Abstract

This study examines whether a CEO with a science and engineering background (CEOSEB hereafter) affects green innovation. Data of A-listed industrial firms registered on the Shanghai and Shenzhen Stock Exchanges are analyzed from 2008 to 2018. Findings indicate that CEOSEB has a significant positive impact on green innovation. This research also tests the moderating effect of the firm’s resources, CEO compensation, and media coverage on the CEOSEB and green innovation nexus. Results show that the firm’s resources and media coverage are positive, whereas compensation negatively affects the CEOSEB and green innovation association. Finally, our results depict that the impact is more pronounced in state-owned firms than in private-owned enterprises. Results remain robust to a battery of econometric techniques. These findings offer novel insights into the clean and sustainable development literature from the perspective of the CEO’s educational background.

Introduction

Science has largely improved material well-being but threatens human life with global warming and environmental degradation. China, the world’s production hub, faces global outrage as the country produces more than a quarter of the world’s gas emissions and substantially contributes to climate change and air pollution. Therefore, innovation, especially green innovation (GI hereafter), is inevitable to overcome these challenges (Ferreira et al., 2020; Rehman et al., 2021). GI refers to technological and ecological innovations that comprise products, business models, organizational structure, and processes for waste recycling, energy-saving, and pollution prevention (Schiederig et al., 2012; S. Zhao et al., 2021). The literature shows that various factors such as government legislation, board composition, and top executive experience significantly contribute to GI (Hao et al., 2019; K. He et al., 2021; Usman et al., 2020; S. Zhao et al., 2021). However, the literature lacks evidence on the association between the CEO’s educational background and GI. This study fills this gap by analyzing the effect of a CEOSEB on a firm’s GI.

Upper echelon theory provides theoretical substance to the CEOSEB and GI nexuses. The theory contends that the strategic outcomes of a firm are influenced by the background traits of top-level corporate managers, particularly the CEO (Hambrick & Mason, 1984). The literature substantiates this perspective by presenting empirical evidence that age, educational background, and prior experience of a CEO play a significant role in shaping the decision-making processes of the firm (K. He et al., 2021; Y. Li et al., 2022; Quan et al., 2023; Shahab et al., 2020; Zhou et al., 2021). A key attribute among these traits is a CEO’s education, which affects a CEO’s analytical and psychological abilities. Existing research indicates that a CEO’s educational background and field of specialization have a profound influence on his decision-making. On the one hand, a CEO’s higher-level qualification highly contributes to the strategic direction of the company (Nawaz, 2021). On the other hand, the area of expertise of a CEO is manifested through their strategic choices in the realm of business (Kallias et al., 2023; Nawaz, 2021; Ting et al., 2021).

We extend this stream of research by examining the role of CEOs who are better equipped with science and engineering knowledge in promoting a firm’s GI. We present several arguments for the CEOSEB and GI associations. First, imprinting theory (Marquis & Tilcsik, 2013) proposes that early life imprints (e.g., education) determine an individual’s cognition and subsequent behavior. In this context, science and engineering education imparts concepts that are essential for fostering innovation. In addition, Swift (2018) argues that scientists are generally innovators and enthusiasts serving the public. Moreover, higher and quality education improves one’s value and moral reasoning (Doyle & O’Flaherty, 2013; Keller et al., 2007). Therefore, a CEOSEB tends to be greener. Second, a CEOSEB’s distinct social capital enables him to easily access important external resources such as scientific resources and technical know-how. Furthermore, a CEOSEB can attract the funds of eco-friendly investors and ease the financial constraints of the firm. Finally, the top executive cadre provides a CEOSEB’s strategic position to make reasonable judgments on the nature and long-term significance of GI for firm value. Moreover, technical knowledge and the CEO position facilitate the initiation and execution of GI. Thus, a CEOSEB offers a promising avenue for GI.

This study explores the relationship between CEOSEB and GI using data on Chinese manufacturing A-share listed companies from 2008 to 2018. The findings show that a CEOSEB has a significant positive effect on a firm’ GI. In addition, the findings reveal that a firm’s resources and media coverage positively moderate the association between CEOSEB and GI, whereas CEO compensation negatively moderates the association between CEOSEB and GI. Finally, the results indicate that the association between CEOSEB and GI is more pronounced in SOEs than in POEs.

This study adds several contributions to the existing literature. First, unlike previous research that examined external factors such as government regulations and public pressure in connection to GI, we consider CEOSEB as a determinant of GI. Despite its profound relevance, the effect of a CEOSEB on environment-friendly innovations remains unexplored. Our findings corroborate the argument that the CEOSEB has a significant positive influence on GI. The findings show that reducing carbon footprints requires the right CEO, that is, CEOSEB. Second, to fill a gap in the literature, this study examines the moderating effect of institutional factors such as firm resources, CEO compensation, and external governance mechanisms (i.e., media coverage) on CEOSEB and GI association. The study also deepens our understanding of whether science and engineering are beneficial or detrimental. Firm-level empirical evidence confirms that scientific and engineering knowledge, along with necessary power, such as a CEO position, contributes to human well-being by safeguarding the environment. Finally, our study provides empirical evidence from China, which has a distinct corporate ownership landscape and faces serious environmental problems. Therefore, the findings from advanced regions may not be generalized in the Chinese context.

The rest of the study continues as follows. Section 2 discusses the institutional settings of China. Section 3 deals with the extant literature and hypothesis development. Section 4 describes the methodology of the study, while empirical results are reported in Section 5. Section 6 presents the robustness checks. Section 7 addresses endogeneity concerns. Finally, Section 8 concludes the study.

