Abstract

Abundant literature infers the negative incidence of financial liberalization in the banking sector. As interest rate marketization is a reality in China, we empirically investigate the determinants of commercial banks’ financial performance using 10 listed Chinese commercial banks for 1999 to 2019. Our findings suggest that net interest margin (NIM), non-performing loans (NPL), and asset size (LnAsset) are the key drivers of profitability in Chinese banks. Interestingly, for the sample of city banks observed, we find that bank performance is strongly driven by sound management of the assets and the retail interest margins. On the opposite, the joint-stock banks’ strong diversification leads to lower reliance on net interest margins. Our results also suggest that joint-stock banks’ asset size puts strong pressure on their overall performance and exert a diminishing return effect as their assets’ critical size generates proportional administrative expenses that hinder profitability.

Introduction

Interest rates are a significant component of a modern country’s finance and economic growth. Changes in the former reflect and affect the country’s capital and currency market operations (X. Li et al., 2021). Because of their significance, nations’ interest rates were tightly controlled until the 20th century; a legitimate approach since interest rates are an essential macroeconomic regulation and control tool. After the 1970s, a wave of interest rate marketization reforms was launched worldwide. The movement led by the United States aimed at supporting the improvement of the financial market while addressing the challenges of financial disintermediation and unbalanced resource allocation. Nowadays, most economies, including Japan, Argentina, and South Korea, have effectively liberalized the interest rate market. Alternatively, China’s economy faced substantial challenges while moving toward a disintermediated finance and optimal resource allocation (B. Liu et al., 2018). In 1996, the Central Bank liberalized the inter-bank lending rate. The following 20 years adopted gradual market-oriented reforms that gradually liberalized the interest rates on bonds, funds, deposits, and loans.

Financial market liberalization in China was a milestone. The liberalization process, which revolved around the adoption of gradual reforms, is often described as watchful and relatively slow in view of the mutations noticeable in the other sectors of the economy (e.g., market of goods and capital). Previous literature points out a sequential approach that forced the Chinese financial sector to lag behind in terms of independence and efficiency. While China has historically reached a point where advanced financial market restructuring was essential to induce greater structural economic prospects, a significant step toward the marketization of interest rates was taken in October 2015, with the removal of the ceiling restrictions on the deposit rates. The deposit and loan interest rates were fully liberalized entirely in October 2017, a date marking the marketization of interest rates in the country. The international experience has shown that the liberalization of interest rates should be accompanied by important structural and quantitative transformations in order to prevent financial disasters. In the case of China, although scantly explored in the literature, Interest rate liberalization was a critical financial reform. Only few works examine the potential impact of marketized interest rates on bank-level performance. As such, this paper attempts to fill the gap.

Market-oriented reforms focusing on interest rates liberalization are steps toward optimizing resource allocation and financial operations freedom (Barrell et al., 2017). However, whereas interest rate marketization often channels greater efficiency and brighter economic prospects, it also conveys risks to the banking industry and the whole financial sector. Interest rate marketization generally leads to narrower interest spreads, significantly cutting commercial banks’ primary income sources (Meng et al., 2020). Commercial banks’ stability is essential for a flourishing real sector, and it is practical to observe the mutations instigated in the listed commercial banks in an interest rate marketization environment. This study focuses on identifying the determinants of profitability in Chinese A-share commercial banks. In the present context, though the interest rates remain a vital instrument of the country’s monetary policy, the lending and deposit rates are strongly affected by the fierce competition among commercial banks. Interest rates on deposits are pressured to rise to attract depositors. On the other hand, financial intermediaries are pushed to lower interest rates on borrowings due to the industry’s price competition. Under this double pressure, the spreads have gradually shrunken (K. Liu, 2017), and commercial banks’ profitability has been severely compressed (H. Wang et al., 2019).

Table 1 provides the net interest margins of listed commercial banks for 2014 to 2019. It shows that the interest spread has fluctuated to varying degrees since 2014. In 2015, the financial bubble pushed the People’s Bank of China to raise its deposit and lending rates. It had naturally had an incidence on borrowers and savers. A similar trend was observed in 2016, as the Central Bank raised the Renminbi (RMB) deposit and loan rates on three occasions. In 2018 and 2019, the People’s Bank of China resumed cutting its interest rates, and relatively few banks saw net interest margins rise. In the interest rate liberalization process, small and medium-sized banks are more exposed. It is mainly due to its asset features and profitability characteristics. However, large banks enjoy an absolute advantage in asset scale, deposit and loan quality, marketing outlets, staffing, and market reputation. These strengths allow them to reduce their dependence on deposits and loan spreads. Hence, large banks easily cope with interest margin cuts while also spurring vigorous innovations in intermediation activity (Chan & Ji, 2020).

Listed Banks Net Interest Margin (%) for the Period of 2014 to 2019.

Source. Listed company annual reports.

