Abstract

The purpose of this study was to examine the relationship between the dimensions of E-Banking service quality and customer satisfaction to determine which dimension can potentially have the strongest influence on customer satisfaction. Data were gathered using a survey instrument, which was distributed among bank clients in the Lebanese banking sector. The data were statistically analyzed using structural equation modeling with SPSS and Amos (20). The findings show that reliability, efficiency, and ease of use; responsiveness and communication; and security and privacy all have a significant impact on customer satisfaction, with reliability being the dimension with the strongest impact. E-Banking has become one of the essential banking services that can, if properly implemented, increase customer satisfaction, and give banks a competitive advantage. Knowing the relative importance of service quality dimensions can help the banking industry focus on what satisfies customers the most.

Introduction

Technology has succeeded in making various aspects of life easier for the societies of today (Rust & Oliver, 1994). More importantly, it has become a fundamental element in improving the quality of services in general and E-Banking services in particular (Joseph & Stone, 2003). E-Banking service is said to rely on the exchange of information between customers and providers using technological methods devoid of face-to-face interaction (Darwish & Lakhtaria, 2011).

Banking sectors in most developed countries have pioneered the area of e-services and have been actively involved in its continuous improvement. The objective was to try to meet the ever-changing needs and lifestyles of modern clients. The Lebanese banking sector, core of the Lebanese economy, has been witnessing unprecedented growth, especially with regard to electronic services (Fakhoury & Aubert, 2015). The usage of E-Banking services by bank clients has grown in the past few years about 25% to 30% (“Bank to the Future,” 2013). Indeed, Lebanese banks are strategically using advancements in E-Banking services for retaining and attracting clients, and are therefore making large investments in implementing the latest E-Banking strategies to maintain and augment their competitive advantage.

Most of the previous studies examined Internet banking to the exclusion of all other types of E-Banking services including applications for smart phones and E-Banking robots. Many studies have investigated how E-Banking service quality is measured, but few have studied the relationship between the quality of E-Banking services and customer satisfaction in Lebanon. This study fills a gap in the literature because it addresses the E-Banking issue in its entirety without making any exclusions, and in Lebanon, a developing Middle Eastern country where, to the knowledge of the authors, no similar study has been conducted before. The implications of this study emphasize the significant influence of E-Banking service quality on customer satisfaction, and the important impact of E-Banking service reliability on service quality perceptions of banking clients.

This study is organized as follows: The following section will present a thorough “Literature Review,” followed by the “Method” and “Findings” of the study. An “Interpretation and Discussion” section analyzes the findings and provides implications as appropriate. Finally, the “Conclusion” section summarizes the study and presents pertinent limitations and recommendations for future research.

Literature Review

E-Banking

Historically, the launching of the first Automated Teller Machine (ATM) in Finland marked the start of a new banking channel, which made Finland the leading country in E-Banking, before it became widely used in any other developed and developing countries (H. Sharma, 2011). More recently, E-Banking, or the distribution of financial services via electronic systems, has spread among customers due to rapid improvement in IT and through competition between banks (Mahdi, Rezaul, & Rahman, 2010).

Lustsik (2004) defines E-Banking services as a variety of e-channels for doing banking transactions through Internet, telephone, TV, mobile, and computer. Banking customers’ desires and expectations with regard to service are expanding, as technology advances and improves. These days, the customer wants to operate and do his or her banking transactions at any location without going to the bank, at any time without being limited to the bank’s working hours, and to do all his or her payments (purchasing, bills, stocks) in a fast and cost-effective way. Consequently, financial services quality ought to be characterized by independence, elasticity, freedom, and flexibility, to accommodate these desires (Khalfan & Alshawaf, 2004).

In Lebanon, E-Banking is still mostly limited to the Internet and mobile telephones. This is due in part to slow development of IT infrastructure in the country. With that in mind, we are defining the concept as the ability to conduct banking and financial transactions electronically via the Internet or mobile telephone applications.

Customer Satisfaction

Customer satisfaction is one of the most important concepts in the field of marketing studies today (Jamal, 2004). Broadly speaking, it links processes culminating in purchasing with postpurchase phenomena such as attitude change, repeat purchase, and brand loyalty (Churchill & Surprenant, 1982). Oliver (1980) explains that the feeling of satisfaction arises when customers compare their perception of actual product/service performance with expectations.

