Abstract

A higher efficient capital market and direct financing environment are key to excellent enterprise performance and high-quality economic development in China. In recent years, institutional investors have gradually significantly impacted market information efficiency, while the existing studies still offer different conclusions. Given this, firstly, we chose the social network analysis as the study method, taking the open-ended equity mutual funds in the A-share stock market from 2010 to 2019 as samples, constructing the shareholding networks by taking the top ten bulk-holding stocks in every sample fund’s annual report as the connection. Then, we chronologically reveal the characteristics of those networks, such as scale, density, centrality, and so on. Lastly, we empirically test the influence of the institutional investors embedded in the shareholding networks on the information efficiency, and so does the robustness check. The results show that the shareholding networks are gradually expanding in scale and increasing in density. Furthermore, institutional investors can improve stock price informativeness and promote market information efficiency through a shareholding network, and the higher the network location of institutional investors, the greater the information effect. The conclusions based on the systemic view not only enrich the research on the information function of institutional investors, broaden the field of social network theory, but also provide guidance for regulating institutional investors and improving market transparency.

Keywords

Introduction

As a typical representative of emerging markets, China’s capital market has both commonality and individuality compared with developed capital markets. In the beginning, China’s capital market was dominated by individual investors. The institutional investors were few, and the information efficiency was low at that stage. Thus, since 2001, the government has intervened in the capital market by creating a series of measures to support the development of institutional investors. By 2021, institutional investors are responsible for 70% of the circulation of A-shares, playing a crucial role in the development of China’s capital market.

Information efficiency is mostly indicated as the ability of stock price to reflection of a company’s firm-specific information (Fama & Malkiel, 1970)—The higher the firm-specific information on the stock price, the higher the information efficiency of the market. That is to say, the higher the level of market information efficiency, the stock price more accurately reflects the internal value of the enterprise, as well as the less volatility in the rate of returns. Stock price plays a signal role in guiding capital flow and authentically functions in the form of financial services to the real economy (Verma & Bansal, 2021). Acquisition and utilization of information are costly. Market information efficiency is affected by many factors, such as investor structure, information disclosure system, timeliness and accuracy of investors’ understanding of firm-specific information, the proportion of transactions based on firm-specific information, and so on (Grossman & Stiglitz, 1980).

In developed capital markets, institutional investors are more mature and efficient in trading information (Bartov et al., 2000). Institutional investors are supposed to perform better than individual investors, especially in the aspects of capital scale, information acquisition, investment experience, and decision-making quality of investment (Mishra et al., 2023; Zahera & Bansal, 2018, 2019). At the same time, institutional investors, being informed traders, incline to have improved the stock price informativeness and promoted market information efficiency (Hou & Ye, 2008; Verma et al., 2021; Wang & Wang, 2011).

That is to say, institutional investors are like the product of the market environment. Therefore, with behaviors such as worse market supervision system, inadequate investor protection behavior, insufficient information disclosure, and unequal violation cost, institutional investors may carry out to have problems of short-term speculation or even illegal acts (i.e., illegal market manipulation and insider trading), that will damage the market information efficiency (Allen et al., 2005; Li & Wei, 2014).

On the other hand, some studies believe that the impact of institutional investors on market information efficiency has contextual and time-varying characteristics (Bansal et al., 2018; Bansal & Singh, 2021), depending on different stages of development, in the form of maturity and openness (Hu & Qi, 2012; Shi & Wang, 2014). Divergent studies have noticed the emerging influence of China institutional investors and their functional structure of the market.

The current developing themes of this research field still focus on the aspects of institutional investors’ shareholding or trading behaviors in terms of market information efficiency, especially the social network theories are gradually adopted to explore the phenomenon of the capital market. This study also uses the social network analysis tool to construct the institutional investor shareholding network, and empirically test its impact on market information efficiency. The authors contribute mainly to revealing the structure of the shareholding network and its evolution characteristics from the perspective of a systemic view, which provides new evidence for the information function of institutional investors.

The conclusions suggest the individual behavioral preferences of institutional investors and their interactions, which not only enriches the research results on the relationship between joint ownership and market information, but also the shareholder coordination and market information, and thus provide more explanations on the sources of firm-specific information, expand the application fields of social network analysis. The research results of this study help improve the competence to explain the unique problems in the socialist market economy, taking Chinese characteristics as an example and should be better in solving the practical economic problems in emerging markets.

