Abstract

This study investigates the effect of macroeconomic and bank-specific factors on the bank interest rate spread (IRS) of six Western Balkan countries (referred to as WB6). We applied the Panel Vector Autoregression (Panel VAR) model to separately analyze the impact of these two sets of factors for 2005 to 2022 using two-panel datasets from 110 banks. The results from the two models show that the IRS is significantly influenced by GDP per capita and the unemployment rate, while other factors, such as bank concentration, performance indicators, and non-performing loans, show limited direct effects. The study identifies a notable gap in the existing literature by emphasizing how macroeconomic and bank-specific variables, particularly in transition economies, can simultaneously affect the IRS. The research highlights the distinctive financial dynamics within the WB6 countries and the relevance of comprehending the region’s banking sector characteristics. It contributes to academic and policy discussions on the significance of financial stability and market competitiveness in determining the bank IRS. The findings can be helpful for banking regulators and policymakers in the Western Balkans seeking to foster an efficient and competitive banking environment.

Introduction

Banking institutions are the cornerstone of modern economies, with interest rates playing a pivotal role in mediating the funds between savers and borrowers. One key metric in this context is the bank interest rate spread (IRS), the difference between the rate banks lend and pay depositors. The IRS impacts a bank’s profitability and influences macroeconomic stability (Bredemeier et al., 2018; Cassola & Morana, 2008). Therefore, understanding its determinants is essential not only for banking institutions but also for banking regulators and policymakers. Generally, the IRS is a reflective metric of the banking industry’s financial health and overall efficiency. Several methodologies quantify the IRS as the differential between a bank’s interest revenue and expenditure or the variance between average lending and deposit rates (Agapova & McNulty, 2016; Entrop et al., 2017; Kumar, 2014; Paul, 2014). Despite these alternatives, no unanimous agreement prevails in the literature regarding the most effective method (Ahmed & Khan, 2022; da Silva & Pirtouscheg, 2015; Divino & Haraguchi, 2023; Hagenbjörk & Blomvall, 2019). Contributing to the ongoing discussions regarding the effectiveness of the banking systems, the study examines the factors that influence the IRS in WB6 countries (Albania, Kosovo, North Macedonia, Montenegro, Bosnia and Herzegovina, and Serbia).

The necessity of understanding the characteristics and challenges of the banking sector in the Western Balkans is another driving force behind our study. This sector has changed significantly due to regulatory shifts, market liberalization, and the integration process into the European Union (EU). A further rationale of our research is the fact that there are constant concerns that interest rates might not accurately represent the risks of the WB6 economies. Furthermore, there have been allegations of collusive agreements among banks. If the interest rates are subject to competition, they must integrate all the economic events and beyond. Since the IRS issue is much more complex, the study partially explains the efficiency/inefficiency of the banking sector in WB6 countries. Therefore, the study seeks to shed light on this direction and address possible concerns.

Banks as financial intermediaries are known to be the primary mechanism through which monetary policy communicates with the real economy. Several studies (Ghosh, 2017; Marinkovic & Radovic, 2010; Nuhiu et al., 2017; Ponomarenko, 2022) highlight that the IRS remains a crucial metric for banks’ intermediation costs and efficiency. Standard financial practices indicate that investors and consumers are less likely to borrow money when loan interest rates are high. On the other hand, if the IRS is too low, risks are being underpriced (Acharya et al., 2020; Arestis & Sawyer, 2010; Rathnayake et al., 2022). Therefore, understanding the factors influencing the IRS is important for maintaining a robust and efficient financial system. In many emerging economies, including those in the WB6 countries, the IRS has often been found to be high relative to the EU standards. According to the World Bank’s open data for 2020, the average IRS within the EU member states ranges from 3.35% to 3.71% (World Bank, 2020). Meanwhile, according to the study dataset for the Western Balkans countries, the average IRS in 2020 ranges from 1.15 to 7.53 interest rate points. While the data suggests a trend of wider IRS in WB6 countries, our analysis seeks to determine the reasons behind these spreads conclusively. Factors such as varying risk assessments, regulatory environments, and market structures may contribute to these differences. Several other factors have been identified as contributing to high IRS in developing countries, including inflation rate and country-risk premium (Ahmed & Khan, 2022; Aliu et al., 2016; Mujeri & Younus, 2009; O’Connell, 2023). These factors are also relevant to the WB6 countries, where inflation, country risk, and market structure vary significantly across the region (European Commission, 2023a; Guo, 2023).

The WB6 countries have undergone substantial banking transformations over the last decades. Their distinctive banking environment has been constantly shaped by post-socialist transformation reforms, global economic events, and a changing regional landscape (European Commission, 2023b; IMF, 2017). As such, these countries provide sufficient indications for exploring the IRS determinants. WB6 countries have experienced a history of ethnic conflicts and wars in the not-so-distant past. These conflicts have created constant tension and instability in the region, which can be an extra risk for international banks. Although they operate in the same geographical area, each country holds diverse monetary policies, banking systems, and regulatory frameworks. Banks operating in the WB6 countries are predominantly backed by Western capital. As a result, foreign investors, especially from Western countries, perceive political risk and ethnic conflicts with greater caution than local investors. This perception could influence the interest rates set by these banks. Moreover, variations in banking regulation, financial development, and standard of living generate implications for the IRS in the WB6 countries (OECD, 2021).

