Abstract

We investigate the empirical nexus between financial inclusion and economic growth for an extended sample of 21 Asian countries spanning over a period from 2004 to 2019. Further, we also conducted a sub-sample analysis by dividing the overall samples into developed and developing countries. Our results reveal a significant positive long-term impact of financial inclusion on economic growth in Asia. Our pair-wise causality test shows bidirectional causality between financial inclusion and economic development. Our robust results are consistent across various estimation techniques. Our findings suggest that the influence of financial inclusion on economic growth is more pronounced in developing countries compared to developed countries. Our results hold across subsamples. These findings posit important policy insights to enable the policy-makers in designing policies that ensure efficient and inclusive financial system on an equitable basis to achieve sustainable economic growth.

Introduction

Access to financial services and inclusion of masses within financial network has been considered an important socio-economic issue within the domain of financial inclusion. Inclusion of broader population into the financial services’ network ensures that benefits of financial services are distributed on equitable basis across the broader spectrum of the national population. Abdul Karim et al. (2022) documented that financial inclusion is one of the most important drivers of economic growth because it brings individuals, families, and firms within financial system which triggers the consumption and expenses, especially in countries characterized by lower income. Although financial inclusion has a pivotal role in economic development, despite of this one-third of the world population have no formal access to financial system in the form of bank accounts (World Bank Report, 2018). Moreover according to the estimates of UFA (2020) despite the recent emergence of financial inclusion across the globe, 31% of adults across the globe do not have a basic transaction account. Among these unbanked individuals, majority of them belong to Asia (Adedokun & Ağa, 2023).

The extant literature supported the opposing views regarding the relationship of economic progress with financial system-related development. The advocates of a positive association of economic progress with an inclusive financial system empirically complement the constructive role of inclusive financial system-related development in shaping sustainable growth (Kapoor, 2014; Mushtaq & Bruneau, 2019 & Raza et al., 2019). They argued that government policies are inclined toward the development of a broader, sound, and inclusive financial system which in turn contributes to sustainable economic progress. The opposing view (Bist, 2018; Pradhan & Sahoo, 2021), argues that the causality delineates from sustainable growth toward the inclusive financial system. There is also a third view that advocates that the bidirectional relationship between of strong and inclusive financial system with progress related to overall economic condition (Kim et al., 2018;Adedokun & Ağa, 2023) and hence complement each other.

Our study contributes to the current debate on inclusive financial system and progress related to overall economic condition in several ways. Firstly, the contribution of the current research stems out from our sample of Asian countries since previous studies are conducted in an individual country or different regions. For instance, Huang et al. (2021) reported on the relationship of sound and inclusive financial system and overall economic progress in old and new Europe; Van et al. (2021) in a broader180 countries sample and Kim et al. (2018) in 31 countries. Whereas, some empirical studies like Dahiya and Kumar (2020), and Song et al. (2020) are conducted in individual markets. However, Asia as a region is focused less in the literature. Our study takes Asia as a sample region due to the following reasons. (i) Asian existing economies are characterized by certain peculiarities such as lower financial inclusion of masses into the financial sector and unsophisticated financial system. (ii) Asian countries are expected to grow at a much faster rate in terms of macroeconomic growth. The recent statistics reveal forecasted overall progress of economic development is 6.3% over the coming 2 years in emerging markets (Le et al., 2019). It is reported that approximately one billion people in our sample region are outside the financial sector (Bhardwaj et al., 2018). These masses have no employment, no access to opening a bank account, and lack a meaningful ability to become a part of online or offline paid jobs. Furthermore, Bhardwaj et al. (2018) reported that about 27% of adults in developing economies across Asia hold a formal bank account. These countries vary along economic, political cultural, religious, and ethnic lines. This situation necessitates exploring the role of financial inclusion in economic development of Asia.

Secondly, there is vast literature that supports the view that the effects of access to financial services over the economic progress varies due to the level of economic and technological advancement related growth of a country (Jiang & Ma, 2019). Furthermore, the effect of access to financial services on overall economic progress varies across countries and previous research reports on the pronounced growth enhancing effect of financial sector development on overall economic progress in the low-income developing countries compared to high-income advanced countries (Abdul Karim et al., 2021). On the contrary Emara and El Said (2021) argue that well developed economies possess stringent governance system and sophisticated industrial base, which ensures overall sustainable economic progress via equitable based inclusive financial system. Due to these opposing views it becomes pertinent to study this interconnection between access to financial system and progress of economic condition in a comparative context between developing Asian and developed Asian countries. To achieve this objective, the study divides the overall sample into to subsamples based on their income level. To cope for the economic differences in a unified framework, our subsamples include developed and developing countries to provide better insights to policy makers.

