Abstract

This present study explores the extent to which financial inclusion influences the impact of trade liberalization on sustainable economic growth. The empirical studies on the effects of trade liberalization on sustainable economic growth are inconclusive. More importantly, how financial inclusion mediates the relationship between trade liberalization and sustainable economic growth remains unexplored. We address these research gaps by employing the quantile fixed effects-OLS regressions model on data spanning the period 2000 to 2021 for 48 SSA countries. The effect of trade liberalization on sustainable economic growth proves to be affected positively by financial inclusion, and the effect of financial inclusion on sustainable economic growth is positively strengthened by an increase in trade liberalization. The study shows that there is a causal relationship between trade liberalization, financial inclusion, and sustainable economic growth. Our study shows novelty in that the marginal effects on sustainable economic growth increase when trade liberalization interacts with financial inclusion in SSA.

Introduction

Sustainable economic growth is a key focus in applied economics, with trade liberalization, financial inclusion, economic globalization, and institutional quality, among others, serving as key determinants. Empirical literature suggests that these factors influence sustainable economic growth in both developed and developing countries. Indeed, these factors have assumed a prominent role in differentiating between developing and developed countries (Adedokun & Ağa, 2023; Bunje et al., 2022a; Duodu & Baidoo, 2020; Ozturk & Ullah, 2022). This study focuses on the role of trade liberalization and financial inclusion in economic sustainability in Sub-Saharan Africa (SSA). It emphasizes that these factors are prerequisites for progress and competitiveness, enabling SSA to achieve sustainable economic growth, as mentioned in the Sustainable Development Goals (SDGs), specifically goal 8 (United Nations, 2015).

The new growth theory offers insights into the relationship between trade and economic growth. However, the empirical literature does not permit consensus. Thus, trade liberalization can promote or worsen sustainable economic growth (Islam et al., 2022; Obobisa et al., 2021). Trade liberalization promotes specialization in goods and services that countries have a comparative advantage in, resulting in improved production efficiency and increased productivity. Countries rich in resources may export natural resources, while technologically advanced nations may export high-tech products (Asamoah et al., 2019; Egyir et al., 2020). For example, the empirical studies have provided convincing evidence suggesting that trade liberalization fuels economic growth in Africa through various channels, including the expansion of markets, technological advancements, and infrastructure development (Asamoah et al., 2019; Cudjoe et al., 2021; Duodu et al., 2024; Duodu & Baidoo, 2020; Egyir et al., 2020; Sakyi et al., 2017). Similarly, studies in other regions across the globe have also provided evidence indicating that trade liberalization promotes sustainable economic growth(Islam et al., 2022; Zuo et al., 2023). Conversely, it is also argued in the empirical literature that, trade liberalization can lead to a rise in both production and consumption, which in turn exerts pressure on natural resources, resulting in environmental degradation and pollution. Industries sometimes prioritize financial gains above sustainable standards, resulting in the detrimental consequences of deforestation and habitat devastation (Abendin et al., 2024; Ma et al., 2022). For instance, the empirical studies also suggested that trade liberalization negatively impacts sustainable economic growth (Bunje et al., 2022a; Fatima et al., 2020; Obobisa et al., 2021; Wasti & Zaidi, 2020).

Also, the role of financial inclusion in sustainable economic growth is unavoidable. Financial inclusion facilitates access to credit for individuals and businesses, promoting investment in education, healthcare, and entrepreneurship. This, in turn, stimulates economic activity, job creation, and contributes to overall economic growth (Lee et al., 2023). Moreover, financial inclusion initiatives promote income equality by facilitating the inclusion of marginalized and low-income groups in the formal financial system. This inclusion enhances their economic status, enables access to improved education and healthcare, and fosters more effective contributions to the economy (Hussain et al., 2024; Lee et al., 2023). For instance, the study by Chima et al. (2021) conducted in sub-Saharan African (SSA) context, concludes that financial inclusion promotes economic growth in the region. Moreover, Adedokun and Ağa (2023) suggest the positive impact of financial inclusion on economic growth in the SSA region. Okelele et al. (2022), provide evidence that financial inclusion increases sustainable economic growth in SSA economies. Ozturk and Ullah (2022) support the positive impact of financial inclusion on sustainable economic growth for countries along the One Belt and Road Initiative (OBRI) region. A more recent study by Hussain et al. (2024) concludes that financial inclusion promotes sustainable economic growth. Conversely, financial inclusion, in the absence of regulatory oversight and risk management measures, can result in financial instability. This can strain the financial system and have a negative impact on economic growth, primarily due to reckless lending practices (Mulungula & Nimubona, 2022). Benczúr et al. (2019) and Mulungula and Nimubona (2022), concludes that financial inclusion hurts sustainable economic growth. Given the current literature on trade liberalization and financial inclusion and their relationship with economic growth, it suggests that this is not conclusive. Thus, it contains both positive and negative effects.

This article aims to examine the impacts of trade liberalization and financial inclusion on sustainable economic growth in the Sub-Saharan African (SSA) region, based on the existing literature gaps. The study will explore both the direct and indirect effects of trade liberalization and financial inclusion on sustainable economic growth. Our study contributes to the current debate on the trade liberalization-finance-growth nexus in several ways. Firstly, the contribution of this study stems from the fact that it is the first to study the trade liberalization-financial inclusion-growth nexus in the context of SSA countries. Most of the studies in the SSA context focus on the trade liberalization-growth nexus or the financial inclusion-growth nexus. For instance, prior studies by Asamoah et al. (2019), Duodu and Baidoo (2020), Egyir et al. (2020), Oloyede et al. (2021), Bunje et al. (2022a), focused on trade liberalization-growth, while those by Anarfo et al. (2019), Chima et al. (2021), and Wang et al. (2023) studied the relationship between financial inclusion and sustainable economic growth in SSA countries. Secondly, it contributes to the existing literature by providing empirical evidence on the complementarities between trade liberalization and financial inclusion for sustainable economic growth in Africa. Apart from the study by Egyir et al. (2020), which investigated only the nexus between financial inclusion, trade, and economic growth in Africa, to the best of our knowledge, this is the first study to investigate the interaction between trade liberalization and financial inclusion on sustainable economic growth in the SSA economies context. Thirdly, our study contributes to the existing body of literature by quantifying the threshold level at which financial inclusion can influence the positive impact of trade liberalization on sustainable economic growth.

In addition to the introductory section and the presentation of stylized facts in Section 1, Section 2 of the paper provides a comprehensive overview of the relevant literature. Moreover, Section 3 expounds on the methodology employed, Section 4 discusses the findings, and Section 5 concludes with the policy ramifications.

