Abstract

Innovation activities are an essential factor to maintain enterprises’ growth. This study takes Taiwan stock market listed companies as the research object and explores the relationship between the corporation’s innovation activities and the chairman and CEO as an inventor. Furthermore, we use panel regression analysis to obtain robust results. Under such a trend of information circulation, innovation plays an important role in various emerging trends advocated in Taiwan in recent years. Therefore, this paper attempts to conduct an in-depth study on it. This paper verifies the important role of CEO duality in corporate innovation, which means that the corporation’s R&D expenditure can be further evaluated by the president and CEO. It is found that the chairman who is an inventor and CEO can reduce the corporation’s R&D expenses but can increase the number of patents of the company, which shows that the chairman and CEO who is an inventor has better R&D efficiency, but this phenomenon only exists in the electronics industry. Therefore, future research is suggested to examine real cases from different innovation activities, and although some case studies may be confusing, cross-cultural real research should also be encouraged in future work.

Introduction

Innovation activities are an important factor for corporations to maintain their competitive advantages. Based on the principle of self-interest (Jensen & Meckling, 1976), the CEO of a corporation tends to reduce the incentive to invest in innovative activities after weighing the risks and returns brought about by innovative activities. On the other hand, CEOs may prefer more innovations because they can earn more profits if the innovative activities are successful. Thus, the relationship between innovation and tenure-based corporate CEOs appears to be ambiguous. In order to obtain the ability of economic globalization and product standardization, the unique innovative content occupying a leading position in the market is a crucial means for corporations, especially high-tech corporations to maintain their leading position (Im & Workman, 2004). Naqshbandi and Jasimuddin (2022) conduct a cross-sectional sample of 530 firms in France, Malaysia, and the UAE, collecting data, which collected from middle and top managers in different industries. The empirical results support a link between managerial linkages and absorptive capacity that may lead to the successful operation of innovation. An IPO provides the first full disclosure of a “listed company” and requires the corporation to combine its governance with innovation. When the CEO is the same person as the board’s chairman with investors, it’s called CEO duality. Almost half of the S&P 500 corporations have dual CEOs (Spencer, 2019). Putting the above together, exploring how the chairman-CEO influences the company’s R&D innovation during the IPO is helpful. This paper takes Taiwan “listed company” as the research object to examine the relationship between CEO duality and corporate innovation. The contributions of this paper are as follows:

First of all, the survival and development ability of an IPO corporation may depend on the tenure and education level of the CEO. IPO corporations are usually emerging and high-growth industries, and they also seek high-tech products and services with future development and innovation. CEOs who are also inventors may be more suitable for a high-tech IPO corporation with shorter technology and product life cycle. If they stay at the forefront of innovation, they can compete more effectively in industries with unclear development. An IPO is a critical stage in the life cycle of a corporation, a major milestone in the journey from start-up to “listed company.” This process is considered to be a period of high uncertainty (Certo et al., 2001). Ritter (2003) finds that IPO corporations typically provide strong initial returns, but about 30% of them fail or are acquired within 5 years of offering. Thus, in preparation for an IPO, corporations are thoroughly investigated by investment bankers and institutional investors, and every level of the corporation is scrutinized. Therefore, Wilbon (2002) points out that the technology experience of IPO corporation executives is positively related to post-IPO survivability. Bayar and Chemmanur (2012) find that industry and corporation characteristics largely explain the choice between IPOs and acquisitions. However, Spiegel and Tookes (2008) show that “listed company” force IPO corporations to disclose private information about their competitiveness to competitors, thereby engaging in practices that may harm corporate investment (Asker et al., 2015) or innovative behavior (Bernstein, 2015) IPO, thereby reducing excess profitability or productivity post-IPO.