Thirdly, in this strand of research some notable recent studies (Abdul Karim et al., 2022; Emara & El Said, 2021, have ignored the issues of cross-sectional dependence and slope heterogeneity. This methodical void has led to challenges while comparing different studies conducted in the context of comparative studies across subsamples. Owing to this methodical ramification our study has applied various advanced and sophisticated techniques to analyze the relation between financial inclusion and economic growth for full sample and across subsamples of Asian countries. In order to cope with the issue of slope heterogeneity and cross-sectional dependency, this study employs cross-sectional augmented autoregressive distributed lags (CS_ARDL) estimation. Further to cope with the issue of endogeneity, the study estimates the parameters using a dynamic panel framework through difference and system generalized method of moments (GMM).

The remainder of the paper is organized as follows. Section 2 presents the literature review while Section 3 describes the research methodology. Sections 4 describe the data, discusses the main findings and illustrate the robustness check. Section 5 presents the conclusion and offers some practical implications.

Literature Review & Hypotheses Development

Theoretical Framework

Endogenous growth theory proposes that accessible financial sector development and particularly expansion in the banking services fuels higher allocation of savings for resource acquisition, encourages innovation in the economy and leads to efficient investment of funds available in the economy. In this context, Hassan et al. (2011) argue that when economy achieves growth stage, demands for financial services increases, which in turns triggers the development in the financial sector. Furthermore, Pradhan and Sahoo (2021) argue that this nexus between financial sector development and economic growth can be debated in the light of four well known hypotheses regarding financial sector expansion and economic development.

The first hypothesis advocates uni-directional causation between accessible financial sector development and overall progress of economic condition based on the supply side provided by the financial sector (De Gregorio & Guidotti, 1995). From the supply-side hypothesis, research studies argue that inclusive financial sector related development drives the economic development. Notable studies in this strand constitute the studies of Cheng et al. (2021), and Ibrahim and Alagidede (2018), these studies advocate that a sophisticated financial sector offers an efficient resource pooling, well-developed mechanism of risk mitigation, stronger corporate governance, and clear price signaling which in turn induces an inclusive economic development. These studies confirmed the supply side hypothesis by analyzing cross country panels and suggested that financial sector development induces the supply leading hypothesis. Luintel and Khan (1999) confirmed the supply leading hypothesis through the VAR estimation approach by utilizing an extensive set of data of 10 developing nations over a longer period from 1950 to 1990. Their results were further confirmed by studies conducted in Taiwan, South Asian countries, Bolivia, India, and OECD countries among many others (Akinci et al., 2014; Bojanic, 2012; Chang & Caudill, 2005; Ray, 2013; Wadud, 2009).

The second hypothesis pertains to the demand side and this view derives from economic sector development put forward by Patrick (1966). The supporters of the demand leading hypothesis advocate that causation stems out from the economic sector growth and moves toward the accessible financial sector development based on the claim that enterprise sector development precedes the development in the financial sector (Polat et al., 2015). Moreover, Kuznets (1955) argued that growth in financial development depends on the economic cycle. Financial sector development subsides as the economic cycle is in its intermediate stage and as the economy shifts toward mature stages financial development also grows at a faster rate (Patrick, 1966). Arestis and Demetriades (1997) argued that the two broader categories of accessible system such as bank-based system and market based systems are followed in developing and developed countries respectively. They reported that market-based system is more connected to short term development and it usually triggers the financial sector development. Zang and Kim (2007) investigated the impact of development related to the financial sector on economic development in 74 countries over a period from 1961 to 1995. Their empirical results revealed that financial sector development precedes economic growth. This demand following hypothesis is supported by various studies such as Baliamoune-Lutz (2003) found similar evidence in Algerian, and Egyptian market settings. Other notable studies in this strand include the studies of Liang and Teng (2006) in the Chinese market setting, and A. Khan et al. (2019) in Pakistan.