The banking sector in WB6 countries exhibits a combination of domestic and international banks, each adhering to distinct business models (Kouretas & Tsoumas, 2016; Lehner & Schnitzer, 2008; Sanfey & Milatović, 2018; Stakić et al., 2021). Given its distinctive combination of financial institutions and macroeconomic conditions, the Western Balkan region is intriguing to examine the factors influencing the IRS. The majority of research has focused on examining the effects of macroeconomic variables while neglecting the potential impact of institutional and bank-specific factors (Azumah et al., 2023; Beckmann et al., 2022; Claeys & Vander Vennet, 2008; Divino & Haraguchi, 2023; Obeng & Sakyi, 2017; Shareef & Shijin, 2017; Souza-Sobrinho, 2010). The study seeks to fill these gaps by providing a comprehensive assessment of the determinants of the IRS in WB6 countries. Moreover, the WB6 countries’ distinctive banking sector attributes and ongoing transformations in their financial systems necessitate a region-specific analysis. Several studies have indicated that financial systems in developing countries generally exhibit higher IRS than those in developed ones (Agapova & McNulty, 2016; Nguyen, 2019; Uribe & Yue, 2006). Less developed markets tend to have limited access to global capital, leading to higher borrowing costs and, subsequently, higher IRS. Market imperfections, information asymmetry, and less efficient regulatory frameworks contribute to wider IRS as financial institutions seek to mitigate potential losses.

While numerous studies have explored the determinants of bank IRS, there is a notable lack of comprehensive research focusing on the combined effects of macroeconomic and bank-specific factors in the WB6 countries. Furthermore, existing literature often overlooks these countries’ unique historical, political, and economic contexts that may significantly influence their banking sectors. Additionally, there is limited empirical evidence on the role of regulatory environments and market structures in shaping the IRS within this specific region. The study aims to bridge these gaps by providing a comprehensive analysis of both macroeconomic and bank-specific determinants of bank IRS in the Western Balkans. The research seeks to offer new insights into the complexities of IRS in emerging markets, particularly in post-socialist economies transitioning to more market-oriented systems. It provides insights to policymakers in WB6 countries on improving banking efficiency. The findings offer guidance for monetary policies, crafting robust regulatory frameworks, and enhancing the region’s banking competitiveness. Our research is timely and relevant given the ongoing banking restructuring in the Western Balkans. Moreover, our results help financial institutions and banking regulators make informed decisions and foster a resilient banking system. Therefore, the study aims to address the following research questions:

RQ1: What is the influence of macroeconomic factors on interest rate spreads in the WB6 countries?

RQ2: How do the bank-specific factors influence interest rate spreads in the WB6 countries?

The remaining sections of this study are structured as follows. Section 2 reviews the existing literature on IRS and its determinants, Section 3 describes the methodology employed. Section 4 reports the results and their interpretation, while Section 5 discusses the study’s findings, policy implications, limitations, and future research.

Literature Review

Analyzing the factors that influence the bank IRS is fundamental for a comprehensive understanding of financial intermediation and its effects on financial stability; thus, it has been the subject of considerable empirical investigation. A high IRS may indicate potential inefficiencies within the banking sector (Agapova & McNulty, 2016; Almeida & Divino, 2015; Aydemir & Guloglu, 2017). The foundational work by Ho and Saunders (1981) introduced the concept of banks as risk-averse entities, facing transaction uncertainties that necessitate an interest spread or margin. Their model has been extended to incorporate variables such as credit risk and regulatory factors, highlighting the complexities of IRS determinants (Allen, 1988; Demirguc-Kunt & Huizinga, 1999; McShane & Sharpe, 1985). Banks use high IRS to cover the risk arising from the stochastic nature of depositors and borrowers, even though a favorable IRS is unnecessary. This is because high IRS can provide banks with a way to manage their risks and protect themselves against potential losses (Hawtrey & Liang, 2008; Rathnayake et al., 2022; Were & Wambua, 2014). However, Aydemir and Guloglu (2017) consider that credit and liquidity risks highly influence the IRS during business cycles in an emerging market. Their findings indicate that credit risk is more important than liquidity risk in explaining bank IRS. Furthermore, Hawtrey and Liang (2008) demonstrated that greater financial inclusion decreases inefficiency and leads to lower IRS. Their study found that when bank managers are risk-averse, they impose higher interest margins.

Most studies on the determinants of IRS have focused on developed countries (Ahmed & Khan, 2022; Aydemir & Guloglu, 2017; Carbó-Valverde & Rodríguez-Fernández, 2007; Cassola & Morana, 2008; Hainz et al., 2014; López-Espinosa et al., 2011; Požlep, 2023; Williams, 2007), Latin American countries (Almeida & Divino, 2015; Brock & Rojas-Suarez, 2000; Chortareas et al., 2012; da Silva & Pirtouscheg, 2015; Gelos, 2009; Souza-Sobrinho, 2010), and more recently Asia (Doliente, 2005; Jung & Kim, 2023; Lin et al., 2012; Rathnayake et al., 2022). African research has been limited to individual countries (Beck & Hesse, 2009; Obeng & Sakyi, 2017; Tarus & Manyala, 2018; Were & Wambua, 2014). Tarus and Manyala (2018) investigated the impact of macroeconomic, bank-specific, and institutional factors on IRS in Sub-Saharan African countries. Their findings show that higher inflation rates are associated with increased IRS.