Institutional Background in Chinese Settings

Soon after the opening of the economy in the 1990s, China became a world factory. The remarkable growth rate helped the country accumulate huge amounts of wealth and attract hefty foreign investment. However, China is paying the price for its growth-driven policy in terms of environmental deterioration, heavy pollution, and rising carbon emissions. The amnesty primarily allowed the producers to use fossil fuels (e.g., coal and crude oil) in their production process (Shahab & Ye, 2018). Consequently, China emerged as the world’s largest carbon dioxide emitter, producing more than one-quarter of global emissions. The internal deteriorating situation and external call for environmental protection compelled Chinese policymakers to formulate sustainable and eco-friendly policies. More specifically, Chinese authorities framed the “Environmental Protection Law,”“State Environmental Protection Administration,” and “Guidelines on Listed Companies’ Environmental Information Disclosure;” then, they signed the United Nations Global Reporting Initiative to mitigate environmental decay (Shahab et al., 2020). China also signed the “Paris Accords” in 2016. However, implementing these policies remains a challenge due to weaker corporate governance mechanisms and top management commitment (Shahab & Ye, 2018). A CEO position is the corporate’s highest ladder and would therefore have a significant effect on the implementation of regulators’ policies. CEOs in Chinese firms have different appointing authorities and therefore pursue different objectives. For instance, a large number of CEOs in SOEs are government officials and follow the government’s socio-political agenda, while CEOs in POEs are shareholders’ agents and mainly work for their wealth maximization. Thus, the peculiar institutional settings and the country’s environmental performance provide an opportunity to investigate the factors that contribute to GI.

Literature Review and Hypothesis Development

Sustainable-oriented innovations such as GI are imperative for economic and environmental development. However, GI is a complex phenomenon encompassing the intentional change in a company’s philosophy, product, process, and structure to control environmental degradation and climate change without compromising its economic benefits (Schiederig et al., 2012; S. Zhao et al., 2021). Policy formulation and resource allocation are the prerogatives of top executives in corporate settings. Therefore, GI may significantly depend on the personal acumen and foresight of the firm’s top management. Extant literature shows substantial empirical evidence on various attributes of CEO personality such as gender, hubris, education, and past working experience on GI (Hao et al., 2019; K. He et al., 2021; Quan et al., 2023). Similarly, Zhou et al. (2021) suggest that highly educated CEOs engage more in environment-friendly innovations. However, the literature lacks empirical evidence on whether a CEO’s education type affects the firm’s GI.

Upper echelon theory (Hambrick & Mason, 1984) provides the theoretical underpinning to the association between CEOSEB and GI. The theory states that a company’s strategic direction can be predicted by knowing its top management’s background characteristics. A key attribute among these features is education, which influences one’s analytical and psychological capabilities. A CEO accumulates professional knowledge in his educational career that affects his cognition and professional judgment. Prior studies confirm that a CEO’s higher qualification positively contributes to the firm’s GI (Zhou et al., 2021). The type of CEO’s education also affects his decisions. To illustrate, CEOs with business degrees highly affect IPO performance (Kallias et al., 2023), financial inclusion (Nawaz, 2021), corporate social responsibility (Sun et al., 2021), environmental disclosure (Lewis et al., 2014), risk-taking (Ahmed & Kumar, 2023), and earnings management (Qi et al., 2018). Similarly, CEOs with an engineering background positively influence corporate innovations (Ting et al., 2021) and research and development (R&D) spending (Jaggia & Thosar, 2021) but negatively affect a firm’s cash holdings (Mun et al., 2020). Moreover, J. Zhao et al. (2023) document that firms with medical background CEOs had a lesser decline in their stock returns during the recent pandemic.

In the same vein, we consider that a CEOSEB would positively contribute to the corporate GI. Science has a paradoxical effect on the environment: it adds to the environment’s ailments but also provides remedies for them. We postulate a positive effect because science subjects not only form a considerable portion of concepts that underpin environmental problems but are also essential for innovations, including GI. Education and experience imprint one’s cognition and are reflected in subsequent behavior. Moreover, higher and quality education improves one’s values (Keller et al., 2007) and moral reasoning (Doyle & O’Flaherty, 2013). Therefore, a CEOSEB would assume additional responsibility to sense environmental decay and put an expert hand on it. Second, a CEOSEB may have good social capital. Personal network allows him to find and access critical external resources such as research and development (R&D) teams and scientific knowledge. Moreover, a CEOSEB can alleviate the financial constraints of the firm by attracting the resources of eco-friendly investors. Therefore, firms with CEOSEB would have a comparative advantage in terms of GI. Third, strategic position and expertise provide CEOSEB with a conducive environment to establish an excellent R&D team and make reasonable judgments on the long-term benefits of GI for the organization. Moreover, technical knowledge makes it easier to initiate, communicate, and implement a green idea. Thus, summing up the above discussion, we hypothesize that CEOSEB could positively contribute to GI.

Moderating Role of a Firm’s Resources (FR)

Managers rely on firm-level resources, both tangible and intangible, that have been built over the lifetime of the business to extract value for the firm. Prior research shows that a FR bring competitive advantage (Lee & Lévesque, 2023), superior performance (Andersén, 2011), affect returns to market deployment (Slotegraaf et al., 2018), and influence the choice of business strategy (Edelman et al., 2002). Innovations, especially the GI, are frequently riskier and require distinctive resources. Extant literature shows that various firm-based resources such as human capital, internally sourced research and development spending, employees’ training, and willingness to exchange ideas have significant effects on a firm’s innovation (Anzola-Román et al., 2018; Fonseca et al., 2019; Julienti et al., 2010; van Uden et al., 2016; Wan et al., 2005). However, GI may be more challenging as it seeks motivation and commitment from all levels of corporate employees. Therefore, the workforce of an organization is often labeled as the most critical resource of any organization than any other form of resource (Gupta & Singhal, 2016; Maier et al., 2014).

