Abstract

The Vietnamese government has advocated developing an export-based economy. In fact, the Prime Minister issued Decision No. 2471/QD-TTg dated December 28, 2011, approving the strategy of import and export of goods for the period 2011 to 2020, with a vision to 2030 formulating policies on development of logistics services, credit, and investment to develop export production, and customs clearance places for import and export goods. That fact prompted us to conduct the research investigating the impact of export support policies on export performance of firms locating in Ho Chi Minh City. The combination of qualitative and quantitative research method was applied. The netnography method and in-depth interview were used to explore support policies influencing export performance, and found Tax Incentives, Credit Incentives, Trade Promotion Support, and Custom Procedures Reform are four policies significantly explaining firms’ export performance. To measure the impact of these policies on export performance, we surveyed 141 firms in HCMC. The quantitative study confirmed that four policies impact positively significantly on export performance. The best explanatory factor is Trade Promotion Support, the second is Customs Procedure Reforms, followed by Tax Incentives. Credit incentives have the lowest effect on export performance. The findings asserted the positive effectiveness of policies promoting export performance implementing in Vietnam, and provided empirical evidence to support institutional theory.

Highlights

Four main government’s supportive policies include tax incentives, credit incentives, trade promotion support, and customs procedure reform.

Of these, trade promotion support has the most significant positive impact on SMEs’ export performance.

Introduction

Vietnam is a socialist-oriented market economy. The Communist Party of Vietnam has advocated linking the domestic market with the world market, well solving the relationship between domestic consumption and export, and multilateralized foreign economic relations. In other words, the Vietnamese government advocates export-based economic development. In 2000, the Prime Minister issued Directive No. 22/2000/CT-TTg to define the import and export strategy of goods and services in the 2001 to 2010. It determined the priority of exports to speed up exports in all fields, create a source of quality, value-added, and highly competitive goods for export, contribute to creating jobs for society, and foreign currency reserves. In 2006, the Government issued Decision No. 156/2006/QD-TTg to approve the export development project for 2006–2010. In 2011, the Government signed Decision No. 2471/QD-TTg and promulgated it on December 28, 2011, to define the export-oriented strategy, which will develop in a sustainable and reasonable way, both expanding the scale and focusing on improving the export value. The strategic goals of export development for the period 2011 to 2020 and orientation to 2030 are to commit to international economic integration, to the exports of high value-added products, finished products with high quality, and to restrict the export of raw products, according to the Prime Minister. According to the Minister of Industry and Trade, the biggest challenges for Vietnamese exporters, especially small and medium enterprises, are the ability to mobilize capital and access bank loans, diversify export markets, and pay highinterest costs; the poor commercial infrastructure system increases costs related to exporting and then decreases exporters’ competitiveness. The export capacity of domestic enterprises is still low compared to FDI enterprises. Vietnam’s export turnover increased by 110.5% in the 2001 to 2005 period, 153% in the 2006 to 2010 period, 133.9% in the 2011 to 2015 period, 131.2% in the 2016 to 2021 period.

Export-led growth has gained significance among governments as a strategic mechanism driving the economic development of many nations, because of the multiple advantages derived from export activity. Increased export competitiveness would result in an increase in revenue, employment, exploitation of economies of scale, and international technological spillovers, among other benefits, especially for small and medium enterprises (SMEs) (Pattnayak & Thangavelu, 2014; Wagner, 2013). As a result, governments are progressively implementing a variety of export promotion programs to boost SMEs’ export activity (Freixanet, 2012; Pickernell et al., 2016). To boost and accelerate export-led growth, exporters are provided with a variety of economic and government policies as incentives (Abou-Stait, 2005). Several government incentive programs are viewed as a resource supplement (Leonidou et al., 2011); their impact on SME export-related resources and capacities might be used to examine their involvement in further detail. In addition, the data on the connection between financial incentives and exporting is scant (Francioni et al., 2016) and requires more study. Regarding the function and impacts of export credits and guarantees, only a small number of research concentrates on SMEs in emerging markets. Consequently, this study answers current suggestions for investigating the influence of governmental and institutional concerns, namely the impact of government public policies on the exporting performance of SMEs in a nation such as Vietnam. To our best knowledge, there has been no empirical study on the impact of policies supporting the export performance of exporting firms located in Ho Chi Minh City until now. Therefore, this study conducted aims to:

− study the role of policies promoting the export performance of exporting firms located in Ho Chi Minh City, and

− examine the impact of identified export support policies on surveyed exporting firms’ export performance.

To achieve the research objectives above, a mixed research method was applied. The remaining sections of this paper are structured as follows. The second section presents the literature review and conceptual framework; The third section presents the qualitative research results, research model, and hypotheses development for a quantitative study. The fourth part shows the development of measurement scales for all research concepts, sampling techniques, and data collecting. The fifth section presents data processing and the results of hypothesis testing. The last section is the discussion of research findings with implications for theory and practice and recommendations for further research.

Theoretical Framework

According to Katsikeas et al. (2000) and Francioni et al. (2016), the success of exporting firms is dependent on both internal and external factors, such as their resources and capabilities (internal factors) and the features of the local and international markets (external factors). In this context, internal factors refer to the resource-based view of the firm, while external ones refer to the institutional-based view (Chen et al., 2016; Sousa et al., 2008). According to Chen et al. (2016), both resource-based view and institutional-based view theories are under the contingency theory, as illustrated in Figure 1.

Theoretical framework of export performance.

Firstly, according to the resource-based view, a firm is a singular entity that owns a collection of valuable tangible and intangible resources that, because of their limited imitable nature and inability to be transferred, give the company a competitive edge in export markets (Barney, 1991; Barney et al., 2001). Secondly, Peng et al. (2008) believed that an exporter’s competitive edge is influenced not only by its resources but also by the external market and environmental variables. In turn, the institutional theory emphasizes the importance of institutional environment and argues that not all nations are the same (North, 1990) and that differences in institutional environments might affect the value a business can create from resource-based advantages (Brouthers et al., 2008; Meyer et al., 2009; Peng et al., 2008). In the context of internationalization, the institutional approach is of great importance (Oparaocha, 2015; Szyliowicz & Galvin, 2010) because it explains how firms exploit institutional links to develop entrepreneurial behavior and international activities (Bruton et al., 2010; Dacin et al., 2002; LiPuma et al., 2013).

Furthermore, Chen et al. (2016) claimed that the competitive advantages derived from both firms’ resources and institutional context are neither stable nor unchangeable. Instead, it is determined by the co-alignment of these forces, highlighted by the contingency theory. Notably, the theory proposes that environmental factors impact the firm’s export plans and performance; exporting is a firm’s strategic reaction to the interaction of internal and external forces (Harrigan, 1983; Katsikeas & Morgan, 1994; Robertson & Chetty, 2000; Yeoh & Jeong, 1995). This theory posits that a firm’s export performance is contingent on the environment in which it operates and that its effectiveness is contingent on the properly matching of organizational contingency variables to that environment (Sousa et al., 2008; Zeithaml et al., 1988). The contingency hypothesis emphasizes the compatibility between marketing techniques and the broader situation (Chen et al., 2016). Hultman et al. (2011) discover that the efficiency of an export promotion plan depends on a complex interplay between export experience and external sociocultural distance, with strategic decisions, export experiences, and sociocultural surroundings determining export success.