In transition economies, high IRS is commonly associated with weak and inefficient financial systems, which potentially constrain economic growth and induce instability (De Nicoló et al., 2003; Gorton & Winton, 1998; Harper & McNulty, 2008). These markets face unique challenges, such as managing the legacy of bad loans and adapting to new regulatory standards, which can influence their interest rate policies and, subsequently, their IRS. However, detailed analyses focused on the Western Balkans remain deficient, indicating a research gap this study aims to address. Studies by (Agapova & McNulty, 2016; Agoraki & Kouretas, 2019; Kasman et al., 2010) analyzed net interest margins as efficiency measures in different countries during the transition period. Their findings suggest larger banks may be able to achieve efficiency gains, but the relative merits of margins versus spreads as efficiency measures are still debated. Kasman et al. (2010) examined how financial reforms impact commercial bank net interest margins in new EU member states and candidate countries. Their findings show a significant negative relationship between bank size, managerial efficiency, and net interest margins. Similarly, Agoraki and Kouretas (2019) investigated the banking sector of Central and Eastern European (CEE) countries from 1998 to 2016. They found that bank-specific aspects like size, capitalization, and liquidity significantly influence net interest margins. Moreover, Demirguc-Kunt and Huizinga (1999) broadened the research by integrating variables such as ownership, tax, financial leverage, and legal and institutional elements. Their study identified a negative correlation between these profitability metrics and the development of banking sectors within developing countries. Whereas, Agapova and McNulty (2016) utilized bank IRS as indicators of financial intermediation efficiency and analyzed the correlation between these spreads and bank efficiency within the transition economies of Central and Eastern Europe. They argued that efficiency issues led to lower net interest margins in emerging economies.

Empirical research typically categorizes the determinants of the IRS into three groups: bank-specific, macroeconomic, and institutional factors (Poghosyan, 2013). These factors include operating costs, bank size, credit risk, the degree of competition, inflation, and economic growth. Cross-country empirical studies leverage balance sheet metrics, such as bank assets, liquidity inputs, total domestic credit, and private sector claims to GDP, as measures of intermediation (Harper & McNulty, 2008; Levine, 2003; McNulty et al., 2007). These studies highlight the significance of the IRS, suggesting that a large gap between loan and deposit rates signals a weak and inefficient financial system. This could impair economic growth and be a potential source of financial instability. Gorton and Winton (1998) theorize that in transition economies, the size of a financial system correlates with its stability. They suggest that the burden of bad loans from previous centrally planned economies pressures banks to keep lending to underperforming state-owned entities, thereby fostering inefficiency. Moreover, the research postulates that introducing capital requirements and market discipline could lead to a contraction in the banking sector and augment financial instability. Research by the IMF, carried out by De Nicoló et al. (2003), applies univariate analysis to investigate spreads in transition economies, discovering a sharp contraction in IRS. They argue that high IRS appears less present in developed Commonwealth of Independent States (CIS-7). Ahmed and Khan (2022) examined the relationship between short-term and long-term IRS risk and government debt, noting a brief decline in short-term spreads aftershocks, with long-term spreads staying consistent. Their findings contrast with those of Almeida and Divino (2015), who identified micro and macroeconomic factors as essential in influencing bank spreads in the Brazilian context. They identified the significant determinants of the ex-post banking spread in the Brazilian banking sector, considering the influence of the macroeconomic environment and specific characteristics of the financial institutions.

A review of global studies reveals various determinants that shape IRS, from banking sector attributes to broader macroeconomic indicators. In the context of Ghana, Azumah et al. (2023) emphasized the profound influence of banking sector reforms on the IRS. Their findings suggest that bank size, profitability, GDP growth, and inflation rate significantly influence Ghana’s bank IRS. Meanwhile, Beck and Hesse (2009) attributed Uganda’s increased IRS to higher operating costs, rising reserve requirements, and a noticeable lack of banking competition. This corresponds with Brock and Rojas-Suarez (2000) in their Latin American study, which also emphasized the destabilizing role of a fluctuating macroeconomic climate. Turning to the European banking sector, both Carbó-Valverde and Rodríguez-Fernández (2007) and Claeys and Vander Vennet (2008) highlighted bank-specific variables, such as size and efficiency, as primary determinants of bank interest margins. From a macroeconomic perspective, Obeng and Sakyi (2017) found that exchange rates and fiscal deficits are primary influencers in the Ghana banking industry. They estimated this using the autoregressive distributed lag approach and the error correction model. Concurrently, Shareef and Shijin (2017) explored the significance of inflation and money supply in the Indian banking industry. They found that the term structure of interest rates and macroeconomic factors significantly impact the Indian financial market. In an Australian context, Williams (2007) highlighted the role of bank market power in magnifying net interest margins. His finding suggests that banks with greater market power can charge higher interest rates, leading to higher net interest margins. Souza-Sobrinho (2010) found that Brazil’s pronounced bank IRS can be primarily accounted for by a policy that requires banks to invest about half of their deposits in mandatory reserves and selected loans. O’Connell (2023) expanded this narrative by exploring profitability determinants in the U.K. banking sector, emphasizing the impact of longer-term interest rates and inflation. The findings show that longer-term rates reflect how banks adapt inflation expectations, allowing management to adjust interest rates toward revenue. Additionally, the study found a positive relationship between profitability and short-term interest rates and a negative one toward inflation. Overall, these studies underline the complexity of IRS determinants, emphasizing the need for detailed region-specific analyses.

The extant literature reveals a consensus on the significance of economic growth, inflation, bank size, and credit risk in determining the bank spread. Our research contributes to the existing literature by empirically investigating what drives the bank IRS, specifically in WB6 countries. Previous studies have primarily explored factors like credit risk, liquidity risk, and financial access when investigating the IRS in the region. Our research holistically examines the influence of bank-specific and macroeconomic factors on the IRS and the potential implications of collusive agreements among banks. The distinctive economic, political, and historical attributes of the WB6 countries may influence their banking sector differently than other regions. Moreover, collusive agreements can introduce inefficiencies, potentially restraining the region’s economic progress. What differentiates our study is its regional focus, comprehensive variable set, and emphasis on the timely issue of collusion among banks. Thus, this research aims to broaden understanding of the banking sector’s challenges and opportunities in transition economies.

