Abstract

Throughout the world, the implementation of innovative strategies to improves organizational performance is widely accepted. Therefore, it is becoming more and more common for companies, especially in developed countries, to implement such practices as opposed to emerging economies where their implementation is very uncommon. To understand this phenomenon, the objective of this paper is to analyze the role of innovation in the relationship between business sustainability and organizational performance in the context of an emerging economy. To achieve this goal, the study conducted a 73 items online questionnaire survey aimed at Colombian company managers, which was designed on a Likert scale from 1 to 7 and was open from March to October 2021. A total of 293 managers from an equal number of medium and large companies from different economic sectors in Colombia were surveyed using non-probability sampling techniques. The information was then analyzed using a Structural Equation Model. The results show that innovation plays a very limited positive role in the relationship between business sustainability and the companies organizational performance. Likewise, the results also indicate that companies give little or no importance to the circular economy practices as an innovation strategy that contributes to environmental care and better organizational performance.

Plain Language Summary

This paper analyses the role of innovation in the relationship between business sustainability and organizational performance in the context of an emerging economy. To achieve this goal, the study conducted a survey aimed at Colombian company managers. In total, 293 managers from an equal number of medium and large companies in Colombia were surveyed using non-probability sampling techniques. The data were analyzed using a Structural Equation Model. In general, it was found that: (i) innovation and business sustainability have a positive impact on firm performance, (ii) firms that use innovation to create value for their stakeholders achieve better competitive and sustainability capabilities, (iii) the proposed model showed that business sustainability has a greater direct relevance on organizational performance than innovation, and (iv) companies implement few circular economy practices as a strategy to contribute to the sustainability principles. The findings of this study could be used by academics, entrepreneurs, and public policy makers, to develop strategies to stimulate innovation practices in companies given that many of the innovation practices identified are widely used by companies in developed economies due to the significant impact they have on the environment, their organizational performance, and their competitive capacity. Although the research included only medium and large companies from different sectors in Colombia which is an economy that over the last 15 years has been characterized by its recognized stability in the Latin American context. Therefore, the findings may not apply to a wider context.

Keywords

Introduction

At the global level, there is consensus on the negative impacts that many of the company’s current production and consumption practices have generated on the environment, society, and economy (Anand & Sen, 2000; Brand et al., 2021; Helne, 2021; Millar et al., 2019; Vlek & Steg, 2007). As a result, , society is increasingly pressuring organizations to make sustainability commitments. To respond to these demands, companies are increasingly thinking about how to generate positive impacts on key areas for society and the planet, rather than how to reduce their negative impacts (Dyllick & Muff, 2016). They can also innovate in their products, processes, and business models (Nidumolu et al., 2009) as this allows them to be sustainable while improving their productivity and thus e their profitability (Manogna & Mishra, 2021; North, 2005).

In this context, companies in emerging economies have great opportunities for growth thanks to the rapid advancement of technology and the increased investment, research, and development in many of these countries (Alam et al., 2019; Sassanelli & Terzi, 2022). However, they must face challenges such as the effects of COVID-19, the turbulent environments, the availability and use of technology and generation of innovation, low productivity, a strong emphasis on the production of natural resources with little added value, and problems related to the well-being of workers and communities, climate change and environmental pollution, among others (Bernal et al., 2021; Gölgeci et al., 2019; Morgan et al., 2021).

In the academic literature there is abundant research that jointly analyzes the relationship between corporate sustainability, innovation, and organizational performance in companies in developed countries. The results show that in medium- and long-term decisions, there is a significant positive relationship between these three variables, while in emerging economies there is little research and the results of these relationships are not conclusive (Hanelt et al., 2017; Maletič et al., 2016; Omar et al., 2017; Tahu et al., 2020). Regarding the latter, the study of Mady et al. (2022) on the role of innovation in corporate sustainability of Chinese companies and that of Gülsoy and Ustabaş (2019) on corporate sustainability initiatives with gender equality in Turkish companies show the importance of innovation in the social and environmental aspects of corporate sustainability as a strategy to improve the organizational performance of companies. In this regard, Larbi-Siaw et al. (2022) consider that research on the relationship between business sustainability, innovation, and organizational performance in emerging economies being very scarce, recent, and with contradictory results, is relevant and necessary.

This phenomenon justifies further research on the subject in the context of these economies where companies are characterized by a short-term vision, poor environmental culture, significant wage inequality, low propensity to invest in environmental, social, and innovation issues (Bernal et al., 2020) and the countries have permissive legislation with environmentally harmful activities, lack of labor protection, and few incentives to invest in technologies and innovation (Bernal et al., 2021; Larbi-Siaw et al., 2022).

On the other hand, according to Fernando et al. (2019) and J. Zhang and Wu (2013) research that analyzes the moderating role of innovation in the relationship between business sustainability and organizational performance is quite limited or almost non-existent despite that currently, in the academic, business, and governmental scenario, the importance of eco-innovation practices as strategies to achieve better business performance with value creation for stakeholders is widely recognized. Therefore, these authors call attention to the need for further research on this topic.

To contribute to this research gaps, this study posed the following research question: Does innovation have a positive moderating effect on the relationship between business sustainability and organizational performance of firms in emerging economies? To answer this question, we applied a 73-item online questionnaire survey to 293 medium and large forms in Colombia (South America) from March to October 2021, which were selected using non-probability sampling techniques. We then used a structural equation model (SEM) to determine the moderating role of innovation in the relationship between business sustainability and organizational performance.

Our research enriches and extends the literature on the role of innovation in firm performance and in different ways. First, this study is in line with previous studies that point to the need to better understand the moderating role of innovation in the relationship between business sustainability and organizational performance (Fernando et al., 2019; Y. Zhang et al., 2013). Second, it is one of the first studies to provide empirical evidence on the relationship between these three variables in firms of emerging economies. Third, the results of the study contribute to the debate on the importance of sustainable practices and innovation as strategies to address the challenges of climate change and the societal well-being, fields on which the results of recent research conducted on the subject are inconclusive (Hermundsdottir & Aspelund, 2021). Our findings suggest that innovation plays a positive mediating role in the relationship between business sustainability and organizational performance of the companies, which is in line with previous studies (Bos-Brouwers, 2010; Maletič et al., 2016; Omar et al., 2017; Tahu et al., 2020). They also reveal that companies give little or no importance to the circular economy practices as an innovation strategy that contributes to environmental stewardship and better organizational performance.

The following sections of this paper are structured as follows: Section 2 reviews the literature on business sustainability, innovation, and organizational performance. Section 3 presents the methodology used in this study. Section 4 shows the results. Section 5 discusses the findings in light of theory, and Section 6 draws conclusions.