A firm’s human resource is the main factor that searches, absorbs, and generates new technologies (Maier et al., 2014). A larger firm with more employees would have more talent and capacity to initiate and assimilate GI activities. Similarly, employees are the agents of society in corporate settings. A firm with a larger employee set represents a bigger part of society. If a firm fulfills its objectives at the cost of society, workers put pressure on the corporate top executives to align the interests of both. Therefore, we argue that a FR, that is, human resources, could positively moderate the nexus between CEOSEB and GI. Hence, our second hypothesis is as follows:

Moderating Role of CEO Compensation (CCOMP)

The board of directors appoints a firm’s CEO and determines his remuneration. Compensation fixation is one of the critical decisions and has fascinated shareholders, regulators, and academia in the recent past, especially after the eruption of high-profile fraud cases such as Enron and WorldCom (e.g., Hill et al., 2016; Zoghlami, 2021). The appropriate compensation package strengthens the principal-agent relationship and aligns the interests of managers with those of the shareholders. Owners duly compensate the executives if they add value to the firm (Sheikh et al., 2017). However, the agency conflict suggests that managers are interested in building their empire instead of pursuing the shareholders’ interests. The rent-seeking behavior of managers is backed by empirical findings suggesting that excess payment to CEO does not motivate him to pursue the shareholders’ interest wholeheartedly (Hill et al., 2016; Zoghlami, 2021). Likewise, powerful CEOs bargain effectively and receive more compensation than less powerful CEOs (Song & Wan, 2019). Consequently, contemporary compensation packages consist of incentives that align the managers’ interests with the shareholders and aim to mitigate agency costs.

However, an appropriate compensation package may not encourage GI. First, a CEO works for shareholders’ wealth maximization rather than stakeholders’ interests or mitigating environmental degradation. The literature shows that the board discipline managers if they act against the shareholders’ interests (Hazarika et al., 2012). Second, CCOMP package mostly consists of equity-based incentives. It encourages him to increase the firm’s value, which positively affects his compensation. Finally, a CEO is appointed for a shorter period; whereas innovation, particularly GI, requires a long-term commitment. Therefore, a CEO attempts to secure maximum compensation for himself as his next assignment pays a premium on it (Bragaw & Misangyi, 2017). Thus, CCOMP fulfills CEOs’ and/or shareholders’ objectives and forgoes the GI. Hence, we postulate that the CEO’s higher compensation hurts the CEOSEB and GI nexus.

Moderating Role of Media Coverage (MC)

Media has gained an important position in society due to its dominant role among information intermediaries. It is an informal external governance mechanism and acts as a watchdog over corporate managers (Wang & Zhang, 2021). Prior studies show that MC is significantly associated with firm performance (Dong et al., 2022), stock price crash risk (Wu et al., 2022), and investment efficiency (Gao et al., 2021). Given that the corporate sector is the main contributor to pollution, media attention to the firm’s environmental behavior has been growing rapidly.

MC may alleviate the firm’s environmental bad practices. First, the media tends to report negative information because it attracts the attention of the masses. Public censure not only hurts the focal firm’s goodwill but also negatively affects the CEO’s job security and compensation (Bednar, 2012). Therefore, managers would attempt to avoid activities that exacerbate environmental problems. Second, the media courtesy of a firm’s investment in GI pressurizes other firms’ behavior, including the rivals. The literature also suggests that knowledge spillover occurs in innovations (Matray, 2021). Therefore, any GI initiative of a peer firm would create a favorable atmosphere for environment-friendly activities. Finally, prior studies show that MC significantly influences firm capital allocation decisions (Bednar et al., 2013; Gao et al., 2021) and GI (Z. Chen et al., 2022). Thus, we assume that MC would positively affect the CEOSEB and GI relationship.

CEOSEB, State and Private-Owned Firms, and GI

Chinese public listed firms have a more distinctive ownership structure than their counterparts in other countries and are divided into state-owned enterprises (SOEs) and private-owned enterprises (POEs) (Hu et al., 2021; Zhang et al., 2019). POEs solely work for shareholders’ wealth maximization, whereas SOEs seek to fulfil their political and economic goals. Unique to its structure, SOEs’ top management has political affiliation and easy access to resources (Cai et al., 2020; Faccio, 2006). Ample economic resources enable SOEs to undertake risky projects such as innovation. In addition, the local officials’ political promotion is associated with their eco-friendly activities. Moreover, SOEs are subject to heavy government intervention due to their close association with national policy. For example, the Chinese government’s initiative of sustainable and green development put extra pressure on SOEs to undertake and pursue environment-friendly technologies (Pan et al., 2021). Likewise, based on institutional theory, firms run and regulated by government officials and agencies face more regulatory and normative pressure than others. By contrast, POEs undergo less government intervention and pay extra attention to their economic objectives. Thus, compliance and legitimacy force SOEs to engage more in environment-friendly activities. Hence, we assume that the positive association between CEOSEB and GI would be more potent in SOEs than POEs (Figure 1).

Conceptual framework.

Methodology

Sample and Data

Our initial sample consists of non-financial A-share firms listed on the Shanghai and Shenzhen Stock Exchanges for the period from 2008 to 2018. The choice of manufacturing firms is based on the notion that they face greater ecological pressure as they consume extra energy and engage mostly in pollution-driven production processes. This study limits the sample period from 2008 to 2018 for several reasons. First, before 2008, different corporate governance changes were made in China, such as the adoption of new accounting standards (IFRS) in 2005 and the implementation of non-tradable shares reforms in 2006. Second, the data on GI for more recent years were inaccessible restricting the sample period to 2018. Following prior studies, we exclude financial services firms due to their unique regulatory mechanisms, firms with abnormal trading status such as special treatment firms (firms that announce losses in any two consecutive years), particular treatment firms (special treatment firms that fail to revive within the next 2 years), and firms with missing data (Liao et al., 2019; Shahab et al., 2020). The final sample consists of 11,126 firm-year observations. We collect firms’ financial, governance, and CEO characteristics data from the China Stock Market and Stock Market database. The green patent data are obtained from the China National Intellectual Property Administration (CNIPA).

