Abstract

Innovation is the first driving force leading economic development, and small and medium-sized enterprises have strategic significance in stimulating innovation activity and promoting economic growth. Few studies concentrating on small and medium-sized businesses examine the connection between executive incentive contracts and business innovation. Therefore, we use them as the research object in this study. We empirically analyze the relationship between executive incentive contracts and enterprise innovation using the research sample of small and medium-sized board-listed companies from 2009 to 2020, focusing on long-term equity and short-term pay incentives. The study also analyzes if the corporate environment will impact a specific motivational system. The results show that improving executive shareholding and pay level can significantly promote enterprise innovation. The areas with better business environments mean practical innovation. Otherwise, organizational equity and pay incentives positively affect innovation in non-state-owned enterprises. This effect might increase the business environment compared to state-owned enterprises. Meanwhile, information transparency is improved by equity incentives and pay incentives, and the implementation intensity of equity incentives reduces the degree of financialization. By demonstrating how CEO equity and pay incentives affect corporate innovation, this study adds to the body of literature in that field. It also offers empirical evidence to assist corporations in creating the most corporate equality and pay incentives. Future studies should continue examining the impact of non-material incentives on enterprise innovation and the relationship between equity and pay incentives.

Keywords

Introduction

On March 5th, 2022, the 13th National People’s Congress proposed “independent innovation to achieve self-reliance and self-improvement in science and technology” and “innovation drives development and makes enterprises the main body of scientific and technological innovation.” Innovation has become an essential driving force for a new round of rapid economic development. According to the global innovation index report by the World Intellectual Property Organization, China’s worldwide innovation index jumped from 25th to 16th from 2016 to 2020. A critical strategy for attaining national construction and development with the application of the innovation-oriented national policy is to encourage technological innovation of small and medium-sized firms with micro-innovation subjects (Zhu et al., 2020). Ye Dingda, the deputy director of the Small and Medium-sized Companies Bureau of the Ministry of Industry and Information Technology, highlighted that the Chinese government should prioritize small and medium-sized businesses’ innovation and entrepreneurship. China’s economic development can only be steady and comprehensive if a favorable external environment is created for transforming and upgrading small and medium-sized enterprises and if several steps are taken to assist these businesses in implementing innovation. The novel coronavirus epidemic in 2020 caused a systematic stagnation in the development of SMEs (Smallbone et al., 2022), so how to promote the innovative development of SMEs to enhance their ability to withstand risks in crises and gain competitive advantage? It is worth discussing.

In a market-oriented economy, the executives make the firm’s marketing strategy and undertake R&D risk. Their decisions play a critical role in improving the firm’s innovation ability. Without an effective incentive mechanism for innovation, the managers are unwilling to undertake innovative decision responsibility and related risks. This condition will undoubtedly affect the firm’s technology and innovation ability (Tsang et al., 2021). Therefore, the enterprise needs to construct an effective incentive mechanism. The managers can avoid adverse selection and moral hazard tendencies in this situation. The key to improving enterprises’ innovation level is focusing on R&D projects. The initial intent of short-term pay incentives and long-term equity incentives was to act as a suitable replacement for supervision tools, weaken management’s self-interested behavior, harm shareholders’ interests and corporate value, and coordinate the agency conflict between shareholders and executives (Jensen & Meckling, 1998). Once this objective was realized, the two development goals were coordinated and consistent, and attention was then turned to innovative development under the influence of these two factors.

High-risk, high-reward corporation innovation often depends on an excellent environment business system to positively interact with enterprises’ innovation input and output (Huo & Zhang, 2022). As a necessary form of the external environment, the business environment is not only essential to support the country in building soft economic power and promoting the development of a multi-level capital market but also affects the critical conditions for enterprises to maintain business vitality and improve comprehensive competitiveness (Yu & Liang, 2019). The business environment often contains market dynamics, legal environment, government efficiency, and international business environment. Therefore, the difficulty of innovation factor flow is affected by the level of marketization. Executive decision-making may also be constrained or facilitated by external conditions, which makes corporate innovation different due to the interaction between executive willingness and the external institutional environment. Many previous studies have reported the effect of executive incentives on enterprise innovation. However, few studies have analyzed the difference between pay and equity incentives for enterprise innovation in different business environments. So how does the difference in business environment affect the effect of incentive mechanisms on enterprise innovation? This question needs to be solved.

Most previous studies related to equity incentives focus on high-tech or large enterprises. However, China’s small and medium-sized enterprises still need to be analyzed. SMEs contribute more than 50% of China’s tax revenue, more than 60% of GDP, more than 70% of technological innovation, more than 80% of urban employment, and more than 90% of the number of enterprises (Zhu et al., 2020). It is an essential carrier for implementing mass entrepreneurship and innovation. It has strategic significance in stimulating innovation vitality, improving economic activity, ensuring the integrity of the production system, and stabilizing employment. Therefore, this paper takes small and medium-sized enterprises as the research object. The research conclusion can contribute to implementing executive incentives contracts and the steady development of small and medium-sized enterprises. Secondly, in the research on the relationship between executive incentives and enterprise innovation, few scholars consider the impact of the external economic environment. This paper incorporates the business environments into the research framework. It explores the regulatory effect of the external macro-environment on the relationship between long-term and short-term executive incentives and enterprise innovation.

The results are beneficial for providing suggestions for the firm to improve innovation. Otherwise, What is the function channel of equity incentive affecting enterprise innovation? What are the constraints? There are few references in the existing literature. This paper considers the intermediary role of information transparency and enterprise financialization. This result helps to thoroughly outline the action mechanism of executive long-term and short-term incentives for enterprise innovation activities. Meanwhile, this article promotes the incentive mechanism for the governance of business, technology, and management, which provides empirical support for uncovering the mystery of enterprise innovation. It offers theoretical and practical guidance on formulating executive incentives and enterprise financialization-related policies.

Literature Review and Research Hypothesis

Executive Incentives and Enterprise Innovation

China is in the critical stage of economic transformation and upgrading, and the importance of implementing the policy of “mass entrepreneurship and innovation” is becoming increasingly prominent. Enterprise innovation is affected by many external factors, including the other firms’ decisions in the industry (Peng et al., 2020), fair market governance (Genin et al., 2021), and environment policy (Fried, 2018), as well as internal objective factors such as independent innovation funds and technical equipment (Mc Namara et al., 2017). Additionally, the innovation relates to the company’s managers (including board members and senior managers), senior managers’ social relationships (B. Li, 2016), stability (Zhang et al., 2018), doctoral education background in the management layer (Z. He & Hirshleifer, 2022), gender heterogeneity, psychological security factors (Griffin et al., 2021), and crossover effect (Han, 2022). These factors play positive roles in a firm’s R&D level and innovation ability.

Therefore, as a critical part of internal corporate governance, managerial incentives on managers’ risk appetite and enterprise R&D investment should not be underestimated. The traditional principal-agent theory points out that separating management rights and ownership puts enterprise managers and shareholders in different interest-oriented areas. Based on the various business concepts of both parties, managers will have a certain degree of short-sighted behavior to maximize their income. In the process of innovation, it is likely to improve power prestige and obtain personal payment through short-term investment and underestimate the potential value of strategic investment projects (Tsang et al., 2021). At the same time, if the enterprise fails in research and development, managers may face a crisis of professional stability, such as demotion without pay or loss of industry reputation. Therefore, in the face of investment projects that are not easy to evaluate, based on the motivation of risk aversion, the exclusion of innovation will hinder the continuous development of innovation activities with long-term benefits. Alleviating the agency conflict of managers includes spiritual incentives such as reputation and promotion, but also needs to pay attention to equity Material incentives such as welfare (Liu et al., 2022).

