Abstract

The premise for institutional investors to participate in firm innovation governance and promote firm innovation’s positive role is that institutional investors have specific decision-making power and are willing to participate in firm innovation governance. Therefore, the influencing factors of institutional investment shareholding stability are an important issue. This study investigates the impact of business connection, risk preference, policy factors, market factors, and firm factors on institutional investors’ shareholding stability using regressional analysis based on the samples of Chinese A-share listed firms from 2014 to 2017. The main findings show that institutional investors with higher business connections, risk preferences, and performance ranking intensity have poor shareholding stability. The reform has significant investment constraints on non-risk preference institutional investors but has insufficient investment constraints on risk preference institutional investors. The substitution and interaction between firm factors and the natural endowment of institutional investors occur alternately. This study’s results provide important policy implications to strengthen related business supervision between institutional investors and shareholding firms. The policy implications include relaxing the investment proportion restriction and establishing a market-oriented performance ranking and institutional investors’ evaluation mechanism.

Keywords

Introduction

As early as 2001, China put forward the “unconventional development of institutional investors” strategy. It has formed a diversified pattern in which more than ten institutional investors, such as securities investment funds, brokerage financial products, private equity funds, and QFII, have been jointly promoted and developed. With the increase of institutional investors’ types and numbers, the institutional investors’ heterogeneity becomes a hot topic. Brickley et al. (1988) first studied the heterogeneity of institutional investors. Whether there is a business relationship between institutional investors and firms, institutional investors are divided into pressure-sensitive and pressure-resistant types.

Since then, the literature on the definition and division of institutional investors’ heterogeneity has gradually enriched. Del Guercio (1996) defines heterogeneity as different institutional investors’ investment behavior according to their actual situation. Bushee (2001) divides institutional investors into short-term, quasi exponential, and focused on cluster analysis based on the diversification of institutional investors’ portfolios. Based on Bushee’s (2001) research, Koh (2007) adds some institutional investors’ characteristics in the new environment and divides institutional investors into short-term and long-term types.

According to the standard of supervision cost, Almazan et al. (2005) divide institutional investors into positive and negative types. Chen et al. (2007) divide institutional investors into the transaction and stable types, considering the two factors of shareholding ratio and holding period. In China, the study of institutional investors’ heterogeneity is relatively later. The institutional investors’ heterogeneity includes the optimistic type and negative type (Li et al., 2011), pressure-resistant type and pressure-sensitive type (Yi et al., 2011), long-term type and short-term type (Ye et al., 2012), and the stable type and trading type (Niu et al., 2013).

Heterogeneity is a concept opposite to homogeneity, which mainly refers to the differences in composition and characteristics of different substances or individuals in the same kind of substances. Specific to institutional investors, different institutional investors have differences in shareholding preference, scale, and strategy called institutional investor heterogeneity. The core issue of institutional investors is the change of ownership ratio within a certain period. This study’s motivation is to explore the essence of institutional investors’ shareholding stability by representing institutional investors’ investment preferences based on the existing research on institutional investors’ heterogeneity.

The investment preference of institutional investors is a permanent research topic. Merton (1987) puts forward the hypothesis of “investor recognition” earlier. He argues that under the condition of incomplete information, investors cannot fully recognize all securities. Therefore, investor recognition is an essential factor in determining the allocation of market resources. Most of the existing studies take investor recognition as an independent variable and examine the impact of different investor recognition levels on different aspects of the firm, such as firm value (Green & Jame, 2013), share issuance (Autore & Kovacs, 2014), share price (Wang et al., 2018), and asset pricing (Hacıbedel, 2014).

The recognition of investors should be empirically reflected in the behavior of investors. Institutional investors have advantages in professional knowledge, information, and capital, and their investment decisions are more rational, which has positive significance for stabilizing the market and improving efficiency (Lei et al., 2011). Prior studies discuss institutional investors’ governance effect in many aspects and fully affirm institutional investors’ critical role in the capital market, such as firm value (Li & Han, 2014; Zhu & Ni, 2014), share market performance (Bodnaruk & Ostberg, 2009; Liu & He, 2016), investor protection (Lei et al., 2011), governance level (Broochin & Yang, 2017; Helwege et al., 2012; Hutchinson et al., 2015), investment and financing efficiency (Attig et al., 2012; Liang, 2018), information quality (Attig et al., 2013; Hsu et al., 2016; Yang et al., 2014), and earnings management (Gao & Chen, 2017; Lin et al., 2014; Sakaki et al., 2017).

However, the market is not entirely efficient. Therefore, although institutional investors have additional advantages over individual investors, they cannot be entirely rational. Therefore, institutional investors must consider different investment decision-making factors and form different investment preferences (Aggarwal et al., 2005), such as corporate governance preference (Wang et al., 2011; Yeh, 2018), information transparency preference (Bird & Karolyi, 2016; Bushee, 2012), dividend policy preference (Huang & Paul, 2017; Jain, 2007), and social responsibility preference (Mahoney & Roberts, 2007; Zhang & Xie, 2018).

With the rapid development of institutional investors in China, institutional investors’ shareholding stability benefits are highlighted. Therefore, it is necessary to analyze institutional investors in-depth to explore their positive value in improving corporate governance mechanisms and capital market operation constitution (Wang & Jia, 2019). Therefore, the investment preference of institutional investors is an essential factor affecting the stability of shareholding.

This study makes several contributions to the existing literature. First, this study divides institutional investors’ investment preferences into the natural endowment and acquired factors and tries to determine both institutional investors’ shareholding stability. Second, this study confirms that institutional investors are not a single type, showing partial stability or partial trading, a random distribution state. The influencing factors of institutional investors evolve with the change of environment, which breaks the previous research that a specific type of institutional investors has been defined as a type for a long time.

Third, this study provides a new perspective to examine firms’ financing difficulties from the supply side as institutional investors are stable or trade-biased in a specific period. Stable institutional investors play a more critical role in alleviating the financing difficulties of firms. Finally, the national policy needs to guide institutional investors to make a long-term investment.

The remainder of this paper is organized as follows. An overview of the natural endowments, acquired factors, and institutional investor shareholding stability is presented in the following section. From this, hypotheses are developed. Then, in section 3, the research design is described, including the variables measuring the institutional investor shareholding stability and the control variables used in the analyses. Section 4 provides preliminary descriptive results and presents the analysis’s main results regarding natural endowments and acquired factors on the institutional investor shareholding stability. Finally, the conclusions and policy implications are presented in section 5.

Theoretical Analysis and Research Hypotheses

The Effect of Natural Endowments on Institutional Investor Shareholding Stability

Business connection

Business connection refers to a relational transaction mode in which firms and their business partners are based on business interests and aim to reduce transaction costs. Some institutional investors’ business nature determines their possible business connections with firms, such as the securities brokerage that operates the securities. Such securities brokerage primarily underwrites, buys, and sells securities, giving them a natural business connection with firms. Nevertheless, the securities investment funds raise the fund to form the independent fund property by selling fund shares and carrying on the securities investment through asset portfolios. Thus, securities investment funds have no business connection with firms.

Yan and Zhang (2009) recommend that institutional investors with information advantages have a strong ability to evaluate. These institutions use their information advantages to trade frequently. Institutional investors with business connections to the firm are more likely to have access to their shareholding firms (Deng et al., 2014) and are characterized by short-term duration, small scale, and low proportion. Such institutional investors pay more attention to short-term profits (Dong & He, 2016).

In general, the business connection of institutional investors is related to their business nature. Institutional investors with business connections likely to prefer trading types to reduce the scale and duration of shareholding. Institutional investors without business connections possibly prefer a stable type, relatively large shareholding, and rather a long shareholding time. Accordingly, this study puts forward the hypothesis as follows:

H1: Business connection has a significantly negative impact on institutional investor shareholding stability.

Risk preference

Facing the investment risk, different institutional investors have different preferences. The social security fund is essentially a special fund set up and raised by the state through legislation to solve social security problems. The social security fund related to people’s livelihood tends to avoid risk by paying more attention to investment safety than other institutional investors.

On the other hand, the securities investment fund investors have a relatively low entry threshold, weak liquidity of their funds, weak risk resistance ability, and high demand for the redemption fund assets. Therefore, either from the fund investors themselves or the fund’s response to the asset redemption, the securities investment fund must invest in the less risky firms to meet the assets’ liquidity (Abarbanell et al., 2003; Covrig et al., 2006).

Insurance funds are essentially liabilities to the policyholders, with a mandatory obligation to repay principal and interest at maturity. Once the insurance firms are challenging to repay the principal due, their operation has a significant impact. The central funds of non-insurance firms come from the equity funds that investors hand over to institutional investors based on the principal and agent’s relation. There are no compulsory demands for the principle from investors. In other words, investors of non-insurance firms allow an inevitable loss of investment. Therefore, insurance firms in the investment also often show a risk aversion, tend to stable shareholding (Bushee et al., 2014; Piccioni et al., 2012).

For brokerage financial products, private equity funds, and other private-equity institutional investors, the target customers are high-income groups with a particular ability to take risks, risk preference, and preference to gain profit through trade (Falkenstein, 1996). Summarizing the above analysis, the second hypothesis of this study is proposed as follows:

H2: Risk preference has a significantly negative impact on institutional investor shareholding stability.

The Effect of Acquired Factors on Institutional Investor Shareholding Stability

Policy factors

To protect institutional investors’ interests or stabilize the capital market, regulators set restrictions on the proportion of funds invested in a single product by institutional investors. In the current laws and regulations, securities investment funds, social security funds, insurance firms, and brokerage wealth management products are subject to the specific provisions of the relevant laws on the proportion of investment in a single share. The restrictions are relatively stringent. For example, the proportion of private equity funds investment in a single share is mainly limited by the trust contract, which means that the restrictions are relatively low or investment is relatively free.

Investment restrictions make institutional investors reluctant to deviate too much from the base level when making investment decisions (Cao et al., 2017). Zhang (2013) finds that insurance firms significantly prefer higher liquidity shares when the investment scope restriction is relaxed. Zhao and Wu (2010) have similar findings that shareholders of insurance firms, especially those in insurance firms with poor operating performance, appear to adopt riskier investment strategies to endanger policyholders’ interests when investment restrictions are relaxed. Therefore, appropriate investment restrictions improve the shareholding stability of institutional investors. This study puts forward the third hypothesis as follows:

H3: Investment constraints have a significantly positive impact on institutional investor shareholding stability.

Market factors

Many institutional investors with the profit-making object are burdened with peer competition pressure to win customers’ funds. The competition is concentrated in the annual performance ranking. The fund providers of securities investment funds, brokerage wealth management products, and private equity funds have the primary goal of pursuing high investment returns. To attract more investors to invest in their products, institutional investors such as securities investment funds have the impetus to achieve higher investment performance than their competitors, reflecting more performance ranking pressure. Investment becomes the main business of insurance firms, leading insurance firms to have more significant performance ranking pressure.

The investment of social security funds primarily aims to maintain and increase the value of funds. Therefore, there is less competitive pressure among institutions of social security funds. A higher ranking attracts many investors to gain high returns (Zhu & Wang, 2016). With short-term performance ranking under the incentive mechanism, fund managers often adopt short-term investment behavior (Peng & Yang, 2013). Due to top-ranked performance’s reputational effect, fund managers choose risky portfolios (Aikman et al., 2015). Accordingly, the performance ranking pressure significantly affects fund managers’ investment behavior and affects shareholding’s stability. This study puts forward the fourth hypothesis as follow:

H4: Performance ranking has a significantly negative impact on institutional investor shareholding stability.

Firm factors

Profit-seeking is common. Rational actors, institutional investors make the best shareholding decision according to the potential shareholding target analysis based on the information already available. Due to profitability representing firms’ ability to obtain profits, the more substantial firms’ profitability, the greater the investors’ benefits. Thus, profitability is an essential indicator for institutional investors to consider for investment.

In general, institutional investors invest in profitable firms because of being easier to achieve their shareholding targets. In addition, given the impact of turnover costs, institutional investors are more inclined to hold on to their holdings. Song (2015) argues that improving firm profitability greatly relieves share volatility and enhances shareholding stability. Non-independent institutional investors prefer firms that invest their limited cash resources in their business dealings without giving away dividends (Brickley et al., 1988), indicating their profit-making preference through business dealings. In general, with more robust profitability, institutional investors bear less risk. Summarizing the above analysis, the hypotheses of this study are proposed as follows:

H5: Firm profitability has a significantly positive impact on institutional investor shareholding stability.

H5a: In institutional investor shareholding stability formation, firm profitability has complementary effects with business connection and substitution effects with risk preference.

Firms with strong growth ability generally have long-term development strategic targets, a strong team, and a set of useful and practical management systems. These advantages attract institutional investors to invest more funds for them. From the investors’ perspective, growth represents future investment opportunities, which brings investors a long-term valuation premium, increasing the likelihood that investors obtain gains in the future. Firm growth also leads institution investors to reserve more patience to wait and see future profits, thereby increasing their holdings’ stability. Xie (2012) finds that firms’ growth ability has a relation to the shareholding behavior of institutional investors. Li (2016) finds that firm growth becomes a more concerned indicator of institutional investors. However, institutional investors with trading purposes have short holding terms and frequent trading, mainly pursue short-term benefits, and fail to emphasize listed firms’ long-term operation (Yan & Zhang, 2009). On the other hand, stable institutional investors have a long-term value investment concept, are willing to invest in long-term development, and prefer higher-growth firms.

Business dealings with shareholding firms are the primary source of profit for non-independent institutional investors. Better-growing firms often use funds to expand the scale of investment to enhance their future value and often face severe financial constraints that are not conducive to developing their business dealings. Nevertheless, independent institutional investors pay more attention to the long-term development of shareholding firms (Li, 2016). Institutional investors with risk preferences have a relatively large ability to bear risk, prefer risk-oriented firms, and tend to short-term investment, capital fast in and out for investment returns. Thus, the shareholding stability is weakened. Summarizing the above analysis, the hypotheses of this study are proposed as follows:

H6: Firm growth has a significantly positive impact on institutional investor shareholding stability.

H6a: In institutional investor shareholding stability formation, firm growth has substitution effects with business connection and risk preference.

According to the agency cost theory, the lower the governance level, the higher the agency cost, which means the higher the institutional investors’ cost to participate in corporate governance. As a result, institutional investors are reluctant to pay excessive fees to intervene in firms. As a result, such institutional investors are less likely to participate in corporate governance. Nevertheless, they tend to invest in listed firms with higher levels of governance (Tan & Fu, 2009). Also, the improvement of the corporate governance level significantly enhances the liquidity of firm shares (Wei & Lei, 2011), which also attracts institutional trading investors to a certain extent. Thus, institutional trading investors are more inclined to hold shares of firms with a higher corporate governance level.

Furthermore, Wang (2014) illustrate that a suitable corporate governance mechanism significantly reduces the probability and scale of related transactions. Therefore, better corporate governance effectively restrains the collusion effect between executives and institutional investors. On the other hand, poor corporate governance increases the uncertainty of firm fundamentals. This study puts forward the hypotheses as follows:

H7: Corporate governance level has a significantly negative impact on institutional investor shareholding stability.

H7a: In institutional investor shareholding stability formation, corporate governance level has substitution effects with business connection and risk preference.

Prior studies demonstrate that high-quality information disclosure weakens information asymmetry, reduces the financing costs and performance volatility of firms, and improves investor protection (Li & Wang, 2011). Also, many previous studies affirm the impact of information disclosure quality on investors’ investment decisions (Wang, Chen et al., 2017). The information disclosure transmits the correct, accurate, complete, and useful information to the public on time.

Data from firms with high information disclosure quality has little difference in investors’ information collected and mastered. As a result, investors investing in such firms bear a relatively small unknown risk. On the contrary, investors investing in low-quality information disclosure firms must take a rather large unknown risk. Therefore, high-quality information disclosure promotes institutional investors’ holding stability to a certain extent and increases the relative number of stable institutional investors.

Non-independent institutional investors have easier access to firms’ private information because they already have or want to have business connections with the holding firms (Deng et al., 2014). Non-independent institutional investors are less concerned about a firm’s information disclosure quality than independent institutional investors. From the perspective of risk preference, institutional investors with neutral risk preference tend to favor firms with higher information disclosure quality and maintain a more extended time series of concern. This study puts forward the hypotheses as follows:

H8: Firm information disclosure quality has a significantly positive impact on institutional investor shareholding stability.

H8a: In institutional investor shareholding stability formation, the firm information disclosure quality has complementary effects with business connection and substitution effects with risk preference.

Institutional investors investing in firms enjoy the dividends nevertheless bear certain risks at the same time. Ji and Du (2017) illustrate a significantly positive relationship between institutional investors’ overall shareholding and firms’ risk-taking. However, from the perspective of institutional investor shareholding stability, the scale of firm financial risk significantly affects institutional investors’ shareholding decision-making. Stable institutional investors have a relatively stable shareholding. The shareholding ratio of stable institutional investors is less affected by the scale of firm financial risk.

Trading institutional investors who have a great degree of speculation concentrate on the scale of immediate returns and trade relatively frequently, frequently adjust the proportion of shareholdings to deal with the financial risk according to the scale of firm financial risk. But in general, the greater the firm’s financial risk, the more dangerous its operation. Consequently, the shareholding stability of the institutional investors is weakened correspondingly, following an increase in the proportion of trading institutional investors.

Institutional investors who have no business connection with the shareholding firms have the motivation to actively participate in the firms’ management decision to obtain long-term benefits and are more willing to support the managers to choose some projects with higher financial risk but can enhance the firm value. Ji and Du (2017) demonstrate that different institutional investors have different abilities to take on firms’ financial risks. Trading institutional investors prefer to regard firm financial risk as a natural attribute. This study puts forward the hypotheses as follows:

H9: Firm financial risk has a significantly negative impact on institutional investor shareholding stability.

H9a: In institutional investor shareholding stability formation, firm financial risk has substitution effects with business connection and complementary effects with risk preference.

Compared with firms with relatively low value, firms with high values obtain higher capital input and more net present value of profits, favorably promoting the shareholding stability of institutional investors and correspondingly increasing the relative proportion of stable institutional investors. The shareholding ratio of institutional investors is also affected by firm value. Institutional investors are more assured to invest more funds for firms with a higher value. Stable institutional investors are more cautious and stable and generally fail to make a more significant response to the change of firm value. Therefore, the firm value has a relatively significant impact on the shareholding ratio of trading institutional investors.

Compared with independent institutional investors, non-independent institutional investors are less motivated to promote firm value for long-term gains through active corporate governance participation. Instead, non-independent institutional investors prefer to echo firm management decisions to obtain benefits of business dealings, and therefore have fewer shareholding incentives to high-value firms. Despite different risk preferences, all institutional investors are concerned about firm value. Nevertheless, institutional investors with risk preferences pay more attention to the short-term market performance of firms. Driven by benefits, stabilizing the market is not undoubtedly the spontaneous target behavior of institutional investors (Cai & Song, 2010). Instead, institutional investors face the choices between value investment and short-term speculation. This study puts forward the hypotheses as follows:

H10: Firm value has a significantly positive impact on institutional investor shareholding stability.

H10a: In institutional investor shareholding stability formation, firm value has complementary effects with business connection and risk preference.

Research Design

Sample Selection and Data Sources

Based on the samples of Chinese A-share listed firms from 2014 to 2017, this study adopts the following selection criteria: (1) excluding the financial industry (as institutional investors include financial institutions. The accounting system of financial firms is different from that of non-financial firms. Financial listed firms need to be eliminated) and ST (which is the Chinese listed firms with losses for two consecutive years) or ST* (which is the Chinese listed firms with losses for three consecutive years and faced with delisting risk) listed firm sample (i.e., ST or ST* listed firms have abnormal profit and firm value. These two types of firms need to be eliminated to avoid the heteroscedasticity of variables); (2) removing the samples with three consecutive years shareholding ratio of 0 and unchanged, and listing for less than 3 years; (3) excluding the samples that do not fully include institutional investors such as securities investment fund, an insurance firm, social security fund, private equity fund, and brokerage financial products (i.e., There are more than ten types of institutional investors. Therefore, five types of institutional investors, including securities investment funds, insurance firms, private equity funds, social security funds, and financial products of securities firms, are selected as the research samples.); (4) excluding the samples of listed firms with uncomplete independent variables and dependent variables as the dependent variable lags one period in the experiment of the influencing factors of firms on institutional investor shareholding stability (i.e., To avoid the impact of IPO (initial public listing) on institutional ownership and then affect the accuracy of regression results, the firms listed less than 2 years are excluded).

Finally, a total of 2,012 samples are obtained for 2014 to 2015, 2,126 samples for 2015 to 2016, and 2,178 samples for 2016 to 2017. According to the institutional investor categories contained in each sample, 7,386, 8,396, 8,766 observations are obtained for 2014 to 2015, 2015 to 2016, and 2016 to 2017, respectively. The data, including Tobin’Q value and corporate governance index, are from the CSMAR database.

In addition, data including a shareholding proportion of institutional investors, earnings per share, a growth rate of operating income, asset-liability ratio, total assets, and information disclosure quality are from the Wind database.

The firm age is calculated based on the investigation year—establishment year + 1. The remaining data are based on the manually and analytically evaluation and extracted from policy documents such as Measures on the Operation and Management of Securities Investment Funds, Regulations of National Social Security Fund, Measures for Supervisions of Social Security Funds, Interim Measures on the Management of Share Investment of Insurance Institutional Investors, Interim Measures on the Supervision and Administration of Private Investment Funds, Measures on the Management of Trust Firms’ Collective Funds Trust Schemes and Securities Investment Funds Law. This study winsorizes all the continuous variables at 1% and 99% level and centers the interaction variables.

Model Setting

This study aims to investigate the impact of the influencing factors on institutional investor’s shareholding stability. The influencing factors are divided into the natural endowment and acquired factors and the interaction between them. Business connection and risk preference are natural endowments related to institutional investors’ industry and nature, not profit and investment loss. The acquired factors are mainly affected by external performance ranking, profitability, and governance level, represented by different performance indicators, such as Tobin’s value, return on assets (ROA), earnings before interest, and tax (EBIT).

Also, corporate governance is related to the time and proportion of institutional investors’ shareholding. A firm with a large proportion of shareholding is more likely to engage in corporate governance. On the contrary, institutional investors with small shareholdings are more likely to act as speculators than investors. Institutional investors have different impacts because of different specific investments. The interaction between the two factors needs the influence of natural endowment and acquired characteristics.

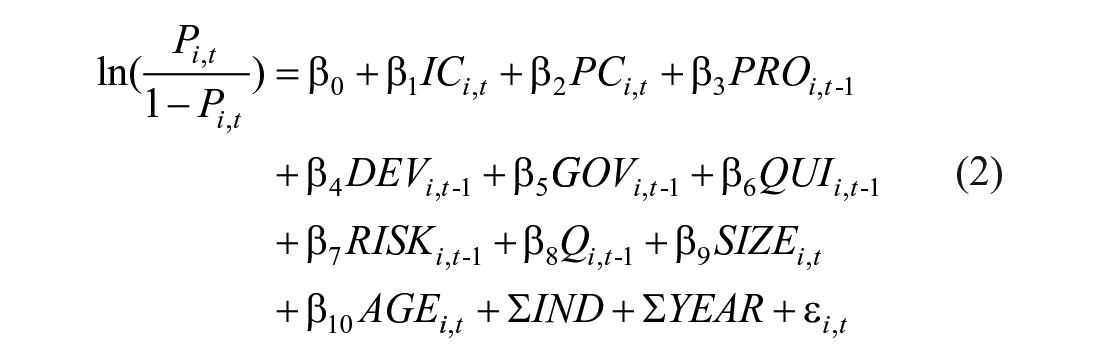

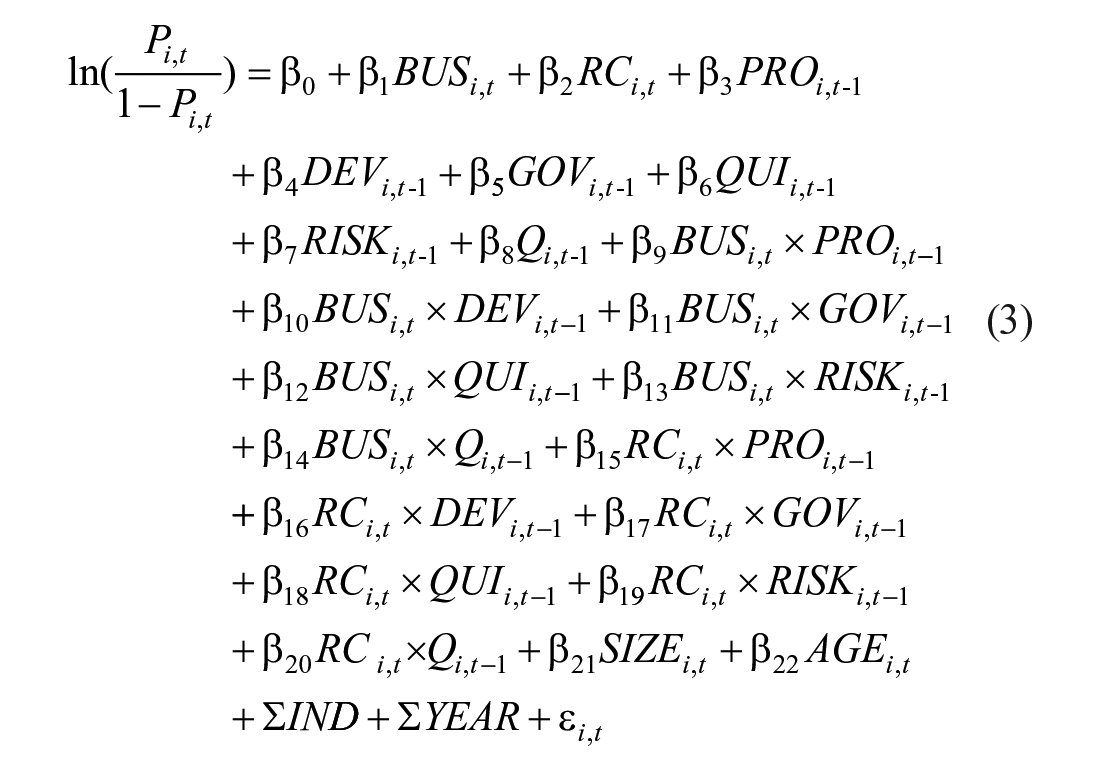

This study, therefore, establishes three different regression models. Models (1) and (2) are set to test the impact of natural endowments and acquired factors on institutional investors’ shareholding stability, respectively. The natural endowment is measured by two indicators: business connection and institutional investor risk. The investment constraint index measures the policy factors in the acquired factors. The market factor is measured by the performance ranking pressure index of institutional investors. Finally, the firm factor is measured by the profitability and information disclosure quality of research samples.

Finally, model (3) is established to verify the interaction between natural endowments and acquired factors on institutional investors’ shareholding stability. The obtained factors in Models (2) and (3) lag one period to eliminate the endogenous effect.

where Pi,t is the probability of a stable institutional investor (INVW = 1) and 1 − Pi,t is an institutional trading investor (INVW = 0).

Definition of Variables

Dependent variable

Considering the scale and scope of shareholding, five prominent institutional investors, namely, securities investment funds, insurance firms, social security funds, private equity funds, and brokerage financial products, are selected as the investigated objects. Referring to Niu et al. (2013), this study defines the institutional investor’s differences in shareholding stability from both industry and time dimensions as institutional investor shareholding stability, as shown in formula (4).

where INVW represents institutional investor shareholding stability. INVH, STD, and SD represent the shareholding ratio of institutional investors, the standard deviation (volatility) of the shareholding ratio of three consecutive years, and the shareholding stability. MEDIAN t,j (SDt,j) represents the median of SD industry j for year t. When SDi,t ≥ MEDIAN t,j (SDt,j), the value is 1, indicating stable institutional investors (INVW = 1) for firm i in year t; Otherwise, trading institutional investors (INVW = 0). MEDIAN t,j (SDt,j) includes the SD of the above five categories of institutional investors at the time of calculation.

Independent variable

Brickley et al. (1988) classify securities investment funds and social security funds as independent institutional investors while securities firms, insurance firms, and trust firms as non-independent institutional investors based on whether these investors have a business connection with shareholding firms. Private equity funds are issued with the help of trust firms. Nevertheless, as an investment adviser, private equity often has the right to investing decisions. Accordingly, this study classifies private equity funds as independent institutional investors. About 1 as institutional investors have a business connection, otherwise 0.

According to the fund source of institutional investors, the ability to take risks and the fund nature, being public offering or private equity, the brokerage financial products, and private equity funds are divided into risk-oriented institutional investors with a value of 1. On the other hand, the securities investment funds, social security funds, and insurance firms are divided into risk-neutral institutional investors with a value of 0.

According to the relative scale of the investment ratio limit, securities investment funds, social security funds, the insurance firm, and brokerage financial products are divided into institutional investors of the high investment restraint with a value of 1. Private equity funds are divided into institutional investors of the low investment restraint with a value of 0. Social security fund investment is in pursuit of stability, whose short-term performance ranking pressure is small, with the value of 1. Securities investment funds, brokerage financial products, private equity funds, insurance firms pursue high investment returns, with a more significant pressure to assess investment performance, with the value of 0.

Earnings per share best reflect the stock profitability, is the most concerning indicator for investors, and significantly impacts investment decisions. On the other hand, the operating income growth rate measures the firm’s operation position and forecasts the business expansion trend, which investors are concerned about. Therefore, this study adopts operational income growth rate as the alternative variable of firm growth ability.

Following Ye et al. (2016), this study employs principal component analysis to construct a comprehensive index of corporate governance to measure the corporate governance level, including the proportion of A-share outstanding shares, the shareholding proportion of board of directors, the shareholding proportion of executives, the status of the chairman and general manager concurrently (1 = concurrent, 0 = non-concurrently), the total remuneration of top three directors (100 million yuan), the total remuneration of top three senior executives (100 million yuan), the number of directors, a ratio of independent director and the degree of equity concentration.

Using the ordinary index of asset-liability ratio as the alternative variable of firm financial risk. Following Liu et al. (2013), this study measures the firm information disclosure quality by the earnings management degree regarding the absolute value of the discretionary accrued earnings, as shown in formula (5). The smaller the value, the smaller the discretionary earnings, the higher the information disclosure quality.

where TA t is the difference between the operating profit of the t period and the cash flow of the operational activities in the same period; At − 1 is the total assets at the end of the t − 1 period; ∆REV t is the difference of primary operation income between the t period and the t − 1 period; ∆AR t is the difference of accounts receivable between the t period and the t − 1 period; PPE t is the original value of the fixed assets at the end of the t period; ROAt − 1 is the return on total assets at the end of the t − 1 period. Based on the formula (5), the regression model is set, and the residuals of the Model calculated by year and industry are the discretionary accruals.

The value of Tobin’Q contains the market value of the share, which intuitively reflects the firm performance in the share market.

Control variables

This study selects a firm scale, firm age, year, and the industry as control variables. The variables and definitions are shown in Table 1.

Variables and Definitions.

Empirical Results and Analysis

Descriptive Statistics

Table 2 shows descriptive statistics.

Descriptive Statistical Results.

Note. All variables as previously defined.

Table 2 shows that the average value and median value of institutional investor shareholding stability (INVW) are 0.499 and 0, respectively, indicating that institutional investors’ overall shareholding behavior is slightly more akin to the trading type. The mean and median of business connections are 0.381 and 0, respectively, indicating that most institutional investors have no business connection with invested firms. The findings seem to suggest that there is still information asymmetry among firms. A firm with information advantage has a strong estimation ability and can use information advantage to decide whether to trade or not.

Nevertheless, the business connections between firms are not easily achieved, including information disclosure and business secrets, and other factors. In addition, the affiliated firm is challenging to achieve information symmetry because of the inconsistency of interest goals.

The average and median values of risk preference are 0.436 and 0, respectively, indicating that the institutional investor is relatively steady overall. The purpose of most institutional investors is related to people’s livelihood. Low entry threshold and repayment of principal and interest are more likely to avoid risks. Only a small part of brokerage financial products and private equity funds are aimed at high net worth customers. The mean and median of investment constraints are 0.798 and 1, separately, indicating many institutional investors subject to investment constraints.

Most institutional investors are concerned with people’s livelihood and cannot pursue high risks and high returns blindly. Therefore, the proportion of investment should be limited. The average value and median value of performance ranking pressure are 0.160 and 0, respectively, representing that the number of institutional investors under the performance ranking pressure is small. As a bounded rational economic man, institutional investors weigh the cost and benefit principle and often determine the current investment according to the historical income to achieve the expected stability.

The top institutions mean good earnings before, which makes it easier to attract investment. There are significant differences among samples based on the maximum, minimum, and standard deviations of Tobin’Q value, profitability, corporate governance, growth ability, and financial risk. However, the information disclosure level has an insignificant difference.

Correlation Analysis

Table 3 shows the correlation analysis among the variables.

Correlation Analysis.

Note. All variables as previously defined.

and ** indicate a significant level of 5% and 1%, respectively.

Table 3 shows that the business connection, risk preference, and performance ranking of institutional investors have a significant negative correlation with the stability of institutional investors. Investment constraints, profitability, growth ability, financial risk, firm value have a significant positive correlation with the stability of institutional investors. A positive Corporate governance and information disclosure quality have an insignificantly positive correlation with institutional investors’ shareholding stability.

In addition, the maximum absolute value of the correlation coefficient between independent variables is only 0.395. VIF = 1/(1 −

Regression Results and Analysis

Table 4 shows the regression results.

Regression Results.

Note. Table shows Z-value, with t-value inside parentheses. *, **, and *** indicate a significant level of 10%, 5%, and 1%, respectively. Model (1) does not include investment constraints and the performance ranking as there is a completely zero or fully collinearity of the interaction terms between investment constraints, the performance ranking, and natural endowments. All variables as previously defined.

Table 4 shows that the business connection and risk preference coefficients are significant at the 1% level, supporting hypotheses 1 and 2. The findings seem to suggest that the institutional investor shareholding stability first comes from natural endowments. Coefficients of policy and market factors are significant at the 1% level, supporting hypotheses 3 and 4. The findings suggest that institutional investor shareholding stability is influenced by the regulatory authority limiting the proportion of funds invested in a single product by institutional investors and the pressure of short-term performance ranking from the market.

The results of Model (2) show that coefficients of profitability, growth ability, firm value are all significant at the 1% level, and the directions of coefficients are consistent with expectations, indicating that these factors have a significantly acquired effect on institutional investor shareholding stability, supporting the hypotheses 5, 6, and 10.

The coefficient of financial risk is significant at the level of 1%, but the coefficient’s direction is contrary to expectations. One possible reason is that institutional investors with accumulated investment experience increase the ability to take risks and enhance firms’ shareholdings with strong growth ability and innovation risk. Another possible reason is that financial risk is expressed in terms of asset-liability ratio usually.

Nevertheless, the higher asset-liability ratio does not necessarily lead to greater financial risk. The key determinants are the firm’s performance level and the guaranteed ability of cash flow after profit. The coefficient of information disclosure quality is insignificant, indicating that institutional investors have a strong ability to obtain and analyze information. The information disclosure quality of listed firms has a weak impact on the institutional investor shareholding stability.

The variable of corporate governance fails to pass the test in Model (2) but passes the test in Model (3), likely because the institutional trading investors choose the firm with a high level of corporate governance. Nevertheless, the average level of corporate governance is only −0.079. Another possible reason is that the regulatory authorities limit the proportion of funds invested in a single product, affecting institutional investment in invested firms’ corporate governance.

Further, the coefficient of interaction terms between firm profitability and the business connection is significantly positive at the 1% level, indicating that the business connection has complementary effects. The coefficient of interaction terms between risk preference and the business connection is significantly negative at the 1% level, indicating that the business connection has substitution effects with risk preference, on the premise that H5a passes the test.

The coefficient of interactions between growth ability and the business connection is significantly negative at the 5% level, indicating that the growth ability has substitution effects

with the business connection. Finally, the coefficient of interactions between growth ability and risk preference is significantly negative at the 1% level, indicating that the growth ability has substitution effects with risk preference, on the premise that H6a passes the test.

Coefficients of interactions between corporate governance and business connection and risk preference are significantly positive at 10% and 1% levels, respectively, indicating that corporate governance affects business connection and risk preference. Thus, contrary to expectations, hypothesis H7a fails to pass the test, indicating that the weak level of corporate governance contributes to strengthening institutional investors’ business connection and risk preference.

The coefficients of interaction terms between firm information disclosure quality and the business connection risk preference fail to pass the significance test, indicating that institutional investors do not pay much attention to the firm information disclosure quality. Instead, the findings suggest that institutional investors have a more vital ability to obtain and analyze information than general investors.

The coefficient of interactions between firm financial risk and the business connection is significantly positive at the level of 5%, indicating that firm financial risk has complementary effects with the business connection. Contrary to expectations, firm financial risk is likely associated with investment constraints, showing the complexity of institutional investor shareholding stability formation.

The coefficient of interactions between firm financial risk and risk preference fails to pass the significance test, indicating that firm financial risk has no complementary effects with risk preference, on the premise that H9a does not pass the test. Likewise, the expected firm value has no complementary effects with business connection and risk preference, assuming that H10a does not pass the test. The possible reason is the effectiveness of the price discovery mechanism in the Chinese capital market results in no reasonable expectations for the use of Tobin’Q value to measure the firm value.

The results illustrate that the negative impact of business connection and risk preference on the stability of institutional investors’ shareholding may be enhanced or reduced with the change of the quality of the investee. For instance, the negative impact of business connections on the stability of institutional investors decreases with the increase of firm profitability. The negative effects of risk preference on the stability of institutional investors’ shareholding increase with firm profitability. The negative impact of business connection and risk preference on institutional investors’ shareholding stability increases with firms’ growth ability.

Robustness Test

Based on Li et al. (2014), with the practice of elongating the time window to examine institutional investors’ stability, this study extends the institutional investor’s calculation year holding stability from 3 to 5 years. After the re-division of shareholding stability of institutional investors, the regression results are shown in Table 5.

Robustness results.

Note. Table shows Z-value, with t-value inside parentheses. *, **, and *** indicate a significant level of 10%, 5%, and 1%, respectively. All variables as previously defined.

The results of the robustness test are consistent with the empirical results, indicating that this study’s conclusions are robust.

Further Discussion

At present, China is vigorously promoting the era of “mass entrepreneurship and innovation.” R&D investment can be used as a variable of firm innovation investment. Stable institutional investors pay more attention to the future earnings of firms. Through R&D investment, firms can expect information related to future development. Therefore, R&D investment is attractive to stable institutional investors.

Trading institutional investors hold shares for a relatively short time, mainly focusing on firms’ short-term earnings. Therefore, R&D investment reduces the expectation of trading institutional investors on the current profit of firms. However, when deciding to hold short-term shares in firms, transactional institutional investors pay attention to the situation of early R&D investment, as R&D investment has a strong lag effect.

The intensity of R&D investment (expressed by R&D investment/primary operation income) is taken as the substitute variable of growth ability. The regression results show that R&D intensity enhances the stability of institutional investors. The findings are consistent with that the era of “mass entrepreneurship and innovation” is a national policy that affects firms’ innovation and development and then affects institutional investors’ shareholding stability.

Conclusion and Policy Implication

Conclusion and Finding

Institutional investors are the prominent participants in the Chinese capital market, and institutional investors’ shareholding stability is closely related to the stable supply of innovative capital. This study’s empirical results show that natural endowments’ characteristics considerably explain institutional investors’ shareholding stability. Furthermore, both business connection and risk preference significantly negatively impact the shareholding stability of institutional investors, indicating that institutional investors with stronger business connections and risk preference decrease shareholding stability.

Additionally, to protect clients’ interests who provide funds to institutional investors, appropriate investment constraints on institutional investors with risk preferences promote shareholding stability. Nevertheless, the current policy imposes more significant investment constraints on institutional investors with non-risk preferences. From the dynamic intensity of pursuing performance ranking, short-term ranking pressure likely forces institutional investors to deviate from value investment and choose speculation, thus preferring to obtain short-term returns from shareholding firms.

Firm profitability, growth ability, financial risk, and market value significantly impact institutional investors’ shareholding stability. Nevertheless, the quality of information disclosure has a widespread impact on institutional investor shareholding stability. The reason is related to the relatively strong ability of institutional investors to obtain and analyze information. Undoubtedly, an increase in the information market’s cost also reflects that the effectiveness of investor demand-oriented information disclosure systems is the core of information disclosure quality.

In addition, the corporate governance level has a widespread impact on institutional investor shareholding stability, likely because excessive investment constraints promote institutional investors’ degree to avoid risk, which restrains institutional investors’ active participation in corporate governance.

Also, institutional investors’ participation in corporate governance is related to the time and proportion of shareholding. Excessive investment constraints promote institutional investors’ risk aversion but inhibit institutional investors’ active involvement in corporate governance. As a result, institutional investors hardly have sufficient impetus to pursue the long-term value behavior of firms. The empirical results of interactions between firm factors and natural endowments of institutional investors show that substitution and interaction occur alternately, proving the complexity of interaction with natural endowments and firm characteristics in the institutional investor shareholding stability formation.

This study has some significant findings. First, prior studies define a specific type of institutional investors as a kind of nature for a long time. However, this study finds that the definition of heterogeneity of institutional investors is unreasonable. This study confirms that institutional investors are not single types and show a skew distribution in a stable or transaction type. Therefore, this study enriches the literature on the heterogeneity of institutional investors.

Second, most literature is based on small and medium-sized firms’ perspectives and puts forward some measures for alleviating insufficient financing. However, this study empirically finds that stable investors play a more significant role in alleviating firms’ financing difficulties than institutional trading investors. Therefore, the national policy is critical to guide institutional investors to make a long-term investment.

Policy Implication

From the supply side to firm financing issues, the institutional investors’ preference demands certain policy constraints and guidance. First, strengthening the supervision of the related business between institutional investors and shareholding firms helps reduce institutional investors’ opportunity to passively echo the managers to obtain private interests in listed firms. Adequate supervision also forces institutional investors to actively participate in the governance of listed firms and reduce institutional investors’ speculative behavior.

Second, severe investment ratio constraints inhibit institutional investors’ participation in listed firms’ governance, weaken the sound effect of investment constraints on institutional investors’ shareholding behavior, and reduce institutional investors’ motivation to pursue long-term value investment actively. Therefore, creating an excellent regulatory environment promotes investors’ rational investment and establishes a reasonable and effective competition mechanism.

Third, the performance ranking of institutional investors is one type of market behavior. Establishing a credit mechanism and a market penalty mechanism for intermediary ranking organizations, lengthening the evaluation period of performance ranking, promoting institutional investors to increase their potential through positive competition, and learning excellent experience outside their institutions contribute to form a long-term value investment concept for institutional investors.

Form the demand to firm financing issues to obtain high-quality institutional investors to inject funds, and firms have to understand institutional investors’ characteristics and the substitution or complementary effects between their factors and natural endowments of institutional investors. Therefore, an urgent task is to improve the corporate governance level and the investor demand-oriented information disclosure quality among the firm’s factors.

Limitation and Future Research

First, this study does not fully consider the complexity of macro factors related to economic, political, and social factors and difficulty in data acquisition. Further research could be carried out.

Second, this study investigates the influencing factors of institutional investors’ shareholding stability to solve the supply side’s financing problem. From the perspective of institutional investors’ decision-making, this study pays special attention to the profitability, growth ability, information disclosure, and corporate governance of the invested firms, but the credit status, investment location, and other factors are not included in the Model. The research could be carried out in the future.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.