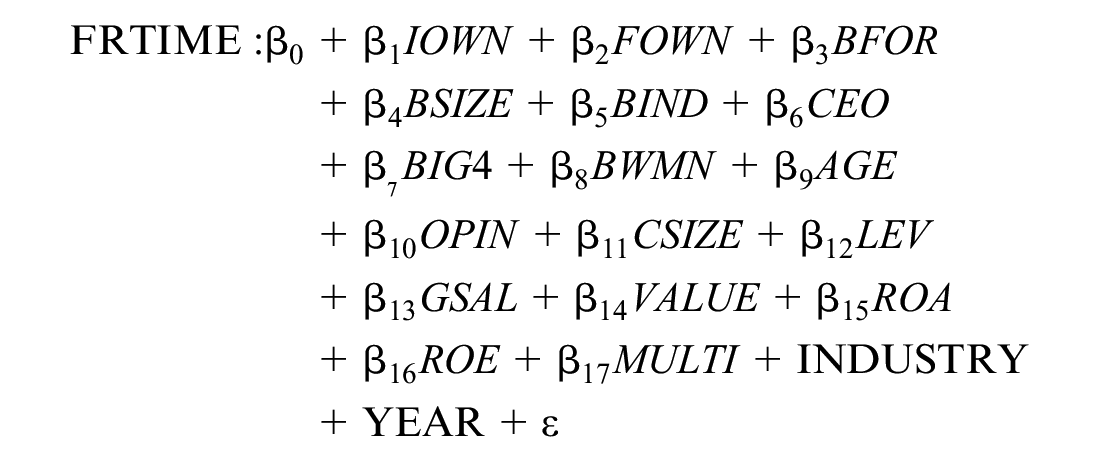

The purpose of this research is to investigate the influence of corporate and foreign ownership structures on the timeliness of financial reporting. Two independent variables, institutional and foreign ownership, were used in the research model. Control variables were handled as corporate governance-based variables, firm-based variables, audit-based variables, and a total of 15 control variables were included in the model. The sample of the study consists of 2,204 observations obtained from 208 non-financial companies trading in BIST between 2008 and 2019. The results indicate that companies with higher rates of foreign and corporate ownership tend to publish their financial reporting earlier. In addition, the results of the analysis show that multinational companies tend to announce their finances later than national companies. We estimate that this result may be due to the possibility that the information flow may be slow due to coordination problems with the affiliates of multinationals in different countries. Furthermore, the results showed that companies where the overall number of board members, the independent membership ratio of the board of directors, the market value versus registered value, the profitability of equity, and the active profitability rate increased and the audit view was positive tended to publish financial statements in a shorter timeframe, while companies with a higher debt rate had the tendency to publish financial reportings later. Additionally, the analysis concluded that the number of foreign board members of the companies did not have a relationship with the timeliness of financial reporting, CEO identity, audit company, female board membership, company age, company size, or gross sales natural logarithm characteristics.

The study presented herein offers several significant contributions. This research makes a valuable contribution to the existing literature by addressing the limited number of studies that have investigated the influence of ownership structure on the timeliness of financial reporting. Additionally, our study employs a comprehensive dataset spanning multiple years to analyze this topic, which is a departure from the more narrow timeframes utilized in previous research. National and international firms are likely to differ from each other in terms of the preparation time of financial reports. We want to test the possible effect by adding the multinational variable to our model. The distinction between national and multinational firms makes it important for users of the financial report to recognize the opportunity to compare national and international firms and contribute to the literature by creating a different perspective. We believe the results will help financial report users make the right decisions. The timeliness of financial reporting, which is a dependent variable, was also addressed from three different perspectives, taking into account abnormal reporting delays and sectoral reporting delays as opposed to other studies, and the effects of independent variables and control variables in the three models established in this context were studied in detail. The use of the sectoral reporting lag variable in the research model will enable the sectors to be compared in terms of timeliness and will help financial statement users such as investors, companies, audit firms, and policymakers make the right decisions. The literature on the relationship between financial reporting timeliness and ownership concentration structures is not extensive, particularly in terms of controlling for other factors such as corporate governance, company-specific characteristics, and audit-based variables. The study of the subject by using a large number of control variables such as corporate management, firm, and audit-based control variables provides a significant contribution to the limited literature. The results will also provide valuable information for financial reporting users, such as investors, companies, regulators, policymakers, and auditors, and will aid them in their decision-making processes as it reduces information asymmetry and contributes to the improvement of financial reporting quality. Financial reporting timeliness is a useful tool to deal with inefficiencies in capital markets. The results obtained are therefore valuable because they will contribute to a more functional capital market.

The rest of the study is organized as follows: The next section gives an organizing and conceptual background and sets out the hypotheses. The data and research methodology are outlined before proceeding to report the regression results and endogeneity tests. The final section summarizes the findings, including the managerial implications, limitations of the study, and recommendations for future research.