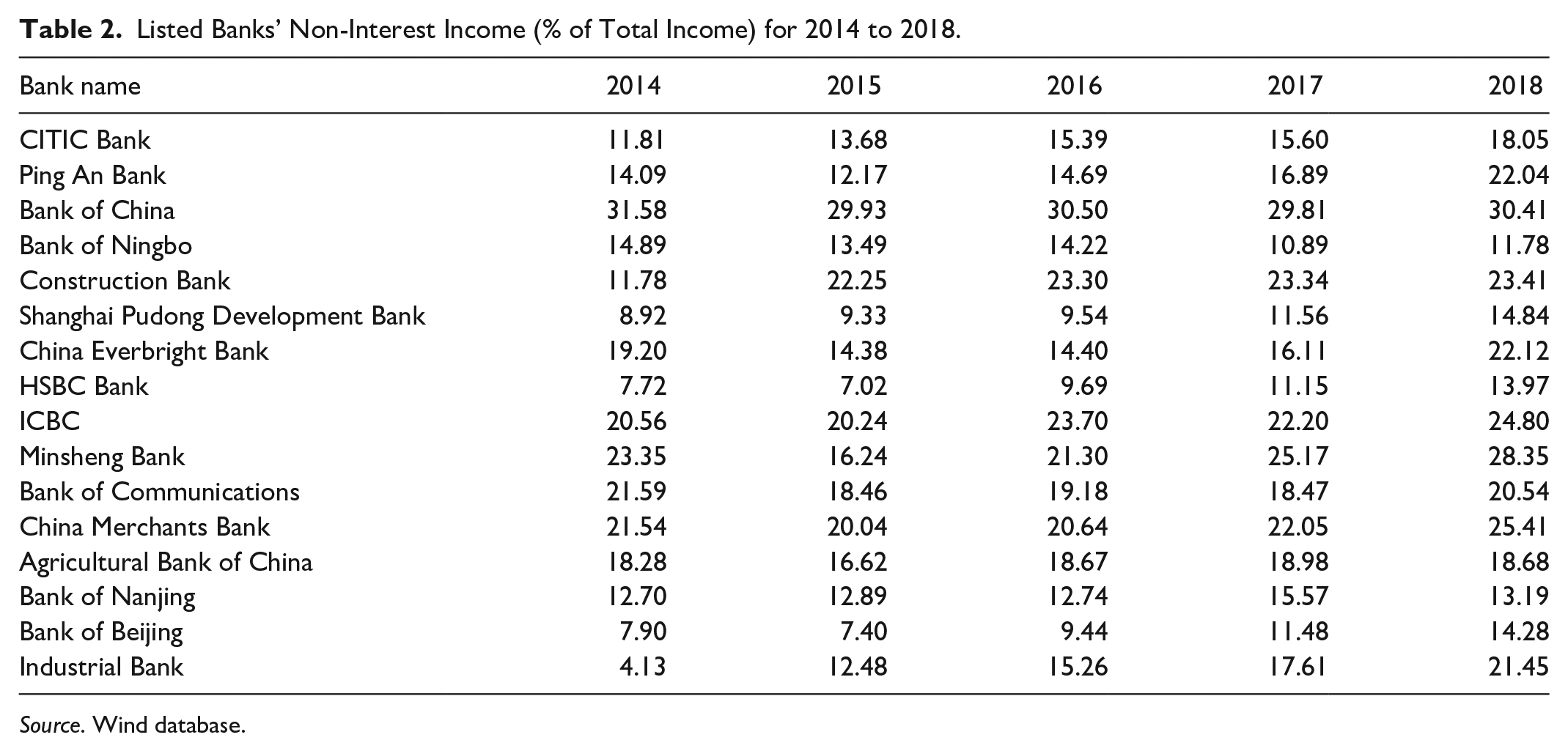

As the primary source of revenue, the intermediation margin directly impacts banks’ long-term development. Its contraction over the years pushes the Chinese banks toward innovation in their business and management model. With the progression of interest rate liberalization, commercial banks seek new profit growth opportunities. Among the adjustments observed in the banking industry, commercial banks in China have strategically expanded their intermediation and off-balance sheet activities to generate interest and non-interest-based income (Zhang & Deng, 2020). A detail of banks’ non-interest income is provided as follows:

As displayed in Table 2, Chinese commercial banks’ non-interest income have consistently increased with the marketization of interest rates. The changes brought into the conventional intermediation business constitute a critical aspect of commercial banks’ product innovation. In the meantime, more importance was attributed to the development supportive financial services. This is because Chinese commercial banks have observed a persistent increase in their underlying revenues over the period of financial restructuring. According to some recent statistics (Wind Financial Database), the first two quarters of 2019 was marked by a 16.10% increase in the revenue of 16 listed Chinese banks. It is a significant upsurge in view of these entities’ performance in the previous year. While, banks individual performance stood at varying levels, Ping An Bank registered the most significant increase in its intermediation revenue with 77.58%, surpassing its first competitor China Merchants Bank.

Listed Banks’ Non-Interest Income (% of Total Income) for 2014 to 2018.

Source. Wind database.

Literature Review

Interest rate marketization is a major component of the financial liberalization process. Early studies sustained interest rates marketization’s importance in enhancing the banking sectors’ efficiency and promoting nations’ economic growth. The “financial suppression theory” and “financial deepening theory” (McKinnon, 1973; Shaw, 1973) are two examples of pioneer theories that hypothesize the beneficial effects of interest rate liberalization. These seminal works theorized that banking sector interest rates should be marketized to induce an adequate allocation of financial resources and promote the industry efficiency (Cho, 1990). Summers (1992) identified three direct channels through which financial deregulation affects intermediation and performance in a subsequent review of financially repressed economies. At first glance, interest rates marketization leads to the market determination of the retail rates. As the former affects the demand deposit rates, the economic agents’ propensity to save rises and commercial banks intermediate more resources. It positively affects interest rate spread, aggregate investment, and economic growth.

