Abstract

This paper analyzes the nexus between energy consumption, financial development, and economic growth in twenty-one (21) sub-Saharan African (SSA) nations by using the nonlinear autoregressive distributed lag (NARDL) framework from 1990Q1 to 2014Q4. First, the study reveals that energy consumption and financial development have asymmetrical impacts on economic growth in most countries in the short and long term. Second, positive shocks to financial development favor economic growth in only a few nations compared to the negative shocks in the short term, whereas they have mixed effects in the long term. Third, we found that adverse shocks to energy consumption boost economic growth in several nations in the short term, unlike the positive shocks, but the scenario has reversed in the long term. We also found that gross fixed capital formation and labor force remain key factors promoting economic growth in many SSA countries, in contrast to the mixed effects of trade openness over time. Accordingly, our study recommends implementing energy-saving policies in specific SSA countries to stimulate sustainable development. Policymakers must embrace an effective credit allocation to the private sector supporting productive investments. Governments should also optimize domestic investments in physical capital, upgrade the labor force, and implement efficient strategies in international trade. These policy recommendations need to be implemented according to the unique socio-economic characteristics of each SSA country.

Introduction

The inevitable use of energy in daily life and its essential role in producing goods and services are the primary reasons for the growing interest in research on the energy-growth link. As one of the least developed regions in the world, Sub-Saharan Africa (SSA) faces many challenges that hamper its sustainable development and its process of catching up with the economic growth of the more advanced regions. Gross Domestic Product (GDP) per capita in SSA increased from −0.30% in 1990 to 3.87% in 2004 and then declined to 2.05% in 2014. 1 This lack of sustainable growth cannot substantially meet the needs of its growing vulnerable population (from around 510 million in 1990 to over 968 million in 20142) in recent decades, despite the region’s substantial natural reserves. Moreover, the financial sector in sub-Saharan Africa (SSA) is underdeveloped compared to the rest of the world. The underdevelopment of the financial sector mainly leads to an inadequate allocation of resources and low-factor accumulation, adversely affecting economic growth (Akinlo, 2019; McDonald & Schumacher, 2007).

Additionally, many studies revealed that too much financial development might not be optimal for sustainable development in all countries (Arcand et al., 2015; Law & Singh, 2014; Samargandi et al., 2015). Although the SSA region has enormous financing needs to fight poverty through inclusive growth, the lack of legal support for creditors’ rights and the risks of credit default still keep the proportion of domestic credit to the private sector at low levels (estimated at 24% of GDP in 2014) compared to other regions (Nyantakyi & Sy, 2015). Thus, given these financial problems in some SSA countries and the heterogeneous level of financial development among countries, governments need to properly allocate their limited financial resources to productive investments for sustainable economic growth in their countries.

On the other hand, the SSA region faced many challenges in the energy sector. Its share of the global population without access to electricity significantly increased from 28% in 1990 to 68% in 2017 (approximately 573 million people). 3 One of the paradoxes of the SSA region’s energy challenge is that the high cost and scarcity of energy supply in many countries coincide with unnecessary, wasteful, and inefficient energy consumption. This situation is often due to obsolete, inefficient machinery and equipment, and dependence on unclean energy sources such as fossil fuels and traditional biomass. The growing concerns over global warming require appropriate energy policies aligned with sustainable development in the SSA region.

These stylized facts mentioned above, among others, make it necessary to explore the underlying challenges and review the main drivers of economic recovery and sustainable development in the SSA region.

Several studies highlighted the importance of financial development and energy consumption in conditioning economic growth in the SSA region (Aka, 2010; Esso, 2010; Fatai, 2014; Kassi et al., 2020; Kouakou, 2011; Le, 2015; Nkalu et al., 2020; Wolde-Rufael, 2005; Zerbo, 2017). These studies mainly focused on linear dynamics among the underlying variables through different empirical frameworks. Recent studies that have investigated nonlinear dynamics in the energy-finance-growth nexus (Chen et al., 2020; Ibrahim & Alagidede, 2019; Nyoni & Phiri, 2018) focused only on a few countries (mainly in a single country) using bivariate approaches. Nevertheless, most of these studies failed to analyze the asymmetrical impacts of financial development and energy use on economic growth in a multivariate analysis under a comparative approach, including several SSA countries.

Unlike most previous studies mentioned above, the main contribution of this study to the existing literature on the financial-energy-growth link involves the investigation of potential asymmetric relationships between variables. Given the uneven constraints of the SSA countries’ real and financial sectors, governments need to know if positive or negative fluctuations in financial development and energy consumption do not have the same impacts on their economic growth. It is essential to consider this asymmetry. Many factors can cause the existence of an asymmetrical relationship between variables. Some of the reasons are the complexity of the economic system and the mechanisms by which the studied variables are generated. Economic activities in the region are characterized by downward and upward trends in natural resources and macroeconomic variables due to business cycles in the financial and real sectors. This intricacy can also be described by regime changes and economic events, that is, changes in the economic environment, energy prices, and socio-economic policies. Besides, it would be challenging to examine the complexity of the dynamics among financial development, energy use, and growth using linear models because of information asymmetries, incomplete markets, fluctuations, and uncertainties in the financial and real sectors (Coval et al., 2009; Ledenyov & Ledenyov, 2013; Meyers, 2010; Stiglitz, 2002, 2017). The asymmetrical effects of financial development and energy consumption on economic growth may also stem from the likelihood of abnormal and inconsistent consumer behavior and unpredictable reactions of market participants to economic shocks and policies. Accordingly, our study addresses the following research questions: Does energy consumption have an asymmetrical impact on economic growth in each SSA country? Does an expansive credit policy affect the economic growth of all SSA countries in the same way as a restrictive bank credit policy for the private sector? How do these short-term and long-term effects differ between SSA countries?

This study contributes to the empirical literature on the finance-energy-growth nexus by allowing for asymmetrical and nonlinear relationships between these variables across several SSA countries in multivariate models. Most studies have only considered linear relationships between financial development, energy consumption, and economic growth in a few African countries (Kassi et al., 2017; Le, 2015; Odugbesan & Rjoub, 2020). Therefore, we provide a country-level analysis of twenty-one (21) SSA countries with quarterly data from 1990 to 2014 in a comparative analysis. We utilized the nonlinear autoregressive distributed lag (NARDL) method of Shin et al. (2014) to analyze the asymmetrical impacts of negative and positive changes in energy consumption and financial development on the economic growth of sub-Saharan African countries in the short and long term. In comparison with the results of our NARDL frameworks (non-linear models), we also present those of the ARDL specifications (linear models) for all countries. Our country-level analysis provides interesting guidance that will help policymakers better comprehend the complexity of the connection between energy consumption, financial development, and economic growth to carry out suitable strategies in SSA nations. Our study examines explicitly whether positive and negative shocks (or changes) to energy consumption and financial development have similar effects on economic growth in each SSA country. Due to the economic specificities of each country in terms of energy mix and level of financial development, some policies arising from possible asymmetrical effects of those variables on economic growth in one country may not be appropriate in another. An expansionary credit policy or an increase in energy consumption in certain circumstances (e.g., in an environment of low institutional quality and inefficient management of resources) may not be an appropriate policy to increase economic growth in some countries and may differ from the effects of restrictive policies.

