Abstract

The globalization of businesses has induced the globalization of boards, and to conform to this trend in the globalization of boards, Chinese firms have had to hire foreign independent directors (FID) as a counterpart to domestic independent directors (DID). Agency theory suggests that an FID contributes to a firm’s financial performance by monitoring and advising the firm’s management. This article explores whether the FID indeed predicts the financial performance of the firm as output and input. Output financial performance refers to the return on investment, and input performance refers to the attraction of foreign investors to the firm after hiring the FID. The evidence from the top 200 Chinese firms shows that the FID does not affect the firm’s financial performance in terms of ROA (return on assets) or ROI (return on investment). However, the FID positively correlates with foreign investment, suggesting that the FID outperforms the DID in attracting foreign investment. These findings point to an alternative explanation, one of which aligns with institutional theory and isomorphism. Institutional theory explains that FID appointments serve conformance rationality more than they serve technical performance rationality. Instead of financial performance pressure, normative conformance pressure influences Chinese firms to adapt to global norms and standards. Such memetic practices support their search for international legitimacy.

Keywords

Introduction

In search of effective governance of industrial organizations for better performance, most extant research has focused on the link between independent directors and firms’ financial performance. Agency theory explains that the independent director monitors and directs the firm’s executives in structure and processes that maximize the shareholder’s value (Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976; Shleifer & Vishny, 1997). Without an independent director, managerial preferences and decisions outweigh shareholder’s’ preferences. Agency theory places the independent director between shareholders and the executive management of the firm. In monitoring and advising the management, this agent (independent director) of the shareholders brings knowledge and technical resources to the firm, contributing to the firm’s financial performance (Dalton et al., 1998; Johnson et al., 1996; Pfeffer & Salancik, 1978). In this sense, agency theory solves the agency problem by implanting an independent director on the firm’s board, despite a lack of support for the firm’s financial performance associated with the independent director (Dalton et al., 1999; Mizruchi, 1996; Rhee & Lee, 2008; Zattoni & Cuomo, 2010).

With the increase in the globalization of enterprises, the globalization of boards has increased to varying degrees across nations and regions (Davis, 2014; Lublin, 2005). Emerging research supports the FID and the firm’s financial performance link, supporting agency theory (Masulis et al., 2012). Ideally, as the appointment of an DID on the board improves the financial performance of the firm, the appointment of an FID enhances the firm’s financial performance (Ahmadjian & Robbins, 2005; Klapper & Love, 2004; Miller & del Carmen Triana, 2009; Peng, 2004). Based on agency theory, the Sarbanes-Oxley Act (2002) requires the appointment of the DID for firms listed on the New York Stock Exchange. Emulating US trends, the Sir Higgs Recommendation Report in the United Kingdom introduced regulations for DID appointments to the boards of listed companies on the London Stock Exchange. Asian companies began to appoint DIDs on their corporate boards (Cho & Kim, 2007). For instance, South Korean corporations began to appoint DIDs and FIDs (Chizema & Kim, 2010). Like other Asian corporations that appointed DIDs and FIDs, Chinese firms began to appoint DIDs and FIDs to their boards (Peng, 2004). With these trends, the FIDs on the boards and the firm’s financial performance have attracted research and practice in the field. However, the question remains whether an FID contributes to a firm’s financial performance. Is it agency theory that explains financial performance (Dalton et al., 1999) or is it institutional theory that explains conformance (Aguilera & Jackson, 2003)? This study explores these questions in the context of Chinese firms.

The current state of the research raises fundamental issues: if DIDs on boards show no concrete effect on firms’ financial performance, then why do firms appoint FIDs? Does an FID contribute to a firm’s financial performance more than a DID does? Two questions guide this study in the globalization of a firm’s board and a firm’s financial performance. (i) Does the appointment of an FID influence a firm’s financial performance? This question points to the output financial performance of the firm. (ii) Does the appointment of an FID attract foreign investment to a firm? This question points to the input financial performance of a firm. Both questions focus on the implications of the FID on the financial performance of the firm. To answer these questions, we develop the framework and hypotheses in the next section, followed by the methods section, the results section, and discussion section.

Framework

Firms appoint DIDs (domestic independent directors) and FIDs (foreign independent directors) for conformance and performance. Conformance refers to the alignment of the firm’s structures and practices to support its leading stakeholders, including shareholders, regulatory agencies, and society. A firm’s performance refers to the financial returns from operational activities concerning inputs. Conformance behavior aligns with institutional theory, and performance behavior of the firm aligns with agency theory. The conformance of a firm with environmental requirements increases the firm’s legitimacy, improving its survival and growth.

The legitimacy argument of institutional theory suggests that firms recruit DIDs to conform to national environmental pressures, and the recruitment of an FID conforms to global standards. Chinese firms appoint both types, DID and FID, to conform to environmental pressures so that their audience perceives them as legitimate business entities. Since European and Asian firms have begun to recruit FIDs, Chinese firms are recruiting FIDs to signal their presence, similar to multinational enterprises (MNEs). Some Chinese firms have relied on DIDs, and others have gone further and recruited FIDs. While conformance follows the institutional theory that legitimacy is necessary for the firm’s survival and the long-term strategic value of the organization, performance follows agency theory, and the financial maximization of shareholders’ values. Hence, the FID has a positive correlation within agency theory and not necessarily within institutional conformance.

