Abstract

This study investigates the influence of corporate governance and the nature of the ultimate owner on the adjustment behavior of corporate cash holdings. This study uses a sample of Chinese listed firms over the period 2003–2016 and opts difference- and system-GMM (generalized method of moments) models to explore the target cash holdings of Chinese firms. The results demonstrate that Chinese firms have target cash holdings and that the cash holdings adjustment behavior varies across the state-owned enterprises and nonstate-owned enterprises. Finally, the results show that cash holdings adjustment rate varies across normal and crisis period. This study adds to the existing literature by showing how corporate governance attributes and the nature of ownership can impact the cash holdings. Finally, this study provides insights that the cash holdings adjustment varies in normal and a crisis period.

Introduction

Corporate cash holdings is one of the important policies of a firm’s financing policies. The finance literature has focused on the determinants of corporate cash holdings and the presence of the target cash holdings (Target-CH; Harford et al., 2008; Opler et al., 1999; Ozkan & Ozkan, 2004).

A stream of literature shows that firms have a Target-CH level, and they adjust toward their target (Alles et al., 2012; Guariglia & Yang, 2016; Harford et al., 2008; Opler et al., 1999; Ozkan & Ozkan, 2004). Studies show that firms hold cash reserves on the basis of marginal costs and benefits associated with holding liquid assets. The costs of holding cash are associated with the opportunity costs of capital invested in liquid assets. The benefits of holding cash reserves stem from two motives—precautionary motive and transaction cost motives, which suggest that firms maintain cash reserves to cope with unforeseen financial shocks and to avail the positive net present value project in case of insufficient external funds. The literature in this area has mostly focused on the developed economies, and only few studies investigate the phenomena in emerging economies, like China.

This study examines the determinants of cash holdings in Chinese firms over the period 2003–2016. We examine the adjustment behavior of Chinese firms toward Target-CH. Consistent with the trade-off theory, this study tests whether Chinese firms also have Target-CH level, if yes, what is the Target-CH adjustment rate? This study will provide information about the adjustment behavior of Chinese firms toward Target-CH. Furthermore, this study investigates the influence of corporate governance attributes on the cash holding behavior of Chinese firms. Our empirical results show evidence of significant adjustment behavior of Chinese firms toward Target-CH. The findings illustrate that approximately 57% adjustment toward Target-CH is achieved in one period. The results are consistent with the trade-off theory, indicating the Target-CH behavior of Chinese firms. Furthermore, the results show that among corporate governance attributes, CEO duality plays an important role in the cash holdings of firms. These conclusions remain consistent with alternative measures and additional analysis.

One of the distinct characteristics of Chinese firms is the nature of ultimate owner, that is, state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs). Studies show that SOEs have a soft budget constraint facility and therefore are less likely to keep large cash balances (Cai et al., 2016; Guariglia & Yang, 2016; Jebran, Chen, & Tauni, 2019; Lin & Tan, 1999). As SOEs are government owned, therefore, state-owned banks in China provide large amount of resources to SOEs in the form of nonperforming loans, especially to those facing financial difficulties. If SOEs face fewer difficulties to acquire state resources, they are likely to maintain lower cash balances. However, non-SOEs mostly rely on internal funds, that is, cash flows, because they face difficulties in accessing financial resources from state-owned banks (Guariglia & Yang, 2016; Jebran, Chen, & Tauni, 2019). Thus, non-SOEs maintain a higher level of cash reserves (Amess et al., 2015). As the cash level varies across SOEs and non-SOEs, we test whether Target-CH adjustment also varies across the firms. Our empirical findings provide convincing evidence by showing that adjustment rate of Target-CH is higher for SOEs than for non-SOEs.

Finally, we test the adjustment rate toward Target-CH in a normal and crisis period. The 2007 global financial crisis provided an opportunity for researchers to investigate its influence on various corporate decisions. Several studies show that the financial crisis has influenced the cash holdings policy of firms (Jebran et al., 2019; Lian et al., 2011; Momeni et al., 2016). Our analyses show that adjustment rate toward Target-CH varies across normal and a crisis period. Specifically, the results demonstrate that Chinese firms’ Target-CH adjustment rate is higher during the crisis period, compared with pre- and postcrisis period. The findings suggest that firms have increased their cash holdings level during the crisis period.