Several studies have been conducted based on these theories to investigate the internal and external barriers that impede export performance. Most focus on SMEs because they may face higher export barriers than larger firms (Alonso et al., 2014; Kahiya et al., 2014; Kahiya & Dean, 2016; Katsikeas et al., 2000; Shoham & Albaum, 1995). Regarding the resource-based view, the barriers may result from insufficient resources and information on the possibilities and constraints of foreign markets (Bagchi-Sen, 1999; Julien et al., 1997; Kahiya & Dean, 2016; Paul et al., 2017). For instance, several studies point out some internal hindrances, consisting of firms’ marketing capabilities (Leonidou, 1995), connections to different local networks (Mackinnon et al., 2004), the owners’ low level of export experience, or the lack of knowledge of foreign markets (Baykal & Gunes, 2004; Cadogan et al., 2002; Fischer & Reuber, 2003; Wu et al., 2007), the lack of competent personnel for exporting activities (Yang et al., 1992), the lack of financing of expenditures related to exports to outside markets (Bellone et al., 2010; Ling-yee & Ogunmokun, 2001; Ughetto, 2008), etc. Such constraints relate to developing acceptable import quality requirements and a suitable design and image for the export market (Czinkota & Ricks, 1983; Kaynak & Kothari, 1984). Likewise, in the institutional-based view, SMEs could encounter higher external exporting barriers than larger exporters. For example, these barriers might come from external sources such as proper trade institutions, unfavorable exchange rates, and the absence of a stimulating national export policy (Brooks & Frances, 1991; Cardoza & Fornes, 2011; Figueiredo & Almeida, 1988; Ghauri & Holstius, 1996); domestic regulations, the economic environment, and poor information about foreign markets’ opportunities (Kaynak et al., 1987).

These constraints and the institutional theory provide a sound theoretical foundation for explaining forces why SMEs are seeking aid from outsiders to boost their internationalization, which is particularly pertinent to the study of government export support or government export promotion programs (Oparaocha, 2015; Wang et al., 2017). Typically, such contacts would offer enterprises access to more resources for international expansion (Oparaocha, 2015). It is felt that this help is essential for SMEs to overcome the hostile and unpredictable export market environment (Seringhaus & Rosson, 1991). It has been widely recognized that export promotion programs assist businesses in enhancing both their internal and external resources (Gençtürk & Kotabe, 2001; Leonidou et al., 2011). According to research by Haddoud et al. (2017), experienced government export promotion programs boost export performance by increasing the quality of SMEs’ ties with international clients. Even while experienced export promotion programs have an indirect impact on export success, these programs assist SMEs in emphasizing the development of business platforms and local networks. Despite playing an important role, the current research vein on the government’s supportive policies affecting SME’s export performance is limited to information-related and financial-related supports, not to mention that their findings are not conclusive (Haddoud et al., 2017; Wang et al., 2017). They are our motivations for us to conduct this study.

Research Model and Hypothesis Development

Our research model is developed based on exploratory research to figure out the government’s supportive policies, including (1) netnography and in-depth interviews with professionals and (2) empirical evidence of previous studies.

Qualitative Research and Results

Qualitative research is based on the inductive process in scientific research methods. Creswell (2009) believes that qualitative research means exploring and understanding human and social problems through groups and individuals. According to Creswell et al. (2007), there are five approaches in qualitative research including (1) narrative research, (2) phenomenology, (3) ethnography, (4) case studies, and (5) grounded theory. In addition, there is a branch of ethnographic research initiated by Kozinets (2002, 2010, 2015), Kozinets et al. (2008), Kozinets and Handelman (1998) is “netnography.” This has been a popular approach in the field of consumer behavior in the last two decades, which has taken advantage of the internet and social networks to exploit consumer behaviors, views, and attitudes.

In this study, the nonparticipant netnographic qualitative study aims to explore the attitudes, views, and behaviors of players related to export activities, including policymakers, businesses, and experts through economic forums, reports on internet discussions, and opinions of businesses at seminars. Adopted from Costello et al. (2017), the research was carried out in three steps:

Step 1: Online communities associated with topics related to research questions were selected. An online community identified is a group of people who participate in commenting on the topics on websites, forums of magazines, or forums of conferences on social networking sites. Visiting websites presented in Table 1, we identified participants commenting on the research issues. They are policymakers, government officials, businessmen, and academic experts (Table 1).

Step 2: We collected their opinions to evaluate the level of interaction through the comments posted and assess whether the collected data is detailed and descriptive.

Many comments mentioned customs procedures, customs clearance inspection, and specialized inspection, causing difficulties for export activities leading to the increase of exported product cost. The difficulty of exporters in terms of marketing their products in foreign markets and exploring new foreign markets was addressed. The obstacles in borrowing bank loans from SME exporters and high-interest rates were raised. A few comments on logistics and export taxes were mentioned.

Step 3: Copy comments to include in data content analysis resulted in that the most mentioned incentives to promote firms exporting being implemented recently are customs procedure reform, trade promotion support, credit support, and tax/fee policy.

The Results of Nonparticipant Netnographic Qualitative Study.

To explore the specific aspect of each incentive policy mentioned above, an in-depth interview was conducted with experts related to export activities. By applying the theoretical sampling technique, we interviewed five interviewers. The fifth interviewer provided similar information as that of previous interviewers, so we decided to stop the in-depth interview. The interview began with introducing the research purpose, the meaning of the interview, and the content to be discussed based on the views, opinions, judgments, and evaluations of each expert interviewed. Further, a commitment to ethical standards in research was also stated before the interview began. Therefore, experts were asked to give their opinions related to relevant export support policies with the general question: “Could you please share your opinions of the export support policies implemented in recent years.”“Please justify your statements,” and “Do you have any evidence supporting your arguments? Please share with us.” The answers were recorded for subsequent analysis and synthesis. The interview’s results are summarized below and illustrated in Figure 2.

The results of in-depth interviews.

The Results of In-depth Interviews of Professionals

a. Regarding to tax/fee incentives: • Mr. Nguyen Thanh T.—ITPC (Investment & Trade Promotion Centre) Specialist—stated: “Even though there is extensive information about incentives, most businesses are still afraid to go through the procedures to enjoy the benefit of the current tax/fee incentives.” • Mr. Nguyen Trong B.—the specialist at the Customs Department in Ho Chi Minh City—said: “Tax/fee incentives are greatly supported. However, it is necessary to review the tax/fee rates for items on the list of restricted exports as well as items, supplies, and raw materials subject to temporary import for re-export.”

b. Regarding to credit incentives: • Mr. Nguyen Duc D.—Specialist at Export Promotion Center in Ho Chi Minh City—stated: “Accessing and receiving credit incentives for goods export is not simple because there are too many procedures. In which, the most important proving the highly guaranteed assets, causing difficulties for small and medium enterprises (SMEs).” • Mr. Nguyen Minh H.—International payment and finance specialist BIDV—said: “The financial support for exporters facilitated by the State is beneficial. Nonetheless, it is not easy to approach credit incentives because of the specific procedures of banks different.”

