Abstract

Innovation is considered a key driver for long-term success of firms in today’s competitive markets. This study explored the effect of innovation adoption on performance of banks in Ghana. Data for the study were obtained from 450 respondents comprising bank employees and customers in the Kumasi metropolitan area in Ghana. An exploratory factor analysis, confirmatory factor analysis, and structural equation modeling were used to analyze the data via SmartPLS 3 and SPSS V.22. Findings from this study revealed that the innovation dimensions that contribute to bank innovation are organizational, product, process, and marketing innovations. The study further revealed a direct and positive relationship between innovation dimensions (product, marketing, and organizational innovations) and bank performance. In addition, findings from this study showed a positive relationship between innovation capability and the four dimensions of innovation (organizational, product, process, and market innovations). Also, the findings revealed a significant and positive relationship between the dimensions of innovation (market, process, and product innovations) and firm performance. The practical implication is that, choosing the appropriate innovation types can enhance bank performance as well as satisfy customer needs. This study extends the literature on innovation adoption and organizational performance in the financial services from an emerging market context.

Introduction

The concept of innovation is gaining ground and plays a significant role in an increasingly competitive and dynamic banking sector. Banks operate in a volatile industry where “customers’ tastes, product-service technologies, and competitive weapons often change unpredictability” (Miller, 1983, p. 775). To be successful and to obtain stability in performance, banks should not only seek new opportunities but also be highly innovative (Tajeddini et al., 2006). Innovation is essential for achieving a competitive advantage in start-ups and established companies (Lichtenthaler, 2020).

Innovation is considered as a key driver for long-term success of firms in today’s competitive markets (Baker & Sinkula, 2012; Darroch & McNaugton, 2002). Businesses with the capacity to innovate are able to respond to market challenges faster and better than non-innovative companies (Brown & Eisenhard, 1995; Faiña Medín et al., 2016; Miles & Snow, 1978). The right kind of innovation and investments in new technologies and strategies would help banks improve their productivity and general performance and growth (Beck et al., 2012; Stiglitz, 2010).

The banking sector in Ghana has witnessed significant changes in recent times following the liberalization of the financial services sector. Banking in Ghana has undergone many changes in service delivery with the aim of improving the quality of service being provided to the customers. Banks were serving their customers through the manual system, which resulted in long queues to transact business. The other problem faced by many banks in Ghana is that, many people including companies do not accept checks as a payment method. This is because of the time and the inconveniences involved in accepting and depositing checks in company accounts.

There is an intense competitiveness in the banking industry which has raised the competitive landscape to unimaginable heights (Yusheng & Ibrahim, 2019). The number of banks operating in Ghana as of January 2020 stood at 23 (Bank of Ghana, 2018). With an increasing customer acquisition costs, customer expectations as well as high rate of customer defection, banks have realised the need to utilize technology in a way of adopting innovative banking solutions first as a response to increasing competitive pressure and second to enhance their service delivery by reducing cost of operations and also developing stronger relationships with customers to enhance customer satisfaction and loyalty. (Yusheng & Ibrahim, 2019)

Research on innovation has been conducted in a number of industries including export (Dalvand et al., 2015), manufacturing (Alam, 2013; Huhtala et al., 2014; Kalay & Lynn, 2015; Karabulut, 2015; Rosli & Sidek, 2013), construction (Akhlagh et al., 2013), and in different countries across the world.

Studies on bank innovation have been explored in recent times with majority of the studies conducted in the developed economies. Nguyen et al. (2014) investigated satisfaction of customers toward bank card payment service quality in China. Hilal (2015) investigated the technological transition of banks and Information and Communication Technologies (ICT) and their impacts in the banking sector in Lebanon. Uzkurt et al. (2013) examined the mediating role of innovation on the relationship between organizational culture and firm performance in Turkey. Gunday et al. (2011) empirically studied the relationship between innovation types and firm performance in Turkey.