Literature Review

Relationship Between Business Sustainability and Organizational Performance

In a broad sense, sustainability represents a balance between the social, economic, and environmental aims to contribute to the efficient use of resources in the long term and thus allow sustainable development (Dabija, 2021; Mensah, 2019; WCED, 1987). For many experts, this balance is complemented by institutional sustainability which refers to the awareness that companies have about the importance of sustainable practices, compliance with standards, and staff training in issues related to climate change, circular economy, and value creation for all stakeholders (Bocken & Geradts, 2020; Dyllick & Muff, 2016; Larbi-Siaw et al., 2022; Silvestre & Ţîrcă, 2019).

Particularly with regard to the environment, recently, with the rise of the circular economy an economic model that proposes not only to restore the damage caused to the environment during the process of acquiring raw materials, but also to reduce the waste generated throughout the production process and the useful life of the product, new business models have emerged, which in addition to being an important source of competitive advantage, allow companies to improve their results in terms of sustainability performance (Geissdoerfer et al., 2018; Rizos et al., 2016) and thus contribute to the achievement of the Sustainable Development Goals through economic growth and the well-being of their employees and society at large (Kalar et al., 2021; Sarfraz et al., 2021; Schroeder et al., 2019; Tahu et al., 2020). Thanks to these benefits, companies from various economic sectors (e.g., Casallas-Ojeda et al., 2021; de Jong & Mellquist, 2021; Riba et al., 2020; van Boerdonk et al., 2021) have started to apply it as part of their strategies aimed at achieving sustainability (Geissdoerfer et al., 2017; Murray et al., 2017).

From the business point of view, the balance between the social, economic, and environmental aims is called business sustainability (Ashrafi et al., 2018; Dyllick & Muff, 2016; Kantabutra & Ketprapakorn, 2020; S. Lee, 2020). This implies that companies must not only guarantee profitability to investors but also care for the environment and the well-being of their workers, which ultimately reflects their organizational performance. In the academic literature, there are numerous studies on business sustainability and its relationship with the organizational performance. Some of them have mainly focused on analyzing the relationship between business sustainability and external factors such as regulations and public policies, competitive pressure, and reputation (Bammens & Hünermund, 2020; Du et al., 2022; García-Granero et al., 2020; Li et al., 2020). Others have analyzed the benefits obtained by companies that apply sustainability-oriented practices (Du et al., 2022; J. Lee & Pati, 2012; Medne & Lapina, 2019) or the relationship between business sustainability and their competitive capability or performance (Hermundsdottir & Aspelund, 2021); however, their findings are diverse (Cai & Li, 2018; Hussain et al., 2018; Rezende et al., 2019), particularly those concerning indicators of the social and environmental dimensions of sustainability, which in many cases are not reflected in the organizational performance of the companies (Saxena et al., 2021), a situation that is more evident in companies of emerging economies (Bernal et al., 2020; Larbi-Siaw et al., 2022).

In general terms, the literature that analyze the relationship between business sustainability and organizational performance in companies from developed economies state that they have a long-term vision and also highlight the existence of a positive relationship between social and environmental practices and business performance, thanks to the fact that these practices improve productivity, generate labor welfare, reduce waste and risks, improve innovation capabilities, create synergies between companies and their stakeholders, and improve reputation which is reflected in better financial results for companies (Doni & Fiameni, 2023; S. Lee, 2020). On the other side, according to Dommerholt et al. (2021), in emerging economies many companies are convinced that being environmentally friendly requires large investments that involves demands that many companies cannot meet, and which are not recoverable in the short term and the economic benefits are not guaranteed. However, for these authors, there are investigations that show that investments in innovation and environmental protection are profitable in the short term and therefore the authors suggest more studies on the subject in emerging economies that contribute to a better understanding of the subject.

Innovation Role in the Relationship Between Business Sustainability and Organizational Performance

Since the publication of the Brundtland Report, there has been great interest in analyzing the relationship between innovation and business sustainability and the relationship between innovation and organizational performance, as innovation is considered a key strategy to address the different aspects of business sustainability and organizational performance (Maier et al., 2020; Melane-Lavado & Álvarez-Herranz, 2018). According to Mahjoub (2023), De la Vega Hernández & Paula (2021), and Kuncoro and Suriani (2018), innovation is directly linked to business sustainability, for which companies develop strategies that include diverse practices associate to both aspects to be competitive and sustainable. In this regard, Du et al. (2022) and Medne and Lapina (2019), argue that organizations that stimulate innovation and change as a strategy to generate value for each one of the stakeholders and constantly care for the environment are more likely to be competitive and sustainable than those that do not.

Commonly, innovation oriented to business sustainability is carried out within companies and with their own resources through the so-called innovation of products, processes, and organizational initiatives. However, many companies, in addition to taking advantage of their own resources, resort to collaborative work as an innovative strategy with other actors in the external environment (e.g., other companies, experts, and government or academic entities), which often allows them to obtain better results (Behnam et al., 2018; Chesbrough & Bogers, 2014; Greco et al., 2021). This collaborative innovation is widely recognized in companies within developed economies, but it is very limited in those within emerging economies (Baptista et al., 2020; Schiuma & Carlucci, 2018).

In the academic field, few authors have studied the relationship between innovation, business sustainability and organizational performance in an integrated way. Despite this, it has been identified that sustainable innovations enable companies to develop new products, share information with stakeholders and cooperate with their suppliers to achieve better environmental performance (Bos-Brouwers, 2010; Doni & Fiameni, 2023; Larbi-Siaw et al., 2022). Likewise, it has been found that implementation of circular economy practices in the supply chain has a positive influence on firm performance (Tahu et al., 2020) or that eco-innovations supported by information systems can improve organizational performance (Hanelt et al., 2017; Omar et al., 2017).

In this regard, Doni and Fiameni (2023), Larbi-Siaw et al. (2022), and Mady et al. (2022) highlight the importance of clarifying that there is a consensus on significant positive relationships between innovation and the resolution of social and environmental issues for highly innovative companies. However, these relationships seem to be absent in companies with a low innovative culture and limited environmental commitment, especially those that prioritize short-term business goals. This situation is very typical of companies in emerging economies, where there is a perception that sustainability policies and practices produce costs that exceed the financial benefits they generate. higher than the financial benefits they generate (Doni & Fiameni, 2023).

On the other hand, according to Hermundsdottir and Aspelund (2021) and Hussain et al., (2018), although in related literature there are studies that analyzes the relationship between innovation, business sustainability, and organizational performance, they focus on environmental aspects, obviating the social aspects that, as is well known, are a fundamental component of sustainability. Therefore, for these authors, it is necessary to carry out new research on this relationship in which innovation involves economic, social, and environmental aspects together. Moreover, as stated by Doni and Fiameni (2023), Fernando et al. (2019), and Y. Zhang et al. (2013)., despite the fact that several studies recognize the moderating role of the innovation in the relationship between business sustainability and organizational performance as a business strategy to respond to the constant, complex, and uncertain changes in the environment, very little research has analyzed this moderating role and therefore, further research is needed in this field for a better understanding by academics, managers, businessmen, and public policy makers in terms of sustainability and business competitiveness.