Literature Review

Suppose there are many irrational investors in the market. In that case, stock prices will be difficult to fully reflect the firm-specific information, leading to a low level of market information efficiency, which is disadvantageous to the rational flow of capital and decision-making to management teams (i.e., decisions of optimal resources allocation and risk management). Due to their advantages in information collection and processing, institutional investors are typically regarded as doing transactions based on the information and the information fusion speed. Therefore, institutional investors usually have improved market information efficiency (Wang et al., 2009). Research in the past has quite consistent conclusions on the impact of institutional investors’ shareholding or trading on stock price with information-based, as well as the impact of information fusion speed. In short, institutional investors play a positive role in improving market information efficiency.

In foreign studies, Ayers (2003) found that the shareholding ratio of institutional investors is directly proportional to the firm-specific informativeness of stock price. Piotroski (2004) found that institutional investors are informed traders, and their trading behavior can improve market information efficiency. Boehmer and Kelley (2009) also found that institutional investors’ shareholding and trading behavior increased stock price informativeness. In domestic studies, Lin and Han (2011) found that institutional investors’ shareholding can improve market information efficiency and play a positive role in maintaining market stability. Lei et al. (2012) found that when institutional investors trade based on information, firm-specific information can be quickly integrated into the stock price. Moreover, Wang and Wang (2011), who used stock price synchronicity, and Kong et al. (2015), who measured information efficiency with three variables of private information measurement, R2 and variance ratio, all got similar conclusions that institutional investors’ shareholding has a positive effect on market information efficiency.

An institutional investor shareholding network refers to a social network composed of multiple institutional investors jointly holding the same shares of one or more listed companies, in which institutional investors are nodes, and joint shareholding relationships are links. The scale of the shareholding network refers to the number of all institutional investors in the network. As institutional investors jointly hold shares (especially bulk-holding stocks), the nodes in the network establish close social relationships based on common interests. Compared with other types of relationships, the shareholding network can better reflect the group function of institutional investors (Pareek, 2012).

Currently, studies on the shareholding network of institutional investors are still few in China, which is still focusing on the construction of the shareholding network and its impact on the risk of stock price collapse and investment performance (Chen et al., 2017; Guo et al., 2018; Xiao et al., 2012). The trading behavior of institutional investors is affected by firm-specific information, and the herd effect caused by this may lead to the continuous rise of stock prices until it crashes (Shen et al., 2013). The institutional investors’ shareholding network and its spillover effect influence investment performance (Liu, 2016); the greater the difference in investment styles of institutional investors embedded in the shareholding network is, the more conducive to improving investment performance (Luo, 2020).

In terms of the relationship between institutional investors’ shareholding network and market information efficiency, it reveals the fact that the shareholding network is an important path for an institutional investor to collect and spread information, especially firm-specific information (Bushee & Goodman, 2007). Institutional investors collect and transmit firm-specific information through the shareholding network, promoting the information to be quickly integrated into the stock price, thus improving stock price informativeness. The higher status of institutional investors in the network, the greater their influence on other institutional investors and the stronger ability to transmit firm-specific information (Colla & Mele, 2010).

If institutional investors keep increasing the shareholding of certain companies, it signals that the company is doing well and will attract more investors and analysts to investigate the company, thus increasing the quantity and quality of the company’s firm-specific information, which eventually forms a virtuous cycle through the market mechanism.

Institutional investors expand their breadth and depth of firm-specific information integrated into stock prices by exploring, exchanging and using it through the shareholding networks, which leads to a greater impact on market information efficiency than individual shareholding. And the ability of institutional investors to collect and transmit information is closely related to their network characteristics (Bajo et al., 2016; El-Khatib et al., 2015). The more central institutional investors position in the network, the more they can exchange information with other institutional investors and the more information advantages they can establish (Han et al., 2014; Walden, 2019). In short, this study proposes that the shareholding network has an information effect, which helps promote stock price informativeness and thus improves market information efficiency.

Through the above literature review, the authors found it necessary to study institutional investors’ shareholding behavior and its functioning mechanisms by constructing networks with social network theories and tools. Therefore the authors try to explore the influence of the shareholding networks on market information efficiency with social network analysis, which reveals that the shareholding network positively impacts market information efficiency. The higher position of institutional investors in the shareholding network, the more information acquisition channels they have, and the stronger their ability to capture and transmit firm-specific information. Therefore, the faster the transaction is facilitated, the more firm-specific information is integrated into the stock price; the more firm-specific information, the higher level of the market information efficiency.