Variable Measurement

Measurement of GI

The dependent variable of the study is GI. For measurement purposes, we use green patent data because they are primarily related to environment-friendly creation and reflect a firm’s GI abilities. Furthermore, patents are usually granted according to a set of criteria. Moreover, a large number of studies use the number of green patents as a proxy of a firm’s GI proxy (e.g., Huang et al., 2021; X. He & Jiang, 2019). Therefore, following Huang et al. (2021), we use the natural logarithm of the green patent plus one to calculate a firm’s GI.

Measurement of CEOSEB

An individual can receive three levels of education: Bachelor (Undergraduate), Master, and Doctoral (PhD). These different levels of education encompass different levels of knowledge and skills. Extant literature also advocates that higher levels of CEO education substantially improve a firm’s performance (Kallias et al., 2023; Nawaz, 2021). Likewise, a CEO’s field of education is reflected in his corporate decisions (Kallias et al., 2023; Nawaz, 2021; Ting et al., 2021). Therefore, in line with prior studies, we target the highest level of education, Ph.D., in this study (Z. He & Hirshleifer, 2022; Urquhart & Zhang, 2022). More specifically, a CEO background will be considered scientific if his qualification is PhD in science or engineering subjects. Thus, CEOSEB is a dummy variable that takes the value of 1 if the CEO has a doctoral degree in science or engineering; otherwise, 0.

Moderating Variables

We use three moderators in this study: FR, CCOMP, and MC. Extant literature suggests that FR affect innovations (Fonseca et al., 2019). Therefore, this study analyzes the moderating role of the FR in CEOSEB-GI relationships. FR is equal to the natural log of firm employees. Second, the CCOMP has consequences for organizational innovation (Mazouz & Zhao, 2019) and is measured as the natural log of the total salary paid to the CEO annually. Finally, MC is labeled as an external governance mechanism. We consider the number of media reports as a proxy for MC. The data are collected from the Chinese Research Data Services Database (CNRDS). The financial news section (CCNFD) of the CNRDS covers more than 600 newspapers published in China. However, financial reports mostly come from the eight major newspapers, namely, China Securities News, China Business News, Shanghai Securities News, Economic Observer, First Financial Daily, Securities Daily, 21st Century Business Herald, and Securities Times. Therefore, following Z. Chen et al. (2022), we retrieved firm-specific reports from these eight newspapers. For measurement purposes, we take the natural log of the number of media reports plus one.

Control Variables

Following prior studies (Huang et al., 2021; Wang & Jiang, 2021), we control for firm, board, and CEO attributes that may influence GI. At the firm level, firm size (Size) is controlled because González-Benito and González-Benito (2010) argue that large enterprises have economies of scale, market dominance, more resources, and a stronger influence on GI. We control leverage (LEV) to account for capital structure as it affects the firm’s capacity to make green investments. Next, we control firm’s profitability (ROA) because more profitable firms face greater pressure to engage in environmental activities (M. Jiang et al., 2020; D. Li et al., 2018). Prior research reveals that capital intensity highly affects company green strategy (Russo & Fouts, 1997). Therefore, we control capital intensity (CAPEX). We also control for research and development intensity (R&D) which affect a firm’s commitment to innovation. Finally, following Tan and Zhu (2022), we also control cash flows (FCF) and audit quality (Big4).