In Africa, more specifically, in Kenya, Ngumi (2014) explored the effect of banking innovations on financial performance of commercial banks, while Lilly and Juma (2014) investigated the influence of strategic innovation on performance of commercial banks. In Ghana, Angko (2013) examined the effect of innovation in bank payment systems; Domeher et al. (2015) also explored financial innovations in the banking sector; Ameme and Wireko (2016) explored the impact of technological innovations on customers’ satisfaction in the banking industry; Yusheng and Ibrahim (2019) explored the effect of service innovation on customer satisfaction and loyalty in the banking sector; Obeng and Boachie (2018) also investigated the effect of IT technology innovation on the productivity of bank employees, while Yusif (2012) investigated different innovation types in the banking sector. There appear however to be little research on innovation and bank performance on the African continent especially Ghana. This study therefore aims at breaching the gap identified as well as contributes to the service innovation literature from developing economy perspective. This article therefore sought to achieve the following objective:

To assess the effect of innovation capability and innovation types on performance of banks in Ghana.

The Concept of Innovation

Innovation is a broad term with several terminologies including “new,” “changes,” “opportunities,” “creative ideas,” “adoption of organization,” and “value creation” (Dadfar et al., 2013: 3). Innovation has been defined as a process of turning opportunities into new ideas (Drucker, 1993; Tidd & Bessant, 2009), the adoption of these ideas within the organization (Damanpour, 1991), and successful application of resulting novelties (Pries & Janszen, 1995) in a way which provides values to the organization. (Dadfar et al., 2013)

Crossan and Apaydin (2010) also defined innovation as the “production or adoption, assimilation, and exploitation of value-added novelty in economic social spheres; renewal and enlargement of products, services, and markets; development of new methods of production, and establishment of new management systems.” Hurley and Hult (1988) mentioned that, “innovation is an aspect of firm’s philosophy and openness toward new ideas.” They added another construct (i.e., the capacity to innovate), which is defined as “the ability of the organization to adopt or implement new ideas, processes, or products successfully.” Lundvall (1985) posits that, “innovation comes from accumulated knowledge and experience and can be an incremental technical change or an upsurge in technical opportunities.” (Prifti & Alimehmeti, 2017: 5)

Also according to Drucker (1988), innovation is “a determined and dedicated work to realize organisational change in economic or social potential.” He stressed that, “innovation is a process of developing organisational growth which can occur in a number of ways, such as better service quality and shorter lead times in non-profit organizations and cost reduction, cost avoidance, and increased turnover in profit-focused organizations” (O’Sullivan & Dooley, 2008: 6). We define innovation based on the definition offered by Hage (1999) as, a new product, a new service, a new technology, or a new administrative practice used by an organization to enhance the delivery of its business or service process. Innovation is thus, “creating the required new products, processes and systems for adapting to changing technologies, markets and models of competition” (Dougherty & Hardy, 1996).

Materials and Hypotheses

Innovation Capability

Adler and Shenbar (1990) stressed that innovation capability enables organizations apply requisite and appropriate technologies to develop new products, meet the market needs, and survive competitions (Rajapathirana & Hui, 2018). It further enables firms manage their capabilities from “supporting to integrating capabilities and from stimulus to successful innovation” (Lawson & Samson, 2001). Dadfar et al. (2013) is of the view that innovation capability is the ability of firms to introduce novel ideas in their product strategy to augment their product portfolio. Dahlgaard-Park and Dahlgaard (2010) explained that to implement innovation processes, firms must “enhance the leadership, people, partnership and organizational capability.” Vicente et al. (2015) opined that, firms that are able to introduce new product or services using a mix of strat he combination of innovation behaviour, strategic capability, and internal technological process. We developed our hypothesis as follows:

Conceptual model and hypotheses of the study.

Relationship Between Innovation Types (Dimension) and Firm Performance

Previous research studies have established a positive relationship between innovation and firm performance (Cho & Pucik, 2005; Gunday et al., 2011; Hernández-Espallardo & Delgado-Ballester, 2009 ; Rajapathirana & Hui, 2018). Some of these empirical findings have shown that, innovation types have significant effect on firm performance in terms of return on investment, market share, competitiveness of firms, and customer value (Neely et al., 2001). Zainal Abidin et al. (2011) report that, despite the high research interest in innovation studies, “the relationship between the multi-dimensional factors of innovation and firm’s performance is limited” (Zainal Abidin et al., 2011). We propose Hypothesis 2 as follows:

Organizational Innovation

Organizational innovation is the extent of introducing change in the way the organization is managed. Rajapathirana and Hui (2018) defined organizational innovation as “implementation of a new organizational method in the firm’s business practice, organization or external relations” (p. 46). Organizational innovation can thus, improve organizational performance through cost reduction, as well as improvement in employee and customer satisfaction (Yusheng & Ibrahim, 2019). Gopalakrishnan and Damanpour (1997) in Zainal Abidin et al. (2011) described organization innovation “as a process of organisational change that directly affects the technical and social systems of an organisation.” This system according to them involves two stages: initiation and implementation. Initiation stage consists of three sub-stages: that is, “awareness of innovation, formation of attitude towards it, and evaluation from organisational standpoint.” The implementation stage also consists of two sub-stages: that is, “trial implementation and sustained implementation” (Gopalakrishnan & Damanpour, 1997).