Methodology

The methodology contains subsection 3.1, where the data are described, and subsection 3.2, where the model is specified.

Data

This study examines the influence of macroeconomic and bank-specific factors on the IRS in WB6 countries. It utilizes two panels for analysis: the first focuses on macroeconomic indicators, while the second analyzes bank-specific ones. Data were gathered from an average number of 110 banks operating across the WB6 banking sector, covering the period from 2005 to 2022 based on annual frequencies (see Table A1. in the Appendix). The dataset series represents a balanced panel, with each variable accounting for 1,600 observations.

Table 1 presents the selected bank-specific and macroeconomic variables and their respective data sources. Bank-specific indicators are derived from the annual reports of the central banks of the WB6 countries, supplemented by macroeconomic indicators sourced from the World Economic Outlook (IMF) and the OECD Economic Outlook. In addressing the issue of null data, we employed a two-pronged approach: for missing values deemed non-systematic and sparse, interpolation methods were used to estimate values based on available data points; where missing data were extensive, indicating potential data collection issues, such banks were excluded from the analysis to preserve the integrity and reliability of our findings.

Definition and Measurement of Study Variables and Data Sources.

Source. Authors’ elaboration.

Note. This table presents the variables used in our work, definitions, measurements, and the primary sources from which the data were obtained. Variables are grouped into bank-specific and macroeconomic. The “Definition/Measurement” column describes how each variable is calculated. On the other hand, the “Source of data” column identifies the primary resource from which the data has been collected.

We integrate several bank-specific variables, including the Return on Average Equity (ROAE), Return on Average Assets (ROAA), and Non-Performing Loans ratio (NPL). The variables shed light on the financial performance, efficiency, and risk profiles. We incorporate Gross Domestic Product per capita (GDPC) and the Unemployment Rate (UNM) to account for macroeconomic conditions, reflecting the country’s economic health and employment scenario. Lastly, we include the Herfindahl–Hirschman Index (HHI), indicating a market concentration.

Table 2 presents the descriptive statistics of study variables for the WB6 countries from 2005 to 2022. Notably, Kosovo shows the highest average IRS at 8.49% and ROAE at 18.75% compared to the other WB6 countries. This implies the highest profitability level and the highest borrowing costs (See Figure 1 for detailed IRS trends for the six Western Balkan countries). Moreover, Kosovo holds the lowest Non-Performing Loans (NPL) at 3.91%, suggesting good credit quality and efficient risk management. Kosovo reports the highest unemployment rate at 34.18%, which could indicate potential future risks for loan repayments. A high Bank Concentration (HHI) at 2,258.83 indicates a less competitive banking industry. Despite Kosovo having the lowest risk components, its IRS has remained higher for an extended period compared to other countries in the region. North Macedonia has a GDP per capita of 4,187.76 EUR, a lower return on equity (ROAE) at 10.13%, and a gross domestic product similar to that of Bosnia and Herzegovina. This may result in reduced borrowing costs but also lower bank profits. It also has the highest rate of non-performing loans at 7.84%, indicating ineffective credit risk management that could explain the low ROAE. Although unemployment in North Macedonia is lower than in Kosovo at 26.84%, it remains relatively high. Furthermore, a bank concentration index 1,415.99 indicates a less competitive banking industry.

Descriptive Statistics for All WB6 Countries in Dataset Range (Year) 2005 to 2022; 11,220 Obs.

Source. Authors’ elaboration.

Note. This table presents a comprehensive breakdown of study variables, segmented for the WB6 countries from 2005 to 2022. The table indicates each variable’s mean, median, standard deviation (St. Dev.), minimum (Min), and maximum (Max).

Interest Rate Spread (IRS) for six Western Balkan countries.

Albania’s NPL rate is significantly higher than Kosovo’s at 12.13%, indicating less effective credit risk management. The lowest unemployment rate among all WB6 countries, at 13.91%, could be a promising indicator of future loan repayments. Its bank concentration index at 2,678.92 indicates a less competitive banking sector. Bosnia and Herzegovina has the second-lowest IRS at 3.71% and ROAE at 5.91%, indicating lower borrowing costs and reduced bank profitability. Its NPL rate of 8.53% is lower than that of North Macedonia and Albania but higher than that of Kosovo. The GDP per capita of 4,187.48 EUR is similar to that of North Macedonia, and the unemployment rate is relatively high at 23.80%. The bank concentration index at 808.28 indicates a more competitive banking sector. Montenegro is the only country in the region with a negative ROAE at −0.75%, indicating that its banks are currently unprofitable. Despite this, Montenegro shows the highest GDP per capita at 5,874.49 EUR, an occurrence that might be related to factors beyond the banking sector, such as a robust tourism industry. Its NPL at 12.75% is the highest, which could explain the negative ROAE.

Montenegro’s unemployment rate of 18.84% is lower than that of Kosovo and North Macedonia yet higher than that of Albania. Its low bank concentration index of 1,143.42 indicates a competitive banking sector. On the other hand, Serbia uniquely exhibits a negative IRS at −6.71%, distinguishing it from the other WB6 countries. Indeed, a negative IRS in Serbia could imply that banks offer higher returns on deposits than the interest rates they charge on loans. This unusual financial scenario might suggest an incentive for depositors and a potential strategy to boost liquidity within the banking sector. Serbia’s ROAE and ROAA are 6.15% and 1.14%, respectively, indicating moderate bank profitability. Meanwhile, its non-performing loan (NPL) rate of 10.65% is higher than Kosovo’s but lower than North Macedonia’s. Its GDP per capita stands at 5,281.83 EUR, which places it in the middle range among WB6 countries. Despite this, it experiences high unemployment at 16.97%, which could pose risks for future loan repayments. Moreover, with an HHI of 526.14, the lowest among the WB6 countries, Serbia’s banking sector indicates high competitiveness. These are general observations based on the provided data. The actual conditions in each country may vary considerably due to numerous factors not included in the data.

