Abstract

This study investigates the financial development–economic growth relationship in Pakistan over the period 1975–2017 using the Markov Switching methodology. The financial development index has been constructed using the principal component analysis. Unexpectedly, the empirical result shows that financial development contributing negatively to economic growth in the high and the low economic growth regimes in Pakistan. Moreover, the results indicate that labor force retards economic growth with a higher magnitude. A significant positive effect of gross fixed capital formation on economic growth is also observed. The results reveal that policymakers may revisit the financial development policies so that the financial sector may contribute positively to economic growth process in Pakistan. In this respect, more steps are needed to further liberalize the financial sector to enhance economic growth in Pakistan.

Keywords

Introduction

It is well established that financial sector plays an important role in economic growth (Chung et al., 2019). This sector is of curiosity for policymakers and academicians as theoretical and empirical literature corroborates that financial development acts as an engine of economic growth in both developed and developing countries. A well-organized financial system provides better quality financial services, which in turn enhances economic growth, while less developed financial sector may restrict the economy from growing. Beck (2008) noted that the level of financial development is most important macroeconomic variable which is highly correlated with economic performance across countries. Likewise, Shahbaz et al. (2017) found positive effect of financial development on economic activities in India and China. Numerous theoretical and empirical studies (e.g., Asteriou & Spanos, 2019; Caporale et al., 2014; Gurley & Shaw, 1955; King & Levine, 1993; Levine, 2005; McKinnon, 1973; Naveed & Mahmood, 2019; Schumpeter, 1911) identified multiple channels through which financial markets exerts positive impact on economic growth across countries. These studies concluded that well-developed financial markets can improve economic growth through efficient allocation of capital resources, lowers information and transaction costs, enhances monitoring and corporate governance, mobilizes savings, mitigates investment risk, overcomes indivisibility of large investment projects, and fosters competition in the financial industry (Beck et al., 2016). There is growing evidence that better financial environment leads to higher economic growth by reducing financing constraints for entrepreneurs, improves efficiency of resource allocation across investment projects, and fosters technology diffusion (Comin & Nanda, 2019; Levine & Zervos, 1998). However, there are conflicting views with regard to the role of financial development in economic growth. For instance, Levine (2005) argued that financial markets boost economic growth by reallocating capital resources to its best productive use. The endogenous growth theory also highlighted the role of financial development in economic growth through the positive impact of financial services on the level of capital accumulation (Odhiambo, 2004; Romer, 1990) and technological innovation (Grossman & Helpman, 1991). Chandavarkar (1992) expressed skepticism by ignoring the role of financial system in economic growth process. However, Lucas (1988) asserted that the importance of financial sector is over-stressed with respect to its role in economic development. Likewise, Robinson (1952) advocated that finance does not contribute to economic growth, rather it fulfills the demands of real sector. Ranciere et al. (2006) asserted that financial liberalization induces excessive risk taking, increases macroeconomic volatility, and leads more frequent crises. Schularick and Taylor (2012) and Mian and Sufi (2014) also maintained that inadequately supervised financial system may attract crises that lead to adverse implications for economic growth and social welfare.

Numerous empirical studies (e.g., Abu-Bader & Abu-Qarn, 2008; Khan & Senhadji, 2000; King & Levine, 1993; Levine, 1997; Samargandi et al., 2014; Shahbaz et al., 2017) have found positive relationship between financial development indicators and economic growth in developed and developing countries. Keeping the significant role of financial sector in economic growth, majority of developed and developing countries implemented financial liberalization programs to purge the impacts of domestic repressive policies. It is believed that these structural shifts in financial policies have changed the relationship between financial development and economic growth from linear to nonlinear. Subsequently, some studies (for instance, Deidda & Fattouh, 2002; Rioja & Valev, 2004) found that financial development has a positive impact on economic growth above the specific threshold value, while others (for instance, Arcand et al., 2015; Cecchetti & Kharroubi, 2012; Law & Singh, 2014; Shen & Lee, 2006) detected the opposite impacts. This suggests that economic growth increases with financial development up to a certain minimum level, afterwards it drags economic growth. Ruiz (2018) also found that countries below the threshold grow less and those above the threshold grew faster. Likewise, Benczur et al. (2019) found the nonlinear impacts of total bank credit on economic growth is more pronounced than that of either household credit alone or the sum of bank credit, debt securities and stock market financing. They also found that credit to nonfinancial corporation tends to have a positive impact, while credit to households exerted negative impact on economic growth even after controlling for nonlinearities. Ductor and Grechyna (2015) observed negative effect of financial development on economic growth, while Swamy and Dharani (2019) found inverted U-shaped relationship between the two. The main reason of nonlinear impacts of financial development on economic growth could be too much finance in many countries, thus questioning the desirability of large financial sector (Benczur et al., 2019). Similarly, some researcher (for instance, Arcand et al., 2015; Cecchetti & Kharroubi, 2012; De Gregorio & Guidotti, 1995; Gennaioli et al., 2012; Zhao, 2017) found that excessive finance drags economic growth.

