Abstract

This study examines the complex interaction between Financial Development (FD) and Economic Growth (EG) in Algeria from 1980 to 2020 using nonlinear modeling techniques. We apply the Non-Linear Causality test with Transfer Entropy, a novel method in this literature, to confirm the nonlinear causality from FD to EG. We also use the Nonlinear Autoregressive Distributed Lag (NARDL) model and the Cumulative Dynamic Multiplier (CDM) to establish the long-run equilibrium and the short-run dynamic relationship between FD and EG. The NARDL results support the Transfer Entropy findings and show that FD has a symmetric impact on EG in both the short and long term. Positive and negative shocks on FD affect EG similarly and the imbalance is corrected in about 6 years. This study provides useful information for policymakers and stakeholders to design policies that promote (EG) and development in Algeria by enhancing FD and mitigating shocks.

Plain Language Summary

We wanted to know how the financial sector and the economy affect each other in Algeria over the past 40 years. We used new and advanced methods to analyze the data. We found that the financial sector and the economy have a one-way relationship that is stable in the long run but can change in the short run due to shocks. We also found that the financial sector and the economy adjust to each other in about 6 years after a shock. Our study can help policymakers and stakeholders improve the financial sector and the economy in Algeria.

Keywords

Introduction

Background

The intricate interplay between financial development (FD) and economic growth (EG) has aroused considerable curiosity among researchers and policymakers. (FD) entails augmenting the efficiency and stability of the financial system, which facilitates the mobilization and allocation of resources for productive endeavors. (EG) denotes the persistent increase in the output and income of a country over time. Theoretically, (FD) can foster (EG) by proffering better financial services, alleviating information asymmetry and transaction costs, spurring innovation and entrepreneurship, and attenuating macroeconomic fluctuations. Empirically, however, the evidence on the causal nexus between (FD) and (EG) is nebulous and context-dependent, fluctuating across countries, time periods, and methodologies. Algeria’s economy faces challenges in achieving diversification, higher growth, and development outcomes. Understanding drivers of growth like FD is crucial for effective policy. However, past studies on Algeria using linear techniques have limitations.

Research Gap

Haibo et al. (2023) have found a two-way causality between FD and EG in Western, Central, Eastern, and Southern African countries and one way causality in Northern Africa. Nawaz et al. (2019) have found mutual causality between FD and EG in Pakistan. Allaoui et al. (2015) have discussed the challenges of Algeria in attaining higher levels of development and diversifying its economy beyond oil exports. Boulila et al. (2018) have analyzed the impact of monetary and fiscal policies on EG and environmental quality in Algeria. Algeria implemented structural reforms and debt-dependent development strategies based on the hydrocarbons sector after signing the structural adjustment agreement with the IMF and the World Bank in 1994. Since 2002, Algeria adopted a new policy of development with more economic liberalization and monetary and fiscal policies to reduce its dependence on hydrocarbons and diversify its income sources. Monetary policy was introduced by the Money and Loan Act, while fiscal policy was expansionary to boost growth, lower unemployment and protect the environment. These policies were applied in five programs from 2000 to 2019, aiming to stimulate national institutions, market demand, infrastructure, production diversification and green growth (Boulila et al., 2018). Algeria’s financial sector has undergone transformations over time, and it has engendered some positive repercussions on the country’s (EG) during the period 2005 to 2014. We can discern these repercussions in the banking sector, which has expanded in size and has conferred more credit to the private sector as a proportion of GDP. This evinces that banks play a pivotal role in financing private sector activity. Although there have been some enhancements in (FD) indicators, they remain insufficient compared to the changes and developments witnessed in the financial systems of other countries. The study by Haguiga and Amani (2019) scrutinizes how financial sector development and (EG) are correlated in Algeria during the period 2005 to 2014. The study utilizes data from 13 Algerian commercial banks and applies some sophisticated statistical methods. The results demonstrate that financial sector development has a positive impact on Algeria’s (EG) during the study period. This impact is conspicuous in the banking sector, which has increased both its assets and its lending to the private sector relative to GDP. This shows that banks facilitate the economy’s growth by financing private sector activity. Our paper investigates how (FD) and (EG) are intertwined in Algeria, a country that relies heavily on oil exports. Algeria has experienced momentous changes in its economic and financial situation since the 1980s, owing to the plummeting of oil prices, the implementation of structural adjustment programs, the liberalization of trade and capital flows, and the political and social turbulence.

Most existing studies on Algeria have utilized linear models that cannot fully capture potential nonlinearities and asymmetries between FD and EG. The motivation is to employ more flexible nonlinear methods like Transfer Entropy and NARDL to uncover nuances missed by linear frameworks.

No prior study has examined Algeria using Transfer Entropy, a technique well-suited for detecting nonlinear causal relationships between complex systems like FD and EG. The motivation is to provide new evidence on the nexus using this novel approach.

The mixed results in the literature suggest the FD-EG relationship is highly context-specific. The motivation is to provide new country-specific evidence for Algeria, where the nexus has been under-examined compared to other regions.

The study utilizes a new IMF FD index to capture multiple dimensions of FD, unlike most studies that use narrow proxies like credit or money.

This study aims to examine the finance-growth nexus in Algeria using nonlinear time series methods new to this context—transfer entropy and the nonlinear ARDL (NARDL) model. Transfer entropy can uncover hidden causal relationships missed by linear Granger causality. NARDL can assess asymmetry and dynamics missed by linear ARDL. This study also utilizes a new IMF FD index to capture multiple dimensions of FD.

Research Objectives

RQ1: To determine the direction of causality between financial development (FD) and economic growth (EG) in Algeria.

RQ2: To examine the long-run equilibrium relationship between FD and EG in Algeria.

RQ3: To analyze the short-run dynamics between FD and EG in Algeria.

RQ4: To assess whether FD has a symmetric or asymmetric impact on EG in Algeria.

Contributions

This study makes several key contributions relative to recent advancements in the literature:

It provides the first application of transfer entropy to ascertain whether (FD) causes (EG) or vice versa, or whether they both influence each other. As far as we know, no previous studies have examined the causal relationship between FD and EG using Transfer Entropy, a method that can detect non-linear causality demonstrating its advantages over linear Granger causality used in influential studies in Algeria like (Hamza & Nassima, 2022).

It employs the NARDL technique to uncover hidden asymmetries and dynamics missed by conventional linear ARDL models widely utilized by authors in Algeria studies like (Bakhouche, 2007).

It utilizes a new multidimensional IMF FD index employed by Svirydzenka (2016) and Sahay et al. (2015), improving on narrow proxies employed in previous studies on Algeria, for example: Lacheheb et al. (2013) used Broad money as a proxy for FD in Algeria.

The paper also accounts for other variables that may impinge on (EG), such as trade openness, inflation, government expenditure, and foreign direct investment.

The most critical outcomes noted in this study are that, first, FD cause EG in Algeria in non-linear way. Second, FD has a symmetric impact on EG. Therefore, Positive and negative shocks on FD affect EG similarly and the imbalance is corrected in about 6 years.

In summary, this study brings modern nonlinear time series analysis tools to an important empirical context where their application has been limited. It demonstrates the advantages of techniques like transfer entropy and NARDL in shedding new light on the complex finance-growth nexus in Algeria.