This article proceeds as follows. Section “Theoretical Background and Review of Literature” presents theoretical background and literature review. Section “Method” presents the methodology. Section “Empirical Results” reports empirical results. Section “Robustness Tests” presents robustness tests. The last section concludes.

Theoretical Background and Review of Literature

Theoretical Background

The theory that explains the Target-CH behavior of the firms is the trade-off theory. This theory stems from the theory of Keynes (1936). The theory posits that firms hold cash reserves because of marginal costs and benefits associated with holding liquid assets. The costs of holding cash are associated with the opportunity costs of capital invested in liquid assets, which suggest that firms can gain a lower return for the similar level of risk compared with other investments (Guariglia & Yang 2016; Opler et al., 1999).

The benefits of holding cash reserves stem from two motives—precautionary motive and transaction cost motive. The precautionary motive illustrates that firms maintain cash reserves to cope with unforeseen financial shocks that may arise in the future. For example, firms hold cash reserves to avail the projects with positive net present values, if there exist asymmetric problems associated with external financing. Hence, firms, with better investment opportunities, are likely to hoard large cash balances to avoid external financing. However, the transaction cost motive assumes that firms hoard cash reserves for business transaction needs or to save transaction costs of raising funds or the costs of liquidating assets. This motive is more relevant for firms having large transactions, such as manufacturing.

Several studies provided supportive evidence for the predictions of trade-off theory, suggesting that firms have a target level of cash holdings. Most of the studies on Target-CH have been carried out for developed countries. For example, Opler et al. (1999) found strong evidence of static trade-off model of cash holdings for U.S. firms. Ozkan and Ozkan (2004) provided supportive evidence for Target-CH for U.K. firms. Ferreira and Vilela (2004) found evidence for Economic and Monetary Union (EMU) countries. Apart from this, some of the studies focused on the emerging markets and reported the presence of Target-CH (Alles et al., 2012; Asante-Darko et al., 2018 Uyar & Kuzey, 2014).

There are also two other theories which explain the firms’ motive of cash holdings—the pecking order theory and the agency theory of free cash flows. The pecking order theory does not consider the existence of the target cash holding behavior. The theory stems from the pecking order theory of the capital structure (Myers & Majluf, 1984). The theory suggests that the cash holdings of a firm depend on the cash inflows and outflows. Firms prefer internal funds (retained earnings) over external (debt and equity) because of information asymmetries and signaling costs associated with external financing. Therefore, firms prefer internal cash flows, and if the internal funds are not sufficient, firms prefer external sources of financing.

The agency theory of free cash flow postulates that managers have incentives to hold cash to enhance their control on the cash level on total assets (Jensen, 1986). Furthermore, managers want to accumulate cash reserves by reducing dividends to shareholders, which leads to agency problems between managers and shareholders. Maintaining an optimal level of cash balance also leads to agency problems between managers and shareholders (Habib & Hasan, 2017; Kusnadi et al., 2015).

In this study, we test the theoretical prediction of the trade-off theory. Specifically, we examine whether Chinese firms have a target level of cash holdings. Furthermore, we examine whether various corporate governance attributes significantly contribute to optimal cash holdings. Prior studies show evidence of the existence of optimal cash holdings mostly in developed countries like the United States and the United Kingdom (Opler et al., 1999; Ozkan & Ozkan, 2004). However, there is still no convincing evidence of which of the theories explain the cash holdings, especially in the emerging economies. In this study, we argue that Chinese firms have Target-CH and they adjust toward Target-CH.

Corporate Governance and Target Cash Holdings

The study of cash holding concerning corporate governance and agency theory perspective remained an interesting topic among researchers because holding the amount of cash and decisions regarding contractual payments on debt and other obligatory contracts are made by managers. Therefore, several studies (Jensen, 1986; C.-S. Kim et al., 1998; Opler et al., 1999; Ozkan & Ozkan, 2004) argue that holding excessive amount of cash to cope with the firm’s operational and financial risk makes it a tool for the manager to pursue their own agenda which may lead to manager–shareholder problems. For example, Opler et al. (1999) argue that risk-averse managers usually hoard more cash to attain their benefits at the cost of shareholders wealth, which may deter timely use of cash to invest in profitable projects. However, Harford et al. (2008) suggest that stable firms keep less cash compared with others because managers tend to avoid any annoying attention of active shareholders. Therefore, the adjustment rate in high cash level is quicker in stable firms as compared with the other firms.