The remainder of this paper is hereafter structured. Section 2 overviews the literature on the finance-energy-growth link in the Sub-Saharan African region. Section 3 presents the methodology and data of the research, while section 4 underlines the results and discussions. Finally, the last section summarizes the paper and highlights the policy implications for the sustainable development of the SSA nations.

Literature Review

Energy Consumption and Economic Growth

The integration of energy as a factor of production in growth models can be linked to its significant contribution to the wealth of nations during the 18th century’s industrial revolution. It is also related to the economic consequences inherent in past oil crises (1973, 1979, and 2008). The KLEM or KLE production functions further underlined the theoretical channels through which energy (E), physical capital (K), labor (L), and raw materials (M) affect the level of output, that is, the economic growth of a country. These functions sparked a theoretical debate leading to several outcomes. Berndt and Wood (1979) postulate the complementarity between physical capital and energy consumption in production. They reveal that most physical equipment, that is, machines needed to create goods and services in a given economy, is energy-intensive. Conversely, Griffin and Gregory (1976) maintain that these two factors of production are substitutable, while Percebois (1999) advocates that the effect of energy consumption on economic growth can vary over time and space. This relationship can also depend on a country’s capital structure, technology, energy price, the behavior of economic agents, climate change, and regulatory framework.

Empirically, the relationship between economic growth and energy consumption consists of four hypotheses: the neutral hypothesis, the conservation hypothesis, the growth hypothesis, and the feedback hypothesis. The growth hypothesis assumes that energy consumption leads to economic growth (Adebayo et al., 2021; Fatai, 2014; Odugbesan & Rjoub, 2020; Wolde-Rufael, 2005). This assumption means that energy consumption is an important determinant of economic growth, among other factors. Efficient and productive use of energy sources and other factors in the production of goods and services can significantly boost economic growth. Proponents of this hypothesis argue that energy consumption is a key production factor that helps drive economic activities. “Wolde-Rufael (2005) investigated the linear relationship between energy demand and economic growth in nineteen African nations through the bounds testing approach to cointegration of Pesaran et al. (2001) and the Granger (1969)’s causality test on data during 1971 to 2001. He confirmed a long-term link between energy consumption and per capita economic growth in eight countries and supported the growth hypothesis for Cameroon, Morocco, and Nigeria.” Using several econometric techniques, such as the ARDL framework, the DOLS, and FMOLS estimators, Adebayo et al. (2021) also proved that energy consumption increased economic growth in South Korea from 1965 to 2019.

However, other studies supported the conservation hypothesis, revealing that growth unilaterally increased energy use in most countries (Durusu-Ciftci et al., 2020; Esso, 2010; Le, 2015; Zerbo, 2017). This hypothesis primarily represents the situation in nations that are not heavily dependent on energy. From this, it can be inferred that approaches to reducing energy demand have little or no effect on economic production. Esso (2010) confirmed this hypothesis in Ghana and the Republic of the Congo using a causality test from 1970 to 2007. The bivariate causality analysis of Durusu-Ciftci et al. (2020) indicated that economic growth led to energy consumption at the 75th quantile in Egypt from 1971 to 2014.

Alternatively, the feedback hypothesis assumes bidirectional causality between energy use and economic growth (Kassi et al., 2017; Kouakou, 2011). It means that the two variables cannot be separated because each affects the other simultaneously in the same way. Thus, less energy consumption will hurt economic performance and vice versa. Kassi et al. (2017) upheld this hypothesis in Cote d’Ivoire from 1971 to 2011 by employing a Vector Error Correction Model (VECM) on annual energy use data from hydroelectric sources and growth. They corroborated the findings of Kouakou (2011) of a two-way causality between electricity consumption and economic growth in the short term in Cote d’Ivoire. The author applied an error correction model to annual data from 1971 to 2008.

Nonetheless, the neutral hypothesis is more radical in arguing no causal link between energy use and economic growth (Esso, 2010; Fatai, 2014; Zerbo, 2017).

In such a scenario, neither a country’s expansionary nor conservative energy policies can affect its economic growth. Although Fatai (2014) proved the growth hypothesis in the South and East Africa sub-regions using a panel error correction model, his study found no causal link between energy use and growth in the West and Central African sub-regions in the 1980 to 2011 period. Zerbo (2017) also confirmed the neutral hypothesis in Togo, South Africa, Benin, Ghana, Cote d’Ivoire, and Congo from 1971 to 2013.

Another series of studies pointed out that the consumption of renewable energies and financial development can improve the quality of the environment, which, coupled with a better quality of governance, is a guarantee of the sustainability of long-term economic growth in the world (Kassi et al., 2021, 2022; Kirikkaleli & Adebayo, 2020). Kassi et al. (2021) revealed that a good quality of governance could moderate the finance-renewables-growth nexus, while Kassi et al. (2022) also showed that good institutional quality conditioned the relationship between financial development and environmental quality in several countries from 1990 to 2017. Renewable energy consumption and environmental sustainability are linked to energy consumption and economic growth.

Finance and Economic Growth

Unlike the neoclassical model, which explains economic growth by exogenous variables (i.e., technological progress and population) and affirms the dichotomy between the financial sector and the real sector, the ideas of the theorists of endogenous growth are very different. They advocated those forces internal to the economic system, such as human capital, research and development, innovation, institutional factors, energy resources, and financial development, allow economic growth to be self-sustaining. Several economists have used endogenous growth models to examine the finance-growth nexus (Greenwood & Jovanovich, 1990; Pagano, 1993). For instance, Pagano (1993) showed that financial development could improve economic growth through three transmission channels: the share of savings invested, the marginal productivity of capital, and the private savings rate.

Numerous empirical studies on the finance-growth nexus revealed mixed results across SSA countries. The supply-leading hypothesis assumes that the increasing supply of financial services (i.e., financial development) leads to economic growth. It suggests that financial services offered by the financial sector provide opportunities for businesses in the real sector to demand them, ultimately leading to economic growth. Following Levine (2005) and Cezar (2012), financial development can drive economic growth through the efficiency of financial markets and institutions in performing six financial functions, such as the mobilization of funds for productive activities, creation and distribution of information, ability to manage risks, investment monitoring and corporate management, transaction cost reduction, and financial investment liquidity. This hypothesis has been corroborated by Agbetsiafa (2004) in Ghana, Zambia, South Africa, Togo, Nigeria, and Senegal. Kassi et al. (2017) proved the supply-leading hypothesis by employing the ARDL and VECM techniques to analyze the linear dynamics between economic growth, financial development, and energy consumption in Cote d’Ivoire from 1971 to 2011. In their bivariate analysis of emerging countries, Durusu-Ciftci et al. (2020) also confirmed that financial development promoted economic growth at the 25th and 75th quantiles in Egypt and South Africa using the Toda-Yamamoto method with a Fourier approximation (TYF) on data from 1971 to 2014. Through the Dumitrescu-Hurlin causality tests, Kihombo et al. (2021) also validated the supply-leading hypothesis in the case of West Asia and the Middle East during the 1990 to 2017 period.