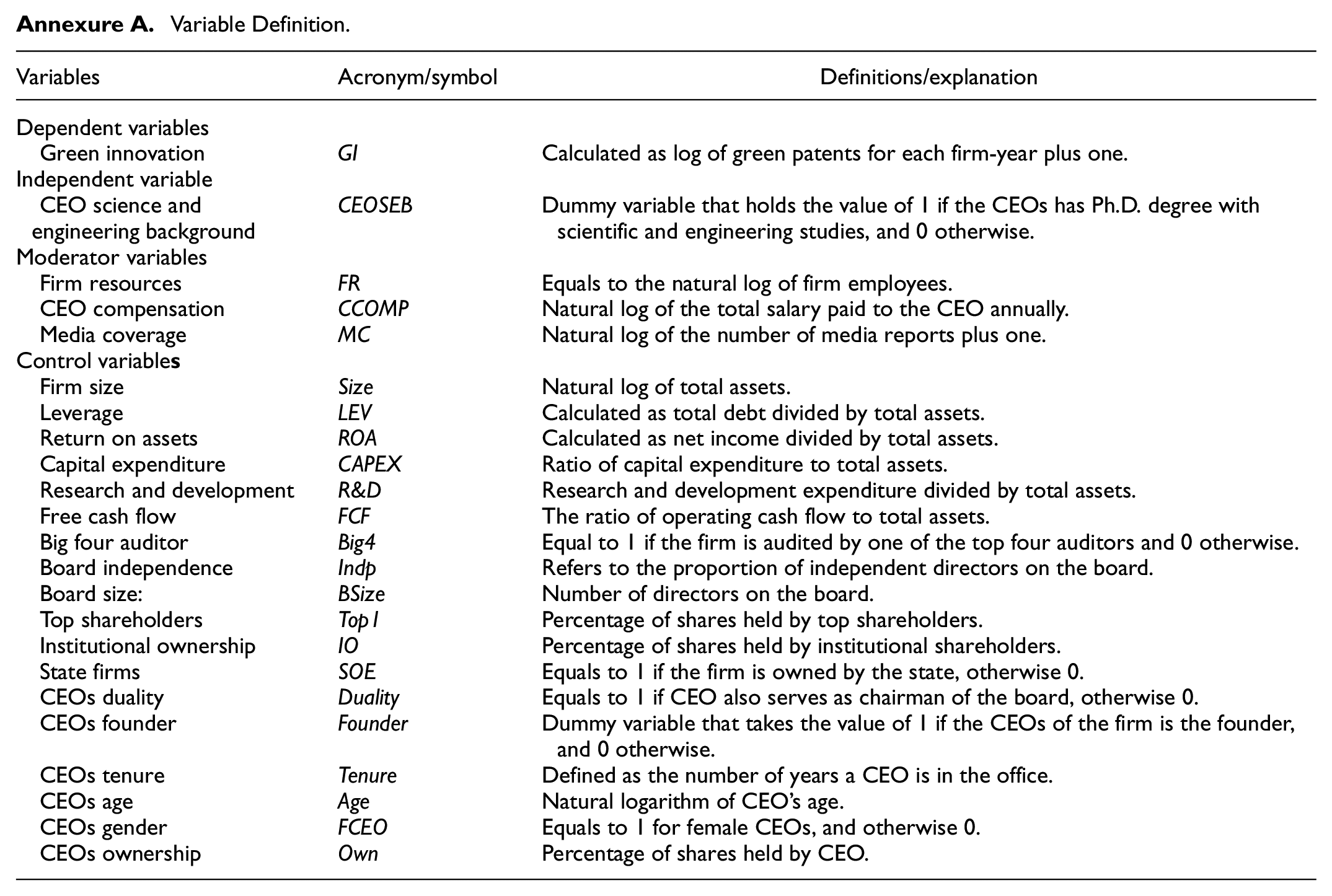

At the board level, we control for board size (BSize) and board independence (Indep) because larger boards with a higher fraction of outside directors are suggested to contribute to higher environmental and GI performance (Zhang et al., 2021). The literature also suggests that greater ownership concentration (Top1) and institutional ownership (IO) affect environmental performance (Earnhart & Lizal, 2006; Huang et al., 2021; Rong et al., 2017). Therefore, the study controls for Top1 and IO. Finally, we control CEO duality (Duality), CEO’s age (Age), CEO gender (FCEO), CEO ownership (Own), and CEO founder (Founder) because they contribute to the firm’s environmental performance (N. Jia, 2018; Liu, 2018; Zhang et al., 2021). We winsorize all financial variables at 1% and 99% levels to reduce the effect of extreme values. Please refer to Annexure A for the variables’ definitions.

Empirical Models

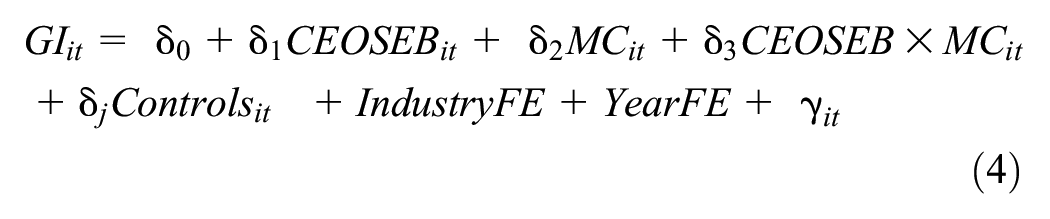

To test the impact of CEOSEB on GI, we estimate the following regression model:

where

Next, we test the validity of our H2, H3, and H4 by employing the following models:

Model (2) investigates the moderating role of FR in the association between CEOSEB and GI. The interaction term, that is,