Structure

The paper is structured as follows: Section 2 reviews past theoretical and empirical literature. Section 3 discusses the data. Section 4 describes the methodology. Section 5 presents results and discussion. Section 6 concludes with policy implications.

Literature Review

The relationship between (FD) and (EG) remains an active area of research, with the literature presenting a diverse range of findings. While some studies have identified a positive association between FD and EG, others have found no association or even a negative association. Furthermore, some studies have detected a non-linear relationship between these variables. This section endeavors to provide a thorough synopsis of the various studies on the subject, elucidating their key findings.

Numerous studies have consistently shown a positive correlation between (FD) and (EG). For instance, Al Khatib et al. (2023) found that FD in Egypt is jointly influenced by the inflation rate, EG, exchange rate, and trade openness. Similarly, Al Khatib et al. (2022) revealed a statistically significant positive impact of FD on EG in Syria. Doran et al. (2022) demonstrated that FD has a positive effect on EG in developing countries. However, the magnitude of this influence changes with different measures of FD, estimation technique, data periodicity, and the mathematical form of the nexus, as reported by Khan and Senhadji (2003). Additionally, the majority of logical arguments and factual data support a direct and positive link between FD and EG, according to Levine (1997). Furthermore, Greenwood and Jovanovic (1990) found that financial intermediation has a positive influence on EG, while De Gregorio and Guidotti (1995) showed that the degree of FD has a positive influence on EG, except for Latin America when panel data was used.

There is strong evidence supporting the correlation between (FD) and (EG), as highlighted by Gurley and Shaw (1967), Goldsmith (1969), and McKinnon (1973), who found that a well-developed and better-functioning financial system supports faster (EG). A recent study by Rehman and Hysa (2021) investigating the impact of (FD) and remittances on (EG) across six Western Balkan countries found that (FD), as measured by the broad money stock ratio, had a positive impact on (EG). Moreover, Ibrahim and Alagidede (2020) revealed the existence of a long-run asymmetric relationship between (FD) and (EG) in Ghana, with both positive and negative shocks to (FD) exerting different long- and short-run effects on (EG). The causal bond between (FD) and (EG) in Africa was explored by Opoku et al. (2019) and they found confirmation for demand-following, supply-leading, and feedback hypotheses, suggesting a positive relation between the two variables.

The supply-leading hypothesis, proposed by Patrick (1966), suggests that (FD) leads to (EG). This hypothesis is supported by a number of studies. For instance, Al Khatib (2023) used the Non-Linear Causality test with Artificial Neural Networks to show that there is a non-linear causality from FD to EG in Syria. Similarly, Al Khatib et al. (2022) found a positive relationship between FD and EG in Syria. Islam (2022) found a linear link between FD and (EG) in the highest remittance-receiving countries. Zhang et al. (2012) found a positive association between FD and EG in China. Herwartz and Walle (2014) used data from 73 economies from 1975 to 2011 and found that the impact of finance on (EG) is typically larger in developed nations. Other studies that support the positive relationship between FD and EG include Musabeh et al. (2020), Abu-Bader and Abu-Qarn (2008), Levine (1997), Levine et al. (2000), King and Levine (1993), McKinnon (1973), and Schumpeter (1911).

Numerous studies have investigated the relationship between (FD) and (EG), with many finding evidence to support the demand-following hypothesis. According to this view, (EG) drives the demand for financial services, which in turn spurs the development of financial markets and institutions. For instance, recent research by Al Khatib (2023) showed that FD in Egypt is jointly influenced by inflation, exchange rates, trade openness, and EG. Other studies, such as Araç and KutalmışÖzcan (2014), Gennaioli et al. (2012), Bolton et al. (2011), and Goldsmith (1969), have also found support for the demand-following hypothesis. This view challenges the traditional notion that (FD) directly causes (EG). Instead, it suggests that FD is an endogenous process that responds to the needs of a growing economy. Empirical evidence further supports this claim, as financial deepening often lags behind periods of strong (EG), and financial innovation tends to follow the emergence of new investment opportunities. Therefore, policies aimed solely at promoting (FD) to drive (EG) may have limited effectiveness. Rather, a more effective approach may be to focus on boosting productivity growth, investment, and entrepreneurship, which can create the demand for financial services and accelerate (EG). By understanding the complex relationship between FD and EG, policymakers can develop more targeted and effective strategies to foster sustainable (EG).

However, the relationship between (FD) and (EG) is not straightforward, as evidenced by various studies. For instance, Cheng et al. (2021) suggested that FD negatively affects EG, particularly in developed countries, Rahman et al. (2020) utilized Markov Switching model in Pakistan and they showed that (FD) impact (EG) negatively, while Ouyang and Li (2018) found a negative impact of FD on EG in China, whereas, Gantman and Dabós (2012) found that (FD) does not have a statistically significant effect on (EG), implying that the finance-growth link is not as strong as suggested in the literature and may depend on the sample of countries and time periods considered. Conversely, Opoku et al. (2019) provided strong support for the neutrality hypothesis, indicating that (FD) and (EG) tend to evolve independently at most frequency levels. In summary, the relationship between (FD) and (EG) is complex and may vary depending on the specific context and time period.

Researchers have utilized methods like time series analysis, panel data models, VARs, and cointegration techniques to study the FD-EG nexus (e.g., Pradhan et al., 2014; Seven & Yetkiner, 2016). Several studies have utilized the non-linear autoregressive distributed lag (NARDL) model to explore the asymmetric effects of (FD) and other factors on (EG). For example, Golder et al. (2023) found that FD and remittances have an asymmetric influence on EG, with positive shocks accelerating EG while negative shocks slowing it down. Azimi (2022) analyzed the asymmetric effects of finance indicators on EG in China using NARDL, revealing a significant long-run relationship between finance and EG, with capital and money market indicators affecting EG differently in both short and long runs. Likewise, Zungu (2022) presented evidence of a nonlinear relationship between FD and EG in a group of African economies, while Mei et al. (2022) demonstrated that internet finance and rural finance contribute to rural EG in China. However, Arcand et al. (2015) have argued that there may be a “too much finance effect,” while Ductor and Grechyna (2013) suggested that there is a nonlinear relationship between FD and EG.

Moreover, some studies have found a U-shaped or inverted U-shaped nonlinear relationship between (FD) and (EG). For instance, Krinichanskii (2022) identified six mechanisms that cause the nonlinearity of the finance-growth relationship and revealed the properties of this nonlinearity in an empirical analysis of 43 OECD countries from 1990 to 2019. Bahri et al. (2018) found that (FD) accelerates (EG) after reaching a turning point, while Bahri et al. (2019) showed that FD accelerates growth after a certain level of (FD) is reached.