With respect to Pakistan majority of empirical studies (e.g., Jalil & Ma, 2008; Khan et al., 2005; Mahmood, 2013; Naveed & Mahmood, 2019; Tahir, 2008) have used linear approach to detect the relationship between financial development and economic growth. However, inferences based on the linear relationship become defunct after the structural changes in the form of financial sector reforms initiated in Pakistan in the early 1990s. Benczur et al. (2019) noted that nonlinear impacts of financial development on economic growth stem from substantial structural change in the composition of finance during the recent decades. In addition, using certain financing components separately or as a ratio may bias the estimations and lead to incorrect conclusions, thus provide spurious implications. It is obvious that structural shifts in financial policies make finance–growth relationship nonlinear as Brooks (2014) indicated that financial time series have leptokurtic distribution. Therefore, linear modeling techniques are inadequate for estimation of finance–growth relationship. It is pertinent to note that historical trend of real gross domestic product (GDP) growth in Pakistan is uneven as Amjad (2014) confirmed that the pace of GDP growth does not remain same during Pakistan’s economic history. He observed the spurts and reversals in high and low economic growth periods; thus, linear modeling techniques are inadequate to capture the spurts and reversal in economic growth in Pakistan.

The present study uses the Markov Switching (

The rest of this article is organized as follow: Section “Literature Review” presents a brief review of literature on finance–growth nexus. Section “Model Specification, Data and Methodology” deals with model specification, empirical methodology, variable description, and construction of FDI. Section “Empirical Findings” discusses empirical results, section “Conclusion” delineates conclusion of the study, while section “Policy Recommendations” presents policy recommendations and directions of future research.

Literature Review

Earlier literature on finance and growth showed positive correlation between the value of financial intermediaries assets and economic growth (Goldsmith, 1969). However, Goldsmith (1969) did not control other variables that may be jointly correlated with financial development and economic growth and did not test whether the link between financial development and economic growth works through productivity or capital accumulation (Levine, 2005). While controlling for initial income, government consumption, trade openness and school enrolment, King and Levine (1993) detected that the size of financial sector in 1960s significantly predicted economic growth, investment, and productivity growth. However, King and Levine (1993) did not determine the direction of causality between financial development and economic growth. The evidence on this aspect of finance–growth nexus were found by Levine et al. (2000) and Beck et al. (2000). They observed strong effect of exogenous components of financial development on long-term economic growth. Thus, their results indicate that financial development has a causal effect on economic growth. The studies that addressed causality issues (e.g., Guiso et al., 2004; Jayaratne & Strahan, 1996) detected positive effect of financial development on economic growth, entrepreneurship, and access to credit by smaller firms. Based on the literature survey, Levine (2005) concluded that the preponderance of evidence suggests that both financial intermediaries and financial markets matter for growth and found that reverse causality alone is deriving this relationship (Panizza, 2014).

However, empirical literature after financial crises 1997–1998 and 2007–2008 cast serious doubts on conclusions that financial development is necessary component of sustainable economic growth. For instance, Demetriades and Hussein (1996), Arestis and Demetriades (1997), Rousseau and Wachtel (2002), and Demetriades and Law (2006) detected no impact of financial development on economic growth. De Gregorio and Guidotti (1995) found negative correlation between financial depth and economic growth in the panel of Latin American countries. Based on threshold model, Deidda and Fattouh (2002) found support for the nonlinear effect of financial development on economic growth. Using Rajan and Zingales’s (1998) dataset, Manganelli and Popov (2013) observed nonlinear effects of financial development on economic growth. In the same vein, Ductor and Grechyna (2015) suggested that the effect of financial development on economic growth becomes negative, if rapid growth in private credit is not accompanied by growth in real output. Ibrahim and Alagidede (2018) showed that below a certain estimated threshold level, finance is largely sensitive to economic growth, while significantly influencing economic growth for countries above the threshold. Swamy and Dharani (2019) found inverted U-shaped finance–growth relationship with the estimated threshold level of 142% of GDP. Based on panel Granger causality results, they concluded that financial development is associated with optimal growth performance in a panel of advanced economies. Asteriou and Spanos (2019) showed that before crisis financial development promoted economic growth in a panel of 26 European Union countries, while after the crisis it hindered economic growth.