Furthermore, prior studies show that corporate governance attributes can significantly influence a firm’s cash holdings level (Asante-Darko et al., 2018; Chen, 2008; Harford et al., 2008; Kuan et al., 2012; Tsai, 2012). For example, studies show that independent directors on board can save the interests of shareholders by increasing the monitoring efficiency (Borokhovich et al., 1996; Mayers et al., 1997; Rosenstein & Wyatt, 1997) and reducing the opportunistic behavior of managers of hoarding large cash balances. Thus, firms with a higher proportion of independent directors are less likely to keep large cash reserves (Chen, 2008; Lee & Lee, 2009).

Board size is also an important governance attribute that influences the decision-making regarding financing activities especially cash holdings decisions. Larger boards are necessary to handle the operational complexity of organizations and can also play a better monitoring role and are helpful in reducing a firm’s debt level (Berger et al., 1997; Bhat et al., 2018; Boone et al., 2007). However, studies argue that smaller boards have less free riding problems, which lead to less cash holdings level (Al-Najjar & Belghitar, 2011; Lee & Lee, 2009).

One of the important positions on corporate boards is CEO duality—CEO also serving as a board chair. The early advocates of agency theory (Fama & Jensen, 1983; Jensen, 1993) argue that merging the role of CEO and board chair negatively affects the board effectiveness. Many studies suggest that CEO duality leads to the ineffectiveness of the board’s monitoring function. For example, K.-H. Kim et al. (2009) argue that CEO duality reduces a firm value by diversification strategies in unrelated industries. Gul and Leung (2004) show that CEO duality is negatively related to voluntary disclosure. Moreover, studies show that firms hoard large cash reserves when the CEO also serves as a board chair (Bokpin, 2011; Kusnadi, 2011). Based on the discussion so far, we can argue that corporate governance factors can influence a firm’s cash-related decisions, and hence we can also expect that such attributes can impact the Target-CH.

Nature of the Ultimate Owner and Target Cash Holdings

One of the distinct features of Chinese firms is the nature of the ultimate owner, that is, SOEs and non-SOEs. According to soft budget constraint theory, SOEs have soft budget constraint facility and therefore are less likely to hold large cash balances. However, soft budget constraint or easy access to funds leads to aggravating the agency problems. For example, entrenched managers in SOEs may intrigue with government officials and invest in politically beneficial projects rather than projects with positive net present value. Furthermore, Chinese state-owned banks provide large amount of credits to SOEs in the form of nonperforming loans. Therefore, Chinese banks have a higher corporate lending ratio compared with other countries due to the inefficient bond market. Moreover, state-owned banks in China give particular treatment to SOEs’ facing financial difficulties. Thus, Chinese SOEs face less difficulties to obtain government resources (Cai et al., 2016; Lin & Tan, 1999) and are less likely to hoard large cash balances.

In contrast, Chinese non-SOEs mostly rely on internal funds, that is, cash flows, because they face difficulties in accessing financial resources from state-owned banks (Guariglia & Yang, 2016; Jebran, Chen, & Tauni, 2019). In this case, non-SOEs will maintain a higher level of cash reserves (Amess et al., 2015). Based on the discussion so far, one can argue that as the level of cash holdings varies across SOEs and non-SOEs, we can also expect that the adjustment rate toward Target-CH should also vary across SOEs and non-SOEs.

Financial Crisis and Target Cash Holdings

The 2007 global financial crisis has significantly influenced both developed and emerging economies. Like other economies, the financial crisis also affected the Chinese economy; however, the impact was relatively less severe compared with other economies, because of its closed financial system. From the perspective of precautionary motive of cash holding, the financial crisis highlights the importance of liquidity, which demonstrates an efficient cash holdings policy to cope with shocks or uncertainty following the crisis (Shiau et al., 2018). Hence, financially constrained firms are likely to adopt or establish a useful framework to hoard cash than do firms with low financial constraints. Thus, firms ideally need to maintain an optimal level of cash holdings to deal with uncertainty and any other random events.