These findings suggest that the relationship between (FD) and (EG) is complex and may vary depending on the specific context and time period. Ang (2008) emphasized that the functional form of the finance-growth relationship is crucial for understanding its nature and implications, as a linear model may not capture the regime-switching behavior of this relationship. Furthermore, recent studies by Arcand et al. (2015) and Cechetti and Kharroubi (2012) have shown that excessive liquidity without proper control and supervision could lead to the “finance curse” or the “too much finance harm growth” propositions, resulting in a negative impact on (EG) beyond a certain threshold point. This phenomenon was attributed to the inefficiency of the derivative market, where financial flows were not directed to productive uses. Therefore, policy makers need to consider the threshold point when regulating the level of financial expansion, and a reliable and valid measurement of the nonlinearity of the finance-growth relationship is essential for addressing specific issues and monitoring the activities of financial intermediaries. Additionally, factors such as corruption, weak rule enforcement, and political interference can also lead to the nonlinearity of the finance-growth relationship, as they divert financial resources to unproductive or wasteful activities (Law et al., 2017). The contradictory conclusions may arise because the impact of FD depends on factors like the level of economic development, quality of institutions, and macroeconomic environment (Law et al., 2017). The relationship may also be nonlinear, regime-switching, or time-varying.

This review examines studies that have investigated the relationship between (FD) and (EG). The findings are diverse and sometimes conflicting, suggesting that the relationship between FD and EG is multifaceted and contingent on various factors. While some studies report a positive correlation between FD and EG, others find no association or even a negative link. Moreover, the direction of causality is uncertain, with some studies proposing that growth drives FD while others argue the opposite. The nature of the relationship between FD and EG may depend on the specific indicators used to measure each variable, as well as on the level of economic development. Some studies suggest that the relationship between FD and EG is not linear, and that the effect of FD on growth may be context-specific. This implies that the connection between the two variables may be more complex than previously assumed.

Overall, the reviewed studies suggest that the nexus between FD and EG is intricate and context-dependent. Further research is needed to comprehend the underlying mechanisms that shape this nexus and to identify the specific circumstances under which FD is most likely to enhance EG. Therefore, the nexus between FD and EG is not only complex but also dynamic, requiring continuous investigation and analysis. However, existing studies suffer from limitations like using narrow proxies for multidimensional FD, ignoring nonlinearities, and relying on restricted samples. The nexus remains underexplored in the context of specific countries like Algeria. This study addresses gaps by applying novel nonlinear techniques like Transfer Entropy and NARDL to uncover hidden dynamics between FD and EG using a new IMF FD index for Algeria.

Data

This study utilizes annual time series data over the period 1980 to 2020 to empirically analyze the relationship between FD and EG in Algeria. The data is obtained from two reputable international databases—the World Development Indicators (WDI) compiled by the World Bank, and the Financial Development Database published by the International Monetary Fund (IMF).

The World Bank adheres to rigorous standards for data collection, validation, and quality control. Any data limitations are clearly documented. Similarly, the IMF follows a robust framework to ensure data integrity and accuracy. The variables have no missing observations for the full sample period.

The span from 1980 to 2020 enables studying long-run cointegrating relationships between the variables, as it captures major structural changes in Algeria including oil crises, reforms, and external shocks. However, higher frequency cycles may be missed given the annual data. While sufficient for the current analysis, future research could examine higher frequency dynamics using more granular data.

The dependent variable is GDP per capita representing EG, commonly used in past literature. The key independent variable is the IMF FD Index, which provides a multidimensional measure capturing depth, access, and efficiency facets. This improves on studies relying on narrow proxies like credit or money.

Control variables are included based on standard growth models and past empirical studies. Their inclusion accounts for other factors impacting EG.

The variables and data sources used in the study are shown in Table 1.

The Variables and Data Sources Used in the Study.

Methodology

This section presents the empirical methodology utilized to analyze the relationship between FD and EG in Algeria.

This study aims to examine the following key research questions regarding the relationship between (FD) and (EG) in Algeria:

Is there a causal relationship between FD and EG in Algeria, and what is the direction of causality?

What is the long-run equilibrium relationship between FD and EG in Algeria?

What are the short-run dynamics between FD and EG in response to shocks?

Does FD have a symmetric or asymmetric impact on EG in Algeria?

To address these questions, the following models and techniques are utilized:

The nonlinear causality test using transfer entropy analysis is applied to determine causality and its direction between FD and EG (research question 1).

The ARDL bounds testing approach is used to establish cointegration between the variables (pre-condition for research questions 2–4).

The NARDL model estimates the long-run equilibrium relationship between FD and EG (research question 2).

The NARDL-ECM estimates the short-run dynamics between FD and EG after shocks (research question 3).

Symmetry tests of the NARDL model examine if FD has a symmetric or asymmetric impact on EG (research question 4).

The study uses Eviews13 program and R Studio to perform data analysis and implement a unit root test in the presence of structural changes, followed by the non-linear causality test (using Transfer entropy analysis) to determine whether the relationship is linear or not, and to determine the direction of this relationship. After verifying a one-way non-linear link from FD to EG, the conditions for the Cointegration test Using the (NARDL) were satisfied. This model helped to examine the impact of FD and some control variables on EG in Algeria. Moreover, an Unrestricted Error Correction Model (UECM) will examine the short-term dynamics of the link.

Some processes may exhibit asymptotic, exponential, or periodic behavior that cannot be captured by a linear model. Nonlinear models can also incorporate more parameters and interactions, which can improve the accuracy and flexibility of the model. some of the advantages of nonlinear models include predictability, parsimony, and interpretability.

Unit Root Tests

The Perron and Vogelsang (1992) test with structural breaks is applied to test the stationarity properties of the variables. This identifies potential breaks and ensures the analysis is not biased by nonstationary data.

Nonlinear Causality Test

Transfer entropy, an information theory approach, is used to assess nonlinear causal relationships between FD and EG. It offers advantages over linear Granger causality for detecting complex linkages.

Transfer entropy is a measure of connectivity and causality between variables in various fields, such as industrial processes (Souza et al., 2019), cryptocurrencies (García-Medina & González Farías, 2020), financial and economic activities (Celso-Arellano et al., 2023), and nonlinear process quality diagnosis (Jiao et al., 2021). It is an information theory measure that identifies and quantifies linear or non-linear directional relationships between two variables. Transfer entropy can estimate the connectivity map of two systems and help identify the root cause of faults. It can also select variables for high dimensional predictive models and predict the co-movement of time series. Transfer entropy is comparable to Granger causality and can confirm directionality more reliably. The RTransferEntropy package in R provides functions for calculating transfer entropy and information flow between time series. Transfer entropy is a measure of the directional influence of one time series on another, based on information theory. It can test for causality or identify the drivers and targets of a complex system. Some advantages of transfer entropy over other methods are:

Non-parametric: It does not require any assumption about the distribution or the functional form of the data. This makes it more robust and flexible than parametric methods, such as Granger causality, that may fail to capture non-linear or non-Gaussian relationships.

Directional: It can measure the amount and the direction of information flow between two time series. This can help identify causal or driving influences, as opposed to mere correlations or feedback loops.

Model-free: It does not require any explicit model of the interactions between the time series. This makes it more suitable for analyzing complex systems, such as the brain, where the underlying mechanisms are often unknown or difficult to specify.

Information-theoretic: It has a clear and intuitive interpretation in terms of uncertainty reduction. Transfer entropy measures how much knowing the past values of one time series reduces the uncertainty about the future values of another time series.