Another strand of literature concluded that financial development contributed more to economic growth in developing countries. For example, Calderon and Liu (2003) suggested that financial development contributed more to economic growth in developing countries rather than industrialized countries. Masten et al. (2008) found similar results in a panel of European countries. They concluded that less developed countries gain more from financial sector development. Rioja and Valev (2004) observed strong positive relationship between financial development and economic growth only for countries with intermediate level of financial development. Beck et al. (2012) noted that positive effect of financial development on economic growth is predominantly driven by enterprise credit rather than consumer credit.

Based on the above literature review, we can deduce that the relationship between financial development and economic growth is inconclusive. This study, therefore, contributes to the empirical literature by examining the relationship between financial development and economic growth by employing Markov Switching modeling approach. This approach is useful in analyzing the regime-dependent impacts of financial development on economic growth.

Model Specification, Data, and Methodology

Model Specification

To examine the relationship between financial development and economic growth, we followed the modeling strategy of Christopoulos and Tsionas (2004) and Khan (2008) and used following model for empirical investigation:

where

Data

The present study is based on the annual data over the period 1975–2017. We used real GDP per capita as proxy of economic growth. The control variables include employed labor force (

Construction of FDI

Adu et al. (2013) argued that single proxy of financial development cannot adequately capture the effects of financial development. However, when numerous indicators of financial development are included in a single equation, this will create the problem of multicollinearity. To avoid these issues, researchers construct the financial development index (

Following Ang and McKibbin (2007), we selected the weights of first component, and these weights have been multiplied with the corresponding values of financial development score to obtain the single index that represent financial development in Pakistan. In equation (2),

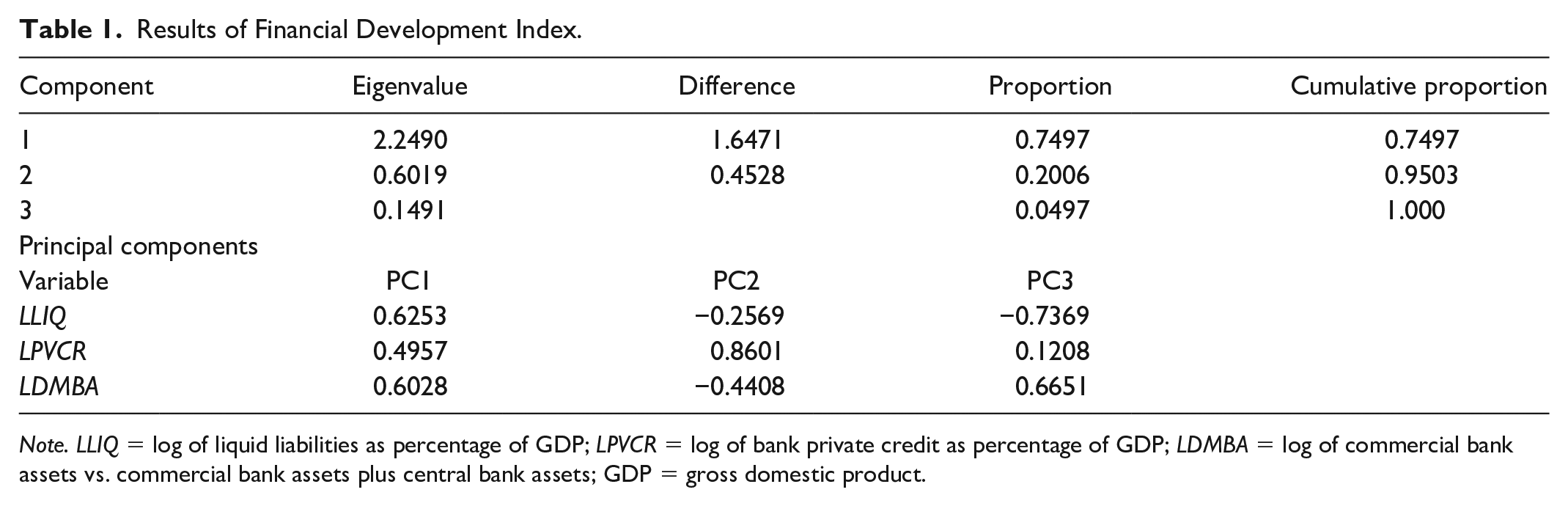

The results of the

Results of Financial Development Index.