Moreover, previous literature also provides adequate empirical support to the third hypothesis based on two way causal associations between financial sector related development and growth (Abu-Bader and Abu-Qarn, 2008; Shan, 2005). For instance, Luintel and Khan (1999) established a uni-directional financial sector development and economic progress running from financial sector related development to economic progress. Likewise, Khalifa Al-Yousif (2002) concluded that financial sector related progress and prosperity varies according to different economic policies adopted by different countries and supported the feedback hypothesis. Similarly, while analyzing a data set for Kenya over a period from 1966 to 2005, Wolde-Rufael (2009) empirically proved the existence of feedback hypothesis. Further, Akinci et al. (2014) extended this debate and established the inclusive financial system related development and economic progress relationship in OECD countries. However, Cheng et al. (2021) reject the feedback hypothesis thereby investigating financial sector related development and economic prosperity relationship in 72 countries.

Finally, there are some research studies which reported on no causal link between financial sector growth and economic development. Lucas (1988) argues that there is no role of financial sector development in triggering economic growth. Solow (1956) reported that there comes a point in the economic cycle where economic growth stagnates and this economic stage persists and no more growth is created by an increase in capital within the financial sector. This claim is supported by Swan (1956). Further, Atindéhou et al. (2005) concluded on a weak causal connection between financial sector development and economic development. This strand of research further includes the studies conducted by Kar et al. (2011) for 15 MENA countries and Ali (2014) for Pakistan.

Empirical Review

Financial Inclusion and Economic Growth

The extant empirical literature supported the impact of accessible financial system as a dimension of development related to financial system on economic progress (Emara & El Said, 2021). Abdul Karim et al. (2022) while using dynamic threshold model, empirically analyzed the impact of accessible financial system on economic progress in Asia and reported that expansion of financial services across broader population results in economic prosperity in overall and subsamples of these countries. The findings supported a more pronounced positive impact of inclusive financial system on growth in developing countries vis-à-vis advance economies. Huang et al. (2021) found that financial growth results in higher economic development for European markets having low level of income vis-à-vis European countries with higher level of income. Dahiya and Kumar (2020) examined the influence of access to financial system on economic progress in India from 2005 to 2017. They reported economic progress is positively associated with accessible financial system, arguing that financial development positively contribute to sustainable economic development. Van et al. (2021) explored the relationship between accessible financial system and economic progress based on panel static regression estimation in 181 countries. Their findings supported the greater impact of accessible financial system on growth in developing countries.

Similarly, Sethi and Acharya (2018) established the uni-directional financial service related development and economic progress relationship in 31 economies, which flows from inclusive financial inclusion related progress to economic development. Sharma (2016) observed a positive association of inclusive financial system and economic progress in India. Using advance statistical techniques such as DOLS and FMOLS over a period from 1970 to 2016, Nazir et al. (2021) suggested the positive association of accessible financial system and growth. Using a panel data of 51 OIC countries, Kim et al. (2018) suggested the constructive role of accessible financial system related progress in shaping overall economic growth. Similarly, Babajide et al. (2015) also supported the financial services related development and progress related to economic development.

The Relationship of Financial Inclusion with Different Macroeconomic Development

The extant literature reported the influence of inclusive financial system on various aspect of macroeconomic development (De Gregorio & Guidotti, 1995; Donou-Adonsou & Sylwester, 2017; Neaime & Gaysset, 2018). For instance, Le et al. (2019) established the impact inclusive financial system on efficiency of banking sector in 31 Asian countries. Hunjra et al. (2022) study the causal influence of financial development on sustainable economic development through advanced statistical panel models and concluded that financial sector development contributes positively to sustainable development. Based on a sample of top 60 Asian countries from 2004 to 2016,Ahmed et al. (2022) examine the causal impact of institutional performance and accessible financial system on green growth in South Asian economies from 2000 to 2018 and observed a long run association among the variables. Similarly, Kim et al. (2018) also supported the uni-directional role of accessible financial system in prospering overall economic growth.