c. Regarding to trade promotion support: • According to Ms. Vo Thi L.—Tax Specialist (Tax Department, District 11): “Trade promotion support is currently taking place in full swing. However, a practical solution is needed so that businesses can directly meet with partners to negotiate and discuss exporting products.” • Mr. Nguyen Van T. added: “Trade promotion activities are the main activities for exports. However, there are still many shortcomings that need to be considered in terms of people, costs, and ways of organization engage.” • Mr. Nguyen Duc D. suggested: “It is necessary to consider linking promotion activities of enterprises directly involved in meeting foreign partners and the State need to clearly show the connecting role in trade promotion activities abroad.”

d. Regarding to customs procedure reform • Mr. Nguyen Trong B. said that “Currently, the customs department is gradually reforming its administrative procedures by applying information technology. In addition, the sense of responsibility of customs officers should always be high, especially those who directly carry out export procedures.” • Mr. Nguyen Minh H. confirmed that “The export is now heavily dependent on the customs procedures. If customs do well, simplification will help businesses a lot.”

Empirical Evidence of Previous Studies

From the results of in-depth interviews with professionals, we continue to review the existing literature to ensure that our research model is consistent with previous studies.

Even though export performance is one of the most widely researched areas Sousa et al. (2008), the majority of studies have concentrated on internal factors (Chen et al., 2016), that is, firms’ marketing, networking, and innovation capabilities (Chauhan & Medda, 2020; Gupta & Chauhan, 2021; Tyagi & Nauriyal, 2017; Yi et al., 2013), human and technology-related factors (Gashi et al., 2014), top management’s characteristics (Agnihotri & Bhattacharya, 2015), and firms’ characteristics such as size, age, and productivity (Bashiri Behmiri et al., 2019; Bekteshi, 2020; Faria et al., 2020).

On the other hand, there is really a dearth of research on the effects of external factors on a firm’s export performance due to the restriction of a single-nation environment (Forte & Carvalho, 2022). To the best of the authors’ knowledge, only a few studies have investigated the external factors involving the impacts of the industry’s features (Reis & Forte, 2016), the country’s financial development, and the degree of investor protection (Castellani et al., 2022), political instability, informal competition, and corruption (Krammer et al., 2018), or government export promotion programs (Tesfom & Lutz, 2008). According to the results of in-depth interviews with professionals, we focus on four of the government’s supportive policies, as further explained below.

Tax Incentives and Export Performance

Tax incentives—favorable tax treatment for qualified research and development expenditures—are an important element of government public assistance (Tian et al., 2020). In an export-oriented economy, tax incentives are seen as more effective than direct government assistance and may thus be used globally to improve economic performance. All nations, particularly industrialized nations, employ tax incentives and create tax systems that encourage export operations to provide their resident firms with a competitive advantage on the global market. Okafor et al. (2020) used a dataset of European countries and found that regardless of the extent of availability of financing and/or financial incentives in the nation where businesses operate, firms that receive tax financial incentives perform better than those that do not. In developing nations, tax incentives are used to promote domestic production and attract foreign investment, therefore reducing the effective tax burden on export projects. For instance, by using quantitative analysis of the Motor Industry Development Program with the difference-in-difference methodology, Madani and Mas-Guix (2011) found that the tax incentives positively promote automotive exports in South Africa. However, they also noticed that exports needed time to fully react to the incentives, and the incentives’ effects lasted in the short run only. Similarly, for the mechanical and electrical industries sector in Tunisia, an increase in taxation affects negatively export performance (Teraoui et al., 2011). A strong promotion policy, such as a tax incentive, could be more effective for firms to export because it helps improve nationwide productivity (Debbarma et al., 2022). Hence, we propose the first hypothesis as below:

Hypothesis 1: Tax incentives positively and significantly affect export performance.

Credit incentives and export performance

Governments rationalize lending incentives as a method for mitigating the negative impact of financial market frictions on exporting businesses (Heiland & Yalcin, 2021). Several recent studies investigate the effectiveness of such initiatives as a means of increasing exports, value-added, and employment. Using Austrian firm-level data, Badinger and Url (2013) claimed that credit guarantee usage has positive effects on firm-specific export performance. Further, Okafor et al. (2020) found that expanding access to financial incentives for financially constrained businesses, especially during times of crisis, can considerably help to strengthen export competitiveness. Access to a credit or public financial incentives encourages export performance better in countries with greater access to credit or financial incentives than in countries with less access to credit or financial incentives Okafor (2020). In contrast, Heiland et al. (2020) found that financing limitations had a detrimental impact on both the likelihood that a business export and the proportion of exports to total sales. They demonstrated that credit limits have a significant negative impact on exports for smaller and younger SMEs, as well as those operating in countries with a less established financial system and poorer institutional environment. Hence, we propose the second hypothesis as below:

Hypothesis 2: Credit incentives are positive and significantly affect export performance.

Trade promotion support and export performance

It is anticipated that exporters’ use of export assistance programs would increase the efficacy of their operations and their strategic decisions regarding adaptation techniques (Lages & Montgomery, 2005). Government export promotion programs, such as trade exhibitions, trade fairs, and trade missions, were recognized by Martincus and Carballo (2010) to assist businesses in establishing international commercial relationships. Export promotion programs are regular components of the foreign trade policy of most nations. Businesses in both developed and developing nations frequently seek assistance and direction to find prospective export markets and prospects. Support from the outside, particularly from the government, might help domestic firms explore their export market potential and boost economic growth (Leonidou et al., 2011; Williamson et al., 2011). Trade promotion support can be divided into informational and experiential government export programs, both of which affect the SMEs’ relationship quality with both local businesses and international buyers, which also improves network promotion mechanisms and increases SMEs’ export performance (Imran et al., 2017). Similarly, export promotion programs caused an increase in export intensity and an increase in the probability of turning to the export of SMEs (Karoubi et al., 2018).

To further explain, utilizing export promotion programs allows a company to minimize operational expenses, become more lucrative, and, consequently, be more effective in its export efforts. Export support enables local businesses to participate in networking activities on foreign markets to expand worldwide (Owusu-Frimpong & Martins, 2010). Wilkinson and Brouthers (2006) found a correlation between the usage of trade fairs and programs and businesses’ satisfaction with their export success. Sraha (2015) asserted unequivocally that export assistance programs contribute favorably to the export performance of a company and improve its competitive position. Van Biesebroeck et al. (2015) stated that the Trade Commissioner Service export promotion program helped Canadian firms diversify their export destinations and increase their share in total exports. Currently, Malca et al. (2020) and Mota et al. (2021) concluded that participation in Export Promotion Programs, which encompass trade mobility, information, education, and training-related programs, does have a positive influence on the export performance of firms, especially for those firms with previous export experience. Hence, we propose the third hypothesis as below:

Hypothesis 3: Trade promotion support positively and significantly affects export performance.