According to the agency view, an independent director plays multiple roles in monitoring, controlling, and advising management (Johnson et al., 1996), depending on the affinity of the independent director with the organizations. Directors with a high level of identification with the organization engage more with organizational tasks than directors with a low level of identification (Veltrop et al., 2018). In Chinese firms, the DID is likely to have a closer affinity with Chinese firms than the FID. Moreover, Chinese investors in Chinese firms have more affinity with the DID than the FID. Naturally, DIDs should outperform in engagement, decision-making processes and effective operations. At the same time, the FID brings technical and structural change for efficient operations. The FID brings knowledge to the firm from a global setting. Likewise, the FID brings structural changes to the firm’s dependence on tightly integrated firms in the localized setting. Autonomy from a localized setting increases opportunities and decreases contextual barriers to innovation and performance. Thus, the FID has the potential to improve the structural and technical activities of the firm. Before developing our FID-specific hypotheses, we define the basic terminology used in the study for clarity and consistency.

Executive directors: Executive directors advise senior managers who directly make the operational decisions of the firm. These executive directors advise inside directors. In some cases, they advise top management teams (TMTs) who make, implement, and signal the firm’s strategic decisions (Cannella et al., 2008; Sanders & Tuschke, 2007). In other cases, the literature relegates the senior management team to the upper echelon (Hambrick, 1981; Hambrick & Mason, 1984). In the hierarchy of these executive directors, the top position is the firm’s CEO (chief executive officer), and other executives follow the CEO at various levels. For instance, the COO (Chief Operating Officer), the CTO (Chief Technology Officer), the CFO (Chief Financial Officer), and the VP (Vice President) comprise the upper management of the firm (Finkelstein et al., 2009). These executives engage in the firm’s day-to-day operations, using their technical knowledge to perform their functional and operational tasks, R&D, manufacturing, and marketing activities represented in the firm’s value chain. Hence, these inside directors (managers) partake in the regular operations of the firm compared to irregular engagement of the DID and FID.

Domestic independent directors (DID): DID refers to a nonexecutive director who has no direct relationship with the firm’s operational activities and is a resident of the same country. An American resident is the DID of an American company, and a Chinese resident is the DID of a Chinese company (Johnson et al., 1996, p. 417). First, the DID differs in the level of familiarity with the firm’s internal operations, and these levels of familiarity and knowledge impact the monitoring and advising of the DID (Aguilera & Jackson, 2003; Chizema & Kim, 2010; Dalton et al., 1998; Zattoni & Cuomo, 2010). Second, the DID has a different level of independence from internal executives (Rediker & Seth, 1995). The degree of autonomy of the DID varies (Hermalin & Weisbach, 1988) because of the differences between firms, sectors and nations. Thus, the engagement level of DIDs varies based on organizational tasks and the DID’s identity with the firm (Veltrop et al., 2018).

Foreign independent directors (FID): The FID is a foreign resident rather than a resident of the home country of a firm. The Wall Street Journal reported that FIDs in multinational firms are increasing among American, European, and Asian firms (Lublin, 2005). The increase in globalization has demonstrated the importance of FIDs in multinational firms (Davis, 2014). In emulating this global trend, large Chinese firms have recruited FIDs. A non-Chinese person on the board of a firm as an independent director is the FID on that firm’s board (Masulis et al., 2012). Compared to the DID, a Chinese person on the board, the FID is a foreign person on the board of Chinese firms. Hence, the FID is analogous to foreign direct investment (FDI), and the DID is analogous to domestic direct investment (DDI) for a better description of the contextualized differences (Malik, Kabiraj et al., 2021).

Foreign investors (FI): Foreign investors refer to non-Chinese investors in Chinese companies. The range of investors includes individuals, firms, or foreign institutions. These foreign investors are making various levels of investment in two ways. One way is the direct trading of shares on the Chinese stock exchange. The other way is equity investment in the ownership of the firm which comprises two types of investors in the literature: institutional and noninstitutional investors. Institutional investors refer to governments, hedge funds, and other similar institutions such as banks and insurance companies. Noninstitutional investors refer to individual investors with excessive equity. These individual investors increasingly invest in emerging economies (Ahmadjian & Robbins, 2005; Klapper & Love, 2004; Rhee & Lee, 2008; Seth et al., 2002). China is one such host of foreign institutional and noninstitutional investors. Thus, for our purpose, foreign investors hold equity ownership in the Chinese firm.

Financial performance: The firm’s financial performance is divided into output financial performance and input financial performance. Output financial performance refers to the conventional measure of returns on assets or investment, ROA (return on assets), which measures the result of activities and managerial decisions (Finkelstein et al., 2009), plays the dominant role in the management literature. Scholars in firm governance use ROA to measure firms’ financial performance because it reflects senior management’s roles and functions (Peng, 2004). The ROI (return on investment), which reflects the interests of investors, shows a direct relation with independent directors. Traditionally, agency theory relies on ROI financial performance (Peng, 2004, p. 246), which attracts short- and long-term investors. We link both measures to output financial performance to differentiate between the effects of DID and FID.

The second measure, which refers to input financial performance, measures foreign investment. Foreign investment in a firm is calculated by the quantity of investments or the number of investors. We used the number of investors as the input performance of the firm because the number of foreign investors signals foreign direct investment in the firm. To measure foreign investment in the firm, we introduced the proportion of foreign investors contrasted with domestic investors. Hence, a firm’s foreign investment signifies firm input performance in response to the FID in the context of theory and empirical analysis in this study. The method section explains that the input dependent variable measures the intensity of foreign investors, which is a ratio between foreign investors and Chinese investors (foreign investors/Chinese investors). Now we are in a position to develop our hypotheses.

Hypotheses

The dominant explanation of the FID and a firm’s financial performance in governance research relies on agency theory; so, we develop our argument based on agency theory. Institutional theory offers an alternative explanation when agency theory fails to find a link between an FID and a firm’s financial performance. Since we aim to test the link between the FID and a firm’s financial return in the Chinese context, we build our initial hypothesis on agency theory. Nevertheless, we use the institutional explanation when agency theory fails to explain the absence of financial performance of a firm in response to recruiting FIDs.