Since 2006, China’s listed companies have implemented an equity incentive system similar to the West. According to a previous study, the widespread use of equity incentive plans can enable businesses to avoid inherent annual salaries, reduce agency costs (Burns et al., 2015), and diversify investments to lower enterprise risk (Brisley et al., 2021). In particular, in the market for fierce talent, the grant period also plays a significant advantage in luring and keeping employees, assessing the managerial skills of employees, and so on (Jochem et al., 2018; Lennox et al., 2020). The practical implementation of equity incentives in developed countries makes Chinese scholars explore the implementation effect of equity incentives from multiple perspectives. The study concluded that the M&A activities of enterprises (Pan & Shen, 2021), operating leverage decisions (Wang et al., 2021), and financial performance evaluation (G. Z. Li et al., 2020) are all affected by the equity incentive mechanism. Based on short-term incentives, scholars have also concluded that compensation incentives are of great significance to optimizing the strategic choice of enterprises, resource allocation (X. N. Yin et al., 2021), and improving production performance (Banerjee & Homroy, 2018). The strong sensitivity of compensation performance of senior management teams can inhibit the conditions required for earnings manipulation and enhance the quality of earnings (Kim et al., 2022). These results show that executives can make business decisions affecting the company’s future development strategy. Therefore, the enterprise cannot ignore the role of innovation activities from executives.

With the development of the corporate governance system and the promotion of innovation theory, academia began to study the relationship between equity incentives and enterprise innovation from multiple aspects and perspectives. Under the “optimal contract theory hypothesis,” equity incentives can form implicit constraints on enterprise executives, reducing their opportunistic behavior and short-sighted tendency in innovation activities under the effect of interest convergence (Shue & Townsend, 2017). Meanwhile, the equity incentive plans can affect the managers’ salaries by fluctuating the company’s stock price. The executives can obtain the additional residual income from the enterprise’s technological innovation investment. It can reduce the contradiction of information asymmetry and incentive disharmony to a certain extent. In this condition, the executives are more willing to improve their support for R&D (Liu et al., 2022). When the equity incentives reach a particular proportion, managers’ tolerance for failure and substantial improvement in systemic risk-bearing capacity (Armstrong et al., 2022; Tian & Meng, 2018). They tend to be a competitive and sustainable strategic orientation in decision-making, avoiding the psychology of abandoning innovation due to unwillingness to bear the consequences of risk. Previous scholars, including Flammer and Bansal (2017), Nguyen (2018), and D. Du et al. (2022), also concluded that appropriate equity incentives could inhibit the tendency of executives to seek quick success and instant benefit. These results are more likely to increase strategies such as long-term investment innovation and stakeholder relations and improve the innovation conversion rate. Therefore, implementing equity incentives can enable the management to enhance the technological innovation ability of enterprises for long-term development.

Bebchuk et al. (2002) put forward the “management power theory” based on the “optimal contract theory.” The theory believes that the management will use its power to control the nomination of the board of directors and participate in the compensation committee to damage the board of directors’ independence. It can gain a favorable position in the compensation negotiation, which leads to equity incentives becoming a rent-seeking tool rather than a tool to solve the agency problem (Nienhaus, 2022). When the management shareholding is too high, they can and are motivated to control performance indicators to meet the exercise conditions. Additionally, they can use the power to make more risk-averse decisions in seeking benefits and cover up accounting information disclosure (Wruck & Wu, 2021). It can result in non-systematic risks and reduce the enterprise’s innovation performance (Biggerstaff et al., 2019; Huang & You, 2020). Moreover, some researchers have found a nonlinear relationship between equity incentives and enterprise innovation. That is, the “convergence of interests effect” and “entrenchment effect” exist at the same time (N. Xu et al., 2019). Biggerstaff et al. (2019), C. S. Xu et al. (2018), and other studies concluded that equity incentives are unrelated to enterprise innovation. All these results indicate that the executive shareholding implemented by China’s listed companies is still an institutional welfare arrangement.

Compared with equity incentives linked to the long-term performance of enterprises, salary incentives belong to the category of short-term incentive mechanisms. The enterprises’ internal salary incentive contract establishes the executives’ salary level based on corporate performance to guide the executives’ incentive effect and risk orientation (M. Q. Yin et al., 2018). When innovating to give senior management teams higher monetary compensation, it can provide them with institutional guarantees to meet short-term economic demands. An incentive mechanism tolerating early failures and rewarding long-term success can attract and retain optimistic and entrepreneurial executives (Xiao & Wang, 2022). Senior executives will take the initiative to develop many plans to implement the business’ technological innovation strategy, such as utilizing external resources, actively seeking research and development partners with cooperative intentions, and so on. Based on pursuing performance goals and image engineering while ensuring they are in a favorable negotiating position in subsequent contracts (Ma & Lu, 2019). Therefore, the enterprise has the resources and capabilities for long-term development to create wealth for its owners. Further, it confirms that the reduction of executive monetary compensation may cause adverse effects, contrary to the original intention of advocating stimulating the long-term development potential of enterprises at this stage (Cai et al., 2021; Y. Li & Wang, 2022). Guay et al. (2019) also concluded that the bonus plan, as an appropriate incentive contract arrangement, can effectively alleviate the management’s use of earnings management to infringe on shareholders’ rights and interests. Restoring supervision can promote the coordination of the entire senior management team. The tenure of senior executives is phased and fluid. Under the premise of salary incentives, the short-term performance of enterprises is a necessary guarantee to determine the income function of management (Xie, 2018). As a rational economic man, the administration will first weigh personal benefits in pursuing short-term benefits such as wages, bonuses, and help and maintain a vigilant and conservative attitude towards innovative projects with high risks and strong positive externalities (Y. Li & Wang, 2022). The asymmetry between benefits and costs makes executives occupy additional allowances from innovative resources for personal consumption while reducing R&D investment expenditures. Ensuring there is enough time and energy to improve the short-term operating efficiency of the enterprise and reduce the degree of effort in R&D projects, resulting in the loss of R&D efficiency and damage to corporate value (Liang et al., 2015).

Through the above analysis, we can find that the impact of the implementation of an internal incentive mechanism on enterprise innovation is a problem with research tension, which has both a positive driving effect and a negative inhibiting effect. Do the incentive characteristics of small and medium-sized enterprises have unique laws? Compared with large-scale enterprises, China’s small and medium-sized enterprises are more difficult to obtain capital, human resources, and technology accumulation. So it is challenging to construct their unique competitiveness (Cathcart et al., 2020). When the resources are relatively scarce, the managers prefer to improve resource utilization by implementing enterprise management mechanisms to realize the close combination of knowledge, technology, and capital and obtain innovation ability and competitive advantage (Kadłubek et al., 2022). Equity and pay incentives are essential strategies to solve this problem (Jochem et al., 2018).

Small and medium-sized enterprises have a fast growth rate and high demand for innovation. Their innovation value management needs a keen scientific decision-making ability, strong cohesion, continuous human resources, and capital investment. First, equity incentives can tolerate short-term innovation failure and match the longer R&D cycle. It gives the motivation a generous reward after exercising the right, attracting and retaining employees who are more willing to accept the risky work of innovation, and maximizing the value of human capital. The other innovative performance carried by the compensation incentive is also conducive to stimulating the enthusiasm and creativity of senior executives. The interest binding enhances their sense of identity with the enterprise so that they can share their interests and risks and create more excellent value by staying in the enterprise (Jochem et al., 2018). Secondly, under the background of “sparing loans” from banks to SMEs, it is difficult for SMEs to obtain monopoly resources. Equity and compensation incentives can transmit information such as improvement of corporate governance and project excellence, making investors and banks more willing to provide funds to alleviate the financing constraints. When small and medium-sized enterprises have innovation resources, executives will focus on long-term value investment under the incentive of huge returns. To seek more remarkable profit and development space, make full use of innovation resources and policy advantages to gain income, and promote the improvement of enterprises’ independent innovation ability (Mc Namara et al., 2017).