Customs procedure reform and export performance

Reforming customs procedures is vital for improving the international movement of goods and services. Customs has generally fulfilled a restricted role, concentrating primarily on collecting of customs and taxes on imported goods (Freeman and Styles, 2014). Most nations joined the WTO to get access to FTAs and considerable technical and financial assistance from wealthy nations (Dacin et al., 2002). Reforming customs procedures can strengthen a nation’s capacity to defend its borders against imports from international rivals. It is all about minimizing the trade transaction costs (also known as trade barriers) associated with commercial transactions. An adequate customs process may facilitate the prompt delivery and free flow of products and services in the international trade chain, therefore enhancing the competitive advantage of a nation’s export activities (Holzner & Peci, 2011). Hence, we propose the fourth hypothesis as below:

Hypothesis 4: Customs procedure reform positively and significantly affects export performance.

Development the Measurement Scales of Latent Variables

To develop items or observable variables of latent variables, the TST (Twenty Statement Test) was used. The interviewers were asked to write down up to 20 words related to each of the factors just pointed out above. The interviewers are persons working in the field of export promotion in Ho Chi Minh City. They are employees of ITPC, Export Promotion Center (of the Ministry of Industry and Trade), officers of the Customs Department, directors, or employees of export companies located in the High-Tech Park in Ho Chi Minh City. Additionally, managers who know the export process, regulations, and operations, experts/specialists who directly handle and have regular contact with firms’ export processes also participated in the in-depth interview. The results of this step were used to develop the preliminary scales of research concepts and conduct a pilot test. A pilot test was conducted to revise survey questionnaires. The extraction method is Principal Components Analysis with Varimax rotation (Appendix) to detect invalid items to remove. Then, the questionnaire was edited and used for data collection. T final questionnaire is shown in Table 2 below.

Measurement Scale of Variables and Definitions.

Source. Synthesized by the authors.

Based on the statements presented in Table 2, the survey questionnaire was designed with two main parts:

Part 1 includes questions about the respondent’s general information and surveyed export firm where the respondent is working for.

Part 2 includes statements about export incentive policies as well as the businesses’ export performance. Respondents were asked about the similarity of the statements stated in the questionnaire with the reality of their business on a 5-point Likert scale, according to the level of agreement from the lowest (1—strongly disagree with the statement) to the highest (5—completely agree with the statement) (See Table 3).

The Scale Type of Observed Variable in Survey Questionnaire.

Source. Synthesized by the authors.

Data

Data Collection

Sampling Technique and Sample Characteristics

A purposive sampling technique was used in the survey. Data was collected through a survey using Google Forms with the support of the Export Promotion Center, the Trade Promotion Center, the Customs Department, the Trade Union, the Labor Union, joint stock commercial banks, etc., in Ho Chi Minh City, and obtained 141 valid questionnaires. The sample characteristics are shown in Table 4 below.

Sample Description.

Source. Synthesized by the authors.

The surveyed export businesses in Ho Chi Minh City are small and medium-sized enterprises with more than 10 years of export experience. The characteristics of the survey sample are the basis for explaining the research results.

Data Processing

The collected data were processed through the following steps:

Step 1: A pilot test was conducted to revise survey questionnaires. The extraction method is Principal Components Analysis with Varimax rotation (Appendix) to detect invalid items to remove. Then, the questionnaire was edited and used for data collection.

Step 2: Factor analysis and reliability test was conducted.

Step 3: Analyze CFA to check the fitness of the model, composite reliability, unidirectionality, convergent validity, discriminant validity, and extracted variance.

Step 4: Check the appropriateness of the model and test the research hypotheses.

Step 5: Do a multigroup analysis to test the difference between groups.

Reliability and Validity of Constructs

The reliability and validity of observed variables are determined based on Cronbach Alpha before being evaluated by Explanatory Factor Analysis (EFA) and Confirmatory Factor Analysis (CFA). The test resulted that all variables in the measurement model satisfy the Cronbach Alpha reliability criteria of .7, so it can be concluded that the measurement model has satisfactory reliability and can be used in subsequent analysis (Table 5).

The Reliability of Measurement Scales.

Source. Calculated by the authors.

Explanatory Factor Analysis

To conduct EFA, the collected data must satisfy Bartlett’s and KMO tests. First, Bartlett’s test was used to test hypothesis H0 that the variables are not correlated with each other in the population. Second, the KMO coefficient was used to check if the sample size was appropriate for EFA. According to Hair et al. (2010), the value of Sig. of Bartlett’s test less than .05 allows to reject the hypothesis H0, and the value .5 < KMO < 1 means that factor analysis is appropriate. The results of the tests are presented in Table 6 below.

KMO and Bartlett’s Tests.

Source. Calculated by the authors.

Next, Principal Components Analysis with Varimax Rotation was used to rotate once for each factor cluster. After rotation, the items with factor loading less than 0.5 were removed and only those with a factor loading greater than 0.5 were kept. The number of factors was determined based on two criteria:

(1) Kaiser Criterion and Eigenvalue. First, Kaiser Criterion determines the number of factors extracted from the scale, in which less important factors are removed. Second, Eigenvalue represents the variation explained by each factor. Only factors with Eigenvalue greater than 1 are kept in the model.

(2) Variance Explained Criteria: EFA is appropriate if the Total Variance Explained is not less than 50%.