Moreover, Bruhn and Love (2014) argued that access to formal banking services in the Amazon region has positively affected the livelihood of the area and people underwent a great social change with the introduction of formal financial services in the region. Brune et al. (2016) further reported that the introduction of fixed saving account in the Malawi area has brought a significant social change in this locality. These saving accounts enabled the people to save the money required to buy necessary agricultural land which in turn uplifted their livelihood. Another study conducted by Acharya et al. (2009) in India, reported on the existence of long term relationship of credit growth and economic progress. Yorulmaz (2013) employed a multifaceted approach to measure the coverage of access to available financial services in Turkey thereby analyzing different aspects of financial inclusion and found that the presence of accessible financial system varies with the levels of income. On a similar note, Rioja and Valev (2004) confirmed that the nexus between financial inclusion and economic progress varies across different level of financial sector growth. Interestingly they reveal that a medium level of progress related to economic development reports a medium level of growth in the financial sector and this nexus becomes weak across higher level of financial sector growth.

Literature Gap

Prior studies regarding the relationship between financial inclusion and economic growth provide some useful insights regarding the advancement of literary work. However, the results regarding the financial inclusion-economic growth nexus are inconclusive and contradictory. Primarily regarding this nexus, there exist two gaps in the literature. Firstly, majority of the above mentioned empirical research has been carried out in emerging and developed economies. However, the most vulnerable region (Asia) is less focused. Secondly, the use of different data, samples, and statistical techniques, has created the challenges to compare research work completed by different researchers. In line with the above limitations, our study contributes to a very rare literature that investigate financial inclusion and economic development connection through advanced statistical techniques such as CS-ARDL approach. This estimation framework is more reliable and produces efficient and robust parameters in an environment of slope heterogeneity and cross sectional dependency. Thirdly, there is a wide empirical literature on the association between financial inclusion and economic growth; however this relation has not been investigated across heterogeneous level of income across different countries, especially in the Asian region. In order to fill this void, the study further analyzed the role of financial inclusion and economic growth across low-income (developing) and high-income (developed countries) to provide a better insight for policymakers and practitioners in the domain of financial inclusion and economic expansion. Based on this, the study formulates the following hypothesis.

Data and Research Methodology

Data and Sample Details

We considered widely known website of World Bank to collect the data of macroeconomic variables data for 21 Asian Countries from 2004 to 2019. Initially, we have collected the data of 31 Asia countries. However, the countries with more than 5 years missing data were removed from the sample, as we required a strongly balanced data to apply the advance statistically techniques for data analysis. The selected 21 Asian countries are further categorized into two groups which consists of High-upper middle income (developed countries) countries and Low-lower income economies (developing countries) in line with Essandoh et al. (2020), Omar and Inaba (2020). Table 2 corresponds to the details of the sample.

Summary of the Recent Empirical Studies.

List of Countries in the Study Sample (21 Asian Countries).

Operationalization (Financial Inclusion and Economic Growth)

We categorized the variables into dependent variable (Economic Growth), and independent variables such as Financial Inclusion, Trade openness, Industry, Population growth and information and communication technology for empirical analysis. The description of variables and summary statistics are presented in Table 3.

List of Variables Used in the Study.

We consider the five proxies of Renzhi and Baek (2020) such as Number of ATM machines, Number of financial intermediaries branches, Number of banks. Furthermore, to cater for the utilization of commercial bank services by the masses, we include the percentage of credit and deposits of a country to the country’s total gross domestic product (Abdul Karim et al., 2021). These five proxies are also known as supply side proxies of financial inclusion( See Nguyen, 2021). We have considered principal component analysis (PCA) technique to construct a composite indicator for inclusive financial system (Radovanović et al., 2018), which would be used as variable of interest in main analysis. We applied to two tests such as KMO test and Bartlett’s test to determine, whether these proxies are suitable for composite index in accordance with provided criteria of Le et al. (2019). The reported findings of both tests in Tables 4 and 5 supported the PCA procedure in whole and subsamples. To construct financial inclusion index, the process of PCA is performed in two steps. In first step, those components were identified that have lowest pair-wise correlation and accounts for more variation in the original variable. In the next step, an index is estimated based on the components that have Eigen value greater than 1 (Gujarati & Porter, 2009). The cumulative variations of each component and pattern of matrix of PCA are reported in Tables 5 and 6 for the overall sample and subsamples respectively.

Results of Bartlett and KMO Tests for Sphericity and Sampling Adequacy (Sub-Sample).

Total Variance Explained ( Full Sample & Sub-Sample).

PCA Pattern Matrix( Full Sample & Sub-Sample).