According to the internal factor growth theory, the motivation and behavior of executives are essential factors for the growth of SMEs. Executives of small and medium-sized businesses are concerned about occupational defense due to the inevitable necessity of creating a competitive advantage through technological innovation. In order to maintain their market reputation and career planning, they are more willing to innovate. They will continue to follow up on cutting-edge technologies to seek new development goals and profit points and improve market recognition (Hsu et al., 2023). Equity incentives can compensate for the defects in the internal governance structure of the company’s small and medium-sized enterprises. Still, its long-term characteristics can also make the salary income of the management level linked to the innovation performance of the enterprise. With the increase of senior executives’ equity shares, its tendency to deviate from maximizing shareholders’ interests will be reduced accordingly. In order to maintain and improve the performance to meet the “exercise conditions,” the management level may pay attention to the quality of enterprise development and promote the implementation of innovation projects. It can actively realize the transformation of innovation achievements. The inherent short-term characteristics of compensation incentives guarantee the primary income of executives of small and medium-sized enterprises in the event of innovation failure. They can eliminate executives’ worries to a certain extent. The timely “innovation compensation effect” allows the management to invest more energy and time to continue to pay attention to new technologies and knowledge and view the future of the enterprise from a holistic perspective (Jochem et al., 2018).

The study indicates that team incentives may also produce the “free riding” phenomenon. The expansion of large-scale enterprises increases the organizational inertia of enterprises. The rapid increase of transaction costs within enterprises and the excessive attention to existing market interests may lead to rigidity in innovation decision-making, management, and other aspects. It becomes more prominent when granting equity and compensation on a large scale, weakening the incentive effect. However, small-scale enterprises have a stronger incentive to supervise each other, and pay incentives are better (Cao et al., 2022). Small and medium-sized enterprises have more robust organizational flexibility and a keen market sense. Under the influence of competitive pressure and crisis awareness, the high incentive level strengthens the supervision of shareholders, and other stakeholders on the management, further improve the construction of internal control, and reduces the damage of internal control defects to the enterprise value. The management subject to external attention and internal control may reduce self-interested activities and pursue R&D activities closely related to enterprise performance, thus improving SMEs’ flexibility and anti-risk ability. The effect of “joint supervision” is more potent than that of “free riding” (Nguyen, 2018).

Therefore, based on the context of listed companies of small and medium-sized enterprises, this paper puts forward hypotheses H1 and H2:

H1: There is a positive correlation between the long-term equity incentive of executives in small and medium-sized enterprises and innovation.

H2: There is a positive correlation between short-term compensation incentives for executives of small and medium-sized enterprises and innovation.

The Moderating Effect of the Business Environment on Incentive Contracts Affecting Corporate Innovation

According to the theory of resource dependence, the survival and development of organizations cannot be separated from the support of external resources, and only by connecting with them can they effectively obtain unique resources in the environment. The variability of economic policies, culture, and geographical location between regions makes the business environment significantly different (Zhou et al., 2020). As a measure of an external system, the business environment has become an essential condition that affects local, high-quality economic growth and collaborative innovation and development (de Bettignies et al., 2023). Areas with a perfect business environment create a good market opportunity, legal management, and economic environment. Secondly, according to the resource dependence theory, the business environment is vital in enterprise financing (Mc Namara et al., 2017). When the business environment is better, the economy will also be better. The fairness and trust between banks, other companies, and institutions that offer outside financing are all improved. Additionally, it provides more funding to help small and medium-sized businesses continue to thrive (Genin et al., 2021). If the business environment is incomplete, it will limit the integration and utilization of technological knowledge and the mobilization of additional resources by small and medium-sized enterprises. Due to the dual issues of lagging innovative technology and the impact of environmental uncertainty, businesses will cut their investment in R&D and lose the resource support for innovative projects, which is not conducive to companies engaging in worthwhile creative R&D activities (Yu & Liang, 2019).

Therefore, this paper puts forward hypothesis H3.

H3: With other conditions unchanged, a better business environment in the area, the more pronounced the role of executive incentives in promoting innovation investment.

Research Design

Sample Selection and Data Sources

The data of small and medium-sized board-listed companies from 2009 to 2020 are selected as the sample in this study. And then, the data are screened and processed below:

① The data of ST and financial enterprises in the statistical year are excluded.

② The missing data and outliers were eliminated, and 5483 sample observation data were obtained.

③ the continuous variables were winsorized with 1% and 99% quantiles. The data comes from CSMAR and Wind databases. The screening and matching are completed in Excel, and stata16.0 complements the statistical and regression analysis.

Variable Selection

Explained Variable

According to previous studies, the impact of senior executives on enterprise innovation is mainly realized through the innovation investment link. The R&D investment measures enterprise innovation more objectively and homogeneously. Therefore, this paper refers to the research of S. G. Li et al. (2022) and takes the intensity of R&D expenditure as the explained variable to explain the impact of senior executives’ equity incentive on enterprise innovation, which is recorded as R&D. Specifically, R&D expenditure indicators include relative indicators and absolute indicators. According to earlier research, a relative indicator is employed to indicate the intensity of R&D expenditure, or the percentage of R&D expenditure in total assets, to reduce the impact of firm size on R&D investment (Liu & Liu, 2022).

Explanatory Variable

The ownership structure is a relatively durable and objective measurement index that does not frequently change. Therefore, we refer to the research ideas of Flammer and Bansal (2017) and regard them as continuous variables. The equity incentive intensity is measured by the proportion of the number of management shares in the total number of shares, which is recorded as Percent; Executive compensation refers to the monetary or other economic remuneration that can be converted into money when the enterprise pays the service to the executive. Therefore, concerning the research of Zhang et al. (2018), the natural logarithm of the total compensation of all the executives is taken as the alternative explanatory variable of the compensation incentive, which is recorded as Lnsal.

Moderator Variable

Previous scholars used the urban competitiveness index to measure the business environment, which may lead to a single and imperfect measurement method (Zhou et al., 2020). The business environment is the sum of various settings throughout the enterprise life cycle, including government affairs, legal system, market, infrastructure, culture, and other domains. The marketization index can reflect the relationship between the government and the market, the development of product markets, and the development of intermediary market organizations. Based on the strength of the study findings and the improvement of environmental control, this work adopts the complete score of the annual marketization index of all Chinese provinces from Wang et al.’s (2021) report on the market-based index by regions in China. Given that the enterprise’s external business environment is pretty steady overall and this data is only current as of 2019, it is impossible to compare it to data from years before 2019 and after 2016. The index from 2017 to 2020 is equal to the index of 2009—the average of the index value-added of N years relative to the previous year’s index.