Nonetheless, other studies validated the demand-following hypothesis that economic growth causes financial development (Ginevičius et al., 2019; Kassi et al., 2021). It stipulates that economic growth will lead to the emergence of financial products and institutions to meet the demand for financial services. Thus, it emphasized that financial development is determined endogenously by the real sector. The level of economic expansion of a country in the early days of industrialization may determine the role of its banking sector. Odhiambo (2009) showed that development in the business world would lead to increased demand for financial services, and attempts to meet demand in the real world would create new financial markets and institutions. Kassi et al. (2021) supported the growth-led finance hypothesis in 33 selected upper-middle-income countries, including Mauritius, Namibia, and South Africa, from 1990 to 2017. They applied a panel Granger (1969)’s non-causality test in Dumitrescu and Hurlin (2012).

The feedback hypothesis assumes that financial development and economic growth are mutually reinforcing. It predicts that financial development is necessary for economic growth, which increases the demand for financial services and products, enabling the development of the financial system. Patrick (1966) argues that supply-side models predominate in the early stages of economic development and then give way to demand-side tracking as the economy develops. Under this hypothesis, financial development and economic growth are complementary to a country’s sustainable production of goods and services. This hypothesis of bidirectional causality between financial development and economic growth has also been confirmed in the SSA region by Aka (2010) in several countries using the VECM framework on annual data from 1960 to 2002, as well as by Kassi et al. (2020) in 35 SSA countries over the period 1990 to 2017 through the use of a panel causality test in Dumitrescu and Hurlin (2012).

Nevertheless, pessimistic views emerge from studies that support the neutral hypothesis of no causal link between financial development and economic growth. This hypothesis implies a dichotomy between the financial and real sectors, assuming that the former does not affect the latter and vice versa. According to this hypothesis, financial policies derived from financial markets and institutions are irrelevant and useless to promoting economic growth (Opoku et al., 2019; Pradhan et al., 2013; Puente-Ajovín & Sanso-Navarro, 2015). Using a frequency-domain causality approach on data from 47 African nations, Opoku et al. (2019) showed that financial and economic growth had no typical relationship in most countries from 1980 to 2016. Moreover, Kassi et al. (2020) found that domestic credits to the private sector positively affected economic growth in the SSA region from 1990 to 2017. The authors applied the two-step system-GMM estimator on panel data from 35 SSA countries.

Nonlinear Approaches in the Finance-Energy-Growth Nexus

Global warming, imperfect markets, and the complex nature of economic and financial systems exacerbate the information asymmetry between market players. These catalysts arouse a growing interest in studying nonlinear dynamics among energy use, financial development, and growth in developing countries such as sub-Saharan Africa. Moreover, imbalances between energy supply and demand and the inefficient use of energy resources differ among SSA countries. Likewise, the level of financial development varies from country to country. The energy and financial challenges (energy deficit, energy inefficiency, credit risk management, and weak financial supervision, among others) are heterogeneous across SSA countries because of the specificities of each country linked to the initial levels of economic growth, institutional quality, regulatory framework, and energy mix. Thus, the possibility of asymmetrical effects of financial development and energy use on SSA nations’ economic growth should be considered when implementing appropriate economic policies.

Recent studies have highlighted the asymmetrical relationships in the energy-finance-growth nexus, primarily in developing and developed countries in Europe and Asia (Araç & Hasanov, 2014; Kisswani, 2017; Shahbaz et al., 2017, 2018; Wang et al., 2021). Shahbaz et al. (2017) revealed that only negative changes in financial development and energy use favored economic growth in India over 1960Q1 to 2015Q4. They utilized the asymmetric causality tests and the NARDL framework of Shin et al. (2014). Wang et al. (2021) found that exchange rate volatility was one of the main reasons for the nonlinear relationship between energy consumption and economic growth between 1980 and 2017 in China.

Few studies have examined the asymmetrical impacts of financial development and energy use on growth in developing regions such as sub-Saharan African countries. Most studies have limited nonlinear effects to a bivariate analysis focusing on a single country (Chen et al., 2020; Ibrahim & Alagidede, 2019; Nyoni & Phiri, 2018) while neglecting the nonlinear dynamics between these variables in a multivariate model. Through threshold cointegration and causality techniques, Nyoni and Phiri (2018) concluded that electricity use in South Africa triggered its long-term economic growth from the first quarter of 1983 to the fourth quarter of 2016. In contrast, there was a two-way causality between the cyclical and trend components of the variables. Utilizing the NARDL framework on annual data, Chen et al. (2020) showed that positive shocks to financial development enhanced growth in the short term, unlike the adverse shocks in the long term in Kenya during the 1972 to 2017 period.

Most studies have not incorporated short- and long-term dynamics in the link between financial development, energy consumption, and economic growth in multivariate models. They also overlooked the critical role of dynamic multipliers in understanding historical responses of economic growth to positive and negative shocks to energy consumption and financial development in SSA countries over time. Accordingly, our study aims to fill these shortcomings in the empirical literature by conducting a country-level analysis with a comparative approach. We utilize a multivariate nonlinear autoregressive distributed lag allowing for asymmetrical links among financial development, energy use, and growth in 21 SSA nations during the short and long terms from 1990Q1 to 2014Q4.

We derived our hypotheses based on the evolving complex economic structures and imperfect and cyclical energy and financial markets, coupled with these recent findings of nonlinear effects in the finance-energy-growth nexus in emerging and developed countries (Araç & Hasanov, 2014; Kisswani, 2017; Shahbaz et al., 2017, 2018; Wang et al., 2021, among others). We hypothesize that energy consumption and financial development have asymmetrical effects on economic growth in SSA countries. Thus, we methodically test this general hypothesis by providing a detailed procedure in the next section.

Data, Modeling, and Methodology

Data

This study examines the asymmetrical nexus between financial development, energy use, and economic growth in 21 SSA countries during 1990Q1 to 2014Q4, owing to data availability for the study period. 4 We chose this sampling period to avoid highly unbalanced data between countries due to incomplete data on more recent periods for most of the selected variables. Our selected period also facilitates comparative analysis between countries based on data availability.