Transfer entropy analysis is a method to measure the direction and strength of information flow between two variables, such as economic policy uncertainty (EPU), investor sentiment and stock market. Transfer entropy is based on the concept of conditional mutual information, which quantifies how much knowing the past values of one variable reduces the uncertainty about another variable, given the past values of the first variable. Transfer entropy can capture non-linear and asymmetric relationships between variables, unlike other methods such as Granger causality.

To perform transfer entropy analysis using the RTransferEntropy package in R, we need to specify the following parameters:

lx and ly: The maximum lags for the dependent and independent variables.

bins: The number of bins for discretizing the continuous variables.

nboot: The number of bootstrap replications for estimating the standard errors and p-values of the transfer entropy estimates.

Cointegration Analysis

The ARDL bounds testing method checks for a long-run relationship between the variables. This is a precondition for using the NARDL model.

NARDL Model

The NARDL (Nonlinear Autoregressive Distributed Lag) model proposed by Shin et al.(2014) is a more robust approach than the ARDL model for cointegration analysis. Unlike the ARDL model, which assumes linearity and symmetry in the relationship between variables, the NARDL model integrates non-symmetrical analysis with the ARDL approach, allowing for the detection of hidden cointegration and avoiding arbitrary assumptions of linearity and intangible relationships. The NARDL model can provide results in both the short and long term in a single equation, separate short-term effects from long-term effects, and determine the integrated relationship between the dependent and independent variables.

The NARDL model estimates asymmetric long-run and short-run relationships. It captures hidden nonlinearities in how FD and EG are connected in Algeria.

Diagnostic Tests

Residual diagnostics, stability tests like CUSUM and CUSUM-SQ, and model specification checks ensure the validity and reliability of the NARDL model before drawing inferences.

Robustness Checks

The symmetry test of NARDL model is a way of testing whether the long-term and short-term impacts of the independent variables are symmetric or asymmetric. Symmetry implies that positive and negative changes in the independent variables have the same magnitude and opposite sign effects on the dependent variable. Asymmetry implies that positive and negative changes have different magnitude and/or sign effects.

The NARDL model utilizes the cumulative dynamic multiplier (CDM) to assess the overall impact of a modification in an explanatory variable on the dependent variable over time. The CDM can take on positive or negative values depending on the direction of the change in the explanatory variable. It can also capture asymmetric effects of positive and negative changes, reflecting differences in the magnitude of the impact on the dependent variable. For example, if a positive change in X has a larger impact on Y than a negative change of the same magnitude, then the CDM will be larger for positive adjustments than for negative ones.

The CDM is computed by summing up the coefficients of the lagged terms of X in the NARDL model, as proposed by Shin et al. (2014). This provides a robustness check for the NARDL model, as it allows for the assessment of the overall impact of each explanatory variable on the dependent variable, taking into account both short- and long-term effects. The CDM can be particularly useful for identifying the most influential variables in the model and for assessing the sensitivity of the results to different specifications and assumptions. Symmetry tests examine long-run and short-run symmetry of impacts. Cumulative dynamic multipliers assess the trajectory of responses over time.

Model Assumptions and Limitations

This study employs two nonlinear time series models—transfer entropy and the NARDL framework—to analyze the nexus between FD and EG. As with any modeling approach, certain assumptions are made which should be noted.

The transfer entropy technique is flexible as it makes minimal assumptions about underlying data distributions or functional forms. This nonparametric nature provides robustness in identifying nonlinear linkages. However, the binning and smoothing parameters can influence results. Best practices are followed to optimize parameter configuration.

The NARDL model assumes cointegrating relationships exist and variables are integrated of order 0 or 1 based on unit root tests. subject to two conditions: the dependent variable is stationary after first differencing, and there is no second-order integrated time series in the model. Nonetheless, other integration orders cannot be definitively ruled out. The model requires a minimum sample size of 30 to comply with the critical values of Narayan (2005), which is met in the present study. The model is also premised on correct specification, though alternatives are possible. Diagnostic testing provides adequate reassurance.

Both models posit no major structural changes occurred within the sample period. The dummy variable for potential breaks offers partial mitigation but does not fully capture regime changes. Additionally, endogeneity and reverse causation are not accounted for given the complexity of incorporating such dynamics within nonlinear frameworks.

To enhance robustness, consistency between the transfer entropy and NARDL results is leveraged by utilizing two complementary techniques. Future research could conduct sensitivity analyses using different model parameters or alternate nonlinear specifications.

Causality Versus Correlation

There are difficulties in empirically establishing definitive causal relationships between FD and EG, as opposed to merely observing correlations. This study relies on time series analysis and statistical tests like transfer entropy to ascertain predictive relationships suggestive of causality. However, the findings have limitations in proving strict causation.

The models currently used cannot account for all potential confounding factors or fully tackle issues like endogeneity and dual causality. Controlling for more variables and using bespoke structural models tailored to Algeria could better address these concerns. But data constraints preclude such analyses presently.

Ultimately, true causality can only be determined through randomized experiments or well-identified models customized to the specific institutional context. The simplified empirical frameworks employed currently have restricted capacity to make definitive causal claims. Correlation does not necessarily imply causation, and the results may potentially be influenced by omitted variable bias.

Given these inherent limitations, the analysis is only able to identify plausible predictive relationships between FD and EG in Algeria. However, the findings cannot conclusively establish causal links. This inability to firmly determine causality versus correlation is explicitly acknowledged as a caveat when interpreting the results. The relationships observed should be characterized as suggestive associations rather than causal effects. Further research using more granular data and institutional details is needed to make stronger causal inferences.

Results and Discussion

Descriptive Statistics

In Table 2, we can find the descriptive statistics related to six variables that have an impact on Algeira’s economy: GDPPC, EXPOFGDP, FDI, TO, INF, and FD, which provide valuable insight into Algeria’s economic performance and structure. Descriptive statistics for each variable can be found in the given table.

Descriptive Statistics for the Study Variables During the Period 1980 to 2020.

Table 2 can help us interpret the characteristics of the six variables and their implications for Algeria’s economy. For example, the variable GDPPC has a mean value of 7.32, indicating that Algeria has a lower-middle income level according to World Bank classifications. The variable FDI has a high standard deviation and skewness, indicating that Algeria experienced a large variation and asymmetry in foreign direct investment inflows, meaning that it faced challenges in attracting and retaining foreign investors. The variable TO has a low mean value, indicating that Algeria has a low trade openness ratio, meaning that it has limited integration with global markets. The variable INF has a high kurtosis and Jarque-Bera value, indicating that Algeria had a highly peaked and non-normal inflation rate distribution, meaning that it suffered from inflationary shocks and instability. The variable FD has a low mean and maximum value, indicating that Algeria has a low level of (FD), meaning that it has limited access to financial services and intermediation.

Nonlinear Causality Analysis

The transfer entropy analysis aims to test whether there is a directional information flow between FD and GDPPC in the long-run and short-run. The data consists of two variables: FD (financial development) and GDPPC (real GDP per capita in US dollars). The data has 41 observations from 1980 to 2020, with no missing values.

The results of Table 3 show that:

The transfer entropy from FD to GDPPC is 0.1724, which means that knowing the past values of FD reduces the uncertainty about the future values of GDPPC by 0.1724 bits. The effective transfer entropy, which is adjusted for autocorrelation, is .1004. The standard error of the transfer entropy estimate is .0653, and the p-value is .0867, which means that there is weak evidence to reject the null hypothesis that there is no information flow from FD to GDPPC.