Empirical evidence suggests a positive link between organizational innovation and firm performance (Chiang & Hung, 2010; Reed et al., 2012). This helps in understanding the types of capabilities firms need to achieve competitive advantage (Camisón & Villar-López, 2012). Yavarzadeh et al. (2015) explored the relationship between organizational innovation and performance in Iran and found that, innovation dimensions including organizational innovation positively influence organizational performance (Rajapathirana & Hui, 2018). We propose this hypothesis as follows:

Product Innovation

The introduction of new product or service which is “significantly improved with respect to features, performance and quality is referred to as product innovation” (Ferrari & Rocca, 2010). Atalay et al. (2013) defined product innovation as “a good or service that is new or significantly improved with respect to its characteristics or intended use.” This includes “significant improvements in technical specifications, components and materials, incorporated software, user friendliness or other functional characteristics” (Atalay et al., 2013). Also, according to Organisation for Economic Co-Operation and Development (OECD; 2005), the product innovation “involves a significant improvement in technical specification, features, component and material, inculcated software, user friendliness, portability, durability and other significant characteristics” (Yusheng & Ibrahim, 2019). Therefore, the quality of a product, its key features, and the way it operates are what is referred to as product innovation.

Johne (1999) asserts that, banks can offer new products/services to customers using innovation. The innovative products banks have introduced over the years include mobile banking, electronic banking, and mobile commerce (M-Commerce). This serves as a way of attracting the unbanked populace to patronize the banking products/services.

To distinguish their offering from other competitors, successful firms most often use product or service innovation to differentiate their product or service from others, giving them a competitive advantage (Martin et al., 2017). Product innovation is thus, considered one of the key factors in the innovation dimensions. In addition to that, product and process innovations play an effective role in organizational performance. Rajapathirana and Hui (2018) found that that innovation (product, process, administrative/organizational) has positive and significant effect on organizational performance in terms of financial, growth, customer, and internal process.

We therefore propose Hypothesis 2b as follows:

Process Innovation

Process innovation “is the introduction of new and enhanced method of production or service delivery (Expósito & Sanchis-Llopis, 2019) by an enterprise that includes significant changes in techniques, equipment, and tool and machine” (Obeng & Boachie, 2018; OECD, 2005). Also, according to the OECD (2005), “process innovation is any organisation that implements a new or significant process of production during the period of organisational review.” It involves small, incremental improvements coming from employees and not necessarily managers. In explaining what constitutes process innovation, the European Union (2013) states that “the outcome of process innovation should be significant with respect to the level of output as increasing quality of product or decreasing cost of production or distribution.”

In considering innovation as a process, Gopalakrishnan and Damanpour (1997) proposed a unitary sequence model to explain the innovation process. They viewed innovation process as a generator or an adopter of innovation. Banking services deals with various processes that lead to delivery of banking services. As such, any process that seeks to enhance the delivery of services to customers would lead to improvement in the business. Fagerberg et al. (2004) thus argued that, process innovation, due to its cost-cutting nature, would have more influence on growth or firm performance (Zainal Abidin et al., 2011). Also, Mabrouk and Mamoghli (2010) in their study, found that, while product innovation improves the profitability of banks, process innovation improves the profitability as well as the efficiency of banks. Therefore, we propose the hypothesis as follows:

Marketing Innovation

Innovation and marketing are two different concepts that complement each other, and the success of one depends on the success of the other. As a discipline, marketing innovation brings together marketing activities in the innovation process. Marketing innovation plays a very important role in ensuring and increasing the success of innovation (Drucker, 2015). Marketing innovation covers all innovation management activities that help to promote market success of new products and services. It is the successful marketing of a new product or service for the satisfaction of customer needs. It anticipates future needs and helps identify future and new market opportunities.