Results

Descriptive Statistics and Correlation

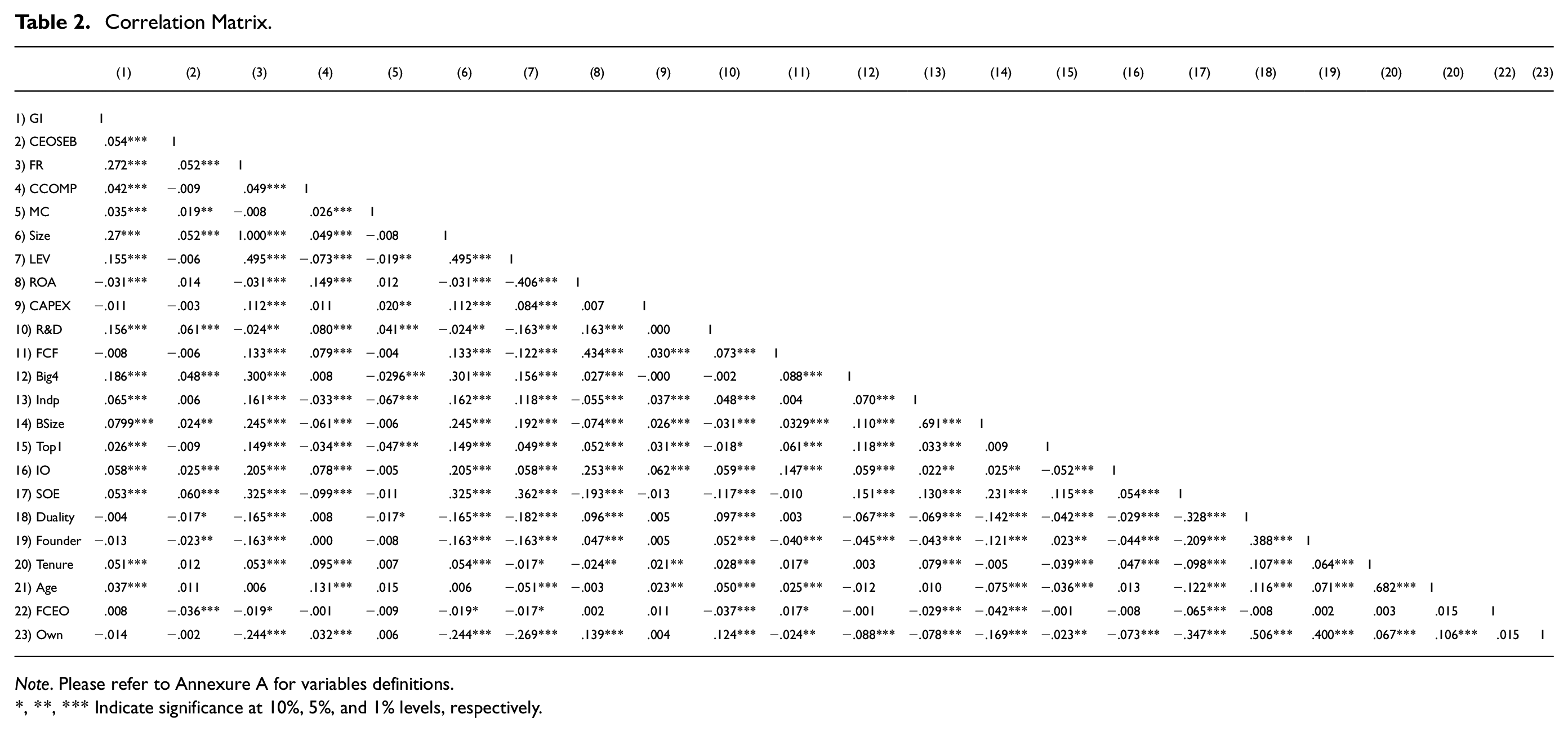

We report summary statistics for the variables in Table 1. The mean values of GI and CEOSEB are 0.302 and 0.054, with standard deviations of 0.695 and 0.226, respectively. Likewise, the averages of FR, CCOMP, and MC are 7.788, 12.908, and 0.144, respectively. Finally, our control variables, which consist of Size, LEV, ROA, CAPEX, R&D, FCF, BIG4, Indp, BSize, Top1, IO, SOE, Duality, Founder, Tenure, Age, FCEO, and Own have a mean value of 21.936, 0.392, 0.048, 0.045, 0.017, 0.048, 0.054, 3.589, 9.159, 0.173, 0.068, 0.345, 0.335, 0.070, 3.137, 0.704, 0.047, and 0.064, respectively. Table 2 depicts the Pearson’s correlation matrix of the study. The relationship between GI and CEOSEB is 0.054 which is significantly positive.

Summary Statistics.

Note. Table 1 shows descriptive statistics of the variables. Please refer to Annexure A for variables definitions.

Correlation Matrix.

Note. Please refer to Annexure A for variables definitions.*, **, *** Indicate significance at 10%, 5%, and 1% levels, respectively.

Main Analysis

Table 3 reports the main results of the study. The estimation of all the models in Columns (1) to (6) incorporates the control of firm-specific factors, boardroom features, and top managers’ personality attributes; while accounting for industry and year-fixed effects. Model (1) reports the effect of CEOSEB on GI. The coefficient of CEOSEB is 0.051, indicating a statistically significant positive relationship at the 5% significance level. This finding suggests that CEOSEB has a determining effect on a firm’s GI. It is in line with our argument that science and engineering education imprints a CEO’s cognition and subsequent behavior. Consequently, H1 is corroborated. These results support earlier research (Huang et al., 2021; Quan et al., 2023; Ting et al., 2021; Zhou et al., 2021) and are in line with imprinting and upper-echelon theories (Hambrick & Mason, 1984; Marquis & Tilcsik, 2013).

CEOSEB, FR, CCOMP, MC, SOEs and POEs, and Green GI.

Note. This table reports main results from OLS regression. Model (1), (2), (3), and (4) repots the results of hypotheses 1, 2, 3, and 4, respectively. Hypothesis 5 is separately tested in Model (5) and (6). Variables are defined in Annexure A. The t-statistics in parentheses are calculated based on standard errors clustered at the firm level.

, **, *** Indicate significance at 10%, 5%, and 1% levels, respectively.

Next, we add interaction terms between CEOSEB and the moderating variables, that is, FR, CCOMP, and MC, to test H2, H3, and H4. Column (2) shows the moderating effect of a FR on CEOSEB and GI relationships. The coefficient of CEOSEB*FR (0.055) is positive and significant at the 5% level, indicating that a FR the positive relationship between CEOSEB and the firm’s GI. Thus, H2 is accepted. These results are similar to prior studies (Gupta & Singhal, 2016; Maier et al., 2014). Likewise, Column (3) shows the moderating effect of CCOMP on the CEOSEB-GI association. The coefficient estimate for the variable CEOSEB*CCOMP (−0.038) exhibits a negative sign and demonstrates statistical significance at the 1% level. This finding illustrates that an increased CCOMP package can potentially reverse the positive impact of CEOSEB on GI, resulting in a negative outcome. These results support our arguments that higher compensation of CEO either shows entrenched behavior by the CEO or aligns the interests of managers and shareholders only and offers nothing for GI to nurture. Therefore, H3 is supported.

Column (4) reports the moderating effect of MC on CEOSEB and GI relationships. The result proves that MC positively moderates the relationship between CEOSEB and GI. Specifically, the coefficient of CEOSEB*MC is 0.405, which is significantly positive, advocating that MC spurs the firm’s GI. This finding is in line with our argument that MC is an external governance mechanism and acts as a watchdog over a firm’s top managers. Thus, H4 is accepted. This finding is consistent with earlier studies (M. Jia et al., 2016; Wang & Zhang, 2021).