The transfer entropy from GDPPC to FD is 0.0669, which means that knowing the past values of GDPPC reduces the uncertainty about the future values of FD by 0.0669 bits. The effective transfer entropy, which is adjusted for autocorrelation, is .0000. The standard error of the transfer entropy estimate is .0455, and the p-value is .3013, which means that there is no evidence to reject the null hypothesis that there is no information flow from GDPPC to FD.

Transfer Entropy Analysis.

p-values: <.001***. <.01**. <.05*. <.1 “.”

The bootstrapped transfer entropy quantiles show the distribution of the transfer entropy estimates under different significance levels. For example, at the 5% significance level, the lower and upper bounds for the transfer entropy from FD to GDPPC are 0.0176 and 4.324 respectively.

The results of Table 4 show that:

Bootstrapped TE Quantiles.

Note. 10,000 replications.

There is a weak and asymmetric information flow between FD and GDPPC in the long-run, with FD having a larger influence on GDPPCC than vice versa. This suggests that (FD) may have a positive impact on (EG) in this sample period.

We conclude that non-linear causality extends from (FD) to (EG) in Algeria, which is consistent with findings of Al Khatib (2023), Golder et al. (2023), Azimi (2022), Zungu (2022), Mei et al. (2022), and Ductor and Grechyna (2013). These Studies found a Nonlinear causality from (FD) to (EG). If significant nonlinear causal effect emerges from the analysis, it could indicate that policy decisions need to be made carefully due to potential discontinuities in their effects.

Unit Root Test

Ignoring structural changes (breaks) in the timeseries could lead to false outcomes (Amsler & Lee, 1995) point out that the presence of one structural change leads to test bias. In anticipation of this, one of the unit root tests that consider the presence of structural changes will be used, which is the Perron and Vogelsang (1992) test. Table 5 shows the unit root test in the presence of structural change:

Results of Perron & Vogelsang Test.

Note. The numbers in parentheses for the ADF statistics show the lag length of the dependent variables used to obtain white noise residuals. The lag length was chosen by Schwarz information criterion. AO = additive outlier; IO = innovation outlier.

,**, and * indicate significance at the 1%, 5%, and 10% level, respectively.

Table 5 shows the results of a unit root test with structural breaks for six variables: FDI, FD, EXP of GDP, INF, TO, and GDP per Capita. Table 5 shows the result of the unit root test for each variable and each model. The outcome is derived from contrasting the DF t-statistic with some critical values that vary with the sample size and the number of breaks. If the DF t-statistic is more negative than the critical value, then the null hypothesis of a unit root is rejected and the variable is considered stationary. If not, then the null hypothesis is not rejected and the variable is considered non-stationary. Table 5 also shows the results of applying the same methods to the first differences of each variable. The first difference of a variable is the change in its value from one period to another. Table 5 indicates that all independent variables are stationary at level. The dependent variable (GDPPC) is stationary at the first difference, according to both methods and both models. The variables exhibit a combination of I(0) and I(1) stationarity levels, meeting the requirements for utilizing (NARDL) model.

Estimation of NARDL Model

The NARDL model is a statistical tool used to analyze the long-run relationship between variables. Before using the model, it is important to test for cointegration between the variables using the Wald test, which involves testing the null hypothesis of no cointegration against the alternative hypothesis of cointegration. If the null hypothesis is rejected, it indicates the presence of a cointegration relationship. The appropriate number of time lags for model variables can be determined utilizing information criterion tests such as the Akaike, Schwarz, or Hannan-Quinn tests. Once the model specification is determined, the long-run relationship between the variables can be estimated using the cointegrating model. In this case, a NARDL (2, 0, 0, 1, 1, 0) model was found to be the best model based on the Schwarz information criterion (SIC), with a maximum lag order of “2” due to the annual data.

Table 6 presents the results of the long-term bounds testing using the F-Bounds Test and T-Bounds Test.

Long-term F Bounds Test and T Bounds Test.

The F-Bounds Test is used to test the null hypothesis of no levels relationship between the variables, while the T-Bounds Test is used to test for a levels relationship between the dependent variable and a lagged value of itself. The test statistic value for the F-Bounds Test is 15.5, indicating a long-term association between the independent and dependent variables, as it is greater than the I(1) values at the 1% significance level. The test was conducted using a finite sample of size 39. The test statistic value for the T-Bounds Test is −5.13, indicating a long-term association between the dependent variable and a lagged value of itself, as it is greater in absolute value than the I(1) value at the 1% significance level.

Table 7 shows the estimation results of (NARDL) model. Table 7 can help us interpret the long-run relationship between GDPPC and the five other variables and their implications for Algeria’s economy. For example, the coefficient of EXPOFGDP is positive and significant, indicating that an increase in Total government expenditures as a percentage of GDP has a positive and significant effect on GDP per capita in the long run. which is consistent with previous studies. For instance, increased government spending can contribute to the development of infrastructure and stimulate private sector investment in the national economy, aligning with the Keynesian perspective. This approach posits that government spending has a positive impact on EG, with expansionary fiscal policy resulting in increased production, aggregate demand, and GDP. Private investment is also positively influenced by government spending, particularly in low-income countries (Ram, 1986). A study on Algeria investigated the causal link between government expenditure and (EG). The study did emphasize the vital role of government expenditure, which was around 20% of government size in 2017, and the significance of fiscal policy as the main macroeconomic policy tool in Algeria (Ayad et al., 2020). Thus, the study implies that government expenditure has a considerable role in the Algerian economy, and policymakers may have to cautiously consider the effect of any alterations in government expenditure on (EG) and GDP per capita in the long run. In other words, the positive coefficient on government spending (EXPOFGDP) aligns with Keynesian theory, whereby an increase in government expenditure raises aggregate demand and stimulates EG.

Estimation of NARDL Model (2, 0, 0, 1, 1, 0) in the Long Run.

and ** representing significance at 1% and 5%, respectively.

The coefficients of @CUMDP(FD) and @CUMDN(FD) are both positive and significant, which implies that (FD) has a positive and lasting impact on GDP per capita, regardless of whether it increases or decreases. Our finding that FD has a positive effect on EG aligns with previous studies such as Al Khatib et al. (2022), who found a similar relationship for Syria, and Doran et al. (2022), who demonstrated that FD has a positive effect on EG in developing countries.

The coefficient of TO is negative and significant, which implies that trade openness as a percentage of GDP lowers GDP per capita in the long run. The negative trade openness effect can potentially be explained by the infant industry argument, though this requires further investigation.

The negative coefficient on trade openness (TO) could indicate that greater exposure to international trade has harmed domestic industries in Algeria, thereby negatively impacting EG. This is consistent with the finding of Belloumi and Alshehry (2020) that trade openness adversely affects long-term EG in Saudi Arabia. According to Fatima et al. (2020), trade can hinder GDP growth when countries have a low level of human capital accumulation.

