Abstract

The concepts of internet banking and mobile banking have led to changes in people’s financial behavior in terms of earning, consuming, and saving. This new concept, which entered the market quite recently, was used at the beginning of the new digital technology in various types of activities, banking operations, and nowadays these services are used by all people who want to save through banks or create new sources of income, as well as to make quick currency exchanges without going to credit institutions. The main purpose of this paper is to analyze people’s behavior toward new digital technologies, e-banking adoption, and non-banking financial institutions internet services. The objectives pursued are: whether e-banking users are homogeneous in their characteristics in the EU 27 and which users have the most convergent or divergent behavior in the EU 27. Statistical data taken from Eurostat 2023 was used for the Sigma convergence analysis, the time series taken into consideration being from 2004 to 2022. The results showed that the changes in the procedural-fiscal-financial sphere are the ones that fully reflect the two principles underlying the tax evolution: digitization and simplification. These results confirm that people are adopting the new digital technology and change their behavior from consumer to prosumer. The study shows that all most categories adopted e-banking using new digital technologies when it comes to consumption and saving, with few exceptions that should be carefully supported.

Plain Language Summary

The concepts of internet banking and mobile banking have led to changes in people’s financial behavior in terms of earning, consuming, and saving. This new concept, which entered the market quite recently, was used at the beginning of the new digital technology in various types of activities, banking operations, and nowadays these services are used by all people who want to save through banks or create new sources of income, as well as to make quick currency exchanges without going to credit institutions. The main purpose of this paper is to analyze people’s behavior towards new digital technologies, e-banking adoption, and non-banking financial institutions internet services. The objectives pursued are: whether e-banking users are homogeneous in their characteristics in the EU 27 and which users have the most convergent or divergent behavior in the EU 27. Statistical data taken from Eurostat 2023 was used for the Sigma convergence analysis, the time series taken into consideration being from 2004 to 2022. The results showed that the changes in the procedural-fiscal-financial sphere are the ones that fully reflect the two principles underlying the tax evolution: digitization and simplification. These results confirm that people are adopting the new digital technology and change their behavior from consumer to prosumer. The study shows that all most categories adopted e-banking using new digital technologies when it comes to consumption and saving, with few exceptions that should be carefully supported. Digital transformation is not just about buying new, modern equipment, or retrieving data quickly and securely, but also about the technical implementation of state-of-the-art IT systems. It should be noted that digitization has had important effects on both public and private organizations and people, which can be translated as follows: time saved in people’s interaction with public and private organizations; efficiency in administrative processes; transparency in their work. The economic environment becomes much more attractive and leads to investment and innovation in all areas. The digitization of all public or private services would also strengthen the administrative capacity of the whole population. Through studies, research, and future studies, it is essential to analyze and demonstrate that new digital technologies and their use could lead to the elimination of tax fraud, increased public confidence in local or central government and confidence in business. Finally, we can say that it is essential that new research in the field of digitization and e-banking use strengthens the literature reviews and explains at a higher level the answers to all research questions.

Introduction

The evolution of digital technology, which includes several stages: the evolution of computers, the development of the Internet, the development of processing and storage capacities, the emergence of new analysis methodologies, etc., and on the other hand, the advent of smart phones, bank cards, and social media have changed people’s culture and consumption and saving behavior (Malecki, 2003). At present, people have three channels for financing their consumption: current income, savings, and bank or non-bank loans.

In the absence of digital technologies these financing channels were used separately by consumers. Any consumer financial or fiscal behavior was based on consumer income (X. Zhang, 2013) or the perception of potential expenditure in case of non-compliance (Aivaz et al., 2022) as significant influencing factors. Permanent income theory appreciates that people adjust their consumption behavior not only according to their current income level, but also according to their current and future income set. Thus, the consumption decision depends on the expected income stream, that is, the long-term average income. Consequently, any policy designed to stimulate the economy by increasing current income cannot produce significant effects. Instead, economic, and social conditions play an important role in directing consumer behavior. Stratification differentiates incomes and, consequently, leads to significant variations in the structure of consumption. There are policies dedicated to stimulate the socio-economic cohesion between individual categories and regions (Munteanu et al., 2020).

With the shift to new digital technology and the development of fintech (Y. J. Shin & Choi, 2019), people’s behavior, fiscal, or financial, has also changed (Das et al., 2017; Hrustek et al., 2019; Khan et al., 2021; Ndou, 2004). At present, there is a permanent financial concern of people and entities. Historically, the concern for saving, reducing expenditure, and increasing income has been a very high priority for the population. The number of people in a precarious financial situation has also increased. Thus, new digital technology is beginning to address more and more financial needs of the population (D. Wang et al., 2021; Dufty et al., 1987). Likewise, advances in the digitization of public services and the development of e-banking have benefited public authorities by improving monitoring and assessment tools (Uyar et al., 2021), while also resonating with corporate social responsibility (Avotra et al., 2021). The modernizations of public services and cost reduction through the implementation of information and communication technology systems have catalyzed the emergence and development of e-governance (Adjei-Bamfo et al., 2019; Fang, 2002; C. Wang & Teo, 2020).

By intertwining the three channels of financing citizens’ consumption, financial behavior also starts to improve significantly. Internet banking solutions are becoming a mass product used by most people, as they bring certain advantages such as major time savings and increased convenience. With the help of these new digital technologies, people can save money, make financial transfers between accounts, make different types of payments, even pay taxes. It is not at all negligible that the money remaining in the bank accounts, after all payments have been made, can be saved. In other words, in this new digital age, people can become their own service providers, income providers, credit providers, savings providers, etc. By using internet banking, people can become their own financial masters, and new digital technologies can offer complex ways of saving and investing.

New financial research has shown that in the EU the digitization of the banking system, for example, that is, the trend toward cashless and contactless banking, is quite accelerated, which is confirmed by the ways in which the EU population makes payments today. Comparative research in the people-digitalization relationship has developed over the horizon of recent years (Aivaz & Condrea, 2012; Malecki, 2003; Pérez-Morote et al., 2020), developing multiple research directions. Similarly, the determinants of individuals’ appetite for digitization have spurred research, showing that digitization is influenced by individuals’ level of education (Elena-Bucea et al., 2021; Nimer et al., 2022; Szeles, 2018).

The problem that is developing is that not all the population adopts e-banking with the central motivation being the desire not to have their income/expenses tracked. Other lines of research have analyzed employee attitudes toward advances in the use of internet banking in terms of concerns about job loss or employer attitudes toward the need for employee specialization in the use of technology in the workplace (Kitsios et al., 2021).

At the same time, researchers have also been interested in investigating the influences that digital transformation has on economic advancement (Cruz-Jesus et al., 2017; J. Shin et al., 2018) or financial systems (Breidbach et al., 2019). According to four studies in the field (Doran et al., 2022; Fu & Mishra, 2022; Guo et al, 2020; Schaupp, 2023) it is observed that there is a convergence of the adoption of digitization amid economic and financial crises post COVID-19. During economic and financial crises, organizations and individuals are often forced to review the way the operate and look for effective solutions to cope with challenges. This digitization is necessary because it will bring to the EU population a significant increase in people’s skills, as they will use online applications or other technological tools in their daily financial activity. The impact of digitization on SME performance or corporate responsibility (León-Gómez et al., 2022; Malaquias et al., 2016; Yingfei et al., 2022), have opened multiple research topics on the role of digitization in the development of sustainable finance.