Furthermore, liberalization enhances intermediation efficiency. Following the market-based determination of interest rates, banks adjust their lending rates to the default risks perceived with investments. It is the basis of the greater allocative efficiency that contributes to overall bank assets quality. At last, deregulation brings additional competitors, which promotes efficiency. As the banking sector deregulation deepens, new banks seize the opportunity led by the increased volume of loans, the greater demand for finance and the derived profitability prospects. Regarding the X efficiency hypothesis, the banking industry concentration is diluted, impacting the intermediation cost and performance (Phan et al., 2016).

Levine (2005) also highlighted the positive influence of financial liberalization. Apart from providing a critical review of the finance-growth literature, Levine (2005) discussed the necessity for lawmakers to liberalize their banking systems to enhance the intermediaries’ productivity. As growth is equally affected by the financial intermediaries’ depth and efficiency, a sufficient level of liberalization becomes a prerequisite for observing finance-induced economic growth. Quinn and Toyoda (2008) provided further evidence for the “McKinnon–Shaw hypothesis” and the “Finance-led Growth Hypothesis” through the study of capital account liberalization for 94 economies and suggested that international financial openness positively impacts growth in their empirical results by investigating no less than 50 years (1950–1999). Recently, Hamdaoui and Maktouf (2018) empirically reviewed the implications of financial liberalization on wealth creation for 49 economies. The analysis underlined the positive effect of financial deregulation on sustained growth throughout the observed period (1980–2010) and did not omit to differentiate between advanced and emerging markets. Although the study’s findings favored the McKinnon-Shaw effect, the authors pointed out the critical role of financial liberalization reforms before financial crises. Chang (2000) reported that countries with developing markets and fragile regulatory frameworks are largely exposed to information bias, and moral hazard problems as such disruptive financial reforms are the ideal background for financial crises.

Several researchers examined the impact of financial deregulation on commercial banks’ performance from a narrower perspective and considered the banking industry’s natural reliance on interest rates (Abbas & Malik, 2008; Robin et al., 2018). Saunders and Schumacher (2000) used data on commercial banks from 1988 to 1995 and observed that the financial sector’s regulatory framework and the volatility of interest rates are strongly affected by the commercial bank performance proxied by bank interest rate margin (NIM). Their results gathered from the investigation of 614 European and American banks show that commercial banks’ profitability is directly exposed to macroeconomic factors that carry equal amounts of risks and opportunities in a liberalized environment. Further evidence on the financial liberalization—banks performance relationship is provided by Robin et al. (2018). Their empirical study used a panel data regression framework with traditional financial performance proxies (ROA, ROE, and NIM) to reveal the overall improvement of the banks’ asset quality, capital strength, and net interest margins (NIM) following the liberalization reforms that prevailed during the period 1983 to 2012. Even though the financial deregulation had no significant direct impact on ROA and ROE, these mutations pushed the intermediaries to adopt viable strategies to strengthen their profitability.

Iftikhar (2016) proved that interest rate marketization and bank interest margins are negatively correlated among the studies that found different results. As the analysis is constructed around a two-step system of the Generalized Method of Moments (GMM) framework, a sample of 1,300 banks from 76 countries and a set of financial liberalization proxies (including credit interest rate liberalization, entry barriers), the results implied that the liberalization of interest rate and the lift specific entry barriers enhance the competition and efficiency of the banking sector thus reduces the bank interest margins. Ting (2016) reported similar views that reveal the negative incidence of financial liberalization on commercial banks’ performance. The author investigates more than 500 banks from 42 countries during the 2008 financial crisis. While inconsistent with the “McKinnon effect,” the outcomes have shown that government interventions enhance the banking sector’s profitability and stability. On the other hand, financial liberalization is proven to yield the opposite effect, leading a diminished profitability and asset quality for commercial banks.

Concerning China’s financial liberalization reforms, M. Li and Lan (2020) surveyed eight A-share banks between 2007 and 2018. The study has found a non-linear relationship between interest rate marketization and the operating performance of commercial banks measured by ROA. The authors exerted that the deepening of interest rate marketization reforms positively affects banks’ ROA in the short run. It mainly derives from the banks’ asset management capabilities. In the long run, commercial banks’ ROA follows has an inverted U-shaped behavior driven by the increase in the cost-income ratio and a decrease in non-interest income ratio and deposit loan ratio. Also, Meng et al. (2020) studied the link that prevailed between interest rate marketization and performance, considering 16 listed Chinese banks from 2008 to 2018. Using Demirgüç-Kunt and Huizinga (1999) approach, the study showed that financial liberalization reforms had induced changes in bank profit characteristics and a lower reliance on interest rate spreads. As the spread has been gradually reduced, the study observed that the profit structure of commercial banks has been affected. Further, J. Li and Liu (2019) marked the efficiency of the monetary policy transmission mechanism before and after the marketization of interest rates. Their study purports the enhanced effectiveness of the transmission mechanisms and stronger competitiveness among Chinese commercial banks due to China’s interest rate marketization reforms.