Methods

The data for this study were obtained from an online survey that aimed to analyze the relationship between business sustainability practices and organizational performance moderated by innovation processes in medium and large companies in Colombia, a country that recently entered to the OECD (April 2020), therefore the sustainability and innovation are relevant aspects to work on. We selected these companies for several reasons: (i) they have a high degree of formality, (ii) they are the largest contributors to the gross domestic product (GDP), (iii) they have the highest probability of investment for innovation and incorporation of new technologies and the most demanding of qualified human talent (DANE, 2023), and (iv) the results of the variables investigated are comparable with those of companies in developed economies.

The questionnaire, which was designed specifically for this study based on the literature and researchers’ expertise, consists of 73 items with Likert scale option response from 1 to 7 where 1 represents “Strongly disagree” and 7 represents “Strongly agree” (Byrne, 2010). It is organized into four sections: general information about the company and questions related to the innovation, business sustainability, and organizational performance activities that the company had developed in the last 5 years. Prior to its application, the questionnaire was subject of the evaluation of three experts: a psychologist specialized in questionnaire design and two economists with expertise in innovation and business sustainability. It was then administered to a pilot sample of managers from medium and large companies, which allowed adjustments to be made, ultimately, a final validated version of the questionnaire to be obtained. The information was collected by the researchers with the support of young researchers from the International School of Economic and Administrative Sciences (Universidad de La Sabana) between March and October 2021.

A total of 750 managers from the same number of companies belonging to different economic sectors were invited, and the objective of the research was explained to them. Of the companies invited, which were selected by non-probabilistic sampling, 552 responded to the survey, achieving a response rate of 74%. However, after reviewing and purging the database, only 293 valid surveys remained (53% out of the answered questionnaires), which are the basis for the results of this research. This sample size is significant considering that the companies participating in the research are the largest and most representative of their respective economic sector. Also, because in Colombia the response rate to the survey is very low (less than 40%), particularly in sensitive issues such as innovation and sustainability.

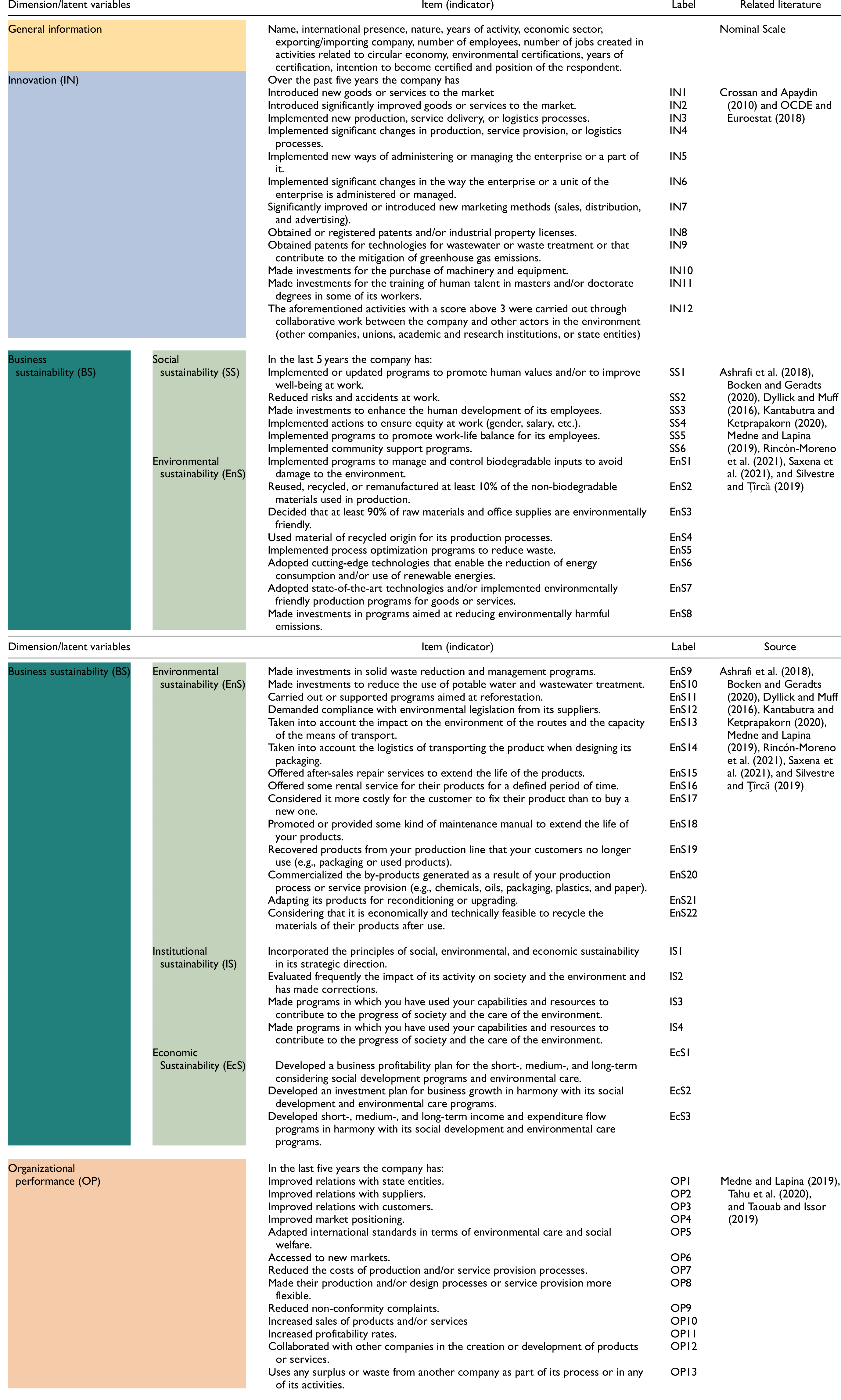

For the analysis, the following were taken as independent variables: (a) the innovation composed of 12 items (questions 11–22 of the survey) and (b) the business sustainability made up of 35 items, organized in four dimensions, namely: (i) social sustainability made up of 6 items (questions 23–28 of the survey), (ii) environmental sustainability made up of 22 items (questions 29–50 of the survey), (iii) institutional sustainability made up of 4 items (questions 51–54 of the survey), and (iv) economic sustainability made up of 3 items (questions 55–57 of the survey). The organizational performance was taken as a dependent variable, which was made up of 13 items (questions 58–70) of the survey. Table 1 presents the dimensions with their respective items and the label assigned to each variable. It is also included in the last column the sources used to define the variables included in the study. It should be noted that the validation of the second-order constructs defined for this study is based on the literature review (described above) on innovation, sustainability, and organizational performance.