Theoretical Framework and Hypotheses

Theoretical Framework

One of the theories explaining the relationship between the ownership structure, the characteristics of the board of directors, and the timeliness of financial reporting is the agency theory. The agency relationship is the subject of an agreement based on a contract that gives the shareholder’s representative the authority to perform certain services on his own behalf and make certain decisions (Jensen & Meckling, 1976). A agency can sometimes make decisions in line with his own interests, disregarding the interests of the company (Agrawal & Knoeber, 1996). If the representative does not act in accordance with the interests of the client, an authority problem arises (Brennan, 1995). Delays in the timeliness of financial reporting can lead to investors losing confidence in the report, and the problem of authority increases (Ilaboya & Iyafekhe Christian, 2014). On the other hand, managers are also information providers for the business. Managers may tend to give little or no information to business owners for their own benefit. Such action may prevent a financial statement from accurately and reasonably reflecting the company’s activities and may not provide useful information to its users (Agrawal & Knoeber, 1996). In order to minimize these behaviors, the shareholders should align their interests with those of the manager. Ownership structure has a significant impact on resolving the proxy issue. In addition to institutional investors, foreign investors with resources and financial expertise in the company are motivated to supervise managers to reduce the agency problem (Bamahros et al., 2016; L. Jiang & Kim, 2004). For this reason, companies with high corporate and foreign ownership are expected to minimize agency problems. According to the stakeholder theory, which is considered an extension of the proxy approach, managers should design and implement processes in a way that satisfies not only the shareholders but also all stakeholders of the company (Freeman, 2010).

Another theory that concerns the subject of our study is asymmetric information theory. This theory was first mentioned in the work of Akerlof (1970) and later developed by Spence (1973), and the study of Rothschild and Stiglitz (1976) is complementary to these two studies. Asymmetric information occurs when one party has less information than the other or has incorrect information. This situation causes those with little knowledge to make wrong decisions and those with information to make decisions against the other party (Akerlof, 1970). Managers may not have enough information about the business, or they may knowingly mislead investors despite having enough information. Asymmetric information theory is used to explain signals to the market by investors about securities of publicly traded companies or to improve the disclosure of accurate information. The current study will contribute to the reduction of information asymmetry about the causes of financial reporting delays and will help investors, managers, and policymakers make sound decisions. Considering all these theories, it is important for companies to publish their financial reports on time.

Literature Review

Quantitative methods were mostly used in studies on the factors affecting timeliness in different countries. In a study conducted on 494 observations from the Australian Stock Exchange, it was stated that audit committee characteristics have an impact on financial reporting timeliness (Sultana et al., 2015). A research of companies traded on the U.S. securities exchange used 46,118 observations and concluded that the type of audit company was influence on timelines of financial reportings (Meckfessel & Sellers, 2017). The study of companies trading on the China Stock Exchange used 4,025 observations and found that audit expertise and audit risk had an impact on timeliness (Chan et al., 2016). In another study of 14,948 observations in the United States, it was concluded that the characteristics of the audit firm influenced the timeliness of financial reporting (Whitworth & Lambert, 2014). In a study of 8,950 observations conducted in Korea, the audit company, the auditor’s opinion, and the variables in the audit fees were related to the timeliness of financial reports (Lee & Jahng, 2011). In the study conducted on 703 companies traded in the Malaysian Stock Exchange, it was concluded that the audit opinion, type of auditor, audit committee size and firm profitability variables have an effect on the timeliness of the companies’ audit reports (Nelson & Shukeri, 2011). In the research of 61 companies operating in Nigeria, it was noted that the size of the company, the age of the company influenced the timeliness of financial reporting (Iyoha, 2012). In the study of 211 non-financial companies trading on the BIST, it has been stated that financial reporting timeliness was affected by auditor opinion and auditing firm size (Türel, 2010). A study of 171 companies traded on the Athens Stock Exchange showed that variables such as audit type, audit fees, and the number of disclosures in the audit report have an impact on the timeliness of financial reporting (Leventis et al., 2005). A study of 105 companies in Spain concluded that industry type and company size variables influenced the timeliness of financial reporting (Bonsn-Ponte et al., 2008).

Ownership structure is among the interesting topics in the corporate governance literature. In most of the studies, the corporate governance performance of the ownership structures of the companies (Boubakri et al., 2005; G. Chen et al., 2006; F. Jiang & Kim, 2020; Xu & Wang, 1999) financial reporting timeliness (Abdelsalam & Street, 2007; Aksoy et al., 2021; Al-Ajmi, 2008; Albawwat et al., 2020; Alsmady, 2018; Apadore & Mohd Noor, 2013; Bamahros et al., 2016; Basuony et al., 2016; Habib et al., 2019; Ishak et al., 2010; Mouna & Anis, 2013), financial reporting quality (Amrah & Obaid, 2019; An, 2015; Yasser et al., 2017), firm performance (Efobi & Okougbo, 2014; Lin & Fu, 2017; Nelson & Shukeri, 2011; Xu & Wang, 1999), corporate dividend policy (Yousaf et al., 2019), credit rating (Ali et al., 2020), profitability (García-Herrero et al., 2009), stock prices (Huang et al., 2019), earnings management (Alves, 2012; Alzoubi, 2016; Saona et al., 2020) etc.

Mouna and Anis (2013), in their research on 33 companies traded in Tunisia in 2009, found that financial reporting timeliness is affected by the variables of ownership structure and CEO duality of companies. Albawwat et al. (2020) revealed that foreign ownership and state ownership are associated with financial reporting timeliness in their research on 72 company data traded on the Jordanian Stock Exchange between 2015 and 2019. In another study conducted on the data of 68 companies traded on the Jordanian Stock Exchange between 2011 and 2015, it was concluded that management ownership is not related to financial reporting timeliness, but foreign ownership is related to financial reporting timeliness (Alsmady, 2018). In a study of 201 companies in the Middle East between 2009 and 2013, it was concluded that the timeliness of financial reporting was associated with the concentration of ownership, corporate ownership, and foreign ownership (Basuony et al., 2016). A study of 180 companies operating in Malaysia in 2009 to 2010 also found that the ownership structure was linked to the timeliness of financial reporting by obtaining similar results (Apadore & Mohd Noor, 2013). Aksoy et al. (2021) revealed that in a study on 187 companies trading in BIST, the structure of corporate ownership was related to the timeliness of financial reports.