The coefficient of FDI is positive but small and marginally significant, indicating that an increase in foreign direct investment has a weak positive effect on GDP per capita in the long run. This is consistent with the findings of Agyei and Idan (2022), who found that foreign direct investment improves inclusive growth in Sub-Saharan Africa. Additionally, Qamri et al. (2022), have revealed that FDI improves (EG) on 21 Asian countries. However, the effect of FDI on growth may vary depending on the country and be sensitive to shocks, as suggested by a study on the impact of FDI on (EG) across 60 countries (Edwards et al., 2017).

The coefficient of INF is positive but insignificant, implying that a rise in inflation rate has no significant impact on GDP per capita in the long run. The lack of a significant impact of inflation on (EG) is consistent with the theory of Sidrauski (1967), who assumed the super-neutrality of money and found no relationship between inflation and (EG). This is also supported by the empirical work of Wai (1959), who found no evidence of a link between inflation and (EG). The findings provide important insights into the factors that influence long-run EG in Algeria.

Estimating the Relationship in the Short Term

After verifying co-integration among the study variables, the NARDL model is estimated using the unrestricted error correction model (UECM), which is displayed in Table 8. The UECM approach, called the Cointegrated Unrestricted Error Correction Model (UECM) by Pesaran et al. (2001), is based on the bounds testing approach and does not impose any restrictions on the short-run relationship. It allows for the inclusion of both long-run/short-run information, represented by the error correction coefficient and the lagged differences of the variables, respectively. The UECM model differs from the traditional ECM model, which only considers the long run. To estimate the UECM model, the-long-run-relationship according to NARDL model is first obtained. Then, the UECM model is estimated, with the UECM representing a special case of the ECM. The-short-run-relationship can be obtained through a linear transformation of the general NARDL model equation. Table 8 shows the estimation of the NARDL (2, 0, 0, 1, 1, 0) model within the framework of the UECM.

NARDL Unconditional Error Correction Regression.

,**, and * indicate significance at the 1%, 5%, and 10% level, respectively.

Table 8 can help us interpret the short-run relationship between GDPPC and the five other variables and their implications for Algeria’s economy. For example, the coefficient of COINTEQ is negative and significant, indicating that there is a long-run cointegrating relationship between GDPPC and the other variables and that GDPPC adjusts to restore this equilibrium in the short run. The adjustment speed toward the long-run equilibrium value for the EG variable is estimated to be 1.1 years, with an imbalance rate of around −0.892 in each time period. The coefficient of EXPOFGDP is positive and significant, indicating that an increase in government expenditures as a percentage of GDP has a positive and significant effect on GDP per capita in the short run. The coefficient of FDI is positive but small and marginally significant, indicating that an increase in foreign direct investment has a weak positive effect on GDP per capita in the short run. The coefficient of TO is negative and significant, indicating that an increase in trade openness has a negative and significant effect on GDP per capita in the short run. The coefficient of INF is negative but not significant. The dummy variable is negative and significant, indicating that there was a structural break in the data that had a negative and significant effect on GDP per capita. It is common for structural changes, such as economic policy, regulatory frameworks, or technological developments, to impact EG. These changes can affect the production and distribution of goods and services and the level of investment and productivity in an economy.

Using the NARDL approach, we corroborate the non-linear Transfer Entropy test results in both short and long run. These Econometrics techniques lend credence to the hypothesis that FD is a key driver of EG, as proposed by Patrick (1966). Our findings indicate that FD causes and enhances EG, consistent with the notion that “more financing leads to more growth” (Levine, 2003). FD is an essential condition for EG, which conforms to the theory of “finance-led-growth.” Our results are in line with prior studies by Al Khatib (2023), Al Khatib et al. (2022), Islam et al. (2022), Musabeh (2020), Herwartz and Walle (2014), Zhang et al. (2012), Abu-Bader and Abu-Qarn (2008), Levine (1997, 2000), King and Levine (1993), McKinnon (1973), and Schumpeter (1911). These studies also support the supply-leading hypothesis. (FD) is regarded as a source of (EG). Our results challenge the hypothesis that “too much finance harms EG.”

Diagnostic Tests for Residuals of the Model

This Table 9 shows the diagnostic tests for the residuals of the NARDL (2, 0, 0, 1, 1, 0). The diagnostic tests are used to check the validity and reliability of the model by examining whether the residuals satisfy some desirable properties. Table 9 includes the following tests and their results:

Normality test (Jarque-Bera): The null hypothesis is that the residuals are normally distributed. The test statistic is the Jarque-Bera statistic, which is based on the skewness and kurtosis of the residuals. The p-value is the probability of obtaining a Jarque-Bera statistic as high or higher than the observed one, if the null hypothesis is true. A high p-value (usually more than .05) means that we cannot reject the null hypothesis and conclude that the residuals are normally distributed. In this case, the p-value is .74, which indicates that the residuals are normally distributed (Bera & Jarque, 1981).

Breusch-Godfrey Serial Correlation (LM test): This test examines whether the residuals are serially correlated or not. The null hypothesis is that there is no serial correlation in the residuals. The test statistic is either the F-statistic or the ObsR2 statistic, which are based on a regression of the residuals on their lagged values and other explanatory variables. The p-value is the probability of obtaining an F-statistic or an ObsR2 statistic as high or higher than the observed one, if the null hypothesis is true. A high p-value (usually more than .05) means that we cannot reject the null hypothesis and conclude that there is no serial correlation in the residuals. In this case, both p-values are .99, which indicates that there is no serial correlation in the residuals (Breusch, 1978).

ARCH (heteroskedasticity test): This test examines whether the residuals are heteroskedastic or not. Heteroskedasticity means that the variance of the residuals, changes over time. The null hypothesis is that there is no heteroskedasticity in the residuals. The test statistic is either the F-statistic or the ObsR2 statistic, which are based on a regression of the squared residuals on their lagged values and other explanatory variables. The p-value is the probability of obtaining an F-statistic or an ObsR2 statistic as high or higher than the observed one, if the null hypothesis is true. A high p-value (usually more than .05) means that we cannot reject the null hypothesis and conclude that there is no heteroskedasticity in the residuals. In this case, both p-values are more than .7, which indicates that there is no heteroskedasticity in the residuals (Engle, 1979).

Ramsey RESET test: This test examines whether the model has any omitted variables or functional form misspecification. The null hypothesis is that the model is correctly specified. The test statistic is either the F-statistic or the t-statistic, which are based on a regression of the dependent variable on its fitted values and their powers. The p-value is the probability of obtaining an F-statistic or a t-statistic as high or higher than the observed one, if the null hypothesis is true. A high p-value (usually more than .05) means that we cannot reject the null hypothesis and conclude that the model is correctly specified. In this case, both p-values are more than .4, which indicates that the model is correctly specified (Ramsey, 1969).

Diagnostic Tests for Residuals of the NARDL (2, 0, 0, 1, 1, 0) Model.

Table 9 shows that all diagnostic tests pass with high p-values, indicating that the NARDL model has valid and reliable residuals that satisfy normality, no serial correlation, no heteroskedasticity, and correct specification.

Figure 1 revealed that the graphs of both tests remained within the critical lines at a significance level of 5%, indicating that the coefficients are stable over time (Brown et al., 1975). Nevertheless, our model exhibits no econometric issues and is therefore suitable for further analysis.