A number of varying definitions have been proposed to clarify customer satisfaction. Yet the notion of comparing postproduct/service performance with pre-formed expectations seems to be common to most definitions. Oliver (1981) defines satisfaction as an emotional postconsumption evaluative judgment concerning a product or service. Similarly, Tse and Wilton (1988) defined customer satisfaction as a “consumer response to the evaluation of the perceived difference between expectations and final result after consumption” (p. 204). Satisfaction can also be described as the feedback of a postpurchase assessment of certain service/product’s quality, and compared with the expectation of the prior-purchasing stage (Kotler & Keller, 2011).

In contrast, other researchers have observed that the impact practiced within the purchasing and consuming stage of the product/service may also have an important effect on the customer’s judgments toward satisfaction (Homburg, Koschate, & Hoyer, 2006). Thus, customer satisfaction is a customer’s feeling of pleasure or displeasure after he or she has distinguished a performance of a product/service with respect to his or her expectancy (Keller & Lehmann, 2006).

Consistent with these definitions, and in so far as this study is concerned, customer satisfaction is the attitude of the customer formulated in response to using any form of E-Banking services. Accordingly, E-Banking attributes may increase, decrease, or keep the same customer satisfaction.

Customer Satisfaction and E-Banking

One main objective of this research is to understand to what extent the quality of electronic services offered by banks would affect the satisfaction of the customer in the Lebanese banking sector. According to Grönroos (1998), there is a steady and positive relationship that gathers both the E-service quality and customer satisfaction. Indeed, Parasuraman, Zeithaml, and Berry (1988) also conclude in a study that the relationship between quality of service and customer satisfaction is very sturdy and durable (Parasuraman et al., 1988). To check this relationship, Jain modifies it in an easier formula and reaches the conclusion that great customer satisfaction immensely depends on receiving a better and higher quality service (Jain & Gupta, 2004).

A number of additional studies point out to a relationship between customer satisfaction and E-Banking services. In their research, Asiyanbi and Ishola (2018) demonstrated that the satisfaction degree of customers in the banking sector increases when using E-Banking services (Asiyanbi & Ishola, 2018). Similarly, Ranaweera and Neely (2003) verified that the quality of E-service is the first step of customers’ satisfaction (Ranaweera & Neely, 2003). Likewise, research conducted in the banking sector by Bei and Chiao (2006) recognized a major relationship between the quality of the service and the customer satisfaction degree of customers. Finally, Zhou (2004) stated that the E-Banking service quality related to reliability has a significant effect on the degree of customer satisfaction.

Dimensions of E-Banking Service Affecting Customer Satisfaction

With a number of studies converging to show a relationship between E-Banking service and customer satisfaction, the question becomes the following: What aspects or dimensions of E-Banking service affect customer satisfaction and in what ways? Our review of the literature reveals that these aspects could be grouped under efficiency, reliability, privacy and security, and responsiveness and communication.

Speed in performing E-Banking services is a determining factor of customer satisfaction according to Parasuraman, Zeithaml, and Berry (1985). Efficiency in terms of quick speedy service is also confirmed by Wirtz and Bateson (1995) and Khadem and Mousavi (2013). Liao and Cheung (2002) find reliability as one of the most important features that customers seek in evaluating their E-Banking service quality. A similar result was also obtained in an empirical study done by Kettinger and Lee (2005).

With respect to privacy and security, a number of elements were identified and studied by researchers including maintaining the confidentiality of operations, refraining from sharing personal information, and insuring a good level of security for the customer’s information (Agarwal, Rastogi, & Mehrotra, 2009; Datta, 2010; Poon, 2007).

According to Madu and Madu (2002), responsiveness is the readiness to support the bank’s customers and deliver them a rapid service. This kind of service can be shaped into four forms. First, the E-Banking system can control and operate the service properly. Second, the E-Banking channels can guide customers toward proceeding properly in case of any failing operations. Third, it can also cover a rapid solution for any possible error in E-Banking transactions. Finally, it can support the customer’s questions with on-the-spot response.