Items of the Evaluated Variables.

For data processing, the following were used: (i) Reliability and Validity Analysis (RVA) (Chronbach’s alpha), (ii) Unidimensionality Analysis (UDA), and (iii) Exploratory Factor Analysis (EFA), using IBM software SPSS Statistics (Statistical Package for the Social Sciences) V21. To perform the Confirmatory Factor Analysis (CFA) of the variable’s innovation, business sustainability, and organizational performance (called latent variables), and the development of the Structural Equations Model (SEM), the AMOS software of SPSS V25 was used. The SEM was used because it is a multivariate statistical analysis method that allows identifying the most relevant items in the variables under study (innovation, business sustainability, and organizational performance) and identifying patterns in the relationship between these studied variables, as well as the mediation of one of these variables (the innovation) in the relationship with the other variables (business sustainability and organizational performance). It is more robust than multiple regression and ANOVA and is widely used for qualitative data processing. It should be noted that the Covariance based Structural Equation Modeling (CB-SEM) with SPSS V25, and Partial Least Squares (PLS) versions were used together with consistent Partial Least Squares based Structural Equation Modeling (PLSc-SEM) with Smart PLS4 with a significance level of 5% (p= 0.05), in order to contrast the results in comparison with the three models. It is important to underline that despite these advantages, SEM also have certain limitations among which are: it requires large samples (n > 200) and it is recommended to use it when similar studies already exist. In addition, for each observed variable, there must be at least 10 cases, which represents a challenge for researchers (Nachtigall et al., 2003; H. Zhang, 2022).

Results

Unidimensionality Analysis (UDA)

This analysis was carried out to determine whether each of the indicators (items) converge toward the respective dimension (known as latent variables), which in this case are innovation, business sustainability, and organizational performance. For this purpose, the Kaiser Meyer Olkin Index (KMO) was used, which suggests values above 0.8 to ensure adequate assessment (Byrne, 2010; Hair et al., 1999; Hoyle, 2015). From this analysis, it was found that the innovation presents a KMO of 0.839, but not all indicators are contributing to a single factor but are disaggregated into two factors which have a representativeness of 48%. Concerning the business sustainability, the KMO is 0.96, but the indicators that are grouped into four dimensions or first-order latent factors are only relevant in three dimensions. For its part, the organizational performance has a KMO of 0.923, but with a contribution to two factors (see Table 2).

KMO Indices for Innovation, Sustainability, and Organizational Performance.

Reliability and Validity Analysis (RVA)

To assess the reliability of the data, Cronbach’s alpha coefficient was used, which for the whole of the survey data applied was .977, indicating a high correlation between all the items used to assess the innovation, business sustainability, and organizational performance, as the values above .7 are indicators of an appropriate level of reliability (Taber, 2018).

To assess the validity of the model, the EFA was used, which showed that the data are grouped into about 10 factors, and 6 latent variables of first and second order are expected; however, in 2 of them, the indicators do not contribute to them. The best evaluated variable is social sustainability because all its indicators and some of the other variables contribute to this factor. Organizational performance is also identified as well evaluated by its indicators as all, but one (OP13, see Table 1) contributes to the factor. For innovation, and environmental sustainability, the factors are distinguishable, but their indicators are contributing to two different factors. Economic sustainability is also identified as a differentiable factor. Finally, the institutional sustainability variable is not identified as a differentiable factor because its four indicators contribute to different factors. This would indicate a possible revision of these metrics for this variable.

Due to the above and consistent with the UDA information, three indicators (IN8, IN9, and IN10—items in blue in Table 1) are suppressed in the innovation variable. Similarly, for the environmental sustainability variable, four indicators are suppressed (EnS15, EnS16, EnS17, and EnS22—items in green in Table 1). For the institutional sustainability variable, four indicators are deleted due to a low impact factor (IS1, IS2, IS3, and IS4—items in green in Table 1). Finally, only one indicator was removed from the organizational performance variable (OP13—item pink in Table 1).

Confirmatory Factor Analysis (CFA)

CFA was performed for each of the three variables under investigation, according to the following considerations: innovation and business sustainability (in their three cleaned dimensions) were considered independent variables, and organizational performance was a dependent or an outcome variable. In doing so, we sought to respond to the following hypotheses:

For this analysis, the following tests were used: Chi-square or CMIN (minimum discrepancy), which defines the degree of statistical likelihood and measures the level of fit of the model hypothesis test (Hoyle, 2015; Raykov & Marcoulides, 2006), CMIN/DF, which is an index of the adjusted Chi-square dividing by the degrees of freedom (DF) of the model (Byrne, 2010) and the root mean square error of approximation (RMSEA) which sought to explain how well the model could fit the population covariance matrix, indicating the average residual correlation, which must be less than .080 to be accepted and less than .050 to identify a very good fit (Hoyle, 2015). Also, the relative-of-fit index (RFI), the Incremental fit index (IFI), normative-of-fit index (NFI), and the Tucker-Lewis index (TLI) explain the level of variance and covariance fit of the matrices, the independent of sample size (Manzano Patiño, 2018; Raykov & Marcoulides, 2006), and the comparative fit index (CFI), which determines whether the hypothesis of the model adequately defines the sample data. To be accepted, these indicators (RFI, IFI, NFI, TLI, and CFI) must have a minimum value of 0.90 (Hoyle, 2015).

Confirmatory Factorial Analysis (CFA) for Innovation (IN)

The results of the CFA analysis for the variable innovation show the fulfilment of the CMIN/DF, RMSEA, and NFI, RFI, IFI, TLI, and the CFI indices suggested by the researchers, for the sample of companies after five iterations (Table 3), with loads for each of the four indicators.

Fit Index and Unstandardized Coefficients for the CFA Iterations for Innovation.

Table 4 shows that the items used to evaluate the innovation variables are valid and reliable because the composite reliability—CR [degree to which the different indicators contribute to the evaluated variable, in this case innovation] are values greater than .7 for the CB SEM and .8 for the PLS and PLSc (Dash & Paul, 2021), and the average variance extracted AVE, which determines the level at which the indicators define that variable are values greater than .7 for the CB SEM and .5 for the PLS SEM (Dash & Paul, 2021; Hair et al., 2017).

Validity and Reliability Indices of the SEM Models for Innovation.