Finally, Columns (5) and (6) report the CEOSEB impact on GI in SOEs and POEs, respectively. We investigate this aspect because firms under state and private ownership have distinct organizational goals and institutional arrangements. The results show that the effect of CEOSEB on GI is pronounced only in SOEs. Specifically, the coefficient of CEOSEB is statistically significant in Column (5). The positive relationship between CEOSEB and GI in SOEs supports the Chinese government’s environmental efforts and validates our arguments that state ownership puts extra pressure on CEOs to pursue eco-friendly policies. Thus, H5 is accepted. These findings are consistent with prior studies (Ding et al., 2022; Wang & Jiang, 2021).

Robustness Check

To examine the robustness of our findings, we employed two alternative econometric tests: Poisson and Negative Binomial regression models. We use the Poisson regression model because it provides unbiased results. Additionally, this model is extensively used in the GI literature (Berrone et al., 2013; Huang et al., 2021). We also use the Negative Binomial regression model. The results of both models are given in Table 4 and are consistent with our earlier findings, that is, Table 3, signifying that CEOSEB has a significant positive impact on GI.

Robustness Analysis: using Poisson and Negative Binomial Models.

Note. This table reports the results of Poisson and Negative Binomial regression models. Panel A (Models (1)–(4)) reports the results of hypotheses 1–4, while Models (5) and (6) shows the results in SOEs and POEs respectively, using the Poisson regression estimation techniques. Likewise, Panel B (Models (7)–(12)) shows the Negative Binominal regression results of all our hypotheses. Variables are defined in Annexure A. The t-statistics in parentheses are calculated based on standard errors clustered at the firm level.

, **, *** Indicate significance at 10%, 5%, and 1% levels, respectively.

Endogeneity Concerns

We use several econometric techniques to address endogeneity concerns. First, we estimate the lead-lag regression model. We lag all the explanatory and moderating variables by a year and estimate the model. This approach is extensively used in the literature (e.g., C. Chen et al., 2016; Usman et al., 2018). The results in Panel A of Table 5 confirm our key findings in Table 3. Second, we employ a generalized method of moment (GMM). GMM is a powerful technique because it pools the observed economic statistics with information in population moment conditions and generates reliable estimates of the unknown parameters. We estimate the system GMM (Arellano & Bover, 1995; Blundell & Bond, 1998) to mitigate dynamic endogeneity, unobserved heterogeneity, and simultaneity. System GMM uses first- and second-level differences of variables as instruments for the equation in level. The residuals in the first-level difference may be serially correlated by construction; however, it cannot be an issue in the second-level difference. Panel B of Table 5 reports the GMM results, which are consistent with our main findings as shown in Table 3. Third, we run 2SLS to remove unwarranted endogeneity arising from the correlation of the regressed variable’s error term with the explanatory variables. 2SLS uses an instrumental variable (IV) approach that correlates the IV with CEOSEB but not with the residuals of the GI. This technique alleviates any endogeneity that arises from omitting variables, measurement error, and reverse causality (Angrist & Krueger, 2001). Panel C of Table 5 depicts the results which support our earlier findings. For brevity, we only report the main findings of these tests.

CEOSEB, FR, CCOMP, MC, SOEs and POEs, and GI.

Note. This table shows the results of lag of independent variables, GMM, and 2SLS in Panels A, B, and C, respectively. Variables are defined in Annexure A. The t-statistics in parentheses are calculated based on standard errors clustered at the firm level.

, **, *** Indicate significance at 10%, 5%, and 1% levels, respectively.

Finally, we estimate propensity score matching (PSM). PSM compares the treatment group with the control group based on propensity points. The possibility of model misspecification increases as the experimental group becomes dissimilar. PSM mitigates this issue by reducing reliance on the specification of correlation between the variables (Rosenbaum & Rubin, 1983). Hence, PSM enhances the reliability of the estimates. Table 6 shows the results of PSM and supports our main finding that CEOSEB has a significant positive impact on GI.

Using PSM.

Note. This table shows the results of PSM. Variables are defined in Annexure A. The t-statistics in parentheses are calculated based on standard errors clustered at the firm level.

, **, *** Indicate significance at 10%, 5%, and 1% levels, respectively.

Conclusion

This study aims to investigate whether CEOSEB contributes to a firm’s GI. We examine Chinese manufacturing firms listed on the Shenzhen and Shanghai Stock Exchanges from 2008 to 2018. Industrial firms are sampled owing to their higher energy consumption and pollution-driven activities. The findings show that CEOSEB has a significant positive effect on the firm’s GI, supporting upper echelon theory and the extant literature (Hambrick & Mason, 1984; Quan et al., 2023; Zhou et al., 2021). In addition, we tested the moderating effect of FR, CCOMP, and MC on the association of CEOSEB and GI. The empirical evidence suggests that FR strengthen the relationship between the CEOSEB and GI. Likewise, the CEO’s higher compensation package turns the positive effect of CEOSEB on GI into a negative one, indicating the entrenched behavior of top executives. Furthermore, MC has a positive effect on the CEOSEB-GI relationship. This finding is in line with prior studies’ argument that MC acts as an external corporate governance mechanism over corporate top managers. Finally, the study examines whether ownership structure matters in terms of CEOSEB and GI relationships. Therefore, we estimate separate regressions for SOEs and POEs. The findings reveal that the impact of CEOSEB on GI is significant in SOEs only. The results confirm that legitimacy and compliance forces support the Chinese government green development’s drive. Several tests, such as lag of independent variables, GMM, 2SLS, and PSM, are estimated to mitigate the endogeneity concerns. The results remain robust, complementing our argument that CEOSEB acts as a determinant of GI. The study offers several theoretical contributions and policy implications.