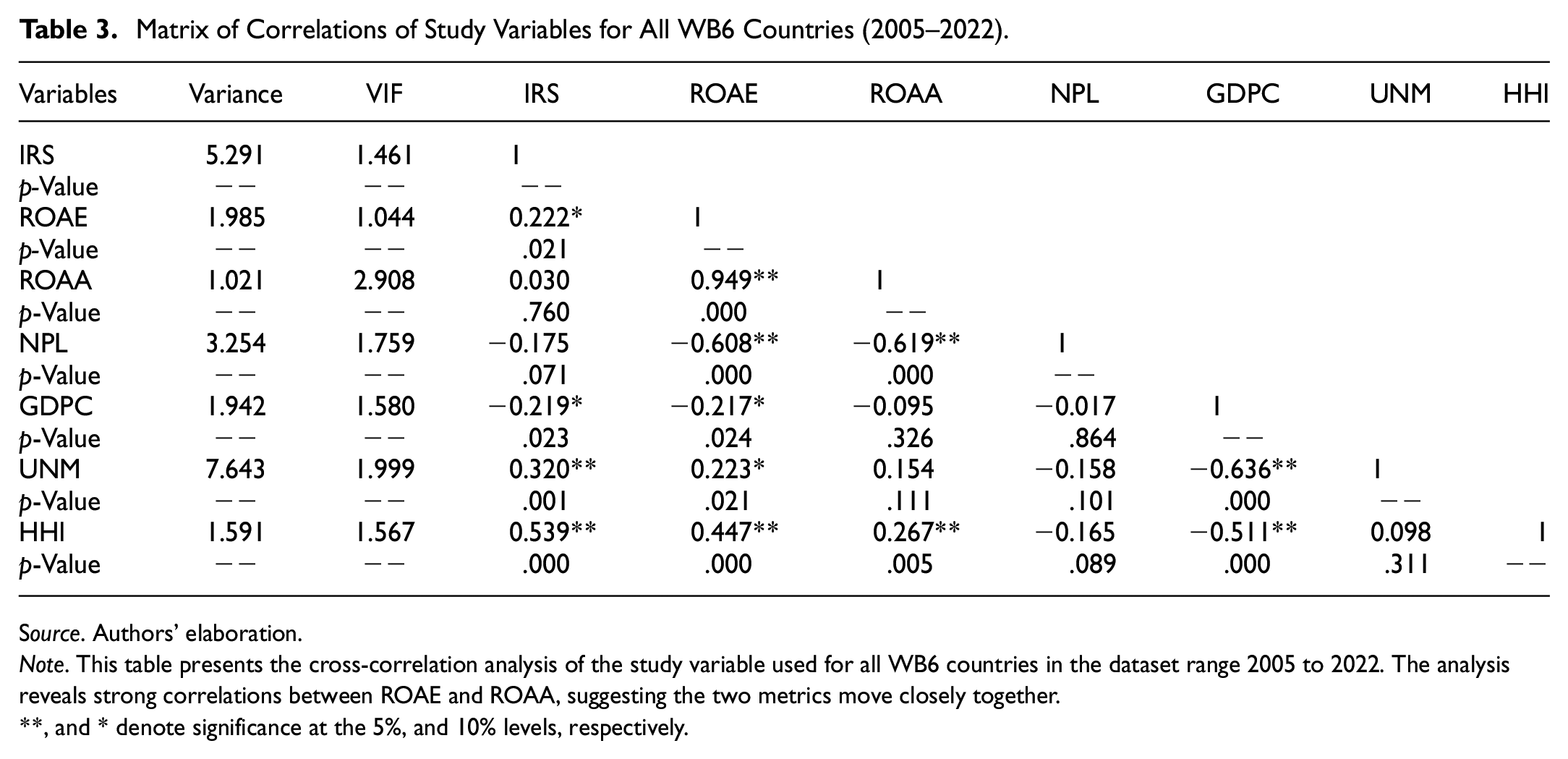

In analyzing the correlation matrix in Table 3, several significant relationships emerge among the study variables. Notably, a strong positive correlation between ROAE and ROAA with a coefficient of .949 indicates a close linear relationship between the two financial metrics. Both metrics are critical indicators of a bank’s financial performance, and their high correlation suggests that banks that manage their equity efficiently also tend to utilize their human and physical resources (assets) effectively. NPL indicates a strong negative correlation with ROAE (−.608) and ROAA (−.619), suggesting that increases in non-performing loans are generally associated with decreases in the return on average equity and average assets. This is an expected relationship, as bad loans often lead to financial losses, adversely affecting profitability. GDP per capita (GDPC) also shows a negative correlation with IRS (−.219) and ROAE (−.217), suggesting potential economic impacts on these financial indicators. This result implies that more stable economic conditions lead to tighter IRS, increased competition among banks, and potentially reduced profitability. UNM maintains a positive correlation with IRS (.320), suggesting that banks may increase the spread between lending and deposit rates as unemployment rises. Higher unemployment poses more significant credit risks, prompting banks to charge higher interest rates on loans to offset potential losses. HHI demonstrates strong positive correlations with IRS (0.539) and ROAE (0.447), suggesting that in more concentrated banking markets—where a few banks dominate—there tends to be higher IRS and greater profitability.

Matrix of Correlations of Study Variables for All WB6 Countries (2005–2022).

Source. Authors’ elaboration.

Note. This table presents the cross-correlation analysis of the study variable used for all WB6 countries in the dataset range 2005 to 2022. The analysis reveals strong correlations between ROAE and ROAA, suggesting the two metrics move closely together.