Digital transformation is inducing a complex process of tradition from “classic banking” to “digital banking.” Could everybody adopt this new digital behavior, especially with a background of the poverty perennity and still higher demand for cohesion? The literature gap, we identified, is the analysis of the specific digitalization characteristics of the banking sector from the users’ perspectives. Our contribution is to make a convergence statistical analysis of users’ e-banking process adoption, during the last two decades, distinctive by their socio-economic characteristics. Therefore, the following four research questions associated with hypothesis were formulated:

Research Question 1 (RQ1): It is growing the adoption of the internet banking across EU countries during 2004 to 2022?

Research Question 2 (RQ2): Are the e-banking adopters homogenous across EU 27 by age, age and level of education, education and gender, age and employment status, residence area urban/rural, and disability level?

Research Question 3 (RQ3): There are the categories with regress in e-banking adoption across EU 27 during the last two decades (2004–2023)?

Research Question 4 (RQ4): Witch are the categories with the highest dissimilarities and divergent evolution of their financial behavior in the studied period?

The aim of the study is to generate an image about the general trend of digital transformation of the banking system and the behavior of the socio-economic categories of users.

Literature Review

Digitalization and e-Banking

Digitization is the process of change brought about by technological leaps in industries and organizations. Digitization is not only the use of more IT processes to take advantage of the benefits of technology and digital data, but it is a comprehensive approach to changes in society and business, respectively in the development of organizations (Malik et al., 2022).

The process of internet-banking adoption has been underpinned by digitization, which has led to significant opportunities to transform old business methods (Angelakopoulos & Mihiotis, 2011; Carranza et al., 2021), socio-economic structures, organizational models, etc. At the level of organizations, that is, credit institutions, the timing of digital transformation planning must be in close interdependence with cultural changes at the level of customers, as well as its members and leaders who are put in the situation of changing their conduct to adapt to new digital technologies (Montazemi & Qahri-Saremi, 2015).

In accordance with the new trends in the economy, the banking system has also changed its strategies and has moved, in recent years, to a hybrid business model, acting both through physical networks and online, moving to omnichannel strategies. The economic and financial crises of recent years have accelerated this digitization process. Digitalization has become a strategic priority for banks in the EU, allowing credit institutions to offer products and services to the public anywhere, anytime, and securely (Lincaru et al., 2018). The entire European banking system is also continuing to invest in infrastructure, in digital platforms, in digital transformation for greater flexibility, agile operation, easy access for customers to classic or innovative products and services, offered online, just a click away, and on a computer or mobile.

Through new digital transformation projects the banking system (Vyas, 2012) aims to achieve greater efficiency of banking operations, cost reductions, in addition to providing superior, dynamic customer experiences dedicated to their real needs.

On the other hand, in addition to investing in digitization and launching new products and services, bankers also talk about the need for investments in cyber security, data protection, combating money laundering and tax evasion. In other words, the last few years have meant accelerating the omnichannel strategy (Rizzi & Taraporevala, 2019), by demanding an ecosystem, based on technology (Mansumitrchai & Chiu, 2012), and responding to the needs of the population (customers).

Currently, one third of all banking units are cashless, and customers can make cash transactions at self-service machines, while most traditional banking is done online. This means that digitized everyday banking products are a modern and affordable alternative for customers (Liébana-Cabanillas et al., 2018), which has spurred banks’ interest in becoming centers for smart financial counseling.

Internet-banking adoption is growing in EU countries. The number of internet banking users has increased dramatically in recent years amid the financial and economic crises. Internet banking is widely used for checking accounts, managing savings, and borrowing (Charmaine, 2022). The self-service area or banking facility is used only for cash payments, deposits, and withdrawals. Self-banking is used only at the premises of the credit institution and relies on the use of ATMs, cash machines, multi-functional machines, banking terminals, thus eliminating the link with a physical bank adviser (Angusamy et al., 2022).

But based on developments in recent years, not all EU countries are ready for mass adoption of digital banking. There is still a significant reluctance toward this change and a low trust in the online environment, especially from certain customer segments. So the traditional and digital banking model will continue to coexist, with banking players incentivized to propose solutions that are as simple and customer-friendly as possible (Shankar & Jebarajakirthy, 2019; Yap et al., 2010), able to break down customer barriers. Platforms that are as explicit, simple, and easy to access for certain age groups (mainly retirees) will have the most to gain. At the same time, the role of the bank advisor remains very important in the process of understanding the needs and finding together with the customers the specific optimal solutions for them (Souiden et al., 2021; Tam & Oliveira, 2017). We appreciate that:

Hypothesis 1 (H1)—The adoption of the internet banking is growing in EU countries.

Convergence

Demand for digital banking services and products have grown over time because of changing lifestyles and the adoption of digital technology. Digitalization, at present, is no longer an option, but most banking operations and products/services tend to become mostly digitalize soon, driving further transformation (Hu et al., 2019; Suryono et al., 2020). In most European countries, given that most people have access to basic financial services such as a bank account, the share of older people is continuously increasing, and the adoption of digital banking among all population groups can bridge the rural-urban divide (Dahl et al., 2008; Furst et al., 2002; Sullivan et al., 2013).

In the era of digital technology, banking customers are witnessing the creation of a new era in which complete (end-to-end) processes have become essential, in which there is a new approach both on the part of customers and their way of banking (Widayat et al., 2020), and on the part of credit institutions that need to adapt quickly to new financial requirements. Demand for digital banking services and products have increased over time because of changing lifestyles and technology adoption.

So, the results show that there is no homogeneity of internet banking users. Most people use online-internet banking on a weekly or even more frequent basis. Individuals, no matter which category they belong to, are in the habit of keeping track of their income and expenditure and even track their monthly budget through digital banking (Krivogorsky et al., 2016). With the development of internet banking and mobile banking (Raman & Aashish, 2021), this is much easier, with digital banking apps providing an overview of income, spending, and savings. There for

Hypothesis 2 (H2)—The e-banking adopters are homogenous across EU 27.

Behavioral Changes

E-banking represents a reform of our financial behavior (Bauer et al., 2005; Haryanti & Subriadi, 2020), regardless of our location (Sharma et al., 2020; Yip & Bocken, 2018). With its help banking customers can make payments, transfers, bank deposits, exchange currency, or find out the status of our bank accounts or card account without going to the bank, via the internet or mobile phone.

In other words, they can consult our bank accounts and even do new banking directly from the computer, without the help of a bank advisor. This means they save time and have access to bank accounts from anywhere in the country or the world (Bharawa et al., 2023). In addition, remote banking is cheaper than traditional over-the-counter banking.