A study of manufacturing companies traded on the Indonesian Securities Exchange between 2010 and 2016 concluded that expert auditors influenced the timeliness of financial reporting based on the independence of the board of directors, ownership concentration, and audit quality (Pradipta & Zalukhu, 2020). In a study conducted on 1,727 observations from the Tehran Securities Exchange, the results highlighted that if the CEO is promoted within the company, the financial reporting timeliness is longer (Oradi, 2021). In a research using 18,921 observations from U.S. companies, it was concluded that the ownership structure of the CEO is significantly related to the timeliness of financial reporting (Azizan, 2019). A study of 13,461 observations from companies listed on the Australian Stock Exchange found that audit committee ownership increased the company’s financial reporting timeliness (Bhuiyan & D’Costa, 2020). A study of 46 companies trading on the Palestinian Securities Exchange highlighted the conclusion that the company was affected by the board size, audit quality, audit committee characteristics, and ownership structure (Hassan, 2016).

In the study of 190 non-financial companies trading on the Amman Securities Exchange for the period 2014 to 2017, it was found that corporate ownership and ownership concentration have an impact on the timeliness of financial reporting (Abed et al., 2020). In a study conducted on 612 observations obtained from 204 non-financial companies traded on the Indonesian Stock Exchange between 2015 and 2017, the effects of board size, board meetings, board independence, audit committee size, and firm size on financial reporting timeliness. However, audit committee independence, audit committee expertise, and leverage are not associated with on financial reporting timeliness (Firnanti & Karmudiandri, 2020). A research of 288 companies that traded on the Malaysian Securities Exchange between 2007 and 2009 indicated that the timeliness of financial reporting is associated with but has no relationship with management ownership (Junaidda, 2017). A 2013 study of companies traded on the Kuwait Securities Exchange (KSE) concluded that financial reporting timeliness was associated with audit quality, board size, board independence, duality, and state ownership (Alfraih, 2016). A study of 543 observations from companies trading on the Kenya Stock Exchange between 2007 and 2016 showed that audit committee financial expertise, board size, board meetings, and independence of the board of directors were related to the delay in financial report increases (Mathuva et al., 2019).

The Development of the Hypothesis

Ownership Structure

The ownership structure and the identity of shareholders are important concepts that affect the timeliness of financial reporting (Habib et al., 2019). Financial reporting timeliness is improved in companies with higher foreign and corporate ownership (Ishak et al., 2010). Similar to this study, we examine the ownership structure in two categories: foreign and corporate ownership.

Foreign Ownership

Foreign investors are long-term investors and do not change their portfolios too often. They avoid investing in companies with more risky financial management practices (Batten & Vo, 2015). In addition, foreign investors’ desire to earn higher dividends causes firms to have more financial discipline and thus higher financial performance (Baba, 2009). The asymmetric information may be mitigated with timely information reaching investors (Jaggi & Tsui, 1999). Foreign-invested companies are supported by practices that associate greater transparency with lower information asymmetry and pressure companies to present their financial information on time (L. Jiang & Kim, 2004). For this reason, it is expected that the asymmetric information problem will be minimized in companies with a high foreign ownership rate. Since the absence of asymmetric information problems will prevent managers from presenting incorrect or incomplete information for their own benefit, the high rate of foreign ownership will also prevent the emergence of agency problems. Due to all these effects of foreign ownership, companies with increased foreign ownership are expected to publish their financial reports earlier (Ishak et al., 2010). Based on the above arguments and the agency theory and information asymmetry theory. Therefore, we suggest the following hypothesis:

H1: There is a negative relationship between the timeliness of financial reporting and foreign ownership.

Institutional Ownership

Institutional investors actively monitor the business of firms because of their advantages, such as financial expertise, size, and having more resources (Shleifer & Vishny, 1986). Corporate Investors have the power to influence the management’s activities directly and indirectly by buying and selling their shares and contribute to the corporate governance of companies (Gillan & Starks, 2002). Thus, the presence of corporate investors makes it possible for auditors to enter lower auditing risk expectations in these companies (Ishak et al., 2010). Due to these advantages, corporate investors could put pressure on the management to act in line with the interests of shareholders (Conover et al., 2008). This pressure prevents managers from sharing wrong or incomplete information with investors and minimizes the problem of proxy and asymmetric information. (Shleifer & Vishny, 1986). For all these reasons, companies with high corporate ownership are expected to publish their financial reports earlier (Ishak et al., 2010). Based on the above arguments and the agency theory and information asymmetry theories, we propose the following hypothesis:

H2: There is a negative relationship between financial reporting timeliness and enterprise ownership.

Control Variables

A review of previous studies dealing with the timeliness of financial information requires that we consider control variables such as corporate governance-based variables, firm-based variables, and audit-based variables in order to analyze the relationship between financial reporting timeliness and ownership structure.

Srinidhi et al. (2011) found a positive relationship between board gender diversity and earnings quality. Given the large number of studies on the relationship between female presence on the board and good governance, the number of female executives is likely to be related to financial reporting timeliness (Aksoy et al., 2021; Alsmady, 2018).