, and * denote significance at the 5%, and 10% levels, respectively.

Regarding multicollinearity, the Variance Inflation Factor (VIF) is an indicator that can be problematic in regression analyses as it can inflate the variance of regression coefficients. A VIF value greater than five typically suggests a problem with multicollinearity. Our results show that all study variables have VIF values well below this threshold. The highest VIF value is for ROAA at 2.908, suggesting that while it has the highest degree of correlation with other variables, it is still within acceptable limits. Thus, the VIF values for all variables indicate that multicollinearity is not a concern in this dataset.

Model Specification

In our research, we applied the Panel Vector Autoregression (Panel VAR) model, which considers all variables within the system as endogenous and recognizes their heterogeneity. The model adheres to the principles of traditional VAR, yet it extends its application through a panel data approach. The choice of the Panel VAR model for our study is grounded in its ability to capture the dynamic interactions between multiple time-series variables across different entities. This model is particularly suitable for analyzing the factors influencing the bank IRS in WB6 countries, as it allows for simultaneous consideration of macroeconomic and bank-specific determinants. This methodology aligns with our research objectives by enabling a comprehensive evaluation of the bank’s IRS determinants and ensuring that the research questions are addressed thoroughly. The Panel VAR requires that the series pass the unit root test and be stationary. For this purpose, three diverse stationarity tests were performed: the Augmented Dickey-Fuller test (ADF), the Phillips–Perron test (P.P.), and the Kwiatkowski–Phillips–Schmidt–Shin (KPSS) tests.

The study presents two models: Model 1 examines the impact of macroeconomic factors, while Model 2 focuses on bank-specific factors affecting the IRS. In general form, the Panel VAR model can be represented as follows:

Where:

Like traditional VAR, Panel VAR allows all variables to be endogenous in the system using autoregressive lags. Another advantage of this method is that it will enable the inclusion of the fixed effect (fi) that identifies invariant factors at a country level. We have used mean differencing since the fixed effects mainly correlate with the regressor. The correlation between fixed effect and regressor creates biased coefficients. This action eliminates all forward means of future observations for each country individually. The established Panel VAR, in our case, follows the same procedures as Love and Zicchino (2006). An additional essential element of the Panel VAR is common time effects (

The Panel VAR model, through orthogonal shock, allows for observing the shock of one input on another while keeping other inputs isolated. Since the errors of the covariance matrix are not orthogonal, in that case, we need to decompose residuals into the system. The estimations were completed through the impulse response function (irf) by restricting the period, the number of simulations, and the confidence band. The Monte Carlo simulation generates the confidence interval within the Panel VAR system. Macroeconomic elements and bank-specific ones maintain lag as it takes time to have their effects on NPL. At the same time, the order of variables in the system is of particular importance. Our ranking aims to assess the shocks originating from macro and bank-specific factors to the IRS. Our model also includes corporate income tax (TX) as an exogenous variable. The ideological orientation of the government influences corporate income tax, the local economic context, and the regional level of taxation. However, it is difficult to think that macroeconomic performance and bank-specific variables can affect TX. The variance decomposition (fevd) stands as an additional test to verify the accuracy of outcomes. The fevd measures the variation of one input to another (holding the others fixed) in a specific time interval. As for irf and fevd, we have limited the forward shocks for the subsequent six periods. Since our data are annual, the effects of irf and fevd are measured for the 6 years ahead. Before the Panel VAR is performed, the variables are tested to see if they maintain long-term co-integration through trace statistics and maximal eigenvalue. Both types of tests show that the test statistic (Test) is greater than the critical value with 1%, 5%, and 10% significance levels.

Results and Discussions

This section is divided into two parts, where in subsection 3.1, the outcomes from the impulse response function (irf) are analyzed, while in subsection 3.2, those of the variance decomposition (fevd).

Impulse Response Function (irf)

This subsection deals with the outcomes from impulse response function simulations for Model 1 and Model 2. To this end, Model 1 holds the impact of macroeconomic variables on the IRS, while Model 2 of the bank-specific ones. The irf for both models is based on the six periods ahead and one lag in the system. The irf plots were generated with 1,000 simulation trials at a 95% confidence band. Model 1 contains four endogenous and one exogenous variable. The system treated the two macroeconomic variables (GDPC and UNM) and two industry-specific variables (HHI and IRS) as endogenous. However, the corporate income tax (TX) was analyzed as an exogenous variable. Our interest in Model 1 lies in the impact that the IRS absorbs from other macroeconomic variables.

Figure 2 shows that from the four variables used in the system, only the GDPC significantly influences the IRS. This is understandable since the increase in GDPC increases the demand for loans and money supply (through deposits). At the same time, the rise in income per capita indicates an improvement in an economy’s health. In our case, a positive shock on GDPC impacts the increase in IRS, which will decrease afterward. The IRS in Model 1 tends to be influenced by its lags, meaning that the IRS maintains continuity (influenced by its past variance).

Orthogonalized impulse response function for Model 1.

On the other hand, the IRS evidently influences bank concentration (HHI) and the unemployment rate (UNM). Therefore, positive shock (increase) in IRS increases bank concentration and vice versa. This fact indicates that the IRS rises (decreases) due to the increased power of some banks in the industry, which reflects pricing power. A constant concern of the financial authorities in these countries has been the market power of specific banks in determining interest rates (both on deposits and lending), which is also reflected in these tests. The IRS also affects UNM, which is reasonable, knowing banks’ financial weight in this region. Banks remain the main creditors of the WB6 economies in the absence of a developed capital market. Banking activities remain the primary source of liquidity and private investments in the WB6. The results of Figure 2 (IRS on UNM) align with economic logic, where a positive shock in IRS increases unemployment and vice versa. The increase (decrease) in the IRS indicates that loans become more expensive (cheaper) for businesses and individuals. Higher spread directly affects the firm’s financial expenses and family budgets and shrinks economic activity.