The results in Table 5 show that, according to the three versions of the SEM, only four items related to innovation are highly significant (those with values greater than .5). These items encompass the introduction of new goods or services to the market, the implementation of new production, service delivery, or logistics processes, the adoption of significant changes in production, service provision, or logistics processes, and the implementation of substantial changes in the administration or management of the enterprise or its units. This indicates that innovation in the companies participating in the study is not very relevant and their emphasis is on process improvement and not on the introduction of new products or services.

Most Relevant Aspects Regarding Innovation in the Companies According to the Different Versions of the SEM.

Confirmatory Factor Analysis for Business Sustainability

For the business sustainability variable, the data in Table 6 show that after 14 iterations a good fit is obtained for all CMIN/DF, RMSEA, NFI, RFI, IFI, TLI, and CFI indices. It also presents the initial and final values of the evaluated indices.

Fit Indices, Unstandardized Coefficients for the CFA Iterations for the Dimensions of Business Sustainability.

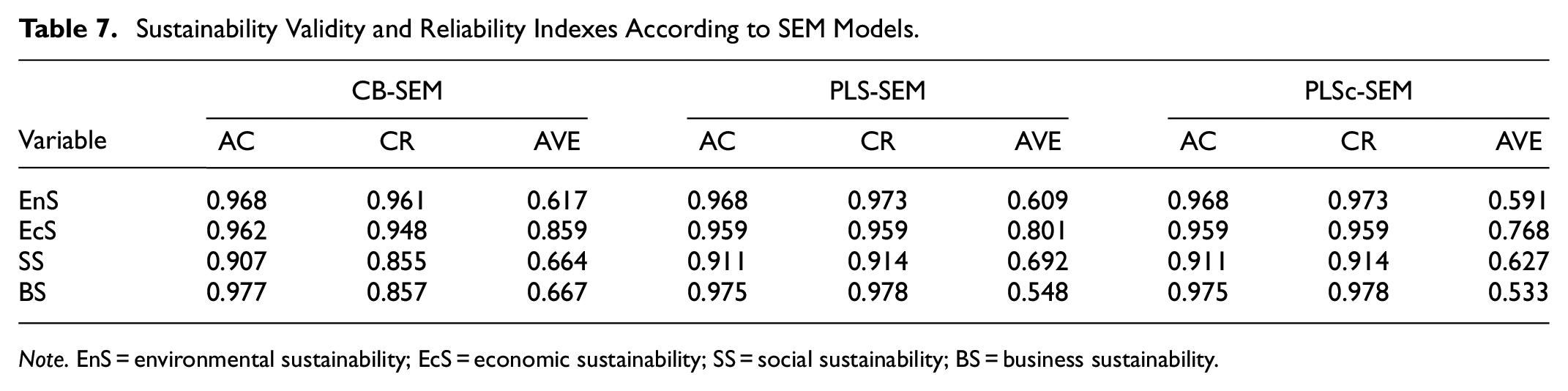

Table 7 shows that the validity and reliability of the items used to assess business sustainability in its three dimensions (environmental, economic, and social), according to the different versions of the SEM, is significant.

Sustainability Validity and Reliability Indexes According to SEM Models.

Note. EnS = environmental sustainability; EcS = economic sustainability; SS = social sustainability; BS = business sustainability.

The CFA analysis to evaluate corporate sustainability in its three dimensions (social, environmental, and economic), shows that of the 26 initial indicators assessed, only 13 of them have values above 0.66, which indicates that only these indicators have a high impact factor on this variable (see Table 8). Regarding social dimension of sustainability, the following stand out: investments to enhance the human development of its employees and to implement or to update programs to promote human values and/or to improve well-being at work. In the environmental dimension, the following stand out: the investments in solid waste reduction and management programs, investments in programs aimed at reducing environmentally harmful emissions and investments to reduce the use of potable water and wastewater treatment. In the economic dimension, all the aspects evaluated are considered very relevant and of greater importance, which indicates that companies give more importance to economic aspects than to social and environmental aspects.

Relevance of the Items Evaluated for Business Sustainability (BS) According to the Different Versions of the SEM.

Confirmatory Factor Analysis for Organizational Performance

The results of the CFA analysis for the organizational performance variable show that the variable is being very well measured by these indicators, since the CMIN/DF, RMSEA, NFI, RFI, IFI, TLI, and CFI indices present outstanding values after nine iterations (Table 9).

Fit Indices, Unstandardized Coefficients for the CFA Iterations for the Organizational Performance Dimensions.

Table 10 shows that the items used to evaluate the organizational performance variable or construct are valid and reliable.

Validity and Reliability Indexes for Organizational Performance According to the SEM.

