Abstract

This study examines the impact of institutional investors on the readability of corporate social responsibility (CSR) reports in the Chinese polluting industry. All available CSR reports in the listed polluting industries in China from 2010 to 2019 are analyzed to develop a readability score for each company. To differentiate the heterogenous motivation of institutional investors, we classify institutional investors into long-term and short-term investors based on their holding purpose and trading frequency. The results show that long-term institutional investors with long-term horizons have strong motivation to engage in the CSR reports disclosure. However, short-term institutional investors pursue near-term interests and they may have weak incentives to participate in the corporate governance and improve CSR report readability. Furthermore, we also find that the positive relationship between long-term institutional investors and CSR readability is stronger in polluting firms with higher environmental, social, and governance (ESG) performance. The significant role of institutional investors in promoting CSR reporting highlights the importance for polluting firms to acknowledge the needs of large and influential investors.

Keywords

Introduction

In recent years, Chinese polluting firms have undergone significant transformations in their corporate ownership structures, witnessing a surge in institutional investors like banks, mutual funds, pension funds, securities investment funds, qualified foreign institutional investors (QFII), insurance companies, social security funds, trustee companies, annuities funds, and financial companies (Wind database, 2023; Tan et al., 2022). These institutional investors possess multinational portfolios and wield substantial influence over the adoption of corporate social responsibility (CSR) policies worldwide (Dyck et al., 2019). Consequently, this trend has led to an increased focus on creating more accessible and informative CSR reports, benefiting all investors. To remain appealing to the growing capital market, polluting companies must recognize the needs and preferences of these large and influential investors (Cotter & Najah, 2012; C.-Y. Wang et al., 2021; Wei et al., 2020). Prior research has underscored the crucial role of institutional investors in shaping firms’ disclosure policies. However, little evidence exists regarding the extent of institutional investors’ influence on environmental disclosure, and the mechanisms explaining the relationship between institutional investors and CSR disclosure remain inconclusive, warranting further investigation.

Our study empirically examines the impact of institutional investors on CSR disclosure decisions within China’s polluting sector, given its environmental sensitivity and the public’s focus on CSR performance. Drawing on social license theory, highly polluting firms must uphold embedded social contracts with the community (Joyce & Thomson, 2000). CSR disclosure serves as a means to communicate social and environmental information to stakeholders and the wider community affected by the firms’ operations (Snider et al., 2003). Stakeholder theory and CSR report readability are closely related through their shared emphasis on stakeholders and their interests. Companies that embrace stakeholder theory are more likely to prioritize transparency, engagement, and accountability, which translates into creating CSR reports that are accessible and meaningful to stakeholders. By presenting ethical images through exceptional and readable CSR reports, polluting companies can enhance their legitimacy within the community, ultimately obtaining a social license and increased public recognition. Moreover, the release of CSR information can significantly influence public perception of polluting enterprises, a concern for institutional investors, as it affects their investment performance in these firms (Q. Li et al., 2013).

To investigate this, we classify institutional investors into long-term and short-term categories and examine their effects on the readability of CSR reports issued by Chinese polluting industries. Our dataset spans from 2010 to 2019, focusing on CSR reports of listed polluting companies since the issuance of the Guidelines on Corporate Social Responsibility of Listed Companies by the Shenzhen and Shanghai Stock Exchanges in 2008. The study encompasses 1528 firm-year observations, and readability is assessed based on six dimensions: table of content, length, charts, chapters, sentences, and words. Our findings indicate that long-term institutional investors contribute more significantly to improving CSR report readability compared to short-term investors. Moreover, foreign institutional investors (QFIIs) also positively impact CSR report readability. Additionally, we observe a positive association between CSR readability and firm valuation, providing evidence of long-term institutional investors’ motivation to enhance CSR readability in large polluting firms.

This research contributes to the literature in several ways. First, we build upon the existing literature (Du & Yu, 2021; Nazari et al., 2017; K. Wang et al., 2018; Xu et al., 2022) by empirically testing the impact of institutional investors on CSR readability and considering the moderating effect of ESG performance. Second, we explore the impact of different institutional investors on CSR report readability, considering the heterogeneity of these investors (see, e.g., Z. Li et al., 2021 & Xiong et al., 2023) and controlling for firm-level variables. Finally, we investigate the impact of environmental, social, and governance (ESG) scores on CSR readability in polluting firms. The integrated framework of stakeholder theory and legitimacy theory offers a comprehensive perspective on the motivation of firms to improve CSR report readability. We identify that polluting firms with higher ESG scores exhibit a stronger and more positive correlation between long-term institutional investors and CSR readability compared to polluting firms with lower ESG performance scores. In conclusion, this study sheds light on the impact of institutional investors on CSR readability and its relationship with ESG performance, offering valuable insights into the role of investors in influencing corporate responsibility practices in polluting firms.