Several researchers (K. Liu, 2017; B. Liu et al., 2018; Tan et al., 2016; Y. Wang, 2016) have explored the consequence of interest rate marketization, however the foremost of these papers have focused on loan pricing risks. Only a scant literature examined the incidence of interest rate liberalization on bank performance while taking into account banks legal structures. This paper fills the gap by using a comparative analysis method to comprehensively analyze Chinese commercial banks with respect to their legal forms.

Data and Methodology

This paper empirically investigates the determinants of banks’ profitability in an interest rate liberalized market for 1999 to 2019. Our final balanced panel data set consists of 10 Chinese A-share commercial banks’ data obtained from the Wind Financial Database. Altogether, these 10 institutions handle most of the intermediation carried out by the Chinese banking sector.

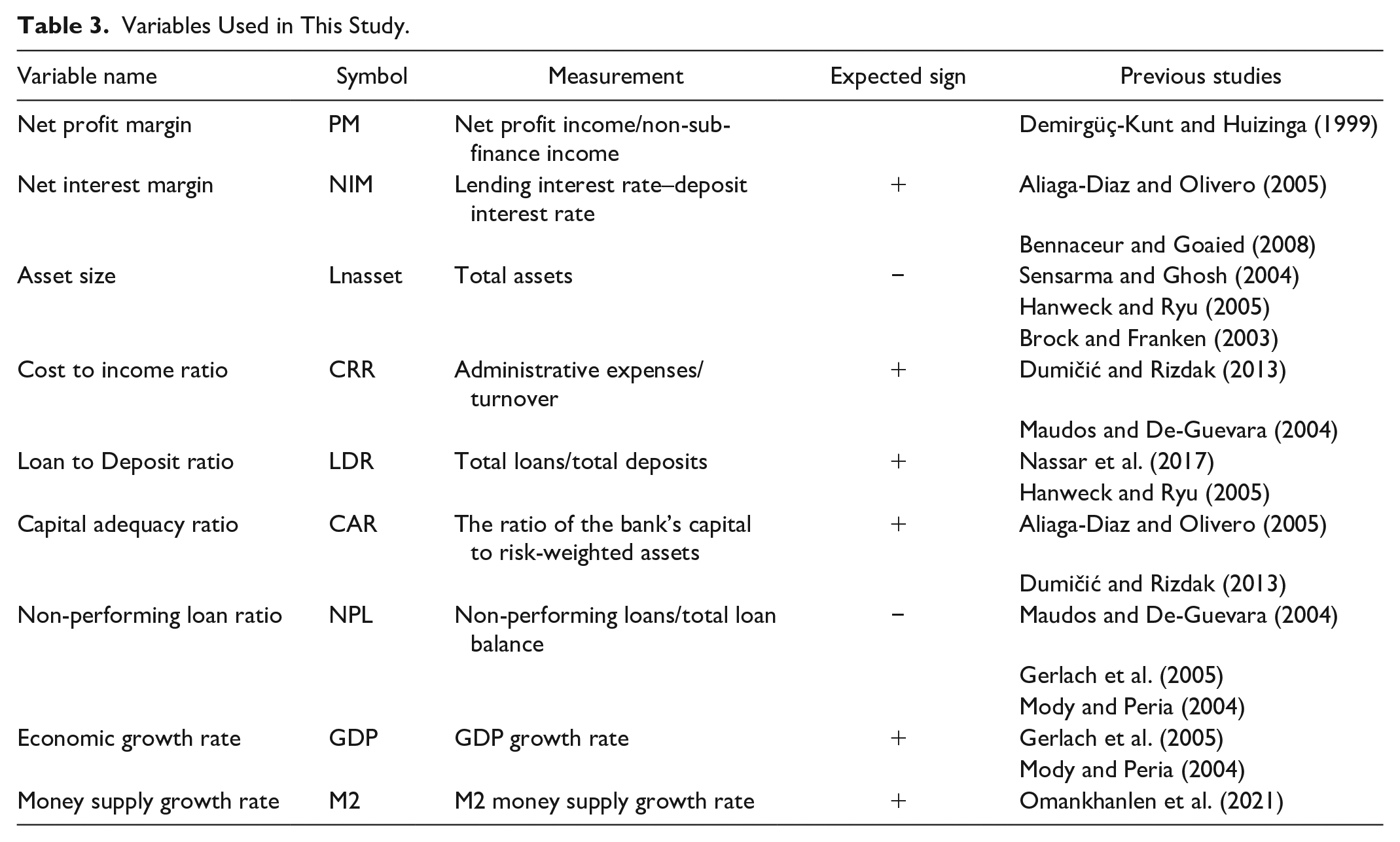

Following Javaid (2016) and Alfadli and Rjoub (2020), the bank-specific determinants are supplemented by macroeconomic variables extracted from China’s National Bureau of Statistics’ quarterly data. Based on the numerous previous studies related to the determinants of bank profitability in the world literature, we have selected some variables. Table 3 presents the exhaustive list of variables in use for the study.

Variables Used in This Study.

Throughout the literature, researchers have adopted various methodologies to observe the determinants of banks profitability. Obviously, the preferred frameworks are tied to the nature of data collected. Gujarati et al. (2012) used a balanced panel data analysis by employing 10 Chinese commercial banks from 1999 to 2019 to provide an efficient econometric estimate compared to other data sets. To make their estimate consistent and comparable, the authors test all the assumptions required at the initial data analysis stage. Subsequently, fixed and random effect linear regressions are applied to the investigation.