Banking customers can say that the adoption of this e-banking presents multiple advantages to customers (Aisha & Rakesh, 2022), such as:

✓ Saving time: banking customers no longer must go to the bank’s office.

✓ Availability: the service is available regardless of the day or time, through any computer that meets the technical requirements and is connected to the Internet.

✓ Minimal costs: fees are up to 50% lower than at the bank counter.

✓ Control: Banking customers always have access to information about our account balances and benefit from 24-hour assistance.

✓ Security: credit institutions use state-of-the-art technology using encryption systems and guaranteeing optimal security for our transactions.

Analyzing the use of digitization in the banking environment and traditional payment instruments (money order, cheque, promissory note, and bill of exchange) can observe that not all individuals have accepted this financial behavior. For some, digitization is not safe and therefore they are skeptical when it comes to using digital services. Although banks assure their customers about the security of their operations (Dong et al., 2020), the very environment in which they are carried out, the internet, makes this service prone to cyber-attacks. So, in these moments the divergent behavior of the customer in the face of digitalization appears.

To attract more customers and to change their behavior toward digitization of operations (Daragmeh et al., 2021) organizations has started to provide customers with two payment methods: the payment section without authentication and the payment section with authentication. Here and now the change in people’s financial behavior intervenes. Some will want to pay, to buy, to make a loan by logging into the system by entering a username and password, while others, who do not trust the security of their information, will pay without logging in precisely to avoid financial fraud. These untrustworthy behaviors in e-banking or internet banking are brought to the attentions of customers by cybercrime prevention researchers. They want to raise awareness of the danger of online crime involving malware, ransom ware, and banking Trojans (Ayinaddis et al., 2023). These campaigns are aimed at all internet and digital device users, both individuals and businesses, in the face of increasing cyber risks.

Hypothesis 3 (H3)—There are the e-banking adopters with the most convergent or divergent behavior across EU 27.

Hypothesis 4 (H4)—There are banking users categories with important dissimilarities and divergent evolution of their financial behavior unable to e-banking adoption.

Research Methodology

for the present study it was used the indicator e-banking and e-commerce [ISOC_BDE15CBC__custom_5257090] from Eurostat (2023) data base, structured as all individuals or individuals types. There are listed 123 characteristics detailed upon sex, age, education, income, labor market participation, health/disabilities, birthplace, ICT specialization degree, and urban/rural.

The time series considered for this research is from 2004 to 2022.

The first stage was to determine the trend of adoption the e-banking by all individual for the last 19 years in EU countries and Romania position. Have been considered minimal, mean, maximal, and Romanian percent of the individuals already adopted the internet banking.

The method used to measure the real convergence was the Sigma Convergence determined based on the variation coefficient. The applied methodology is Iancu (2007) with the equation (1):

Where:

σ = Standard deviation at time t of the Percentage of individuals which are using Internet Banking;

Yi = Percentage of individuals which are using Internet Banking from country i, with characteristic j;

n = number of countries consider in the analysis

The standard interpretation of the model is for discrete time intervals tn, tn+1, and measures the dispersion of the considered value:

(a) CVtn+1 < CVtn convergence trend, process of σ convergence

(b) CVtn+1 > CVtn divergence trend, process of σ divergence

where CV

The closer CV values to 0 are meaning the more homogeneous of the statistical series and the more representative the mean μ. The closer CV values to 100 shows the more heterogeneous the statistical series and the mean μ is less representative. This is due to the fact that the CV measures the deviation from the mean value. For the practical use of the coefficient of variation it was established the threshold of passing from homogeneity to heterogeneity at 30% to 35% if the dispersion covers 100%. This can be reconsider based on the specific results (Serener, 2019).

Goleţ (2009) considered synthetic indicator of the dispersion around the central tendency an information provider for the evolution of mass phenomena and a base for the decision makers to intervene. The dispersion (Feldman, 2022) reflects the scattering of the values from the central value, a large dispersion reflecting a widely scattered, since a small shows a clustered tendency.

The Research Results

Evolution of e-Banking and COVID-19 Pandemic Effects

The digital transition is done slower or faster based on various variables as cultural behavior (Alhassany & Faisal, 2018; Zhang et al., 2018), client category (Chan et al., 2019), technology evolution and accessibility of users (Rodrigues et al., 2016), customer satisfaction (Ayo et al., 2016), or external factors as COVID-19 pandemic. The first picture we take is the evolution of e-banking adoption from 2004 to 2022 for EU27 and Romania. The results are presenting in Figure 1 the minimal, mean, and maximal values for EU27 countries and Romania.

Information society evolution 2004 to 2022; All individuals’ e-banking users Romania and EU27 (percentage of individuals).

It can be seen that in the last 18 years the gap between minimal and maximal value significantly increased from about 60 to 80 ppt. This reflects an increase of discrepancies between the European countries and lack of cohesion.

Since 2015 there are EU countries that reached approximately 95% of e-banking adoption and enter in a level of stability. The mean growth with about 50 ppt, higher than maximal (40 ppt), that could be consider as a fast adoption on the countries with a consistent e-banking.

The minimal values highlighted the existence of EU countries with low adoption of e-banking, a slow process, only 20 ppt in 18 years, two times less than the maximal. Unfortunately Romania is peripheral/marginal country in e-banking adoption, with few exception the evolutions follows the minimal curve.

We expected that COVID-19 pandemic to speed up the process of e-banking adoption, as it influenced the e-commerce, e-learning, e-governance, e-administration, and so on. This effect is present only for minimal level that knows a consistent increase by double its value.

E-Banking Adopters’ Characteristics Hierarchy by Homogeneity Degree

As we mentioned before the used indicator [ISOC_BDE15CBC__custom_5257090] for e-banking is presented in Eurostat data base for “All individuals” and for 123 types of users considered based on various characteristics. Only for 103 of these categories are data collected for the studied period 2004 to 2022, even so, there are few missing completed by exclusion method (the CV was calculated as average for the number of countries with available data).

We considered in our analysis the value for “All individuals” as a mile stone to determine the categories less convergent, or with higher risk of exclusion. In Figure 2 are presented the CV for 2022 upon age categories and the “All individuals” as average mark.

Coefficient of variation for 2022 upon age.

It is obvious that the marginal categories in e-banking adoption are the very young less than 24 years or aged over 55 years. Potential reasons is less interest for the new technology for the elders and low accessibility to internet facilities, combined with the change resistance, cultural behavior etc (Kuisma et al., 2007). For the yoghs, it can come from lack of funds, unemployment reflected in not constant income.

Age is important and combined with the education level gives a better hint about capabilities of usage the e-banking (Figure 3).

Coefficient of variation for 2022 upon age and education.

The better convergence is recorded for the high educated individuals, no matter the age and medium educated from 25 to 54/64 years, segment of active people. The less convergent are the individuals with low education between 55 and 74 years. These results highlight the role of education in digital adoption especially for the old individuals.