Method

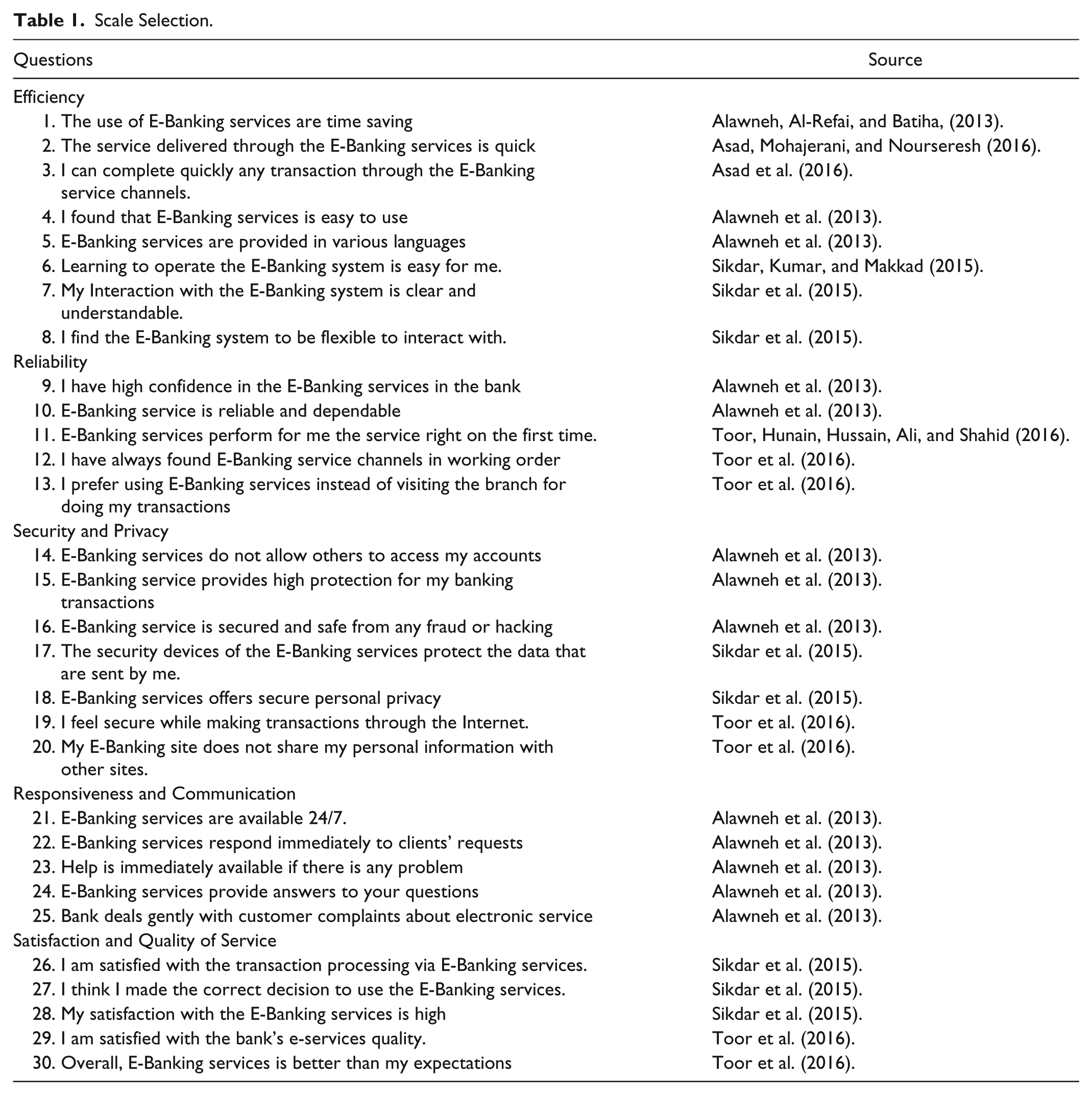

The literature suggested that efficiency, reliability, security and privacy, and responsiveness and communication are four important dimensions of customer satisfaction with E-Banking service quality. Thus, a survey was developed from prevalidated scales to assess the impact of the aforementioned dimensions on customer satisfaction. The scales were chosen from Alawneh, Al-Refai, and Batiha (2013), Asad, Mohajerani, and Nourseresh (2016), Sikdar, Kumar, and Makkad (2015), and Toor, Hunain, Hussain, Ali, and Shahid (2016), as indicated in Table 1.

Scale Selection.