The financial crisis provided an opportunity for researchers to investigate its influence on various corporate decisions. Several studies show that the financial crisis has influenced the cash holdings policy of firms. For example, Momeni et al. (2016) documented that financial crisis adversely affected the operating cash flow of the firms. Lian et al. (2011) found that compared with other periods, Chinese firms have significantly increased their cash holdings during the financial crisis. Jebran et al. (2019) argue that the financial crisis has a significant influence on the cash holdings policies during the crisis period. Based on the discussion so far, we can argue that the financial crisis has influenced the cash holdings decisions. Thus, we can expect that the financial crisis has also influenced the Target-CH of Chinese firms.

Method

Data

Our sample consists of all A-share Chinese firms listed on Shenzhen and Shanghai Stock Exchanges over the period 2003–2016. Following prior studies, we drop firm-year observations: pertaining to finance industry, firm-year observations for missing data, and firms that issues B or H shares (Alles et al., 2012; Amess et al., 2015; Cai et al., 2016; Guariglia & Yang, 2016; Guney et al., 2007; Iona et al., 2017). Following the criteria above, we obtained a sample of an unbalanced panel consisting of 24,070 firm-year observations. The data are from the China Stock Market and Accounting Research Database. The variables are winsorized at the 1% and 99% level to minimize the influence of outliers.

Variable Measurement

Cash holdings

Following the literature on cash holdings, we measure the cash holdings as cash and cash equivalent scaled by total assets (Harford et al., 2008; Jebran, Chen, & Tauni, 2019; Kuan et al., 2012; Ozkan & Ozkan, 2004; Uyar & Kuzey, 2014).

For checking the robustness, we follow Itzkowitz (2013) and use another measure of cash holdings—the natural logarithm of the one plus ratio of cash and cash equivalent scaled by total assets. Several studies have used this approach (Habib et al., 2017; Habib & Hasan, 2017; Jebran, Chen, & Tauni, 2019; Jebran, Iqbal, et al., 2019).

Corporate governance variables

We follow prior studies and use three main corporate governance attributes which can influence cash holdings (Harford et al., 2008; Iona et al., 2017; Kuan et al., 2012). The three attributes are board size, board independence, and CEO duality. We measure board size (BOARD) by the total number of directors on a board. We measure board independence (IND) by the ratio of the independent directors on a board. We measure CEO duality (DUALITY) by an indicator variable, which equals 1 if the CEO and board chair are the same, and 0 otherwise.

Control variables

Following the literature, we control for several factors which can influence the cash holdings (Al-Najjar & Belghitar, 2011; Harford et al., 2008; Opler et al., 1999; Ozkan & Ozkan, 2004; Siddiqua et al., 2018; Uyar & Kuzey, 2014). We control for cash dividend (DIVIDEND), measured with a variable that takes a value 1 if the firms paid a cash dividend, and 0 otherwise. We control for capital expenditure (CAPEX), measured using the change in fixed assets plus depreciation over total assets. We control for cash flow ratio (CF), defined as the pretax profit plus depreciation over total assets. We control for cash substitutes (CSUBS), which is the net working capital minus cash over total assets. We control for financial debt (FINDEBT), which is the financial debt over total assets. We control for the leverage (LEVERAGE), which is the total debt over total assets. We control for the market to book ratio (MTB), defined as the market value of equity over book value of equity. We control for firm size (SIZE), which is the natural logarithm of total assets. We control for tangibility (TANGIBILITY), which is the tangible fixed assets over total assets. We control for cash flow volatility (VOLATILITY), which is the standard deviation of cash flow over total assets.