The above findings are confirmed by the CV values obtained for education and gender and education categories. Figure 4 highlights the fact that high educated individuals, no matter gender are having a more convergent e-banking behavior and low educated, manly females are the category most exposed to exclusion from the digital transformation.

Coefficient of variation for 2022 upon education and gender and education.

Figure 5 presents the employment role in digital transformation adoption and e-banking usage. This drives us to the conclusion that the “employed” status is linked to the bank activity (account, card, e-banking application). Holding a bank account to get the income, the individual is “caught” by the bank facilities finding out the options of e-payments and later he finds out about banking products and services as consumer credit, payment in installments, discounts, bonuses, and sieving tools.

Coefficient of variation for 2022 upon age and employment.

The less convergent are the unemployed, retired, or not included in labor force. The studied category are not spited in age segment, they are covering the active life from 25 to 64 years.

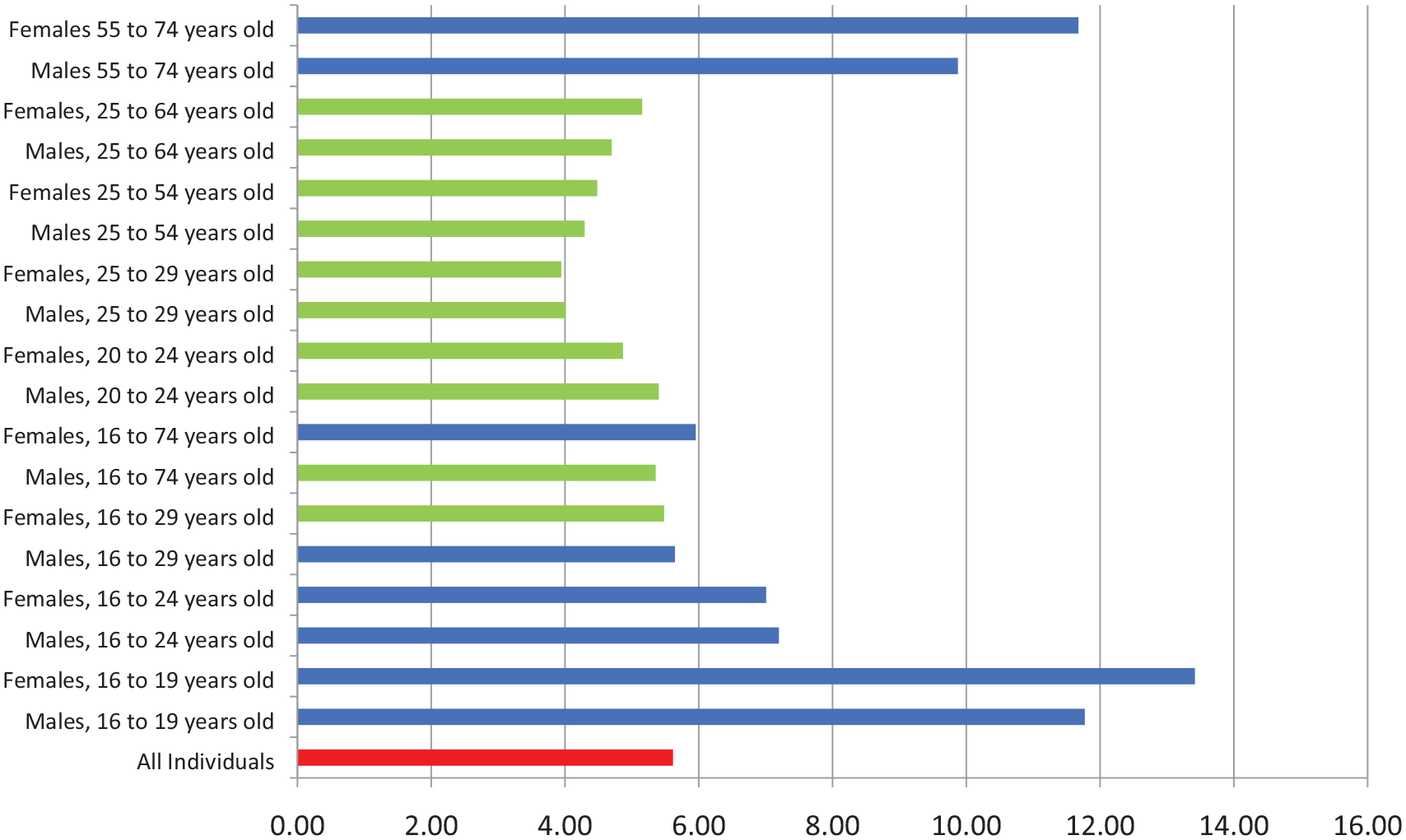

In Figure 6 were selected the gender categories and age segments to evaluate if there are potential discrimination factors. The results confirm a similar behavior of the males and females, no matter the age with some exceptions: females 16 to 74 years have a CV of 5.96 since males a 5.36 one, placed over and under the “All individuals” and females 16 to 29 years versus males with CV of 5.48 respectively 5.64. The +/− difference from “All individuals” CV of 5.62 are very small and the can be term effect, without reflection in behavioral differences. The highest values are found for 16 to 19 and 55 to 74 years old for both female and male. These are reconfirm the fact that the less integrated in the digital transformation from e-banking perspective are very young and old individuals. The age can be correlated with the entry and exit on the labor market, these categories being more exposed of less income and less education, at least up to date education (see Figures 7–9).

Coefficient of variation for 2022 upon age and gender.

Coefficient of variation for 2022 upon location (rural/urban).

Coefficient of variation for 2022 individuals with disability.

Categories of individuals with regress in e-banking adoption (sigma convergence, Eu27 countries, 2004–2023).

Other segmentation variable is the living location; rural and urban developments are different and influence the entire socio-economic environment. The results show that the rural, towns and suburbs are having a lower convergence that the people living in cities. The difference from cities to rural is consistent, but also we find out the agglomeration impact on e-banking convergence. This can be a starting point for research about agglomeration, time saving or socializing behavior, and e-banking adoption.

Among individuals there are persons with disabilities. Unexpected the convergence is below the average for the ones with no activity limitation compared with limited or severely limited.

Additional results show the less convergence for categories without significant differences between male and female ore age. The heist value is calculated for Individuals aged 55 to 74 years with disability (activity limitation)—limited or severely limited 14.04, respectively, for Individuals aged 55 to 74 years with disability (activity limitation)—severely limited 15.00.

The e-banking adopters’ are on a large scale homogeneous, but there are marginal categories with significant deviation from the behavioral main stream.

Discussions

The e-Banking Convergence Across EU27 Countries During 2004 to 2023

The temporal analysis of the e-banking adoption using Sigma convergence identifies three clusters of categories: regression, stagnation, and progress in the last 18 years.