Methodologically, the analysis adopts three samples investigated with equation (1). The primary selection (sample 1), composed of 10 Chinese A-Share commercial banks, is examined in its state and, side by side, with two subsamples formed in consideration of the institutions’ legal structure. Hence, sample 2 encompasses seven commercial banks of joint-stock form (China Merchants, CITIC, Huaxia, Industrial, Pudong Development, Minsheng, Ping An Bank, respectively). The third sample considers banks of three cities recognized for their strong ties to the local government and their state-owned characteristics: (Bank of Beijing, Bank of Nanjing, and Bank of Ningbo).

Due to China’s financial system’s imperfection and over-concentration, financial institutions lack sufficient competition. For several years, banks in China have counted on interest rate spreads as their primary source of profitability. Following the western experience, interest rate market reforms came to break this bottleneck and enhance banks’ competition while narrowing the spread of retail rates. Considering the findings proposed by M. Li and Lan (2020) and Robin et al. (2018), this research assumes that interest rate marketization positively affects commercial banks’ profitability. However, while the latter holds, the analysis hypothesizes a dissimilar effect of interest rate marketization on banks’ profit-making mechanisms in small and larger commercial banks. Considering the asset size and bank nature captured by samples 2 and 3, city commercial banks’ profitability would depend highly on net interest margins and asset quality. In contrast, joint-stock commercial banks shall be less exposed to retail rates contraction. Following Demirgüç-Kunt and Huizinga (1999) and Meng et al. (2020) investigated this relationship through the regression model.