Overview of Trade Liberalization, Financial Inclusion and Economic Growth

This part of the study analyzes data on trade liberalization, financial inclusion, and economic growth to contextualize Africa’s position relative to other regions worldwide. Figure 1 illustrates the trade liberalization in Sub-Saharan Africa (SSA) and selected regions, as per the World Bank Development Indicators (WDI). We measure trade liberalization by dividing a region’s total merchandise trade by its gross domestic product (GDP). The results indicate that trade liberalization values are higher in the Middle East and North Africa (MENA), East Asia and Pacific (EAP), Europe (EU), and Latin America and Caribbean regions compared to SSA. The implication is that the countries within the SSA region are comparatively slower in implementing trade liberalization measures when compared to other regions. This aligns with the argument that Africa’s trade liberalization has been underwhelming in comparison to other regions (Abendin & Duan, 2021; Manwa & Wijeweera, 2016).

Regional distribution of average trade liberalization, 2021.

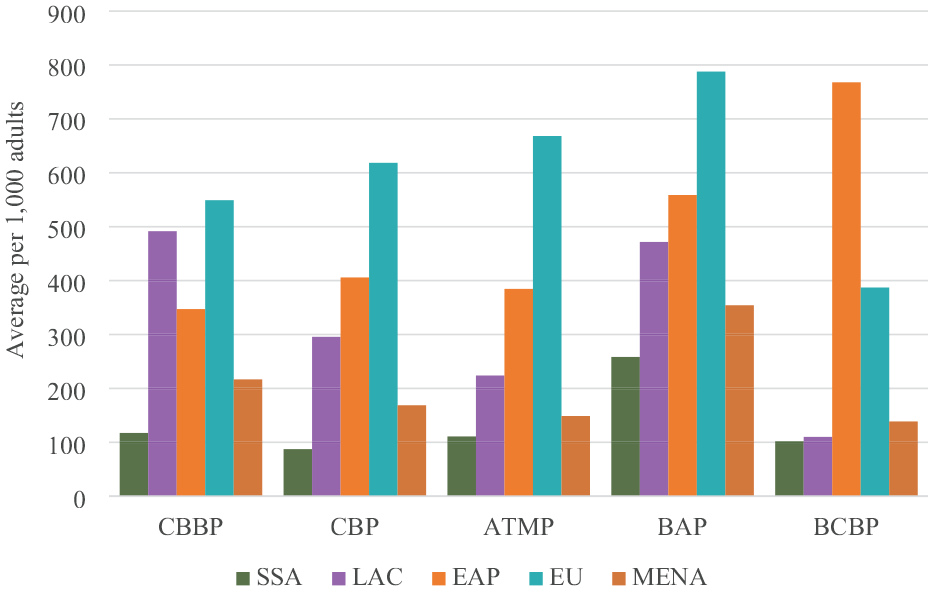

We compute financial access measures from the World Bank Database for financial inclusion to evaluate each selected region’s performance over a 22-year average (2000–2021). Based on the outcomes, the EU countries are leading in all the measures of financial inclusion. The results show that the EU’s member states are at the forefront of financial inclusion across the board, while the SSA region, when compared with other regions, is lagging behind. For instance, in terms of the commercial bank branches per 1,000 adults (CBBP), every 1,000 adults have access to 117 branches of commercial banks in the SSA region, which is lower than regions like the Middle East and North Africa (MENA; 217), the European Union (549), East Asia Pacific (347), and Latin America and the Caribbean (492). Moreover, a similar trend of results is observed for the other measures of financial inclusion, as shown in Figure 2. These results suggest that the SSA region is associated with relatively low financial inclusion compared to the other regions.

Regional distribution of financial inclusion, 2021.

Figure 3’s study of GDP per capita indicates that SSA performs less well economically than other areas. Our studies of the stylized facts assume that ineffective trade liberalization and insufficient financial inclusion in the region are the reasons for SSA’s dismal performance on the average GDP computed across time. This serves as a preamble to the empirical analysis below. The observed gains in GDP in the areas with high levels of trade liberalization and financial inclusion demonstrate this. The data illustrates that other regions with substantial trade liberalization have a robust financial inclusion framework and increased economic performance (GDP), highlighting the crucial role that financial inclusion plays as an intermediary. For policy implications, however, a valid and trustworthy empirical study is needed to determine how much trade liberalization can improve economic sustainability and how much financial inclusion can mediate between the two. This is what the next sections will discuss.

Regional distribution of average GDP per capita.

Literature Review and Hypothesis Statements

Trade Liberalization and Sustainable Economic Growth

Economic growth and trade openness theories propose that global trade is the primary driver of economic progress. While Heckscher-Ohlin theory (Heckscher, 1919; Ohlin, 1933) employs factor endowments and Krugman (1979) intra-industry trade theory utilizes product differentiation and domestic economies of scale for development, classical theory places emphasis on absolute and comparative advantage. These theoretical foundations can be traced back to influential works like Smith (1776), which first presented the idea of absolute advantage and highlighted the advantages of specialization and trade in promoting growth. Expanding on Smith’s research, Ricardo (1817) introduced the theory of comparative advantage, suggesting that nations could gain from trade despite lacking an absolute advantage in producing all commodities. After the Ricardo theory, Heckscher (1919) and Ohlin (1933) further expanded the knowledge of trade-growth by developing the Heckscher-Ohlin model, which highlighted the role of factor endowments in determining trade patterns and hence growth. Krugman (1979) examined the relationship between trade and growth, focusing on product differentiation and economies of scale in intra-industry trade. He highlighted that economies could gain from trade even without variations in factor endowment. These foundational works are crucial for shaping research on the complex connection between trade and economic growth. Empirical studies in Africa and other regions consistently support the positive impact of trade on economic growth within a theoretical framework. The following sections provide a concise examination of empirical research on trade liberalization, financial inclusion, and economic growth.

The empirical literature presents conflicting findings regarding the impact of trade liberalization on sustainable economic growth, leaving the argument unresolved. However, the majority of empirical research suggests that trade liberalization is essential for promoting sustainable economic growth. For instance, Sakyi et al. (2017) investigate the effects of trade liberalization and trade facilitation on economic growth in Africa using the GMM approach. They find trade liberalization beneficial to the economic growth of African countries. The results of the study further suggest that trade facilitation serves as an important channel through which trade affects economic growth. Gnangnon (2018) study the effect of trade liberalization on economic growth in selected developing and developed countries across the globe. Using the two-step GMM estimator, it is concluded that trade positively affects the economic growth of developing and developed countries. Similarly, Asamoah et al. (2019) investigates the effect of trade liberalization and FDI on economic growth in 34 sub-Saharan African countries. Using the structural equation modeling (SEM) technique, the study outcome reveals that trade liberalization leads to an increase in economic growth in the selected SSA countries. Moreover, Egyir et al. (2020) examine the impact of trade openness on economic growth in African countries using the dynamic system GMM technique. The study found that trade promotes economic growth in Africa in both the short- and long-run. Focusing on Ghana, Duodu and Baidoo (2020) examine how institutional quality influences the effect of trade openness on the Ghanaian economy using the autoregressive distributed lag model (ARDL) estimation model. The authors suggest that trade openness has a direct positive impact on economic growth as well as positive indirect impact on growth through institutional quality.