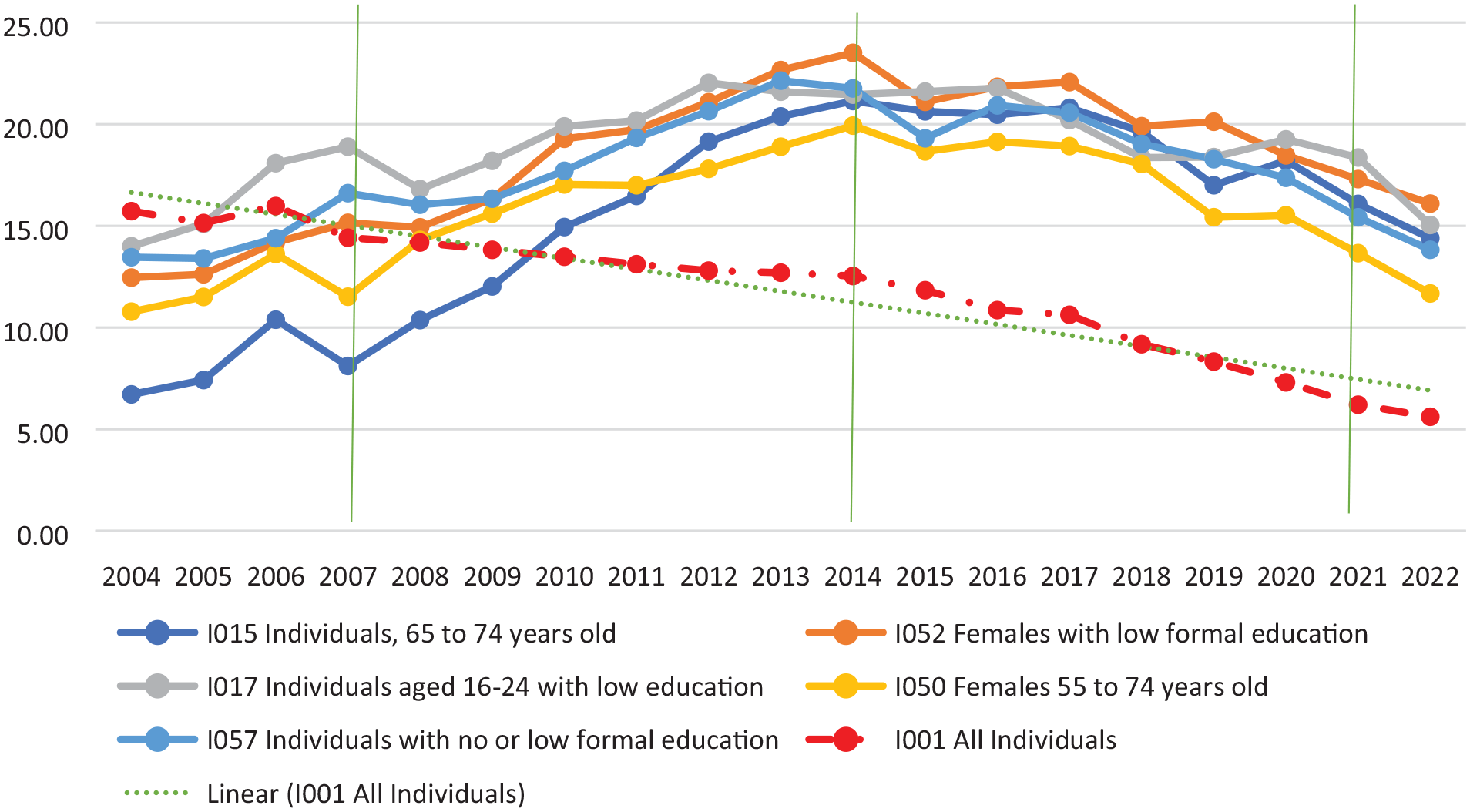

The studied period 2004 to 2023 is covering two of the programing period of EU assistance: 2007 to 2014 and 2014 to 2021. One of the most important objectives of these programing periods was the economic and social convergence encompassing all the directions of action related with the cohesion effect (Weill, 2008). We identify, among the 103 categories studied, 5 categories that had a regression effect up to year 2014 with a recovery tendency from 2014 to 2022, but still with a regress effect. They are 16 to 24 years old or 55 to 74 years for females and 65 to 74 years old and low education youth, females of in general. The findings raise questions about the effects of the EU policies implemented like: At first the policies were not valid for these categories? Were these categories excluded from the cohesion intervention tools? Nevertheless these categories are at a high risk of exclusion if there are not finding ways to speed up the adoption of e-banking.

The most concerning aspect is not necessarily the regress of the category convergence, but the fact that in 2004 they were below the red line of “All individuals” and they are now they a much higher above it. This signals a totally wrong direction and high exposure.