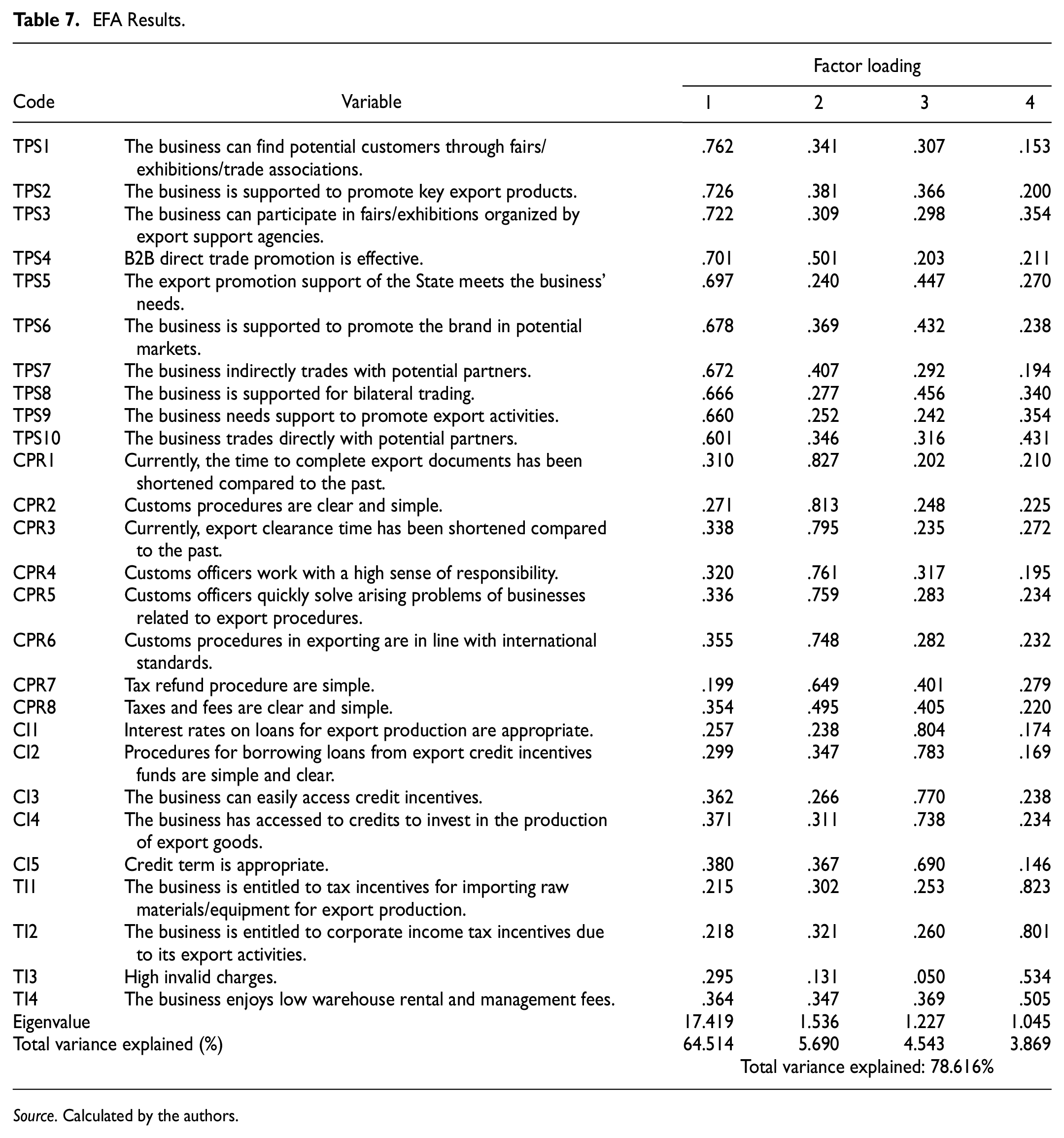

The results of EFA are presented in Table 7, showing that all 27 observed variables are separated into four factors with the Total Variance Explained is 78.616% (>50%) at an Eigenvalue of 1.045 (>1); KMO’s coefficient is 0.949 (.5 < KMO < 1) and the Bartlett’s test with Sig. = .000 (<.05). All satisfy the mentioned requirements, so all 27 observed variables were used in the CFA.

EFA Results.

Source. Calculated by the authors.

CFA and SEM Testing

SEM involves the construction of a model to represent how various aspects of an observable or theoretical phenomenon are thought to be causally structurally related to one another. The criterion for testing research hypotheses is traditionally taken at the 5% significance level (95% confidence level); however, it can also be chosen at the 10% significance level (90% confidence level) (Hair et al., 2010). In CFA analysis, considering the standard fit of the model with the data is a formal evaluation of the scale. The study used indicators such as Chi-squared, Cmin/df, CFI, TLI, and RMSEA. The model is said to be suitable for the collected data when the Chi-square test has a p-value > .05. On the other hand, the Chi-square test has limitations because it depends on the sample size. Therefore, if a CFA model (or SEM) has the following indexes: Cmin/df <4; CI > 0.90; CFI > 0.90; and RMSEA < 0.08, it can be concluded that the model is consistent with the market data. Besides, tests of Composite Reliability (CR), discriminant validity, and convergent validity of the research variables were also performed. The evaluation criteria are presented in Table 8.

CFA/SEM Indicators.

Source.Hair et al. (2010).