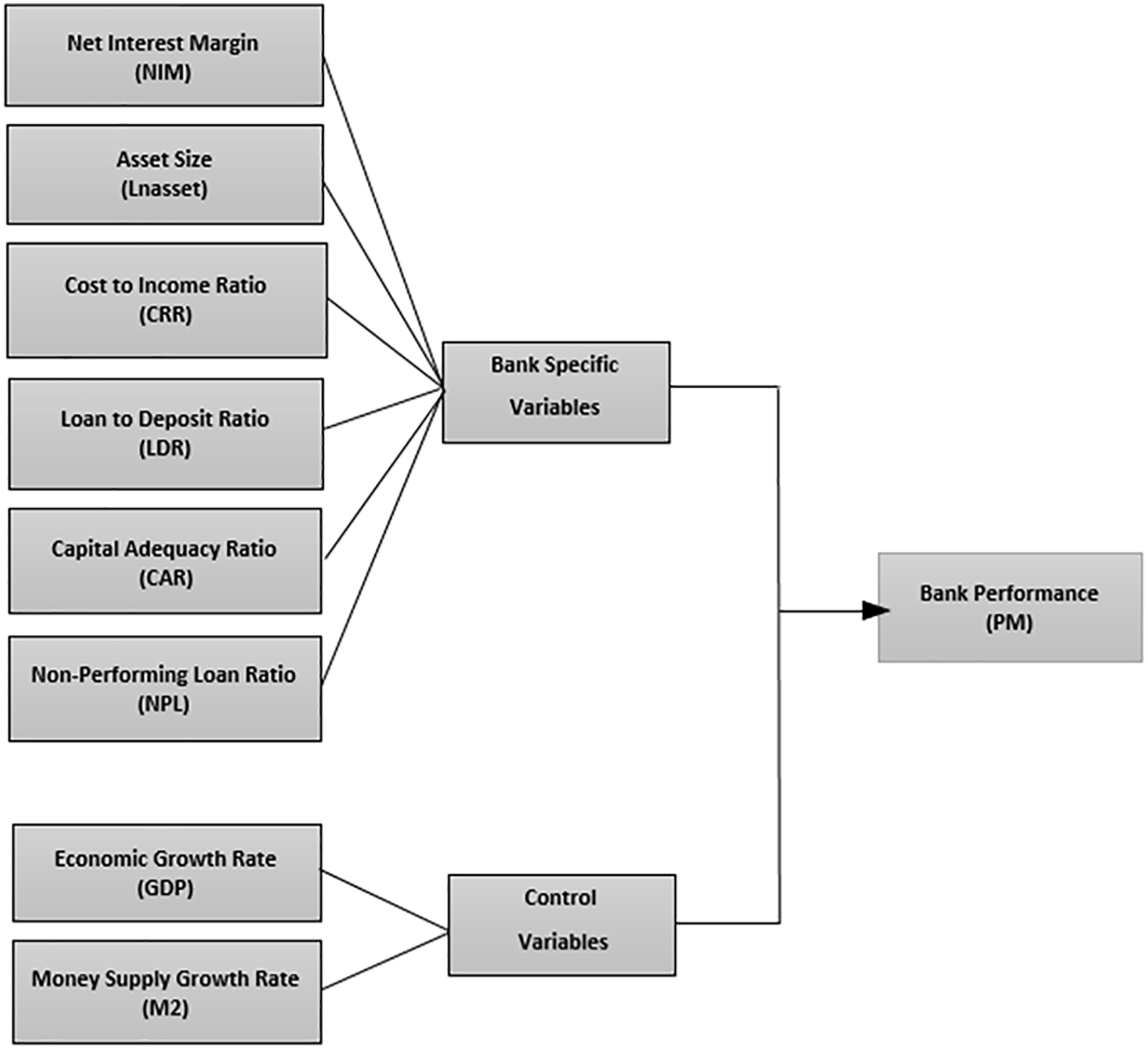

Where PM is the single measure of commercial banks’ profitability used as a dependent variable, NIM stands for bank i net interest margin in year t, and X includes a set of bank-specific variables (Lnasset, CRR, LDR, CAR, and NPL). Similarly, D represents the set of macro-factors used as control variables (GDP and M2), while α is a constant term. β0, β1 to β3 are regression parameters corresponding to the explanatory variable and ε is a random error term corresponding to the explanatory variable. Figure 1 presents the detailed conceptual framework of the study.

Conceptual framework of the study.

Empirical Results

Table 4 provides a self-explanatory descriptive statistics analysis. To assess the stationarity of data, we carried out the Augmented Dickey-Fuller and Phillips-Perron tests using E-views software (Rathnayake et al., 2019). Results for the unit root test are summarized in the following Table 5. According to the results, all the variables are stationary at the first difference in a 1% significance level since the calculated t statistic values are greater than −3.5482 (p < .01). Further, the variables exhibit a 1% significant level trend that allows a linear regression fit.

Descriptive Statistics.

Note. The detailed definitions are reported in Table 3.

Unit Root Test and Trend Results.

Note. We observe similar results while running the test under intercept or trend and intercept configuration. Table 5 provides the only trend and intercept values. The detailed definitions are reported in Table 3.

**, and * means significant at 1%, 5%, and 10% level, respectively.

Panel data models include fixed-effect, random-effect, and mixed-effect models. To ensure the accuracy of the results, we first run the F test with the null hypothesis for mixed-effect. The results in Table 6 show that the three models’ p-values are all less than .01; therefore, we reject the null hypothesis.

F Test Results.

Note. The detailed definitions are reported in Table 3.

means significant at 1%.

In the second step, we use a Hausman Test to determine the proper setting for the investigation (Fixed effect or Random effect). The Table 7 results indicate that the random effect is preferred for model 1 investigating the total sample. The fixed effect setting is more appropriate for models 2 and 3 that examine smaller samples (two and three samples).

Hausman Test Results.