Agency Theory and FID Financial Performance

Agency theory posits that a typical independent director monitors managerial behavior and recommends that internal executives align the firm’s operation with the interest of shareholders. The underlying assumption of agency theory explains that independent directors monitor and advise the firm in two ways. First, it assumes that shareholders’ interests and managers’ interests differ (Fama, 1980; Jensen & Meckling, 1976; Shleifer & Vishny, 1997). A shareholder values the maximization of ROI; a manager has the propensity to maximize long-term career development. Naturally, managers formulate and implement strategies to advance their firm’s capabilities and financial performance to serve shareholders. Second, agency theory and other related theories suggest that independent directors have sufficient knowledge to advise internal management for the operational efficiency of that firm, leading to shareholders’ value maximization. (Fama, 1980; Fama & Jensen, 1983). Therefore, shareholders expect the independent director to safeguard their interests by monitoring manager’s’ activities (CEO) and the team, provided the independent director has affinity with the firm and engages in organizational tasks (Veltrop et al., 2018).

Based on the monitoring and advising assumptions of agency theory, studies have shown an increase in domestic and foreign independent directors on boards of companies because these DIDs and FIDs have the incentives and ability to monitor and control internal management for the interests of shareholders. Their incentives come from economic links with shareholders and technical links with other professionals. For instance, scientists, professors, accountants, and lawyers bring their professional affinity to the board. Moreover, their effectiveness on the board increases the firm’s autonomy because they respond to shareholders rather than the CEO. As a result, the incentives and abilities of independent directors induce restructuring of the organization for efficiencies and financial performance (Ahmadjian & Robbins, 2005; Filatotchev et al., 1996, 2000). The evidence also points out that independent directors improve a firm’s financial performance (Walsh & Seward, 1990). Empirical research explains that independent directors improve the financial efficiencies of firms (Baxter & Jermann, 1997; Rhee & Lee, 2008). Most of this positively correlates the DID to the firm’s financial performance anywhere. Since DID correlates with the firm’s financial performance in any setting, we propose the following hypothesis in the Chinese context.

Hypothesis 1: The DID on a firm’s board positively correlates with a firm’s financial performance.

As agency theory informs the link between a DID on the board and its positive link to financial performance in a national-level setting, agency theory also appeals to independent directors beyond a national location. In the last three decades, the increasing trends of globalization have encouraged agency theory research in FID (foreign independent directors) of large firms. With the internationalization of firms’ operational activities, the globalization of the boards has emerged as a new phenomenon (Davis, 2014; Masulis et al., 2012). Recent evidence shows that Chinese firms have begun to appoint FIDs to firms’ boards (Chen et al., 2016). According to the assumption of agency theory, global firms appoint FIDs for better financial performance because firms distance themselves from domestic capital and production systems (Oxelheim & Randøy, 2003).

Furthermore, the level of independence of FIDs increases firms’ financial performance compared to DIDs because of the degree of independence from boards (Finkelstein et al., 2009). Further studies show an increase in FID’s human and social capital in firms’ financial performance (Lai et al., 2019). Since an increase in the independence of FIDs from DIDs increases firms’ financial performance (Shleifer & Vishny, 1997) and foreign institutional investors react positively to a FID (Cao et al., 2017), we link the FID to a firm’s financial performance.

Hypothesis 2: The FID on a firm’s board positively correlates with the firm’s financial performance.

The preceding FID hypothesis follows agency theory to conclude that a firm’s financial performance is its output. Agency theory also includes the input of a firm’s financial performance. The input of a firm’s financial performance refers to foreign investment compared to domestic investment. Foreign investors bring FDIs to the firm, and domestic investors bring DDIs to the firm (Malik & Kabiraj, 2021). Earlier, we explained that agency theory links the FID to a firm’s financial performance. Once an FID is appointed, the firm’s financial performance improves because the firm’s restructuring becomes aligned with shareholder value.

Moreover, an independent director brings human and social capital to a firm in its restructuring process and output (Lai et al., 2019). Although the empirical relationship between an FID and a firm’s financial performance as output is mixed at best and weak at worst (Mizruchi, 1996), the FID trends are increasing globally, except for the USA (Lublin, 2005). Therefore, the agency theory’s potential reasoning considers a firm’s input financial performance in the form of foreign investment vis-à-vis domestic investment.

Agency theory explains that FIDs attract foreign investors to a firm, increasing its input financial performance. The FID on the board brings technical knowledge and organizational and operational skills to the firm, thus attracting foreign investment flows to the firm for its expansion and growth, generating opportunities for the potential financial performance of the firm. However, agency theory combines output financial performance and input financial performance (investment) of a firm. Output financial performance exceeds input financial performance because agency theory prefers existing investors in a firm more than potential investors. The potential investor draws on institutional theory to reduce uncertainty for future returns on investment. The existing investor draws on agency theory to reduce the gap between management and shareholders. Therefore, attracting investors requires institutional mechanisms as signals to reduce uncertainty for a potential investor.

Institutional theory suggests that organizational structures, strategies, and activities rarely align perfectly with the technical core for efficiency and financial performance (Scott, 2001). Instead, structures, strategies, and activities are mostly aligned with institutions in the environment for conformity and credibility (Deephouse & Suchman, 2008). To these firms in their fields, conformity with the standards and rules of others becomes more important than efficiency and financial performance in terms of their survival and growth (DiMaggio & Powell, 1983). From the institutional theory perspective, firms seek isomorphism with their environment for other reasons: (a) coercive, (b) mimetic, and (c) normative (DiMaggio & Powell, 1983). Coercive isomorphism rests on regulatory mechanisms; normative isomorphism rests on the norms and standards of the industry; and mimetic isomorphism rests on cultural cognitive assumptions (Scott, 2001).