Model

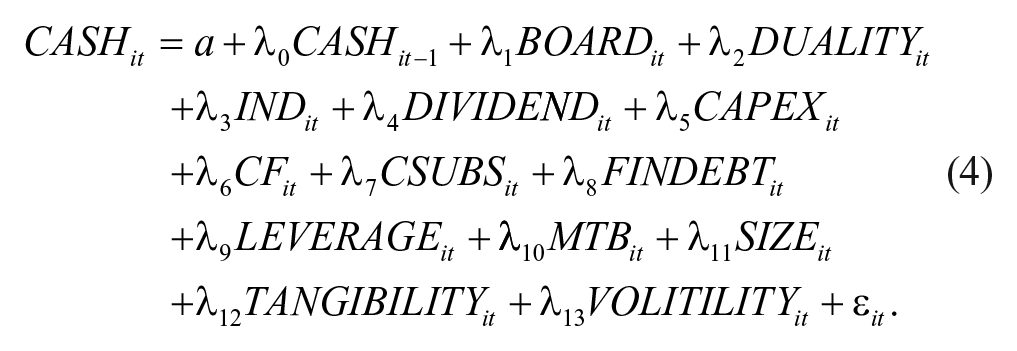

The main aim of the study is to find out the Target-CH. Following prior studies, this study selects the partial adjustment model to identify Target-CH (Opler et al., 1999; Ozkan & Ozkan, 2004). Specifically, we opt generalized method of moments (GMM) model for exploring speed of adjustment of cash holdings. This model is also suitable to control for endogeneity problems. To obtain more reliable results, this study selects the difference-GMM model. For robustness test, we apply the system-GMM model for estimation of results. We first estimated the partial adjustment model as

where

where a denotes constant; xjit denotes the vector of firm characteristics for firm i at time t; and ε it denotes error term.

Thus, substituting Equation 2 in Equation 1, the equation that explains the cash level retained by firms is

where λ0 = (1 − λ), that measures adjustment rate toward Target-CH; λ j = β j and ε it denotes error term. A higher coefficient value of λ0 denotes lower adjustment rate.

Since, xjit denotes firm-specific characteristics, which includes: BOARD, IND, DUALITY, DIVIDEND, CAPEX, CF, CSUBS, FINDEBT, LEV, MTB, SIZE, TANG, and VOL. Thus, including these factors in Equation 3, we obtain the following equation:

Empirical Results

Descriptive Statistics

Table 1 reports the summary statistics. The mean value of CASH is 15.9%, which illustrates that Chinese firms hold a large portion of the cash (Jebran, Chen, & Tauni, 2019; Rehman & Wang, 2015; Wang et al., 2016). The mean value of BOARD demonstrates that on average there are nine directors on a board. The mean value of DUALITY indicates that 20.8% of the directors are serving as CEO and chairman on board in Chinese firms. The mean value of IND shows that independent directors hold 36% of the total directors on a board. The mean values for control variables DIVIDEND, CF, CAPEX, CSUBS, TANGIBILITY, FINDEBT, VOLATILITY, LEVERAGE, MTB, and SIZE are 0.61, 0.06, 0.04, −0.01, 0.25, 0.45, 0.11, 0.48, 2.53, and 21.71, respectively.

Descriptive Statistics.

Note. CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CF = cash flow ratio; CAPEX = capital expenditure; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size.

Correlation Matrix

Table 2 presents the correlation analysis among variables. The notable findings show that all explanatory variables (except VOLATILITY) have significant associations with cash holdings. The results show that BOARD, CAPEX, FINDEBT, LEVERAGE, SIZE, and TANGIBILITY have significant negative associations with CASH. In contrast, DUALITY, IND, DIVIDEND, CF, CSUBS, and MTB have significant positive correlations with CASH.

Correlation Matrix.

Note. CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CF = cash flow ratio; CAPEX = capital expenditure; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size.

Denotes significance at the 5% level.

Corporate Governance and Target Cash Holdings

Table 3 presents the regression results obtained using difference-GMM model. Consistent with the trade-off theory, we find that Chinese firms have a Target-CH level and they adjust toward the target level. We find that the coefficients on L.CASH (lagged cash variable) are significant across all columns and are consistent with and without inclusion of corporate governance variables. The results in Columns 1, 4, and 5 show that the adjustment rate toward Target-CH is approximately 57%. This result suggests that Chinese firms achieve their Target-CH level in less than 2 periods.

Corporate Governance and Target Cash Holdings.

Note. AR(1) and AR(2) denote Arellano–Bond tests for serial correlation in residuals. Standard errors are in parenthesis. GMM = generalized method of moments; L.CASH = lagged cash variable; CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CAPEX = capital expenditure; CF = cash flow ratio; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size; J test = Hansen–Sargan test of overidentifying restrictions.