Econometric Approach

Our baseline econometric model envisages the basic production function where production (GDP) is the function of capital’s stock, labor and other factor of production. Our econometric model delineates from the basic notion that inclusive financial system triggers the accumulation of capital, and labor and improve economic progress. Further accessibility and utilization of banking services facilitates higher saving in the economy and these funds are then allocated to production units, which in turn results in higher productivity as confirmed by Sethi and Acharya (2018). In line with this, our study follows Abdul Karim et al. (2021) and specify the following econometric model to examine the effect of financial inclusion on economic growth.

Where,

Estimation Techniques

The study employs several pre-estimation tests before estimating our baseline econometric model. H. Pesaran (2004) test is executed to look for cross sectional dependency. We checked the stationarity through Im, Pesaran, and Shin (CIPS) panel unit root test. Further we conduct cointegration test among the study variables following Pedroni (2004) and Kao (1999). To cater for the issue of endogeneity this study utilize CS-ARDL model to explore both the long-run and short term association between financial inclusion and economic development (Z. Khan et al., 2021). To confirm the direction of casual relation the study applies Dumitrescu-Hurlin (D-H) panel causality approach. Furthermore, the extant literature supported the existence of endogeneity issues in inclusive financial system and economic progress relationship. Hence, For the purpose of robustness, instrumental GMM and 2SLS estimation techniques are employed to cater for the endogeneity problem such as simultaneity and reverse causality instead of dynamic panel data estimation due to the bias of small sample (Altonji & Segal, 1996; Hayakawa, 2007). Further we introduce the lag of financial inclusion as instrument to cater for any reverse causality between financial inclusion and economic growth. We extend our analysis along the same estimation lines for our sub samples of developed and developing economies.

Empirical Results

Cross-Sectional Dependence and Slope Homogeneity Tests

For the confirmation of cross-sectional dependence for both full and sub samples this study applies H. Pesaran (2004) test. This test is suitable for our study since this study employs a dataset of 21 cross sections for 16 years. The results for H. Pesaran (2004) are reported in Table 7. Our results are consistent with Le et al. (2020) for cross sectional dependency thus rejecting the null hypothesis and accepting the alternate hypothesis on the presence of cross sectional dependence at a statistical significance of 1%. These results reveal the presence of cross sectional dependency among the variables for selected countries of Asian region. We also report cross sectional dependency for our sub samples of technologically advanced, and developing countries. We further apply M. H. Pesaran et al. (2008) to test for the presence of slope heterogeneity. The significant values of delta (Δ) and adjusted delta (Δ adj) reported in Table 8 confirms the presence of slope heterogeneity while estimating our base line model for full sample as well as sub samples.

Results from Cross-Section Independence Tests.

Cross Sectional Dependency and Slop Homogeneity.