Network Construction and Characteristics Analysis

Among all the institutional investors, the shares held by those open-end funds account for more than half of the total shares held by all institutional investors, in which the open-end funds are the main institutional investors. In addition, under the existing institutional arrangements, the open-end funds bear greater pressure on asset liquidity and performance, so they have the stronger motivation and the ability to dig out any firm-specific information. Finally, the data on open-ended funds are informative and available, which is convenient to research. Above all, the open-end funds are selected as representatives of institutional investors and samples to construct the shareholding network. In order to avoid the interference of the warehouse building period, the funds with less than one year of establishment are eliminated.

Network Construction

The social network theory is to study a group of actors and their relationships (Pareek, 2012). In a social network, nodes represent various actors (individuals, organizations, groups, communities, and even countries.), and links represent relationships among actors. The network among nodes based on certain social relations is not only a resource exchange medium but also a mutual aid and reciprocity mechanism, which can facilitate arranging rewards and punishments. When a node is embedded in a network, its behavior is not only constrained by its goal orientation and external environment but also influenced by the behavior of other nodes directly or indirectly, formally or informally. Nodes can obtain or exchange information (especially firm-specific information) and resources, and detect the behavior of other nodes. Compared with those separate nodes, nodes embedded in the network observe and interact with each other more frequently with better intimate relationships.

The validity of investor shareholding networks has been investigated and confirmed by lots of literature; the connection between institutional investors based on joint shareholding is equal and non-directional (Pan & Zhu, 2015; Pareek, 2012; Xiao et al., 2012). The authors focus on the network characteristics of institutional investors and their impact on market information efficiency via some relatively simple, undirected and unauthorized shareholding networks.

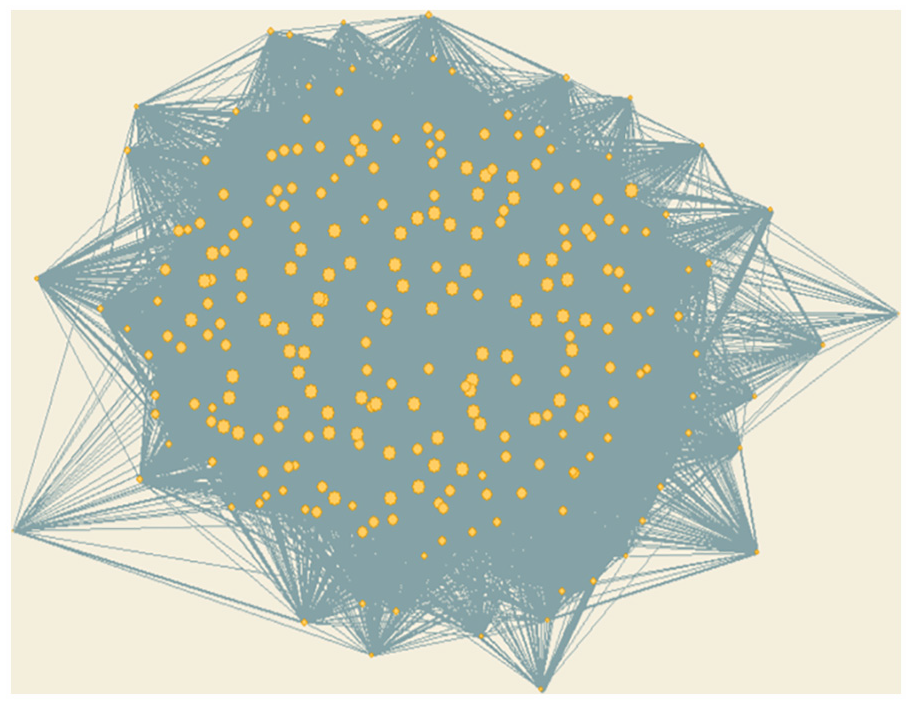

Here is the network construction process. This study uses the sample data of 2009 as an example: At the end of 2009, 102 funds, including Huaxia Growth (000001.OF), Bosera Select A (050004.OF), Harvest Growth (070002.OF), simultaneously held significant positions at eight stocks, including Yili(699887), Wuliangye(000858), and Gree Electric(000651), thus establishing a network connected by joint shareholding with these funds. In this network, the only red circular node at the center represents Huaxia Growth (070002.OF), the green square nodes represent the eight stocks it holds, and the red triangle nodes connected to the square nodes represent other funds that also hold these eight stocks. This two-mode network includes two types of nodes containing funds and stocks. The connection between the nodes represents the relationship. The rest sample funds and their top ten holdings are all added to the two-mode network of fund-stock. Thus, a complete network is constructed. Finally, all stock nodes in the network are filtered, and a one-mode network containing the funds’ node is obtained, which is the annual shareholding network of institutional investors (Figure 1). The other annual shareholding networks are constructed in the same way.