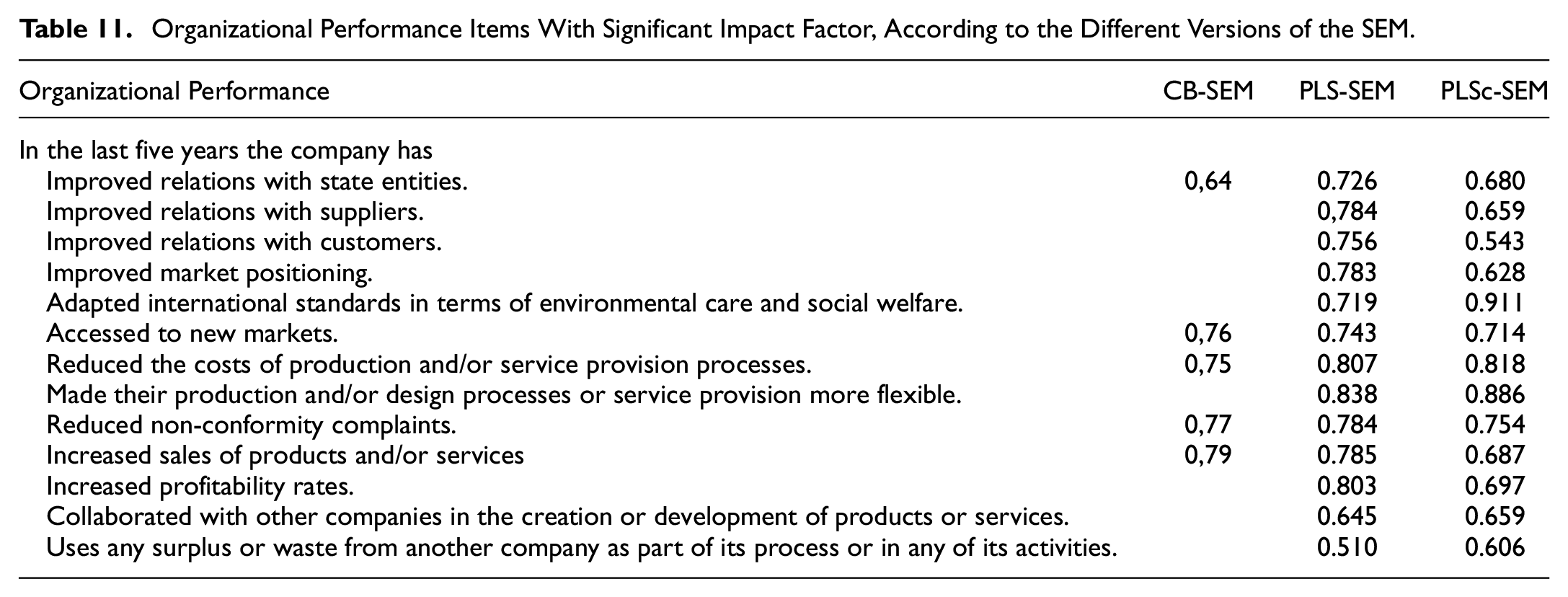

Table 11 shows that of the 12 items used to measure organizational performance, only 5 were considered relevant because their impact factor was above 0.64: increased sales of products and/or services reduced non-conformity complaints, accessed to new markets, reduced the costs of production and/or service provision processes, and improved relations with state entities. This confirms the emphasis of the economic aspect by the companies in relation to the social and environmental aspects.

Organizational Performance Items With Significant Impact Factor, According to the Different Versions of the SEM.

Structural Equation Model for the relationship between Innovation, with Business Sustainability, and Organizational Performance

Based on the results obtained previously and using an CB-SEM, we analyzed (i) the impact of innovation and business sustainability on organizational performance and (ii) the mediating role of innovation in the relationship between business sustainability on organizational performance. Regarding the first case, the CB SEM shows that not only the proposed fit indices are adequate (Table 12).

Fit Indices, for the Structural Model Iterations for the Innovation and Business Sustainability Dimensions in the Organizational Performance.

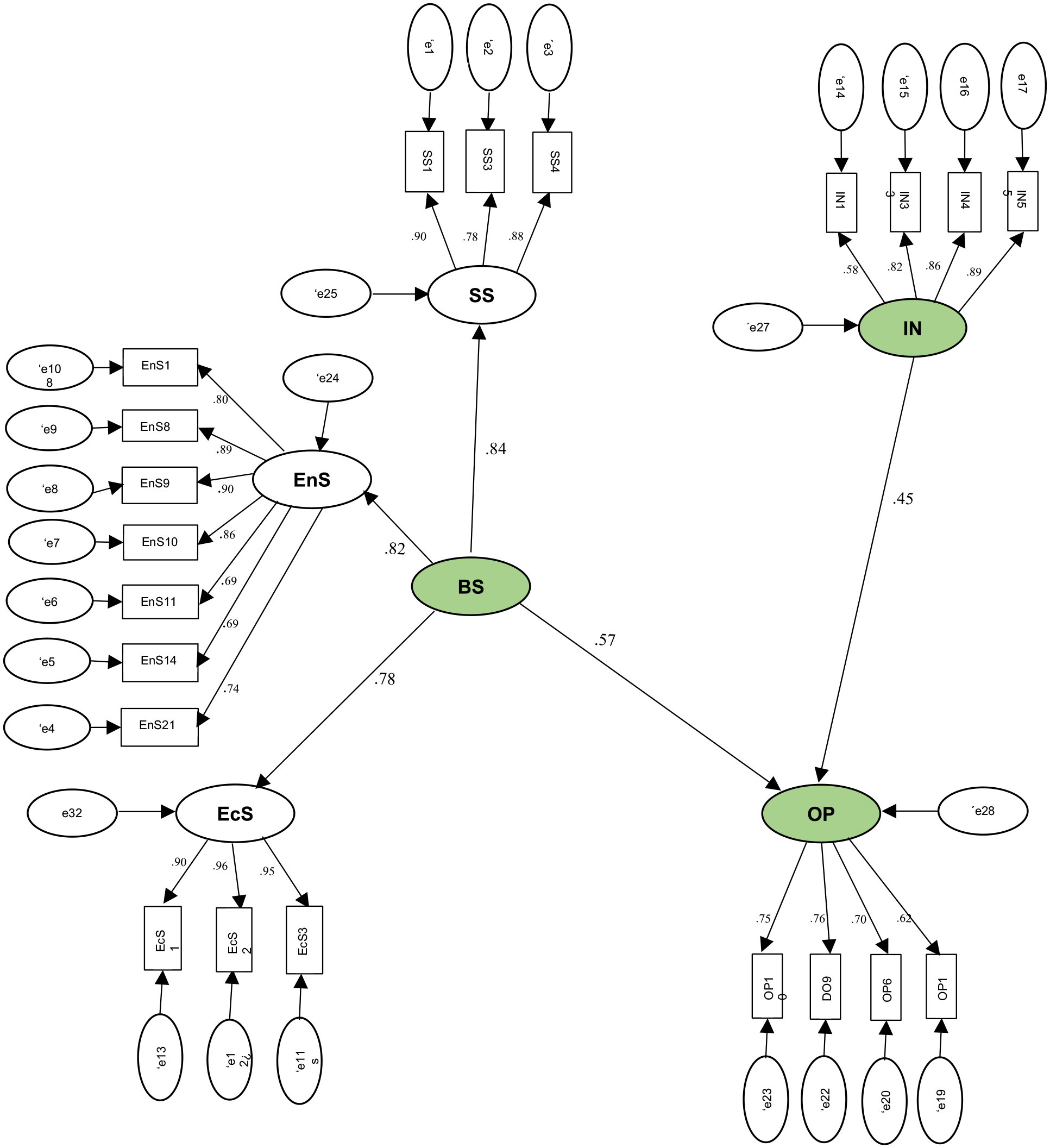

Figure 1 shows that, when the impact of innovation and business sustainability on organizational performance is analyzed independently, business sustainability has a greater impact (0.57) on organizational performance than innovation (0.45). This indicates that entrepreneurs give more importance to environmental aspects than to those related to innovation.

CB SEM of the relationship between innovation, business sustainability, and organizational performance.

As for the second analysis, the mediating role of innovation in the relationship between business sustainability and organizational performance, after three iterations that involved eliminating one indicator from those evaluated by innovation (item IN4) and one from organizational performance (item OP1), acceptable indicators were obtained from this adjusted model (Table 13).

Fit Indices for the Structural Model Iterations for the Dimensions of Business Sustainability and Organizational Performance, as Moderated by Innovation.