Panel Unit Root and Co-integration Estimation

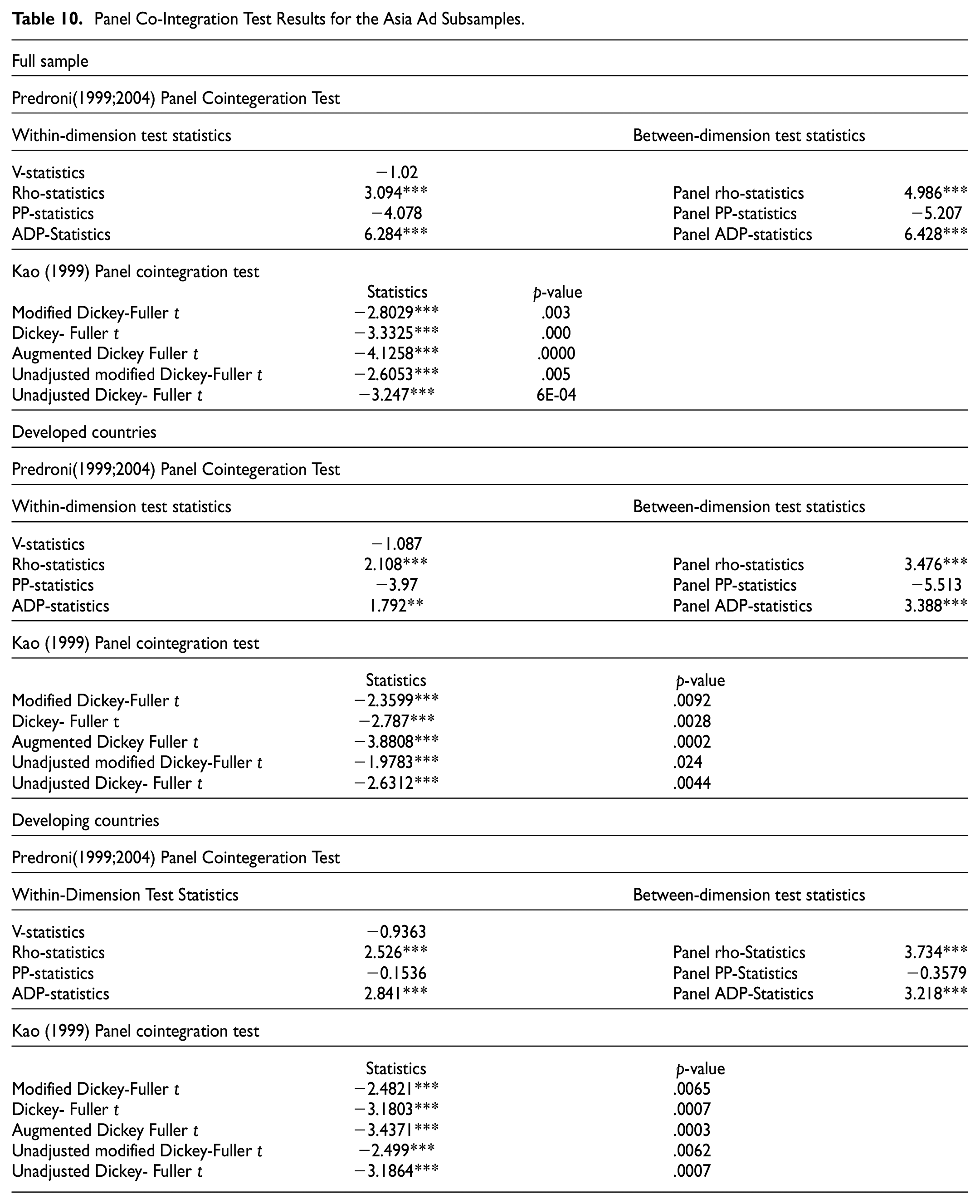

Following Granger and Newbold (2014), we look for the integration value at level I (0) of first difference for each variable to cope with the issues of spurious regression through CIPS. The reported finding of CIPS unit root test in Table 9 supported all variables are stationary at first difference with few exceptions. For testing of co-integration this study follows the framework of Pedroni (2004) reported in Table 10. Since our sample is composed of 21 countries across 16 years, Pedroni (2004) is the suitable method to test for co-integration among the selected variables. Four out of seven co-integration tests supports the notion that co-integration exists among the selected variables. For the purpose of robustness we follow the method of Kao (1999). The results of Kao (1999) test also support the presence of long term co-integration among the selected variables. These results were consistent across the sub samples. Thus on the basis of these findings we conclude that a long term co-integration does exist among the selected variables for our full as well as subsamples.

Results of CIPS Unit Root.

Panel Co-Integration Test Results for the Asia Ad Subsamples.