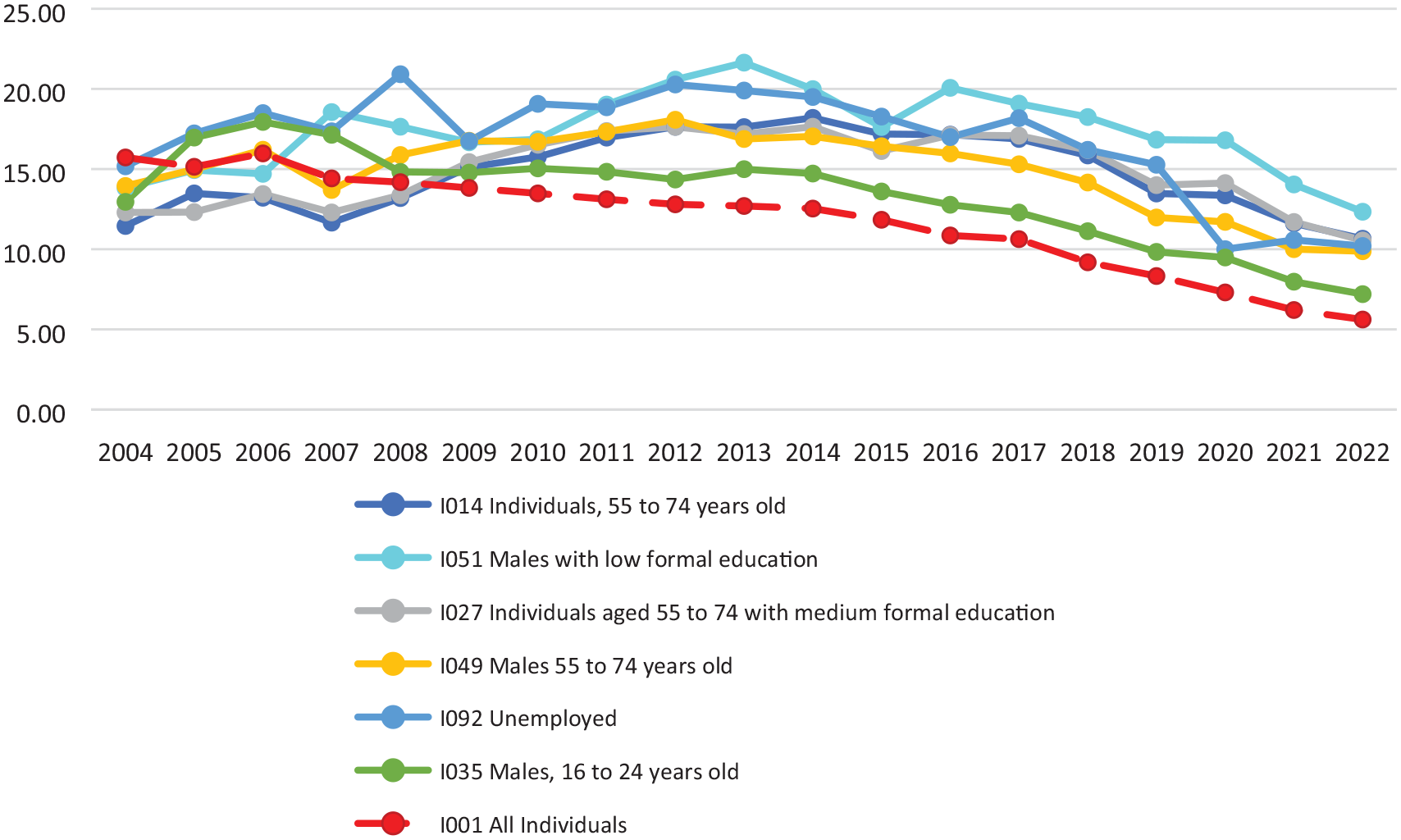

The categories with stagnation are mainly related with the age of 55 to 74 years, unemployed, low and medium education, are presented in Figure 10. The stagnation is relative. If we are considering the initial and final effective value of CV they had a positive evolution, but if they are comparing with the red line of “All individuals” they had a negative evolution. This is the reason we consider them stagnation categories to put them under the lights and to ask for proper public policies.

Categories of individuals with stagnation in e-banking adoption (sigma convergence, Eu27 countries, 2004–2023).

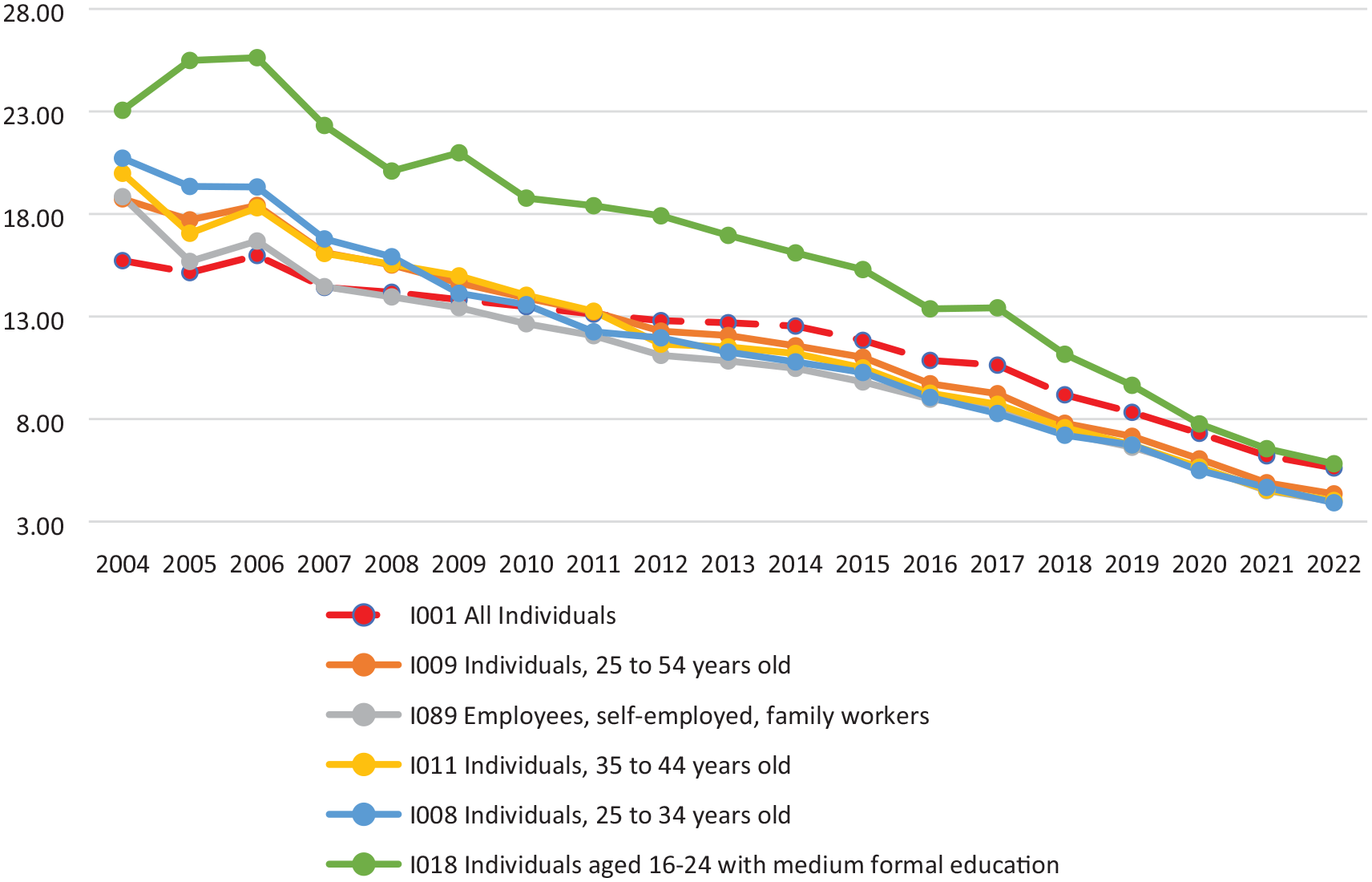

Last but not least the categories with significant progress were identified (Figure 11). They are 25 to 34, 35 to 44 or 25 to 54 years old, employed and 16 to 24 years old with medium education they had a fast convergence in adopting the e-banking. As we commented before they are belonging to the active population, educated, and connected to the social and economic digital transformation.

Categories of individuals with progress in e-banking adoption (sigma convergence, Eu27 countries, 2004–2023).

Figure 12 presents the categories with the highest dissimilarities and divergent evolution in the studied period of time. The positive effect was for the individuals aged 25 to 54 years with low education. Even if they had an accelerated convergence they are still over the average. On the contrary the individuals aged 55 to 74 years with low education had, unfortunately, a negative evolution. The gap between their CV and average is 21.62 about four times. They are most probably unemployed or retired, low and medium education, and rural inhabitants very difficult to be reached by the public policies without a specific, dedicated action of the public authority.

e-Banking adopters with the highest dissimilarities in convergence during 2014 to 2022 in EU27 countries.

Conclusions

From the analysis our opinion is that digitization and the new era of digital technology have greatly changed people’s financial and fiscal behavior in most EU27 countries (Konle-Seidl & Danesi, 2022). The behavior of the new consumer must be anticipated by most companies, be they banking or non-banking institutions, multinationals or public limited companies, and this different behavior is driven by many internal and external factors as well as the COVID 19 pandemic .