The estimations from Figure 2 might be treated as an alarm for the national competition authorities in the WB6 countries. To this end, the IRS absorbs impact only from GDPC and its lags but not from HHI and UNM. Figure A1 in the Appendix shows that HHI has had continuous variation, with a downward trend (except in the case of North Macedonia). Standard microeconomic textbooks and economic history document that competition affects market prices. Apart from increased banking competition in this region (Figure A1 in Appendix), the IRS was influencing HHI, but the other way around. This result is consistent with the findings of previous research (Beck & Hesse, 2009; da Silva & Pirtouscheg, 2015). Since the liberalization of the banking sector in WB6, two to three banks have been the leading players (Aliu et al., 2016; Hake & Radzyner, 2019; Sanfey & Milatović, 2018). This fact and other concerns from various non-governmental organizations (NGOs) raise doubts about collusive agreements among banks. Collusion can be related not only to the interest rates but also to the division of the market in terms of customers.

Figure 3 presents the Oirf estimation for Model 2, standing on four endogenous and one exogenous variable. The plots clearly show the need for more significance of bank-specific elements (ROAA, ROAE, and NPL) in the IRS. At the same time, Oirf estimation shows that the IRS also does not influence ROA, ROAE, and NPL. So, the IRS in Model 2 moves unaffected by performance indicators (ROAA and ROAE) and non-performing loans (NPL). In contrast, other studies (Almeida & Divino, 2015; Azumah et al., 2023; Rathnayake et al., 2022) found that the IRS significantly impacts performance indicators. Changes in NPL affect the bank’s performance and the possibility of bankruptcy. These changes are not seen to be priced in the IRS, which raises doubts about the origin of this fact. Additionally, bank performance (ROAA and ROAE) should also be priced in the IRS, which is not. The banking industry has been more profitable than other industries since the liberalization of WB6 economies. It shows that the banks in these countries have kept the IRS changes detached from performance indicators (since they have constantly generated high profits). Bank profits were almost inevitable due to customer segmentation and the market power of particular banks.

Orthogonalized impulse response function for Model 2.

Considering Models 1 and 2, we can conclude that IRS is only affected by income per capita (GDPC). So, the interest rate on loans and deposits (IRS) depends on the economy’s capacity to take and offer liquidity. This result is similar to the findings of previous research on another area (Agapova & McNulty, 2016; Ahmed & Khan, 2022). If the banking industry in WB6 were sufficiently competitive, at least the IRS would be affected by HHI and NPL. These claims stand beyond the purpose of this research. However, they raise doubts linked to bank competitive issues.

Due to the low level of financial development in these countries, banks generate profits mainly from interest rates and banking services (IMF, 2017; Milenković et al., 2022). Consequently, the IRS remains a significant source of the bank’s earnings in the WB6 countries. To this end, the results lead us to the concern that banks in these countries are price takers or makers. Table A2 in the Appendix presents the regression results for the two models (A1 and A2). The results in the table align with those of irf and fevd. However, regression estimation is a snapshot of past movements, while irf and fevd analyze future shocks.

At the beginning of 2005 (Figure A1 in Appendix), the banking industry in Albania, Kosovo, and Montenegro was highly concentrated (HHI > 2500). Over the years, the industry has become more competitive due to banking sector liberalization, reducing the bank concentration level. North Macedonia is an exception, where since 2005, the level of concentration was constantly increasing. This lack of competitiveness in these three countries could justify higher IRS than in other WB6 countries. A decrease in IRS is observed with the increase in the number of banks (decrease in concentration).

Forecast Error Variance Decomposition (fevd)

This section analyzes the fevd results for Models 1 and 2 based on the differentiated series. As in Oirf and fevd, estimated forecasts have been generated for the 6 years ahead. In Table 4, the fevd results for Model 1 confirm those of Oirf, where the impact on the IRS comes mainly from GDPC. As can be seen, the effect of GDPC is growing; in the sixth year, it reached 21.3%. In this table, we have presented only those outcomes related to the influence of other variables on the IRS.

The Forecast Error Variance Decomposition.

Source. Authors’ elaboration.

Note. This table estimates Models 1 and 2 based on forecast error variance decomposition (fevd). The data covers the period from 2005 to 2022 based on different series and one lag in the system. As with or irf, forecasts for fevd are performed for the six periods ahead. Estimates have not been extended for additional years since the results remain unchanged. The calculated results are prepared in R studio through the “Panelvar” package and the “fevd_orthogonal” function.

The results for Model 2 show that IRS affects GDPC on average at 70.1%, UNM at 73.6%, and HHI at 64.9%. However, the fevd results regarding Model 1 differ from those of Oirf. The fevd estimations for Model 1 show that IRS affects ROAE at 25.3%, ROAA at 19.2%, and NPL at 28.1%. Estimates showing the impact of the IRS on other variables are available on request. The order of the endogenous variables has been changed, but the fevd results have remained the same. Estimates of Model 2 indicate that the IRS stands unaffected by other variables in the system.

To ascertain the robustness of our impulse response function (irf) and forecast error variance decomposition (fevd) outcomes, we conducted a series of tests varying the time horizon (periods ahead) used in our analysis. Initially, we extended the forecasting period from our baseline of six (6) periods ahead to ten (10) periods ahead, assessing the stability and consistency of the results over this longer timeframe. Subsequently, we condensed the analysis to a shorter horizon, again reducing the periods ahead to six (6) to examine if our findings persist under a more immediate temporal scope.