Note. LLIQ = log of liquid liabilities as percentage of GDP; LPVCR = log of bank private credit as percentage of GDP; LDMBA = log of commercial bank assets vs. commercial bank assets plus central bank assets; GDP = gross domestic product.

It can be seen from Table 1 that first component captures almost 75% of the variations. Therefore, we plugged weights of first component (PC1) in equation (2) to obtain equation (3).

The

Regime Switching Model

Several studies confirmed nonlinear impacts of financial development on economic growth (Arcand et al., 2015; Levine et al., 2000). It is worth mentioning here that linear models fail to capture the nonlinear impacts of financial development on economic growth. Therefore, the present study employs the

In

In Equation (4), ∆

where

In

where

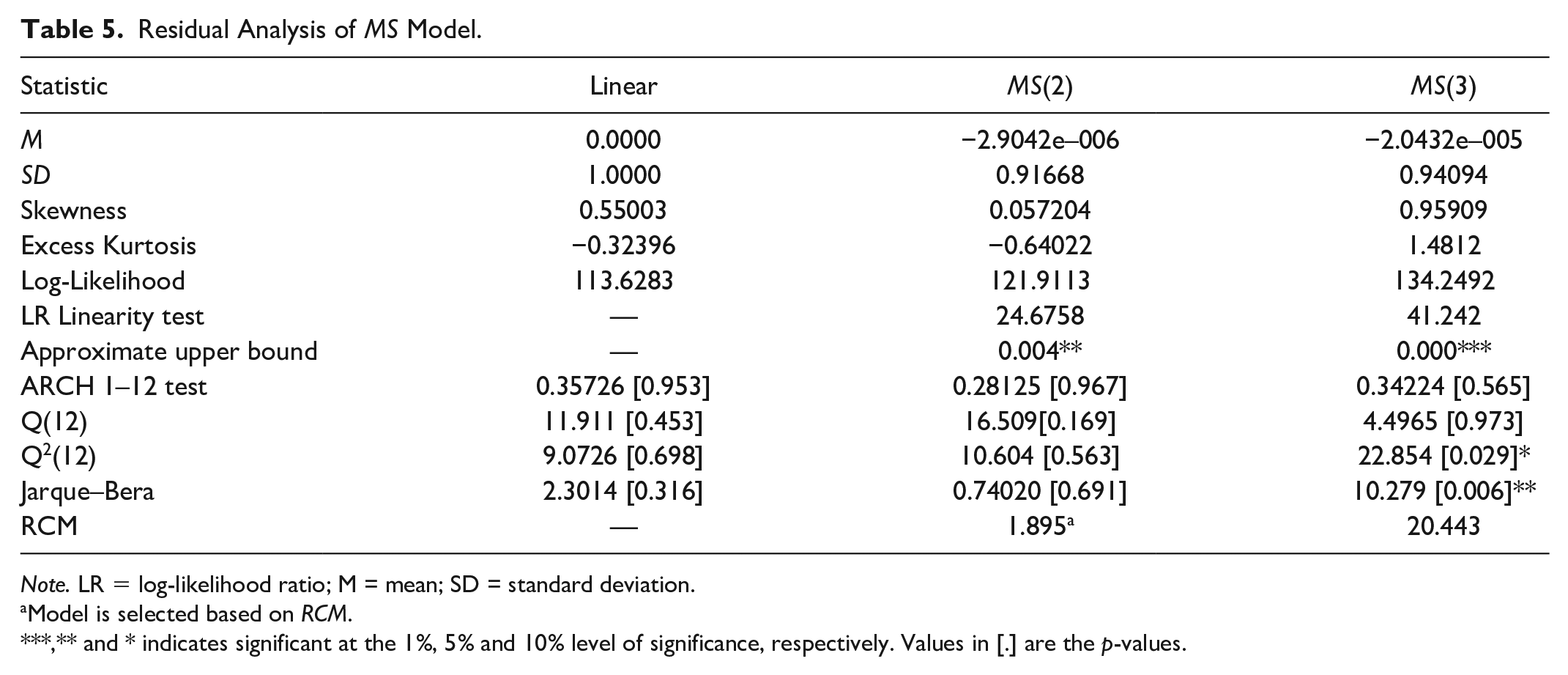

We have used more than 1000 starting values for estimated specification to optimize parameters globally. Besides, we considered the maximum log-likelihood ratio (LR) statistic, residual analysis, and Regime classification measure (