Following Kassi, Sun, Gnangoin, et al. (2019), “we firstly utilized annual data from World Development Indicators (WDI, 2017) on energy consumption (energy use, in kg of oil equivalent per capita), gross domestic production (GDP) per capita (constant 2010, U.S. $), financial development (measured by domestic credit to the private sector, as % of GDP), trade openness (trade, as % of GDP), gross fixed capital formation (% of GDP), and the labor force (total). Most empirical studies support the use of these variables in our analysis (Kassi et al., 2020, 2021; Le, 2015; Shahbaz et al., 2017). Domestic credit to the private sector denotes the financial resources that financial institutions provide to the private sector. Most studies have used domestic credit to the private sector as a percentage of GDP as a standardized measure of financial development (Cihák et al., 2012; Kassi et al., 2017, 2021; King & Levine, 1993; Law & Singh, 2014; Opeyemi et al., 2019; Rousseau & Wachtel, 2011).

Second, we converted the annual data to quarterly data to improve the correctness of the results. We used a variation of the low-to-high-frequency method (the quadratic-match option) consistent with previous research (Kassi, Rathnayake, et al., 2019; Kassi, Sun, et al., 2019; Shahbaz et al., 2017).” This method applies an interpolation that approximates the local quadratic polynomial such that the mean value of the next four quarters equals the data of the matching year. We transformed all the variables into their logarithmic form to derive reliable results and normal distributions. It also makes it easier to interpret the results.

Figures 1 and 2 portray the variables’ descriptive statistics to highlight the different economic characteristics in each of the 21 SSA nations from 1990Q1 to 2014Q4. Figure 1 depicts the evolution of the average income per capita, energy consumption, and labor force. In contrast, Figure 2 shows the average domestic credit distribution to the private sector, investments in fixed assets, and trade openness levels across countries. The complete results of the descriptive statistics are available upon request.

Average growth rates of output, energy, and labor force.

Average growth rates from 1990Q1 to 2014Q4.

The Base Model

Based on the theories of endogenous growth, we started with an extended Cobb-Douglas production function described as follows:

The explained variable GDP denotes the gross domestic product, which is a function of the level of financial development (FIN), energy consumption (ENC), gross fixed capital formation (GFCF), trade openness (TRADE), and the labor force (LAB) in each country at time t. Our linear transformation of model (1) is an extended version of that in Le (2015), with the inclusion of the labor force:

Where ln indicates the logarithmic operator αi is the constant, whereas β, δ, σ, ω, and κ represent the parameters of the corresponding explanatory variables, and ε is the error term which is supposed to be identically and independently distributed (iid).

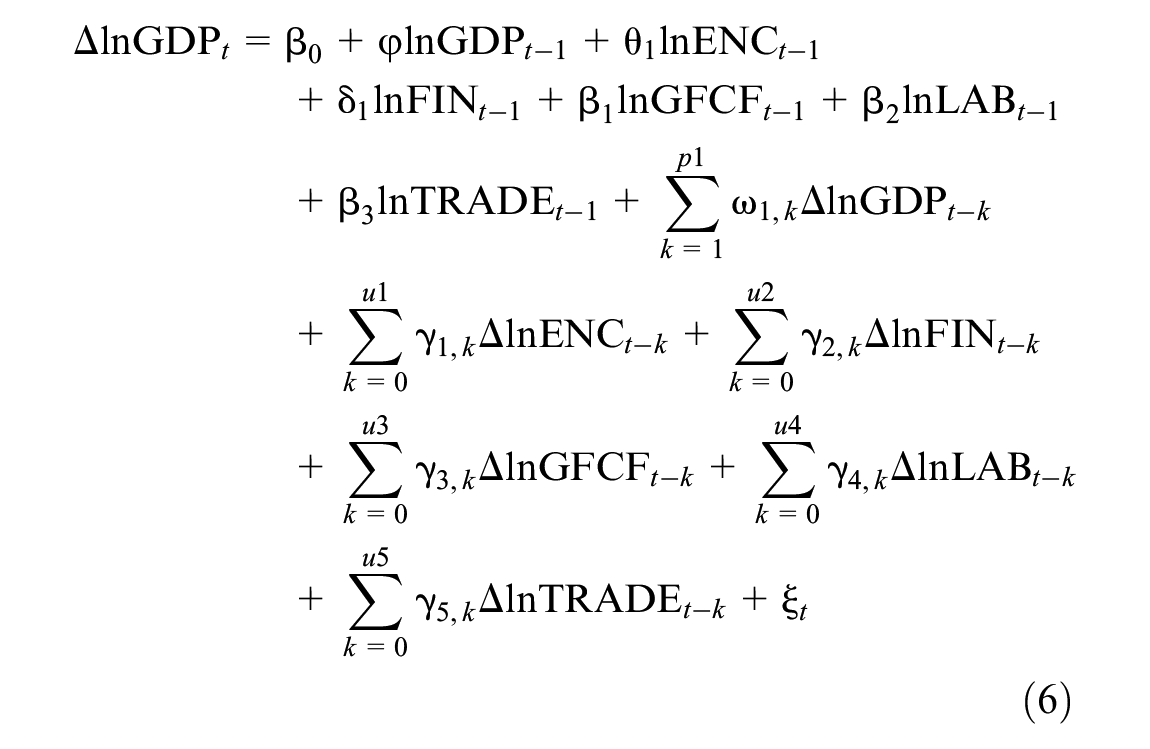

Moreover, we differ from Le (2015) in considering the eventuality of asymmetrical relationships in the finance-energy-growth nexus. He showed the positive effects of energy use and financial development on output per capita in a panel of 15 SSA countries using the mean group estimators (MG) from 1983 to 2010. In this study, we utilized the NARDL method of Shin et al. (2014) to distinguish between short-term and long-term asymmetrical impacts of independent variables on the dependent variable within an error correction framework. In addition, the NARDL method is still valid in multivariate models and a combination of variables with different orders of integration, that is, I(0) and I(1), unlike the traditional frameworks. The NARDL technique provides a graph of cumulative dynamic multipliers that plot the asymmetrical adjustment patterns based on positive and negative shocks to the independent variables. This method also combines the dynamic error correction coefficient with long-run asymmetric cointegration regression in a bounds-testing procedure. Monte Carlo simulations show that the NARDL method has low estimation bias and considerable power in test statistics.

Accordingly, we proposed an augmented NARDL model similar to Shahbaz et al. (2017):

“Where

The long-term coefficients are calculated as follows:

The dynamic specification of the model (3) differs from the theoretical and static models (1). Model (3) accounts for both short and long-term dynamics in a nonlinear multivariate autoregressive distributed lag (NARDL) which has many advantages as described above, unlike the linear and static model (1). Thus, model (3) is a logarithmic transformation of model (1) in a NARDL framework with short-term and long-term dynamics.

Methodology and Hypotheses Development

We first started the analysis with descriptive statistics for all variables. Then we performed three famous unit root tests for each nation’s variables to avoid false results for non-stationary variables. The unit root analysis involved the tests in Kwiatkowski et al. (1992), Phillips and Perron (1988), and Dickey and Fuller (1981), following the optimal lag selection of the Akaike Information Criteria (AIC).