Shareholding network of institutional investors (2009).

Network Characteristics Analysis

There are many characteristics of a social network, including the number of nodes, the number of links and the centralization that measure the whole characteristics of the network, the centrality that measures the importance of node location, and the network density that measures the efficiency of network information transmission.

Referring to the shareholding network of institutional investors, the number of nodes (NUM) refers to the number of institutional investors embedded in the network, and the number of links represents the joint shareholdings among institutional investors. The minimum value of the number of links is 1, and the larger the value is. The more the joint-holdings the higher density of the network represents the level of a close relationship among all institutional investors, in which the calculation formula is: 2 × the number of links/(the number of nodes × (the number of nodes−1)). Network centralization is the difference between the centrality of the core nodes compared with other nodes in the network, reflecting the degree of difference between nodes. Through the trend of network centralization, it can be seen whether the overall structure of the network has a central tendency. Network centralization is divided into degree centralization and betweenness centralization. The degree of centrality (CED) represents the number of any institutional investor associated with other institutional investors. The higher the value is, the higher the degree of joint-shareholding of institutional investors is, and the more prominent the clustering phenomenon is. The betweenness centrality (CEB) represents the number of institutional investors between any two institutional investors. The larger the value is, the stronger the bridging role of institutional investors is. The eigenvector centrality (CEH) represents the network position of institutional investors. The larger the value is, the more core the position is. The network density represents the closeness of links among nodes in the network. It is related to the network scale and the number of links and generally decreases with the increase of the network scale.

This study investigates the evolution of the shareholding network scale of institutional investors from 2009 to 2019, including nodes and the number of shareholdings and their corresponding tendency (Table 1). The authors find that the number of institutional investors embedded in the network continues to increase during the sample period. The number of top-10-holding stocks increased rapidly during the bull market of 2014 to 2015 and decreased slightly after 2016, which is consistent with the reality that institutional investors tend to adopt a group strategy after the stock market crash. This shows the fact that with the development of the capital market, the scale of the shareholding network of institutional investors has been increasing, and so does the shareholding concentration and the institutionalization year by year.

Characteristics of the Shareholding Network of Institutional Investors.

Then, the overall characteristics of the network are investigated, including network density, centrality, and the number of links. In the sample period, the overall characteristics of the shareholding network of institutional investors are exhibited in Table 1. The results can reflect the following facts in brief.

Firstly, the network density shows a U-shaped trend of left decreasing and right increasing, which is roughly consistent with the market index. Table 1 shows that the network density maintained in a relatively stable range in most years without significant fluctuation. However, it increased during 2009 to 2012 and 2018 to 2019, reflecting the number of joint-held stocks of institutional investors increased too, and the group strategy of sticking together is becoming popular. From 2014 to 2015, the network density was at a historical bottom, reflecting institutional investors were more affected by the decline of stock prices in an extreme bear market, and their cognitive divergence on market also increased.

Secondly, the total number of links is increasing. The number of links represents the degree of joint shareholding between two institutional investors. If the number is 1, indicating that only one bulk-holding stock is joint-held by two institutional investors. This connection is relative weak, and may be broken after the next position adjustment. If the number is greater than 1, it means that the joint-held bulk-holding stock is more than one. This kind of connection is relatively close and cannot easily be terminated suddenly, so the information exchange between them will be more frequent and stable. As Table 1 shows, whether the stock of sample funds is one or more, the number of joint-holdings both shows an increasing trend, with a brief decline in the stock market crash in 2015 and a rapid recovery after then. This suggests that while the scale of the shareholding network is expanding, the relationship between institutional investors is getting closer and closer, and the network is becoming more and more stable.

Thirdly, the centralization situation presents to be stable. The centralization situation represents the degree of difference between core nodes and other nodes in the network. Table 1 shows that both the betweenness-centralization and the degree-centralization of the shareholding network remain in a stable range, indicating that the overall structure of the network is relatively stable. After 2018, the centralization shows a downward trend, indicating that the difference between the core nodes and other nodes tends to be decreasing. This is mainly because institutional investors adopt the group strategy, which leads to the increase of the core nodes; the boundary between the core and the edge becomes indistinct; the gap between different nodes becomes smaller, and the edge nodes gradually move closer to the center.