CUSUM and CUSUM-SQ tests.

Robustness Check With Symmetry Test and the Cumulative Dynamic Multiplier (CDM)

Table 10 shows the results of testing the null hypothesis of long-run symmetry between FD and EG using the NARDL (2, 0, 0, 1, 1, 0) model. Both the F-statistic and the χ2 statistic have p-values greater than .05 (.8872 and .8861, respectively), which means that we cannot reject the null hypothesis and conclude that there is no long-run asymmetry between FD and EG in the NARDL model. This result is inconsistent with the findings of Chen et al. (2020), who reported an asymmetric relationship between growth and finance in Kenya. This result also differs from the findings of Kassi et al. (2023), who found asymmetric impacts of FD on EG in 14 out of 21 Sub-Saharan African countries in the long term.

Symmetry Test NARDL (2, 0, 0, 1, 1, 0) Model in Long-Run.

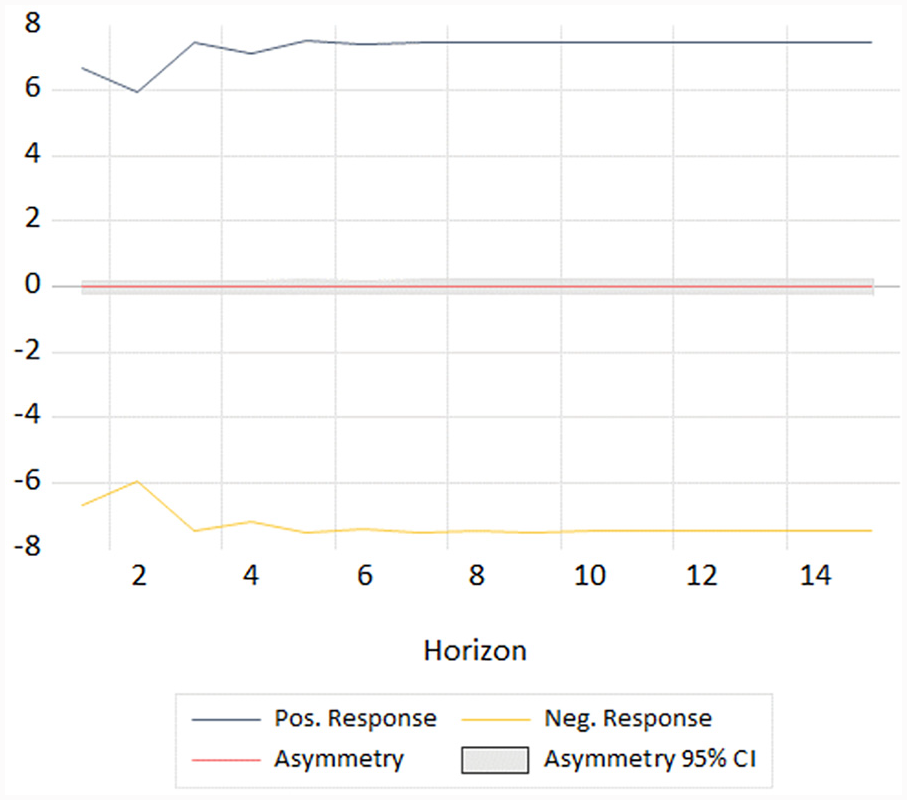

Figure 2 depicts the analysis of the dynamic multipliers of the variable FD in the NARDL model and their impact on the GDP per capita (EG) variable in Algeria. The chart illustrates the impact of positive and negative shocks on the FD variable on EG for 15 years, revealing how EG adjusts to its new equilibrium in the long run after a shock in FD. Additionally, the chart displays the asymmetry line, which represents the difference between the positive and negative effects of shock multipliers in FD on EG, along with the confidence intervals to indicate the 95% confidence level for asymmetry.

Cumulative dynamic multipliers of the variable: FD on EG shock evolution.

The chart confirms that FD has a symmetric impact on EG in Algeria. Positive and negative shocks on FD have a similar impact on EG for the entire period, both in the short and long term, as they are on the zero line. The impact of positive shocks on FD is positive for the period, while the impact of negative shocks on FD is negative for the period. The imbalance is corrected in around 6 years. Therefore, the figure shows symmetry in the impact of FD on EG in the short and long term.

It is worth noting that the dynamic multipliers can capture any potential asymmetry in the adjustment path, even if no evidence of short-term asymmetry is found. This is because the adjustment path depends not only on long-term parameters but also on error correction coefficients and model dynamics (Abdel-Latif et al., 2018; Shin et al., 2014). Therefore, examining the adjustment paths and the duration of the imbalance after a shock can provide helpful information about asymmetry patterns in the short and long terms.

The IMF FD Index measures the development of financial systems in countries, including Algeria. It is important to understand the relationship between (FD) and (EG) to assess the impact of positive and negative shocks on FD in Algeria.

Although there is no specific study focusing on Algeria, studies on the nexus between FD and EG in other countries can provide insights. For example, a study on the causal relationship between FD and EG in the USA found a bilateral relationship between the two, with FD having a negative and significant impact on EG, while the influence of EG on FD was positive but not significant (Oyelami et al., 2016). Another study on emerging economies, including Nigeria, found that FD had a considerable impact on EG (Ehiedu et al., 2022). Based on these findings, it can be inferred that positive and negative shocks on FD may have a similar impact on EG in Algeria, both in the short and long term. However, it is important to note that the relationship between FD and EG can be influenced by various factors, such as trade openness, inflation, capital formation, and debt servicing (Shah et al., 2023). Therefore, the impact of FD on EG in Algeria may also depend on these factors and the specific context of the country. In conclusion, while there is evidence to suggest that FD has a symmetric impact on EG in other countries, it is essential to consider the specific context of Algeria and other influencing factors when assessing the impact of positive and negative shocks on FD and EG. Further research focusing on Algeria would be necessary to provide a more accurate and comprehensive understanding of this relationship. The finding that positive and negative shocks on (FD) have a similar impact on (EG) in Algeria is significant because it suggests that the Algerian economy responds symmetrically to both types of shocks. This means that the economy is equally sensitive to improvements and declines in (FD), which can have implications for policymakers and economic planning. This implies that the economy is equally affected by both positive and negative changes in FD, and therefore, policymakers should consider the potential consequences of both types of shocks when designing economic policies and strategies. Additionally, the finding that FD causes EG in Algeria in a nonlinear way, as determined by transfer entropy nonlinear causality, further highlights the complex relationship between FD and EG in the country. This complexity suggests that policymakers should take a nuanced approach when addressing the impact of FD on EG, considering not only the level of FD but also the nature of its relationship with EG. In conclusion, the significance of the finding lies in its implications for economic planning and policy formulation in Algeria. Policymakers should be aware of the symmetric impact of positive and negative shocks on FD and EG and consider the nonlinear nature of their relationship when designing strategies to promote (EG) and stability.

Theoretical Contributions

Our finding of a positive impact of (FD) on (EG) in Algeria supports the supply-leading theory proposed by Patrick (1966), who argued financial markets promote growth by improving capital allocation. This also aligns with McKinnon (1973) financial deepening view, where financial intermediaries boost growth through better savings mobilization and investment efficiency. As Pagano (1993) notes, this perspective fits with neoclassical growth models where finance facilitates productive capital accumulation.