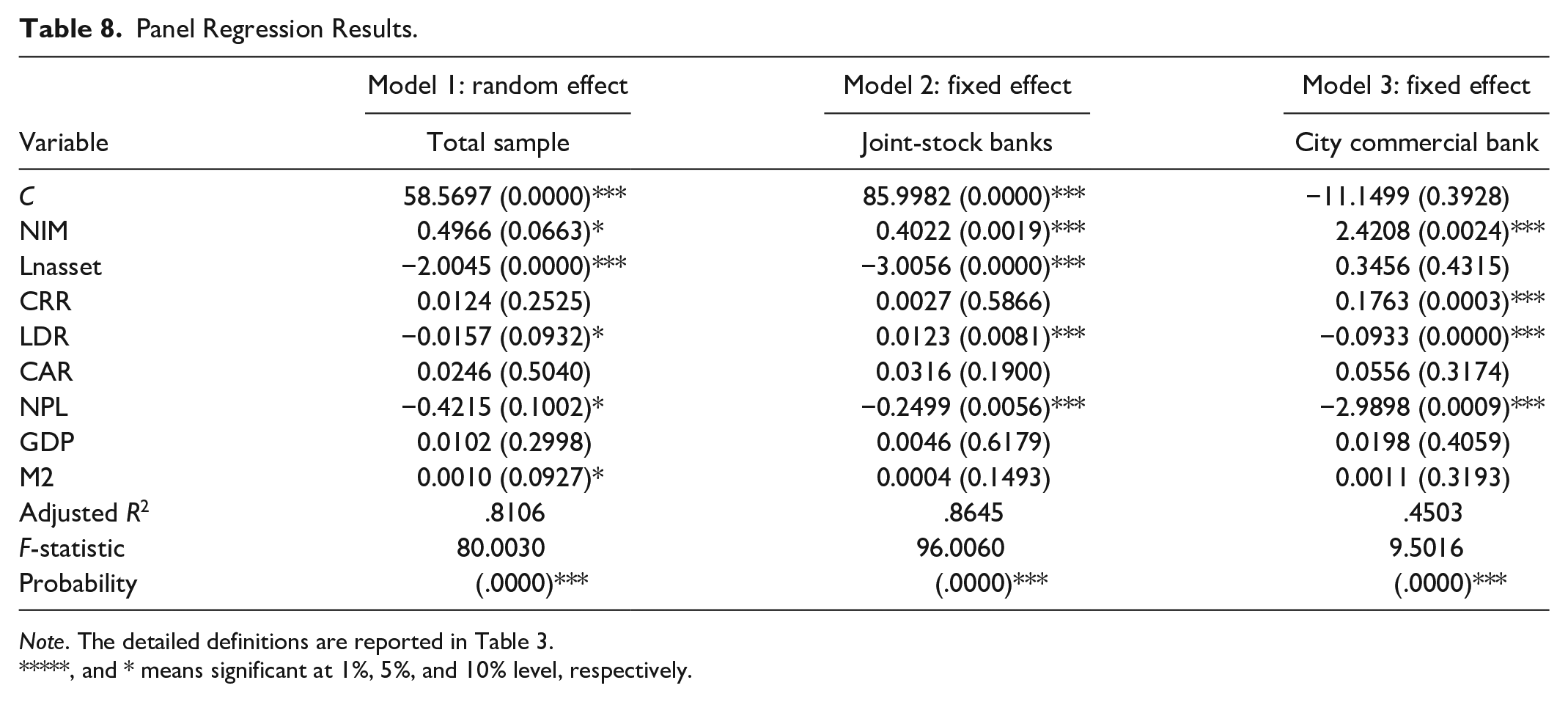

Table 8 reports the empirical results of models 1 to 3. The adjusted R2 observed in panels 1 and 2 (.8106 and .8645, respectively), indicate a good model fit. Model 3 adjusted R2 is also satisfying since panel three’s low R2 value can be explained by the smaller size of the investigated sample. Sample 3 is composed of the observations collected for three city banks. Besides, Table 8, the last row, shows that the three models’ F values are large, while the overall p-values are close to 0. It indicates the overall relevance of the three models selected for the investigation.

Panel Regression Results.

Note. The detailed definitions are reported in Table 3.

**, and * means significant at 1%, 5%, and 10% level, respectively.

On other grounds, the estimated coefficients of NIM are all positive and significant for models 1 to 3, in line with previous studies (Aliaga-Diaz & Olivero, 2005; Bennaceur & Goaied, 2008). That implies that despite the bank’s intrinsic characteristics (joint-stock or city commercial banks), the NIM has a significant incidence on commercial banks’ performance. The positive correlation suggests that shrunken NIM drives down the banks’ performance measured by PM in a liberalized environment. While these results align with the assumption made in Section 3, the NIM coefficients observed in panels 2 and 3 also show the different magnitude of NIM in smaller and larger banks. The NIM’s coefficient for the joint-stock Banks is much smaller than that of the city commercial banks, indicating that a change in interest spread significantly impacts the city commercial banks’ profitability. These values show that joint-stock and city commercial banks pursue different profit creation strategies. While the city commercial banks remain strongly dependent on their primary intermediation activity (granting loans and accepting deposits), larger commercial banks (joint-stock commercial banks) prioritize diversification and innovation. These two approaches toward profit generation are one reason for the banks’ exposure to non-systematic risks. As the estimated coefficients of NPL are significant and negatively correlated to bank performance for the three models, the values displayed in panels 2 and 3 indicate that city commercial banks are twice more affected by defaulting borrowings than joint-stock banks. These findings are in line with the results of Laryea et al. (2016). Financial liberalization causes important market pressure that forces commercial banks to enhance their assets quality; the former being closely related the intermediation margins.

Table 8 reports a significant negative correlation for the total sample and joint-stock banks concerning the size and profitability relationship where, Gul et al. (2011) and Singh and Sharma (2016) obtained similar results. While Pasiouras and Kosmidou (2007) found similar results, the estimated values suggest that joint-stock commercial banks’ asset size has exceeded their optimal size, leading to a phenomenon of diminishing marginal return. The substantial scale of the joint-stock banks’ assets and the cost pressure induced by the financial sector’s liberalization are plausible reasons to sustain these findings. Besides, model 3 estimates exert an insignificant but positive association between the variables size and profitability. It depicts a conservatism strategy that mitigates the costs of a strong presence in the market. City commercial banks would prioritize a strategic expansion to promote the profit model’s transformation in the present context.

When assessing the cost-income as a determinant of performance in Chinese listed commercial banks, models 1 and 2 estimates reveal a positive but insignificant correlation between the CRR and PM. However, model 3 coefficients point out a significant positive correlation concerning the sample of city commercial banks. Although the bank assets size may partially induce these values, they suggest that improving the cost control capability after interest rate reform shall promote commercial banks’ profitability transformation. In this setting, city commercial banks are particularly favored mainly due to the scale of their assets.

Another variable of significance in the investigation loan to deposit ratio (Menicucci & Paolucci, 2016; Regehr & Sengupta, 2016) indicates banks’ liquidity. The estimated coefficients for models 1 and 3 suggest that LDR is significantly and negatively correlated with profitability. In contrast, the variable positively affects the net profit margin for the sample of joint-stock commercial banks. These results denote major strategic differences in the conduct of lending-deposit activities. For the sample of joint-stock commercial banks, the positive value observed suggests that banks relatively mitigate the intermediation activity risk. It might result from a diligent assessment of the customers seeking funding and a sign of reliance on deposits to finance new loans. Proper deposit-loan ratio control can ensure asset quality and reduce risks. Increasing the loan-to-deposit ratio would incentivize profitability in an efficient funding strategy for city commercial banks.

Alongside the former proxies (Djalilov & Piesse, 2016; Menicucci & Paolucci, 2016), the capital adequacy ratio is considered as it stands for the overall measure of banks’ solvency. The empirical results in Table 6 depict a positive but insignificant relationship between capital adequacy ratio and profit margin. While similar findings are observed for the three models used, they could be tied to the China Banking Regulatory Commission (CBRC) attachment to the capital adequacy ratio standard among the Chinese banks. Hence, although raising the capital adequacy ratio may positively influence profitability, the variable does not appear to be a strong determinant of Chinese banks’ performance.