“Second, we used the general-to-specific method to evaluate the NARDL model (3) for each nation with up to 10 lags. This approach reduces most of the irrelevant lagging variables from the model to obtain robust results. We then investigated the long-term nexus between the variables using two tests, the F-test in Pesaran et al. (2001) and the t-test in Banerjee et al. (1998).

Under the null hypotheses, the F-test (Hypothesis 1b:

Third, following the reasons mentioned above of imperfect and cyclical markets, the complexity of financial and real sectors, as well as recent empirical findings of asymmetrical effects in emerging and developed countries (Kisswani, 2017; Shahbaz et al., 2017, 2018, among others), we examined the asymmetrical effects in the energy-finance-growth nexus in SSA countries. Thus, we implemented Wald tests to investigate the existence of nonlinear effects in long-term parameters in the model (3) as follows:

Hypothesis 3a assumes a symmetrical impact of energy use on economic growth, whereas hypothesis 3b supposes a symmetrical link between financial development and growth during the long term. In the case where the Wald tests fail to reject hypotheses 3a and 3b, a restricted version of the NARDL model (3) is expressed below:

Equation 4 shows a restricted model with only long-term symmetrical dynamics.

In this circumstance

Hypotheses 4a and 4b assume the symmetrical impacts of energy use and financial development on short-term growth. We also estimated the NARDL model (5) in each nation where there were only symmetrical impacts in the short term:

Equation 5 underlines the long-term asymmetrical impacts of financial development and energy use on growth in the case of short-term symmetries.

Moreover, the restricted model (6) highlights the case where one cannot reject the hypotheses of short and long-term symmetries:

Then the dynamic multipliers were recursively derived to represent the asymmetrical growth (GDP) responses to negative and positive shocks to financial development and energy consumption over the years, respectively.

Following the outcomes of the symmetry tests, we used the approach described by Shin et al. (2014) to compute the dynamic multipliers after assessing the appropriate NARDL models in each nation:

Where:

Results and Discussions

Results and Interpretations

The results of the stationarity analysis showed that the variables are primarily stationary at the first difference at the 1% significance level. These results are available upon request. Hence, we applied the NARDL approach to investigate the cointegration among the variables since neither is I(2).

Next, Table 1 displays that the calculated tBDM or FPSS values are greater than the upper limits of their corresponding critical values in several specifications (see Table A1 in Appendices). This finding supports hypotheses 2a and 2b of a long-term nexus between energy use, financial development, and growth in many SSA nations. The Wald tests’ significance in Table 2 indicates several cases of asymmetrical impacts of energy use and financial development on growth during the long term (rejection of hypotheses 3a and 3b) and the short term (rejection of hypotheses 4a and 4b). In addition, we estimated the suitable NARDL model based on the Wald test outcomes for each nation, following the last column of Table 2. Table 3 indicates the results of the adequate NARDL model in each nation.

Cointegration Tests.

Note. “Values reported in the table are t-statistics for the tBDM test and F-statistics for FPSS. Based on the particular sample size for each nation, we utilize the critical values of Narayan (2005) in the cases of any small sample size (see Table A1 in Appendices). The critical values for tBDM using t-Bounds test with k = 7 for models [3] and [5] are [−2.57; −4.23] at the 10% level, [−2.86; −4.57] at the 5% level, and [−3.43; −5.19] at the 1% level of significance. The similar critical values for tBDM with k = 5 for models [4] and [6] are [−2.57; −3.86] at the 10% level, [−2.87; −4.19] at the 5% level, and [−3.43; −4.79] at the 1% level of significance. Table A1 reports the corresponding critical values for FPSS in Appendices. Like other studies (Kassi, Rathnayake, et al., 2019; Kassi, Sun, et al., 2019), we used the general-to-specific approach (unidirectional method and p-value backward 10% significance level as stopping criteria) with a maximum lag length of 10. The results are the Authors’ computations in Eviews 9.” LTA = long-term asymmetry; STA = short-term asymmetry; STS and LTS denote the Short-term and Long-term Symmetrical models, respectively; FPSS and tBDM denote the Pesaran et al. (2001)F-test and Banerjee et al. (1998)t-test, respectively.

p < .1. **p < .05. ***p < .01.

Symmetry Tests.

Note. “We performed the tests by utilizing the unrestricted (Unr.) NARDL model [3] as the reference model. The ‘Conclusion’ column indicates the suitable model for each nation based on the Wald test outcomes. The NARDL models [a] to [e] denote other restricted (Rest.) NARDL models. They show various asymmetrical cases between financial development, energy use, and growth in the short or long-term following the results of the Wald tests. The results are the authors’ calculations in Eviews 9.”

p < .1. **p < .05. ***p < .01.

Estimations of the NARDL Models.

Note. See Table 1 for country descriptions. “χ2SC(2) is the F-statistic of Breusch-Godfrey serial correlation (L.M.) test of order 2. Arch (1) is the F-statistic of the heteroskedasticity test: ARCH of order 1. These results are authors’ calculations using Eviews 9.

p < .1. **p < .05. ***p < .01.

Regarding the long-term dynamics, we showed that positive shocks to energy consumption decreased economic growth in five countries (Botswana, Eritrea, Mozambique, Nigeria, and Sudan), unlike their significant positive effects at the 1% level in twelve countries (the Republic of the Congo, Gabon, Ghana, Kenya, Mauritius, Senegal, Togo, South Africa, the Democratic Republic of the Congo, Cote d’Ivoire, Cameroon, and Tanzania). However, adverse shocks to energy consumption increased economic growth in eight (Botswana, Cameroon, the Democratic Republic of the Congo, Gabon, Ghana, Mozambique, South Africa, and Tanzania) out of seventeen countries. In most cases, these impacts are significant at the 1% level, except for Gabon, Mauritius, Nigeria, Sudan, and Togo.

Besides, positive shocks to financial development hurt economic growth in the Democratic Republic of the Congo, Namibia, and Nigeria, significantly at the 5% level, and in Cote d’Ivoire, Eritrea, Ghana, and Senegal at the 1% level, respectively. In contrast, they stimulated economic growth in Botswana, the Republic of the Congo, Gabon, South Africa, and Togo at the 1% level, and Kenya and Mauritius at the 5% level in the long term, respectively. Adverse shocks to financial development significantly enhanced (respectively hindered) economic growth in Ghana, and Senegal (respectively in Botswana, Eritrea, the Republic of the Congo, Mauritius, and South Africa) at the 1% and 5% levels, in the Democratic Republic of the Congo at the 10% level, non-significantly in Gabon, Namibia, and Nigeria (respectively in Cote d’Ivoire, Kenya, and Togo).