In the same vein, Abendin and Duan (2021) explored the role of international trade in Africa’s economic growth. The authors document mixed results using various econometric approaches. They found that a pooled OLS regression trade hurts economic growth while promoting it using the GMM, random, and fixed effects approaches. These findings imply that the method of estimation has an influence on the impact of trade on economic growth. Moreover, Cudjoe et al. (2021) examines the economic growth effects of China’s aid, trade and FDI flows to Africa. In a more recent study in the context of Africa, Duodu et al. (2024), used AMG and IV-2SLS estimators and data from sub-Saharan African countries to examine how Chinese and American trade impact economic growth. the study found that both China and the US trade with African countries, which promotes economic growth in the region. Barros and Martínez-Zarzoso (2022) conducted a systematic review of studies examining the impact of international trade and trade liberalization policies on socio-economic indicators related to the Sustainable Development Goals (SDGs). The review on trade liberalization and sustainable economic development demonstrates the positive impact of liberalization on sustainable development. Zuo et al. (2023) investigated the economic growth effects of trade openness and natural resources development. They claimed that trade openness enhances sustainable economic growth in China. Islam et al. (2022) focused on the Kingdom of Saudi Arabia and examined the impact of trade openness on economic growth using the Auto-Regressive Distributed Lag (ARDL) cointegration regression model. The study discovered that trade liberalization promotes economic growth in the Kingdom of Saudi Arabia.

However, despite the theoretical and majority of the empirical literature, as shown above, asserting that trade promotes economic growth, other empirical studies have posited negative effects of trade liberalization on sustainable economic growth. This suggests that the impact of trade liberalization on economic growth is not conclusive. Thus, it contains both positive and negative effects. For instance, a study by Bunje et al. (2022a) investigated the effects of trade liberalization on economic growth in Africa. The outcomes of the study indicated that trade liberalization hurts economic growth in African countries. A similar study by Wasti and Zaidi (2020) conclude on a negative impact of trade liberalization on economic growth. Fatima et al. (2020), investigate trade openness-growth nexus using the two-step system GMM estimation method in a panel data of 34 developed and developing economies over the period 1980 to 2014. The results of the study in that trade openness negatively affect economic growth in economies with low human capital development. In addition, Obobisa et al. (2021) explored the impact of China-African trade on economic growth for 24 African countries using the feasible generalized least squares (FGLS) estimation technique, the authors claimed that China-African trade negatively impact African economic growth, while China’s FDI inflows to Africa promotes economic growth in the region. Further, Abendin and Duan (2021) provided evidence that trade negatively affects economic growth in Africa in a pooled OLS estimator, while the system GMM estimator suggested positive impact of trade liberalization on economic growth. Based on the dominant view about the effect of trade liberation on sustainable economic growth in the empirical literature and the theoretical views mentioned above, we hypothesized that:

Financial Inclusion and Sustainable Economic Growth

The issue of financial inclusion has garnered significant interest since the late 1990s, primarily driven by policy-making and research studies that have highlighted the financial exclusion of marginalized individuals. From a theoretical perspective, the endogenous growth theory posits that economic growth is not exclusively determined by external factors such as the accumulation of labor and capital but is also shaped by internal factors driven by knowledge, innovation, and technological advancement. The theory asserts that financial inclusion facilitates the ability of individuals and businesses to take advantage of financial services, thereby fostering investments in education and the improvement of skills. Financial inclusion has the potential to foster the development of human capital through the facilitation of credit, savings, and insurance accessibility. Enhanced human capital plays a pivotal role in fostering productivity gains, driving innovation, and facilitating technological advancements, all of which are critical factors for achieving sustainable economic growth.

Regarding the empirical literature view, Kempson and Whyley (1999) reported that, the provision of a fundamental bank account is imperative for individuals with low income to gain entry into formal financial systems. Kim et al. (2018) investigate how 55 Organizations of Islamic Cooperation (OIC) nations’ economic growth is affected by financial inclusion. According to the study’s findings, financial inclusion helps the OIC members’ economies flourish. Gao (2022) investigated the role of financial inclusion in economic growth in developing economies from 1990 to 2020. The study found that financial inclusion positively influences economic recovery in developing economies. Huang et al. (2021) also examined whether urbanization, international commerce, and economic growth support environmental sustainability in 34 SSA nations using panel quantile regression. They discovered that the SSA region’s environmental sustainability is enhanced by international trade. In a same vein, Okelele et al. (2022) used the feasible generalized least square (FGLS) method to investigate the impact of trade on the ecological footprint in Sub-Saharan Africa. They found that trade openness improves the environment by reducing the ecological footprint. The PHH and scale effect theories in SSA were not supported by these investigations.

Younas et al. (2022) conducted a study that provides additional evidence to support the notion that trade activities in developing nations have economic growth effect from financial inclusion. Likewise, Liu et al. (2021) examined the role of digital financial inclusion on Chinese economic growth from 2011 to 2019 and reported that China’s digital financial inclusion induces higher economic growth. Chima et al. (2021) examined the nexus between financial and economic growth sustainability in SSA countries from 1995 to 2017. Their study shows that financial inclusion increases sustainable economic growth in SSA countries. Similarly, Chinoda (2020) employed the dynamic pairwise Granger causality to examine financial inclusion-trade-economic growth nexus in Africa. The authors concluded a causal relationship between financial inclusion and economic growth in the region. In line with the theoretical arguments of the Heckscher-Ohlin theory in favor of factor endowment of an economy, and the empirical review, financial inclusion can be considered as a factor endowment. Hence, we hypothesize that:

Financial Inclusion and Trade

The theory of comparative advantage, as formulated by David Ricardo, posits that economies ought to concentrate their production efforts on goods and services in which they possess a comparative advantage. By engaging in international trade, countries can reap the benefits of specialization and exchange. This study posits that financial inclusion can contribute to the support of the aforementioned theory by granting individuals and businesses the means to access financial services that enable investment in sectors where they possess a comparative advantage. Trade liberalization can then facilitate the entry of these specialized sectors into expanded markets, thereby leading to sustainable economic growth and development. Previous empirical research has demonstrated favorable outcomes in the link between financial inclusion and trade liberalization (Chinoda, 2020; Hajilee & Niroomand, 2019). For instance, Hajilee and Niroomand (2019) concluded that financial inclusion positively influences trade openness. Chinoda (2020) reported a shred of evidence that indicates a causal relationship between financial inclusion and trade. However, the study by Mulungula and Nimubona (2022) documented the negative trade liberalization effects of financial inclusion in Africa. Given the existing literature’s positions and the theoretical arguments, we therefore hypothesized that:

Methodology

Theoretical Framework and Empirical Model Specification

This study employed a panel data of 48 Sub-Saharan Africa (SSA) countries over the period 2000 to 2021. All the 48 SSA countries were chosen due to the fact that there is data available for them with respect to our studied period. This study paper applies endogenous growth theory to model the functional relationships between trade liberalization, financial inclusion, and sustainable economic growth (SUSEG) in SSA. Endogenous growth theory challenges two key assumptions made by the Solow growth theory. Firstly, it questions the notion that technological change is identified externally, suggesting instead that it is influenced by internal factors within an economy. Secondly, it challenges the assumption that all countries have equal access to the same technological opportunities (Barro, 1996; Howitt, 2018; Silberberger & Königer, 2016; Waverman et al., 2005). Moreover, the concept of diminishing returns on a limited definition of capital, which solely encompasses physical capital, is replaced by the assumption of constant returns on a comprehensive measure of capital that encompasses human capital and infrastructure as well. Endogenous growth theory posits that technology and knowledge are regarded as economic goods that play a crucial role in elucidating long-term growth through mechanisms such as learning-by-doing, investment in human capital, and the adoption of new technologies (Barro, 1996; Waverman et al., 2005). The selection of this theory is justified by four motivations. Firstly, the neoclassical Solow growth model inadequately addresses the effects of trade and regulations, whereas endogenous growth theory provides a comprehensive framework for understanding these impacts (Silberberger & Königer, 2016). Secondly, the theory provide a fundamental reference point benchmark for analyzing variations in output per worker growth rates among different economies (Busse et al., 2012; Mankiw et al., 1992). Thirdly, the theory recognizes the significance of human capital as a critical resource for enhancing productivity of labor and fostering economic growth (Zahonogo, 2016). Lastly, given that this study aims to examine the influence the impact of trade liberalization and financial inclusion on SUSEG, the theory is deemed suitable from both theoretical and empirical perspectives. Empirical studies including, Abendin and Duan (2021), Egyir et al. (2020), and Duodu et al. (2024), suggest that trade liberalization and financial development are key determinants of economic growth. This study measured financial development based on five indicators In accordance with the theory of endogenous growth and supported by empirical research, a linear panel growth model is developed to examine the impact of LIB on SUSEG. The model is formulated as follows:

Here: lnSUSEGit denotes the sustainable economic growth index; CAPit represents capital; HCAPit denotes human capital development index; LIBit is the trade liberalization; Xit represents the selected control variables, which includes: Financial development (FD), foreign direct investment (FDI), and government expenditure (GOVEXP). Prior studies including, Abendin and Duan (2021), Egyir et al. (2020), and Bunje et al. (2022a) used similar variables as control factors. while ϑit is the error term. The equation can thus be rewritten to capture the variables explicitly thus:

To also investigate the role of financial inclusion (FINDEX) in the attainment of SDG-8. In this study, FINDEX is measured using four indicators: commercial banks branches per 1,000 adults, commercial banks per 1,000 adults, numbers of ATMS per 1,000 adults, bank accounts per 1,000 adults, borrowers from commercial banks per 1,000 adults to create an index using the principal component analysis (PCA) technique as in Odugbesan et al. (2022). The great possibility for multicollinearity and the loss of degrees of freedom make it impossible to incorporate all of these variables in the same model. To analyze the impact of financial inclusion on sustainable growth in SSA countries, a more comprehensive approach is possible by creating a composite financial inclusion index that captures the direction of greatest variance between all the variables stated above. rewrite Equation 2 to capture financial inclusion impact thus:

Further, we examine the interactive impacts of LIB and FINDEX, we estimate the relationships among them and their combined effects in the following equation:

The data for all the variables were transformed to their natural logarithms form before using them for the estimation of the results. The purpose of converting the variables into their natural log is for data consistency, since the variables applied in this study are measured in different unit (Table 1).

Variables Description.

Estimation Strategies

The study performs preliminary analyses on the sample variables, such as cross-sectional dependence (CD), heterogeneity, unit root, cointegration tests, and normality test to guarantee unbiased estimates. The existence of CD, non-stationarity, and lack of cointegration might result in erroneous findings, as stated by Pesaran (2007). Hence, the Pesaran (2004) CD test was used to examine the presence or absence of cross-sectional independence. In addition, Likewise, making the mistake of assuming slope homogeneity in cases where slopes are actually heterogeneous typically leads to inaccurate inferences. Therefore, the data series is examined for heterogeneity using the slope heterogeneity (SH) test proposed by Pesaran and Yamagata (2008). Further, understanding a time series’ stationary or non-stationary nature is crucial for selecting the right econometric model, as statistical techniques like regression analysis may yield misleading results if they are applied on non-stationary data. The Pesaran (2007) cross-sectionally augmented ADF (CADF) and IPS (CIPS) tests are performed to ensure that our variables are stationarity to avoid biased results. The Westerlund (2007) cointegration test was applied to check whether there is a long-run relationship among the variables or not. The Westerlund cointegration test is highly efficient in addressing cross-sectional dependency and provides four cointegration testing outcomes. Consequently, it becomes a valuable instrument for examining the enduring relationships among parameters in data (Westerlund, 2007).Based on the CD test (Table 3), heterogeneity (Table 3) and the normality check (Table 2), this study found that the presents of CD, heterogeneity and that the data is non-normally distributed. Therefore, these results underpin the suitability of the quantile regression (QR) and Driscoll-Kraay fixed effect OLS methods for this study. The QR technique builds upon the influential studies conducted by Koenker and Bassett (1978), Koenker (2005), and Powell (2022). The QR estimation model is robust to the non-normal distribution of the data as it the case of this study. Moreover, we utilized Driscoll-Kraay fixed effect-OLS approach proposed by Driscoll and Kraay (1998) to solve the problems of CD and the heterogeneity found in the data. Furthermore, the novel Second-stage instrumental (2SIV-DPD) model by Kripfganz and Sarafidis (2021),was employed to account for the econometric issue of endogeneity of possible reverse causality between trade liberalization and sustainable economic growth. Trade liberalization has the potential to foster economic growth by enhancing market accessibility and fostering healthy competition. Conversely, economic growth can also lead to an increase in trade liberalization. Economies that are affluent, possess abundant resources, and exhibit political stability are more inclined to effectively implement policies promoting free trade. In this study, we specifically employed the one lag values trade liberalization and sustainable economic growth as their IVs.