Coercive isomorphism states that a firm is required to hire a certain number of independent directors. The Sarbanes-Oxley Act of 2002 requires all listed companies to appoint a few independent directors to the board. Likewise, in the UK, the 2003 Sir Higgs Recommendation Report requires independent directors on the board of listed firms. Firms in other countries emulate these models for their firm governance (Zattoni & Cuomo, 2010). The Chinese Securities Regulatory Commission (CSRC, 2001) requires a firm to appoint certain independent directors. A Korean firm governance regulation requires listed companies to appoint 50% independent directors to the board (Chizema & Kim, 2010; Rhee & Lee, 2008), considered as coercive isomorphism in institutional terminology compared to normative isomorphism.

Normative isomorphism explains that firms mimic the structures, strategies, and behaviors for the symbolic purpose of being legitimate and attractive to their audience. Long before the current development of institutional theory, Veblen (1920) suggested that firms may behave to conform to the rules of the industry, as individuals conform to the rules of their societies. If other industrial leaders or groups of small firms behave in a certain way, the focal firm needs to follow that behavior in its structure and practices. The normative part of the isomorphism argument is that less legitimate firms gain legitimacy by mimicking the policy and practice of firms that have already gained legitimacy for those structures and practices (Suchman, 1995). Although mimicking may or may not contribute to financial performance or new resource acquisition (Zimmerman & Zeitz, 2002), its motives extend beyond the technical efficiencies associated with agency theory (Oliver, 1997). Instead, the firm develops a governance structure that appears proper to its audience from the perspective of the industry leaders. In other words, normative institutional isomorphism explains that firms hire DIDs and FIDs to adapt to their environmental requirements (Ahmadjian & Robinson, 2001) by adapting to or ignoring industry norms and standards.

Some firms follow suit related to changing trends. In so doing, they follow industry rules such as DID or FID recruitment trends, regardless of the contribution of these appointments. These firms perceive their actions as part of the innovation framework (Staw & Epstein, 2000, p. 528) and copy industry leaders’ state-of-the-art structures and practices, such as adaptive structure and practice, regardless of their technical ineffectiveness. This bias is recognized in the organizational and management literature (Abrahamson, 1991). Those firms who ignore or reject this bias may face normative pressure that reduces their acceptability and importance (Peng, 2004). The second group of normative isomorphism consists of those firms that ignore industrial norms and standards and venture into isolated fields and practices.

In line with normative practices in Western industrial governance structures, Chinese firms widely recruited DIDs and FIDs after Chinese government regulation in 2001 (Peng, 2004). However, some Chinese firms recruited DIDs and FIDs before the regulation became effective. The regulation requires DIDs, not FIDs, to be appointed to Chinese firms. Therefore, normative isomorphism explains why Chinese companies appointed FIDs without evidence of financial performance before the regulatory mandate became effective.

Like their international counterparts, Chinese firms have joined the global trend in innovative governance structures and practices. For instance, they have hired independent directors, domestic (DIDs) or foreign (FIDs), for symbolic purposes. Evidence shows that firms in developing economies have begun to adapt to governance mechanisms because hiring independent directors has become the hallmark of effective governance structure after the United States introduced policies to regulate firms. The argument states that these appointments of FIDs signal a firm’s effectiveness, appropriateness, or both to audiences of the firm. Among the critical audiences of firms, investors expect to see the conformance of firms with global norms and standards for legitimacy to fill the unanswered blanks (Deephouse & Suchman, 2008).

This credibility argument falls into the mimetic isomorphism of institutional theory, and it explains why firms appoint FIDs. Foreign investors tend to be reluctant to invest in markets in which they lack understanding. The lack of understanding of the market (institutions and management practices) generates information asymmetries, leading to uncertainty between investors and foreign markets. For instance, Chinese companies’ structures, strategies, or operations differ from Western firms in many ways: ownership structure, information disclosure, and management style. Moreover, the information asymmetries between foreign investors increase in culturally different markets (Malik, 2020b; Malik, Xiang et al., 2021; Malik & Zhao, 2013). National culture shapes the logic of managers, which translates into management styles (Finkelstein et al., 2009; Mintzberg, 1979). To bridge the foreign-local information gap, it becomes imperative for Chinese firms to send understandable signals to their foreign investors. Hiring an FID is one such signal that Chinese firms indeed conform to international standards. Such mimetic isomorphism in institutional theory explains this chain of reasons. (DiMaggio & Powell, 1983).

Foreign investors have a better understanding of Chinese firms when the Anglo-Saxon model of the structure is practiced, which allows a focal firm to meet the necessary conditions for the memetic pattern of isomorphism. A Chinese firm resembles a foreign firm, regardless of whether the foreign firm and Chinese firm differ in processing the functional context due to different local contexts and technical advantages. Technically, foreign directors rarely attend frequent board meetings in China that provide consultative services to firms’ executive management. This lack of attendance by independent directors affects other attendees, impacting the organization’s overall operation (Nowland & Simon, 2018). Logistics, timing, and cost prohibit the FID’s contribution to the firm’s financial performance (Lublin, 2005). Although the FID contributes to firms’ human and social capital, failure to attend board meetings impedes the FID’s ability to monitor organizational tasks (Lai et al., 2019). Even though the FID does not have an active role in monitoring and controlling the board, the FID has a symbolic role of representing legitimacy and reducing foreign investors’ uncertainty. If these assumptions hold, then the FID attracts foreign investors without evidence of financial performance.