Empirical Test

Research Design

Using the top 10 bulk-holding stocks in every sample fund’s annual report as a connection, this study chose the social network analytical method and the open-ended equity mutual funds in the A-share stock market from 2010 to 2019 as samples to construct its shareholding networks. The samples of the A-share stock market are collected only from 2010 to 2019 because the authors were concerned about the fact that the impact of covid-19 showed up in the year of the beginning of 2020, which will influence the accuracy and availability of the data.

Market information efficiency refers to how much firm-specific information is contained in stock prices. At present, market information efficiency is still not usually measured by appropriate direct indicators but often by proxy indicators. When Roll (1988) studied the return rate of an individual stock, he found that the R2 fitting coefficient of the market model was low, only 0.2 to 0.3. This indicates that only a small part of the return rate could be explained by market and industry factors, while most other parts of the return rate being related to firm-specific information have not been explained. On this basis, Morck et al. (2000) proposed a concept of stock price synchronicity and took it as a proxy indicator for market information efficiency. Stock price synchronicity refers to the degree of correlation between individual stock price fluctuation and market average price fluctuation, reflecting the level of firm-specific information contained in stock price. The higher the synchronicity is, the more the stock price fluctuation is explained by the market, the less firm-specific information is contained in stock price, and the lower the market information efficiency is. He used th

Given the high recognition of stock price synchronicity as a proxy indicator of market information efficiency, we use it too. Specifically, the annual financial data of bulk-holding stocks are screened first, then the

Equation(1) shows that the trend

In order to test the impact of the shareholding network on market information efficiency, we construct the following benchmark test model as equation (2).

Among the variables in equation (2), the variable RSQ represents the market information efficiency calculated by equation (1). The variable Network represents network characteristics of institutional investors, mainly including four items of NUM CEB CED, and CEH. The variable Control represents the control ones. All the variables and their meanings are shown in Table 2. We mainly use the multiple linear regression model to estimate equation (2) and expect that the value β is significantly negative.

Control Variables and Their Meanings.

Data acquisition and Processing

The data of each variable are mainly obtained from the website of Tiantian Fund and the database of Wind. Data processing uses software like Excel2013, TXT2PAjek, Pajek, and Stata16. Excel2013 is used to store the original data and save it as. TXT format and the txt2pajek are used to convert. TXT files into .net format files. Then, the .net format files are imported into the Pajek to obtain the shareholding network and its characteristics. Finally, the Stata16 is used to carry out the empirical test. In order to prevent the adverse effect of extreme values on the results, the continuous observation data used are shrunk at 1 and 99% quantiles.

The descriptive statistics of variables are shown in Table 3. Among them, the mean value of

Descriptive Statistics of Variables.