Regarding the symmetrical cases, we found that energy use positively affected economic growth in Angola and Niger (significant at the 10% level), unlike its adverse effects in Benin and Namibia in the long term. Financial development positively fostered economic growth in Angola and Niger at the 1% level, Tanzania (significant at the 10% level), and Sudan. Still, it adversely affected economic growth in Benin, Cameroon, and Mozambique during the long term. In many cases, Table 3 shows that labor force, gross fixed capital formation, and trade openness positively affect economic growth in the long term in 11, 14, and 10 countries. In contrast, their detrimental effects on growth occur in ten, seven, and eleven SSA nations.

About the short-term analysis, Table 3 indicates that positive shocks to energy consumption significantly stimulate economic growth in only seven (Togo, Tanzania, Sudan, Cote d’Ivoire, the Democratic Republic of the Congo, Benin, and Angola) out of seventeen countries. In comparison, adverse shocks to energy use have significant positive impacts on economic growth in 12 out of 18 countries, at the 1% level, respectively. Nevertheless, positive shocks to financial development had detrimental impacts on economic growth in 12 out of 17 countries. In contrast, adverse shocks to financial development promoted economic growth in 10 out of 16 nations during the short term. The results also showed that energy consumption symmetrically decreased Eritrea’s economic growth, whereas financial development symmetrically fostered economic growth in Cameroon, Gabon, and Togo.

As for the control variables, there were positive effects of the labor force, trade openness, and gross fixed capital formation on economic growth in twelve, five, and eleven nations, while we found their harmful effects on growth in nine, fourteen, and eight SSA countries in the short term, respectively.

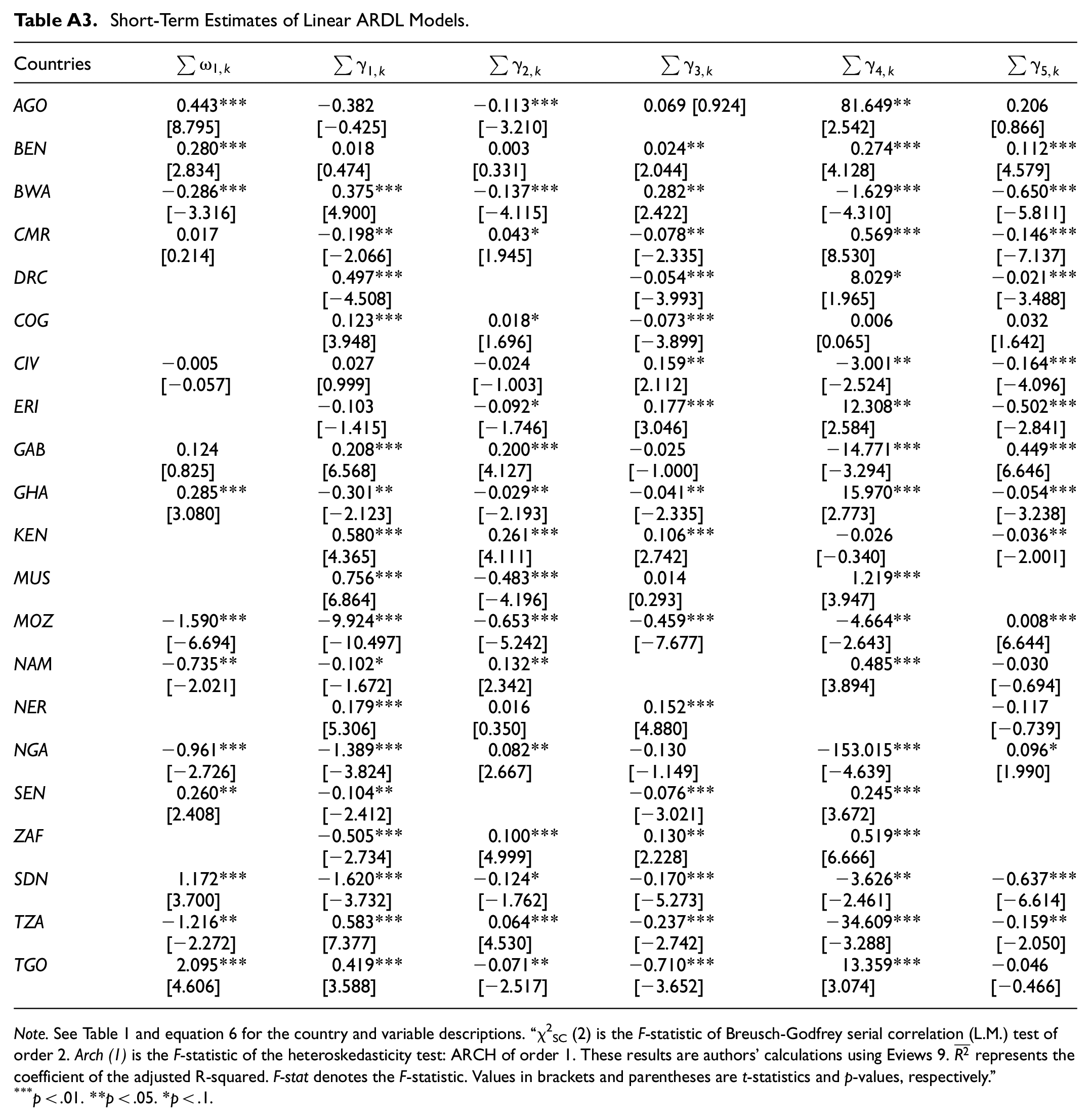

Moreover, we report the results of the estimates of the linear ARDL models in Tables A2 and A3 for comparison with those of the NARDL models (see Appendices). Table A2 shows that most variables positively affect long-term economic growth in most countries. In contrast, Table A3 shows that only gross fixed capital formation and trade openness reduce economic growth in several countries in the short term. However, we found that the long-term cointegrating relationships between the variables were insignificant in many countries (see Table 1), unlike the NARDL models. Also, linear ARDL estimates were mainly significant in the short term.

Dynamic multipliers illustrate the asymmetrical effects in the finance-energy-growth nexus in many countries, as the line of asymmetry (the difference between negative and positive shocks to these variables) deviates from the horizontal axis (see Figures 3 and 4).

Dynamic cumulative impacts of energy consumption on economic growth in sub-Saharan African nations.

Dynamic cumulative impacts of financial development on growth in sub-Saharan African nations.

Discussions of the Results

This paper shows that an increase in energy use (a positive change) slows economic growth in many nations only in the short term, unlike restrictive or controlled energy consumption (negative changes). This evidence reveals that inefficient management of energy use in daily activities occurs mainly in the short-term, where high levels can lead to environmental degradation, global warming, and public health problems, damaging the labor force and other production factors necessary for economic growth in most countries. Many SSA countries face several challenges in their energy sector, such as poor management, low investment, high costs, and inefficient operating system. System losses in sub-Saharan Africa are twice the world average, including technical losses stemming from inadequate revenue collection, commercial losses, poorly maintained power transmission, and distribution networks. These losses were evaluated at 18% in the region, excluding South Africa (International Energy Agency, 2014). These losses expose utilities to significant financial risk and raise end-user fees (Castellano et al., 2015).