Hypothesis 3: The FID on the board of the firm positively correlates with foreign investors of the firm.

Methodology

Setting

The research draws evidence from the top 200 Chinese firms in the high-technology sectors. Chinese firms in high-technology sectors are increasingly internationalizing their operations in different stages of the value chain. They aim to attract foreign investors, gain legitimacy for their domestic and foreign operations and develop global brand names. With the globalization of business operations through different changes, Chinese firms have begun to appoint FIDs on their boards. The internationalization of corporate boards in China follows institutional changes and global adaptation. In 2001, the first institutional change occurred in governance regulations in China (CSRC, 2001). Public policy introduced DIDs in Chinese firms, and some Chinese firms began to appoint independent directors to their boards. The second institutional change occurred in response to Chinese firms’ globalization. Some Chinese firms shifted operations overseas, others listed on foreign stock exchanges, and others acquired a part or whole of a foreign firm in the host markets.

This rapid growth of Chinese high-technology firms offers another reason for this research. Chinese firms have surpassed their counterparts in the world in patent applications, except for those in the USA. Likewise, the Chinese high-technology sectors have grown exponentially based on science and innovation productivity (Malik & Huo, 2019). Chinese competitiveness for foreign investment has resulted in China being among the top 5% of FDI destinations (Malik et al., 2021). We conclude that high-technology firms need to recruit FIDs for their foreign markets for high-technology exports (Malik et al., 2020), to attract foreign investors. Recent tension between Huawei’s high-technology firm in the information and communication technology (ICT) sector and firms in the United States (and United States’ allies) suggests a good reason for FIDs.

Sample

The sample comprises the sales revenue of the top 200 Chinese firms. In these firms, foreign investors hold a minority stake, while Chinese firms hold a majority stake in all 200 firms by the end of 2010. We excluded three firms because of missing data, leaving a sample size of the 197 largest firms in China. These firms represent two sectors: the service and manufacturing sectors. Thomas et al. (2007) use the first two digits of the standard industrial code (SIC) to differentiate the two sectors. In line with the SIC two-digit codes, we coded the data, which divided the sample into 26% of firms in the service sector and 73% in the manufacturing sector in China. Both manufacturing and service sector firms build on information processes, knowledge inputs, and high-technology fields. Therefore, large firms in low technology sectors are not included in this sample.

Data Sources

The data came from Osiris, relevant stock exchanges, firm websites, and online open sources. We used this database for the financial performance, governance structure, and industry of the firm. The data include approximately 46,000 active and non-active companies in the world. Indeed, this source covers almost all Chinese firms listed on any stock exchange. Stock exchanges provide public announcements and senior management-related information. Likewise, firm websites provide some information in Chinese and English, which complemented our required data for the final analysis.

Dependent variable

The dependent variable has two dimensions: output financial performance and input financial performance. The output financial performance is further divided into two measures: ROA and ROI. We averaged both measures for a firm’s last 10 years. The input dependent variable refers to the intensity of foreign investors. The intensity is measured as the ratio of foreign investors to Chinese investors in Chinese firms (foreign investors/Chinese investors). Previous literature uses the percentage of foreign ownership (Rhee & Lee, 2008). In our sample, the foreign ownership of a typical Chinese firm stays closer to 25%, and the share of the investment value lacks clarity. Therefore, we rely on the number of investors and their ratios in the input dimension of financial performance.

Independent variables

The first independent variable refers to the DID, and it measures the proportion of the DIDs on the board (DID/Board size). The second independent variable measures the proportion of the FID on the board. Furthermore, we used the FID and DID ratio to find the intensity of the FID on the financial performance and foreign investment between the two types of independent directors.

Control variables

The first control variable represents the firm’s business sector. We used a dummy variable to differentiate the sector and coded 1 for service and 0 for the manufacturing sector. The two-digit SIC helped us to differentiate industries. Based on previous research, the SIC code offers stylized facts in management research (Thomas et al., 2007); therefore, we defined industry differences based on formal categories to control inter-industry differences. In previous literature, the contingencies of firm- and sector-level variables reflect the firm’s directors or financial performance (Minichilli et al., 2009).

The second control variable measures the firm’s size. Following other studies (Peng, 2004), we measured the number of the firm’s employees, taking an average of 10 years of the firm’s size variable. The firm’s size influences its management’s decisions and the audience’s response in two ways. On the one hand, a firm’s power in its environment increases with its size. On the other hand, a firm’s larger size opens the firm to scrutiny from its audience for its structures and behaviors. In the context of governance structure, large firms attract and hire DIDs or FIDs for a different purpose than small firms with different levels of organizational legitimacy. Small firms face legitimacy deficiencies and the threat of non-survival. They may hire more foreign directors to gain legitimacy in their environment. Hence, we controlled for firm size, as did some previous authors in the firm governance field (Dalton et al., 1998).

We also controlled for the firm’s age for the same reasons as the visibility and legitimacy of the firm. Age measures the number of years since the birth of the firm.

The fourth control variable measures the board’s size. The board’s size reflects the scope of the board structure, comprising the number of directors on the board. Because the size of the board affects the organization’s strategy, structures, and financial performance (Finkelstein et al., 2009, p. 229), we included it in the analysis.

Analysis

We used ordinary least regression (OLS) based on the dependent variables. The dependent variables are continuous variables, and they are normally distributed: the ratio (FID/board) and financial performance (ROA and ROI). Thus, a continuous dependent variable should use ordinary regression (Greene, 1993). The following equations present the model-specific captions.

Y = dependent variable (financial performance and/or foreign investors).

Xi = Independent variables (DID and FID)

Βi = coefficients.