The

The value of RCM (ranges from 0 to 100) close to 0 reveals perfect regime classification, while it approaching to 100 means no regime classification.

Empirical Results and Discussion

Preliminary Investigation

We started our investigation with descriptive analysis and the results are reported in Table 2 (Panel A), whereas results with respect to correlation analysis are reported in Panel B of Table 2. The results indicate that the average change in all the variables is positive except for trade openness. The average growth in physical capital stock is relatively low as compared to labor force, indicating pivotal role of labor force in Pakistan economy. The statistics reveal that the highest level of economic growth was 0.065 that coincides to the year 1980, while the lowest level of economic growth was −0.015 which corresponds to the year 1997 when the economy was in the recession. Likewise, the average value of financial development was positive and equal to 0.014, indicating positive role of financial development in economic growth. The maximum value of financial development was 0.138, while the minimum value observed to be −0.207 that may be associated with repressed era. In addition, Inflation rate, government expenditures, trade openness, and financial development are relatively more volatile. Real GDP per capita and labor force has low volatility as indicated by the values of standard deviation. Likewise, financial development, physical capital, government expenditures, and trade openness have almost the same volatility. Only inflation rate is found highly volatile. Most of the variable possesses low mean with high volatility. Financial development is negatively skewed, whereas rest variables are positively skewed. The data have a heavier tails than normal distribution in case of financial development, physical capital, labor force, inflation, and government expenditures since the kurtosis is greater than three in all the cases. Thus, aforementioned series have leptokurtic distribution. Except labor force and government expenditures all other series are normally distribution as indicated by the significance of Jarque–Bera statistics.

Descriptive Statistics and Correlation Analysis.

Note. JB = Jarque–Bera.

The 1% level of significance.

It can be seen from Panel B of Table 2 that real GDP per capita is negatively correlated with labor force and inflation rate, whereas other variables have a positive correlation with real GDP per capita. More importantly, we observed positive correlation between financial development and real GDP per capita. However, correlation coefficient of financial development with real GDP per capita is relatively low as compared to other variables. The physical capital and government expenditures have relatively high positive correlation with real GDP per capita, while financial development has a negative correlation with government expenditures and inflation rate.

To check nonlinearity in the finance–growth relationship, we employed the Brock et al.’s (1987) test (Brock, Dechert, and Scheinkman [BDS] test). The BDS test indicates that an increment to a data series is independent and identically distributed (

Results of BDS Test.

Note. The p-values are based on bootstrap with 100,000 replications using standard deviation. The null hypothesis is that series are linearly dependent. BDS = Brock, Dechert, and Scheinkman.

The 1% level of significance.

It is evident from Table 3 that the relationship is nonlinear because all the dimensions are significant at 1% level of significance. Therefore, we can use

Results of Unit Root Tests.

Note. ∆ denotes first difference of the variables.

, **, and *1%, 5%, and 10% level of significance. In Lee and Strazicich (2003) structural break test, we applied crash model with a single break. Values in [.] are the break dates. C stands for constant term. ADF = Augmented Dickey–Fuller; PP = Phillips–Perron.

The results of the ADF and PP unit root statistics show that all the differenced variables are stationary, that is I(0), at appropriate level of significance. Furthermore, no structural break was detected in the levels of all variables as indicated by the Lee and Strazicich (2003) structural break test.

Regime Switching Model

The impact of financial development on economic growth was investigated using the Markov switching framework. To avoid estimation of a large number of parameters when the number of regimes increases, we consider a parsimonious state-dependent finance-growth model with two regimes (Ayadi et al., 2018). This choice is also more intuitive to interpret empirical results because the behavior of economic growth is generally depending on the trends of the economy, such as a high- or low-growth regimes. Fallahi (2011) documented that

Residual Analysis of MS Model.