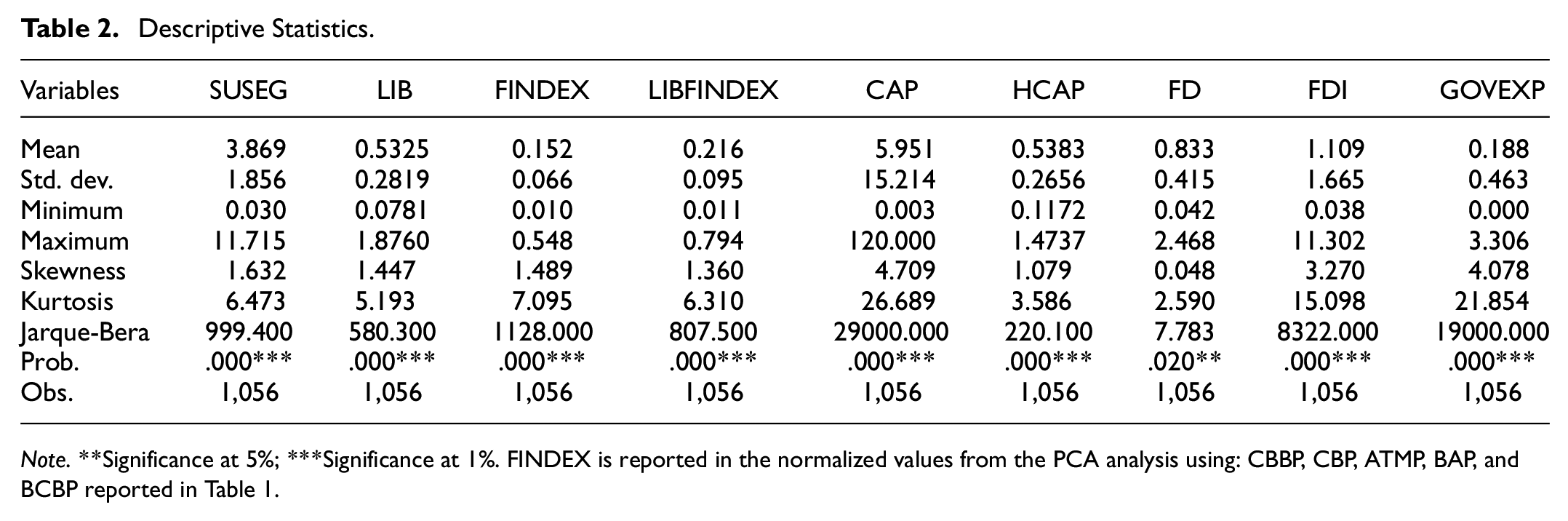

Descriptive Statistics.

Note. **Significance at 5%; ***Significance at 1%. FINDEX is reported in the normalized values from the PCA analysis using: CBBP, CBP, ATMP, BAP, and BCBP reported in Table 1.

Cross-Sectional Dependency and Slope Homogeneity Results.

Significance at 10%; ***Significance at 1%.

The literature generally acknowledges that the presence of a relationship among the two variables does not always imply causation between them (Bunje et al., 2022b). Therefore, the Dumitrescu and Hurlin (DH; 2012) causality test is employed to ascertain the causal linkage between trade liberalization, financial inclusion, and sustainable economic growth. The DH test effectively addresses the issue of heterogeneity in slope parameters and mitigates cross-sectional dependence, rendering it a viable and effective approach for establishing causal relationships.

Empirical Results and Discussions

Descriptive Statistics

Table 2 presents the descriptive statistics for the variables applied in this study. Upon a quick review of Table 2, it becomes apparent that SUSEG and CAP exhibits the highest level of volatility among all the variables, as seen by a direct comparison of their means and standard deviations. This is because on average, SUSEG and CAP have shown relatively higher dispersion around the mean values as their standard deviations does deviate largely from the mean. Comparing the mean values, CAP tend to be associated with the highest mean value of 5.951, followed by SUSEG with a mean value of 3.869, while FINDEX is associated with the lowest mean value of 3.869 when with the rest of the variables applied in this study. The Jarque-Bera test was conducted to check normality of the data. The null hypothesis in this test postulates a normal distribution, while the alternative hypothesis posits that the data deviates from a normal distribution. The Jarque-Bera (JB) results reported in Table 2 suggest that the data of the series is not normally distributed by rejecting the null hypothesis of normal distribution at 1% significance level for all the series.

Cross-Sectional Dependency and Slope Homogeneity

As aforementioned, the data series have been analyzed for cross-sectional dependence to ensure unbiased outcomes, and the outcomes have been documented in Table 3. The table indicates that all tests conducted provide evidence to reject the null hypothesis of no cross-sectional dependence, even at a significance level of 1%. The results of the SH tests indicate that the null hypothesis pertaining to slope homogeneity ought to be rejected, even when considering a significance level of 1%. The findings suggest that the analytical methods utilized in the study must possess the capability to address the challenges linked with cross-sectional dependence (CD) and slope homogeneity (SH).

Panel CIPS and CADF Unit Root Test

Table 4 presents the results of the panel stationarity test. According to the information presented in the Table, it can be observed that all variables exhibit nonstationarity in their level forms, but achieve stationarity upon being subjected to differencing. Due to the presence of CD and heterogeneity in the sample data, it is essential to utilize second-generation unit root tests and estimators that consider CD to guarantee reliable and stable estimates.

Panel CIPS and CADF Unit Root Test Results.

Significance at 5%; ***Significance at 1%.

Westerlund (2007) Cointegration Test

From an economic standpoint, the presence of CD indicates that fluctuations in the variables are interconnected. This necessitate the use of second-generation cointegration test such as the Westerlund (2007) test which is capable of handling the issue of cross-sectional dependence. The findings of the panel cointegration tests, as presented in Table 5, validate the presence of a long-run association between the predictors and sustainable economic growth. The null hypothesis of no cointegration is rejected by all four tests, even when considering a significance level of 1%. The results suggest a long-term connection between the variables, supporting the computation of long-term characteristics in this study.

Westerlund (2007) Cointegration Test.

Significance at 5%; ***Significance at 1%.