Marketing innovation focuses on meeting customer’s needs and buying preferences by selecting appropriate market mix and market selection (Johne, 1999). It generates significant improvements in some of the marketing elements, including product, price, promotion, and distribution (Ganzer et al., 2017). Higgins (1995) asserts that, “marketing innovation is based on product differentiation, promotion, distribution, market or costs, in this case, the price” (Yusheng & Ibrahim, 2019). Thus, marketing innovation leads to the utilization of new methods, with significant changes in product development, packaging, promotion, positioning, and pricing. Also according to OECD (2005), what marketing innovation does is address the needs of consumers through the establishment of new markets and product repositioning with the aim of increasing sales. Marketing innovation therefore needs to be carried out continuously, as it helps businesses compete effectively and efficiently (Johne, 1999). Banks can therefore achieve growth and profitability when they innovate their marketing activities by introducing innovative ideas, products, and services (see Figure 1). We therefore hypothesize as follows:

Firm Performance, Innovative Performance, and Market Performance

Innovation adoption is expected to influence the performance of organizations in different aspects. Four main dimensions mentioned in the literature to represent firm performance are “innovative performance, production performance, market performance and financial performance” (Narver & Slater, 1990; Yilmaz et al., 2005). Gunday et al. (2011) investigated the relationship between innovation types and firm’s performance. Their findings revealed a positive relationship between innovations and firm performance in manufacturing industries. Innovative performance is thus, considered an important ingredient of other aspects of organizational performance (Gunday et al., 2011). Han et al. (1998) stressed that innovative performance contributes significantly to the growth and performance of firms.

Marketing performance, on the contrary, is seen as an outcome of innovation performance. Gunday et al. (2011) further asserts that, “once innovative performance improves, production and marketing performances will also improve and then through their mediation the financial performance will start to improve.” Innovative performance in the form of new product success is thus linked to increase in sales and market shares, through customer satisfaction and new customer acquisition (Wang & Wei, 2005). We therefore hypothesize that

Method

In undertaking this study, we employed the survey design methodology. A survey design was used with a semi-structured questionnaire as the primary data collection instrument. The survey strategy was chosen due to its ability to sample a larger element. Adopting a convenience sampling technique, the study sampled 500 respondents comprising bank employees and customers of the major commercial banks operating in the Kumasi metropolitan area in Ghana. The research sample (bank employees and customers) were selected randomly from 10 bank branches of the major banks operating in Ghana. Forty respondents were selected from each of the 10 bank branches randomly bringing the total number of respondents (customers) to 400. In addition, 10 employees each were selected randomly from the 10 bank branches making the total number of bank employees 100 respondents.

A self-administered, structured questionnaire was developed, pre-tested, and finally administered to the customers through personal contact by researchers within 8 weeks. The researchers first and foremost used an informed consent form to seek respondents’ permission and assured them of the anonymity and confidentiality of their responses. In all, a total number of 500 questionnaires was distributed to the respondents out of which 450 questionnaires were useful after screening and data cleaning.

A 5-point Likert-type scale coded strongly disagree = 1, to strongly agree = 5 were used to measure the research constructs as recommended in previous works (Danaher & Haddrell, 1996; Delvin et al., 1993; Rajapathirana & Hui, 2018). The questionnaire was in three sections. Section A measured the demographic characteristics of the respondents; Sections B and C measured the other constructs, that is, the independent variables (innovation capability and innovation types) and dependent variable (innovation types and firm performance).

The collected data were coded and screened to remove any outliers or any other variation in the data set. We analyzed the data with the help of the Statistical Package for Social Sciences (SPSS v. 22) and SmartPLS 3. Data validation was done using content and construct validations as discussed later in the article. We also carried out a confirmatory factor analysis (CFA) to “clean the items, assess the suitability of the scales items and assess discriminant validity among the constructs” (Yusheng & Ibrahim, 2019).

Results of the Study

CFA

To do the CFA, the researchers first performed an exploratory factor analysis (EFA) to select the number of factors and loading three items on one factor. Thirty items were initially entered but six of the items were later removed leaving 24 items. Together, these components explained about 93% of the variance in the sample.