The aforementioned scale items constituted the first part of the survey and sought banking customers’ perceptions about the variables under study. Client perceptions were measured using a Likert-type scale with 1 through 5, 1 being strongly disagree and 5 being strongly agree. The second part of the survey was designed to collect some pertinent personal data from the respondents, such as age, gender, qualifications, income, and period and frequency of E-Banking usage. These items were used as control variables assessing any potential impact on the dependent variable. The survey instrument was translated to Arabic and then retranslated into English to ensure exact translation and that the intended meanings of the items were conveyed. Corrections were made as necessary. The survey questions appear in the appendix.

Not all banks agreed to participate in the study, so the surveys were sent to the branches of the banks that did agree. The convenience sampling technique was used to gather the data, and the surveys were completed by the banking clients who visited the branches and agreed to complete the survey. The survey instrument was also posted online through Google Survey Form and was shared on different social media channels like Facebook. This allowed for the participation of a diverse pool of respondents, and increased the participation rate. The final number of usable surveys collected and analyzed was a total of 258 samples.

The dependent variable was customer satisfaction with the E-Banking service, and it was measured by four items with a high reliability (Cronbach’s alpha = 0.94), while the independent variables suggested by the literature were efficiency and ease measured by four items (Cronbach’s alpha = 0.86), reliability measured by three items (Cronbach’s alpha = 0.87), safety and privacy measured by four items (Cronbach’s alpha = 0.91), and responsiveness and communication measured by three items (Cronbach’s alpha = 0.83). The data were analyzed with AMOS (20) where a sample ranging from N = 100 to 150 was considered acceptable for conducting covariance-based structural equation modeling (CB-SEM) (Tabachnick & Fidell, 2001).

While the main overall hypothesis in this study proposed a positive and significant relationship between Service Quality of E-Banking and customer satisfaction with E-Banking, this main hypothesis was broken down into four testable hypotheses related to the four independent variables considered, as follows:

Findings

Descriptive Statistics

The respondents of the survey were bank clients across different banking institutions in Lebanon. The sample was normally distributed with males constituting 49.2% of the sample and women constituting 50.8%. The majority of the respondents were relatively young with 32.2% less than 25 years old, and 47.7% between 26 and 35 years of age, while clients aged more than 36 constituted only about 20% of the sample. Most of the respondents had college education with 53.1% holding a bachelor’s degree and 41% holding a graduate degree or professional certification.

Most of the respondents (56%) earned an annual income that ranged between US$6,000 and US$17,999, while 23% earned between US$18,000 and US$29,999, indicating that most of the respondents belonged to the middle-to-low income category. Regarding their use of E-Banking services, the majority of respondents (74%) had been using E-Banking services for more than 1 year, and 67.7% used E-Banking services two or more times a month. However, none of the control variables seemed to have any significant relationship with the dependent variable in the model. These statistics are shown in Table 2 below.

Descriptive Statistics.