Literature and Hypothesis

CSR Disclosure and Institutional Investors and

Companies in polluting industry are obligated to publish CSR report to communicate and engage with different stakeholders. Previous research shows CSR disclosure is used by companies to gain legitimacy and reduce risks (see, e.g., Samkin & Schneider, 2010; Zhang et al., 2021). In China, the New Environmental Protection Law (NEPL: https://www.gov.cn/xinwen/2014-04/25/content_2666664.htm) was enacted in 2015 by the Chinese governments, which is the first law that stipulates environmental information disclosure by high-polluting enterprises (C.-Y. Wang et al., 2021). Since then, great importance has been attached to CSR disclosure. Additionally, there has been an increase in the punishment of environmental violations, which has forced polluting firms to increase CSR disclosure. It can be observed that tough environmental regulation played a particularly important role in determining the level of CSR disclosure (Zheng et al., 2020). Social pressure and market punishment further promote the compliance of CSR disclosure. More voluntary CSR disclosure is derived from the requirement to ensure their legitimacy under social pressure (Kalu et al., 2016). One of the social anticipations that firms may encounter is satisfying the expectation of stakeholders. “Red Queen” effect is documented in the companies’ CSR practices which require companies to continuously improve their CSR performance to meet stakeholders demands or they will fail in a competitive environment (Tetrault Sirsly & Lvina, 2019). Furthermore, polluting companies can be subject to penalty for not following environmental disclosure, for example, not disclosing emissions information in their CSR report (Matsumura et al., 2014). Indeed, CSR disclosure can bring reputation and financial benefits to polluting companies. Instead of being labeled sticky, a dynamic model of reputation was discovered where improvement in CSR practices results in enhancement of corporate reputation over time (Tetrault Sirsly & Lvina, 2019).

Apart from social benefits, a number of studies focus on the core question that does it pay to be green. CSR disclosure are proved to be highly value relevant in emerging economies because it leads to a higher market valuation (Boubakri et al., 2021; Cheung et al., 2010; K. T. Wang & Li, 2016). In addition, CSR can reduce equity financing costs in emerging economies (Boubakri et al., 2021) and decrease the debt financing costs in China when CSR performance doesn’t exceed the optimal level (Ye & Zhang, 2011). Moreover, CSR can play a positive role in corporate financial performance for current and subsequent years (Z. Liu, 2020; H. Chen & Wang, 2011) and the influence is also significantly positive in the context of Chinese heavily polluting listed companies (Ang et al., 2022). In terms of its potential impacts on external stakeholders, Firms with good CSR practices will appeal to institutional investors and have a wider variety of investors as shareholders (W. Li & Lu, 2016). A central premise is held by some scholars that these advantages brought by CSR reports can be interconnected. The increase in reputation and corporate transparency will hence reduce the borrowing cost, attract the investors and increase sales volume (Saeed & Zamir, 2021). What’s worth mentioning, CSR disclosure not only has value-adding effects, but also acts as a value-protection role. When firms are experiencing ethical failure, CSR disclosure can positively influence market’s perception of corporate image and play an insurance-like role when trust of stakeholders is destroyed and reputation is damaged (Zhang et al., 2021).

Institutional investors in China have grown significantly and exerted great influence on corporate disclosure practice. Since early 2000s, the exponential growth of institutional investors has made them the major participants in China’s securities market (W. Li & Lu, 2016). By January 2021, according to the data of Asset Management Association of China (AMAC), domestic institutional investors hold 18.44% of the circulating market value of A-shares in China. The substantial shareholdings make it a key player in corporate governance (Cotter & Najah, 2012). Also, institutional investors influence environmental disclosure practices because they demand relevant information about corporations’ exposure to environmental risks. The demand of institutional investors for environmental information has driven the polluting sector to act more quickly than the regulators. Cotter and Najah (2012) showed that presence of institutional investors increases the expectations from companies to disclose climate change information through major corporate communications channels such as CSR reports. The needs for CSR disclosure in polluting industry and associated financial and social benefits illustrates institutional investors’ influence on CSR disclosure.

Readability of CSR Report

CSR reports provide the non-financial information mainly in the form of textual and non-quantifiable descriptions regarding firms’ CSR policies, practices and performance (Dhaliwal et al., 2011). It is of great importance to study the readability of CSR reports because it determines the communication between companies and stakeholders. The recommended guidance such as Global Reporting Initiative (GRI) can help to standardize the CSR report, but the non-financial and narrative nature of CSR reports leave managers in the polluting firms to have significant discretion in deciding the reporting form and contents (Muslu et al., 2019). The determinants of CSR readability can be various. Previous literature suggests that the readability of CSR is influenced by the CSR performance of enterprises. Firstly, companies with better CSR scores tend to issue CSR reports with higher readability (Muslu et al., 2014; Z. Wang et al., 2018). This is in accordance with voluntary disclosure theory implying that companies that perform well are inclined to disclose more information (Cao et al., 2019). Secondly, companies with worse CSR performance are inclined to release less readable CSR reports (Gao et al., 2023). Polluting companies will intentionally change the readability of CSR reports to achieve self-interests. They may deliver information vaguely to decrease the readability and obfuscate negative information, which can deliberately hide the truth and avoid public reaction toward bad news (Z. Wang et al., 2018). In addition, controlling shareholders in Chinese listed firms will provide lower quality of CSR disclosure to exploit the interests of other stakeholders (Cao et al., 2019). Hence, the controlling shareholders’ entrenchment effect on CSR reports may also decrease the CSR readability. The study analyzes the CSR reports in Chinese language. The euphemistic language feature gives more opportunities for adding complexity of information, thus increases the possibility of manipulating the CSR disclosure readability (K. Wang et al., 2018).

Hypothesis Development

Institutional investors play an essential role in improving the corporate governance structure and monitoring management, as suggested by theory and confirmed by empirical evidence (see, e.g., Gillan & Starks, 2003; Lewellen & Lewellen, 2022). However, not all institutional investors equally show their willingness or ability to serve this function and investor heterogeneity determines institutional investors’ role. Bushee (1998) divided institutional investors into three types, dedicated investors who hold concentrated portfolios, transient investors with high portfolio diversification and quasi-indexer. There are two ways in the implementation of governance mechanism strategy when organizations adopt CSR practices. One is rigorously implementing corporate governance practices and make substantial efforts to promote positive CSR results. Another is emblematically employing governance structure and “greenwashing” to improve company impression (Gupta & Das, 2022). Our first hypothesis predicts that long-term institutional investors are more connected with readability. Based on their investment horizons, institutional investors are classified into two categories, long-term institutional investors and short-term institutional investors.

First, long-term institutional investors may limit the opportunistic and self-interest behavior of management and reduce the possibility of “greenwashing” in CSR disclosure. Bushee (2001) finds that transient shareholdings are positively associated with interim earnings. Koh (2007) finds that long-term institutional ownership helps to mitigate aggressive earnings management due to their negative association with discretionary accruals. Further we posit long-term institutional investors are motivated to increase the CSR readability to suppress the possible opportunistic manipulation such as “greenwashing” in CSR practices. The improvement in the CSR readability can help readers to perceive the corporate’s true efforts on CSR expenditures, outputs and activities.

Second, long-term institutional investors can play its supervisory role to promote CSR practices and disclosure. Long-term institutional investors can contribute to governance since the incentives to monitor is driven by their long-term angles (McCAHERY et al., 2016). Long-term investors support continuing and consistent CSR objectives because they know polluting firms fulfilling CSR triggers certain expense long before it brings financial and reputational benefits (Gloßner, 2019). In addition, previous research finds that CSR disclosure can bring benefits to enterprises and the benefits of CSR disclosure can be realized with the assistance of long-term institutional investors. Companies that perform well in CSR practices tend to issue CSR reports with higher readability (Muslu et al., 2014; Z. Wang et al., 2018). CSR reports with high readability signal high future CSR performance which leads to favorable future returns (Du & Yu, 2021). Therefore, long-term institutional investors may align their interests with the benefits arising from improvement on CSR readability.

H1: There are positive relationship between the shareholdings of long-term institutional investors and CSR readability.

Institutional investors play a crucial role in driving the improvement of Environmental, Social, and Governance (ESG) performance in their investment portfolios. They are particularly interested in firms with strong ESG performance while avoiding those with ESG risks (CFA Institute Research Foundation, 2020). Previous research has already established a positive association between institutional investors and ESG performance (W. Li & Lu, 2016). When companies have low ESG performance, it can negatively impact the readability of their CSR reports. This can lead to information overload and make it difficult for stakeholders to comprehend the reports effectively (Z. Wang et al., 2018). On the other hand, companies that embrace stakeholder theory tend to prioritize transparency, engagement, and accountability. Consequently, they create CSR reports that are accessible and meaningful to stakeholders. CSR disclosure, as highlighted by Snider et al. (2003), acts as a mechanism to convey social and environmental information to stakeholders and the wider community affected by the company’s activities. In short, institutional investors’ interest in firms with high ESG performance can drive better CSR reporting practices. Companies with strong ESG performance are more likely to provide clear and informative CSR reports that facilitate effective communication with stakeholders.

We propose that ESG performance may enhance the positive relationship between long-term institutional investors and the readability of CSR disclosure. CSR performance encompasses a wide range of actions and strategies that companies adopt to make positive contributions to society and minimize any adverse impacts they may have (Z. Wang et al., 2018). Two underlying assumptions support this hypothesis. Firstly, improving the readability of CSR reports enhances information transparency and reduces the cost of processing information, leading to increased trading volume. Secondly, an increase in the readability of CSR reports signals higher future CSR performance, fostering investor trust and yielding high abnormal returns. Stakeholders pay close attention to CSR practices, and their assessment of CSR disclosure aligns with their expectations, influencing whether they reward or penalize companies (Tetrault Sirsly & Lvina, 2019).

The readability of CSR reports acts as the “voice” or information content, while ESG performance represents the outcomes of ESG practices, measuring the effectiveness of actions. When the actions (ESG performance) align with the voice (CSR language and readability), stakeholder trust significantly increases, amplifying the reputation benefits brought by improved CSR readability. In the case of polluting firms with strong ESG performance, the financial and reputational advantages of CSR readability are further strengthened. This is because higher ESG performance serves as effective certification of CSR practices, reinforcing the association with improved CSR readability. As a result, institutional investors have a stronger incentive to promote CSR readability when ESG performance is higher. Consequently, ESG performance moderates the positive relationship between long-term institutional investors and the readability of CSR disclosure.

H2: ESG performance plays a moderating role in the positive relationship between long-term institutional investors and the readability of CSR reports.

Methodology

Sample and Data

This study selects Chinese listed firms in polluting industries over the period from 2010 to 2019 according to the industry classification of the China Securities Regulatory Commission in 2012. The reason for choosing year 2010 as the starting point is that the Shenzhen Stock Exchange and the Shanghai Stock Exchange successively issued the guidelines on corporate social responsibility for listed companies in 2008. The number of enterprises that issued CSR reports before 2010 is small. With the implementation of guideline in 2010, the number of enterprises disclosing CSR reports is increasing dramatically. Web Crawler technology is used to attain the CSR report from CNINF (www.cninfo.com.cn) and we attain a sample of 1528 firm-year observation. We combine computerized textual analysis and manual reading of CSR reports to obtain the relevant indicators of CSR readability. Following Loughran and McDonald (2016), Wu et al. (2020), Ji et al. (2016), and Huang and Xu (2021), this study measures CSR report readability from several dimensions: words, sentences, chapters, length, contents, and charts, as illustrated in section 3.3. In this panel data study, we have collected cross-sectional data over a 10-year period. Although the cross-sectional sample is relatively small, it does include all available cross-sectional units. Given these conditions, the fixed effect model is considered appropriate for our analysis. The data of institutional investors are downloaded from the RESSET database, and the rest mainly comes from the China Stock Market Accounting Research Database (CSMAR database).

Institutional Investors

Following the classification of RESSET database, the sample of institutional investors consist of securities investment funds, qualified foreign institutional investors (QFII), securities companies, insurance companies, social security funds, trustee companies, annuities funds, financial companies and banks. Institutional ownership (IO) is defined as the number of shares held by institutional investors divided by the total shares outstanding, representing the shareholding percentage of institutional investors. The following models are used to determine institutional investors as long-term and short-term (Yan & &Zhang, 2009).

First, we calculate the total buy and sell volume attributed to institutional investor K:

where CR_buyk,t CR_sellk,t represents institutional investor K’s total buy and sell for period t, respectively. Sk,i,tSk,i,t-1 are the number of shares of stock i held by investor k at the end of period t and t-1. P,

i,t

P,i,t-1 are the share prices of stock I at the end of period t and t-1, and △Pi,t is the difference in share price between period t and t-1.

CR_sellk,t represents institutional investor K’s total buy and sell for period t, respectively. Sk,i,tSk,i,t-1 are the number of shares of stock i held by investor k at the end of period t and t-1. P,

i,t

P,i,t-1 are the share prices of stock I at the end of period t and t-1, and △Pi,t is the difference in share price between period t and t-1.

Second, Institutional investor K’s Churn Rate (CR) is defined as:

Third, the average churn rate (AVG_CR) of institutional investor K over the period t and t-1 is calculated as:

Finally, we classify institutional investors according to the average churn rate (AVG_CRk,t ). Short-term institutional investors exhibit the highest average churn rate, whereas long-term institutional investors reside at the lower end of the spectrum with the lowest churn rate.

Readability of CSR Reports (CSRR)

This study measures the readability from the report’s vocabulary, sentence, chapter, length, table of contents and Chart (X. Chen et al., 2018; Ji et al., 2016, and Huang & Xu, 2021).

(1) Vocabulary—We measure the complexity of the vocabulary by calculating the proportion of common words in the CSR report. The proportion of common words is calculated by dividing the number of common words by total number of the words used in CSR reports. X. Chen et al. (2018) shows the complexity of Chinese characters or vocabularies used in the financial reports influence the readers’ comprehension. The formula is: Normalized Common Word Ratio = (Current Report Common Word Ratio—Minimum Common Word Ratio of All Reports)/(Maximum Common Word Ratio of All Reports—Minimum Common Word Ratio of All Reports).

(2) Sentence—We use the average sentence length of the report to measure sentence complexity. Limited by the processing ability of human brain, people can only process five to nine words at one time (Miller, 1956). Compared to long sentence, short sentence is more refined and concise, promoting higher degree of understanding. Punctuation has significant influence on the length of sentence by its role of text segmentation. (Shriberg et al., 2000). The formula is: Normalized Average Sentence Length = (Current Report Average Sentence Length—Minimum Average Sentence Length of All Reports)/(Maximum Average Sentence Length of All Reports—Minimum Average Sentence Length of All Reports); Standardized Average Sentence Length = 1—Normalized Average Sentence Length. (3) Cohesion—We measure the cohesion of CSR report by the density of conjunctions and pronouns. Various types of conjunctions such as causal conjunctions, purpose conjunctions and concession conjunctions can help readers to facilitate reader a consistent and logical understanding in the CSR report (Wu et al., 2020). Also, the use of pronouns can highlight the subjects in the report (Gordon et al., 1993; Krahmer & Theune, 2002). The processing formula is: Normalized Conjunction Density = (Current Report Conjunction Density—Minimum Conjunction Density of All Reports)/(Maximum Conjunction Density of All Reports—Minimum Conjunction Density of All Reports). (4) Length—We measure the length of CSR report by the total number of pages and words. It is assumed that a detailed CSR report can provide rich information for the reader to understand (Luo et al., 2020). The standardization process is as follows: Normalized Report Page Count = (Current Report Page Count—Minimum Page Count of All Reports)/(Maximum Page Count of All Reports—Minimum Page Count of All Reports), where the report page count refers to the page count of the report after controlling size effects.(5) Table of content—We measure this indicator by manually decided whether the report has provided a table of content, which shows the structure of the report and helps users locate the content in a convenient way, thereby increase the readability. This is a dummy Variable testing whether a CSR Report has a table of content.

(6) Chart—We measure this chart by manually decide whether the report has provided charts for understanding. The use of chart in report can convey information to users in a more intuitive way. Also, a chart can elevate the understanding of information and increase reading interests. This is a dummy Variable testing whether a CSR Report provide charts.

Finally, the sum of value from six dimensions creates the readability of the CSR report, denoted as CSSR. A larger CSSR value indicates stronger readability of the CSR report.

Control Variables

Following Qin et al. (2018) and Pham and Tran (2019), this study selects the following variables for control: the location of headquarters (Location), the shareholding held by the largest shareholder (Top1), ownership type (State), firm age (Age), firm size (Size), leverage (Lev), return on assets (ROA), revenue growth (Growth), board size (BDSize), management size (MgnSize), proportion of independent director (Indep), CEO duality (Dual), shareholding held by management (MgnShare), etc. The detailed definition and measurement are presented in Table 1.

Variable Definition.

Empirical Model

Equation 4 is used to test the impact of long-term and short-term institutional investors on CSR readability (H1). We use fixed effect model to control for year and industry variables. In view of the economic contact between long-term institutional investors and short-term ones (W. Liu & Cao, 2018), this paper includes LIO and SIO in the same equation to examine the impact of long-term and short-term institutional investors on CSRR. The test results from Equation 4 will show the coefficient and significant level of α1 and α2.

Empirical Result

Descriptive Statistics and Correlation Matrix

Table 2 presents the descriptive statistic. First, the average value of CSRR is 5.671 with standard deviation of 1.062. The minimum and maximum values are 3.887 and 7.542, showing the readability variances among different companies’ CSR reports. Second, the average shareholding held by institutional investors (IO) is 15.38% indicating institutional investors have some voting power in the polluting companies’ long-term decision-making process. However, it is still relatively weak when compared with the average shareholding held by the controlling shareholders of 40.18%. The standard deviation of IO is 9.90% with a minimum value of 0.26% and maximum value of 79.94%. Third, the mean of SIO and LIO are 3.02% and 8.21% respectively, showing that polluting firms have more long-term institutional investors than short-term institutional investors. The result is similar to the statistics in Y. Li and Yan (2017)’s study. Approximately 25% of institutional investors cannot be categorized as either long-term or short-term institutional investors. Fourth, it shows that the proportion of qualified foreign institutional investors (QFII) is still relatively small in polluting companies with an average shareholding of 1.36%.

Descriptive Statistics.

There is a significant and positive correlation between IO and CSRR as shown in the correlation matrix (Table 3). LIO is significantly and positively correlated with CSRR while SIO is not significantly correlated with CSRR. Because institutional investors are divided into long-term and short-term ones, the coefficient between LIO and SIO is 0.782 (VIF = 6.69) showing a high level of collinearity. In addition, the correlation coefficients of the majority of control variables are less than .5 indicating a low level of multicollinearity in the model.

Correlation Matrix.

Note: The asterisks ***, **, and * indicate 1%, 5%, and 10% significance levels, respectively.

Main Regression Results (H1)

Table 4 presents the heterogeneity effects of institutional investors on CSR readability. First, Colum (1) show that institutional investors including short- and long-term ones, are positively and significantly associated with CSRR. The positive association are strengthened by the long-term investor (ß = 0.362, p < .001) as revealed in Colum (2). Long-term institutional investors hold shares with long-term horizons and have strong motivation to engage in the CSR reports disclosure. However, the coefficient of SIO turns negative and become insignificant, indicating short-termism may hinder the improvement of CSR report readability, which is shown in Column (3). Short-term institutional investors pursue near-term interests and their investment purpose is to attain the stock trading profits through frequent transactions. Therefore, they may have weak incentives to participate in the corporate governance and CSR strategy (McCAHERY et al., 2016). We observe that adjusted R square (Adj.R2) value is not high in our regression result. See, for example, the Adj. R2 value is in the range of 11% to 14% in Table 4. It is comparative to Du and Yu (2021) and Harjoto et al. (2020) result which provides Adj R2 values of less than 10% in the relationship between readability and abnormal trading volume and female leadership.

Association of Long-Term and Short-Term Institutional Investors and CSR Readability.

p < .05. **p < .01. ***p < .001.

Colum (4) shows the positive and significant relationship between QFII and CSRR. Foreign institutional investors can positively influence managers’ information disclosure decisions and motivate enterprises to enhance the information disclosure quality (Tsang et al., 2019). In addition, we also find consistent result for different types of institutional investors after control for firms’ financial and governance variables. Overall, different from short-term institutional investors, long-term institutional investors are motivated to enhance the readability of their CSR reports owing to the benefits such as corporate financial performance (Ang et al., 2022), reputation and sustainable competitive advantage (Tetrault Sirsly & Lvina, 2019), higher firm value (Boubakri et al., 2021; Cheung et al., 2010; K. T. Wang & Li, 2016), lower cost of capital (Boubakri et al., 2021; Ye & Zhang, 2011), increase in investors base (W. Li & Lu, 2016) and value-protection role in ethical failure (Zhang et al., 2021).

The Moderating Role of ESG Performance (H2)

The ESG performance data is retrieved from the Chinese Research Data Services Platform (CNRDS). CNRDS provides ESG data comprising 58 indicators in six major categories covering product, charity and community, diversity, corporate governance, employee relations and environment. Each category contains binary indicators in concern and strength dimensions. For example, indicators such as employee safety disputes or downsizing that is detrimental to ESG is identified as concerns. We construct each categorial score by adding strengths scores and subtracting total concern scores. Following Hillman and Keim (2001) and Erhemjamts and Huang (2019), a value of 1 was assigned to ESG concerns and strengths.

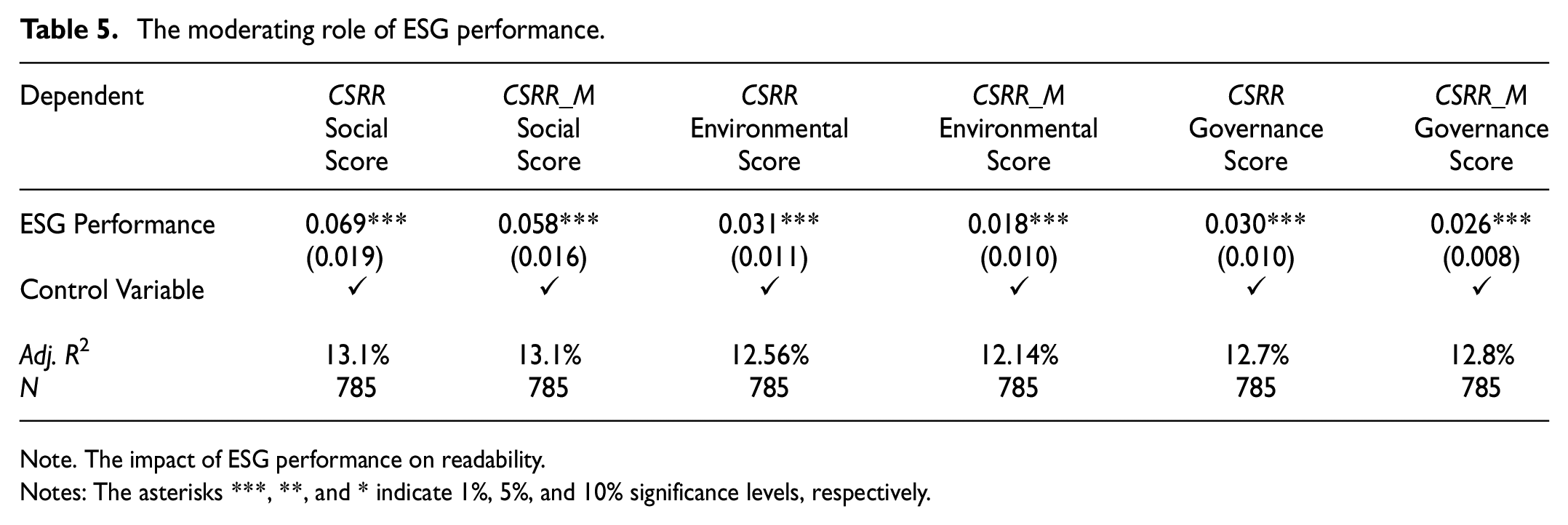

In panel (1) of Table 5, we modify CSRR and develop CSRR_M which eliminate the effects of professional jargon. The differences between calculating CSRR & CSRR_M is the inclusion of dummy variables (whether providing table of content and charts) in the formula. The CSRR_M is measured based on four aspects: the complexity of Chinese characters and words, sentence structure, length, and coherence. Following this measurement, it is assumed that a more readable CSR report will use a high proportion of common words, less complex Chinese characters, simpler sentence structure, and grammar. It is evident that all coefficients of three categories of ESG performance for CSRR and CSRR_M are significantly positive at the 1% level. The result illustrates that polluting firms with higher performance in corporate governance, diversity and environment tend to issue more readable CSR reports.

The moderating role of ESG performance.

Note. The impact of ESG performance on readability.

Notes: The asterisks ***, **, and * indicate 1%, 5%, and 10% significance levels, respectively.

Note. The relationship between long-term institutional investors and CSR readability in different ESG performance groups.

Notes: The asterisks ***, **, and * indicate 1%, 5%, and 10% significance levels, respectively.

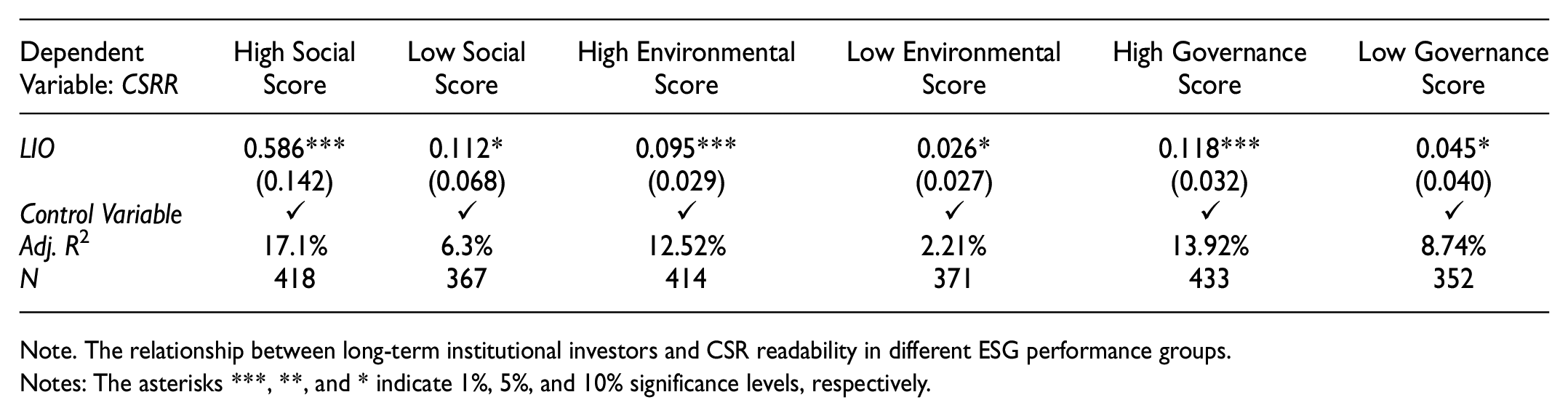

We further test the moderating role of ESG performance on long-term institutional investors and readability of CSR report. The polluting firms are divided into high- and low-performance groups according to their social, environmental and governance score. Based on the regression results in Panel (2) of Table 5, it can be observed that the coefficient of long-term institutional investors (LIO) is significant at the 0.1% level for firms with high social, environmental, and governance scores, positively impacting CSR readability. However, in the categories of low social, environmental, and governance scores, the coefficient of LIO is only significant at the 5% level. Specifically, when compared to firms with low ESG scores, the positive influence of long-term institutional ownership on CSR becomes more pronounced. For instance, the coefficient of high social score drops from 0.589 to 0.107 in the low social score category. We have identified that polluting firms achieving higher social scores, environmental scores, and governance scores exhibit a more significant and positive relationship between long-term institutional investors and CSR readability (CSRR) compared to firms with lower scores. There is no doubt that ESG performance amplify the effects of LIO on CSRR and play a moderating role. The results from panel (2) also verify the validity of hypothesis 1.

Discussion and Conclusion

This study finds significant positive influence of long-term institutional investors on the readability of CSR reports. Our results extend findings by Gloßner (2019), Kim et al. (2019), Garel and Petit-Romec (2021), Oikonomou et al. (2020) and Erhemjamts and Huang (2019) on the positive role played by the long-term institutional investors in promoting CSR. Furthermore, long-term institutional investors may restrain managerial manipulation, since readability of CSR can also be manipulated by managers to conceal the negative CSR performance and achieve personal interests (Harford et al., 2018). Dedicated institutional investors are positively linked with the adoption of strategic competitive actions compared with negative impacts associated with transient institutional investor (Connelly et al., 2010). Long-term institutional investors are dedicated to increasing CSR readability, as their influence should be classified as strategic competitive actions. One of the reasons explaining the positive relationship is improvement in readability of CSR reports can greatly promote the information transparency and the credibility of better CSR performance in the future which is consistent with the long-term horizon of long-term institutional investors (Du & Yu, 2021). Stakeholder theory encourages businesses to adopt responsible practices, maintain open communication, and strive for sustainable and mutually beneficial relationships with their stakeholders. Legitimacy theory, on the other hand, focuses on how a company’s actions and operations are perceived and accepted by society. It suggests that organizations often engage in activities such as social and environmental reporting, corporate social responsibility initiatives, and stakeholder engagement to demonstrate their alignment with societal norms and values. Both stakeholder theory and legitimacy theory acknowledge the significance of considering broader societal impacts and engaging with diverse stakeholders (Phillips, 2003). They share the common objective of enhancing a company’s reputation and social standing through the display of responsible and ethical behavior (O’Donovan, 2002). Effectively managing stakeholders can indeed help companies maintain and bolster their legitimacy, as stakeholders typically anticipate responsible and ethical conduct from businesses.

In summary, the transparency and credibility achieved through improved CSR readability can yield numerous advantages for the company. It can attract responsible investors, enhance brand reputation, increase consumer engagement, boost employee morale, foster innovation, and lead to potential cost savings. These collective benefits contribute to the company’s long-term financial benefits and establish a strong reputational advantage in the market. Our paper contributes to testing one of the causes of firms’ CSR readability by examining the hypothetical corporate ownership structure that may affect CSR disclosure. We complete previous research by investigating whether differences in shareholders’ perspective can affect CSR readability.

Practical Implications

Important managerial implications in many aspects of this study are as follows. For regulators or policy makers who desire to improve information transparency and effectiveness of information disclosure in the area of CSR reports, it’s appropriate to encourage a substantial holding by long-term institutional investors in polluting companies due to its significant impact on the improvement of CSR readability. Polluting companies which are the supporter of the readable CSR reports believe that their efforts will be valued by long-term investors who will also drive further improvements in CSR disclosure. Non-institutional investor can also reap the benefit of elevated share prices and reduced downside risk. The evaluation of ESG performance in China is still developing and the lack of consistency problem also exits in Chinese market. Thus, caution should be exercised when these ESG ratings is used to draw conclusion (Chatterji et al., 2016). What’s more, endeavors should be made by polluting firm to promote its ESG performance because the positive effect of long-term institutional investors on CSR readability is strengthened in firms with a high ESG performance.

Footnotes

Acknowledgements

The authors would like to thank Xinying Qiu, M. Huchinsion, Adrian Cheung, Mingyue Pang and the anonymous reviewer for suggestions that greatly improved the article.

Author Contribution

Conceptualization, T. Lin and Y. Jin. Methodology, T. Lin and Y. Jin. Software, Y. Jin and Q. Lin. Validation, T. Lin and Q. Lin. Formal Analysis, T. Lin. Investigation, T. Lin. Resources, T. Lin. Data Curation, T. Lin. Writing—Original Draft Preparation, T. Lin and Y. Jin. Writing—Review & Editing, T. Lin., R. Yang and Q. Lin. Visualization, T. Lin. Supervision, T. Lin and F. Gao. Project Administration, T. Lin. and R. Yang. Funding Acquisition, T. Lin and F. Gao

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is supported by the Humanities and Social Sciences Fund of China’s Ministry of Education [grant numbers [20YJA630041& 20YJC820014], the grant from Guangdong University of Foreign Studies [grant numbers [299-X5219010] and the General Project of Philosophy and Social Science planning of Guangdong Province (GD19CFX03).

Ethics Statement

This is not applicable.