Panel Estimation Results

Table 6 demonstrates that the employed methodologies (QR and Driscoll-Kraay fixed effect-OLS) yield comparable results, with negligible variations observed in terms of the magnitudes of the variables and their statistical significance. The findings derived from both approaches demonstrate that liberalization, financial inclusion, capital, human capital development, financial development, foreign direct investment, and government expenditure have a significant effect on the sustainable economic growth of African nations. Moreover, the interaction between trade liberalization and financial inclusion significantly affects sustainable economic growth. Concerning the QR results, as shown in Table 6, 1% increase in trade liberalization (LIB) causes sustainable economic growth to increase by 3.388% at the beginning stage (Q_25), by 4.214% (Q_50), by 5.281% (Q_75) in middle stages and by 5.505% at the latter stage (Q_95). The findings suggest that trade liberalization has a favorable conditional marginal impact on sustainable economic growth across all the quantiles examined. This outcome is justifiable as trade liberalization measures are widely considered to be one of the key determinants that impact the attainment of sustainable economic development. This is because trade liberalization provides countries with the opportunity to not only produce and export environmentally sustainable goods to the international market, but also to procure a diverse range of eco-friendly products from other countries. This suggests that nations can foster their trade activities while safeguarding their ecological well-being, thereby attaining sustainable economic growth in the long-run. Another economic argument in favor of the result is that, trade liberalization policy incentivizes nations to prioritize industries in which they possess a comparative advantage, resulting in higher productivity, increased output, and sustainable economic growth. The present analytical inference indicates that the augmentation of trade liberalization can potentially contribute to the promotion of sustainable economic growth in Africa. This finding is in line with theoretical of views the endogenous growth theory, classical theory of trade, and Heckscher-Ohlin theory. Empirically, the result is inconsistent with Manwa and Wijeweera (2016) and Wasti and Zaidi (2020) and consistent with Egyir et al. (2020), and Zuo et al. (2023) which indicate a favorable impact of trade liberalization on economic growth. Hence, our results confirm

Quantile Regression and Driscoll-Kraay Fixed Effect-OLS Results.

Note. Standard errors are reported in parentheses.

Significance at 10%; **Significance at 5%; ***Significance at 1%.

The results across the quantiles also show that there is a positive relationship between financial inclusion and sustainable economic growth in the 48 African countries. It can be seen that as financial inclusion increases by 1%, sustainable economic growth increases by 3.043% at Q_25, by 2.788% at Q_50, by 3.158% at Q_75, and by 2.429% at Q_95. This is an indication that financial inclusion has a positive conditional marginal effect on sustainable economic growth in SSA. The present discovery suggests that financial inclusion can have significant economic implications by facilitating the involvement of marginalized and low-income individuals in the formal financial system, thereby contributing to the reduction of income inequality. The provision of financial services, such as savings accounts, credit, and insurance, can facilitate effective financial management, asset accumulation, and resilience to financial adversity for individuals. Consequently, this aids in mitigating the disparity in wealth, fostering all-encompassing economic expansion, and augmenting societal unity. The finding aligns with those of Kim et al. (2018), and Gao (2022) who concluded that nations with a greater degree of financial inclusion and more modern technology have better sustainable economic growth. Thus, giving credence to the

The study indicates a positive interaction between trade liberalization and financial inclusion across all quantiles. Based on these findings, we can conclude that the positive impact of trade liberalization on sustainable economic growth is proportional to the degree of financial inclusion in the 48 SSA countries. The implication of this result is that a 1% improvement in extent to which of financial inclusion complements trade liberalization is associated with 1.261%, 1.773%, 3.158%, 2.631%, increase in sustainable economic growth at Q_25, Q_50, Q_75, and Q_95, respectively in SSA countries. Thus, in the presence of financial inclusion, trade liberalization overwhelmingly stimulates sustainable economic growth. The result further indicates that the potential complementarity between trade liberalization and financial inclusion in stimulating sustainable economic growth is effective in SSA countries. Hence, confirming the hypothesis H3 of this study that the interaction effect of trade liberalization and financial inclusion positively influence sustainable economic growth in SSA economies.

Regarding the control variables, the results reveal that, physical capital (CAP), and financial development (FD) decrease sustainable economic growth. However, the sustainable economic growth effects of human capital development (HCAP), foreign direct investment (FDI), and government expenditure is positive, but the FDI coefficients are only significant in the Q_25 and Q_95. Specifically, a percentage increase in CAP decreases sustainable economic growth by 0.020%, 0.017%, 0.021% and 0.019%, at Q_25, Q_50, Q_75, and Q_95, respectively. This indicates that as physical capital increases, sustainable economic growth decreases for the 48 African economies. This result is in line with the findings of Jiahao et al. (2021) who provide evidence that physical capital negatively impact sustainable economic growth, while in contrast with those of Huang et al. (2021) who showed positive impact of capital on economic development. With respect to FD, the results indicate that a 1% increase in financial development decreases sustainable economic growth in Q_25, Q_50, Q_75, and Q_95 by approximately 0.002%, 0.003%, 0.005%, and 0.004%, respectively. These findings suggest that financial development initiatives in Sub-Saharan Africa do not effectively support sustainable economic growth, despite their intended purpose. The pursuit of growth and development in SSA economies necessitates the adoption of policies that prioritize economic growth over sustainable economic growth. Hence, it is imperative for policymakers in the SSA economies to prioritize policies that foster the sustainable economic growth. This finding conforms to the study by Jiahao et al. (2021) who concluded that financial development decreases economic growth sustainability, while in contrast with those of Hung (2023) who posits that financial development promotes economic sustainability.