The Measurement Model

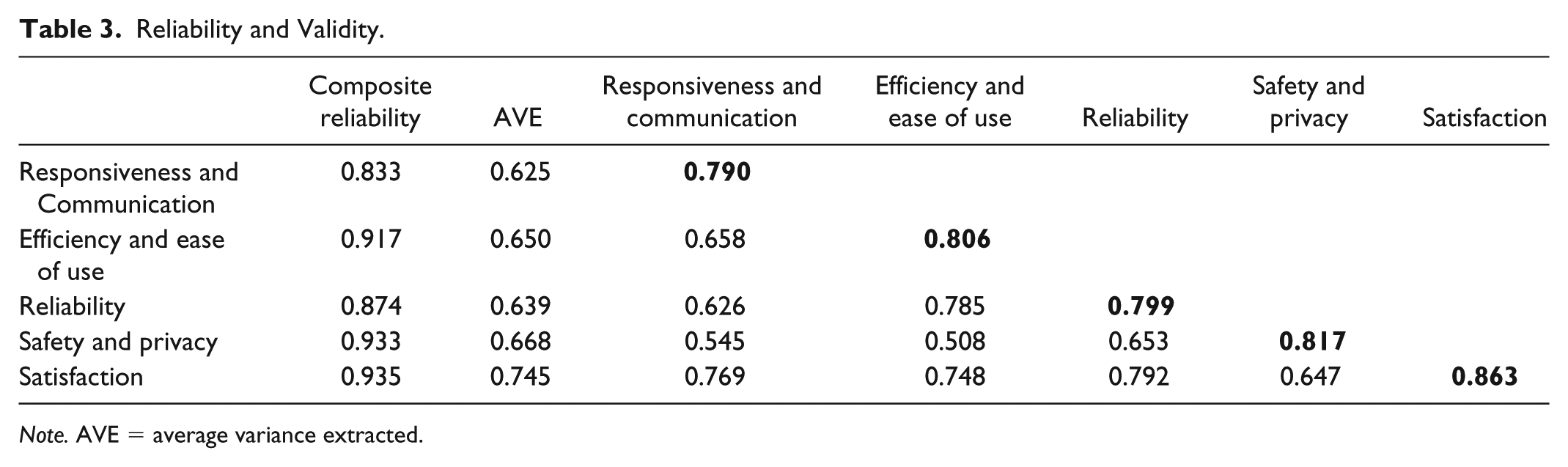

In structural equation modeling (SEM), the measurement model is used to assess the relationships between the indicators and the latent constructs in terms of reliability and validity. The tests of robustness produced the reliability and validity scores shown in Table 3. An explanation of these results appears below.

Reliability and Validity.

Note. AVE = average variance extracted.

Various aspects of reliability and validity were assessed in the measurement model: composite reliability (CR), convergent validity, and discriminant validity. CR measures the reliability of the constructs in the measurement model. It assesses the internal consistency of the construct scales that were used in the survey instrument (Hair, Black, Babin, Anderson, & Tatham, 2010). As shown in Table 3, the CR scores all exceeded the recommended 0.7 threshold (Hair et al., 2010), ranging between 0.83 and 0.93, indicating adequate scale reliability.

Convergent validity was assessed through standardized factor loadings in the measurement model (Figure 1). These loadings show the extent to which indicators of a construct converge on that construct. As shown in the model, all factor loadings, after eliminating items with low loadings, were above the suggested cutoff of 0.5 (Byrne, 2016) ranging between 0.68 and 0.92, thereby indicating adequate convergent validity.

The measurement model.

Discriminant validity assesses whether the constructs under study are distinct from each other by verifying that all average variance extracted (AVE) values exceeded the 0.5 recommended cutoff (Byrne, 2016). AVE is a measure of the variance captured by a construct as related to the amount of variance due to measurement error (Fornell & Larcker, 1981). In this study, the AVE values ranged between 0.62 and 0.74, suggesting that there are no discriminant validity issues with our constructs.

Discriminant validity was further verified by checking that the square root of each factor’s AVE was greater than the correlation between that factor and all other factors in the model (Anderson & Gerbing, 1988; Fornell & Larcker, 1981). This criterion proved reliable for covariance-based SEM such as the one used in this study with AMOS. As shown in Table 3, the square root of each factor’s AVE appears on the diagonal and is greater than the correlations between that factor and the other factors, thus indicating no issues of discriminant validity. See Table 3 for these scores.

The measurement model was assessed for good fit using standard model fit indices (Hair et al., 2010) and was found to have adequate fit according to the following measures: χ2(125, N = 258) = 245.44, where CMIN/df (minimum discrepancy divided by degrees of freedom) = 1.96 (<3), comparative fit index (CFI) = 0.96, Tucker–Lewis index (TLI) = 0.96, normed fit index (NFI) = 0.93, and root mean square error approximation (RMSEA) = 0.06 (<0.08; Hu & Bentler, 1999; Kline, 1998). The measurement model and the standardized factor loadings are shown in Figure 1.

The Structural Model

In this model, there were four exogenous variables (efficiency and ease, reliability, safety and privacy, and responsiveness and communication), and one endogenous variable (satisfaction with service quality). This model fit the data well as per the following standard model fit indicators: χ2(130, N = 258) = 289.61, where CMIN/df = 2.22 (<3; Hu & Bentler, 1995, 1999; Kline, 1998), goodness of fit index (GFI) = 0.89, adjusted goodness of fit index (AGFI) = 0.85, CFI = 0.95, TLI = 0.95, NFI = 0.92, RMSEA = 0.06 (<0.08), and we checked standardized root mean square residual (SRMR) = 0.04 (<0.05).