It is expected that the presence of foreign members in the board of directors will add value to the company by enabling them to take advantage of the expertise and monitor the board (Fama & Jensen, 1983) and help the management to make decisions in line with the interests of the shareholders (Coughlan & Schmidt, 1985). The presence on the Board of Directors of independent members reduces the delays in the timeliness of financial reporting by contributing to the reduction of monitoring problems (C. J. P. Chen & Jaggi, 2000), as it is perceived as a tool to monitor management behavior (Abdelsalam & Street, 2007).

In companies where the chairman of the board of directors and the CEO are separated, it is highly likely that financial reports will be presented to the shareholders in a timely and effective manner (Abdullah, 2007). Mouna and Anis (2013) and Afify (2009) show that CEO duality is negatively associated with financial reporting timeliness. The size of the board of directors is a widely used variable in the literature on timeliness, and research has concluded that it is negatively associated with the timeliness of financial reporting (Ibadin et al., 2012; Olabayo et al., 2018). As a result, companies with a high number of board members are expected to announce their financial statements earlier.

Since the four big audit companies have superior technology, international connections, qualified manpower, and more resources, they work more efficiently than other audit companies. These features enable the big four auditing companies to perform their audit activities faster and to reduce audit report delays (Adebayo & Adebiyi, 2016; Basuony et al., 2016; Leventis et al., 2005; Owusu-Ansah & Leventis, 2006; Türel, 2010). Companies with positive opinions may be expected to publish their annual reports earlier than others because they send a positive signal to the public about corporate financial performance (Habib et al., 2019; Nelson & Shukeri, 2011; Vuran & Adiloğlu, 2013). Therefore, companies with favorable audit opinions are likely to release their financial reports to the public sooner.

Old firms are likely to be more competent in gathering, processing, and releasing information when needed due to their greater learning experience compared to newer companies (Owusu-Ansah, 2000). Thus, old firms tend to publish their reports earlier than other companies (Al-Juaidi & Al-Afifi, 2016; Al-Tahat, 2015; Basuony et al., 2016; Efobi & Okougbo, 2014; Iyoha, 2012). The size of the company was calculated based on the literature related to timeliness, taking into account the total assets of the company (Afify, 2009; McGee, 2006). Larger companies identified in this scope are more likely to disclose their financial statements in a timely manner than small companies (Afify, 2009; Karim et al., 2006; McGee, 2006).

Companies with high return on assets (ROA) and return on equity (ROE) tend to present their financial reports earlier (Al-Ajmi, 2008). Since total sales are one of the factors that positively affect firm performance (Kılıç & Ayrıçay, 2018), companies with low gross sales are likely to have a delay in financial reporting time compared to companies with high sales. Since a high leverage rate representing the ratio of total debt to total assets is classified as bad news, companies with a high leveraging rate are expected to publish their financial statements later (Aksoy et al., 2021; Al-Ajmi, 2008; Carslaw & Kaplan, 1991; Mert & Cömert, 2014), while companies with a high market-to-book value ratio will be expected to present their financial reports earlier (Azami & Salehi, 2017).

The fact that the company has subsidiaries in different countries other than the country in which it operates makes the company a multinational company (Lewellen & Robinson, 2013). Because of the increased diversity of information required by multinational companies, it is expected that multinational companies will voluntarily disclose more non-financial information than national companies (Meek et al., 1995). This expectation and the idea that multinational firms are more corporately governed make it likely for multinationals to publish their financial statements earlier than national firms. However, the prediction that data collection may take longer due to coordination problems and potential disruptions in the flow of information between affiliated firms and connected environments (Wu & Tihanyi, 2013) allows us to think that multinationals will be able to submit their financial reports later than national companies.

Research Methodology

The purpose of this research is to examine the relationship between ownership structure and financial reporting timeliness. In this context, regression analysis was conducted, and the relationship between ownership structure and financial reporting timeliness was investigated. In this section, firstly, the details of the sample required for the analyses to be carried out are given. Afterward, the definitions of all variables used in the analysis and the measurement details are mentioned. Finally, the statistical models used to test the hypotheses of the study are shown.

Sample Selection

Regression analysis was carried out using 2,204 observations obtained from 208 non-financial companies traded in Borsa Istanbul between 2008 and 2019. All non-financial companies traded in Borsa Istanbul, whose financial statement information can be accessed, are included in the analysis. Similar to the literature, all financial companies were excluded from our sample because the balance sheet and income statement data were different. Table 1 shows the sample selection of the study and the sectoral distribution of the companies forming the sample (by firm-year observations). As seen in Table 1, the number of observations of all companies operating in the BIST between 2008 and 2019 is 5,126. From these observations, the observations of financial companies (1,355) and the observations of companies with missing data (1,567) were excluded. Thus, the final sample number was 2,204. In addition, as seen in Table 1, 70.37% of the companies that make up the sample operate in the industrial sector. The second rank is the service sector with 21.19%, and the third rank is the technology sector with 8.44%.

Sample Description.

As of 2008, in Turkey, the fiscal statements of the companies operating in Borsa/Istanbul are published in the Public Information Platform (PIP). As a result of the pandemic of 2020 and 2021, we did not add financial table data for these years in order to ensure that our regression results were not inconsistent, so that health and economic difficulties occurred in our country as well as in the rest of the world. We obtained the data manually using the following sources: (1) Public Information Platform; (2) Borsa Istanbul; (3) Company Websites; and (4) Finnet Database.