Results

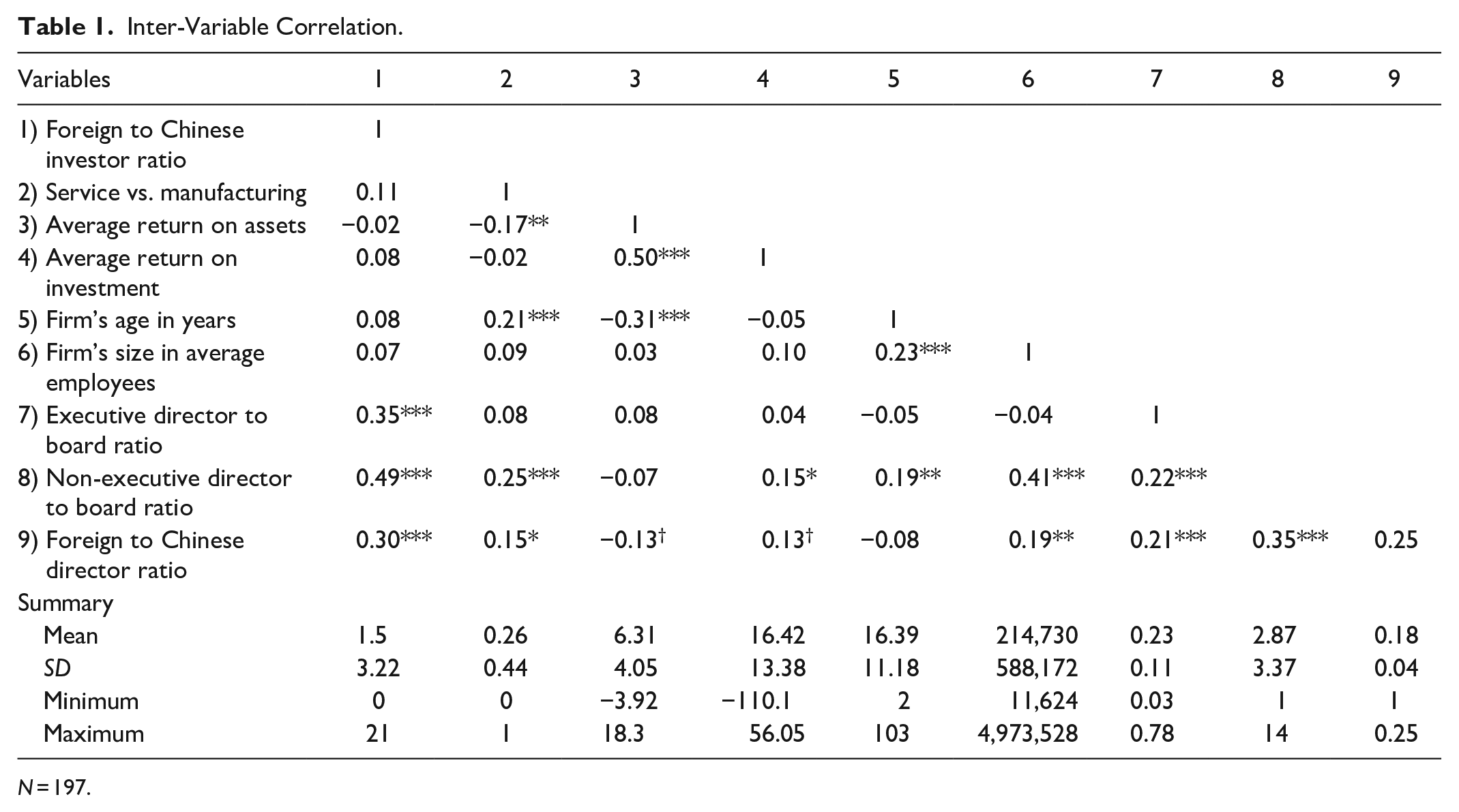

The results are presented in Tables 1 to 6. Table 1 shows the inter-variable correlation and summary statistics. The two dependent variables in the summary statistics represent foreign investors and the ratio of foreign directors to the board’s size. The mean of foreign investors/domestic investors exceeds 1.5, and the proportion of FID is 18%, which means that 18 out of 100 directors make up the FID. Previous research reports similar proportions of FIDs to national board members (Masulis et al., 2012).

Inter-Variable Correlation.

N = 197.

Table 2 shows the multicollinearity diagnostics measured using the variance inflation factor (VIF). The table shows the financial performance measures of ROA and ROI with their respective VIF values. Neither side violates the multicollinearity assumption. In social sciences research, a VIF value below ten does not violate the assumption because our highest VIF value (2.14) remains far below the threshold (Cohen et al., 2002).

Variance Inflation Factor.

Note. VIF for two dependent variables, ROA and foreign investor ratio.

Table 3 introduces four models to assess whether the independent director contributes to the firm’s financial performance. This part of the analysis tests agency theory, which proposes a positive correlation between independent directors and firms’ financial performance. The results show insignificant coefficients for both types of firm financial performance (ROA and ROI). Therefore, agency theory has no support, except marginally significant (p < .10) in Model 3 on ROI financial performance. Therefore, incentives other than technical motives justify the hiring of independent directors.

Independent Directors Affecting Performance.

Note. Dependent variables: ROA & ROI. Standard error in parentheses.

p < .05. **p < .01. ***p < .001. †p < .1.