Control Variables

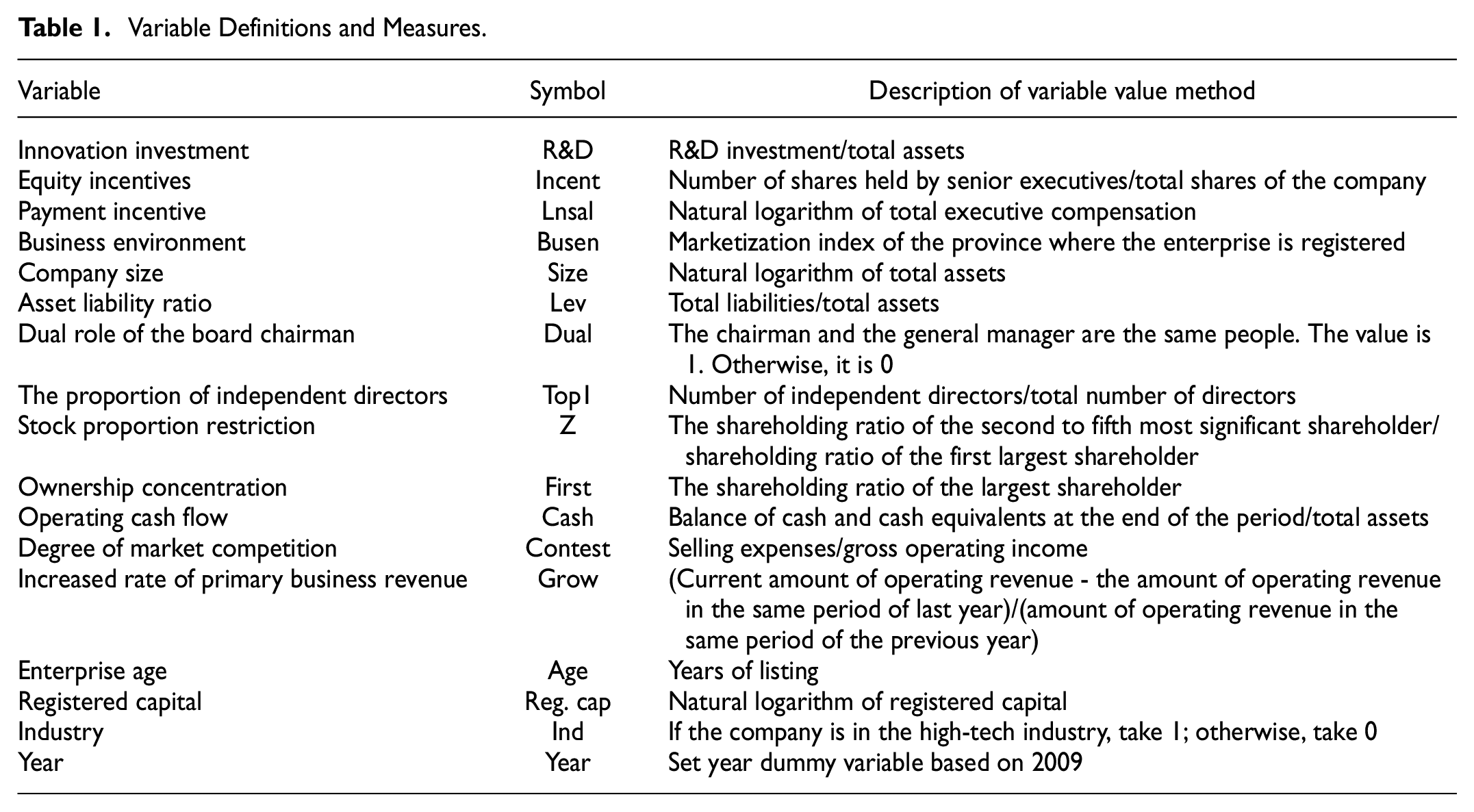

According to research by Balsmeier et al., the control variables chosen in this paper include enterprise scale (Size), asset-liability ratio (Lev), integration of two positions (Dual), the percentage of independent directors (Indept), equity balance (Z), equity concentration (Top1), cash flow (Cash), market competition (Contest), enterprise age (Age), registered capital (Reg_cap), and the growth rate of operations (Grow). Salary incentives, equity incentives, and enterprise innovation are each examined separately. And in the empirical analysis, this paper adds annual and industry dummy variables to control the fixed effect. See Table 1 for the specific definitions of the main variables:

Variable Definitions and Measures.

Model Setting

This research sets up models (1) and (2) to see if H1 and H2 are established to examine executive equity incentives’ effect on enterprise innovation:

Among them, R&D is enterprise innovation; Incent is a long-term equity incentive. Lnsal is a short-term compensation incentive. Busen is a business environment. Controls are the control variable, and ε is a random disturbance term. The robust standard error is used in empirical analysis to eliminate the influence of heteroscedasticity.

In order to test the regulatory impact of the business environment, this paper adds the cross-products of equity incentive and business environment (Percent × Busen) based on model (1) and the cross-product of salary incentive and business environment (Percent × Busen). Since the explanatory variable and the adjusting variable in this paper are continuous variables, using the cross-product of the explanatory variable and the adjusting variable can obtain more effective parameter estimates (2). That is, model (3) and model (4) to verify whether H3 is tenable:

Empirical Test and Result Analysis

Descriptive Statistics

Table 2 reports the results of descriptive statistics for the entire sample.

Descriptive Statistics of Variables.

Among the 5,483 observed values, we found that the average value of R&D is 0.023, the median value is 0.02, and the maximum value is 0.106. The influence of varied degrees of variables is evident in the significant differences in enterprise R&D spending. A limited number of small and medium-sized enterprises invest in innovation, and most of them are hesitant to do so. Therefore, the overall R&D expenditure activities still have a lot of room for improvement. Regarding equity incentives, if the minimum value is 0, some enterprises have not implemented equity incentives. The average value of equity incentive is 0.099, and the median value is 0.018. As can be seen, the shareholding intensity of various small and medium-sized firms varies significantly, there is a right deviation distribution in the degree of equity incentive, and the average shareholding ratio is not high. It suggests that the equity incentive system used by small and medium-sized enterprises in China is still in the exploratory stage.

Regarding short-term salary incentives, the average total salary of senior executives is about 14.85, but the maximum and minimum values differ significantly. It can be seen that there are apparent differences in the salary treatment given to senior managers by different small and medium-sized enterprises. In terms of the business environment, the average is 7.737, and the minimum and maximum are −0.230 and 10, respectively. It can be seen that there are significant differences in the business environment.