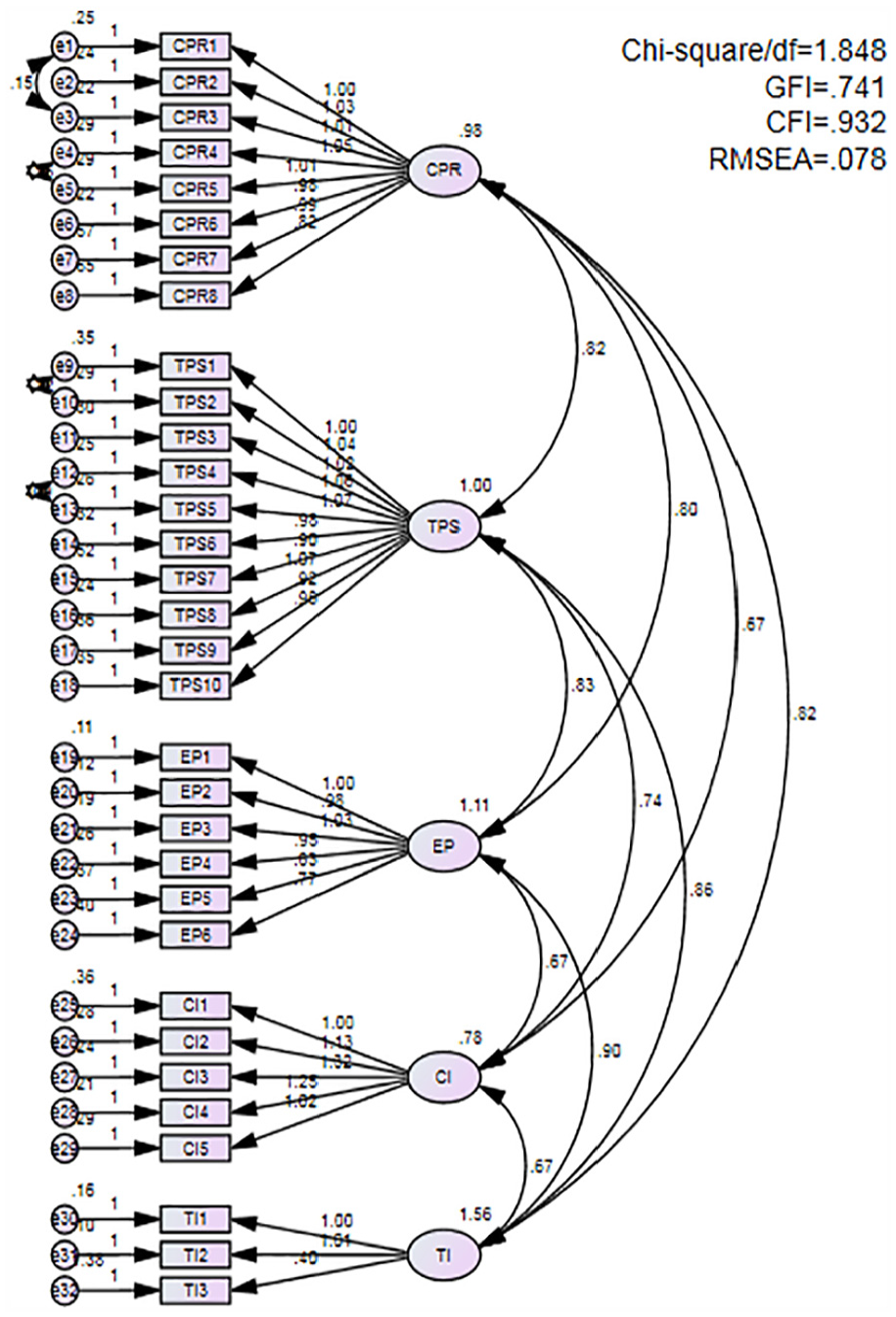

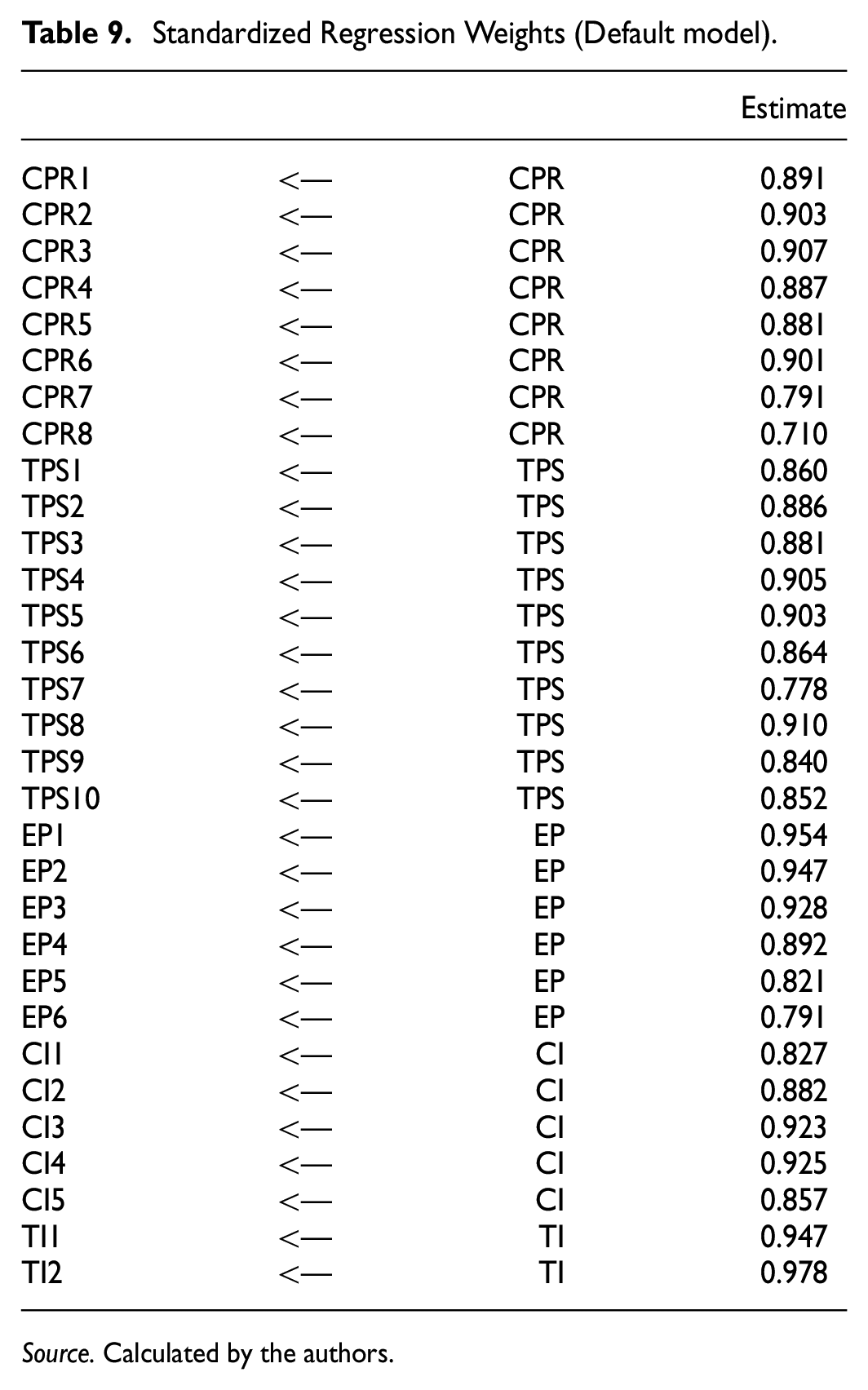

The results of the first CFA analysis (Figure 3) showed satisfactory outcomes, and TI3 is the item that was removed because of its Standardized Regression Weight of less than 0.5, and then CFA was re-performed and resulted in satisfactory outcomes as shown in Figure 4 and Tables 9 and 10.

The first CFA analysis.

The second CFA analysis.

Standardized Regression Weights (Default model).

Source. Calculated by the authors.

Goodness of Fit.

Note. ***p < .001.

Source. Calculated by the authors.

The second CFA analysis showed that the values of the standardized loading estimate of the observed variables were all greater than 0.7, so no observed variables were removed.

Goodness of Fit and Research Hypotheses

The test results show that the CR of all research variables is greater than 0.7, and the AVE of all research variables is greater than 0.5. Thus, it can be concluded that the convergent validity is satisfied. Furthermore, the MSV values are all smaller than the corresponding AVE values, and the SQRTAVE values of each variable are larger than the Inter-Construct Correlations value of that variable compared to the other variables. It can be concluded that the discriminant validity is satisfied.

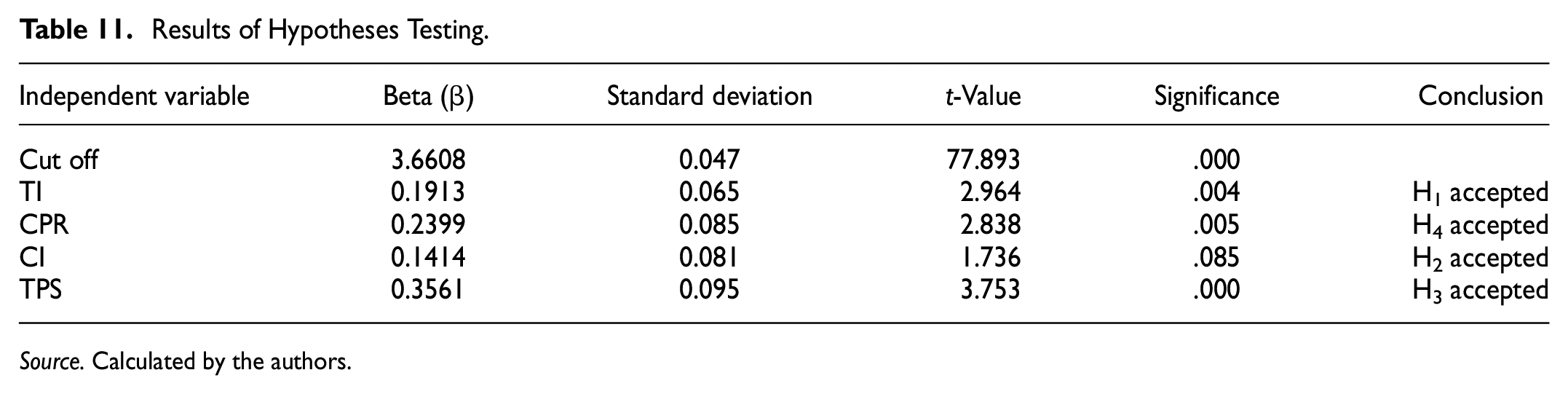

The results of testing the research hypotheses (Table 11) show that trade promotion support for businesses is the factor that explains the businesses’ export performance the most (β = .3561) at a 1% significance level. In other words, trade promotion activities positively and significantly affect business’ export performance. The second factor is Customs procedure reform that positively and significantly affects export performance (β = .2399, p-value = .005), followed by tax/fee incentives (β = .1913, p-value = .004). Credit incentives have the lowest effect on export performance at the significant level of 10% (β = .1414, p-value = .085).