Second, corporate innovation is the key to maintaining a competitive advantage in performance (Cho & Pucik, 2005; Rubera & Kirca, 2012). M. T. Lee and Suh (2022) advocate a procedural and comprehensive approach to modeling the causality relationship between ESG behavior and financial performance variables; and propose ways to analyze models that ESG behavior can reveal about financial performance. Li et al. (2022) use the panel data of 1,307 corporations listed on the Shenzhen and Shanghai stock exchanges from 2006 to 2016 to explore the relationship between the acquisition market and corporate innovation. The research results show that the acquisition market has a positive and significant impact on corporate innovation through the compensation incentives of new managers. Lev (2001) points out that R&D is a high-risk, non-tradable property for corporations, which is difficult to evaluate by the market. Therefore, R&D is an investment activity that corporations attach great importance to. Zhou and Sadeghi (2019) believe that the level of R&D expenditure is a reliable indicator of corporate innovation activities and a measure of corporate innovation capabilities. The number of patent applications filed by a corporation is a useful measure of the value of innovation (Aghion et al., 2013; Hall et al., 2005). Investors believe that the main driver of growth for patented corporations is innovation (Lev, 2001). Using survey data from 212 Chinese firms, Guo et al. (2022) conceptualize a new concept of generative capability, a unique ability of corporations to organize experiential learning activities to enable rapid iterative computational innovation. The empirical results show that the structure and standard validity of generative capabilities are positively correlated with corporate innovation performance. Measures of corporate innovation include R&D spending and patents. R&D costs are the innovation input of corporations, and patents are the output of innovation (Griliches, 1990). Therefore, this study uses the R&D ratio and the number of patents to represent the innovation capability of the corporation.

Third, research on entrepreneurial identity is increasingly accepted by scholars (Wagenschwanz, 2021), especially as a basis for studying differences in entrepreneurial behavior (Gruber & MacMillan, 2017). Since the founder is the first person to establish a new corporation and various important affairs, it is necessary to have the ability to have all professional knowledge and skills without analyzing the founder’s personal entrepreneurial choice. In the past, personal characteristics such as seniority, education, and financial status could be used to play a key role in the decision to become an entrepreneur (Evans & Jovanovic, 1989; Holtz-Eakin et al., 1994). The personal characteristics of CEOs are closely related to innovation activities. Zacharias et al. (2015) show that a CEO’s upbringing and life environment (educational background and work experience) influences a corporation’s attitude toward innovation. Barker and Mueller (2002) point out that CEOs with business or MBA degrees tend to be conservative and risk-averse in business style, and CEO education is positively correlated with innovation acceptance. R&D spending is relatively higher for CEOs with marketing, engineering, or R&D experience. Using age as a proxy for measuring risk aversion bias. Older adults have a harder time accepting new ideas and learning new technologies, so age is positively associated with risk aversion (Bantel & Jackson, 1989; Barker & Mueller, 2002; Joos et al., 2003).

Fourth, CEO tenure is an important factor in a corporation’s R&D policy. Barker and Mueller (2002) and Lundstrum (2002) show that when longer-tenured CEOs retire, they tend to have personal preferences, shift to conservative strategies, and invest less in R&D innovation. Naveen (2006) finds that CEO tenure is negatively correlated with R&D expenditure. Therefore, this paper is expected to provide clearer results after controlling for confounding factors.

The reasons obtained from the Taiwan stock market are as follows. First, the OECD has advocated for knowledge-based economic development since 1996 and has actively advocated for the importance of innovative investments and services. Under such a trend of information circulation, artificial intelligence (AI), which is very popular recently, must also be a topic of government attention and investment. Taiwan’s industrial exports and investments are highly concentrated in the manufacturing industry, and the information electronics industry is the main source of economic growth. In contrast, traditional industries are facing globalization and economic instability. Second, Taiwan’s economy is known as a small manufacturing entrepreneur (SME)-dominated structure (T. R. Lee & Jioe, 2017), accounting for 98% of the total number of entrepreneurs and employing 71% of the national labor force (Chen et al., 2021). Taiwan’s manufacturing industry has the characteristics of an industrial cluster and is considered a business ecosystem. Small start-ups often form a network of hub-satellite systems where hub factories and partner factories are clustered together (Chen et al., 2021), and they are key suppliers to larger companies, responsible for most of the innovation and productivity in the corporate world (Wu & Wang Chiu, 2016). Therefore, the Taiwan data can clearly explain the duality and innovativeness of CEOs.

The challenge for Taiwan will be how to transform from hardware to a knowledge and information center in Asia and the world. The entrepreneurs are good at controlling costs, continuously improving efficiency and technology, and producing faster, thinner, and more functional products in Taiwan. The new competitive landscape requires a high degree of innovation. Therefore, it is worth exploring how CEO duality affects innovation. The empirical results show that corporate duality is positively correlated with the degree of corporate innovation. Corporation duality is negatively correlated with R&D expenditure.