Theoretical Contribution

Our study provides several theoretical contributions. First, based on upper echelon theory, it enriches the green and sustainable development literature by suggesting a new determinant, that is, CEOSEB, for GI from inside the organizational factors. Nevertheless, contemporary literature reveals that top management background characteristics significantly affect a firm’s strategic outcomes (e.g., Shahab et al., 2020; Zhou et al., 2021). However, none of the existing studies investigated the CEOSEB impact on GI in the firm’s settings. Our empirical results fill this gap. Second, we extend the literature by analyzing the moderating impact of a firm’s internal factors, such as FR and CCOMP and external governance mechanism, that is, MC, to highlight the factors that positively (negatively) affect the CEOSEB-GI association. In support of our hypotheses, we find that the FR and MC have significant positives, whereas CCOMP has a negative moderating impact on the association between CEOSEB and GI. Finally, we augment the literature by providing empirical evidence from a distinctive economy where the corporate governance mechanism is weaker, environmental problems are severe, and the economy is in transition from a centrally planned to the market-based economy.

Practical Implication

The findings of our study have several important implications for environmental management in China. First, the environmental degradation can be controlled through the encouragement of executives who possess degrees in science and engineering to ascend to higher positions within business hierarchies. A CEOSEB possesses the required knowledge, power, and access to the critical external resources that are imperative for GI. Second, our findings highlight that a robust governance mechanism is the need of the hour for the successful implementation of sustainable development programs. To demonstrate, a positive significant effect of CEOSEB on GI in SOEs and the insignificant effect in POEs raise questions regarding the quality of governance in the country. Sturdy governance rules will compel entrenched managers to align their firms’ objectives with the government and society. Third, our study suggests that deteriorating environmental situation in the country can be controlled by encouraging the media to cover the firms’ activities. Through the formulation of media-friendly policies, the country’s corporate governance deficiencies can be minimized. Finally, our study reveals serious issues in the country’s top management remuneration regulations. For example, our findings show that higher remuneration exacerbates environmental problems because it turns the positive effect of CEOSEB on GI into a negative and hence needs to be aligned with the eco-friendly strategy.

Limitations and Future Research

The study has several limitations that provide an opportunity for further research. To illustrate, we do not consider the quality of CEO education and GI. The type of institution from which one obtains his degree may have significant implications for GI. Likewise, a CEO’s professional experience in middle management may affect his strategic choices. Furthermore, the scope of the study excludes the value of the GI for firms and society. The study also ignores whether CEOSEB brings GI to the product(s), business model, organizational structure, or processes. In addition, we do not compare the effect of CEOSEB with those who lack such a background. Finally, our study does not highlight the appropriate level of GI that ensures environmental safety without hurting the shareholders’ wealth maximization objective.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440241232767 – Supplemental material for CEO’s Science and Engineering Background and Green Innovation: Evidence From China

Supplemental material, sj-docx-1-sgo-10.1177_21582440241232767 for CEO’s Science and Engineering Background and Green Innovation: Evidence From China by Aurang Zeb, Irfan Ullah, Amjad Iqbal, Mohib Ur Rahman and Shahab Aziz in SAGE Open

Footnotes

Appendix

Variable Definition.

| Variables | Acronym/symbol | Definitions/explanation |

|---|---|---|

| Dependent variables | ||

| Green innovation | GI | Calculated as log of green patents for each firm-year plus one. |

| Independent variable | ||

| CEO science and engineering background | CEOSEB | Dummy variable that holds the value of 1 if the CEOs has Ph.D. degree with scientific and engineering studies, and 0 otherwise. |

| Moderator variables | ||

| Firm resources | FR | Equals to the natural log of firm employees. |

| CEO compensation | CCOMP | Natural log of the total salary paid to the CEO annually. |

| Media coverage | MC | Natural log of the number of media reports plus one. |

| Control variable |

||

| Firm size | Size | Natural log of total assets. |

| Leverage | LEV | Calculated as total debt divided by total assets. |

| Return on assets | ROA | Calculated as net income divided by total assets. |

| Capital expenditure | CAPEX | Ratio of capital expenditure to total assets. |

| Research and development | R&D | Research and development expenditure divided by total assets. |

| Free cash flow | FCF | The ratio of operating cash flow to total assets. |

| Big four auditor | Big4 | Equal to 1 if the firm is audited by one of the top four auditors and 0 otherwise. |

| Board independence | Indp | Refers to the proportion of independent directors on the board. |

| Board size: | BSize | Number of directors on the board. |

| Top shareholders | Top1 | Percentage of shares held by top shareholders. |

| Institutional ownership | IO | Percentage of shares held by institutional shareholders. |

| State firms | SOE | Equals to 1 if the firm is owned by the state, otherwise 0. |

| CEOs duality | Duality | Equals to 1 if CEO also serves as chairman of the board, otherwise 0. |

| CEOs founder | Founder | Dummy variable that takes the value of 1 if the CEOs of the firm is the founder, and 0 otherwise. |

| CEOs tenure | Tenure | Defined as the number of years a CEO is in the office. |

| CEOs age | Age | Natural logarithm of CEO’s age. |

| CEOs gender | FCEO | Equals to 1 for female CEOs, and otherwise 0. |

| CEOs ownership | Own | Percentage of shares held by CEO. |

Acknowledgements

Not applicable.

Authors’ Contributions

All authors of this research paper have directly participated in the planning and execution of this study. Aurang Zeb and Irfan Ullah wrote the research paper and designed the organization of this paper. Amjad Iqbal and Mohib U. Rahman did the methodological part of this paper including; statistical analysis, interpretations, and discussion. Shahab Aziz contributed in improving the introduction part, literature review, discussion, and the English language of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Not applicable.

Data Availability Statement

The data for financial indicators, governance, and CEO characteristics is collected from CSMAR. Green patent data is collected from China National Intellectual Property Administration (CNIPA).

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.