Significance at 10% level. **Significance at 5% level, ***Significance at 1% level.

Furthermore, the results show that corporate governance attributes, that is, BOARD and IND have an insignificant influence on the cash holdings. However, we find that CEO duality has a significant positive influence on cash holdings of Chinese firms. This result is consistent with Kuan et al. (2012) that find a significant positive effect of CEO duality of cash holdings.

Most of the variables, if significant, have the same sign across all columns, which corroborates with prior studies. Specifically, we find that CAPEX, FINDEBT, and SIZE have significant positive effects on cash holdings. Whereas, we find that CF, CSUBS, TANGIBILITY, and LEVERAGE have significant negative effects on cash holdings.

Target Cash Holdings in SOEs and Non-SOEs

Table 4 reports the results of adjustment rate toward Target-CH in SOEs and non-SOEs. We divided the sample into SOEs and non-SOEs and estimated the regression results separately. Columns 1 and 2 reports the regression results of difference-GMM model for SOEs and non-SOEs respectively. The results show the existence of a target level of cash holdings for both types of firms. The notable findings show that the adjustment rate of cash holdings for SOEs is 63.9%, whereas for non-SOEs is 60.6%. Such results illustrate that as SOEs are controlled by the state, they can adjust toward the Target-CH easily by acquiring the financial resources from the state. However, non-SOEs face difficulties in accessing to external resources and rely mostly on internal sources; therefore, their cash holdings adjustment rate is relatively lower than SOEs.

Nature of Ultimate Owner and Adjustment of Cash Holdings.

Note. AR(1) and AR(2) denote Arellano–Bond tests for serial correlation in residuals. Standard errors are in parenthesis. SOE = state-owned enterprises; L.CASH = lagged cash variable; CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CAPEX = capital expenditure; CF = cash flow ratio; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size; J test = Hansen–Sargan test of overidentifying restrictions.

Significance at 10% level. **Significance at 5% level, ***Significance at 1% level.

Furthermore, we find that the BOARD and IND have insignificant effects on the cash holdings. The notable finding shows that CEO duality (DUALITY) has a significant positive influence on the cash holdings for the non-SOEs. This result suggests that CEO duality plays an important role in maintaining the cash holdings policy of the non-SOEs.

For control variables, we find that DIVIDEND has a significant negative influence on the cash holdings of SOEs. We also document that SIZE has a significant positive effect on cash holdings of SOEs. Moreover, we find that CAPEX and VOLATILITY have significant negative impacts on cash holdings of non-SOEs. These results show important evidence that cash holdings determinants vary across firms of different nature.