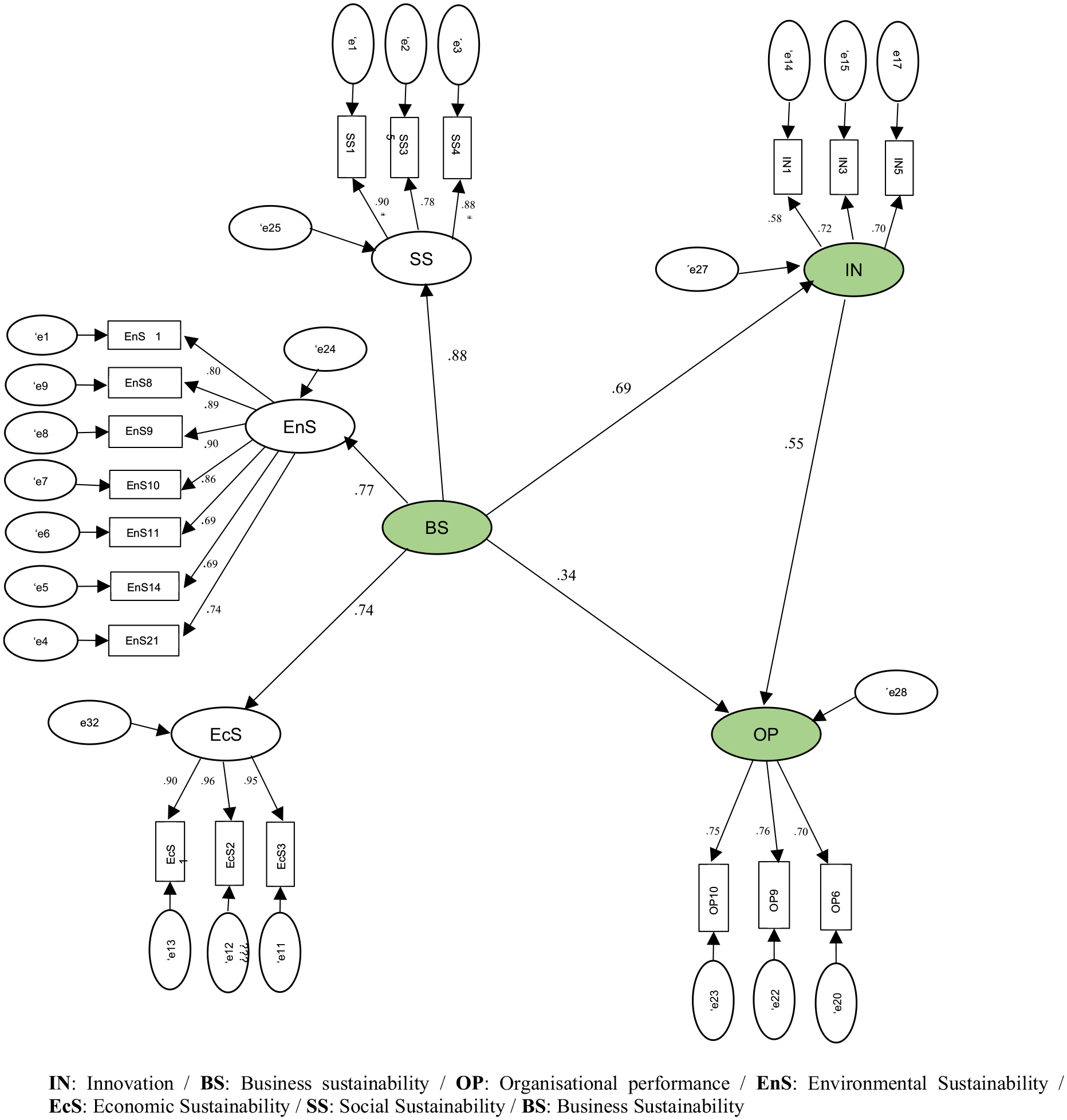

The data presented in Figure 2, which examines the relationship between business sustainability and organizational performance moderated by innovation using CB SEM, indicates that the effect of innovation on this relationship is relatively limited. While the impact of innovation on organizational performance increases from 0.45 (when is analyzed without mediation) to 0.55 with mediation, the impact of business sustainability decreases from 0.57 (without mediation) to 0.34 with mediation. This limited significant impact may be attributed to the perception among business leaders regarding the high investments required to enhance sustainability through innovative practices. In addition, this situation is largely influenced by the short-term perspective often adopted in decision-making processes within companies in emerging economies.

SEM of the relationship between business sustainability and organizational performance moderated by innovation.

Discussion

This study analyzes the relationship between business sustainability, innovation, and organizational performance based on a sample of 293 medium and large companies from an emerging economy. Our findings reveal that according to the literature review on research conducted for companies in the context of developed economies, the innovation and business sustainability are key factors to improve the organizational performance and the innovation plays an important moderating role in the relationship between business sustainability and organizational performance. However, the results of the data analysis of this study show that, in the context of emerging economies, this relationship is low, and in some cases null, as mentioned by Doni & Fiameni (2023), Fernando et al. (2019), and Larbi-Siaw et al. (2022), when stating that companies in these economies have a short-term vision that prevents them from investing in innovative and environmental activities because they perceive that this requires high investments without positive effects on financial results.

In accordance with the aforementioned, hypotheses 1 and 2 of the study are partially confirmed, because the impact of this relationship is low, and in general, it is due to the characteristics of the companies in the context of the study, where innovation, environmental culture, and the use of new technologies are not very relevant factors for the business activity (Bernal et al., 2020; Doni & Fiameni, 2023; Larbi-Siaw et al., 2022). Also, hypothesis 3 was much less confirmed than hypotheses 1 and 2, because the effect of innovation as a moderator in the relationship between business sustainability and organizational performance is not very significant and is due to the same reason described above.

In this sense, despite the limited effect of innovation on business sustainability, it was identified that the innovation practices that have the greatest impact on business sustainability are: (i) creating new production or service delivery or logistics processes, or implementing significant changes in these processes, (ii) managing the company or any of its units differently, (iii) introducing new goods or services, and (iv) registering patents and/or licensing industrial property. This confirms the findings of Mahjoub (2023), Du et al. (2022), and Walker et al. (2015) about the benefits of innovation on firm performance and competitiveness, which is positive in a highly competitive, complex, and uncertain environment, particularly in emerging economies where innovation is unusual (Bernal et al., 2021; Gölgeci et al., 2019).

In addition, we found that the economic dimension of sustainability remains the most important criterion for business sustainability relative to the environmental and social dimensions, which is consistent with other studies such as those carried out by Du et al. (2022) and Medne and Lapina (2019). Despite this, the following key aspects were highlighted for the social dimension: (i) to make investments to enhance the human development of their employees, (ii) to create programs to promote human values and/or improve well-being at work, and (iii) to implement actions to ensure equity at work. Our results are consistent with Hestad et al. (2021) and Li et al. (2020) findings, who show that companies achieve better organizational performance when they care about the well-being of their employees and other stakeholders.