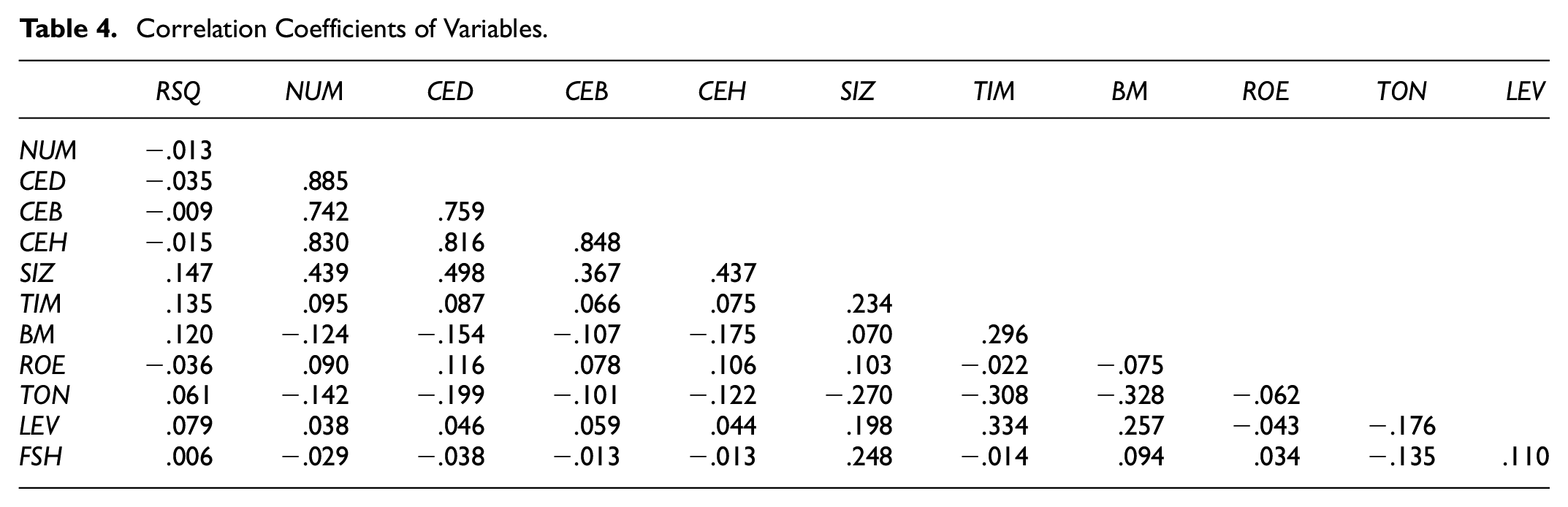

In order to test whether there is a serious collinearity problem among variables, we conduct a Pearson correlation coefficient analysis, and the results are shown in Table 4. The correlation coefficients of the four main explanatory variables are all above 0.7, showing high collinearity, indicating that the four variables can respectively represent the shareholding network characteristic and need not be adopted simultaneously. The absolute correlation coefficients between the four variables and the control variables are all between 0.1 and 0.4, far lower than 0.7, indicating that there is no multicollinearity and regression analysis can be carried out.

Correlation Coefficients of Variables.