Furthermore, the R-square values provide an indication of the predictive ability of the constructs of the model. Efficiency and ease of use scored an R-square of 0.66, reliability scored 0.75, safety and privacy scored 0.46, and responsiveness and communication scored 0.63, thereby confirming the predictive ability of the model and all four hypotheses related to antecedents of service quality in this study. The structural model appears in Figure 2.

The structural model.

The SEM results show that reliability of the E-Banking service has the greatest contribution (standardized beta = 0.87) to customers’ perceptions of service quality, followed by efficiency and ease of use (standardized beta = 0.81), responsiveness and communication (standardized beta = 0.79), and safety and privacy (standardized beta = 0.68), the last being the factor with the smallest contribution to service quality of E-Banking.

Next, it was necessary to examine the nature of the relationship between the service quality dimensions in general and customer satisfaction with E-Banking. The main hypothesis in this study predicted a positive and significant relationship between service quality of E-Banking and customers’ satisfaction with E-Banking, and the SEM results supported this hypothesis. The standardized beta was high and positive (β = 0.92; p = 0.000) indicating a significantly high influence of service quality on customers’ satisfaction with E-Banking. Therefore, the main hypothesis in the study was supported. See Table 4.

Summary of SEM Results.

Note. SEM = structural equation modeling.

Interpretation and Discussion

The findings of this study showed not only that service quality is a factor that has a significant relationship with customer satisfaction with E-Banking services but also that reliability is the strongest dimension of service quality affecting customer satisfaction. This is supported by previous research (Bedi, 2010; Kumar, Mani, Mahalingam, & Vanjikovan, 2010; Tan & Teo, 2000), which suggested that service quality is an antecedent of customer satisfaction with a significant and positive influence on it. The findings also showed that the four independent variables (efficiency and ease of use, reliability, security and privacy, and responsiveness and communication) as related to the quality of E-Banking services have a significant effect on customer satisfaction in the Lebanese banking sector. These results are supported by previous research (G. Sharma & Malviya, 2014) which empirically shows that there is a direct relationship between the dimensions of Internet banking service quality and customer satisfaction with banks.

An important dimension of service quality is efficiency and ease of use of that service. According to Lustsik (2004), using a bank’s electronic services offers clients a chance to be cost effective in performing transactions, not only by saving money but also by saving time (Ho & Ko, 2008). Our result is consistent with studies done in other markets (Wirtz & Bateson, 1995), which suggested that higher levels of efficiency increase customer satisfaction with E-Banking.

Reliability, an important element of service quality (Parasuraman et al., 1988), was shown in this study to have the greatest influence on customer satisfaction with E-Banking. This confirms results found in previous research on this topic, as people need to be able to depend on a steady delivery of the E-Banking service (Kettinger & Lee, 2005; Tan & Teo, 2000).

On the other hand, although the dimension of security and privacy had a positive and significant effect on customer satisfaction, thus confirming previous research (Jun, Yang, & Kim, 2004), its impact seems to be lower than the other variables of service quality.

Finally, the variable responsiveness and communication was shown to have a significant and positive influence on customer satisfaction, which is consistent with previous studies (Parasuraman, Zeithaml, & Berry, 2002). Timely responsiveness and effective communication, which can be essential for customers facing issues with E-Banking services, seem to affect customer satisfaction significantly.

Conclusion

This study aimed to examine the impact of E-Banking service quality on customer satisfaction in the Lebanese banking sector. Similar studies had been done for other countries and markets, as was shown in the literature review; however, none to the authors’ knowledge had been done in the Lebanese banking sector. The study followed the quantitative approach where a survey was distributed among bank clients in Lebanon and the data were analyzed using SEM with AMOS. Findings suggest that the four hypotheses in this study were supported by the data, and the main contribution of this study was that reliability, as a service quality variable, was the main predictor of customer satisfaction in this particular market.

With E-Banking services still relatively new to Lebanon and, consequently, still below full development and usage, the results of this study will contribute to a better understanding of what and how Lebanese banks may leverage advancement in information technologies to develop services that meet the expectations of Lebanese customers.

To further extend this research, it is recommended that ways to increase the reliability of “E-Banking” service be investigated, particularly within the Middle East. Moreover, the meaning of “reliability” may differ across countries even within the region, which warrants a careful investigation of this construct, and others, in multiple cultural contexts.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.