Note. LR = log-likelihood ratio; M = mean; SD = standard deviation.

Model is selected based on RCM.

**,** and * indicates significant at the 1%, 5% and 10% level of significance, respectively. Values in [.] are the p-values.

To investigate the relationship between financial development and economic growth, we considered

Results of Linear and MS Models (1975–2017).

Note. Values in (.) are the t-statistics. 0 and 1 in subscripts indicate Regimes 1 and 2, respectively.

, **, and * indicates 1%, 5%, and 10% level of significance, respectively.

The results reported in Table 6 show that in case of

With regard to regression parameters, the result reveals that

Among nonswitching variables (see Table 6), the results reveal that physical capital exerts significant positive impact on economic growth. The results confirm that with a 1% increase in physical capital, the level of economic growth would increase by 0.089%. The positive relationship of physical capital with economic growth is consistent with the findings of Jalil and Feridun (2011), Qureshi and Ahmed (2012), and Naveed and Mahmood (2019). Labor force has significant negative relation with economic growth. The result shows that a 1% increase in the labor force causes economic growth to decrease by 0.090%. The negative influence of the labor force on economic growth is not surprising because Pakistan is a labor-abundant country and a major proportion of labor force is unskilled. Our results are consistent with those of Ali and Mustafa (2012) and Bist (2018). Growth of government expenditures and trade openness exerted negative but insignificant impact on economic growth. The insignificance of trade openness is an indicative of weak performance of Pakistan economy in the international market. Likewise, insignificance of government expenditures could be attributed to the overall role of government agencies in expanding economic growth. We also observed a negative and significant effect of inflation on economic growth in Pakistan, which shows that a 1% increase in inflation leads to decrease economic growth by 0.001%. Although the effect of inflation on economic growth is negligible, but its negative effect on financial development is more severe (Rousseau & Yilmazkuday, 2009). Increase in inflation restricts economic growth as it is associated with repressive policies.