Reliability and Validity of Scales

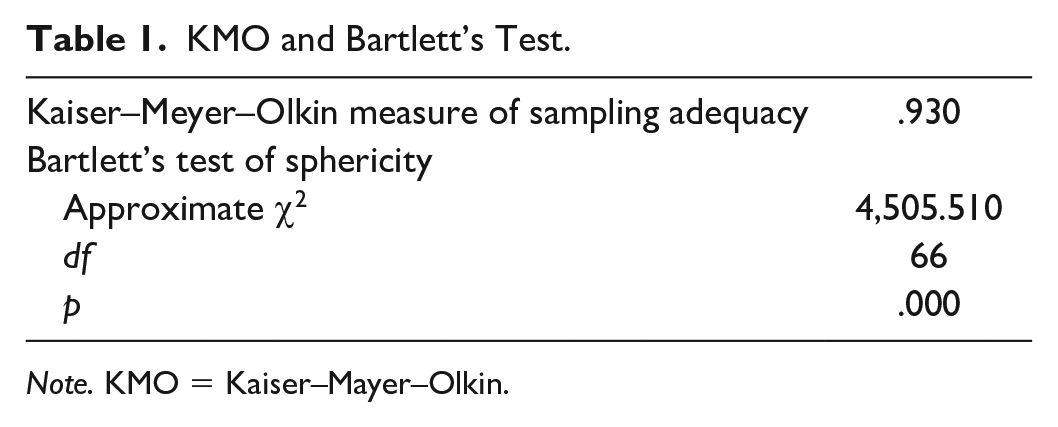

The reliability of the data was ensured through both convergent and discriminant validity. We first conducted an EFA involving 24 items using SPSS v.22. The constructs validity was then checked using Bartlett’s test of sphericity and Kaiser–Mayer–Olkin (KMO; Rajapathirana & Hui, 2018). The KMO’s overall score is considered valid if it is 0.6 or more to perform factor analysis (Özdamar, 2017). The results of both the Bartlett’s test of sphericity and KMO (0.9) revealed that the data were suitable for the factor analysis (Table 1).

KMO and Bartlett’s Test.

Note. KMO = Kaiser–Mayer–Olkin.

The cumulative variance explained is 93% which exceeds the acceptable limit of 60% (Özdamar, 2017). The value of Bartlett’s test of sphericity indicates sufficient correlation between the variables, it shows 4,505.510 and significant (p < .001). The factor loading of each scale exceeds 0.5 (Hair et al., 2011; Ringle et al., 2015). The obtained values therefore show that our scales are valid (see Table 1).

Measurement model reliability and validity

Construct reliability measures “the extent of internal consistency, and is assessed through item factor loadings with acceptable value of 0.70 and Cronbach’s alpha of 0.7” (Hair et al., 2011; Ringle et al., 2015). From Table 2, all of the constructs have item loadings higher than the recommended 0.70.

Item Loading and Construct Reliability.

Note. FL = item loadings; CA = Cronbach’s alpha; CR = composite reliability; AVE = average variance extracted; RHO_A = reliability; IC = innovative capability; Iperf = innovation performance; Mkti = market innovation; Mperf = market performance; Orgi = organizational innovation; Pdti = product innovation; Perf = performance; Pcsi = process innovation.

All the variables returned Cronbach’s alphas above .70 threshold (see Table 2). This means that items used are highly reliable for the measurement of each construct. Construct validity “assesses the degree to which a measurement represents and logically connects the observed phenomenon to the construct through the fundamental theory” (Fornell & Larcker, 1981). “It is assessed through convergent validity and discriminant validity” (Ringle et al., 2015). Convergent validity was also achieved as the average variance extracted (AVE) and composite reliability (CR) are higher than the minimum thresholds of 0.50 and 0.70, respectively (Fornell & Larcker, 1981; Ringle et al., 2015).

Again, one of the methods of ensuring reliability of the scales is through discriminant validity. According to Messick (1989), “discriminant analysis requires a factor to correlate higher than with any other construct on its scale.” The values in the diagonal represents the square root of AVE values which should load higher than its corresponding values on the same scale. From Table 3, all the factors loaded higher than their corresponding factors on the same scale. Financial performance on its scale had a value of about 0.86 which is higher than any other construct on that scale. Innovative capability (0.86), innovation performance (0.83), market innovation (0.8), market performance (0.84), organizational innovation (0.86), process innovation (0.89), and product innovation (0.82) (see Table 3).

Discriminant Validity.

Note. FP = financial performance; IC = innovative capability; IP = innovation performance; MKTI = market innovation; MP = market performance; ORGI = organizational innovation; PCSI = process innovation; PDTI = product innovation.