Correlation Analysis

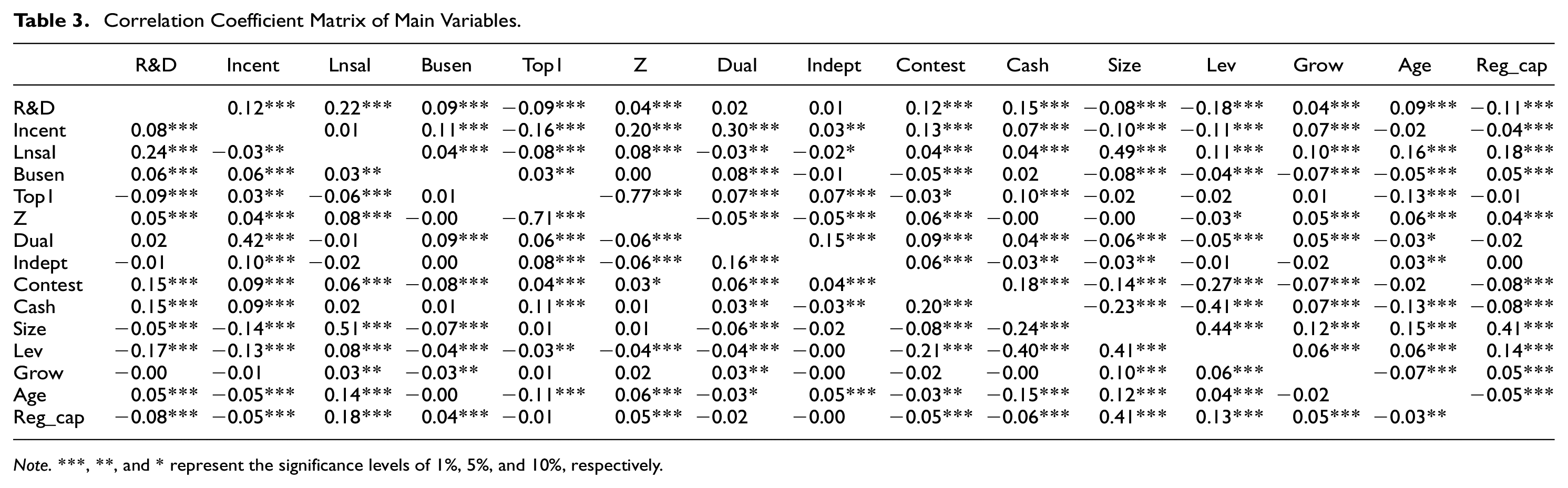

Table 3 shows the Pearson and Spearman correlation analysis of variables. Executive equity incentives (Incent) and payment incentives (Lnsal) are positively correlated with R&D and are significantly positively correlated at 1%, which preliminarily verifies the theoretical analysis in the previous section. The business environment (Busen) also has a significant positive correlation with the R&D of enterprise innovation investment at 1%. It indicates that the better the business environment is, the more enterprises pay attention to the investment in innovation to win a position in the market. Its specific moderating mechanism needs to be further proved in the regression. The correlation coefficient of most other variables is [−0.5–0.5], less than the threshold of collinearity of 0.5, and the significance level is 1%. Preliminary description: there is no severe collinearity problem. In addition, this paper conducts a variance inflation factor VIF test on the previous model, which avoids multicollinearity problems, indicating that the selected indicators and the designed model are appropriate.

Correlation Coefficient Matrix of Main Variables.

Note. ***, **, and * represent the significance levels of 1%, 5%, and 10%, respectively.

Regression Analysis

This paper uses OLS multiple regression to estimate the impact of incentive contracts on enterprise innovation. Due to the need to analyze the moderating effect, the key variables are centralized. Table 4 reports the relationship between long-term equity incentives, short-term compensation incentives, and enterprise innovation, as well as the regulatory effect of the business environment in their relationship.

Regression Results of the Business Environment, Executive Incentives, and Enterprise Innovation.

Note. The values in brackets are standard errors; The symbols ***, ** and * represent the significant levels of 1%, 5%, and 10%, respectively the same as below.

Regression Analysis of Executive Incentives and Enterprise Innovation

According to the regression results in column (1), it can be seen that there is a significant positive relationship between equity incentives (Incent) and corporate innovation investment (R&D) at the level of 1%. For each standard deviation increase of equity incentive, the proportion of enterprise innovation investment will increase by 6.61% standard deviation (the regression coefficient of Incent to R&D, Incent standard deviation/R&D standard deviation). As can be seen in column (3), the estimated coefficient of executive compensation incentive (Lnsal) and enterprise innovation (R&D) 0.006 is significantly positive at the level of 1%. For each standard deviation increase of compensation incentive, the proportion of enterprise innovation investment will increase by 24.82% standard deviation. That is to say, no matter the statistical significance or the economic significance, the equity incentive and salary incentive of senior executives have a significant effect on the innovation investment of enterprises, which verifies hypothesis 1 and hypothesis 2. This result shows that establishing and improving the management incentive mechanism, to a certain extent, provides an “inducement” for critical executives to try to win the promotion championship. This incentive encourages employees to invest in high-risk, high-reward innovation projects, pay attention to new technologies for job advancement and pay increases, and integrate the innovation concept into the business operation and management processes. This incentive also helps businesses overcome path dependence and growth inertia to realize their innovative development. At the same time, we can see that the business environment (Busen) is significantly and positively related to firms’ innovation inputs (R&D) at the 1% level. This result indicates that optimizing the business environment and incentives mechanism collectively promotes firm innovation.

Regression Analysis of Executive, Environment, and Enterprise Innovation

The (2) and (4) columns of Table 4 are the test results of Hypothesis 3, showing the relationship between executive incentive and enterprise innovation in different business environments. First, the business environment positively regulates the incentive effect of equity incentives on innovation investment, with the coefficient of 0.007 being significant at 1%. At the same time, the business environment positively regulates the promotion effect of salary incentives on innovation investment, with the coefficient of 0.005 being significant at the level of 1%, indicating that the optimization of the business environment magnifies the positive impact of equity incentive and salary incentive on enterprise innovation. From the above results, optimizing the business environment will promote fair competition in the market, and the protection of enterprises’ intellectual property rights will be sufficient. When facing more fair and fierce market competition, their past little development experience and slow adjustment speed will hinder enterprises’ development. Motivated executives will strengthen innovation awareness and behavior to maintain the leading edge and consolidate their positions from threats. The project innovation decision is made based on the enterprise’s long-term development. Hypothesis 3 is verified.

Robustness Test and Endogeneity Test

Robustness Test

The following robustness tests are performed to confirm that the conclusions of this research are reliable: (1) Replace the dependent variable index (R&D1). Referring to Huang and You (2020), the proportion of R&D investment in operating revenue is taken as the dependent variable to measure enterprise innovation, and the above assumptions are regressed again. The results are shown in columns (1), (2), (3), and (4) of Table 5a.

(a) Regression Results of the Robustness Test.

Note. The values in brackets are standard errors; The symbols ***, ** and * are expressed at the significant levels of 1%, 5%, and 10%, respectively; controls is a control variable, which is limited to space, and the related results are not listed in detail.

(b) Regression Results of the Robustness Test.

Note. The values in brackets are standard errors; The symbols ***, ** and * are expressed at the significant levels of 1%, 5%, and 10%, respectively; Controls is a control variable, which is limited to space, and the results are not listed in detail.

(2) Shrink the sample. High-tech enterprises have the characteristics of knowledge and technology intensity. They often have more development potential and advantages than ordinary small and medium-sized enterprises in innovation. Therefore, it can not fully reflect the impact of executive incentives on regular small and medium-sized enterprise innovation. The result is universal and representative of most small and medium-sized organizations, omitting high-tech businesses (information transmission software and information technology service sector, scientific research, and technology service industry). After elimination, the sample size is reduced to 5,441, and the regression results are shown in columns (5), (6), (7), and (8) of Table 5.

(3) Tobit model test. Although we have all the observed data of innovation investment of small and medium-sized enterprises, which are continuously distributed on the positive value, more than 10% of the deal is zero. To solve the problem of data truncation, we use the Tobit model to cut the data of enterprise R&D investment left to 0 (Huang & You, 2020) and re-regress the models (1), (2), (3), and (4). The regression results are shown in columns (5) and (6) of Table 5.

(4) One phase behind. Considering that executive incentives may have a specific lag effect on enterprise innovation, the measurement time point of equity and salary incentives is reset to T-1 year as the proxy variable of executive incentives. The models (1), (2), (3), and (4) are regressed to investigate the impact on Enterprise Innovation in t year. The inspection results are shown in columns (5), (6), (7), and (8) in Table 5b. The above results show that the previous conclusion is still valid after the robustness test from multiple perspectives.

Endogeneity Test

(1) Instrumental variable method.