Variable Definition and Measurement

We list and define our variables in Table 2. In our model, we use three financial reporting timetables as dependent variables: financial reporting timeliness (TIME), sectoral reporting delay (SECRD), and abnormal reporting delay (USND). Financial reporting timeliness refers to the total number of days spent between the end of the accounting period and the date on which the company published its financial statements (Al Daoud et al., 2015; Owusu-Ansah, 2000), the difference between the company’s financial reporting timeliness and the average sector reporting time (Baatwah et al., 2015; Mande & Son, 2011), and the abnormal delay represents the distinction between the firm’s financial reporting delay and the median financial reporting delay (Bamber et al., 1993). We measure the ownership structure we use as an independent variable, such as corporate ownership and foreign ownership. Corporate ownership (IOWN) is the percentage of company ownership in the total capital of the company, while foreign ownership (FOWN) is measured by the percentual of foreign ownership in the overall capital of the company. The number of female members of the Board of Directors (BWMN) we measure by taking into account the total number of women members in the board of directors of the company, the number of foreign members (BFOR) in the board, and the size of the board (BSIZE) we take into consideration the overall number of board members. We measure the independence of the Board of Directors (BIND) by the ratio of independent members on the board of directors. The CEO duality (CEO), if the chairman of the board and the CEO are the same, person, is 1; otherwise 0, if the audit service is received from four big audit firms (BIG4) 1; 0 otherwise, and takes a value of 1 if the opinion of the audit report (OPIN) is positive; otherwise it is 0. We measure the leverage (LEV) with the debt-to-equity ratio, the return on equity (ROE) with net income divided by shareholders’ equity, return on assets (ROA) by dividing a company’s net income by its total assets, market to book value ratio (VALUE) with market price per share divided by book value per share, total sales (GSAL) with the natural logarithm of total sales, company size (CSIZE) with the natural logarithm of total assets, company agee (AGE) the natural logarithm age of the company, and finally If the company is multinational, it takes the value 1; otherwise 0.

Variable Descriptions.

Research Model

This study uses multiple regression analysis to investigate the relationship between ownership structure and financial reporting timeliness. Three different models have also been established to investigate the impact of the ownership structure on the timeliness of financial reporting.

The first model was created to show the impact of independent variables on financial reporting timeliness, the second model on sectoral reporting delay, and the third model on the abnormal delay of independent variables. In the first model, the Financial Reporting Timeliness variable is consistent with most of the studies in the literature and is quite popular (Al Daoud et al., 2015; Al-Tahat, 2015; Owusu-Ansah, 2000) Sectoral reporting delay and abnormal delay models were created with the aim of showing the effect of the ownership structure on the sector and company’s financial reporting timeliness. Structural equations of three models:

Model 1:

Model 2:

Model 3:

Results and Discussion

Explanatory Analysis

The following Table 3 lists the average, median, standard deviation, maximum, and minimum values of the variables. According to Table 3, the companies involved in the study disclosed their financial statements to the public on average 66,869 days after the end of the period. This also shows that the companies in the sample published their financial statements within approximately 2 months. The minimum and maximum periods of financial reporting are 21 and 157 days, respectively. This statistic shows that there are considerable differences between the dates companies disclose their financial statements. In studies conducted in other countries, the average financial reporting delay was 48.42 days in Bahrain (Mousa et al., 2022), an average of 76.31 days in Iran (Oradi, 2021), and an average of 80.67 days in Australia (Sultana et al., 2015), an average of 67.47 days in the USA (Meckfessel & Sellers, 2017), an average of 76 days in France (Khoufi & Khoufi, 2018), an average of 97.56 days in Greece (Leventis et al., 2005), an average of 84.34 days in China (Chan et al., 2016), and an average of 67.21 days in Egypt (Afify, 2009).

Descriptive Statistics.

According to Table 3, the corporate and foreign ownership averages of companies are 47,934 and 11,710, respectively.