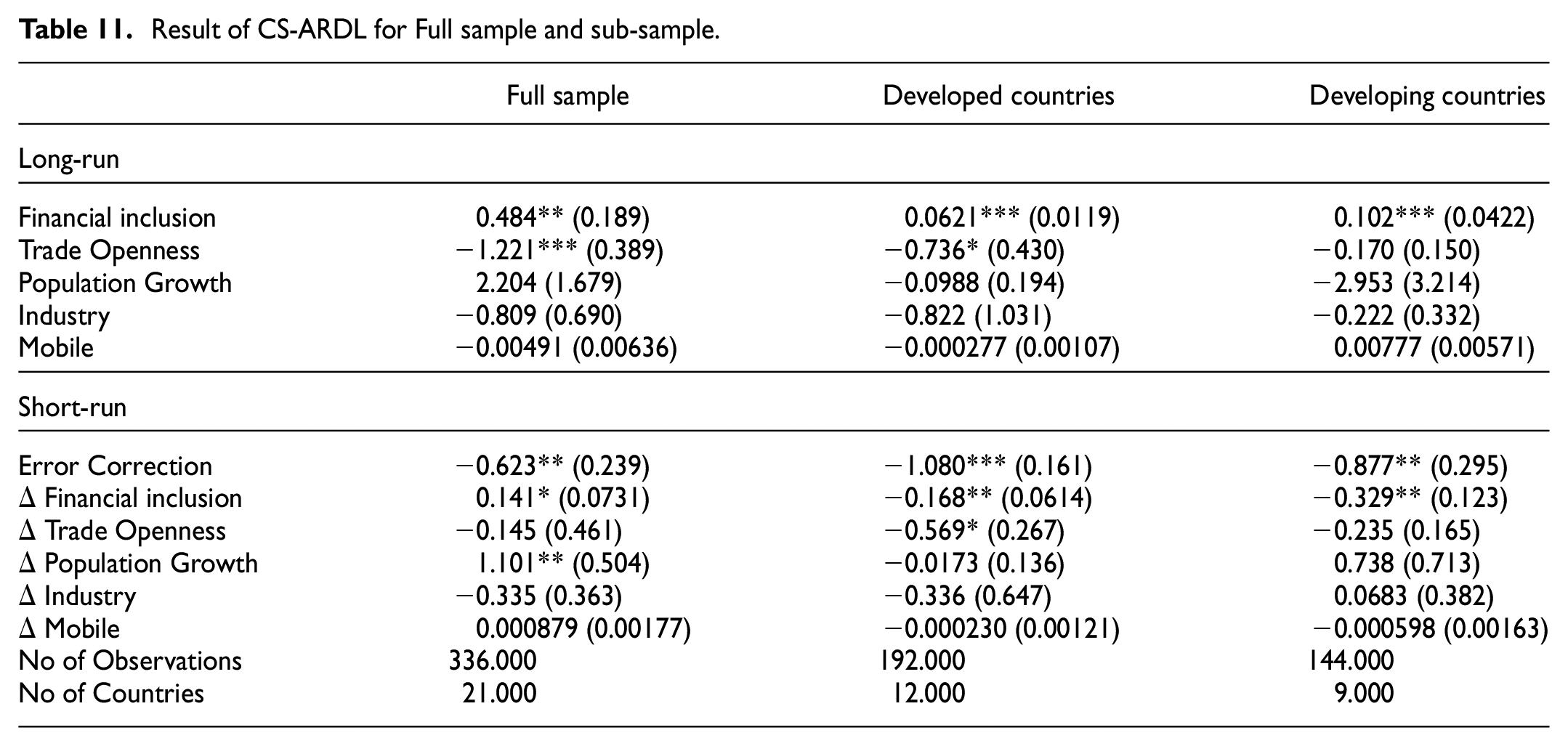

Panel CS-ARDL Estimates

We have applied CS-ARDL to examine the inclusive financial system and economic progress relationship and the results are presented in Table 11. This positive coefficient of financial inclusion imply that inclusive financial system boosts the industrial and manufacturing activities through lending at affordable cost which in turns leads to positive contribution to economic growth (Cheng et al., 2021). Several scholars consider financial development as important pillar for economic development, since it accumulates the capital through mobilization and pooling of savings (Huang et al., 2021), and ensure optimal allocation of financial resources for better economic prospects thereby reducing the issues related asymmetric information (Chatterjee, 2020; Kayani et al., 2020). Our results are in line with the impression that well functioned financial system lessens the borrowing cost, which promotes the businesses to acquire the required funds to further enhance the production scale that further contribute to sustainable development (Makina & Walle, 2019; Song et al., 2020).

Result of CS-ARDL for Full sample and sub-sample.

Our findings related to the regression coefficients for financial inclusion reveal in subsamples reveal that the higher impact of inclusive financial service related development in developing economies vis-à-vis developed countries. Since, a stronger magnitude of this relationship is documented in countries with low level of income, the statistical variations across sub-samples are consistent with the findings of Abdul Karim et al. (2021), Van et al. (2021), and Kim et al. (2018), which argue that the aggregate impact of financial inclusion is greater in low-income vis-à-vis higher-income countries since the businesses tends to expand the production scale through accessible financial loans in the developing countries because these economies have greater potential to grow exponentially at a much faster rate.

Panel Causality Results

We tested the bi-directional relationship between the variables via Dumitrescu and Hurlin (2012) in a panel setting. Due to short study period, the study employs lag order one as suggested by the study of Žiković et al. (2020). Table 12 reports the results for D-H panel estimation. These complement the bidirectional inclusive financial system and sustainable growth relationship in whole sample. This bidirectional causality also holds for our sub samples. Our finding shared common grounds with the reported bi-direction inclusive financial system and growth relationship of Hassan et al. (2011).