Results of structural model

The structural model was assessed through the regression weights, t values, and p values for significance of t statistics (Chin, 2010; Ringle et al., 2015). To assess and analyze the path coefficient, bootstrapping was used. Innovation capability has a positive influence on the dimensions of innovation: organizational innovation (0.813), product innovation (0.716), and market innovation (0.500) in that order. However, innovative capability was seen to have a negative relationship with process innovation (–0.756). Also, the four dimensions of innovations (process innovation, product innovation, organizational innovation, and market innovation) showed a positive relationship with organizational performance: organizational innovation (0.514), product innovation (0.190), and market innovation (0.326), respectively. Process innovation was however seen to have a negative relationship with organizational performance (–0.323). This means that organizational innovation influences organizational performance more than the other dimensions. The result of the structural model which tested for the research hypotheses is presented in Figure 2 and Table 4.

Results of structural model.

Results of Hypothesis Test.

Note. SE = standard error; ORGI = organizational innovation; IC = innovative capability; PDTI = product innovation; PCSI = process innovation; MKTI = market innovation; FP = financial performance; PERF = performance; MKTPERF = market performance; INNOPERF = innovation performance.

Significant at .05. **Significant at .01. ***Significant at .001.

Hypothesis Test

We carried out test of hypothesis using bootstrapping of 5,000 samples (see Table 4). In the first model, we tested the effect of innovation capabilities on the innovation dimensions. All the four hypotheses in the first model were supported. Thus, the direct effect of innovation capability on innovation dimensions was supported (H1a, H1b, H1c, and H1d; p < .001); this led to the acceptance of H1a, H1b, H1c, and H1d (see Table 4).

The second model also shows a positive and significant relationship between the innovation dimensions and firm performance. The dimensions of service innovation (market innovation, product innovation, and process innovation) had significant effect on performance (H2b, H2c, and H2d; p < .001) and this led to the acceptance of H2b, H2c, and H2d. Organizational innovation had a positive but insignificant effect on firm performance (β = .799; t = 1.32; p > .05); H2a was therefore not accepted. Product innovation had a positive and significant effect on firm performance (β = .208; t = 2.78; p < .001) which led us to accept H2b. The β score (.208) means that when product innovation increases by 1%, firm performance increases by about 21%. Process innovation also had a negative but significant relationship with firm performance (β = −.322; t = |4.91|; p < .001); H2c was also accepted. The negative effect of the Beta score means that when process innovation reduces by 1%, firm performance also reduces by about 32%. It is therefore imperative to focus more on enhancing the process innovation of banks as they are crucial in the performance of the day-to-day business transactions of banks. Market innovation also had a positive and significant effect on firm performance (β = .347; t = 6.26; p < .001) and this led to the acceptance of H1a. This means that when market innovation increases by 1%, firm performance increases by 35%. The R2 score (.639) for Model 2 shows that, together, the independent variables (product innovation, process innovation, and market innovation) predicted firm performance by about 64%. This means that together, the independent variables contributed about 64% to firm performance.

Also, in the third model, we tested two hypotheses, that is, H3 and H4. The third hypothesis found a negative but significant relationship between performance and market performance (β = −.136; t = −2.03; p < .05) and thus H3 was also accepted. H4 was however rejected as it returned a negative and insignificant relationship between performance and innovation performance (β = −.078; t = −1.15; p > .05). The third model however had a low prediction power as the R2 score for H3 (.002) means that the independent variable performance only predicted about 0.2% of the dependent variable (market performance).

Discussion

First, this study revealed that the innovation dimensions that contribute to bank innovation are organizational, product, process, and marketing innovations. Organizational innovation contributes more significantly to innovation capabilities of banks (66%), followed by process innovation dimension (59%), product innovation (51%), and marketing innovation (25%). This finding is significant as it shows the type of innovation needed by banks in the subregion to augment their service provision and also enhance their output. These findings support earlier findings (Ameme & Wireko, 2016; Rajapathirana & Hui, 2018; Yusif, 2012) who made similar findings. Yusif (2012) was of the opinion therefore that, banks should look for the best type of innovation that is likely to contribute significantly to its performance than adopting bundles of different types of innovation. In effect, organizations should focus more on organizational innovation dimension as well as market innovation to spur the needed growth and increase performance.