Our results also provide empirical evidence about sustainability activities with a greatest impact on the environment. They are: (i) to develop programs focused on reducing and managing solid waste and environmentally harmful emissions, (ii) to make investments to reduce the use of potable water and wastewater treatment, (iii) to adapt their products in a way that allows them to be reconditioned or updated, (iv) to implement programs to manage and control biodegradable inputs to avoid environmental damage, (v) to support programs aimed at reforestation, and (vi) to take into account the logistics of product transportation when designing the packaging of their products. These results demonstrate the importance of companies implementing actions that reduce the impact of their actions on the environment, which has been widely recognized by several researchers in the field (Li et al., 2020; Long et al., 2017; Wang & Berens, 2015).

Finally, the findings show the low importance that companies in emerging economies attach to collaborative work with their stakeholders (Du et al., 2022; Kantabutra & Ketprapakorn, 2020; Silvestre & Ţîrcă, 2019) and other environmental actors, with whom they can collaboratively develop projects (Behnam et al., 2018; Chesbrough & Bogers, 2014; Greco et al., 2021). This finding is relevant because the collaborative work with stakeholders is a key factor for both the innovation and environment processes and it is widely valued by companies in developed economies.

Theoretical Contributions

Although, the literature review evidences that there is abundant research on the relationship between innovation, business sustainability and organizational performance (Du et al., 2022; Mady et al., 2022; Maier et al., 2020; Moradi et al., 2021), in general these studies analyze this relationship in the context of developed economies and in particular in companies and sectors with high propensity to invest in technologies, innovation and environmental commitment, but not in that of emerging economies (Doni & Fiameni, 2023; Du et al., 2022; Fernando et al., 2019; Kantabutra & Ketprapakorn, 2020; Larbi-Siaw et al., 2022; Silvestre & Ţîrcă, 2019). Furthermore, research on the subject is not conclusive, since although because the results of some of them show a direct and positive relationship between innovation, business sustainability, and organizational performance, others indicate that this relationship is not always positive, especially in relation to social and environmental issues (Tahu et al., 2020).

On the other hand, very few studies have analyzed the moderating role of innovation in the relationship between business sustainability and organizational performance, and even less in the context of emerging economies (Doni & Fiameni, 2023; Fernando et al., 2019). In this sense, this research contributes to fill the gap of lack of sufficient empirical information for the understanding of the relationship between innovation, business sustainability, and organizational performance particularly in the context of emerging economies that present different features from those of developed economies.

Managerial Implications

The findings of this study could be used by policy makers to develop strategies to stimulate innovation practices in companies. They should also be discussed and analyzed by academics, entrepreneurs, and public policy makers, given that many of the innovation practices identified are widely used by companies in developed economies due to the significant impact they have on the environment, their organizational performance, and their competitive capacity (Geissdoerfer et al., 2018; Rizos et al., 2016; Sarfraz et al., 2021; Schroeder et al., 2019; Tahu et al., 2020). We recommend companies from emerging countries to emphasize innovative practices such as social innovation that emphasizes labor welfare and its positive implications for companies and their stakeholders; eco-innovation, especially from the open innovation approach, with the participation of different stakeholders to improve its impact on the environment; and circular economy through the implementation of strategies related to reuse or recycling of products or materials, among others activities to enhance sustainability and organizational performance rather than engaging in traditional practices. All these practices can be implemented in companies with little investment and with positive returns in the short, medium, and long term.

Limitations and Suggestions for Future Research

There are some limitations to the present study that warrant consideration. First, the research included only medium and large companies from different sectors in Colombia which is an economy that over the last 15 years has been characterized by its recognized stability in the Latin American context. Therefore, the findings may not apply to a wider context. A reasonable approach to overcome this limitation in the future could be to invite companies from other emerging economies with similar conditions to Colombia’s to participate in the study and to compare the results. A second limitation is that our study includes a relatively small number of companies (293), but with the characteristic of being the most representative in their respective sector of economic activity; therefore, a better understanding of the results could be obtained through a large sample of companies, representative of the country’s economic activity and, hopefully, in which previous experiences in innovation could be evidenced. Likewise, it would be interesting to evaluate whether there are differences in the behavior of the variables analyzed by countries, economic sectors, and company size. This with the purpose of identifying whether the sector of activity and the size of the company are criteria to be taken into account in the case of implementing innovation and sustainability practices in the activity or performance of the companies.

Conclusion

The objective of this study was to examine the relationship between corporate sustainability and innovation-moderated organizational performance in medium and large companies in Colombia. In general, it was found that (i) innovation and business sustainability have a positive impact on firm performance, so firms should focus their efforts on promoting sustainability-oriented activities that are moderated by innovation, and (ii) firms that use innovation to create value for their stakeholders achieve better competitive and sustainability capabilities. Furthermore, the proposed model showed that business sustainability has a greater direct relevance on organizational performance than innovation, which is an important finding of this study, since it has not been reported in the literature that firms can leverage much more business sustainability activities than innovation activities to improve their organizational performance. Also, the study results show that, in general, companies implement few circular economy practices as a strategy to contribute to the sustainability principles. These results are striking because the circular economy practices are widely used in companies in developed economies due to the benefits they provide, not only for sustainability but also for their competitiveness.

Footnotes

Acknowledgements

César A. Bernal-Torres y Luz Elba Torres-Guevara are grateful for the support received to develop this study from the research groups “Innovation and Strategy” and “Business, Economy and Finance”, from the International School of Economic and Administrative Sciences at Universidad de La Sabana in Chia, Colombia. Likewise, all authors thanks the students from the “Seedbed of innovation and knowledge management as competitiveness strategies in organizations,” from the International School of Economic and Administrative Sciences at Universidad de La Sabana for their valuable support to develop this study.

Author Contributions

César A. Bernal-Torres: Conceptualization, Methodology, Validation, Investigation, Writing—Original Draft, Writing—Review & Editing, Visualization. Luz Elba Torres-Guevara: Conceptualization, Methodology, Validation, Investigation, Writing—Original Draft, Writing—Review & Editing, Visualization. Juan Carlos Aldana-Bernal: Formal analysis, Data curation. Yoni Wildor Nicolás-Rojas: Writing—Review & Editing. Tamara Tatiana Pando-Ezcurra: Writing—Review & Editing.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded and supported by the Project “Obstacles to Innovation in the Colombian Manufacturing and Services Sectors (EICEA-115-2018)”, sponsored by the Universidad de La Sabana in Chia, Colombia. Likewise, it was supported by the Escuela de Educación Superior Tecnológica Privada La Pontificia in Ayacucho, Perú.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.