Results of Hypotheses Testing.

Source. Calculated by the authors.

Finding Discussions

The policy of export-based economic development has been a policy throughout the Sixth Party Congress (1986) until now and it is the basis for the Vietnam Government to develop export support policies. Several export support policies have positively affected the export performance of enterprises in Ho Chi Minh City, as indicated in this study. Export revenues of Vietnam in general and Ho Chi Minh City in particular have grown very impressively in recent years as well as a result of the policy of international economic integration through open economic policies and increased participation in the global supply chain. The becoming a member of WTO and the signing of many bilateral and multilateral trade agreements with many international partners have brought many opportunities to expand the market for Vietnamese enterprises to penetrate foreign markets. This study was conducted to explore incentives offered by the Vietnamese Government and their impact on the export performance of export firms located in Ho Chi Minh City. Applying qualitative research methods combined with quantitative research to explore four support policies that have a meaningful impact on the export performance of enterprises in Ho Chi Minh City through qualitative research: (1) Tax support policy, (2) Credit support policy, (3) Trade promotion support, and (4) Simplify customs procedures. The study built a scale for five research variables in the quantitative research model. The study collected data from 141 exporters in Ho Chi Minh City through a survey questionnaire. Research results showed that trade promotion activities have the strongest and most positive impact on the export performance of surveyed enterprises. The second factor is the reform of customs procedures, followed by the tax/fee support policy, and finally the credit support policy. It is concluded that the supportive policies of the State play an important role in increasing the export performance of exporters in Ho Chi Minh City.

Impact of Export Promotion Activities

Export promotion activities have a positive and meaningful impact on the export performance of enterprises in Ho Chi Minh City. Our results aligned with previous studies that export promotion activities play a significant role in fostering export activities (Imran et al., 2017; Karoubi et al., 2018; Malca et al., 2020; Mota et al., 2021; Owusu-Frimpong & Martins, 2010; Sraha, 2015; Wilkinson & Brouthers, 2006). Government-designed export promotion instruments and services (EPS) are among the externally accessible tools businesses may use to enhance their export performance. For instance, EPS refers to public measures designed to support firms’ exporting activity (i.e., seminars for potential exporters, counseling, how-to-export handbooks, export financing) and market information and development programs (i.e., the distribution of sales leads to local firms, participation in foreign trade shows, market analysis preparation, and export newsletters) (Durmuşoğlu et al., 2012).

Further, export promotion activities are especially crucial for SMEs, which may lack the resources and experience to access overseas markets on their own. These SMEs may benefit greatly by participating in export promotion activities. In the survey sample, more than 50% are small and medium-sized exporters, so international marketing activities rely on the support of the Investment and Trade Promotion Center of Ho Chi Minh City (ITPC). On average, ITPC annually organizes about 100 exhibitions and fairs of large and small scale in Ho Chi Minh City. In addition, the State stipulates that the financial support level for enterprises’ expenses for participating in trade promotion activities is 50% according to Clause 1, Article 6 of Circular No. 171/2014/TT-BTC dated November 14, 2014, of the Government.

In short, export promotion efforts may be helpful to businesses in assessing the prospective demand for their goods and identifying the export prospects that are most likely to be successful since they provide knowledge about overseas markets. Activities aimed at promoting exports may also assist businesses in increasing their competitiveness in international markets. Through the provision of adequate training and assistance, exporting enterprises will be assisted in enhancing the quality of their goods, lowering their production costs, and conforming to rules and standards imposed by foreign governments (Gençtürk & Kotabe, 2001).

The Impact of Customs Procedures Reform

According to Peterson (2017), lower trade costs and the possibility for higher economic welfare among countries with fewer trade restrictions are two significant effects of customs reform. Also, on average, developed countries do better than developing counterparts on measurements of customs and border administration (i.e., trade facilitation). Trade facilitation, however, necessitates a commitment to strong regulatory governance for all nations. Overall, it is evident that despite the fact that many countries have strengthened their customs policies in accordance with the World Customs Organization’s objectives and, more recently, the WTO’s Trade Facilitation Agreement, difficulties still exist. For instance, in developing countries (including Vietnam), efforts to improve customs are hindered by inadequate infrastructure and weak regulatory environments.

Our results are consistent with the studies of Iwanow and Kirkpatrick (2007, 2009) and Portugal-Perez and Wilson (2012), which stated that custom procedure reforms did improve the export performance of developing countries. However, the cumbersome and complicated customs procedures have received too much negative feedback from exporters because they have increased costs and negatively affected the export business results of enterprises. Therefore, the government has focused on promoting the reform of customs procedures to reduce compliance costs for businesses. In that context, with the attention and direction of the General Department of Customs, the Ho Chi Minh City Customs Department has continuously innovated and perfected customs clearance processes and procedures based on applying information technology. These efforts have been highly appreciated by import and export enterprises because they contribute to increasing the efficiency of export activities. The positive impact of the reform of customs procedures on the export results of enterprises has been confirmed through the results of this study. On May 12, 2020, the Government of Vietnam issued Resolution No. 68/2020/NQ-CP on accelerating the reform of administrative procedures, reducing and simplifying regulations related to business activities.

Impact of Tax/Fee Policy

Taxes and fees related to the export activities of enterprises include warehouse and container rental fees, goods preservation fees, and transportation fees. These fees take away most of the profits earned from the business’ exports. Therefore, the tax support will stimulate enterprises to promote export activities. Our results are in line with the findings of Madani and Mas-Guix (2011), which stated that though the effectiveness of tax incentives fades over time, they still have positive effects on export performance in developing countries. However, exports need time to fully react to these incentives. Further, in accordance with the findings of Chen et al. (2006), the output of finished goods for export by the domestic firm increases when a government increases the export rebate rate, whereas the output of the foreign competitor decreases; the domestic firm’s profit increases when a government increases the export rebate rate, whereas the foreign competitor’s profit decreases. In fact, these costs in Vietnam are many times higher than in regional countries such as Thailand and Singapore. This problem stems from the weakness of the transportation system, the underdevelopment of the logistics industry, and the customs clearance time of exports.

Impact of Credit Support Policy

Although the government has a policy to support credit for export businesses, access to this capital is not easy, according to the opinion of businesses and experts. To be able to borrow working capital to fulfill export orders or invest in export production projects, enterprises need collateral. This is the weakness of small and medium enterprises because these enterprises have low asset value and are often old or have very small residual value. Moreover, to receive preferential loans, businesses need to meet the requirements of banks’ procedures, but there is no consensus among banks, so it also causes many difficulties for businesses. They often use trade credit to meet capital needs.

In the post-pandemic period, exporting firms’ access to financial incentives helped mitigate the effect of financial restraints on export activity. This study suggests that giving enterprises financial incentives and credit support policy may boost export competitiveness, particularly in an uncertain environment. Further, these results aligned with the research from Okafor et al. (2020) and Chaney (2016) that firms can access credit support or financial support can reduce barriers to entry to new markets or increase the volume of export activities. Moreover, these results also aligned with Cardoza et al. (2015) that the favorable impact of credit on exporters’ sales volume and number of product lines during the crisis proved that access to credit leads to a large boost in export revenues.