The impact of long-term equity incentives and short-term wage incentives on the innovative activities of small and medium-sized businesses can be somewhat demonstrated by the analysis above. Small and medium-sized enterprises’ superior governance and innovation performance can entice investors to use the two-way incentive mechanism. Still, there may also be endogenous issues brought on by reverse causality. Therefore, this paper refers to the practice of Shao and Wu (2020). The model (1), (2), (3), and (4) are tested by using equity incentive and salary incentive lag as instrumental variables. Columns (1), (2), (3), and (4) of Table 6 are the regression results after adding instrumental variables, which are consistent with the previous conclusions. As an instrumental variable, the salary incentive with one lag period passed the DWH (Durbin-Wu-Hausman) test with robust heteroscedasticity, with p values of .0002 and .0001, respectively, indicating that the independent variable is endogenous. Secondly, the weak instrumental variable test (F statistic is greater than the empirical value of 10) was carried out. The results show that the selected instrumental variables meet the academic requirements. The lagged equity incentive instrument variables can get p values of .7584 and .7490, respectively, through the robust DWH test of heteroscedasticity (Durbin Wu Hausman test), which does not meet the academic requirements of instrument variables. Therefore, this paper analyzes the relationship between equity incentives and enterprise innovation with the PSM model.

Regression Results of the Endogenous Test.

Note. The values in brackets are standard errors; The symbols *** and** are expressed at the significant levels of 1% and 5%, respectively; Controls is a control variable, which is limited to space, and the results are not listed in detail.

(2) PSM test.

This paper adopts the PSM model for analysis, learns from Sun et al.’s (2016) work, kernel-matches individuals from the experimental group (implementing equity incentive plans) and the control group (not implementing equity incentive plans) in the same industry, the same year, and the exact type of ownership, using the control variable as the matching variable of propensity score and resampling to avoid the endogenous problem caused by sample selection deviation. The regression results are shown in columns (5) and (6) of Table 6, consistent with the previous conclusions. The ATT value after matching is 8.71. The balance test shows that the standardized deviation of variables after matching is less than 10%. The T-test is insignificant except that the cash flow (Cash) p-value is .086, indicating that the matching effect is good.

Further Analysis and Discussion

Heterogeneity of Enterprise Property Rights

There are apparent differences in corporate governance and incentive systems between state-owned and non-state-owned enterprises because of the different strategic objectives, institutional environment, and relationships between governments and businesses. These differences may result in other innovative development characteristics in the operation and development of companies. Therefore, by grouping them according to property rights, this paper tests whether hypotheses H1, H2, and H3 remain valid in state-owned and non-state-owned enterprises.

The results of subgroup regressions are shown in Table 7. Although the business environment, executive incentive, and enterprise innovation investment are closely related, they offer different results due to the nature of property rights. The enhancement effect of equity incentives on the innovation of non-state-owned enterprises is significant at the level of 1%, and the business environment significantly strengthens this enhancement. This conclusion is consistent with the regression results of the overall sample, and hypotheses H1, H2, and H3 are tenable. For state-owned enterprises, equity incentives show a negative role in enterprise innovation investment. That means implementing equity incentives in state-owned enterprises is harmful to enterprise innovation. The salary incentive to enterprise innovation coefficient of 0.009 is significantly positive at 1%. The previous hypothesis H2 has been verified, while the business environment has no significance in the promotion effect of equity and salary incentives on enterprise innovation.

Regression Results for the Difference in Nature of Property Rights.

Note. The values in brackets are standard errors; The symbols ***, ** and * are expressed at the significant levels of 1%, 5%, and 10%, respectively; Controls is a control variable, which is limited to space, and the results are not listed in detail.

This paper believes that the reason for this conclusion is that there are differences in the willingness to invest in innovation and resource allocation efficiency held by enterprise executives due to different property rights. Specifically, in China’s non-state-owned enterprises, their operation and development are more dependent on the process of the economic market. The intense market rivalry forces businesses to constantly enhance their innovation management and uphold their hegemonic status by relying on their competence, which fuels the passion of business leaders to implement innovation projects. At the same time, optimizing the business environment further reduces the degree of government intervention, alleviates the administrative distortion of resources, and reduces the government’s preference for some enterprises in terms of resources. An excellent external environment can optimize the allocation of innovation resources so that limited resources flow to the technological innovation activities required by the market with higher efficiency. The market-oriented attitude can encourage business management to focus on innovation activities and enhance enterprise innovation by fully utilizing the technical assistance already available in market transactions.

Executives do not need to adopt more innovative strategies for state-owned enterprises in fierce market competition. Obtaining the required financial results to get equity income may cause a reduction in innovation initiatives with a sluggish impact and high risk, reducing the reliability and organization of company R&D planning and indirectly harming enterprise innovation. The Trial Measures for the Implementation of Equity Incentives by State-controlled Listed Companies (Domestic) stipulates that: “the cumulative equity of the company granted to the incentive objects of a listed company through an effective equity incentive plans shall not exceed 1% of the total share capital of the company, and the cumulative total number of underlying shares involved in all effective equity incentive plans of a listed company shall not exceed 10% of the total share capital of the company,” When the managers of state-owned enterprises are expected to obtain only limited equity incentive income, they will not spend more energy on R&D and innovation projects, which weakens the enthusiasm of innovation. At the same time, state-owned enterprises usually have more policy advantages and financial subsidies in production and operation. They are also interfered with and affected by the goal orientation of “national publicity.” To maintain social stability and achieve full employment, state-owned enterprises have prominent risk aversion characteristics in the face of market investment opportunities and competitive pressure brought about by improving the business environment. The transfer of human capital between industries and enterprises is limited, hindering senior executives’ full utilization of innovation resources. Equity incentives are thus still in the early stages of development to enhance innovation in state-owned firms, and their impact has not been completely realized. However, this does not mean that the effect of equity incentives is not good. As for the overall development of enterprise innovation, there are often a variety of motives and uncertainties in the process of equity incentives affecting it. The impact of equity incentives on enterprise innovation is highlighted after the business environment is relatively perfect.

Mechanism Testing

At present, scholars focus more on the research on the direct relationship between executive incentives and enterprise innovation but lack an in-depth exploration of its internal mechanism. What channel do management shareholding and payment contracts affect enterprise innovation? In fewer research areas, scholars analyzed financing constraints (Mc Namara et al., 2017), risk-bearing capacity (Armstrong et al., 2022), and the effectiveness of internal control (Nguyen, 2018). According to theoretical research, enterprise innovation is frequently fueled by the investment of resources in the innovation subject and external oversight. However, enterprise financialization may result in a strain on innovation resources (L. L. He & Shi, 2022). Therefore, this paper believes that we can also explore two aspects: internal resource management and external supervision environment, that is, enterprise financialization and information transparency, and analyze their impact on the relationship between incentive mechanism and enterprise innovation with actual data to outline the influence mechanism more completely.

Intermediary Effect of Information Transparency

Researchers started looking into information transparency to reduce the degree of information asymmetry between company leaders, shareholders, and outside investors. Dong and Zhang (2022) concluded that analysts are effective information media in the capital market, providing valuable enterprise information through professional tracking. It considerably increases enterprise information transparency and widens the ways via which market participants can get specific enterprise information.