Second, with regard to the hypotheses stated in this study, all the hypotheses stated were supported except H2a and H4. Thus, H1, H2, and H3 were all supported by this research’s findings. The first hypothesis (H1a, H1b, H1c, and H1d) showed a positive relationship between innovation capability and the four dimensions of innovation. Thus, innovative capability was found to have a direct and positive influence on organizational innovation, product innovation, process innovation, and market innovation in that order. This finding is very important because as Rajapathirana and Hui (2018) noted, “innovation capability is one of the most influential factors for developing the innovation activities within the firm.” Banks therefore need to focus much of their efforts and attention in searching, developing, and implementing new innovation capabilities to stay competitive. This is because the business landscape is changing and non-financial institutions are now developing products and services that compete effectively and indirectly with financial institutions through various mobile money platforms that allow individuals and businesses deposit, transfer, and pay for goods and services without the use of banks. This is in line with a study by Accenture where it was observed that, there would be a decrease in the use of traditional payment instruments in favor of digital payments in few years (Accenture Consulting, 2015).

Furthermore, the second hypothesis also revealed a significant and positive relationship between the dimensions of innovation (market, process, and product innovations) and firm performance. Thus, H2b, H2c, and H2d were all found to have a positive effect on performance of banks. Organizational innovation was found to have a positive but insignificant effect on firm performance. This finding however contradicts earlier findings which shows that organizational innovation positively influences innovation performance (Camisón & Villar-López, 2012; Chiang & Hung, 2010; Reed et al., 2012). Product innovation however had a significant and positive effect on firm performance. This means that emphasis on new products, technical specification, features, user friendliness, portability, durability, and other significant characteristics of products would influence overall performance of the organization as it gains acceptability and usability by customers and users. In addition, the study revealed a positive and significant relationship between market innovation, process innovation, and firm performance. This is true, as market innovation and process innovation focus on developing new market and also seeking to generate additional revenue through market expansion, new customer acquisition, and product differentiation. Thus, product innovation, market innovation, and process innovation appeared to be the critical driver for service innovation in the banking sector which also indicated a strong link with bank performance.

Finally, the results of the study also revealed a positive and significant relationship between firm performance and market performance. This suggests that improving the innovativeness of banks will enhance overall bank performance including innovative performance, production performance, market performance, and financial performance (Gunday et al., 2011). Results of this study thus established the relationship between firm performance and market performance. However, the relationship between firm performance and innovative performance was not established in this current study. This finding is contrary to previous research findings (Ameme & Wireko, 2016; Gunday et al., 2011; Huhtala et al., 2014; Nguyen et al., 2014; Rajapathirana & Hui, 2018), which found that innovation adoption in the banking sector could effectively influence innovation performance. This finding suggests that the more banks adopt innovation in their activities, the better they perform in terms of market performance, financial performance, and customer value creation.

Conclusion

This study examined the effect of innovation types on bank performance in the Ghanaian banking sector. Findings from this study suggest that, innovation as a strategy drives performance of firms and should be executed as an integral part of business strategy in boosting operation performance such as production performance, market performance, and financial performance. Innovation is thus, a catalyst that propels organizational performance. Firms with supportive innovation culture and supportive staff with innovative mind-set would explore profitable and competitive ideas then convert them into the profitable business concepts and strategies for long-term growth and profitability.

Managerial Implication

This study found a significant and positive effect between innovation and firm performance. This means that innovation is very crucial to the survival of banks. One of the major findings in this study identified the four main types of innovation as influencing firm performance. In this regard, banks should put special emphasis on organizational, process, product, and marketing innovations, as these types of innovations are found to be important instruments for achieving growth and profitability.

In addition, due to the new challenges faced by banks with regard to growing customer acquisition costs, increased customer expectations, increased competition as well as rapid technological changes, banks need to engage in an open innovation ecosystem by creating a strategic business alliance with other businesses in technology, telecommunication companies, and other ISPs (Internet service providers) to strategically realign their operations to reduce cost, increase revenue, and create new channels and flexible products and services to augment the already existing services and to also give customers innovative and pleasurable, easy and convenient banking services.

Theoretical Contribution

The findings of this study add to the empirical investigation in service innovation from a developing country context. Also, as discussed earlier, this study proposed a modified conceptual framework on bank innovation and performance using scales from previous studies. This study thus offers theoretical support for the adoption and implementation of innovation in the banking sector.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.