The rest of this paper is organized as follows. Section 2 discusses the literature review, while Section 3 introduces variable measures and data sources. Section 4 for empirical results. Finally, Section 5 gives conclusions and a final discussion.

Literature Review

When the CEO and the inventor’s chairman of the board are the same person, it is called CEO duality. Almost half of the S&P 500 corporations have dual CEO roles (Spencer, 2019). The CEO has influence over the board of directors, top management, and the corporation’s internal organization. Mak and Roush (2000) find that after the corporation’s IPO, corporations with dual CEOs have better growth opportunities. In corporations with dual CEOs, the board’s decision-making process can reduce conflicts with managers’ decision-making (Amzaleg et al., 2014; Howton et al., 2001). Christensen (2013) points out that inventors are proficient in a particular technology, but an inventor who is also a CEO may not be capable of running a corporation. Corporations with an inventor as CEO are associated with a large number of registered patents, higher cited patents and innovation efficiency. They are more likely to spark disruptive innovations, a performance that makes them more inclined to produce patents that are not only important but have demonstrable economic value. Consequently, corporations led by inventors and CEOs also tend to release more new products, suggesting that patents filed during their tenure can also transform into more successful products. Therefore, assume the following:

Hypothesis 1: The corporation duality is related to corporation innovation.

What are the factors influencing the CEO’s commitment to innovation activities? First, corporation innovation investments are unique but unpredictable (Holmstrom, 1989). Second, senior managers prefer a quiet life (Bertrand & Mullainathan, 2003), and corporations use different mechanisms to force them to innovate. Third, managers do not like the risk of layoffs brought about by innovation (Holmstrom, 1989), therefore, managers prefer real investment. This increases the risk of managers being fired if innovation activities fail due to external factors, such as the COVID-19 epidemic. Fourth, the innovation process takes a long time, therefore, innovation activities may not be completed by the end of the CEO’s tenure (Dechow & Sloan, 1991; Gibbons & Murphy, 1992). For example, Cho and Pucik (2005) and Rubera and Kirca (2012) point out that corporations can maintain or improve their competitive advantage and performance through innovative activities. Lev (2001) points out that R&D has high risks and is not easily evaluated by the market. Zhou and Sadeghi (2019) elaborate on the impact of patents on the level of R&D spending, which is an indicator of a corporation’s innovation capability. Hall et al. (2005) and Aghion et al. (2013) point out that the number of patent applications can be used as an indicator to measure the value of innovation. If the CEO himself is not a member of the board of directors, he is susceptible to the influence of moral hazard appetite and prefers capital expenditures, because if the innovation project has substantial performance development, he may receive a good promotion channel due to the improvement of the corporation’s performance. However, if the CEO is also on the board, he may have multiple considerations when considering capital expenditure, so he may be skeptical about capital expenditure. Based on the above literature, this study fully explores the innovative activities of the chairman of the board and the CEO on the corporation’s patents. The following assumptions are as follows:

Hypothesis 2: Corporation duality is related to corporation R&D spending.

Variable Measures and Data Sources

Variable Measures

The corporation’s innovative activity in this paper is measured by the corporation’s R&D expenditure and the number of patents, respectively. The definitions of relevant variables in this paper are as follows:

Data Sources

The data used in this article are mainly from the IPO database of “listed company” on the Taiwan Stock Exchange. “TEJ Corporation” module in Taiwan Economic Journal Database (TEJ) and the “Directors, Supervisors and Managers’ Learning Experience” module in TEJ. In addition, corporations in the financial industry (which have different financial reporting standards than other industries) are also excluded from this paper. After the above selection criteria, the number of sample companies in this paper is 269, including the observation of 255 IPO companies in 23 industries in 1995. 1 The board year and manager year are available from the post-IPO sample corporations, the average tenure of the board chairman and CEO is 4 years, the longest has 14 years of experience, and the shortest has a maximum of 1 year of experience. The number of corporations in the electronics industry and non-electronics industry is 1,304 and 691 respectively, but the sample size of education level and the electronics industry is missing 22 corporations, and the remaining sample is 1,282 corporations.