Previous studies have shown that information transparency is essential to enterprise innovation (Guo et al., 2019). Equity and payment incentives can improve enterprise information transparency (Kwangjoo & Jonghwan, 2018) and create a favorable market environment for enterprise R&D. From the above analysis, the implementation of equity incentives for executives will have a strong influence on the enterprise development strategy as well as information resources, and analysts are good at paying attention to and evaluating the sensitivity and undisclosed information of the enterprise, especially the plans and events that can bring excess returns to the enterprise, so as to improve their salary and popularity in the industry. At the same time, if the short-term salary incentives meet executives’ expectations, it will significantly improve senior management’s enthusiasm and sense of responsibility. Likewise, the corporate information will be fed back to stakeholders in the capital market on time, reducing analysts’ costs to capture private information (Dong & Zhang, 2022).

It is challenging for shareholders and outside investors to receive unbiased information on innovation because the current profits and losses in the R&D stage are not mentioned in detail in the enterprise’s financial statements. Meanwhile, unsupervised management may engage in insider trading using the company’s first-hand information sources, harming the company’s interests (Guo et al., 2019). When the corporate information environment is more transparent, the real-time oversight of shareholders can lessen executives’ shortsightedness and self-interested behavior in R&D projects by denying them the opportunity and freedom to conceal moral hazards and unfavorable hiring practices. At the same time, the attention of shareholders to enterprise R&D projects makes executives pay more attention to realizing their commitment to innovation activities (Dong & Zhang, 2022). When external investors predict that the capital security is high through the information of an independent third party, they are more willing to provide financial support for the enterprise’s R&D investment, which facilitates the management to obtain innovation funds (Mc Namara et al., 2017).

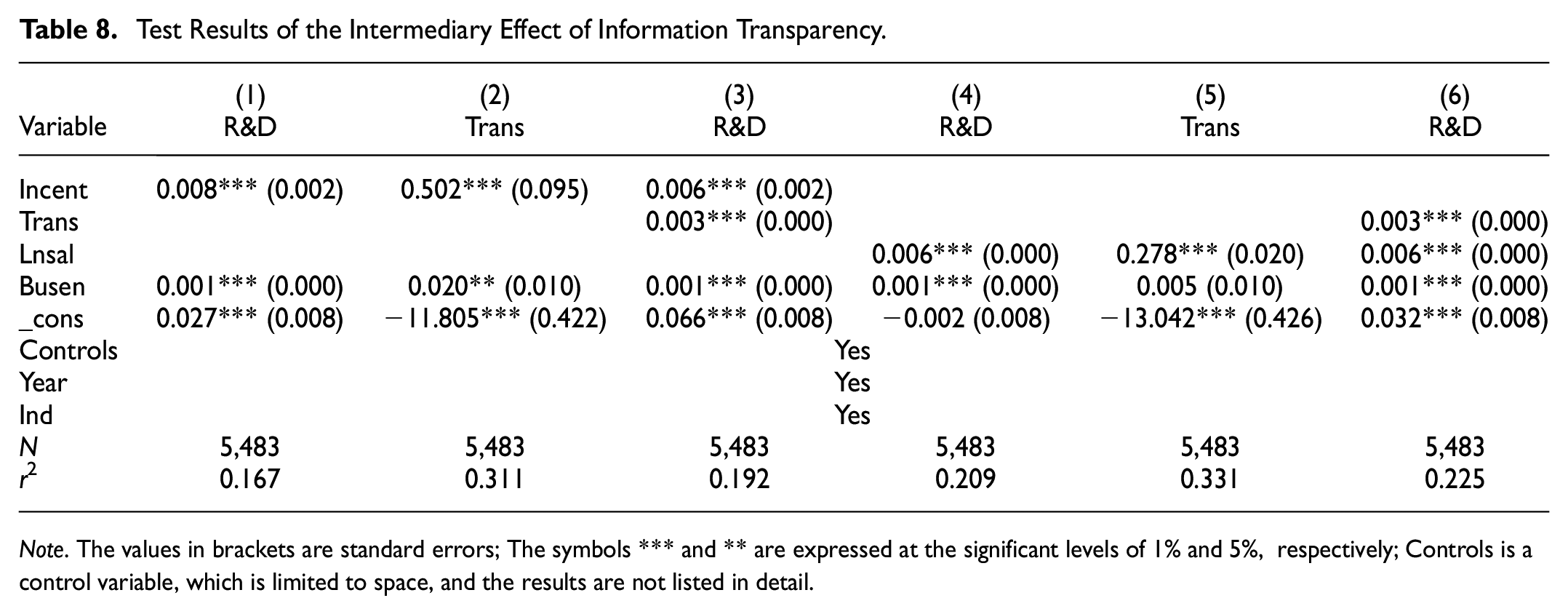

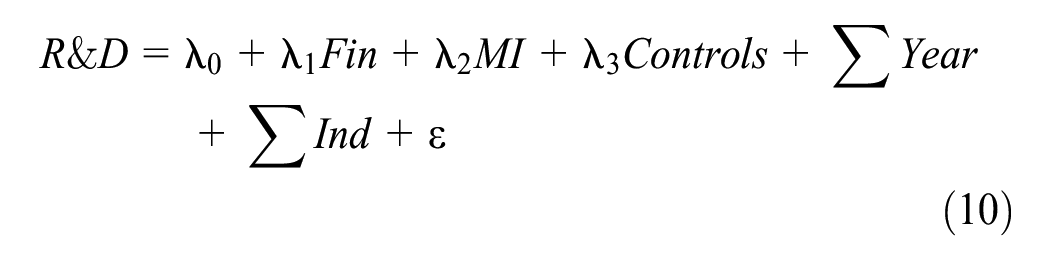

This paper argues that executive incentives can produce a transmission path of “executive incentive—higher information transparency—higher R&D investment” for enterprise innovation. We explore whether information transparency plays an intermediary role in executive incentives and enterprise innovation based on principal-agent theory, information asymmetry theory, and the signaling approach. Based on Chen et al.’s (2017) research, this paper measures the degree of attention of analysts by the natural logarithm of the number of analysts tracked plus one. The number of analysts tracked is directly proportional to the information transparency of enterprises. This paper analyzes the mediating effect of information transparency according to the three-step test procedure proposed by Wen (2014), that is, the regression of models (5), (6), and (7). Here, the parameter MI refers to long-term equity (Incent) and short-term salary incentives (Lnsal) Trans is considered the mediating variable to be tested, representing information transparency. The inspection results are shown in Table 8:

Test Results of the Intermediary Effect of Information Transparency.

Note. The values in brackets are standard errors; The symbols *** and ** are expressed at the significant levels of 1% and 5%, respectively; Controls is a control variable, which is limited to space, and the results are not listed in detail.

Columns (2) and (5) report that the influence coefficient of equity incentives (Incent) and salary incentives (Lnsal) on information transparency (Trans) is 0.502 and 0.278, respectively, which is significant at the level of 1%, indicating that executive incentives can enhance enterprise information transparency and liquidity. The coefficient of information transparency (Trans) on enterprise innovation (R&D) investment in columns (3) and (6) are all 0.003, which is significant at the level of 1%, indicating that the intermediary effect of information transparency is established. The coefficient of equity incentive (Incent) and salary incentive (Lnsal) have all passed the significance level test, meaning that information transparency plays a partial intermediary effect in the path of equity incentives on enterprise innovation. According to the model proposed by Wen (2014), it can be calculated that the proportion of intermediary effect in the total impact is equal to 13.28% and 4.82%, respectively. The regression results demonstrate that management shareholding’s impact on company innovation is significantly mediated by information transparency in an additive manner. In other words, the tracking and forecasting of analysts widen the informational channels and make it easier for businesses to use market resources to foster company innovation. In addition, the bootstrap test can overcome the defect of weak statistical effect in the stepwise regression coefficient test and make the test result more robust. This paper again carries out the bootstrap test for the intermediary effect of information transparency. One thousand random samples are taken from the original samples, and the confidence intervals are [0.0006, 0.0017], [0.0002, 0.0004], respectively, excluding 0. This intermediary effect test verifies the logical analysis of this paper.