The study carried out over the period 2004 to 2022 showed that the transition to the new digital era has evolved differently in the EU27 countries. In some EU27 countries the transition has been slower than in others due to cultural attitudes, distrust of internet banking and digital security (Basdekis et al., 2022). Romania is one of the countries that use internet banking at a minimum level. Digital literacy in Romania is basically only ensured through banking institutions with large customer portfolios. The outbreak of the COVID 19 pandemic has caused profound changes in people’s consumption behavior from cashless to contactless shopping; a shift confirmed by the ways in which people choose to make their payments today. These issues were also identified in the study conducted by Debardvuti, Ashutosh, and Arindam and in which he investigated the impact of COVID-19 on lifestyle change and consumer purchasing behavior according to their socio-economic background. He conducted a questionnaire survey to understand the impact of COVID-19 on consumers’ affordability, lifestyle, and health awareness and how these effects influenced their purchasing behavior (Debardyuti et al., 2022). The adoption of the internet banking is growing in EU countries (H1) was confirmed, but were not find a significant change after the COVID-19 pandemic (speed up or slow down). The adoption has, in our opinion, a moderate rhythm.

For all EU countries, the digital transformation is going on, but the polarization increases between the mean and minimum in regard of the percentage of the individuals (H1). This indicates an increasing tendency to divergence especially after the 2018. Our conclusion is in line with (Hajro et al., 2022) “Countries are converging in digital adoption. Countries with the greatest digital adoption showed, in most cases, consistent adoption across all sectors adoption trends fell into two groups: a consolidated group of leaders, including banking, telcos, and insurance, that are maintaining high adoption levels of 80 to 90 percent.”

The indicator, “all individuals,” used in our research highlighted that the marginal groups in terms of e-banking adoption are the very young, under 24 years, or those over 55 years. Potential reasons are lower interest in the new technology among older people and reduced accessibility to internet facilities, combined with resistance to change, and cultural behavior. In terms of adaptability and use of e-banking, the best convergence is recorded for the highly and medium educated, ranging in age from 25 to 54/64 years. Less convergent are people with a low level of education, aged 55 to 74 years. All these results highlight that the role of education in the adoption of digitization is very important. Highly educated individuals, regardless of gender, have more convergent e-banking behavior, and low educated females and males are the category most exposed to exclusion from digital transformation.

A conclusion is that there is a continuing need for digital inclusion programs. Technology offers many opportunities if it is accessible and if there are programs that not only bring people closer to technology but also help them to use it. The e-banking adopters are homogenous across EU 27 (H2) if it is considered strictly the theoretical interpretation of the results. Practically our findings had shown exceptions, categories very vulnerable with high risk of exclusion. The digital convergence and innovative technologies are forming remarkable disruption in the banking sector and the rate of change is increasing. All these issues related to digital convergence and innovative technologies in banking have been studied by many researchers, including Zahir and Imtiaz. They have analyzed how digital transformation is accelerating in Pakistan’s banking industry due to the changing payments landscape, competition from fintech and the arrival of mobile money services through telecoms (Zahir & Imtiaz, 2019).

In other words, the conclusion is that the young population, both in Romania and in the EU 27, with an average or high level of education is converging much more to the new digital technological era than the population that is inactive. Digitization, across the EU27, is the future for banking and non-banking organizations. Can be appreciate that many consumers will choose to work with different organizations offering remote services and innovative solutions.

Digitalization is the future, because it helps us not only in times of pandemics or financial crises but also in other types of crises. Therefore, from the research the findings are that in all EU27 countries, all types of customers, whether we are talking about unemployed people, people over 65 to 74 years old, women or men, people with disabilities, will want to use services through digital technology. All digital solutions should be implemented gradually, to give consumers time to get used to, understand, and trust them.

Age, level of education, gender, residence area, and status on labor market could be relevant predictors for adopting e-banking behavior and becoming e-banking users. On the reverse, the financial digital vulnerable persons request specific support policies to allow them the access at these highly important services.

Our snapshot analysis indicates that, in 2022 e-banking users differ by the socio-demographic characteristics compared to reference (all individuals):

a. The higher risk of vulnerability in the sense of financial digital exclusion is for Low education aged persons (55–74 years old);

b. The medium risk of vulnerability in the sense of financial digital exclusion is for the youth (16–24 years old) with low education, Individuals with no or law formal education and for Females with low formal education;

c. Still an important risk of vulnerability in the sense of financial digital exclusion is for individuals with disability severely limited, individuals living in rural area, individuals 25 to 64 years retired, or not in the labor force as well as for the unemployed.

There are the e-banking adopters with the most convergent or divergent behavior across EU 27 (H3) was confirmed. Individuals aged 25 to 54 years with low education are the most convergent category since individuals aged 55 to 74 years with low education are the most divergent. The same conclusions can be found in the study conducted in 2021 by two researchers from the Czech Republic. They concluded that the digitization of banks is considered the ubiquitous challenge currently facing the banking industry. In this process of digital change, banks are facing disruptive innovations that require adaptation of almost all cooperation processes. For adults, the study shows that there are many main barriers found in the areas of market and product knowledge, employee and customer engagement, and public benefits. Each main barrier is characterized by several subbarriers of varying importance for banks’ digital transformation and is described in detail (Diener & Spacek, 2021).

(H4)—There are banking users categories with important dissimilarities and divergent evolution of their financial behavior unable to e-banking adoption.

Many organizations in the EU27 need to find a balance between legislation and market regulation, managing the risks that may arise and consumers. The future belongs to digitized, standardized organizations/banks that understand; comply with legislation and regulation and value innovation. They should adopt digital transformation toward the employees and customers. Individuals are in a way forced to adopt the e-banking by the integration in financial flows, need, and regulations.

There are radical changes in financial behavior toward new digital technologies, e-banking is adopted in a large scale, but individuals aged 55 to 74 years old with low formal education do not change their banking services consumer behavior.

Implications

The study on the convergence of e-banking services and the change in the behavior of adopters in EU countries has significant practical, social, theoretical, and managerial implications.

Theoretical Implications

This research contributes to furthering literature with the findings showing that in this new era of modern digital technologies that increasingly penetrate all aspects of consumer life, both economically and politically, the need to adapt to the new trends, rhythms, and coordinates imposed by digitization has become more a matter of avoiding the risks and dangers of falling into irrelevance and inefficiency than a way forward and modernization. For better or worse, digital technologies are reshaping everything from customer behaviors and expectations to organizational and production systems, business models, markets, and ultimately society. To understand this global transformation, research by Dabrowska et al. (2022) has extended previous literature, which has focused primarily on the organizational level, by developing a multi-level research agenda for digital transformation (DT.

Globally, within the EU 27 countries, digitization is the need to integrate it into the information systems established by new technologies. These not only take over from humans’ various tasks that were previously carried out repetitively and even manually, but can create truly automated, domain-specific, self-contained processes that do not require human intervention.