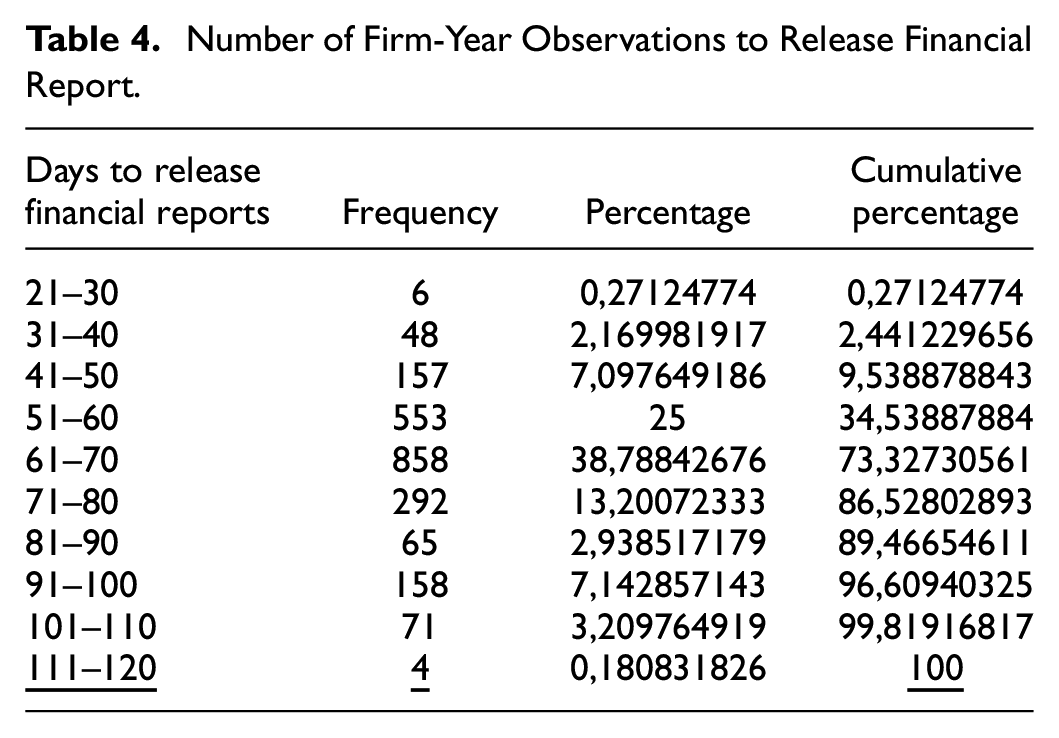

Table 4 shows the percentage distribution of the day intervals in which the companies in our study publish their financial reports. The financial reporting timeliness of the sample companies is shown in the table as 10-day period. According to this table, 38% of the companies in the sample declare their financial reports in the range of 61 to 70 days, 21% in the range of 51 to 60 days, and 14% in the range of 71 to 80 days.

Number of Firm-Year Observations to Release Financial Report.

Legislation regarding financial reporting timeliness differs from country to country. The obligations to report the annual financial statements of companies traded on the stock exchange in Turkey, which constitute the sample of our study, are specified in the Capital Markets Board (CMB). According to the “Communiqué on Accounting Standards in the Capital Markets,” published by the Capital Markets Board (CMB) (2013) and valid as of 2005, companies must publish their unconsolidated financial statements within 10 weeks from the end of the fiscal year and their consolidated financial statements within 14 weeks from the end of the financial year. With the communiqué published by the Capital Markets Board (CMB) (2013) and entering into force in 2014, the deadlines were regulated, and it became obligatory for listed companies to publish their annual consolidated financial statements within 70 days and their unconsolidated financial statements within 60 days. With this change, it is seen that the publishing period of financial statements of companies traded on the stock exchange has shortened (CMB, 2013).

When we add the rates between 71 and 120 days in Table 4, we reach a result of 26.67%. This result shows that 26.67% of the companies in the sample do not comply with the CMB rule. In order to improve the quality of investment decisions made by financial statement users, companies should tend to publish their financial statements early. For this reason, all companies traded in Borsa Istanbul, must comply with the rules of the CMB. In order to ensure that all companies comply with this rule, applying legal sanctions to companies may be a solution.

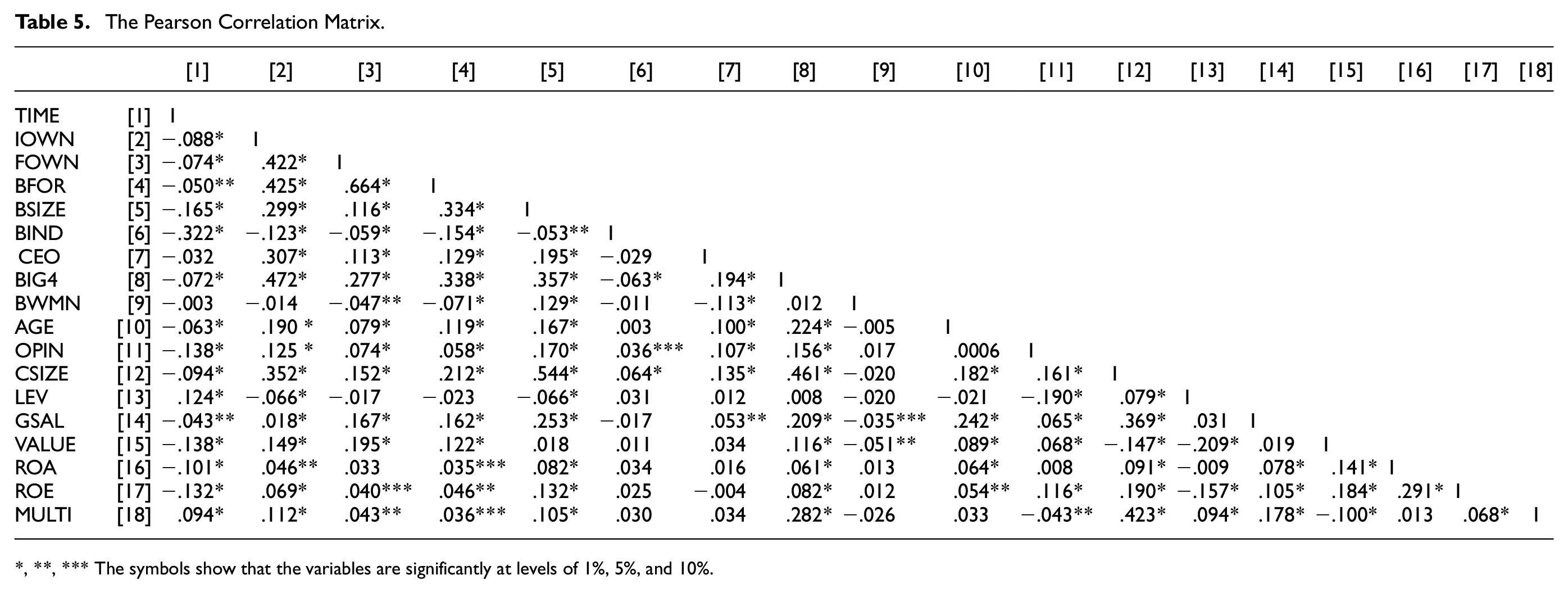

Correlation Analysis

Table 5 below shows the results of the Pearson correlation matrix for the sample. The results show that foreign and corporate ownership structures are statistically significant and negatively related to the timeliness of financial reporting.