Empirical Results

Descriptive Statistics

This paper divides these corporations into the electronics industry and the non-electronics industry, as shown in Table 1. During the study period of this paper, there is no significant difference in R&D expenditure between the electronics and non-electronics industries, but the number of patents in the electronics industry is significantly higher than in the non-electronics industries. The non-electronics corporations significantly outperform electronics corporations in terms of chairman of the board and CEO. There is a CEO binary in the non-electronics sector at the time of the corporation IPO, and it is significantly higher than in the electronics sector. The results support the view that in non-electronics industries (in the past, most started as family businesses), the chairman and CEO want to fully demonstrate board resolutions. In addition, the number of CEO changes in the electronics industry is also higher than that in the non-electronics industry, which shows that in the case of separation of management rights and ownership, it is the senior executives who are really responsible for the corporation’s operating performance. The education level and qualifications of CEOs in the electronics industry are also significantly higher than those in the non-electronics industries. The operating performance of corporations in the electronics industry is significantly lower than that of corporations in the non-electronics industry.

Descriptive Statistics of Variables in Total Industry.

, **, and * are at the 1%, 5%, and 10% significance levels, respectively.

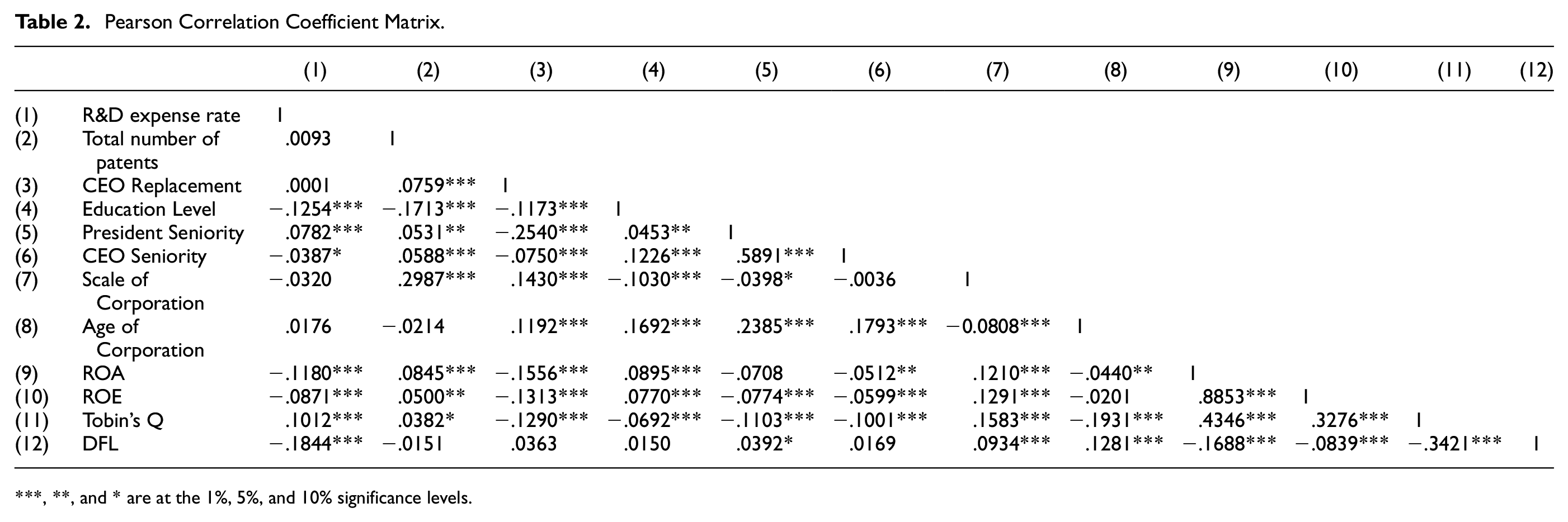

Correlation Analysis

Table 2 is Pearson’s correlation coefficient matrix analysis. The results show that there is no significant relationship between the R&D expenditure ratio and the number of patents, as discussed in the previous section, which further suggests that both can fully represent innovation variables. The number of CEO turnover is positively correlated with corporate innovation, while education level is negatively correlated with corporate innovation activities. Studies have shown that the more educated a CEO is, the lower his preference for innovative activities and the lower his risk of being fired. Corporate R&D expenditure is negatively correlated with corporate performance, such as ROA and ROE. But it’s positively correlated with the market value of the corporation, like Tobin Q. The higher the debt ratio, the lower the corporation’s research and development expenses, but the higher the number of patents. All values in the Pearson correlation analysis were less than.3. These results could reduce the possibility of multicollinearity problems in the latter regression analysis.