Likewise, our findings imply that energy conservation technologies (renewable energies), fostered by sound legal and regulatory policies, are necessary for sustainable development in specific SSA countries. Nevertheless, the beneficial effects of positive changes in energy consumption on economic growth indicate that energy-intensive investments for the development of the industrial sector and technological progress will continue to promote economic growth in several countries in the long term, particularly in the Republic of the Congo, Cote d’Ivoire, Gabon, Ghana, Kenya, Mauritius, Senegal, and Togo. Energy-intensive investments may not be an appropriate policy to promote growth in Eritrea, Namibia, Nigeria, Sudan, and Benin. For instance, expanding and powering the gas infrastructure requires careful management to avoid methane leaks. This is one of the primary issues in mitigating global warming and climate change while supplying electricity. The abundant use of coal in southern Africa electrified the region but left severe public health challenges and air pollution. SSA nations that are heavily dependent on fossil fuels, that is, the oil industry, namely Nigeria, are impacted by price fluctuations in international markets. The sharp drop in oil prices from July 2014 to January 2015 reduced Nigeria’s income by 28% (International Renewable Energy Agency, 2015).

Furthermore, the influence of financial development on growth varies across nations. The adverse effects of excessive credit (positive shocks) in most nations during the short term, may be related to the relatively low quality of institutions, flexible banking regulations, and the lack of investment supervision, mainly in low-income nations in the SSA region (Kassi et al., 2020). In line with Rousseau and Wachtel (2011), these results show that excessive credit growth or too rapid financial deepening can trigger inflation and weaken banking systems, causing financial crises that stifle growth. In the same vein, Arcand et al. (2015) revealed a threshold above which financial development hindered economic growth. Our results show that credit that is easily accessible to the private sector is not always adequately managed to drive economic growth in all countries (Law & Singh, 2014).

The absence of a rigorous credit allocation process to the private sector by banks (i.e., the lack of proper borrower solvency analysis, adequate investment supervision, and cost-optimal borrowing) may lead to inefficient management of these financial resources to make fruitful investments in these nations (Kassi et al., 2020, 2021). Kassi et al. (2020) showed that only an optimal level of good governance quality (for instance, corruption control, the rule of law, and regulatory framework) could mitigate the adverse effects of financial development on economic growth in most developing countries of the SSA region.

Conversely, many banks’ controlled or restrictive credit policy to the private sector and its positive impact on the SSA nations’ economic growth may stem from a monetary policy focused on price stability and a sound political environment. In the CFA francs’ zone, 5 the fixed exchange rate indexed to the euro prevents the monetary authorities from increasing lending to the private sector (Akinlo, 2019). Nevertheless, an expansionary credit policy to the private sector (positive shocks) significantly stimulates economic growth only in Togo, South Africa, Mauritius, Kenya, Gabon, the Republic of the Congo, and Botswana in the long term. This finding can be justified either by the relatively mature financial system in most advanced SSA economies or by the efficient use of financial resources by their private sector to generate productive investments coupled with their relatively sound institutional and regulatory frameworks, especially in Anglophone nations (Akinlo, 2019). Domestic credit growth to the private sector also enhances economic growth in Niger, Sudan, and Tanzania in the long term, unlike the other SSA nations that necessitate further improvements in their financial and economic structures.

In most countries, the positive effects of gross fixed capital formation and labor force on economic growth are consistent with the findings of Le (2015) and Epaphra and Amin (2022), who applied the generalized method of moments (GMM) to linear panel data models in SSA countries during the period 1996 to 2019. The majority of SSA countries are developing countries, still far from their production frontier and therefore have enormous needs both in skilled labor and in domestic investments in physical capital, which are key factors of production promoting their wealth creation and economic expansion. Our findings also complement the results of Fatima et al. (2020) by confirming the negative effects of trade openness on economic growth in specific SSA countries using a nonlinear framework. This result can be justified by the fact that most SSA countries still have low levels of human capital accumulation and industrialization and a lack of diversified access to global market opportunities. Moreover, their poor institutional framework cannot help them exploit the positive externalities of trade openness because their market power and participation are relatively insignificant in international trade. Accordingly, we suggest that policymakers consider these asymmetrical effects in elaborating economic policies in the SSA region.

Overall, our study enriches the previous empirical studies by revealing the asymmetrical impacts of financial development and energy use on growth using a multivariate NARDL framework. In most SSA nations, our results align with the studies of Kisswani (2017) and Shahbaz et al. (2017) related to Asian countries. Unlike the study of Chen et al. (2020) in Kenya, we extend the analysis with the asymmetrical dynamics among financial development, energy use, and growth in 21 SSA nations using multivariate models. The results of our multivariate NARDL approach contrast with those of Fatai (2014) in the West and Central African sub-regions from 1980 to 2011.

Conclusion and Policy Implications

This paper analyzed the asymmetrical relationships between energy consumption, financial development, and growth in 21 SSA nations from 1990Q1 to 2014Q4 using the multivariate NARDL method of cointegration of Shin et al. (2014).

The results showed that energy use and financial development have asymmetrical impacts on economic growth in 17 and 14 countries in the long term, but in 20 and 18 countries in the short term. Besides, positive changes in energy use and financial development had detrimental impacts on economic growth mainly during the short term, unlike the beneficial effects of their corresponding negative changes in most countries. Concerning the long-term analysis, positive changes in energy use enhanced growth in several nations, except in Botswana, Eritrea, Mozambique, Nigeria, and Sudan. In contrast, positive shocks to financial development promoted growth only in a few countries, characterized mainly by a relatively mature financial system and a sound political environment compared to the other SSA countries. We also found that adverse shocks to energy use and financial development had mixed effects on economic growth, which varied across countries during the long term. These asymmetrical effects could be due to heterogeneous levels of good governance, the macroeconomic environment, the inefficient management of financial resources, and the dependence on traditional biomass and polluting non-renewable energies, namely coal, petroleum, and natural gas, in the production process across countries. We also found that gross fixed capital formation and labor remain key factors promoting economic growth in many SSA countries, in contrast to the mixed effects of trade openness over time.