The Pearson Correlation Matrix.

, **, *** The symbols show that the variables are significantly at levels of 1%, 5%, and 10%.

Results of Regression

In Table 6, the results of the analysis are presented separately for the three models. In the first model, the timeliness of financial reporting is significant and negatively associated with corporate ownership (p < .05, t = 2.10) and foreign ownership (p < .10, t = 1.69). In the second model, the sectoral reporting delay is statistically significant and negative associated with corporate ownership (p < .10, t = 1.72) and foreign ownership (p < .10, t = −1.79). According to this result, it is expected that the sectoral reporting delay will decrease as the corporate and foreign ownership ratios of companies increase. In the third model, it is seen that the abnormal reporting delay is significantly and negatively related to corporate ownership (p < .01, t = −2.76), but not significantly related to foreign ownership. According to the results of the analysis, the financial reporting timeliness is shortened as corporate ownership increases. The H1 hypothesis is based on these findings. The results obtained by Aksoy et al. (2021), Ishak et al. (2010), and Alfraih (2016) do not support their studies. In addition, the results of the analysis show that as the foreign ownership rate of the companies increases, the financial reporting periods shortens. Based on these findings, the H2 hypothesis is accepted. This result is obtained by Ishak et al. (2010) and Albawwat et al. (2020), who are consistent with the results, while Junaidda (2017) does not support the study.

Results of Regression.

Note. t-Statistics are in parentheses.

, **, and *** indicate two-tailed statistical significance at the 10%, 5%, and 1% levels, respectively.

In all three models, the control variables of the dependent variable were statistically significant and negatively related to the total number of board members, the ratio of independent members of the board of directors, audit opinion, market value or book value, return on equity, and return on assets. statistically significant and positively correlated.

Board size is inversely proportional to financial reporting timeliness. The financial reporting timeliness of companies with an increase in the total number of board members will be shortened. Board size is an important factor in ensuring that financial reports are presented to shareholders in a timely and effective manner. Therefore, the obtained result confirms our predictions, and Ibadin et al. (2012) and Olabayo et al. (2018) support their work. The rate of independent board members is inversely proportional to financial reporting timeliness. As the ratio of independent members of the board of directors increases, the timeliness of the financial reporting of companies will shorten. Considering that independent members of the board of directors are perceived as a tool to monitor management behavior (C. J. P. Chen & Jaggi, 2000), this result is expected. The obtained result supports the study of Abdelsalam and Street (2007), who argue that the presence of independent members of the Board of Directors will contribute to the reduction of agency problems and reduce delays in financial reporting timeliness. Audit report opinion is inversely related to financial reporting timeliness. Companies that receive a positive opinion publish their annual reports more actively. The reason for this is that companies that receive positive audit opinions give a positive signal to the public regarding corporate financial performance. This result confirms our initial predictions, and Habib et al. (2019), Vuran and Adiloğlu (2013), and Nelson and Shukeri (2011) support their work. The market cap/book value ratio is inversely proportional to financial reporting timeliness. Companies with a high market value-to-book value ratio will present their financial reports sooner than other companies. This result is consistent with the findings of the Azami and Salehi (2017) study. Return on assets (ROA), calculated by dividing the net profit with total assets, is inversely proportional to financial reporting timeliness. The financial reporting timeliness of companies with increasing return on assets (ROA) will be shortened. This result is consistent with our initial estimates and supports the work of Al-Ajmi (2008), Vuran and Adiloğlu (2013). Return on equity (ROE), calculated by dividing net income by equity, is inversely proportional to financial reporting timeliness. The financial reporting timeliness of companies with an increased return on equity (ROE) will be shortened. This result is consistent with our initial estimates and supports the study of Al-Ajmi (2008).

In the analysis results, it is seen that financial reporting timeliness is statistically significant and positively related to leverage ratio and multinationality variables. This result can be interpreted as companies that finance most of their assets with debt and multinational companies that have subsidiaries in various countries later on disclosing their financial reports. Since a high leverage ratio, which expresses the ratio of total debt to total assets, is considered bad news, it is expected that companies with high leverage ratios will publish their financial reports later. This result is found in Carslaw and Kaplan (1991), Al-Ajmi (2008), Mert and Cömert (2014), Aksoy et al. (2021), which supports their work. Coordination problems of subsidiaries in different countries of multinational companies and the possibility of slow information flow due to subsidiaries can be seen as the reason for companies to announce their financial reports late.

In addition, the results show that the number of foreign board members, CEO Duality, audit quality, number of female board members, company age, company size, and total sales have no significant effect on financial reporting timeliness.

Corporate ownership and foreign ownership are independent variables used in the analysis. Since there is a predicted high positive relationship between these two variables, two additional regression analyses have been carried out in order to examine the effects of these variables on the timeliness of financial reporting separately. Table 7 shows the regression results where corporate ownership and foreign ownership variables are used separately as independent variables. This result shows that there is a significantly negative relationship between corporate and foreign ownership structures and the timeliness of financial reporting. The results are similar to those in Table 6.

Financial Reporting Time on Corporate and Foreign Ownership.

Note. t-Statistics are in parentheses.

, **, and *** indicate two-tailed statistical significance at the 10%, 5%, and 1% levels, respectively.