Pearson Correlation Coefficient Matrix.

, **, and * are at the 1%, 5%, and 10% significance levels.

The Panel Regression Analysis

This paper explores the relationship between CEO duality and corporate innovation activities. In this paper, the dependent variable (Y) is the innovation variable, while the independent variable (X) is as described above (see Table 3). The equation is as follows:

Definitions of Variables.

Tobin’s Q has become an increasingly popular measure for investors and academics to evaluate whether ESG conduct impacts a firm’s market value to be under or over its assets’ replacement cost (Gillan et al., 2021).

After considering the cluster standard error, the empirical model combines the industry effect and the annual effect through annual and industry corrections to reduce the inaccuracy of the estimated value (see Table 4). The chairman of the board and the CEO are inventors and are positively correlated with the total number of patent filings, suggesting that the inventiveness of inventors helps us to increase the corporation’s patent acquisition rate. Combining the R&D expenditure and the number of patents, the chairman of the board and the CEO are an inventor and will increase the corporation’s R&D efficiency. Hypothesis 1, the corporation duality is positively correlated with corporation innovation, is supported. Furthermore, corporation R&D expenditure is negatively correlated with the chairman of the board and the CEO as an inventor. The R&D expenditure of corporations whose chairman and CEO are inventors are lower than those of corporations whose chairman and CEO are not inventors. Therefore, Hypothesis 2 is supported. In addition, the chairman of the board and CEO are positively related to the corporation’s R&D expenditure, but negatively related to the corporation’s patent number. It is pointed out that the effectiveness of the chairman and CEO in R&D is unclear and that there may be an agency problem. The results were unchanged after including other control variables. The education level of CEOs is negatively correlated with corporate innovation activities, indicating that CEOs with higher education levels have lower preferences for innovation activities.

CEO Duality and Corporation Innovation.

, **, and * are significant levels of 1%, 5%, and 10%, respectively; standard errors are in brackets; both industrial effects and annual effects exist and are also considered in this analysis.

The empirical results of our study are consistent with Islam and Zein (2020). CEOs with inventor status can more effectively evaluate and execute investment projects that are conducive to innovation, have higher innovation efficiency, can stimulate innovation performance, and are more inclined to produce patents. There is a consensus that “doing” innovation by a corporation led by an inventor CEO brings unique innovative capabilities to the business. This study further considers whether the innovation activities of corporations are related to the industrial effect. The empirical results are shown in Table 5. The results are roughly the same as the previous conclusions. Therefore, this paper can briefly explain that industry effects do not affect the results between CEO duality and innovation.

Sub-sample Analysis: Electronic Versus Non-Electronic Industries.

, **, and * are significant levels of 1%, 5%, and 10% in the table; standard errors are in brackets; both industrial effects and annual effects exist.

Conclusion

This study considers whether inventors’ roles as board chairmen and CEOs affect corporations’ ability to innovate. The empirical results show that CEO duality plays an important role in innovation activities. The research shows that whether CEO duality has inventor characteristics is an important factor affecting corporate innovation activities. CEO duality is negatively correlated with R&D expenditure.

This study can bring some management implications. How to improve Taiwan’s traditional industries will be a difficult problem for the sustainable development of industries. The five innovative industries of Asia’s Silicon Valley, smart machinery, green energy technology, biotechnology and healthcare, and defense industry are at the heart of driving the growth of Taiwan’s next-generation industries. On this basis, combined with the development needs of traditional industries, carry out effective technological upgrading and transformation of innovative industries.

The limitation of this paper is the definition of innovation variables, so future research is recommended to examine real cases of innovative activities from start to finish, although such case studies can be very scary and difficult to obtain. Next, follow-up researchers can be encouraged to do transnational case studies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Data Availability Statement

The data are available from the authors upon request.