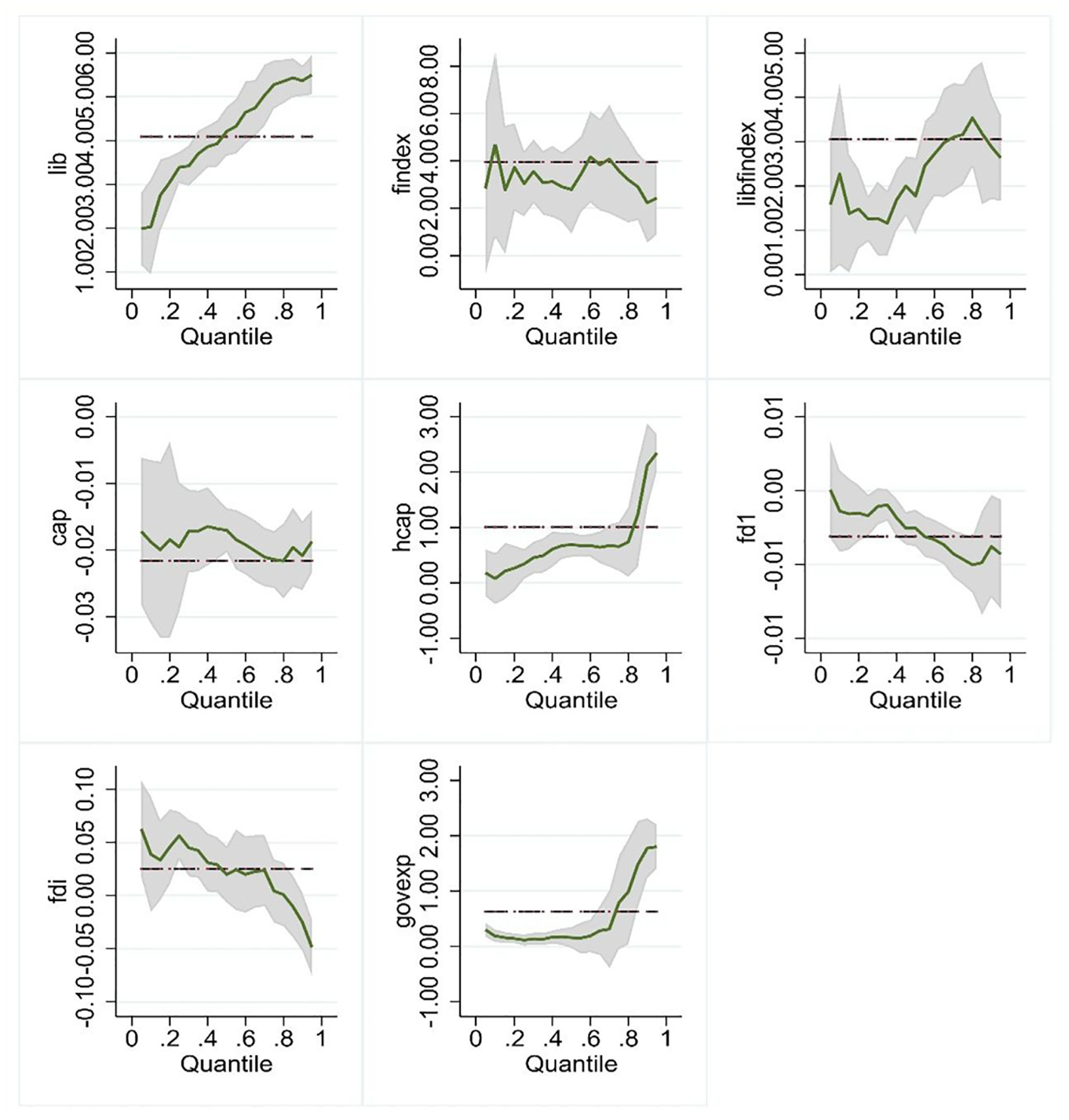

Furthermore, the results in Table 6 show that an additional increase in HCAP increases sustainable economic growth in Q_25, Q_50, Q_75, and Q_95 by about 0.341%, 0.687%, 0.659%, and 2.348%, respectively, with other variables, held constant. The results suggest that HCAP plays a significant role in promoting sustainable economic growth in SSA in all the quantiles. With regards to foreign direct investment (FDI), the coefficients suggest that a 1% rise in FDI inflows increases sustainable economic growth in Q_25, and Q_95 by about 0.056%, and 0.049%, respectively keeping other covariates constant. The result implies that FDI inflows in SSA directed toward sustainable investments will stimulate sustainable economic growth. The findings in SSA are in line the results documented by Ozturk and Ullah (2022). Turning to the government expenditure (GOVEXP), we observed from Table 6 that a 1% increase in GOVEXP is associated with an increase in sustainable economic growth in the SSA region by 0.120%, 0.160%, 0.797%, and 1.805% for Q_25, Q_50, Q_75, and Q_95, respectively. This outcome indicates that government spending on developmental initiatives brings about sustainable economic growth. The allocation of public funds by governments for the purpose of constructing and sustaining infrastructure, including but not limited to transportation systems including roads, bridges, railways, ports, and communication networks. This phenomenon stimulates economic activity, improves trade and commerce, encourages investments, and boosts productivity. These results are additionally confirmed through Figure 4.

Panel quantile regression coefficients. Source: Author(s) own computations.

The Driscoll-Kraay fixed effect ordinary least squares analysis is employed as a robustness check for the quantile regression findings. The results of this analysis corroborate the outcomes derived from the quantile estimation. It can be seen from Table 6 that the core independent coefficients which are trade liberalization, financial inclusion and the interaction between trade liberalization, and financial inclusion all have positive relations with sustainable economic growth. Specifically, the estimated coefficients suggest that a percentage increase in trade liberalization increase sustainable economic growth by 3.017%. Similarly, the coefficient of financial inclusion indicates that increase sustainable economic growth by 5.199% when there is a 1% increase in financial inclusion in SSA countries. The sign of the interaction between trade liberalization and financial inclusion is likewise positively significant, indicating that improvements in financial inclusion help increase the ability of trade liberalization to increase sustainable economic growth in SSA countries. Thus, a 1% improvement in financial inclusion would stimulate trade liberalization effect on sustainable economic growth by 4.450%, holding all other variables constant. Hence, the Driscoll-Kraay fixed effect-OLS model also confirmed that the expected complementarity between the financial inclusion and trade liberalization in stimulating sustainable economic growth in SSA countries is effective.

Regarding the possible endogeneity issue, Table 6 suggest that the results of 2IV-DPD are similar to the quantile regression results. All the parameters (LIB, FINDEX, LIBFINDEX, CAP, HCAP, FD, FDI, and GOVEXP) show similar effects on sustainable economic growth. The results in Table 6 also indicate that past sustainable economic growth adjustments do not lead to convergence, indicating the need for sustainable economic growth policies. Thus, the coefficient indicates that sustainable economic growth has decreased from its past value. The p values estimate of the Sargan, and Hansen, exhibit both efficiency and consistency. Thus, the results in Table 6 show that there is not enough evidence to reject the null hypothesis of instrument exogeneity using the Difference in Hansen Test (DHT).

Our study contributes to the existing body of literature by quantifying the threshold level at which financial inclusion can influence the impact of trade liberalization on sustainable economic growth. The financial inclusion threshold value is calculated by dividing the coefficient of trade liberalization by the coefficient of the interaction term; Q25: 3.388/1.261 = 2.687, Q50: 4.214/1.773 = 2.377, Q75: 5.281/3.158 = 1.672, Q95: 5.505/2.631 = 2.092 as in Asongu et al. (2020). The findings suggest that trade liberalization has a positive impact on sustainable economic growth, which may be further enhanced when the calculated threshold for financial inclusion is surpassed.