However, our results diverge from the “too much finance leads to less growth” view suggested by Arcand et al. (2015) and Cecchetti and Kharroubi (2012). We find no evidence of declining marginal returns or a threshold where excessive FD hinders EG in Algeria, suggesting a more nuanced relationship. Our work also adds to the debate on how financial innovation impacts growth (Arcand et al., 2015; Frame & White, 2004). The symmetric response to FD shocks implies financial innovations have not been growth-depleting in Algeria thus far.

We further enrich the discussion on the nonlinear finance-growth nexus (Greenwood & Jovanovic, 1990; Rioja & Valev, 2004). Rather than an inverted U-shape, the nonlinear causality points to regime-switching dynamics between FD and EG as theorized by Rioja and Valev (2004) and Shen and Lee (2006). This underscores the context-specificity highlighted in recent empirical literature.

Situating in Existing Evidence

Our results corroborate studies finding positive FD-EG links in developing countries (Abu-Bader & Abu-Qarn, 2008; Al khatib et al., 2022). However, the symmetric response conflicts with recent evidence of asymmetry in Africa (Chen et al., 2020; Zungu, 2022). Though nonlinear like Azimi (2022), our findings diverge from Ibrahim and Alagidede (2020) who uncovered asymmetric impacts in Ghana.

The supply-leading influence of FD on EG echoes Islam and Alhamad (2022) but contradicts Opoku et al.’s (2019) demand-following conclusions. Overall, this study deepens theoretical and empirical understanding of the complex finance-growth nexus in Algeria. It highlights the need for bespoke models tailored to country-specific conditions.

The findings of this study are specific to the Algerian context and cannot be directly extrapolated to other countries given differing economic structures and histories. As noted, Algeria’s reliance on hydrocarbons and unique policy shifts imply the finance-growth nexus may exhibit country-specific dynamics. The use of timeseries analysis centered on a single country also intrinsically constrains wider generalization. However, the nonlinear modeling approaches could be fruitfully applied to other developing economies to uncover potential heterogeneous relationships and hidden asymmetries. While the precise response to financial shocks found here may not necessarily hold elsewhere, the overarching notions of nonlinearity and regime-switching effects are likely generalizable features.

Therefore, this study primarily makes a methodological contribution demonstrating the value of techniques like Transfer Entropy and NARDL in illuminating nuances in the finance-growth nexus even for a single country case. The techniques add to the literature by enabling a more granular understanding of complexity. However, care is warranted in directly extrapolating the results to other contexts given Algeria’s distinct structures.

In conclusion, while the specific findings have limited generalizability, the study highlights the merits of bespoke nonlinear models tailored to individual countries over one-size-fits-all frameworks. The need to account for context-specificity when examining the drivers of EG is perhaps the key wider insight. Comparative analysis across similar countries can help identify commonalities while respecting heterogeneous dynamics.

There is need for caution in generalizing the results outside Algeria, given the importance of country-specific geopolitical and institutional structures.

Conclusion and Policy Implications

The study investigated the relationship between (FD) and (EG) in Algeria from 1980 to 2020 using nonlinear modeling techniques. The key findings are:

The transfer entropy analysis detected a one-way nonlinear causality running from FD to EG, suggesting FD influences EG in Algeria. However, the effect was found to be moderately significant.

The NARDL results revealed FD has a symmetric impact on EG in both the short-run and long-run. Positive and negative shocks to FD affect EG similarly.

Shocks to FD are corrected within about 6 years, as evidenced by the cumulative dynamic multiplier.

Robustness checks using the symmetry test and stability diagnostics supported the NARDL findings.

Overall, the study finds evidence that FD influences EG in Algeria, though the relationship exhibits some nonlinearity and takes time to adjust after shocks. While FD promotes EG, other country-specific factors may also influence Algeria’s economic performance.

This study finds a positive and symmetric relationship between FD and EG in Algeria, aligned with the predictions of endogenous growth theory. The results suggest FD causes EG in a non-linear fashion, supporting Patrick’s (1966) supply-leading hypothesis.

The long-run cointegrating relationship and short-run dynamics revealed by the NARDL model provide empirical evidence for the finance-led growth theory. FD is confirmed as a crucial determinant of EG, contrary to the neutrality view. However, the non-existence of any inverted U-shape indicates that the “too much finance leads to less growth” effect suggested by Arcand et al. (2015) does not hold for Algeria.

The positive effect of government spending conforms to Keynesian theoretical notions of countercyclical fiscal policy stimulating aggregate demand. However, the insignificant inflation coefficient substantiates Sidrauski’s (1967) superneutrality hypothesis. The negative trade openness effect can potentially be explained by the infant industry argument, though this requires further investigation.

While the symmetric response of growth to financial shocks may lend support to adaptive market hypothesis, the nonlinear causality indicates inefficiencies that contrast with the efficient market assumptions. The results demonstrate a complex finance-growth nexus that warrants nuanced policy interventions adhering to Lucas critique precepts.

Future research areas include:

exploring the underlying transmission channels that link finance and growth, the heterogeneous effects across sectors, incorporating institutional quality, and the nonlinear and time-varying specifications. Expanding the conceptual framework to include emerging heterodox theories could also provide valuable insights.

Future work could further account for external factors by incorporating global financial/economic indices, terms of trade shocks, regional dummies, and technology proxies as data permits.

Using mixed methods that combine quantitative analysis and case study of how major events influenced Algeria’s history could yield a more nuanced understanding.

Comparing Algeria with similar resource-dependent economies could shed light on the relative role of external versus domestic factors.

Using more granular data and sophisticated techniques to properly account for the two-way feedbacks between FD and EG.

Comparing a wider range of nonlinear and nonparametric techniques such as neural networks, fuzzy logic models, and support vector machines to determine the most robust specification.

Employing causality detection methods such as convergent cross mapping to complement the transfer entropy nonlinear causality findings.

Performing case studies and scenario analyses to evaluate the potential effects of different policy initiatives to promote finance and growth.

The study makes important empirical contributions while also deepening theoretical understanding of the finance-growth debate in the specific context of Algeria’s economy. Meaningful linkages are forged between empirical findings and economic theory.

Based on the key findings, some policy recommendations for Algeria include:

Enhance access to finance by deepening financial markets and broadening financial inclusion. This could stimulate growth.

Introduce macroprudential regulations to mitigate the symmetric effects of FD shocks on EG and reduce adjustment time.

Diversify the economy and promote sectors beyond oil/hydrocarbons to reduce volatility from external shocks.

Improve infrastructure and the business climate to attract more FDI and boost productivity growth.

Provide targeted support to SMEs, which are constrained by access to finance. This could spur job creation and private sector activity.

Strengthen financial sector oversight and stability to build resilience against future crises and maintain confidence in the system.

The above recommendations aim to optimize the interplay between FD and EG given Algeria’s country-specific dynamics, based on evidence from the nonlinear analysis conducted.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are publicly available from the World Bank World Development Indicators (WDI) database and the Financial Development (FD) database issued by the International Monetary Fund (IMF). The data can be accessed from the following links: