Abstract

This study examines the relationship between interest rate and defunct platform risk of China’s peer-to-peer (P2P) lending platforms. P2P lending provides an alternative funding source for individuals and micro-enterprises and offers a new investment tool for households. But the frequent collapses of many platforms were huge losses to market participants and even led to a decline in China’s P2P lending industry. In this study, weekly data of 76 platforms from December 3, 2017, to October 6, 2019, are employed, and empirical research based on the normal and skew-normal panel data model respectively is conducted. Statistical indicators prove that the skew-normal panel data model is preferable to another one in modeling the data set of interest rates. The empirical results show that China’s P2P market is efficient overall. But the positive correlation between the interest rate and risk is not significant for platforms with excessively high interest rates, whose interest rates are more determined by the types of ownership. The findings and implications are provided in the end.

Introduction

P2P lending is a form of direct lending realized by the suppliers and demanders of funds through online platforms. It is a digital financial innovation that combines private lending with internet technology (Chen et al., 2020). Originated in Britain in 2005 (Bachmann et al., 2011), the new form of lending was quickly introduced to China in 2007. As a result of the huge demand from the real economy and the big Macmillan gap (Stamp, 1931; Zhou, 2007), numerous P2P lending platforms sprung up and developed rapidly in China. However, along with the huge scale, China’s P2P industry was fraught with crises. By 2020, many P2P platforms have been withdrawn from the market with the tightening of the regulatory framework and the deepening of the operational transformation. From more than 5,000 at the time to only 29 in operation, China’s P2P lending industry has experienced a difficult process from disordered growth to rectification.

The information held by lenders and borrowers is different, which is called information asymmetry. A typical example is a market for lemons (Akerlof, 1970). In the credit market, the borrowers know their repayment ability and willingness better than the lenders. To make up for the asymmetric information, large credit intermediaries like commercial banks often conduct strict information approval or require high pledge guarantees when issuing loans to micro-enterprises. These raise the cost of transaction matching, making it far more profitable to serve the 20% high-net-worth customers than the remaining 80%. Naturally, individuals and some micro-enterprises are excluded from the traditional financial system, which leads to the booming of P2P lending in China.

The P2P lending platforms are skilled in big data analysis and credit risk management, which can alleviate Pareto’s principle in the traditional financial system. As an information intermediary connecting borrowers and lenders, the P2P platform reduces the cost of maturity matching, thereby reducing adverse selection and moral hazard problems caused by asymmetric information. The form of P2P is reasonable theoretically (Xie & Zou, 2012), but due to the relatively lagging supervision of financial innovation, many fraud platforms dressed in P2P have disrupted China’s P2P industry. Today, with the improvement of financial infrastructure and the regularity of supervision, compliant platforms have become one of the driving forces for China’s digital financial innovation of their professional technologies of big data and risk management (Zhou et al., 2020).

This paper focuses on the relationship between interest rate and platform risk in digital finance. Interest rate is an ideal starting point to investigate the characteristic of digital finance (He & Peng, 2016), whose marketization is an inevitable trend for the steady development of the entire financial system. Capital Asset Pricing Model (CAPM) points out that interest rate is positively correlated with risk, which occupies a dominant position in modern financial theory. However, the assumption of CAPM is too strict and the actual financial market is usually inefficient. Specifically, behavioral finance and signal effect may distort the positive correlation between interest rate and risk in digital financial market. Therefore, it is meaningful to study the relationship between P2P lending interest rate and risk. Three research questions are proposed below.

A quantitative analysis from an industry perspective has been extensively adapted in P2P fields. It should be noted that financial data including short-term interest rates generally show asymmetric and skew-normal characteristics (Hong & Lin, 2006). But various studies (Duarte et al., 2012; Liao et al., 2014b; Schmid, 2005; Xiang et al., 2019; Zhou et al., 2020) directly establish their models under the assumption of normal distribution. This unreasonable assumption makes the results of the study lack statistical robustness and thus is easy to draw misleading conclusions (Zhang & Davidian, 2001). Therefore, we have to find an appropriate statistical model and an effective optimization algorithm.

This paper uses the normal and skew-normal panel data model to study the relationship between the P2P interest rate and risk, respectively. We will focus on the following three research questions.

Literature Review

Existing researches on the P2P interest rate mainly focus on the credit risk management, the relationship between interest rate and risk, and the determinants of the P2P interest rate.

Credit Risk Management of P2P Platforms

The problem of asymmetric information is inherent in the credit market, while P2P lending based on social networks can alleviate the information problem (Freedman & Jin, 2008). The premise is a professional and effective credit risk management system based on the Internet. Duarte et al. (2012), Liao et al. (2014a, 2015a, 2015b) and Wang et al. (2020) analyzed the problem of credit risk assessment in the P2P market from the perspectives of borrowers’ characteristics, including appearance, region, education background, and consumer behavior, respectively. The descriptive information of borrowers also affects the success rate and default rate significantly (Gao & Lin, 2013; Herzenstein et al., 2011; Li et al., 2014; Lin et al., 2013). Wang and Liao (2014) found that borrowers with high credit ratings have higher success rates and lower borrowing costs. Besides, compared with the simple online credit authentication method, the combination of online and offline credit authentication methods can improve the success rate of borrowing and reduce the borrowing cost.

From the perspective of the herd effect, Duarte et al. (2014) indicated that investors make systematic errors in forming expectations and the errors will impact prices. However, Liao et al. (2014b) argued that P2P investors are intelligent and can identify the different default risks behind the same rates based on public information. Also, Liao et al. (2015) discovered that with the increase in herd behavior, the default rate of loans decreases. Riggins and Weber (2017) revealed the information asymmetry and identification bias in P2P microloans. Furthermore, Liao et al. (2018a) proved that the crowd has wisdom and the wisdom of the crowd offers new information to P2P investment. From the perspective of the investor learning effect, Liao et al. (2018b) indicated that if investors have the experience of borrowing money as borrowers, their investment performance will be significantly improved. Methodologically, Huang and Qiu (2021) compared the traditional risk control model with the big data risk control model and found that the big data risk control model had prominent information advantages and model advantages, which could predict credit risks more accurately.

Relationship Between Interest Rate and Defunct Platform Risk

Interest rate is an important factor in studying the online lending form of P2P and identifying the defunct risk of different platforms. Chen and Ye (2016) used the AR-GARCH model to analyze the fluctuation characteristics of P2P interest rates from a macro perspective, and the results showed that the fluctuations demonstrate significant effects of aggregation and reversal with a characteristic of a wide tail. He and Peng (2016) found that the volatility of P2P interest rates in China shows a clustering and risk-accumulating effect, and the risk awareness of the market participant is not strong despite the high risk in the P2P lending market.

With the tightening of the regulatory framework for the P2P lending market and the frequent occurrences of defunct platforms, the research emphasis of academia has shifted to the identification of the defunct platform risk. Ye et al. (2016) and Wang et al. (2016) discovered that a high level of interest rate is the most important feature of a defunct platform. Fan et al. (2017) found that the fluctuation of the average interest rate plays an important role in risk monitoring. Xiang et al. (2019) performed probit regression to examine the cross-sectional relationship between the interest rate and defunct platform risk. He et al. (2017) used Logistic model to analyze the determinants of platform risk and found that the problem platforms were basically private companies with high interest rates. Their results indicated that the interest rate is positively related to defunct risk in general and there are heterogeneous effects across different interest rate levels.

Determinants of the P2P Interest Rate

Based on Bayesian game theory with incomplete information, Chen and Ma (2016) analyzed the forming of interest rates in different operation models. Their finding indicated a certain negative relationship between the interest rate and the ratio of investor number to borrower number. Zhou and Fan (2016) used data from a P2P lending platform (renrendai.com) to compare the variation of interest rates 1 month before and after August 25, 2015, when The People’s Bank Of China announced a new monetary policy. Their analysis showed that the interest rate pricing mechanism is highly market-oriented and the P2P lending market is a buyer’s market. Xie and Xu (2017) analyzed the influence of the interest rate and user scale on P2P lending transaction from the angle of the platform's ownership with macroscopical industrial data, and the result indicated that the ownership has a moderating effect on the relationship between the interest rate and lending transaction with the user scale as a complete intermediary. Zheng et al. (2017) found that the interest rate of the private platform is significantly higher than that of the platform with other ownerships. For P2P supply chain finance, Zhang et al. (2019) pointed out that the loan term was positively related to the interest rate, while the registered capital of the borrowing enterprise was negatively related to it. Zhou et al. (2020) constructed a game model under incomplete information, and the research showed that the number of participants, the average term of the loan, transaction volume, risk level, and loan balance of both parties are all important factors influencing the comprehensive interest rate of P2P lending. Guo et al. (2021) discussed the influence of non-specific and external factors on the interest rate of P2P microloans and found that the interest rate of private lending is the most significant factor, with a positive coefficient.

The above literature provides useful references on the P2P interest rate, but there is still room for improvement. For example, researchers on the interest rate data with skew-normal characteristic are still under the assumption of a normal distribution, whose results often lack statistical robustness and easily draw misleading conclusions (Zhang & Davidian, 2001). Also, the existing researches are mostly based on the cross-sectional data of micro-individuals or the time series data of a macro-industry, and there is little study considering both the heterogeneity of individuals and the dynamics of time series. The panel data model is widely used in empirical research in economics. However, the existed studies on the panel data model are only conducted under the assumption of normal distribution (Karlsson & Skoglund, 2004). Hence, this paper will fill this gap by studying the relationship between interest rate and risk based on the skew-normal panel data model.

Methods

The actual data increasingly presents commonly and frequently asymmetric skew-normal distribution characteristics. Therefore, the empirical study for the panel data model based on skew-normal assumption is of great scientific and practical importance.

Data Collection

Based on the random sampling method, we select 76 P2P lending platforms in China as the research sample. Compared with the rapid growth in the number of platforms, China’s legal supervision of the P2P lending industry was relatively lagging. It was not until the end of 2017 that the “1+3” regulatory system of the P2P lending industry began to take shape. Thus, we set the research period from December 3, 2017, to October 6, 2019, with a total of 7,372 weekly records involved. The data come from CSMAR.

Variables

The dependent variable of the research is the weekly average interest rate of the P2P lending platform. Because the interest rate is determined by the dynamic game between investors and the platform, we set two independent variables of interest: platform risk and platform ownership nature. Firstly, investors will pay attention to whether the platform can operate normally during their investment period. Secondly, the nature of platform ownership is also important (Fan et al., 2017; Ye et al., 2016; Zheng et al., 2017). When investors have a sense of trust in platform ownership, they are more likely to accept lower returns. Besides, indispensable control variables are added to the model (Chen & Ye, 2016; Fan et al., 2017; Lin & Zhang, 2016; Wang et al., 2016; Xiang et al., 2019). The variables of the model are described in Table 1.

Description of the Variables.

It should be noted that the investors participating in the P2P lending market must consider the defunct platform risk (Risk) during their period of investment. Because the average period of investment (AveLimTime) in the P2P lending industry is about 40 weeks, we set the time window for observing whether a risk event occurs on a platform as 40 weeks. Specifically, the risk events in this study refer to the difficulties in withdrawal, investigation intervention, running away, delayed payment or website closure, and so on.

Before strict measures are taken to control the P2P lending market, the risks of P2P platforms were related to the factors of the platforms themselves. The dummy variable risk represents a long-term risk. There is a lag relationship between the risk variable and other variables, which can avoid the influence of platform exiting.

To exclude the impact of extreme values on the empirical results, this paper truncates the loan term (AveLimTime), the accumulated loan balance (CumulateRepay), the number of trades (TradingNum), the number of investors, and the number of borrowers at the bilateral 1% level. For the possible non-linear relationships, the quadratic terms (AveLimTimeSq and ShiborSq) of AveLimTime and Shibor are added to the model. The natural logarithms of the number of trades and the ratio of investors and borrowers are used in the research.

Skew-Normal Distribution

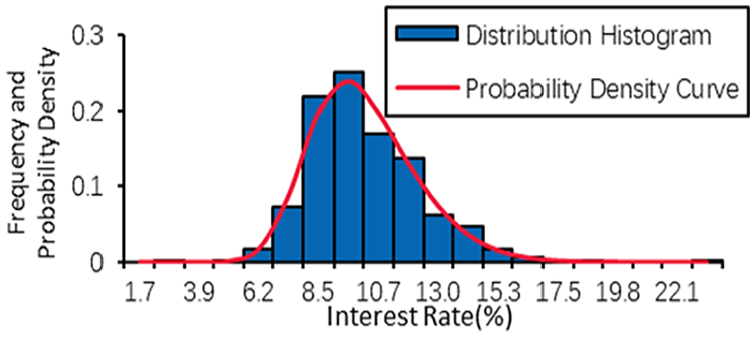

The data of the short-term interest rates often show asymmetric and skewed characteristics. To verify the distribution characteristics of the P2P interest rate, we visualize the data set of weekly average interest rates of 76 representative P2P platforms in China from December 3, 2017, to October 6, 2019, and draw the distribution histogram and probability density curve of it, see Figure 1.

Distribution histogram and probability density curve of the data set of P2P interest rates.

As shown in Figure 1, the data set of P2P interest rates doesn’t follow the normal distribution but shows asymmetric and right-skewed characteristic. To confirm, four test statistics including Shapiro-Wilk, Kolmogorov-Smirnov, Anderson-Darling, and Cramer-Von Mises are used to examine the normality of the data set of P2P interest rates. The p-values corresponding to the four test statistics are 4.016e-13, 4.841e-14, 2.2e-16, and 7.37e-10, respectively. Thus, at the nominal significance level of 5%, the data set of P2P interest rates doesn’t follow the normal distribution, which answers RQ1 that the data set of the P2P platform’s interest rates follow the skew-normal distribution.

From Azzalini and Valle (1996) and Azzalini and Capitanio (1999), we have the following definition.

where

Then, we prove whether the distribution of the P2P interest rates is skew-normal by the Chi-square goodness-of-fit test. By calculation, the fitted value is

where

Skew-Normal Panel Data Model

The research on the skew-normal model has attracted scholars’ attention. Meng and Xiao (2015) found the skewed characteristic of the actual insurance loss data and then used the skew-normal model to estimate the reliability premium. Their model was proved to have a preferable prediction effect compared with the traditional model. The empirical experience and statistical test all indicated that the data set of P2P interest rates follows the skew-normal distribution. In this case, the estimated coefficients obtained under the normal distribution assumption may be biased, so this research considers an econometric model with a skew-normal random error term.

Considering the heterogeneity of individuals and the dynamics of time series, it is reasonable and preferable to use the panel data model.

As a kind of mixed effect model containing time series and cross-sectional data, the panel data model has been widely used in the field of econometrics (Ye & Jiang, 2018). Besides skew-normal model, there are different econometric tools to model the panel data, such as panel GEE or panel GMM. Zhou (2015) gave the comparison between the skew-normal model and GEE method. The results show that the conclusions of the two methods are similar, which demonstrate the robustness of the skew-normal model. However, due to limited space of this paper, we will systematically study the comparisons and applications of the skew-normal model, GEE, GMM, and other methods in the next paper. Thus, we consider the panel data model with a skew-normal error term. It extends the assumption about the error term from a normal distribution to a skew-normal distribution.

For platform

where

Let

Assume

Parameter Estimation

In the skew-normal panel data model, the maximum likelihood (ML) estimation approach is useless because the number of unknown parameters is more than that in the normal panel data model. Thus, the expectation-maximization (EM) algorithm (Moon, 1996) is used to estimate the parameters of the model in equation (4). EM algorithm is an iterative algorithm for ML estimation of missing data models.

Let

To obtain the likelihood function of unknown parameters, model (4) can be rewritten as

where

For

where

where

Let

By (7) and (8), we have

Let

where

By the above joint density function (10), the conditional density function, first order and second order origin moments of

The log-likelihood function of complete-data

where

For model (7), the following steps can be used to estimate the parameters

where

By software R, the M-step can be easily implemented. Given the starting values, we can obtain the estimates of the parameter by repeating E-step and M-step until the convergence of parameters. The starting values are often chosen to be the corresponding estimates under the assumption of a normal distribution.

Results

Regression Analysis

The normal and skew-normal panel data models are constructed respectively. The specific form of the skew-normal panel data model is shown in equation (4), and the estimation results are shown in Table 2. From Table 2, when the error term follows the assumption of skew-normal distribution, the Akaike information criterion (AIC) value and Bayesian information criterion (BIC) value of the model are significantly lower than those under the assumption of normal distribution. It indicates that the skew-normal panel data model fits the data of P2P interest rates better. From Table 2, the relationship between platform interest rate and defunct platform risk is underestimated by the normal panel data model.

Parameter Estimation of the Normal and Skew-Normal Panel Data Model.

Note. Numbers in parentheses denote standard errors. NPDM = normal panel data model; SNPDM = skew-normal panel data model.

p < .01. ***p < .01.

The regression result shows that the interest rates of the risky platforms are higher than those of other platforms, indicating that P2P investors can identify the failure risk of the platform and demand higher risk-return. It answers RQ2 that there is a positive correlation between the interest rate and risk in China’s P2P lending market. Also, ownership is significant in both two models, showing its importance for investors when choosing platforms. This finding is consistent with Ye et al. (2016) and Fan et al. (2017). China’s P2P lending market is still an emerging market, and investors are more inclined to platforms with capital endorsements or state-owned platforms. In this way, private platforms can only raise interest rates to attract investors, which results in the average interest rate of private platforms being significantly higher than that of non-private platforms by 1.105%. It is worth mentioning that from the estimation results of the control variables, the interest rate of the P2P platform has an inverted U-shaped relationship with the loan period and Shibor.

Heterogeneity Analysis

The previous analysis shows that the variables of platform risk and ownership both have a positive effect on the interest rate of the P2P platform. But there may be heterogeneity across different interest rate levels. For example, Zhang (2016) indicated that the interest rates of fraudulent P2P platforms are more concentrated at a higher level.

In this section, the whole sample is divided into three subsamples according to the rankings of platforms’ interest rates. The subsamples consist of platforms with “low” interest rates (interest rates lower than 35% quantile), “medium” interest rates (interest rates between 35 and 65% quantiles), and “high” interest rates (interest rates higher than 65% quantile), respectively. For each subsample, the normal and skew-normal panel data models are constructed respectively. The estimation results are shown in Table 3. It can be seen from Table 3 that among the three groups with different interest rate levels, the AIC and BIC values of the skew-normal panel data models are significantly lower than those of the normal models, indicating that the skew-normal panel data model fits the data of P2P interest rates better.

Parameter Estimation of the Normal and Skew-Normal Panel Data Model of Three Interest Rate Levels.

Note. Numbers in parentheses denote standard errors. “Low: <35%,”“Medium: 35–65%,”“High: >65%” represent subsamples with “low,”“medium,” and “high” interest rates, respectively. NPDM = normal panel data model; SNPDM = skew-normal panel data model.

p < .01. **p < .05. ***p < .01.

From Table 3, we find that the positive relationship between interest rate and defunct platform risk is significant in model (2), with an average of 1.168% higher. It answers RQ3 that there is heterogeneity between platforms with different interest rate levels. Acting as normal credit intermediaries in the lending relationship, low interest rate platforms generally do not participate in high-risk behaviors such as guarantees. Compared with other platforms, low interest rate platforms usually do not attract investors by raising the rate of return, which means the signal effect is not dominant in those platforms. Therefore, there is a closer relationship between interest rate and risk in low interest rate platforms.

From models (3) and (4), we observe that the two variables of risk and ownership are not significant. It shows that after controlling the variables such as the loan period, base interest rate and transaction factors, there is no significant linear relationship between the interest rate of risk and ownership.

From model (6), the relationship between interest rate and ownership is significant, and the estimated result of 1.493% is much higher than the result of the full-sample regression (1.105%). It shows that the investors are cautious about the emerging lending forms, especially towards the platforms that provide ultra-high returns. Under the same other conditions, the average transaction interest rate of private platforms is higher, which is caused by investors' mistrust. In model (6), the relationship between risk and interest rate is not significant. It may be a function of the signal effect. In China, the P2P lending industry is an emerging market with fierce competition. To occupy the new market, P2P intermediaries may increase returns to investors to attract capital. In other words, high-quality platforms have the incentive and capability to send signals to investors by increasing the rate of return.

Discussion

Since 2014, the government work report has mentioned “Internet finance” almost every year, but the tone has gradually shifted from assessing the value of its innovations to warning of risks. China, which once formed the world’s largest individual online lending industry, collapsed after regulators announced interim regulations in August 2016, even spreading anxiety and unease across the digital finance industry.

Throughout the development of P2P in China, we believe that regulatory factors have the greatest impact on the failure of P2P platforms. If P2P platforms only act as information intermediaries, building bridges between lenders and borrowers in order to collect information fees for profit, then the industry is unlikely to have a systematic panic. However, the initial lax regulatory approach encouraged P2P platforms to lure investors with promises of unrealistically high returns. To guard against major financial risks, the government finally adopted strict management measures to establish discipline in the P2P lending market.

This paper focuses on the relationship between interest rate and platform risk in digital finance. Sharpe (1964) pointed out that when the market reached equilibrium, there would be a linear relationship between risk and return theoretically. But one of the assumptions is that the participants in the market have perfectly symmetrical information. However, the problem of asymmetric information always exists. The trading behavior of both parties will be affected due to their different degrees of information mastery (Bagehot, 1971).

Our contributions are (1) verifying the skew-normal characteristics of interest rate data in China’s P2P market and first adapting the parameter estimation method of the skew-normal panel data model in the financial field. (2) Proving the significant positive correlation between interest rate and risk in China’s P2P market, and practicing the rationality of CAPM theory in China’s p2p market. (3) Providing theoretical support for the practice of digital financial risk governance by discovering heterogeneity between high interest rate platforms and other platforms.

Theoretical Implications

(1) The distribution of interest rates is skew-normal and the skew-normal panel data model is preferred and has proved to be more robust in empirical studies on interest rates. (2) There is a significant positive correlation between the interest rate and platform risk in China’s P2P market on the whole, which is consistent with the research conclusions of Puro et al. (2010) and He et al. (2017), providing empirical data support for the rationality of market efficiency hypothesis. (3) The risk performances of P2P platforms vary with their average interest rates. And the relationship between platform interest rate and platform risk is only significant in the low interest rate platforms.

Practical Implications

(1) The interest rate control system of Internet financial products should be improved. Specifically, conduct risk modeling with an interest rate as the main feature, and prevent excessive risky operation of digital financial enterprises. (2) Strengthen information disclosure. Encourage or force platforms to disclose more information, screen and eliminate fraudulent platforms, and protect the legitimate rights and interests of market entities. (3) Enhance regulatory technology and risk forecasting capabilities to detect highly hidden digital financial risks promptly. A supervision sandbox system of financial innovation is essential to encourage financial innovation while keeping it on the legal track.

In addition, the P2P lending market is essentially a credit market. Full information disclosure is the key factor to ensure the efficiency of the credit market. As a place of capital financing, an efficient credit market can accurately guide the scarce economic resources to efficient enterprises and realize the optimal allocation of the entire social resources. For the P2P lending market, sufficient, timely, and accurate information disclosure is the basis for investors to make investment decisions. However, compared with the listed platforms, information disclosure on private platforms is inadequate and inferior. As a result, the interest rates of private platforms are higher than other platforms in the market, which is consistent with Wang et al. (2016), He et al. (2017), and Ba et al. (2018). The higher interest rate is not only a temptation for investors but also an indispensable compensation for the “smart money” in the P2P lending market.

Conclusion

We investigate the relationship between interest rate and defunct platform risk of China’s P2P lending platforms. We found that the data set of interest rates follows the skew-normal distribution. The skew-normal panel data model is statistically superior in modeling the data. The relationship between interest rate and risk is positive overall. For platform with excessively high interest rate, the interest rate is more related to platform ownership.

The limitations of this paper are the incomprehensive data collection and insufficient sample size. With a larger sample size in future research, we will establish SNPDM, GEE and GMM models, and find the optimal one.

Footnotes

Declaration of Conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the National Social Science Foundation of China (Grant No. 21BTJ068).

Ethical Approval

The ethics statement (including the committee approval number) for animal and human studies is not applicable.