Marginal and Net Effects Trade Liberalization on Sustainable Economic Growth as Financial Inclusion Increase

In order to determine the true impact of trade liberalization on sustainable economic growth in SSA countries, this study also looks at the marginal effects of trade liberalization on sustainable economic growth when financial inclusion is maximized. To do so, we generated the partial derivatives of sustainable economic growth with respect to trade liberalization at the 25th, 50th, 75th, and 95th percentiles.

Table 7 clearly shows that when financial inclusion is at its mean for all quartiles at the 1% level, the marginal effect of the conditional impact of trade liberalization boosts sustainable economic growth in the SSA region. In particular, the coefficients indicate that if trade liberalization in SSA countries increases by one-point, sustainable economic growth will be improved, with estimates ranging roughly from 4.936% to 5.516% at all percentiles, when financial inclusion in SSA is at its mean.

The Marginal and Net Effects of LIB on SUSEG as FINDEX Increases.

Note. Standard errors are reported in parentheses.

Significance at 10%; **Significance at 5%; ***Significance at 1%.

We also present the results of our quantile regression in terms of net effects, highlighting the impact of financial inclusion on trade liberalization, which in turn supports sustainable economic growth. Recent research supports the notion of net effects (Bunje et al., 2022b). On the one hand, the net effect on sustainable economic growth is produced by the interaction of variable trade liberalization and financial inclusion (LIBFINDEX) and the unconditional influence of trade liberalization. The net effects for the relationship between trade liberalization, financial inclusion, and sustainable economic growth are significant in all quantiles (25th–95th). The mean financial inclusion value is 0.152, as reported in Table 2. From Table 7, the net effect of trade liberalization on sustainable economic growth in the 25th quantile is ([4.873 × 0.152] + 2.358) = 3.099. We follow a similar process to calculate the net effects for the remaining quantiles in the relationship between trade liberalization, financial inclusion, and sustainable economic growth. The favorable net effects of trade liberalization and financial inclusion on sustainable economic growth provide proof of the synergistic benefits. The positive synergies are compatible with our theoretical and empirical justifications due to their double-positive impact on boosting sustainable economic growth. We can explain this by citing the following reasons: (1) the positive impact of trade liberalization in Table 7; and (2) the positive effects of trade liberalization and financial inclusion interacting. Therefore, it is reasonable to conclude that there is an empirically valid relationship between trade liberalization and financial inclusion. Trade liberalization benefits from financial inclusion, and their interaction improves sustainable economic growth.

Granger Causality Test

It is broadly acknowledged in academic literature that a correlation between two variables does not inherently imply a causal link (Bunje et al., 2022b). In order to examine whether or not an increase trade liberalization and financial inclusion would cause sustainable economic growth to increase, we employed the Dumitrescu–Hurlin (2012) panel causality approach to perform to task. Table 8 shows the outcome from Dumitrescu–Hurlin panel causality approach. The results indicate that any policy aimed at trade liberalization will influence sustainable economic growth in Sub-Saharan African economies. The findings also verify that there is a two-way causal relationship between financial inclusion and sustainable economic growth. These results imply that trade liberalization and financial inclusion have predictive power of sustainable economic growth in SSA economies.

Dumitrescu and Hurlin Causality Test Results.

Significance at 10%; ***Significance at 1%.

Conclusion and Policy Implications

Scholars in development and trade economics have extensively discussed the impacts of trade liberalization on sustainable economic growth as the impacts of financial inclusion (Bunje et al., 2022a; Egyir et al., 2020; Hussain et al., 2024). However, the combined role of trade liberalization and financial inclusion and their interconnected impact on sustainable trade have been ignored, particularly in the context of SSA countries. Hence, this study examines the role of trade liberalization and financial inclusion and their interaction and impact on sustainable economic growth using quantile regression (QR) model, Driscoll-Kraay fixed effect-OLS approach and the second-stage instrumental variable (2SIV-DPD) model. The study makes use of a panel dataset that spans 22 years, from 2000 to 2021, and includes 48 sub-Saharan African nations. We employed the panel quantile regression approach to conduct our baseline estimations. The results show that trade liberalization has a positive impact on sustainable economic growth in Sub-Saharan Africa. Moreover, the results also suggest financial inclusion enhance sustainable economic growth in Sub-Saharan Africa. In addition, the results suggest that financial inclusion complements trade liberalization to promote sustainable economic growth in Sub-Saharan Africa. We further discovered that trade liberalization and financial inclusion have a bidirectional causal relationship with sustainable economic growth. Our study uncovers a significant novelty in that the marginal effects on sustainable economic growth increase when trade liberalization interacts with financial inclusion in the SSA countries. On top of that, our study adds to the body of research on sustainable development by figuring out the exact level of financial inclusion that can change how trade liberalization affects the achievement of sustainable economic growth in SSA countries. Regarding the other explanatory variables, we find that physical capital (CAP) and financial development (FD) decrease sustainable economic growth, while human capital development (HCAP), foreign direct investment (FDI), and government expenditure promote sustainable economic growth in the SSA region.

In terms of policy implications, the finding indicates that an increase in trade liberalization among African countries positively impacts the sustainable growth of the region. Therefore, given the influence of trade liberalization on sustainable growth, it is advisable for nations in Africa to shift toward trade integration activities, such as promoting of the implementation of the African continental free trade area (AfCFTA) agreement which seeks to liberalize trade in the continent. Moreover, financial inclusion exhibits positive and significant effects on sustainable economic growth in Africa. In line with this finding, it is recommended that policymakers in Africa should focus on policies that promote financial inclusion. This can be achieved by investing in digital infrastructure and mobile banking adoption by expanding network coverage, reducing transaction costs, and promoting interoperability between financial service providers.

This study proposes that future research should prioritize the examination of other developing regions, specifically the developing Asian economies and Caribbean economies. This study is conducted using a sample of 48 economies in Sub-Saharan Africa (SSA), thus its findings are applicable solely to countries within the SSA region. In order to derive policy implications that are applicable to developing economies, future research endeavors could consider incorporating expanded data sets from other developing regions. This would enable a comprehensive examination of the significance of trade liberalization and financial inclusion, particularly within the framework of fostering sustainable economic growth.

Footnotes

Acknowledgements

We would like to acknowledge and give our warmest thanks to Mr. Wang Wei who has been a great help and support. His guidance and advice carried us through all the stages of writing of this article. We would also like to thank Simon Abedin for his brilliant comments and suggestions.

Ethical Approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting this study's findings are available from the corresponding author upon request.