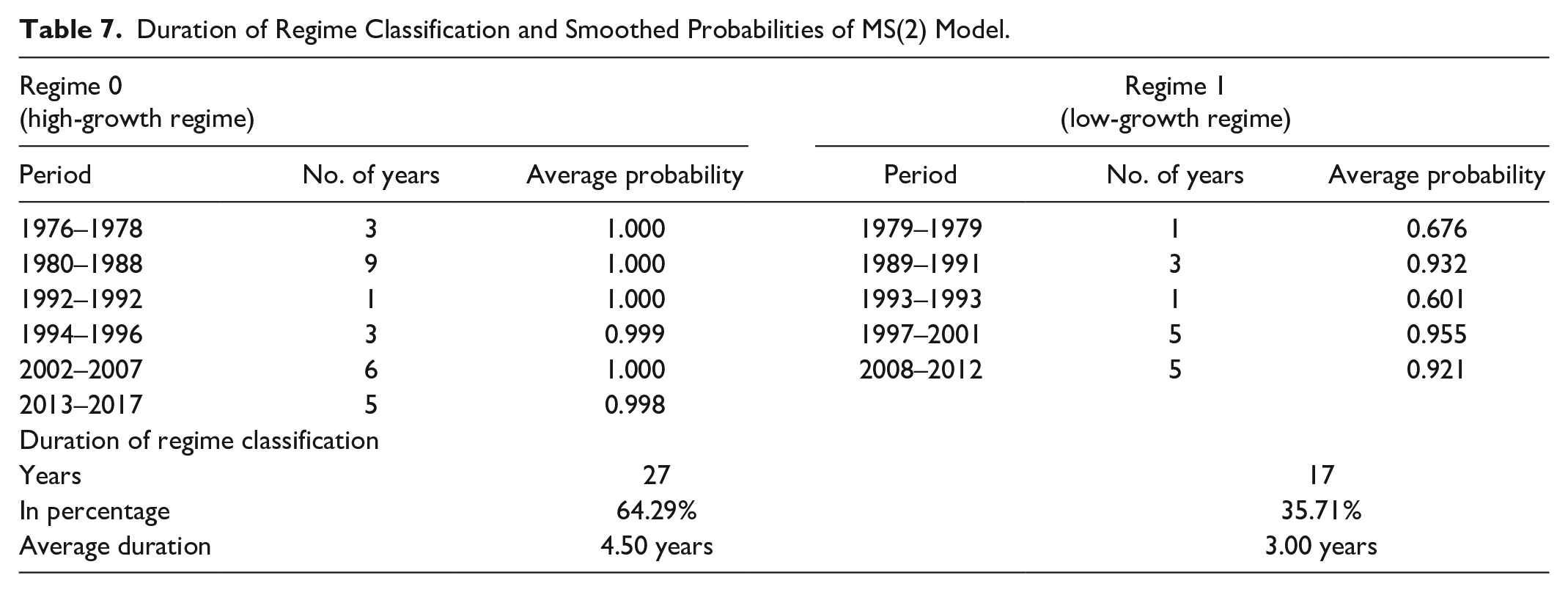

The outcome of regimes classification with reference to the high-growth and low-growth regimes is presented in Table 7.

Duration of Regime Classification and Smoothed Probabilities of MS(2) Model.

It is evident from Table 7 that both regimes are persistent because the estimated transition probabilities are greater than 0.5. For example, there is 64.29% probability of staying in the high-growth regime, which is higher than the probability of staying in the low-growth regime (that is, 35.71%). This implies that high-growth regime is more persistent than low-growth regime. The behavior of smoothed probabilities is depicted in Figure 1, which confirms that smoothed probabilities are persistent.

Smoothed probabilities of MS(2) model of finance–growth nexus.

Conclusion and Recommendations

This study examines the relationship between financial development and economic growth under the Markov regime-switching framework in Pakistan for the period 1975–2017. The empirical analysis is based on two-state Markov switching model. Using the PCA, we have constructed FDI by considering liquid liabilities as percentage of GDP, private credit as a percentage of GDP, and commercial bank assets as a ratio of commercial bank assets plus central bank assets.

The results support the existence of nonlinear relationship between financial development and economic growth in Pakistan. The findings reveal an evidence of high growth with low volatility in the high-growth regime, while low growth was associated with high volatility. Furthermore, financial development exerts negative and significant impact on economic growth per capita in high- and in low-growth regimes. In the high-growth regime, the absolute effect of financial development on economic growth is more than that of in low-growth regime. These results confirm the presence of nonlinearities in finance–growth relationship in Pakistan. The negative effect of financial development on economic growth could be that financial liberalization may lead to fragility and financial crises, which in turn have severe recessionary effects on economic growth. Therefore, the State Bank of Pakistan may introduce protective measures that may undermine incidence of financial fragility and financial crises on economic growth. Among the nonswitching variables, labor force contributes negatively to economic growth. Therefore, there is a need to improve the quality of labor force through technical education and training. The physical capital is positively contributing to economic growth in Pakistan. The contribution of trade openness and government expenditures in economic growth observed to be insignificant. Therefore, policymakers may take necessary steps to increase the exports of goods and services by adopting export-led strategies. Furthermore, policies on better utilization of government expenditures may be familiarized so that fungibility practices may vanish. With these steps, both trade openness and government expenditures would contribute to economic growth. With respect to smoothed probabilities and regimes classification, we observed that the high-growth regime is relatively long-lived during the period 1975–2017. This indicates that during the period 1975–2017, growth of physical capital played a key role in enhancing economic growth in Pakistan. Therefore, policymakers may take appropriate measures to boost the growth of physical capital to achieve sustainable economic growth.

Policy Implications and Future Research Direction

The empirical findings of this study could offer implications for prudent macroeconomic policy regulations. The financial development exerts negative impact on economic growth in both the regimes. However, the response of economic growth to change in financial development is heterogeneous in the high- and low-growth regime. Therefore, the policymakers may consider nonlinear aspect of financial development in formulation of credit and monetary policies. Furthermore, State Bank of Pakistan may take appropriate initiative to balance the growth of financial sector and the growth of real sector of the economy. The findings suggest that the role of physical capital in promoting economic growth is important since financial development alone cannot drive the path for economic growth. Therefore, policymakers may frame policies that enhance capital accumulation, which is considered as an important component of economic growth.

Although, the present study offers insightful information with respect to finance-growth nexus in Pakistan based on the regime switching framework. However, the findings are subject to some limitations. The effect of financial development, following sudden changes in the political regime, would be interesting to study. It would also be more interesting to test the finance-growth nexus using the cross-country panel data. It would be more insightful to investigate the responses of economic growth to financial development using the quantile regression approach. We leave this for future research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.