Intermediary Effect of Enterprise Financialization

In the fierce market competition, excessive financialization has seen explosive yield growth. According to L. L. He and Shi (2022), enterprises invest in the financial sector for arbitrage and convert industrial capital into the financial capital investment to generate excess profits. As a result, the disconnect between depressed real investment and inflated financial investment is a crucial component of structural imbalance.

According to the shareholder value theory, the financial market essentially reflects the profit-seeking characteristics of enterprise capital (Roberts & Kwon, 2017). As a result, managers’ priorities for investment projects change due to the straightforward pursuit of capital appreciation to obtain non-operating profits. However, financial investment and physical investment often have a relationship of trade-offs. Suppose small and medium-sized enterprises invest their limited funds in the financial industry at the expense of the basics. In that situation, it will have a “crowding-out impact” on actual firm investment, resulting in a lack of capital allocation for investment in innovation activities and impairing enterprises’ core competitiveness (Wan et al., 2020). According to the short-sighted market theory, enterprise managers may avoid long-term investment activities with unpredictable risks and high trial-and-error costs to meet performance indicators. It prevents enterprises from transitioning continuously from financial investment to productive investment. In a fierce market, executives have to increase the acquisition of financial capital to obtain income. The “substitution effect” of financial asset allocation further reduces enterprises’ innovation and development space (L. L. He & Shi, 2022).

According to this study, establishing incentives for business executives can reduce the investment behavior of business managers who choose to venture outside their core competencies. This paper examines whether the degree of enterprise financialization is the channel of the impact of equity incentives and salary incentives on enterprise innovation in order to coordinate the resource allocation of financial and physical investment, along with principal-agent theory and resource-based theory. According to the practice of L. L. He and Shi (2022), this paper measures the financial level of enterprises by the ratio of financial assets to the total assets on the balance sheet. That is, the level of financialization (Fin) = (trading financial assets + available-for-sale securities + held-to-maturity securities + financial derivative + loans and payments + investment real estate)/total assets. Regressions are performed on models (8), (9), and (10), and Fin represents the financial level of the enterprise. The test results are shown in Table 9.

Test Results of the Intermediary Effect of Enterprise Financialization.

Note. The values in brackets are standard errors; The symbols *** and ** are expressed at the significant levels of 1% and 5% respectively; Controls is a control variable, which is limited to space, and the results are not listed in detail.

According to column (2) of the regression results, the impact of equity incentives (Incent) and salary incentives (Lnsal) on enterprise financialization (Fin) is significantly negative at the levels of 1% and 5%, respectively. This finding suggests that executive incentive programs can lessen the degree of enterprise financialization. The influence coefficients of enterprise financialization (Fin) on enterprise innovation (R&D) are −0.032 and −0.031, respectively. They are significant at 1%, as shown in columns (3) and (6). The significance test results for equity incentives (Incent) and salary incentives indicate that the financial market is a part of the intermediary factor of executive motivation that influences innovation investment (Lnsal). In this part, in the bootstrap test, the confidence interval of equity incentive is [0.0000, 0.0005], excluding 0. The outcome demonstrates that the management equity incentive has potential institutional effectiveness as a long-term incentive mechanism to optimize corporate governance and enhance corporate value. It can be used to boost the management team’s operating power and innovation momentum, restrain its short-term speculative behavior, and coordinate the financial and real economies. However, the confidence interval of salary incentive is [−0.0000, 0.0000], including 0. The intermediary effect is not established, which may be because small and medium-sized enterprises face more serious financing constraints. Financial capital has a “reservoir” effect (Y. Du et al., 2017). When there is a shortage of funds, executives motivated by salary are forced to realize them in time under the pressure of declining performance, to resolve the risk of corporate capital chain rupture.

Conclusions and Implications

Innovation is the core element for China to promote technological evolution and break through the constraints of international competition. China and developed nations confront the vulnerability of small and medium-sized enterprises in the context of a new technological revolution and industrial transformation. This vulnerability is not only manifested in the physical exposure caused by a lack of resources and marginalization but also in the environmental vulnerability to cope with external shocks and risks and the susceptibility to respond to disasters and recover (Smallbone et al., 2022). Therefore, the research conclusion of this paper has essential reference significance not only for domestic producers but also for foreign policymakers and corporate investors.

For the government, further enhancing the legal framework for salary and equity incentives and maintaining the healthy and orderly development of the market is necessary. If not, it should support market-driven enterprise innovation decision-making and improve and broaden the structure and breadth of incentive contracts for state-owned businesses. The “egalitarian” compensation system is dismantled, and the firm leaders’ incentive focus is shifted away from on-the-job consumption and political promotion. At the same time, the regulatory authorities should further improve and implement the information disclosure mechanism and regulatory governance system, strengthen financial management and risk prediction, and establish and improve the financial service system suitable for scientific and technological research and development. Enterprises need to correctly understand and evaluate the role of equity incentives in senior executives in combination with their operating conditions and the business environment atmosphere in their regions, implement the performance appraisal system centered on innovative performance, and establish a “top-down” and “bottom-up” salary distribution method that links the evaluation of enterprise managers to enterprise performance, so as to continue to optimize market-oriented recruitment and contractual management, It can form a benign competition relationship of tournament nature between senior executives and encourage managers to innovate and invest in order to strengthen the core competitiveness of enterprises. In the event that it does not, it can employ information transparency to engage with the enterprise incentive system, assess the relationship between financial and physical investment in light of the internal and external environment, and prudently allocate financial assets to play up the restraint that equity incentives have on enterprise financialization.

Shortcomings and Future Studies

This study divides the types of executive incentives into long-term incentives and short-term incentives. It analyzes the impact on the level of enterprise technological innovation, but there are still some limitations. In the future, we can expand the research in the following three aspects.

First, the impact of long-term equity and short-term compensation incentives on the innovation level of enterprises may be complementary. That is, based on implementing short-term compensation incentives for senior executives, embedding equity incentives will help further enhance the innovation motivation of senior executives. In the follow-up study, we can further investigate the interaction of the two types of incentives and the effect of the effective combination on improving innovation levels.

Secondly, this paper mainly studies material incentives, namely, “salary and bonus” and “options and dividends,” while the incentives for senior executives also include non-material incentives, namely, “promotion and comfortable working environment,”“training and learning opportunities.” Later, non-material incentives can be included in the research system to more comprehensively examine how material and non-material incentives affect the long-term innovation level of enterprises.

Finally, the mechanism for evaluating the current business environment has not been consolidated. The relevant micro-data update has a certain lag, which is also one of the recent institutional research’s difficulties. In the future, we can combine the individual micro-factors with the regional macro-environment to create a cross-layer configuration model that influences regional innovation activities. Otherwise, we will further examine the indirect and direct impacts of various business environment components on innovation activities and play a significant role in exploring the variations in the effect of the business environment on innovation levels and the underlying causes for these differences.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We acknowledge the National Social Sciences Foundation of China (No.:23BGL148), foundation of the Natural Science Research Key Project of Universities in Anhui Province: Research on the forecasting utility of business model on financial failure—modeling analysis based on Kalman filtering and logistic regression (No.: KJ2019A0661), and Major Humanities and Social Sciences Research Projects in Zhejiang higher education institutions (2023QN040).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.