Policymakers should enhance credit regulatory and supervisory frameworks because increasing levels of financing to the private sector, in the absence of good governance and productive investment, will hamper economic growth in some SSA countries. However, most developing countries face low levels of financial literacy and underdeveloped financial markets, mainly in low-income countries. Thus, governments should establish attractive and flexible institutional regulations to promote financial inclusion and financial literacy for enhancing economic growth in these countries facing socio-economic challenges, unlike developed SSA countries where an expansionary credit policy can harm economic growth. Based on the socio-economic characteristics of each country, we believe that efficient allocation of financial resources will promote energy efficiency and sustainable development in specific SSA countries. Furthermore, the SSA region must evolve toward a balanced energy mix by improving the quality of the regulatory framework and the supervision of the loans granted to direct them toward green projects and renewable energies in the financing of economic activities while taking into account the different levels of economic growth from one country to another. Most governments need to move away from the inefficient and intensive use of impure energy sources and rely more on low-carbon and environmentally friendly energy sources that can sustainably boost economic growth. Among the alternative energy sources, governments may subsidize green projects to deploy modern renewable energy technologies in daily activities while reducing unproductive investments and energy-consuming activities that hamper sustainable growth in the SSA region. The renewal and modernization of outdated electrical installations are also necessary to avoid losses and waste of energy that do not benefit certain SSA countries’ economic growth. Besides, expansionary credit policy and positive changes in energy consumption promote economic growth in some SSA countries. In these cases, governments should take advantage of these expansionary mechanisms to strengthen their economic fundamentals and industrial structures until a mature stage. However, they should gradually shift to more environmentally friendly practices in energy conservation and long-term sustainable financing for sustainable development in the SSA region and globally. Governments should also increase domestic investments in more sophisticated physical capital and implement educational programs and training systems that continually upgrade the workforce with modern skills and know-how in the use of efficient technologies that allow the sustainability of the economic growth of their countries. Improving the quality of economic structures and human capital accumulation in SSA are also necessary conditions for harnessing technological diffusion and knowledge spillovers through trade to increase regional economic growth.

For reasons of brevity and simplicity, our study has certain limitations because we do not consider alternative financial development indicators and the different types of energy consumption in the analysis. Moreover, this study is limited to comparative analysis at the country level, neglecting the sub-regional comparative analysis on the topic in the SSA region. Therefore, this research paves the way for future studies to explore these issues, and panel models in the analysis, such as nonlinear panel ARDL-PMG and Cross-Section Augmented ARDL (CS-ARDL) models, since there may exist cross-sectional dependencies between countries in the sample. Finally, we encourage future studies to consider the likelihood of structural breaks in the data while using newer nonlinear models, that is, asymmetrical causality analysis, threshold, and regime-switching models, among others, on a large sample of African countries over longer and recent time periods.

Footnotes

Appendices

Short-Term Estimates of Linear ARDL Models.

| Countries |

|

|

|

|

|

|

|---|---|---|---|---|---|---|

| AGO | 0.443*** [8.795] | −0.382 [−0.425] | −0.113*** [−3.210] | 0.069 [0.924] | 81.649** [2.542] | 0.206 [0.866] |

| BEN | 0.280*** [2.834] | 0.018 [0.474] | 0.003 [0.331] | 0.024** [2.044] | 0.274*** [4.128] | 0.112*** [4.579] |

| BWA | −0.286*** [−3.316] | 0.375*** [4.900] | −0.137*** [−4.115] | 0.282** [2.422] | −1.629*** [−4.310] | −0.650*** [−5.811] |

| CMR | 0.017 [0.214] | −0.198** [−2.066] | 0.043* [1.945] | −0.078** [−2.335] | 0.569*** [8.530] | −0.146*** [−7.137] |

| DRC | 0.497*** [−4.508] | −0.054*** [−3.993] | 8.029* [1.965] | −0.021*** [−3.488] | ||

| COG | 0.123*** [3.948] | 0.018* [1.696] | −0.073*** [−3.899] | 0.006 [0.065] | 0.032 [1.642] | |

| CIV | −0.005 [−0.057] | 0.027 [0.999] | −0.024 [−1.003] | 0.159** [2.112] | −3.001** [−2.524] | −0.164*** [−4.096] |

| ERI | −0.103 [−1.415] | −0.092* [−1.746] | 0.177*** [3.046] | 12.308** [2.584] | −0.502*** [−2.841] | |

| GAB | 0.124 [0.825] | 0.208*** [6.568] | 0.200*** [4.127] | −0.025 [−1.000] | −14.771*** [−3.294] | 0.449*** [6.646] |

| GHA | 0.285*** [3.080] | −0.301** [−2.123] | −0.029** [−2.193] | −0.041** [−2.335] | 15.970*** [2.773] | −0.054*** [−3.238] |

| KEN | 0.580*** [4.365] | 0.261*** [4.111] | 0.106*** [2.742] | −0.026 [−0.340] | −0.036** [−2.001] | |

| MUS | 0.756*** [6.864] | −0.483*** [−4.196] | 0.014 [0.293] | 1.219*** [3.947] | ||

| MOZ | −1.590*** [−6.694] | −9.924*** [−10.497] | −0.653*** [−5.242] | −0.459*** [−7.677] | −4.664** [−2.643] | 0.008*** [6.644] |

| NAM | −0.735** [−2.021] | −0.102* [−1.672] | 0.132** [2.342] | 0.485*** [3.894] | −0.030 [−0.694] | |

| NER | 0.179*** [5.306] | 0.016 [0.350] | 0.152*** [4.880] | −0.117 [−0.739] | ||

| NGA | −0.961*** [−2.726] | −1.389*** [−3.824] | 0.082** [2.667] | −0.130 [−1.149] | −153.015*** [−4.639] | 0.096* [1.990] |

| SEN | 0.260** [2.408] | −0.104** [−2.412] | −0.076*** [−3.021] | 0.245*** [3.672] | ||

| ZAF | −0.505*** [−2.734] | 0.100*** [4.999] | 0.130** [2.228] | 0.519*** [6.666] | ||

| SDN | 1.172*** [3.700] | −1.620*** [−3.732] | −0.124* [−1.762] | −0.170*** [−5.273] | −3.626** [−2.461] | −0.637*** [−6.614] |

| TZA | −1.216** [−2.272] | 0.583*** [7.377] | 0.064*** [4.530] | −0.237*** [−2.742] | −34.609*** [−3.288] | −0.159** [−2.050] |

| TGO | 2.095*** [4.606] | 0.419*** [3.588] | −0.071** [−2.517] | −0.710*** [−3.652] | 13.359*** [3.074] | −0.046 [−0.466] |

Note. See Table 1 and equation 6 for the country and variable descriptions. “χ2

SC (2) is the F-statistic of Breusch-Godfrey serial correlation (L.M.) test of order 2. Arch (1) is the F-statistic of the heteroskedasticity test: ARCH of order 1. These results are authors’ calculations using Eviews 9.

p < .01. **p < .05. *p < .1.

Acknowledgements

The authors are thankful to the editorial office and four anonymous reviewers for their valuable comments.

Author Contributions

DFK designed the article, wrote the methodology, performed the econometric analysis, and discussed the results. YL drafted the concepts, oversaw the investigation and drafted the conclusion. YTG drafted the article, interpreted the data, discussed the results and policy implications. MGRN has compiled and analyzed the data, and drafted the literature review. FEG analyzed the data, drafted and revised the article. AJRE acquired the data, drafted and revised the article. All authors read and approved the paper, and are accountable for all aspects of this work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Henan University funded this work under the postdoctoral research grant FJ3050A0670233.