Among the macroeconomic variables used in the study, GDP has no significance in the three models. Money supply growth rate (M2) is significantly positively related to profitability for the total sample, which aligns with our expectations and our results are similar to Omankhanlen et al. (2021). However, considering the estimated coefficients for the three models, we conclude that bank-specific proxies rather than macroeconomic proxies determine much of the banks’ profitability. Our results are consistent with the similar outcomes of Ahmad et al. (2016).

Robustness Check

We repeated the panel regression analysis for the robustness check by using the GMM estimation model (Table 9). We have found the signs of all explanatory variables to be almost identical and unchanged from the results in Table 8. However, the new results have created some variations in the significance of the variables. Interestingly, all R2 values are increased, and the significance of the F-statistic remains the same in the new results. Thus, we conclude that our results are robust.

Panel GMM Results.

Note. The detailed definitions are reported in Table 3.

**, and * means significant at 1%, 5%, and 10% level, respectively.

Discussion

Commercial banks must revisit their risk management strategies and adapt to the new market characteristics in an era of interest rate liberalization and the banking industry’s steady opening. As interest rate liberalization increases the competitiveness of the banking industry, Chinese commercial banks should seize the opportunity to innovate in both strategy and products to control the industry-related risks while enhancing their profitability (Nisar et al., 2018).

During the past decade, an increasing number of non-financial entities, including Internet companies, started providing finance-related services. With the propagation of liberalization policies, financial services providers and their products’ nature face increasing diversification. The channels of capital circulation shall also become more accessible, leading to stronger financial industry competition. According to Senchun and Weiwei (2016), as market integration is continuously pushed forward, innovation will undeniably continue to emerge. In these circumstances, Chinese commercial banks shall migrate from the traditional forms of intermediation to securities, insurance, leasing, trust, etc., that yield additional income. Likewise, emphasis shall be put on providing customers with one-stop cross-border platforms that provide numerous services. In the coming years, product design and innovation will become a key element in measuring financial institutions’ operating capabilities. In this sense, a major step was the enactment in May 2019 of a joint “Notice Regulating Financial Institutions interbank business.” The former was proposed to support financial institutions to accelerate the development of asset securitization business practices.

Similarly, the banking industry could actively restructure demand deposits, including current accounts and money market deposit accounts (MMDA/MMA). Commercial banks can also establish new time deposit schemes, including large transferable fixed deposit certificates (CDs) and money market deposit certificates (MMCD). Commercial banks could also consider shifting to low-cost and low-risk banking services and improve cost management capabilities while reducing their costs to maximize profits. Commercial banks should revamp their strategies, enhance customer management, and expand their operating platforms. Considering the empirical results exposed throughout section 4, the set of adjustments suggested formerly would address some of the Chinese commercial banks’ challenges regarding their asset size, quality, and client base development.

With the diversification observed in China’s banking industry, the risks faced by its actors increase gradually. As a result, one suggestion would be to set in place a proficient risk management strategy. Following the principle of matching risks and benefits, commercial banks’ premise to reasonably price products aftermarket interest rates are to quantify risks reasonably. Commercial banks should increase their investments in developing risk measurement technologies while adopting more efficient mechanisms to scrutinize the risks accurately and directly. As risk management strategies in the banking sector broadly imply mitigating banks’ exposure to losses while enhancing their asset value, Chinese commercial banks should effectively analyze possible risks associated with their specific business prospects. It would result in more effective customer loan funding while allowing, for instance, to reduce the borrowers’ default risk. A risk management strategy will be prioritized following a critical assessment to deal efficiently with the opportunity/threat. Simultaneously, Chinese commercial banks shall set efficient control mechanisms to effectively implement risk response strategies. Effective internal control mechanisms in commercial banks appear to be an aspect that significantly reduces the occurrence of non-systematic risks.

Conclusion

This study investigates the determinants of profitability for 10 Chinese commercial banks. For the sample period 1999 to 2019, we analyze the data of Chinese joint-stock commercial banks and city commercial banks. The empirical results show that interest rate liberalization actively promotes innovation and diversification among Chinese banks. It also leads to strategic adjustments in profitability mechanisms as Chinese commercial banks are strongly dependent on their assets size, quality, and risk management capabilities. Our investigation demonstrates that their intermediation margins strongly determine city commercial banks’ performance as it constitutes an important income source. In comparison, Joint-stock commercial banks prioritize diversification and innovation. They combine a diligent customer funding strategy with product diversification, leading to reduced exposure to interest rate spreads and customer default risk. For these institutions, it is essential to manage risks non-systematic risks efficiently. We hence suggest the prompt adoption of an innovative risk management system to develop the banks’ efficiency due to the market mutations.

Footnotes

Acknowledgements

We greatly appreciate the comments and suggestions given by the anonymous referees. The opinions expressed in this paper are those of the authors and do not necessarily represent those of the PBC. All errors remain our responsibility.

Author Contributions

Conceptualization: Li Qi and P. A. Louembé; writing—original draft preparation: Li Qi and P. A. Louembé; writing—review and editing: D. N. Rathnayake, P. A. Louembé, and Y. Bai; supervision: D. N. Rathnayake.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.