Results for D-H granger Causality Test (Sub-Sample Analysis).

Robustness Check

Our previous findings confirmed the positive association of inclusive financial system with economic progress. Nevertheless, the extant literature supported the existence of endogeneity related issues in the nexus of inclusive financial system and growth and hence we adopted several approaches to address endogeneity issues. Since our study pertains to small sample, due to these reasons dynamic panel data framework will result in biased results (Altonji & Segal, 1996; Hayakawa, 2007). For this reason we employ the instrumental variable GMM and 2SLS estimation to cope with the endogeneity issues related to financial inclusion and economic growth. In this estimation we incorporate the lags of financial inclusion and other control variables as instruments to cater for endogeneity Table 13 reports the results of Instrumental variables GMM and 2SLS for whole and subsamples. The financial inclusion has positive coefficients in the full sample (βFI = 0.445, p < .01) and the two sub-samples of developed countries (βFI = 1.368, p < .01) and developing states (βFI = 1.948, p < .1). All the coefficients of financial inclusion are positive and statistically significant at 1% level for the whole sample and subsamples, which implies that causation leads from financial inclusion to economic growth. The results are in line with prior results of Van et al. (2021), who found a more prominent positive association between financial inclusion and economic development for low-income countries compared to the high-income and advanced countries.

Results for Instrumental Variables Generalized Method of Moments (GMM) and two Stage Least Square (2SLS).

Note. Robust standard errors in parentheses.

***p < .01, **p < .05, *p < 0.1.

The overall results supports the claim of endogenous growth theory that in the early stage of economic development financial system ensures the efficient channelization of funds from lenders to the borrowers that lubricate the wheels of the economy and accelerate economic growth (Emara & El Said, 2021). This acceleration in the economy induces demand for financial services, which in turns results in the expansion of financial sector. Our findings shared common grounds with notable prior empirical studies conducted by Hassan et al. (2011), and Huang et al. (2021). The findings of these studies also suggested the endogenous positive development of financial system and economic growth relationship.

Conclusion

Since last two decades the growing debate regarding the role of inclusive financial system in shaping economic progress has attracted many researchers around the world. Many research studies supported a positive association inclusive financial system and economic progress relationship. However, the empirical studies on this concern and with a specific focus on Asia are scant. On these lines, this research endeavors to examine the nexus between inclusive financial sector related development and economic progress by employing a dataset of 21 Asian countries. The investigation further demarcates to sub sample analysis by dividing the overall sample into two subsamples of Advanced and developing Asian countries based on the national income of the respective countries. For overall as well as subsamples we report a positive relation between inclusive financial sector related progress and growth. Further, the study reveals that the positive nexus between inclusive financial system and economic development is more pronounced in developing countries compared to the developed Asian countries.

The current study has multifaceted and far-reaching policy implications for the Asia region. The study recommends to revisit the structural reforms of inclusive financial system to overcome the existing hurdles and provide easy access to the available financial services for sustainable economic growth. Furthermore, a deep understanding of financial inclusion may facilitate the regulatory authorities of the financial sector to design policies that ensure efficient allocation of available resources from the less productive sector to the more productive sector and execute policies that would ensure inclusive and equitable access to financial services, thus reducing poverty and promoting income equality and economic development. In case of developing countries, the positive role of inclusive financial system in shaping economic progress suggests that inclusive financial sector development is crucial for the economic development of these countries in the presence of less sophisticated financial sector. Furthermore, for greater access of financial service and utilization of banking system, the regulatory bodies need to design policies that results in significant decrease in the transaction costs of using financial service to encourage both borrowing and saving over boarder mass of population.

Our study has several limitations that need to be researched by future studies. First, the study established the relationship of accessible financial system and overall economic growth in Asia region and in subsamples. Therefore, future studies may consider individual country to replicate this methodology since these countries are prevalent with different economic, political, ethnic, cultural, and religious attributes. Lastly, the investigation of non-linear inclusive financial system and sustainable economic progress could another interesting avenue for future research.

Footnotes

Author’s Note

This research was conducted while Dr. Ajid ur Rehman was at Faculty of Management Sciences, Riphah International University, Islamabad. They are now at NUST Business School, National University of Science and Technology, Islamabad and may be contacted at

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.