Financial Crisis and Target Cash Holdings

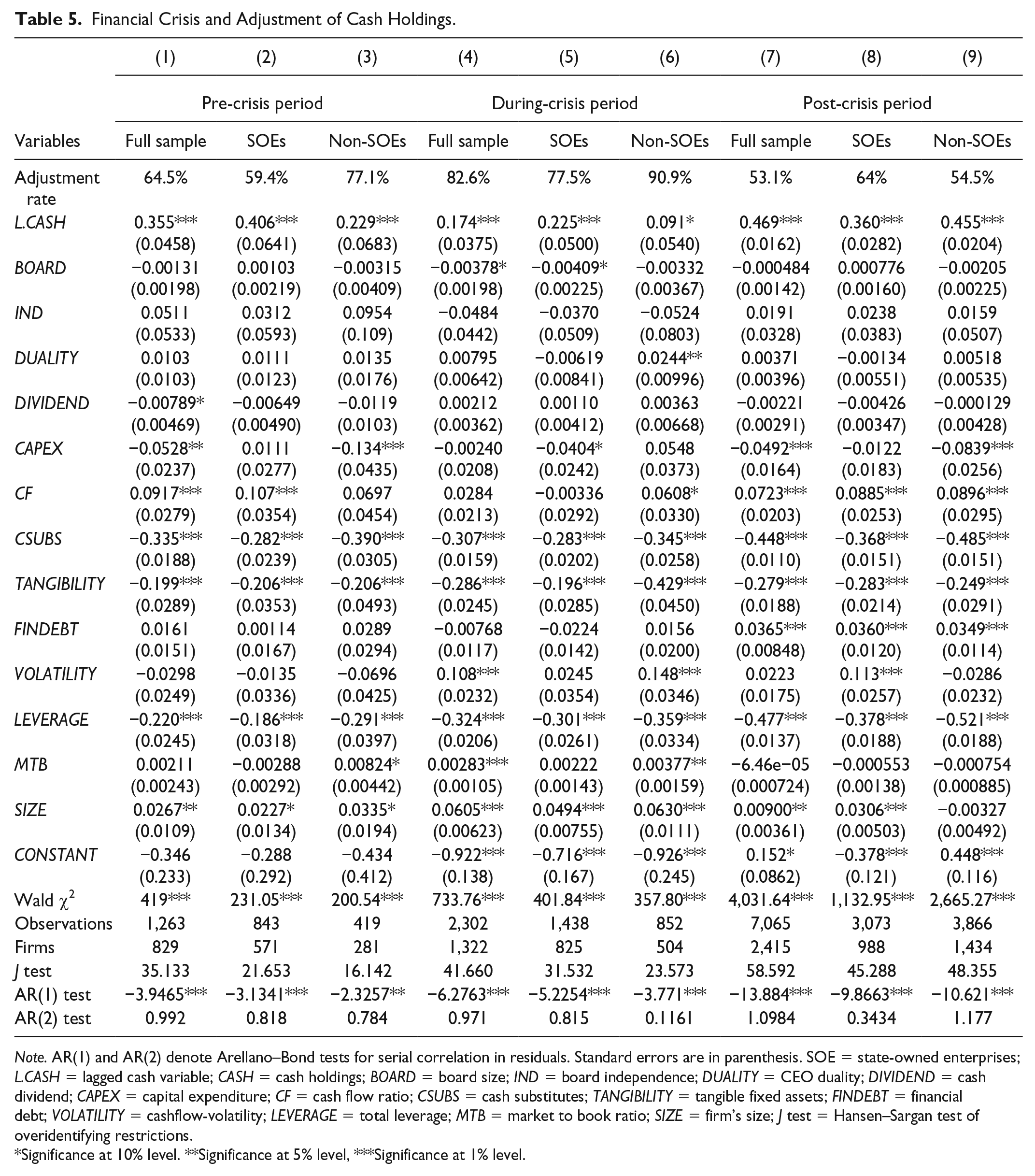

To investigate the adjustment rate toward Target-CH in normal and crisis period, we divided the sample into pre-, during- and post-crisis period. The pre-crisis period is from 2003 to 2006. The financial crisis period is from 2007 to 2010. The post-crisis period is from 2011 to 2016. We estimate the regression results for each period separately and report the results in Table 5.

Financial Crisis and Adjustment of Cash Holdings.

Note. AR(1) and AR(2) denote Arellano–Bond tests for serial correlation in residuals. Standard errors are in parenthesis. SOE = state-owned enterprises; L.CASH = lagged cash variable; CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CAPEX = capital expenditure; CF = cash flow ratio; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size; J test = Hansen–Sargan test of overidentifying restrictions.

Significance at 10% level. **Significance at 5% level, ***Significance at 1% level.

Columns 1, 4, and 7 reports the results for the full sample period. The results show that cash holdings adjustment rate is higher in financial crisis period (77.5%) as compared with pre-crisis (64.5%), and the post-crisis period (53.1%). Similarly, Columns 2, 5, and 8 indicate that the adjustment rate for SOEs in crisis period (77.5%) is higher than pre-crisis (59.4%), and post-crisis period (64%). Furthermore, the results in Columns 3, 6, and 9 show that non-SOEs adjustment rate is higher in financial crisis period (90.9%) as compared with pre-crisis (77.1%), and post-crisis period (54.5%). These results suggest that Chinese firms’ adjustment rates significantly increased during the financial crisis period. These findings are consistent with Lian et al. (2011) that show that Chinese firms have increased their cash holdings during the financial crisis period.

Robustness Tests

Robustness Test Using System-GMM Model

For robustness test, we apply the system-GMM model which is the improved version of the difference-GMM model. Column 1 of Table 6 reports the findings using the full sample, whereas Columns 2 and 3 report the results for SOEs and non-SOEs, respectively.