Analysis of Empirical Test Results

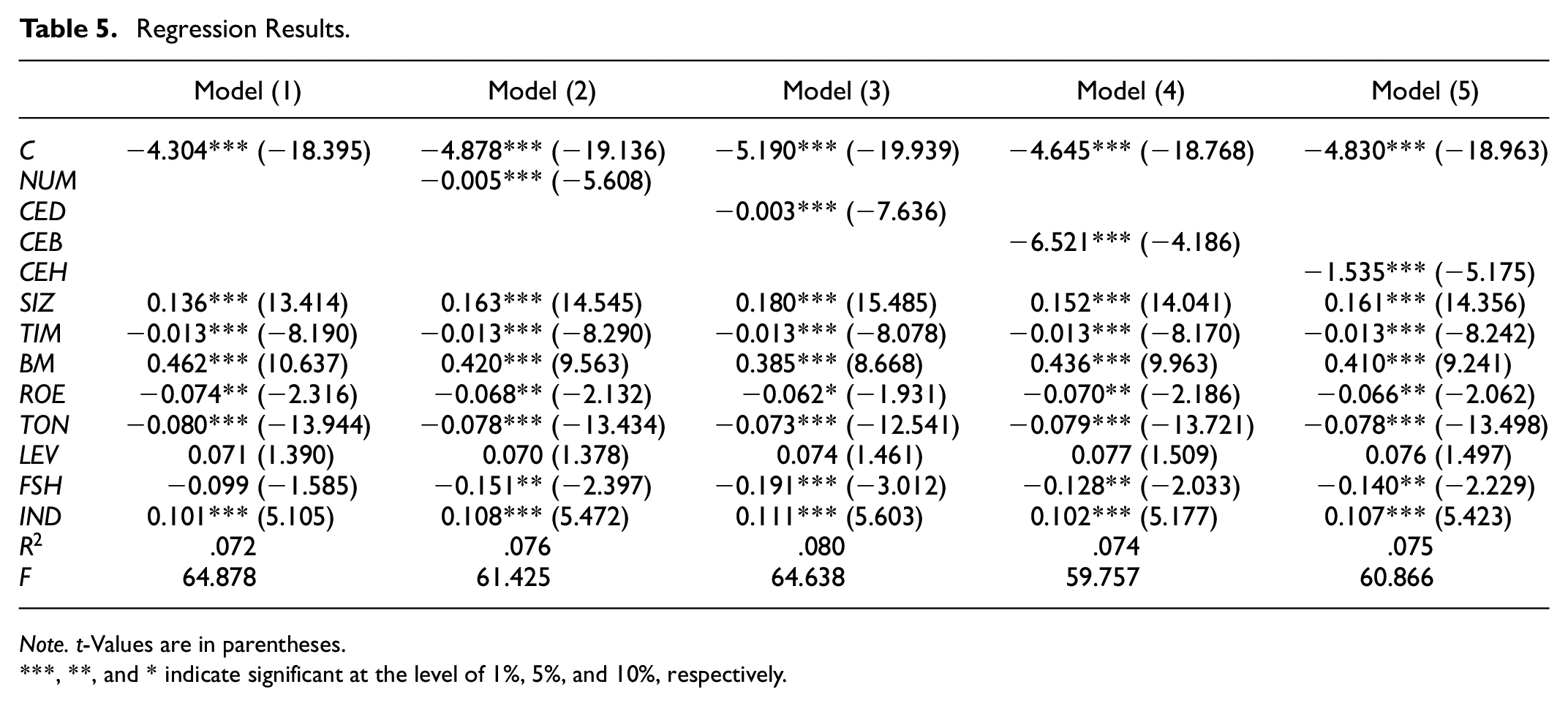

The regression results based on equation (2) are shown in Table 5. Where Model (1) shows the regression results of using only control variables without adding four network characteristic variables, and Model (2) to (5) exhibits the regression results by adding one network characteristic variable at a time based on Model (1). The variable C in the first row represents the constant term.

Regression Results.

Note. t-Values are in parentheses.

, **, and * indicate significant at the level of 1%, 5%, and 10%, respectively.

According to Model (1), the variables of company size, book-to-market ratio, and asset-liability ratio are positively and significantly correlated with information efficiency, while the variables of listing time, return on equity, turnover rate and the shareholding ratio of the largest shareholder are all negatively correlated with information efficiency. This shows that without considering the shareholding factors of institutional investors, the larger the company size is and the higher its weight in the stock index is, and the higher the consistency between stock price fluctuation and stock index fluctuation.

The less firm-specific information the stock price contains, the stronger the inhibition of information efficiency. The higher the book-to-market ratio value of a company, the worse the operating condition of the company is. The lower the attention it attracts, the less firm-specific information the stock price contains, and the stronger the inhibition of information efficiency is. The longer period a company goes public, the more available information and research materials are available. The more comprehensive and deep understanding of the company is, the more firm-specific information the stock price contains, and the greater the promotion of information efficiency is. The higher the return on net assets and turnover rate of a company are, the faster the information integrated into the stock price is, the more firm-specific information the stock price contains, and the stronger the promotion of information efficiency is. The regression coefficients of the asset-liability ratio and the shareholding ratio of the largest shareholder are not significant, and it is temporarily uncertain whether the two factors will inhibit or promote information efficiency. The above results are consistent with the expectation in Table 2 and the reality.

It can be seen from Model (2) to (5) that the relationship between these variables and information efficiency is significantly negative after including the variables of institutional investors’ shareholding network characteristics. This means that the increase of the network scale or the status rise of the institutional investors in the shareholding network will reduce the stock price synchronicity, improve the firm-specific informativeness, and then promote market information efficiency. Among them, the larger the scale of the shareholding network is, the more sufficient and rapid the information diffusion is, the faster the arbitrage speed of firm-specific information is, and the higher the firm-specific informativeness and market information efficiency are. The larger the value of degree centrality is, the more other institutional investors associated with the institutional investor are, the more firm-specific information it obtains or disseminates, the stronger the information advantage of the institutional investor is, the greater the external supervision role it plays, the higher the firm-specific informativeness is, and the stronger the market information efficiency is. Similarly, the larger the value of betweenness centrality is, the greater the bridge role of institutional investors in the shareholding network, the stronger the transmission of firm-specific information is, and the higher the market information efficiency is. The larger the value of eigenvector centrality is, the stronger the role of core institutional investors in the network is, the more remarkable the “pseudo-herding effect” of institutional investors is, and the higher the market information efficiency. Institutional investors have many advantages over individual investors, and their function can be performed better by joint shareholding than by individual shareholding. The above empirical results are scientific and receivable. The results are in line with theoretical analysis and assumptions.

In addition, the plus-minus sign and significance of regression coefficients of all control variables are unchanged after adding the variables of network characteristics, except the variable of the shareholding ratio of the largest shareholder. This shows no conflict with the impact of network characteristics on market information efficiency and the impact of various control variables on market information efficiency. Moreover, the coefficient of the shareholding ratio of the largest shareholder becomes more significant, indicating that once a company is joint-held by multiple institutional investors, its largest shareholder has a stronger motivation to dig out and transmit firm-specific information and a stronger ability to improve the market information efficiency too. It means that when institutional investors are embedded in the shareholding network, they promote themselves and the largest shareholder (usually the controlling shareholder) to positively affect market information efficiency.