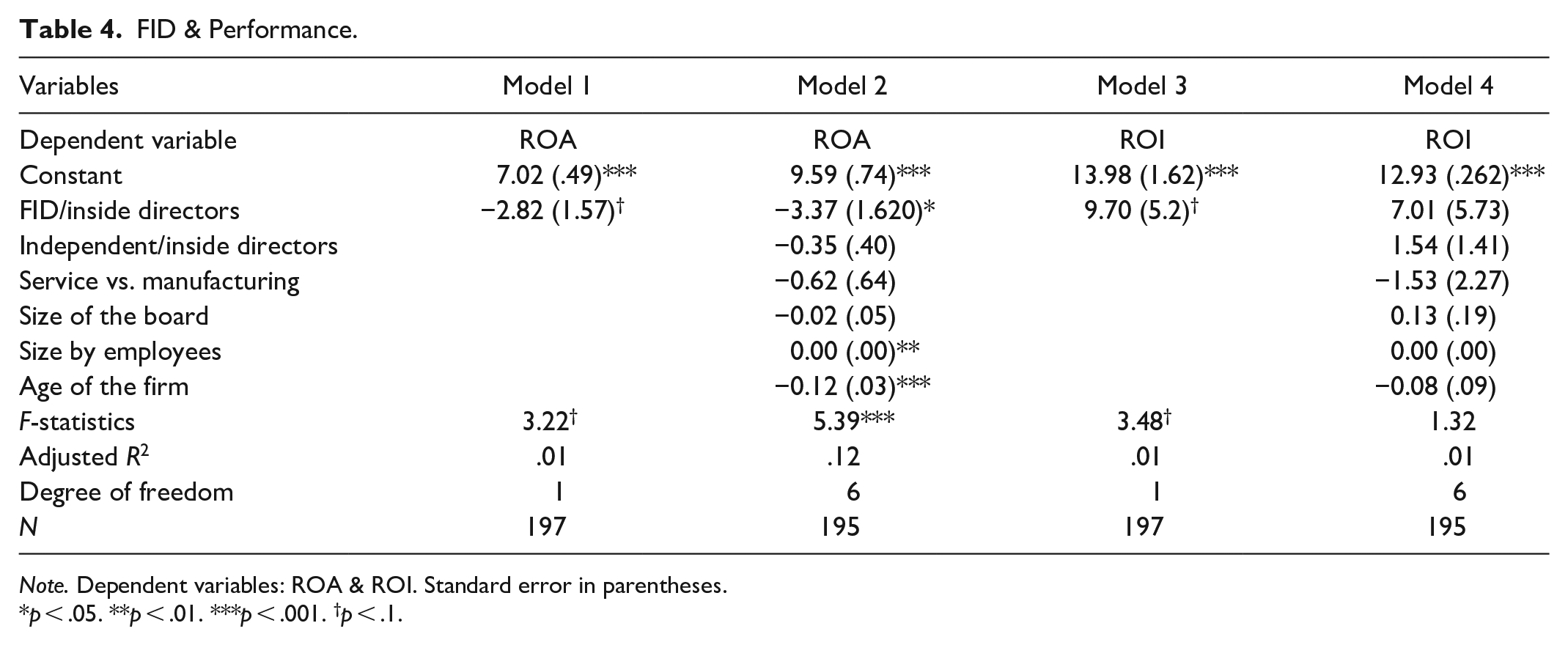

Table 4 shows FID and the firm’s financial performance compared to both types (DID and FID). After controlling for other changes, we see similar results between Tables 3 and 4. The FID/inside ratio shows a marginally significant (p < .10) correlation with the ROI.

FID & Performance.

Note. Dependent variables: ROA & ROI. Standard error in parentheses.

p < .05. **p < .01. ***p < .001. †p < .1.

Table 5 shows the reverse hypothesis and its result: Does a firm’s low financial performance trigger hiring independent directors? Agency theory suggests an affirmative answer. Model 2 shows support for a firm’s declining financial performance and hiring of FIDs in ROA in Model 2. Furthermore, it appears that service firms have higher numbers of FIDs when their financial performance increases and manufacturing firms have higher numbers of FIDs when their financial performance decreases in Model 4 (ROI). These mixed results lead us to the main result.

Firm Performance & FID Hiring.

Note. Dependent variable = ratio of foreign directors. Independent variables = ROA and ROI. Standard error in parentheses.

p < .05. **p < .01. ***p < .001. †p < .1.

Table 6 answers the question of whether hiring an FID attracts foreign investors. After controlling for other variables, the positive and significant correlation between FID and foreign investors supports our proposition that the symbolic value of FID attracts foreign investors to Chinese firms. The increase in the ratio of FID/Chinese directors also increases foreign investment. Thus, the results indicate legitimacy and thus the attention of a related audience of the firm.

The FID Hiring & Foreign Investors.

Note. The dependent variable = Ratio between foreign and Chinese investors. Standard error in parentheses.

p < .05. **p < .01. ***p < .001. †p < .1.

Discussion

We posed an outstanding question in the management literature on whether the increase in FID on the board indeed contributes to the firm’s financial performance. Using agency theory, we developed three hypotheses. Hypothesis 1 predicted that DID on the firm’s board positively correlates with the firm’s financial performance. Hypothesis 2 predicted that the FID on the firm’s board positively correlates with the firm’s financial performance. Hypothesis 3 predicted that the FID on the firm’s board positively correlates with foreign investors of the firm. We used the data from the top 200 Chinese firms. The results in Table 6 show that the FID does not affect the financial performance of the firm. Nor does the decline in financial performance trigger the appointment of FIDs. In other words, the foreign director’s appointment on the board of the Chinese firm is neither a cause nor an effect of the firm’s financial performance.