Robustness Test Using System-GMM Model.

Note. AR(1) and AR(2) denote Arellano–Bond tests for serial correlation in residuals. Standard errors are in parenthesis. SOE = state-owned enterprises; L.CASH = lagged cash variable; CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CAPEX = capital expenditure; CF = cash flow ratio; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size; J test = Hansen–Sargan test of overidentifying restrictions.

Significance at 10% level. **Significance at 5% level, ***Significance at 1% level.

The findings indicate that the coefficients on L.CASH are significant, suggesting the presence of a Target-CH level. Specifically, we find that for the full sample, the adjustment rate is 59.7%, suggesting almost similar results to that reported in Table 3. Furthermore, we find that the adjustment rates for SOEs and non-SOEs are 61.5% and 62.5%, respectively. Overall, these results tally with our main findings reported in Table 3.

Alternative Proxy of Cash Holdings

For checking the robustness, we follow Itzkowitz (2013) and use another measure of cash holdings and report the results in Table 7. We find that the coefficients on L.CASH are significant across all cases, suggesting a Target-CH. We document that the adjustment rate for the full sample is 58.7%, which is almost similar to Table 3. Furthermore, we find that the adjustment rates of SOEs and non-SOEs are 64.8% and 62.3%, respectively. These results indicate that the SOEs’ adjustment rate is higher than that of non-SOEs, which is consistent with our prior results.

Robustness Test Using Alternative Proxy of Cash Holdings.

Note. AR(1) and AR(2) denote Arellano–Bond tests for serial correlation in residuals. Standard errors are in parenthesis. SOE = state-owned enterprises; L.CASH = lagged cash variable; CASH = cash holdings; BOARD = board size; IND = board independence; DUALITY = CEO duality; DIVIDEND = cash dividend; CAPEX = capital expenditure; CF = cash flow ratio; CSUBS = cash substitutes; TANGIBILITY = tangible fixed assets; FINDEBT = financial debt; VOLATILITY = cashflow-volatility; LEVERAGE = total leverage; MTB = market to book ratio; SIZE = firm’s size; J test = Hansen–Sargan test of overidentifying restrictions.

Significance at 10% level. **Significance at 5% level, ***Significance at 1% level.

Conclusion

This study investigates the existence of Target-CH in Chinese firms and further tests whether corporate governance attributes, such as CEO duality, board size, and board independence, can influence Target-CH. The study also examines whether the adjustment behavior toward Target-CH varies across SOEs and non-SOEs. We apply the difference-GMM model to examine the Target-CH and to control for endogeneity issues among variables.

Using a sample of Chinese firms during 2003–2016, this study finds the presence of significant adjustment behavior of Chinese firms toward Target-CH. We document that Chinese firms’ adjustment rate is approximately 57% in one period. We also find that the adjustment rate varies across SOEs and non-SOEs. The results are consistent with the trade-off theory, by suggesting a target level of cash holdings. Furthermore, the results show that corporate governance attributes, board independence, and board size have insignificant influence on the cash holdings adjustment behavior of the firms. However, CEO duality plays an important role in cash holdings of firms. Our additional analyses show that adjustment rate of Target-CH varies across the different periods. We find that the adjustment rate toward Target-CH in higher during the financial crisis period as compared with the precrisis and postcrisis period. Our results are consistent and robust to alternative measures and methods.

This study has important implications. First, the results of this study lend important support to the trade-off theory hypothesis and suggest the adjustment behavior of Chinese firms toward Target-CH. Second, the results also provide evidence that the adjustment rate toward Target-CH differs across firms of different nature, that is, SOEs and non-SOEs. Finally, our results also provide evidence that the adjustment rate toward cash holding varies across a normal and a crisis period.

Overall, the findings suggest that corporate governance and ultimate owner are important attributes of cash holdings behavior of Chinese firms. In this study, we have considered only three governance attributes. Understanding how other governance attributes influence cash holdings seems to be a promising avenue for future research.

Footnotes

Acknowledgements

The earlier draft of the manuscript was presented at the International Academic Conference on Management, Economics, Business and Marketing at Budapest, Hungary (on March 16–17, 2018).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We are thankful to the National Natural Science Foundation of China (Project Number: 71472030) for financial support.