Robustness Test

The model’s dynamic establishment with the smallest squares and predictors of fixed effects leads to the association of delayed values with the term “error.” This leads to the endogeneity problem and the deviation of the estimated parameters (Arellano & Bond, 1991). Therefore, it is necessary to determine whether there is an endogeneity issue or not. The generalized method of moments (GMM) is an analysis that controls endogeneity problems (Abbas & Ali, 2022; Abbas et al., 2021; Ali et al., 2022). Robustness analysis was carried out using the GMM method in order to verify the main results and determine whether there was an endogeneity problem. Table 8 shows the results of the GMM analysis. The Corporate ownership and foreign ownership variables have a significant and negative relationship with the timeliness of financial reporting. This result confirms the main regression results. The Arellano-Bond test was also used to confirm that delayed values are not associated with the error term. The results indicate that the zero hypothesis, indicating that the delayed values are not associated with the error term, should be rejected in the first test AR(1) (p = .005) but not in the second test AR(2) (p = .375). Then the Sargan test and the Hansen J-test were applied to assess the validity of the instrumental variables. The Sargan test found a p-value of .003. Therefore, Sargan’s statistics showed that we could reject the zero hypothesis and that our tools were not valid as a result (Sargan, 1958). The Hansen J-test results indicate the opposite of this result. Hansen’s J-test found a p-value of .215, the opposite of this result. Hansen’s J-test found a p-value of .215. Hence, Hansen J statistics shows that we cannot reject the zero hypothesis and that, as a result, our tools are valid (Hansen, 1982). As seen in Table 8, the results of the robustness test indicate that companies with increased corporate ownership and foreign ownership rates will announce financial reports earlier.

GMM Test Results.

Note. t-Statistics are in parentheses.

, **, and *** indicate two-tailed statistical significance at the 10%, 5%, and 1% levels, respectively.

Conclusion

The main factors that determine information asymmetry between information providers and users in capital markets are the timeliness and comparability of financial information. It is especially important for users of financial statements to investigate the factors that affect financial reporting timeliness. This study examines the effect of ownership structure of Turkish companies on financial reporting timeliness. Corporate ownership and foreign ownership variables were used as independent variables. Control variables have been widely dealt with in the form of corporate governance-based variables,, firm-based variables and audit-based variables. Three distinct models have been established to address the timeliness of financial reports from three different perspectives. Regression results show that the timeliness of financial reporting is significant and negatively related to corporate ownership (Abed et al., 2020; Aksoy et al., 2021; Basuony et al., 2016; Ishak et al., 2010). This result, supporting the work of the company, allows us to expect companies with a higher corporate ownership rate to publish their financial statements earlier than other firms. The fact that corporate investors prefer lower information asymmetries accelerates the timely disclosure of financial reports. Alfraih (2016) emphasized that corporate ownership does not have a relationship with the timeliness of financial reporting. Our results do not support Alfraih (2016).

The regression results indicate that the foreign structure is significant and negatively related to the timeliness of financial reporting. This result is consistent with the findings of Albawwat and Alomari (2020). Junaidda (2017) did not find a significant relationship between foreign ownership and financial reporting timeliness. Therefore, this result we obtained does not support the findings of Junaidda (2017). Therefore, the results we obtained do not support the work (Junaidda, 2017). These results show the importance of institutional and foreign investors’ market participation in terms of financial reporting timeliness, especially in developing economies. Financial reporting timeliness is a useful tool in dealing with inefficiencies in capital markets. The findings show that as the corporate ownership and foreign ownership ratios increase, the financial reporting time will shorten, thus contributing to a more functional capital market. For this reason, listed companies must implement policies to attract institutional and foreign investors. In general, the results support both the proxy theory and the asymmetric information theory. In addition, robustness analysis was carried out using the two-stage GMM method, and it was determined that there was no internality problem.

Managerial Implications

This study offers several implications for managers, regulators, and policymakers. Companies that do not present their financial statements in a timely manner may have difficulty finding investors, as investors see timely reporting as an ideal component of corporate governance. The results will help investors, managers, and policymakers make healthier decisions by reducing information asymmetry about the causes of reporting delays. In addition, the results are valuable as they provide the opportunity to compare the results of companies that shorten their financial reporting timeliness with those of other companies. In addition, the results are valuable as they will contribute to a more functional capital market.

Limitations and Future Research

This study is subject to some limitations. First, the fact that our sample consists of non-financial companies traded on the BIST limits the generalizability of the results. In future studies, using the same variables, research that covers only financial companies traded in BIST can be done. Secondly, in our study, we discussed the ownership structure of corporate ownership and foreign ownership. Future studies may consider other ownership structures when examining the relationship of ownership structure to financial reporting timeliness. The pandemic we are experiencing in 2020 has caused economic problems as well as health problems in our country as well as all over the world. The third limitation of the study is that the financial statement data for the years 2020 and 2021 are not included in the study, so the regression results are not inconsistent. Future studies may cover the pandemic period.

Supplemental Material

sj-pdf-1-sgo-10.1177_21582440231207458 – Supplemental material for The Effect of Ownership Structure on Financial Reporting Timeliness: An Implementation on Borsa Istanbul

Supplemental material, sj-pdf-1-sgo-10.1177_21582440231207458 for The Effect of Ownership Structure on Financial Reporting Timeliness: An Implementation on Borsa Istanbul by Beylem Çelik, Gökhan Özer and Abdullah Kürşat Merter in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Approval Statement

Ethics approval was not required for this study.

Supplemental Material

Supplemental material for this article is available online.

Data Availability Statement

Research data are not shared.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.