Conclusion

The research provides empirical evidence of the important role of incentive policies for export activities in Ho Chi Minh City. The export promotion policy is highly appreciated, helping exporters, especially SMEs, with accessing new markets, capturing the consumer tastes of foreign markets, promoting brands, and marketing new products. Shortening and simplifying customs procedures have received positive responses from the business community. In addition, implementing of a series of tax/fee support policies and credit support policies have brought about favorable conditions for exporters to improve their export performance. The research results also contribute empirical evidence to confirm the correctness of the contingency and institutional theories. The findings imply that the export support policies of the Vietnamese Government have brought about positive effects for Vietnamese exporters. However, this study has certain limitations, such as a small sample size (141 exporters) and carrying out in one location (Ho Chi Minh City). The weaknesses may limit the generalizability of the research results. Further research should consider the expansion of the sample with diversified locations.

Footnotes

Appendix

Rotated Component Matrix a

| Component | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| The business is entitled to tax incentives for importing raw materials/equipment for export production. | 0.275 | 0.243 | 0.271 | 0.216 | 0.712 |

| The business is entitled to corporate income tax incentives due to its export activities. | 0.331 | 0.236 | 0.281 | 0.194 | 0.704 |

| The business enjoys low warehouse rental and management fees. | 0.143 | 0.384 | 0.334 | 0.457 | 0.380 |

| Simple corporate tax refund procedure. | 0.139 | 0.638 | 0.259 | 0.388 | 0.215 |

| High invalid charges. | 0.028 | 0.170 | 0.242 | 0.084 | 0.622 |

| Clear and simple taxes/fees. | 0.097 | 0.524 | 0.344 | 0.435 | 0.202 |

| The business needs credit incentives for supports. | 0.367 | −.002 | 0.508 | 0.169 | 0.367 |

| The business can easily access credit incentives. | 0.291 | 0.206 | 0.354 | 0.733 | 0.228 |

| The business has accessed to credits to invest in the production of export goods. | 0.292 | 0.235 | 0.410 | 0.667 | 0.216 |

| Interest rates on loans for export production are appropriate. | 0.236 | 0.186 | 0.288 | 0.729 | 0.186 |

| Procedures for borrowing loans from export credit incentives funds are simple and clear. | 0.249 | 0.307 | 0.289 | 0.739 | 0.187 |

| The business meets the requirements for export credit incentives (i.e., collaterals). | 0.397 | 0.311 | 0.521 | 0.323 | 0.173 |

| Credit term is appropriate. | 0.363 | 0.288 | 0.401 | 0.586 | 0.142 |

| The business needs support to promote export activities. | 0.176 | 0.238 | 0.730 | 0.188 | 0.313 |

| The export promotion support of the State meets the business’ needs. | 0.228 | 0.247 | 0.629 | 0.471 | 0.262 |

| The business is supported for bilateral trading. | 0.271 | 0.268 | 0.622 | 0.467 | 0.275 |

| The business trades directly with potential partners. | 0.208 | 0.374 | 0.551 | 0.345 | 0.379 |

| The business indirectly trades with potential partners. | 0.322 | 0.399 | 0.566 | 0.313 | 0.163 |

| The business can participate in fairs/exhibitions organized by export support agencies. | 0.300 | 0.303 | 0.671 | 0.305 | 0.281 |

| The business can find potential customers through fairs/exhibitions/trade associations. | 0.377 | 0.312 | 0.679 | 0.281 | 0.116 |

| B2B direct trade promotion is effective. | 0.362 | 0.481 | 0.654 | 0.176 | 0.135 |

| The business is supported to promote key export products. | 0.363 | 0.367 | 0.640 | 0.365 | 0.139 |

| The business is supported to promote the brand in potential markets. | 0.306 | 0.365 | 0.597 | 0.453 | 0.180 |

| Customs procedures in exporting are in line with international standards. | 0.352 | 0.697 | 0.323 | 0.236 | 0.210 |

| Customs procedures are clear and simple. | 0.315 | 0.766 | 0.233 | 0.228 | 0.212 |

| Currently, the time to complete export documents has been shortened compared to the past. | 0.290 | 0.769 | 0.303 | 0.157 | 0.236 |

| Currently, export clearance time has been shortened compared to the past. | 0.299 | 0.739 | 0.329 | 0.190 | 0.292 |

| Customs officers work with a high sense of responsibility. | 0.405 | 0.696 | 0.231 | 0.312 | 0.160 |

| Customs officers quickly solve arising problems of businesses related to export procedures. | 0.372 | 0.698 | 0.263 | 0.273 | 0.212 |

| Ho Chi Minh City focuses on developing logistics infrastructure (seaports, warehouses). | 0.410 | 0.434 | 0.269 | 0.079 | 0.407 |

| The cost of transporting containers to the port is significantly reduced compared to before. | 0.616 | 0.323 | 0.151 | 0.493 | −.052 |

| The cost of storage is reasonable. | 0.668 | 0.357 | 0.144 | 0.479 | 0.041 |

| Public logistics service quality is good. | 0.623 | 0.417 | 0.127 | 0.430 | 0.191 |

| The storage time is shorter than before. | 0.572 | 0.458 | 0.154 | 0.464 | 0.160 |

| Storage time affected by pandemic/war | 0.331 | 0.377 | −.036 | 0.365 | 0.549 |

| Export sales have increased over the years. | 0.740 | 0.221 | 0.351 | 0.152 | 0.297 |

| The proportion of exports in total sales has increased. | 0.767 | 0.272 | 0.398 | 0.146 | 0.181 |

| The number of export markets has increased. | 0.779 | 0.227 | 0.373 | 0.181 | 0.247 |

| Exports are becoming more and more diversified. | 0.605 | 0.395 | 0.379 | 0.188 | 0.199 |

| The proportion of exported processed products has decreased. | 0.442 | 0.367 | 0.200 | 0.264 | 0.391 |

| The proportion of finished products for export has increased. | 0.618 | 0.278 | 0.298 | 0.299 | 0.276 |

| Profits generated from export activities have increased. | 0.742 | 0.233 | 0.302 | 0.246 | 0.256 |

Extraction Method: Principal Component Analysis. The items were translated from Vietnamese into English for the ease of interpretation.

Rotation Method: Varimax with Kaiser Normalization. a

Rotation converged in nine iterations.

Author Contributions

Quy T. Vo: Conceptualization, Supervision, Validation, Project administration, Visualization; Tho V. Nguyen: Data curation, Investigation, Resources; Tin H. Ho: Writing original draft, Methodology; Hien T.T. Bui: Formal analysis, Writing original draft; Khoa N.A. Le: Funding acquisition, Software.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the Vietnam National University Ho Chi Minh City (VNU-HCM), under grant number B2022-28-08.

Data Availability Statement

The data that support the findings of this study are available on request from the corresponding author. The data are not publicly available due to privacy or ethical restrictions.