The domestic independent director does not affect the ROA or ROI of the firm. Likewise, foreign independent directors do not affect the ROA or ROI of the firm. Then, we tested whether FIDs attract foreign investments. The DID does not affect the firm’s foreign investment. However, the FID shows a consistent and strong positive effect on foreign investment. The correlation between foreign investment and FID goes both ways: high foreign investment attracts FID appointments, and a high ratio of FID attracts foreign investors. We focused on the latter in the study design. The result is clear and concrete in partial support of the theory. Without evidence of the financial performance of the firm, agency theory lacks technical rationality. An alternative reason must exist for trends in FID appointments, and institutional theory can offer a plausible explanation. While agency theory restricted to the firm’s financial performance has failed to produce expected results, the institutional theory of conformance comes to the fore to explain the positive correlation between FID and foreign investors.

This study contributes to the literature at the field level, theoretical level, and policy level. At the field level, the phenomenon of globalization of boards merited analysis for its antecedent and consequential factors. The phenomenon of FID and a firm’s effectiveness in providing shareholder value has dominated the literature in recent years. The extant research either promulgates the diffusion of FIDs on globalized businesses (Lublin, 2005) or draws various patterns of the globalization of boards (Davis, 2014). In other cases, it draws discrepancies between the rise in FIDs without financial implications because of the lack of engagement (Chizema & Kim, 2010; Cho & Kim, 2007; Peng, 2004). Some authors turn to the annual meetings and engagement of FIDs to explain the lack of performance, claiming that FIDs do not attend meetings of the firm (Masulis et al., 2012). Others go a step further, claiming that FIDs reduce board meeting frequency (Hahn & Lasfer, 2016). Yes, some others claim a positive and strong role of the FID in a firm’s financial performance (Oxelheim & Randøy, 2003). Our study resolves part of this issue and answers some of the outstanding questions about the field.

Theoretically, we contribute to the institutional explanation for the rise in FIDs as a concept of conformance rather than a concept of performance associated with agency theory. Similar to previous research on FIDs and institutional explanation, we locate our findings on the institutional side of the argument, supporting the conformance argument. The previous literature builds on the foreign director’s link to the legitimacy of firms, explaining that the isomorphism perspective explains the FID’s role more than the functional role (Peng, 2004). Another study claims inconsistent patterns in a firm’s financial performance and associates this variation with national institutions (Miletkov et al., 2017). These studies imply that firms conform to the standards and norms of leading global firms’ structures and practices to appear legitimate (DiMaggio & Powell, 1983). Our study empirically confirms this assumption by showing the absence of a correlation between the FID and financial performance and the correlation between the FID and foreign investors. Thus, we make an incremental theoretical contribution to the literature in the management field.

Empirically, several studies indirectly support our claim that the FID attracts foreign investment to the firm in line with the logic of institutional theory. A study in Russia supports the FID’s contribution to the firm’s financial performance (Buck & Shahrim, 2005). In Korea, independent directors predict investment responses by foreign investors. Our study shows that although FIDs make up approximately 13% to 18% of global firm governance (Davis, 2014), the conformance logic explains the absence of the financial performance logic (Masulis et al., 2012). In line with the inter-country differences, the DID attracts foreign investment in Korea (Cho & Kim, 2007); the FIDs attract foreign investors even more in China in our study. Therefore, we add the empirical dimension to the contribution.

For policy-level contributions, an FID increases the visibility of Chinese firms for the global audience. The global audience interprets these signals as adaptive trends to global standards. For instance, foreign investors face information asymmetries, and FIDs reduce some of the investment uncertainty of foreign investors. Likewise, Chinese firms benefit more than they contribute to foreign directors. Notably, in the BRI (belt and road initiative) case, Chinese firms need legitimacy, and the FID complements this purpose for legitimacy among BRI member countries (Malik, 2020a). According to the Chinese Ministry of Commerce, Chinese outward FDI has decreased, and inward FDI has increased. Foreign investment increased by 7.5%.

Moreover, a trend from a global to a regional focus of the flow of investment to China is likely after China initiated the RCEP (Regional Comprehensive Economic Partnership) with 14 Asia-Pacific countries. It is the world’s largest trade agreement, and it excludes India and the USA. China has also legitimized its position among stable countries by effectively managing the COVID-19 pandemic. Therefore, we expect an increase in the interest of foreign investors.

Our study also has limitations. First, the sample size represents 20% of the 2,000 listed Chinese firms. Increasing the sample to more than 50% of the listed firms may strengthen the empirical part of the study. Second, the study lacks demographic attributes, such as the experiences, ages, nationalities, and board meeting attendance, of FIDs or DIDs (Nowland & Simon, 2018). Third, the data lack information on European investors, such as whether a Canadian director attracts a Canadian investor or a non-Canadian investor to a Chinese firm. Fourth, the Chinese governance system differs from other countries because of institutional diversity (Malik & Huo, 2019). Fifth, the time lag requirement between the appointment of the FID and the response of the foreign investor raises another issue, demanding a longitudinal study design.

Institutional theory explains why the appointment of independent directors takes place when there is no systemic link between independent directors and the firm’s financial performance (Chizema & Kim, 2010; Cho & Kim, 2007; Peng, 2004). Institutional theory explains this irrational behavior by building on social rationality to justify the appointment of independent directors. The concept of social rationality implies that social norms influence strategic organizational decisions. For instance, firms hire independent directors because industrial leaders have implemented such practices, which become appropriate behavior (DiMaggio & Powell, 1983). The legitimacy of a firm’s stakeholders is gained by following appropriate and normative rules in the industry. In this sense, the hiring of independent directors appears to be a memetic phenomenon rather than a technical phenomenon because it shows an unclear link between hiring independent directors and the firm’s financial performance (Ahmadjian & Robbins, 2005; Dalton et al., 1998; Payne et al., 2009).

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.