The results in Table 5 show a clear increasing impact of GDPC on the IRS variance from 10 to 6 periods ahead, indicating that GDP per capita becomes a more significant determinant of the IRS over time. UNM and HHI have made minimal contributions to the IRS variance, though a slight increase has occurred. IRS variance is unaffected by ROAE, ROAA, and NPL across two periods, which suggests that these bank-specific variables might not explain the variability of IRS in this particular model setup. Across both modifications, our results demonstrated consistent patterns and conclusions, indicating significant robustness of our irf and fevd findings to changes in the time horizon. This evidence supports the reliability of our baseline results, suggesting that they are robust and not contingent upon the specific duration initially chosen for the analysis.

Robustness Check for fevd Model Results.

Source. Authors’ elaboration.

Note. This table shows the results from Forecast Error Variance Decomposition (fevd) for two models. In Model 1, the table illustrates how macroeconomic factors like GDPC, UNM, and HHI contribute to the variance of IRS. Model 2 displays the influence of bank-specific factors like ROAE, ROAA, and NPL on IRS variance. A higher percentage indicates a stronger contribution to the IRS variance over different time horizons.

Conclusions

The banking industry remains the primary source of financing business operations in the WB6 countries. In this context, a competitive banking environment and lower IRS are essential to fostering the region’s economic growth. The region has experienced high lending and low deposit rates for a considerable period, leading to substantially higher IRS. The research examined the influence of macroeconomic (Model 1) and bank-specific (Model 2) factors on the IRS within WB6 countries, employing a Panel VAR model to analyze comprehensive data from 110 banks from 2005 to 2022. The findings reveal that macroeconomic indicators significantly impact the IRS, particularly GDP per capita (GDPC) and unemployment rate (UNM). An increase in GDPC and a reduction in UNM correlate with a decrease in IRS, suggesting that an improved standard of living can ease bank lending conditions and subsequently lower interest rates. However, it’s noteworthy that bank-specific factors such as Return on Average Assets (ROAA), Return on Average Equity (ROAE), and Non-Performing Loans (NPL) do not significantly influence IRS changes. This phenomenon may be attributed to the banks’ profitability in the WB6 driven by market segmentation. NPLs are maintained at manageable levels, allowing banks to base interest rate adjustments predominantly on macroeconomic indicators rather than internal factors.

Furthermore, our findings emphasize the importance of the banking sector in liquidity provision within the WB6 economies, especially given the limited alternatives for business financing. The significant influence of the GDPC, UNM, and the HHI movements on the IRS emphasizes the banking sector’s role in reducing unemployment and improving income per capita in the region. Interestingly, our findings indicate that the IRS influences HHI rather than the reverse, pointing to certain banks’ pricing power. Despite the decrease in HHI, the market concentration remains an ongoing concern for the competition authorities in WB6 countries. Our analysis highlights the need for enhanced regulatory frameworks to promote competition within the banking sector and improve financial inclusion. Given the significant impact of macroeconomic stability on the IRS, policies aimed at stabilizing inflation and fostering economic growth could indirectly contribute to narrower spreads.

One potential limitation of the study is the exclusion of variables such as liquidity, the degree of risk aversion, and operational costs from our model. Despite their recognized importance in the literature, these were omitted due to data availability constraints and the initial scope of the study. These variables represent essential aspects of banking operations that could further explain the determinants of the IRS. Additionally, future research should consider exploring the effects of political risk factors and regulatory frameworks on the banking sector by developing a holistic view of the challenges and opportunities within the WB6 countries. It sets a precedent for future studies to explore the implications of competitive practices and regulatory interventions on the banking sector’s efficiency and stability. As the banking industry continues to evolve amidst the changing economic environment and technological advancements, the insights derived from this study could serve as a valuable reference for policymakers, regulators, banking professionals, and scholars in examining the complexities of the banking sector in transition economies and beyond.

Footnotes

Appendix

Panel VAR Regression Results of Models 1 and 2.

| Model 1 | ||||

|---|---|---|---|---|

| IRS | GDPC | UNM | HHI | |

| Lag1_IRS | −0.0025* | 0.0991* | −0.0002 | −0.0599 |

| Lag1_GDPC | −5.0046* | 1.2968*** | 3.3150* | −0.0108 |

| Lag1_UNM | 0.0193* | −0.3123* | −0.0109* | 0.2045* |

| Lag1_HHI | 0.0026 | 1.2325 | −0.2962* | −1.6693 |

| TX | −0.0038* | −0.0396* | 0.0025* | 0.0272* |

| Const. | −0.0000* | −0.0086* | 0.0000* | 0.0062* |

| Model 2 | ||||

| IRS | ROAE | ROAA | NPL | |

| Lag1_IRS | 0.0000** | 0.4775 | 0.0618* | 0.5266** |

| Lag1_ROAE | 0.0000 | 0.6214 | 0.0112 | −0.2190 |

| Lag1_ROAA | 0.0000 | 0.1423*** | 0.0091 | −0.0744** |

| Lag1_NPL | 0.0000 | −0.7922* | −0.1892** | 1.2286*** |

| TX | 0.0000*** | 0.9191** | 0.0266 | 0.3679 |

| Const. | 0.0000** | 0.0765** | 0.0020 | 0.0306* |

Source. Authors’ elaboration.

Note. This table presents estimated coefficients and standard errors related to Panel VAR regression results. Model 1 deals with macroeconomic factors, while Model 2 with bank-specific factors. The data are differentiated to pass the unit root tests and cover the period from 2005 to 2022. Each variable holds 1,600 observations, while the regression is performed based on one lag in the system.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.