The study consolidates and extends previous researches on technology adoption and consumer behavior in the context of e-banking, adding new insights and understanding in the field. The perspective offered from users’ side and the slightly different behavior of the socio-economic categories contributes to literature with a deeper analysis.

One need only think of the internet banking services offered by some banking and non-banking financial institutions that replace the need for physical presence or interaction between employees and customers to solve problems ranging from the simplest to the most complex, such as granting loans up to a certain limit. Virtual bank branches, for example, have eliminated the need for employees to handle simple transactions, and customers only need a smartphone, an internet connection, and a specific app to interact with the bank where they have accounts. The literature examines the stages of digital transformation facing existing banks in the process of converting to digitally oriented institutions and contributes to this process by clarifying the parameters that define each stage and the key indicators to be tracked. The research carried out represents a reinforcement of the findings obtained by Papathomas and Konteos (2023). Their research identifies three stages for the digital transformation of banking institutions and defines the characteristics of the stages and the distinct actions required for a banking institution to progress through them (Papathomas & Konteos, 2023).

Practical Implications

This example is just one of many that demonstrate the level of efficiency and convenience that digitization can bring when fully implemented in an industry such as banking. However, the digital revolution that has revolutionized all technology cannot change the paradigm either at the microeconomic level or in certain branches of the economy (finance, accounting, management, and production) or in singular domains. The changes are already beginning to be felt at the level of the population, consumers in their social interactions and in their relations with public or private institutions/organizations. Regardless of gender or education, they are beginning to converge on a large scale, to new digital technologies, as digital transformation offers them numerous financial opportunities and is moving with great speed. Besides the individual user are the companies and institutions that are using the e-banking services integrating them in their one digital transformation (Manta et al., 2022).

In this context, digitization and the use of e-banking, which are part of those digital skills, at the global level of the EU 27 are no longer an option, but simply the future. Digital literacy now enables new ideas, new ways of consuming and saving to be found, produced, and distributed.

Social Implications

Social implications refer to the impact that the adoption of e-banking can have on society at large. Behavioral change toward the use of e-banking can lead to increased financial accessibility and inclusion for more people. This can be beneficial for marginalized groups or people who have difficulty accessing traditional financial services or on contrary can become a treat if they are not supported to access the technological change.

The biggest risk that can arise in this new period is the risk of people not being sufficiently prepared for the future. Moreover, this research can be seen as an important pillar in supporting the economic growth and development of the population and organizations, with the most important task falling on preparing individuals to make the most of the opportunities offered by the new technological era. The study could also be used to analyze the challenges in people’s lives posed by the globalized, interconnected, and fast-moving world, as highlighted by Eurostat data. Thus, this piece of scientific research can stimulate and accelerate a much faster transition to the new digital era, from the point of view of individuals, but also of organizations.

Managerial Implications

The managerial implications relate to how the results of the study can be applied in practice and in strategic decision-making in financial institutions. Managers can use the results of the study to guide investments in technology and e-banking development, as well as to improve user experience and customer satisfaction.

These implications can contribute to the development and improvement of e-banking in EU countries in a way that better responds to customer needs and preferences, and the results of the study can have a significant influence on the banking industry as a whole (Xue et al., 2011). The beneficiaries of our study are:

“Banking managers as they decide how to allocate resources to retain and expand their current customer base” (Capece & Campisi, 2013) and how to optimize and design the services to assure the quality. Main goal of the managers is to provide “satisfaction based on quality and ease of use” to a larger spectrum of users (Capece & Campisi, 2013). Even to keep available the tailored banking services for vulnerable customers;

cohesion policies makers in the sense to create appropriate support mechanism in view to assure adequate access to banking services to everyone;

initial education and adult education providers in both areas of financial education and digital skills development; and

users—any individual should have the right to choose the type of service and relation with bank.

Hajro et al. (2022) formulate a strong message: companies need to invest differently in digital offerings looking at the users socio-demographic characteristics. The literature gap identified and address by the current study offers a picture of the users segregation and helps the decision makers to find specific solutions. Our results are in concordance with the classes formulated by (Capece & Campisi, 2013) in Heavy users turned aka younger (21–30 years old), normal users (50–63 years old). “Older people use online services less intensively, seeing them as a complementary channel of conventional usage.”

Regardless the highest quality and ease of use of digital banking services, there are groups of individual exposed on vulnerability risk in the sense of digital exclusion. These individuals’ groups do not change their financial behavior. In other words, the digital transformation of the banking sector if is implemented in simplistic manner increases the inequalities, jeopardize the cohesion. The e-banking is a new digital sector complement by the “classical banking system” and it must be integrated and developed under the innovative and sustainable banking paradigm (Panait et al., 2023).

Limitations and Futures Directions

Digital transformation is not just about buying new, modern equipment, or retrieving data quickly and securely, but also about the technical implementation of state-of-the-art IT systems. It should be noted that digitization has had important effects on both public and private organizations and people, which can be translated as follows: time saved in people’s interaction with public and private organizations; efficiency in administrative processes; transparency in their work.

Key steps toward digitization have been and are the implementation of single portals for paying taxes, setting up bank accounts and taking out loans that reduce the time spent at the counter. Progress is also being made in filing documents and obtaining various authorizations or approvals exclusively online, again improving the relationship between people and public or private authorities.

However, all these developments in the new digital age are not yet uniform. The digitization of banking and non-banking services means increased capacity and possibilities to make people’s lives easier, but it also has major implications for businesses. A simpler, more efficient, and much friendlier relationship between authorities, the public, and business would bring immediate benefits through increased effervescence. The economic environment becomes much more attractive and leads to investment and innovation in all areas. The digitization of all public or private services would also strengthen the administrative capacity of the whole population.

Through studies, research, and future studies, it is essential to analyze and demonstrate that new digital technologies and their use could lead to the elimination of tax fraud, increased public confidence in local or central government, and confidence in business. Finally, we can say that it is essential that new research in the field of digitization and e-banking use strengthens the literature reviews and explains at a higher level the answers to all research questions.

Footnotes

Data Availability Statement included at the end of the article

Author Contributions

Conceptualization, A.G. and O.O.; methodology, C.L. and S.P.; software, C.L.; validation, A.G.; and S.P.; formal analysis, C.L.; investigation, O.O., resources, O.O.; data curation C.L.; writing-original draft preparation, A.G. and O.O.; writing-review and editing, S.P.; visualization, A.G. and C.L.; supervision, A.G.; and S.P.; project administration, A.G.; funding acquisition, O.O. and S.P. All authors have read and agreed to the published version of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by a grant from the Romanian Ministry of Research and Innovation, Program NUCLEU, 2022 to 2026, Spatio-temporal forecasting of local labor markets through GIS modeling [P5]/ Previziuni spaţio-temporale pentru pieţele muncii locale prin modelare în GIS [P5] PN 22_10_0105

Data Availability Statement

Data are available on Eurostat statistics; Eurosat Code SOC_BDE15CBC, E-banking and e-commerce, ICT usage by individuals.