Analysis of Robustness Test Results

In order to verify the robustness of the results exhibited in Table 5 and avoid possible endogenous problems, we replace or adjust several variables accordingly and then implement multiple linear regression based on the benchmark equation (2). The results are shown in Table 6. The variable C in the first row still represents the constant term.

Robustness Test Results.

Note. t-Values are in parentheses.

, **, and * indicate significant at the level of 1%, 5%, and 10%, respectively.

Firstly, we select other indicators reflecting the importance of institutional investors’ network location to replace the variables of network characteristics, such as the closeness centrality (CEC), to re-estimate equation (2). The results are shown in Model (6). The relationship between each variable and market information efficiency is consistent with the results in Table 5, indicating that the impacts of institutional investors’ shareholding network characteristics and those control variables on market information efficiency are robust.

Secondly, we replace the variable of market information efficiency. Based on the market model, we fit the adjusted R2 in equation (1) to obtain the adjusted market information efficiency variable

Finally, to avoid possible endogenous problems, the authors conduct a test by using the residuals again. Specifically, the authors regress all control variables with each indicator of the four network characteristics each time. The obtained residuals are the very part that control variables cannot explain. Then we replace those original explanatory variables and use the residuals to regress equation (2). The results shown in Model (11) to (14) are consistent with those in Table 5. That is, there is no endogenous problem, and the conclusions are robust too.

Conclusions

Institutional investors have become important participants in the capital market, especially in China, impacting the informativeness of stock prices and market information efficiency. By using the social network analysis method and the data of some selected open-end funds and their top ten bulk-holding stocks from 2009 to 2019, we construct the annual shareholding network of institutional investors, investigate the dynamic change of the network characteristics from the perspective of system view, and empirically test the relationship between the network characteristics and market information efficiency. The results show that the scale of the shareholding network has been gradually expanding. The number of institutional investors embedded in the network has been increasing yearly. It offers a positive and significant impact on market information efficiency. Institutional investors enhanced the firm-specific informativeness of stock price, reduced the stock price synchronicity, and improved market information efficiency through the shareholding network. The higher the position of an institutional investor in the network, the stronger its ability to collect and spread firm-specific information, the greater its function as an informed trader and information disseminator, and the more significant its impact on the market information efficiency. Moreover, as one of the shareholders of a company, the higher the position of an institutional investor in the network, the stronger its external supervision, and the greater its promotion effect to the largest shareholder.

Firstly, this study contributes to providing a piece of compelling evidence for the supportive policy of “unconventional developing institutional investors.” That is also one of the reform goals of China’s capital market is to continuously improve the ability and efficiency of financial services to the real economy. Institutional and networked investors can make stock prices timely and fully contain firm-specific information, which could promote stock prices to reflect the intrinsic value of the enterprise accurately and guide the capital to flow rationally and use efficiently. Secondly, institutional investors can accelerate information diffusion more quickly, improve market information efficiency more highly, and promote the development of the capital markets more healthily and stably through the shareholding network. Finally, the network characteristics of institutional investors are the cross-sectional factors affecting the fluctuation of individual stock prices, which can be used to implement security analysis and risk management. It is helpful even for individual investors because they can learn from and copy the behavior of institutional investors with high locations in the network and make their investment decisions more scientific. All these network advantages are beneficial to increase firm-specific information on stock prices, reduce market noise, and improving market information efficiency.

Directions for Future Studies and Research Limitations

However, there are some research limits to this study. Firstly, only the social connection of joint-holding is considered when constructing the institutional investor’s network. While some other social connections, such as relatives, friends, classmates, alumni, fellow townsmen and clansmen, or even more complex relationships between institutional investors and enterprise managers, securities analysts, media staff, or government officials, are not yet considered. These relationships all could choose as connections to form social networks, which will also affect the flow of information. Secondly, we highlight the cooperative relationship between institutional investors but pay insufficient attention to their competitive relationship. Institutional investors are willing to improve market information efficiency through shareholding networks because they are assumed to cooperate with each other for win-win results. However, their relationship may be competitive, which will hinder information sharing. Lastly, we take stock price synchronicity as the representative of market information efficiency, which has certain rationality. In this case, China’s capital market has emerging market characteristics so that the stock price synchronicity may differ from that of developed markets. It is not only affected by firm-specific information but also related to noise trading. The authors hope they or other researchers can further analyze those unfinished works in the follow-up study.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by National Social Science Foundation Project, grant number 19BJY249.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.